Abstract

We analyze the optimal harvesting problem for an ecosystem of species that experience environmental stochasticity. Our work generalizes the current literature significantly by taking into account non-linear interactions between species, state-dependent prices, and species seeding. The key generalization is making it possible to not only harvest, but also ‘seed’ individuals into the ecosystem. This is motivated by how fisheries and certain endangered species are controlled. The harvesting problem becomes finding the optimal harvesting-seeding strategy that maximizes the expected total income from the harvest minus the lost income from the species seeding. Our analysis shows that new phenomena emerge due to the possibility of species seeding. It is well-known that multidimensional harvesting problems are very hard to tackle. We are able to make progress, by characterizing the value function as a viscosity solution of the associated Hamilton–Jacobi–Bellman equations. Moreover, we provide a verification theorem, which tells us that if a function has certain properties, then it will be the value function. This allows us to show heuristically, as was shown by Lungu and Øksendal (Bernoulli 7(3):527–539, 2001), that it is almost surely never optimal to harvest or seed from more than one population at a time. It is usually impossible to find closed-form solutions for the optimal harvesting-seeding strategy. In order to by-pass this obstacle we approximate the continuous-time systems by Markov chains. We show that the optimal harvesting-seeding strategies of the Markov chain approximations converge to the correct optimal harvesting strategy. This is used to provide numerical approximations to the optimal harvesting-seeding strategies and is a first step towards a full understanding of the intricacies of how one should harvest and seed interacting species. In particular, we look at three examples: one species modeled by a Verhulst–Pearl diffusion, two competing species and a two-species predator–prey system.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Real populations never evolve in isolation. As a result, a key question in ecology is finding conditions that allow multiple species to coexist. There is a general theory for deterministic coexistence (Hofbauer 1981; Hutson 1984; Hofbauer and So 1989; Hofbauer and Sigmund 1998; Smith and Thieme 2011). However, due to the intrinsic randomness of environmental fluctuations, deterministic models should be seen only as first order approximations of the real world. In order to get a better understanding of population dynamics we have to take into account environmental stochasticity. Recently there has been significant progress towards a general theory of stochastic coexistence (Schreiber et al. 2011; Benaim 2018; Benaïm and Schreiber 2018; Hening and Nguyen 2018).

Many species of animals live in restricted habitats and are at risk of being overharvested. Harvesting, hunting and other forms of overexploitation have already driven species to extinction. On the other hand, underharvesting can lead to the loss of valuable resources. One has to carefully balance both conservation and economic considerations in order to find the optimal harvesting strategies. It can take a population a significant amount of time to recover from large harvests. This, in combination with the random environmental fluctuations, can make it impossible for the population to survive and can lead to extinctions (Lande et al. 1995, 2003).

In certain cases, added conservation efforts have to be made in order to save a species from extinction. Therefore, it makes sense to be able to repopulate a species by seeding animals into the habitat. There is no reason to assume that the price of the harvesting or seeding is constant. If the harvested population is smaller the cost of harvesting is usually higher due to the fact that it is harder to find the individuals one wants to harvest. Similarly, the marginal cost of seeding will be lower, if one has a large population. We present a model that incorporates all these factors and effects. We consider \(d\ge 0\) species interacting nonlinearly in a stochastic environment where the species can be harvested as well as seeded into the system and the price of harvesting and seeding is density-dependent. The problem becomes finding the optimal harvesting-seeding strategy that maximizes the expected total income from the harvest minus the lost income from the species seedings. Mathematically, the problem we consider belongs to a class of singular stochastic control problems. Singular stochastic control problems have been studied extensively in various settings. To mention just a few, we refer to works of Alvarez and Shepp (1998), Alvarez (2000), Lungu and Øksendal (1997), Song et al. (2011), Hening et al. (2019), Alvarez and Hening (2018) for single species ecosystems in random environments and of Lungu and Øksendal (2001), Tran and Yin (2015), Tran and Yin (2017) for interacting populations. The reader can also find analogous results in the setting of corporate strategy (Radner and Shepp 1996), and optimal dividend strategies (Asmussen and Taksar 1997; Jin et al. 2013; Scheer and Schmidli 2011). Numerical methods for optimal harvesting have been developed by Jin et al. (2013), Tran and Yin (2016) and capital injections have been introduced by Dickson and Waters (2004), Kulenko and Schmidli (2008), Scheer and Schmidli (2011).

Considering optimal dividend problems in insurance and risk management (Dickson and Waters 2004; Jin et al. 2013; Kulenko and Schmidli 2008; Scheer and Schmidli 2011), it was observed that higher profit can be obtained if investors are allowed not only to remove but also to inject capital. In the harvesting setting, the idea of repopulating species (which we will call seeding) is natural and has been done for conservation efforts as well as for fisheries and agriculture. We propose a general model in which the control consists of two components: harvesting and seeding. In contrast to the existing literature, in our framework, to maximize the expected total discounted reward, the controller can add individuals of various species to maintain the system at a certain level and to avoid extinction. Moreover, we work with a system of interacting species. There are few theoretical results regarding the multi-species harvesting problem (Lungu and Øksendal 2001; Tran and Yin 2017). In a model with several species, one needs to decide which species to harvest at a given time. In addition, our model is complicated because we also allow seeding. At a given time, there are several possibilities. One can do nothing and let the population dynamics run on its own, or one can have any possible combination of seeding and harvesting of the d species.

To find the optimal harvesting-seeding strategy (also called the optimal control) and its associated total discounted reward (also called the value function), the usual approach is to solve the associated the Hamilton–Jacobi–Bellman (HJB) partial differential equations. However, for the singular control problems we consider, the HJB equations become a system of nonlinear quasi-variational inequalities. We use the viscosity solution approach for partial differential equations to study the value functions and associated control problems. It is usually impossible to find closed-form solutions to the HJB system. In order to side-step this difficulty and still gain valuable information, we develop numerical algorithms to approximate the value function and the optimal harvesting-seeding strategy. We do this by using the Markov chain approximation methodology developed by Kushner and Martins (1991).

The main contributions of our work are the following:

-

(1)

We formulate the harvesting-seeding problem for a system of interacting species living in a stochastic environment.

-

(2)

We establish the finiteness and the continuity of the value function and characterize the value function as a viscosity solution of an associated HJB system of quasi-variational inequalities.

-

(3)

We develop numerical approximation schemes based on the Markov chain approximation method.

-

(4)

We discover new phenomena by analyzing natural examples for one and two-species systems.

The rest of our work is organized as follows. In Sect. 2 we describe our model and the main results. Particular examples are explored using the newly developed numerical schemes in Sect. 3. Finally, all the technical proofs appear in the appendices.

2 Model and results

Assume we have a probability space \((\Omega , {\mathcal {F}}, {{\mathbb {P}}})\) satisfying the usual conditions. We consider d species interacting nonlinearly in a stochastic environment. We model the dynamics as follows. Let \(\xi _i(t)\) be the abundance of the ith species at time \(t\ge 0\), and denote by \(\xi (t)=(\xi _1(t), \dots , \xi _d(t))'\in \mathbb {R}^d\) (where \(z'\) denotes the transpose of z) the column vector recording all the species abundances.

One way of adding environmental stochasticity to a deterministic system is based on the assumption that the environment mainly affects the growth/death rates of the populations. This way, the growth/death rates in an ODE (ordinary differential equation) model are replaced by their average values to which one adds a white noise fluctuation term (Turelli 1977; Braumann 2002; Gard 1988; Evans et al. 2013; Schreiber et al. 2011; Gard 1984).

Under this assumption the dynamics becomes

where \(w(\cdot )=(w_1(\cdot ), ..., w_d (\cdot ))'\) is a d-dimensional standard Brownian motion and \(b,\sigma :[0,\infty )^d\rightarrow [0,\infty )^d\) are smooth enough functions. Let \(S=(0, \infty )^d\) and \({{\bar{S}}}=[0, \infty )^d\). We assume that \(b(0)=\sigma (0)=0\) so that 0 is an equilibrium point of (2.1). This makes sense because if our populations go extinct, they should not be able to get resurrected without external intervention (like a repopulation/seeding event). If \(\xi _i(t_0)=0\) for some \(t_0\ge 0\), then \(\xi _i(t)=0\) for any \(t\ge t_0\). Thus, \(\xi (t)\in {{\bar{S}}}\) for any \(t\ge 0\).

For \(x, y\in \mathbb {R}^d\), with \(x=(x_1, \dots , x_d)'\) and \(y=(y_1, \dots , y_d)'\), we write \(x\le y\) or \(y\ge x\) if \(x_j\le y_j\) for each \(j=1, \dots , d\), while \(x < y\) if \(x_j < y_j\) for each \(j=1, \dots , d\).. We also define the scalar product \(x\cdot y=\sum _{j=1}^d x_j y_j\). For a real number a, we denote \(a^+=\max \{a, 0\}\) and \(a^-=\max \{-a, 0\}\). Thus, \(a=a^+-a^-\) and \(|a|=a^++a^-\). For \(x=(x_1, \dots , x_d)'\in \mathbb {R}^d\), \(x^+=\big ( x_1^+, \dots , x_d^+\big )'\) and \(x^-=\big ( x_1^-, \dots , x_d^-\big )'\). Let \(\mathbf{e_i}\in \mathbb {R}^d\) denote the unit vector in the ith direction for \(i=1, \dots , d\).

To proceed, we introduce the generator of the process \(\xi (t)\). For a twice continuously differentiable function \(\Phi (\cdot ): \mathbb {R}^d\mapsto \mathbb {R}\), we define

where \(\nabla \Phi (\cdot )\) and \(\nabla ^2 \Phi (\cdot )\) denote the gradient and Hessian matrix of \(\Phi (\cdot )\), respectively.

Next, we have to add harvesting and seeding to (2.1). Let \(Y_i(t)\) denote the amount of species i that has been harvested up to time t and set \(Y(t)=(Y_1(t), \dots , Y_d(t))'\in \mathbb {R}^d\). Let \(Z_i(t)\) denote the amount of species i seeded into the system up to time t and set \(Z(t)=(Z_1(t), \dots , Z_d(t))'\in \mathbb {R}^d\). The dynamics of the d species that takes into account harvesting and seeding is given by

where \(X(t)=(X_1(t), \dots , X_d(t))'\in \mathbb {R}^d\) are the species abundances at time \(t\ge 0\). We also assume the initial species abundances are

Notation For each time t, \(X(t-)\) represents the state before harvesting starts at time t, while X(t) is the state immediately after. Hence X(0) may not be equal to \(X(0-)\) due to an instantaneous harvest Y(0) or an instantaneous seeding Z(0) at time 0. Throughout the paper we use the convention that \(Y(0-)=Z(0-)=0\). The jump sizes of Y(t) and Z(t) are denoted by \(\Delta Y(t):=Y(t) - Y(t-)\) and \(\Delta Z(t):=Z(t) - Z(t-)\), respectively. We use \(Y^c(t):= Y(t) - \sum \nolimits _{0\le s\le t} \Delta Y(s)\) and \(Z^c(t):= Z(t) - \sum \nolimits _{0\le s\le t} \Delta Z(s)\) to denote the continuous part of Y and Z. Also note that \(\Delta X(t):= X(t) - X(t-)= \Delta Z(t)-\Delta Y(t)\) for any \(t \ge 0\).

Let \(f_i: {{\bar{S}}}\mapsto (0, \infty )\) represent the instantaneous marginal yields accrued from exerting the harvesting strategy \(Y_i\) for the species i, also known as the price of species i. Let \(g_i: {{\bar{S}}}\mapsto (0, \infty )\) represent the total cost we need to pay for the seeding strategy \(Z_i\) on species i. We will set \(f=(f_1, \dots , f_d)'\) and \(g=(g_1, \dots , g_d)'\). For a harvesting-seeding strategy (Y, Z) we define the performance function as

where \(\delta > 0\) is the discounting factor, \({{\mathbb {E}}}_{x}\) denotes the expectation with respect to the probability law when the initial abundances are \(X(0-)=x\), and \(f(X(s-))\cdot dY(s):=\sum _{i=1}^d f_i(X(s-)) dY_i(s)\).

Control strategy Let \({\mathcal {A}}_{x}\) denote the collection of all admissible controls with initial condition x. A harvesting-seeding strategy (Y, Z) will be in \({\mathcal {A}}_x\) if it satisfies the following conditions:

- (a):

-

the processes Y(t) and Z(t) are right continuous, nonnegative, and nondecreasing with respect to t; moreover, \(\Delta Y_i(t) \Delta Z_i(t)=0\) for \(i=1, \dots , d\) and \(t\ge 0\),

- (b):

-

the processes Y(t) and Z(t) are adapted to \(\sigma \{w(s): 0\le s\le t\}\), augmented by the \({{\mathbb {P}}}\)-null sets,

- (c):

-

The system (2.2) has a unique solution \(X(\cdot )\) with \(X(t)\ge 0\) for any \(t\ge 0\),

- (d):

-

\(0< J(x, Y, Z)<\infty \) for any \(x\in S\), where \(J(\cdot )\) is the functional defined in (2.4).

Remark 2.1

The condition \(\Delta Y_i(t) \Delta Z_i(t)=0\), for any \(i=1, \dots , d\) and any \(t\ge 0\) means that we do not allow the simultaneous harvesting and seeding of the same species. Note that this would never yield an optimal harvesting-seeding strategy because of the assumption \(f_i < g_i\).

The optimal harvesting-seeding problem The problem we will be interested in is to maximize the performance function and find an optimal harvesting strategy \((Y^*, Z^*)\in {\mathcal {A}}_{x}\) such that

The function \(V(\cdot )\) is called the value function.

Remark 2.2

We note that the optimal harvesting strategy might not exist, i.e. the maximum over \({\mathcal {A}}_x\) might not be achieved in \({\mathcal {A}}_x\).

Assumption 2.3

We will make the following standing assumptions throughout the paper.

- (a):

-

The functions \(b(\cdot )\) and \(\sigma (\cdot )\) are continuous. Moreover, for any initial condition \(x\in {{\bar{S}}}\), the uncontrolled system (2.1) has a unique global solution.

- (b):

-

For any \(i=1, \dots , d\), \(x, y\in \mathbb {R}^d\), \({f_i(x)}< g_i(y) \); \(f_i(\cdot )\), \(g_i(\cdot )\) are continuous and non-increasing functions.

Remark 2.4

Note that Assumption 2.3 (a) does not put significant restraints on the dynamics of the species. Our framework therefore contains a very broad class of models. In particular, this covers all Lotka-Volterra competition and predator–prey models as well as the more general Kolmogorov systems (Du et al. 2016; Li and Mao 2009; Mao and Yuan 2006; Hening and Nguyen 2018). The continuity and monotonicity of the functions \(f(\cdot ), g(\cdot )\) from Assumption 2.3(b) are standard (Alvarez 2000; Song et al. 2011; Tran and Yin 2017). In particular, \(g_i\) is non-increasing because one can see this as an economy of scale which implies that the per unit cost of restocking decreases as more is restocked The additional requirement that \({f_i(x)}< g_i(y) \) for any \(x, y\in {{\bar{S}}}\) can be explained as follows: the cost of seeding an amount of a species is always higher than the benefit received from harvesting the same amount. This makes sense because in order to seed the species, one has to have access to a pool of individuals of this species. For this, one either has to keep individuals at a specific location (thus using resources to sustain them) or one has to transport/buy individuals. In the setting of optimal dividend payments, these extra costs reflect penalizing factors (Kulenko and Schmidli 2008) and transaction costs (Jin et al. 2013; Scheer and Schmidli 2011).

We collect some of the results we are able to prove about the value function.

Proposition 2.5

Let Assumption 2.3 be satisfied. Then the following assertions hold.

- (a):

-

For any \(x, y\in {{\bar{S}}}\),

$$\begin{aligned} V(y)\le V(x) - f(x)\cdot (x-y)^++g(x)\cdot (x-y)^-. \end{aligned}$$(2.6) - (b):

-

If \(V(0)<\infty \), then \(V(x)<\infty \) for any \(x\in {{\bar{S}}}\) and V is Lipschitz continuous.

Example 2.6

In the current setting, contrary to the regular harvesting setting without seeding, V(0) can be nonzero because of the benefits from seedings. Consider the single species system given by

where a, b, and \(\sigma \) are constants and the price function is \(f(x)=1, x\ge 0\). It has been shown in Alvarez and Shepp (1998) that, if there is no seeding, the value function is given by

where \(x^*\in (0, \infty )\) and \(\psi : [0, \infty )\rightarrow [0, \infty )\) is twice continuously differentiable, and \(\psi (x)>x\) for all \(x\in (0, x^*]\). Let \(g(x)=\kappa \in {\mathbb {R}}\), where \(1<\kappa <\psi (x^*)/x^*\). Let \((Y, Z)\in {\mathcal {A}}_0\) be such that \(J(0, Y, 0)=V_0(x)\) and \(Z(t)=Z(0)=x^*\) for all \(t\ge 0\). Then

Since \(V(0)>0\), the system does not get depleted in a finite time under an optimal harvesting strategy.

Proposition 2.7

Let Assumption 2.3 be satisfied. Moreover, suppose that there is a positive constant C such that

Then there exist a positive constant M such that

Remark 2.8

We note that the condition on the drift \(b(\cdot )\) is very natural. Consider the one-dimensional dynamics given by

with \(f(x)=1, x\ge 0\) and any function \(g(\cdot )\). It is clear that if \(b>\delta \), the value function in the harvesting problem with no seeding is

As a result the value function for (2.9) will be \(V(x)=\infty , x>0.\)

Seeding can also change the finiteness of the value function. Indeed, consider the harvesting problem

with \(f(x)=1, g(x)=2, x\ge 0\). Suppose that \(g(x)=\sigma (x)=0\) for \(x<1\) and \(b(x)=(1+\delta ) x( 1-x)\) and \(\sigma (x)=0\) for \(x>1\). Then it is clear that without seeding we get the value function \(V_0(x)=\infty \) for \(x>1\) and \(V_0(x)=x\) for \(x\le 1\). When seeding is allowed, we have \(V(x)=\infty \) for all \(x\ge 0\).

We get the following characterization of the value function.

Theorem 2.9

Let Assumption 2.3 be satisfied and suppose \(V(x)<\infty \) for \(x\in {S}\). The value function \(V(\cdot )\) is a viscosity solution to the HJB equation

Remark 2.10

Theorem 2.9 is a theorem that tells us how to find the value function. The problem is that the solutions of (2.11) are not always smooth enough for \({\mathcal {L}}V\) to make sense. This is why we work with viscosity solutions of (2.11).

We next explain what a viscosity solution means. For any \(x^0\in S\) and any function \(\phi \in C^2(S)\) such that \(V(x_0)=\phi (x_0)\) and \(V(x)\ge \phi (x)\) for all x in a neighborhood of \(x^0\), we have

Similarly, for any \(x^0\in S\) and any function \(\varphi \in C^2(S)\) satisfying \(V(x_0)=\phi (x_0)\) and \(V(x)\le \phi (x)\) for all x in a neighborhood of \(x^0\), we have

This extends the results by Haussmann and Suo (1995a, b), Lungu and Øksendal (2001) where the authors had to assume that the coefficients \(b, \sigma \) are bounded or the prices \(f_i\) are not density-dependent. Usually the functions \(b,\sigma \) are not bounded and the prices depend on the abundances of the species. Moreover, we consider both harvesting and seeding. Therefore, our results provide a significant generalization of those previously shown by Haussmann and Suo (1995a), Lungu and Øksendal (2001).

We also get the following verification theorem, that tells us that if a function satisfies certain properties, then it will be the value function. We note that this is natural analogue with seeding of Theorem 2.1 of Lungu and Øksendal (2001), Alvarez et al. (2016).

Theorem 2.11

Let Assumption 2.3 be satisfied. Suppose that there exists a function \(\Phi : {{\bar{S}}}\mapsto [0, \infty )\) such that \(\Phi \in C^2({{\bar{S}}})\) and that \(\Phi (\cdot )\) solves the following coupled system of quasi-variational inequalities

where \(({\mathcal {L}}-\delta )\Phi (x)={\mathcal {L}}\Phi (x)-\delta \Phi (x)\). Then the following assertions hold.

- (a):

-

We have

$$\begin{aligned} V(x)\le \Phi (x)\quad \text {for any } x\in {S}. \end{aligned}$$(2.13) - (b):

-

Define the non-intervention region

$$\begin{aligned} {\mathcal {C}}= \left\{ x\in S: f_i(x)<\dfrac{\partial \Phi }{\partial x_i}(x)<g_i(x) \right\} . \end{aligned}$$Suppose that

$$\begin{aligned} ({\mathcal {L}}-r)\Phi (x)=0, \end{aligned}$$(2.14)for all \(x\in {\mathcal {C}}\), and that there exists a harvesting-seeding strategy \(\big (\widetilde{Y}, \widetilde{Z}\big ) \in {\mathcal {A}}_{x}\) and a corresponding process \(\widetilde{X}\) such that the following statements hold.

- (i):

-

\(\widetilde{X}(t)\in \overline{{\mathcal {C}}}\) for Lebesgue almost all \(t\ge 0.\)

- (ii):

-

\(\int \nolimits _0^{t} \left[ \nabla \Phi (\widetilde{X}(s))- f(\widetilde{X}(s))\right] \cdot d\widetilde{Y}^c(s)=0\) for any \(t\ge 0\).

- (iii):

-

\(\int \nolimits _0^{t} \Big [g(\widetilde{X}(s))-\nabla \Phi (\widetilde{X}(s)) \Big ] \cdot d\widetilde{Z}^c(s)=0\) for any \(t\ge 0\).

- (iv):

-

If \(\widetilde{X}(s)\ne \widetilde{X}(s-)\), then

$$\begin{aligned} \Phi (\widetilde{X}(s))-\Phi (\widetilde{X}(s-))=- f(\widetilde{X}(s-)) \cdot \Delta \widetilde{Z}(s). \end{aligned}$$ - (v):

-

\(\lim \limits _{N\rightarrow \infty }E_{x}\Big [e^{-rT_N}\Phi (\widetilde{X}(T_N))\Big ]=0\), where for each \(N=1, 2, \dots \),

$$\begin{aligned} \beta _N:=\inf \{t\ge 0: |X(t)|\ge N\},\quad T_N: = N \wedge \beta _N.\end{aligned}$$(2.15)

Then \(V(x)=\Phi (x)\) for all \(x\in S\), and \(\big (\widetilde{Y},\widetilde{Z}\big )\) is an optimal harvesting-seeding strategy.

Remark 2.12

Following (Lungu and Øksendal 2001) we note that if we can find a function satisfying (2.12), (2.13) and (2.14), then one can construct a strategy satisfying assumptions (i), (ii), (iii) and (iv) from Theorem 2.11 part b) by solving the Skorokhod stochastic differential equation for the reflection of the process X(t) in the domain \({\mathcal {C}}\). We refer the reader to check further literature (Lungu and Øksendal 2001; Bass 1998; Freidlin 2016; Lions and Sznitman 1984) for more details about Skorokhod stochastic differential equations.

We can extend Principle 2.1 of Lungu and Øksendal (2001) as follows.

Principle 2.13

(One-at-a-time principle) Suppose the diffusion matrix \(\sigma (x)\sigma '(x)\) is nondegenerate for all \(x\in S\). Then it is almost always optimal to harvest or to seed from at most one species at a time.

Proof

We follow (Lungu and Øksendal 2001). Assume for simplicity \(d=2\) so that we have two species. The non-intervention region \({\mathcal {C}}\) is bounded by the four curves curves \(\Lambda ^f_1, \Lambda ^f_2, \Lambda ^g_1, \Lambda ^g_2\) given by

and

Note that we would have simultaneous harvesting and seeding of species i only when the process is at \(\Lambda ^f_i \cap \Lambda ^g_i \), simultaneous harvesting of the two species only when the process is at \(\Lambda ^f_1 \cap \Lambda ^f_2 \), simultaneous harvesting of species 1 and seeding of species 2 only when the process is at \(\Lambda ^f_1 \cap \Lambda ^g_2\), etc. Now, if the diffusion is non-degenerate, the probability it hits a set of the form \(\Lambda ^f_i \cup \Lambda ^f_j\) for \(i\ne j\) or \(\Lambda ^f_i \cup \Lambda ^g_j \) is equal to zero. This argument can be extended to n dimensions—see Principle 2.1 of Lungu and Øksendal (2001). \(\square \)

2.1 Numerical scheme

A closed-form solution to the HJB equation from Theorem 2.9 is virtually impossible to obtain. Moreover, the initial value of V(0) is not specified. In order to by-pass these difficulties and to gain information about the value function and the optimal harvesting-seeding strategy we provide a numerical approach. Using the Markov chain approximation method (Budhiraja and Ross 2007; Jin et al. 2013; Kushner and Martins 1991; Kushner and Dupuis 1992), we construct a controlled Markov chain in discrete time to approximate the controlled diffusions. For the convergence analysis, we also suppose that both \(f(\cdot )\) and \(g(\cdot )\) are constant functions. Let \(h>0\) be a discretization parameter. Since the real population abundances cannot be infinite, we choose a large number \(U>0\) and define the class \({\mathcal {A}}^U_{x}\subset {\mathcal {A}}_{x}\) that consists of strategies \((Y,Z)\in {\mathcal {A}}_x\) such that the resulting process X stays in \([0,U]^d\) for all times. The class \({\mathcal {A}}^U_{x}\) can be constructed by using Skorokhod stochastic differential equations (Bass 1998; Freidlin 2016; Lions and Sznitman 1984) in order to make sure that the process stays in \([0,U]^d\) for all \(t>0\).

Let \(({\tilde{Y}}^U, {\tilde{Z}}^U)\in {\mathcal {A}}^U_{x}\) and \(V^U(x)\) be defined as the optimal harvesting-seeding strategy and the value function when we restrict the problem to the class \({\mathcal {A}}^U_{x}\subset {\mathcal {A}}_{x}\)

Remark 2.14

We conjecture that, generically, the optimal strategy will live in \({\mathcal {A}}_x^U\) for U large enough, i.e. there exists \(U>0\) such that for all \(x\in [0,U]^d\) we have

The verification Theorem 2.11 provides a heuristic argument for this conjecture.

Assume without loss of generality that U is an integer multiple of h. Define

Let \(\{X^h_n: n=0, 1, \dots \}\) be a discrete-time controlled Markov chain with state space \(S_{h}\). We define the difference

At any discrete-time step n, one can either harvest, seed, or do nothing. We use \(\pi ^h_n\) to denote the action at step n, where \(\pi ^h_n=-i\) if there is seeding of species i, \(\pi ^h_n=0\) if there is no seeding or harvesting of species i, and \(\pi ^h_n=i\) if there is harvesting. Denote by \(\Delta Y^h_n\) and \(\Delta Z^h_n\) the harvesting amount and the seeding amount for the chain at step n, respectively. If \(\pi ^h_n=0\), then the increment \(\Delta X_n^h\) is to behave like an increment of \(\int b dt +\int \sigma dw\) over a small time interval. Such a step is also called “diffusion step”. If \(\pi ^h_n=-i\), then \(\Delta Y^h_n=0\in \mathbb {R}^d\) and \(\Delta Z^h_n=h\mathbf{e_i}\). If \(\pi ^h_n=i\), then \(\Delta Y^h_n=h\mathbf{e_i}\) and \(\Delta Z^h_n=0\in \mathbb {R}^d\). Note that \(\Delta X^h_n=-\Delta Y^h_n + \Delta Z^h_n\). Moreover, we can write

For definiteness, if \(X^{h}_{n, i}\) is the ith component of the vector \(X^h_n\) and \(\{j: X^{h}_{n, j}=U\}\) is non-empty, then step n is a harvesting step on species \(\min \{j: X_{n, j}^{h}=U\}\). Let \(\pi ^h = (\pi _0^h, \pi _1^h, \dots )\) denote the sequence of control actions. We denote by \(p^h(x, y)|\pi )\) the transition probability from state x to another state y under the control \(\pi \). Denote \({\mathcal {F}}^h_n=\sigma \{X^h_m, \pi ^h_m, m\le n\}\).

The sequence \(\pi ^h\) is said to be admissible if it satisfies the following conditions:

- (a):

-

\(\pi ^h_n\) is \(\sigma \{X^h_0, \dots , X^h_{n}, \pi ^h_0, ..., \pi ^h_{n-1}\}\text {---adapted},\)

- (b):

-

For any \(x\in S_h\), we have

$$\begin{aligned} {{\mathbb {P}}}\{ X^h_{n+1} =x | {\mathcal {F}}^h_n\}= {{\mathbb {P}}}\{X^h_{n+1}= x | X^h_n, \pi ^h_n\} = p^h( X^h_n, x| \pi ^h_n), \end{aligned}$$ - (c):

-

Denote by \(X^{h}_{n, i}\) the ith component of the vector \(X^h_n\). Then

$$\begin{aligned} {{\mathbb {P}}}\big ( \pi ^h_{n}=\min \{j: X^{h}_{n, j} = U\} | X^{h}_{n, j} = U \text { for some } j\in \{1, \dots , d \}, {\mathcal {F}}^h_n\big )=1.\nonumber \\ \end{aligned}$$(2.18) - (d):

-

\(X^h_n\in S_h\) for all \(n=0, 1, 2, \dots \).

The class of all admissible control sequences \(\pi ^h\) for initial state x will be denoted by \({\mathcal {A}}^h_{x}\).

For each couple \((x, i)\in S_h\times \{0, \pm 1, \dots , \pm d\}\), we define a family of the interpolation intervals \(\Delta t^h (x, i)\). The values of \(\Delta t^h (x, i)\) will be specified later. Then we define

For \(x\in S_h\) and \(\pi ^h\in {\mathcal {A}}^h_{x}\), the performance function for the controlled Markov chain is defined as

The value function of the controlled Markov chain is

Theorem 2.15

Suppose Assumptions 2.3 and B.1 hold. Then \(V^h(x)\rightarrow V^U(x)\) as \(h\rightarrow 0\). Thus, for sufficiently small h, a near-optimal harvesting-seeding strategy of the controlled Markov chain is also a near-optimal harvesting-seeding policy of the original continuous-time problem.

3 Numerical examples

3.1 Single species system

We consider a single species ecosystem. The dynamics that includes harvesting and seeding will be given by

For an admissible strategy (Y, Z) we have

Based on the algorithm constructed above and in Appendix B, we carry out the computation by value iterations. Let \((Y_0,Z_0)\) be the policy that drives the system to extinction immediately and has no seeding. Then \(J(x, Y_0, Z_0)=f(x)x\) for all x. Recall (Alvarez and Shepp 1998) that \(J(x, Y_0, Z_0)\) is also referred to as current harvesting potential. Letting \((Y_0, Z_0)\) be the initial strategy, we set the initial values

We outline how to find the values of \(V(\cdot )\) as follows. At each level \(x=h,2h, \dots , U\), denote by \(\pi (x, n)\) the action one chooses, where \(\pi (x, n)=1\) if there is harvesting, \(\pi (x, n)=-1\) if there is seeding, and \(\pi (x, n)=0\) if there is no harvesting or seeding. We initially let \(\pi (x, 0)=1\) for all x and we try to find better harvesting-seeding strategies. We find an improved value \(V^h_{n+1}(x)\) and record the corresponding optimal action by

where

The iterations stop as soon as the increment \(V^h_{n+1}(\cdot )-V^h_n(\cdot )\) reaches some tolerance level. We set the error tolerance to be \(10^{-8}\).

The numerical experiments provide evidence that the following conjecture holds

Conjecture 3.1

Suppose we have one species that evolves according to (3.1) and suppose Assumption 2.3 holds. One can construct the optimal harvesting-seeding strategy \((Y^*,Z^*)\) as follows. There exist lower and upper thresholds \(0\le u^*< v^*<\infty \) such that after \(t\ge 0\) the abundance of the species always stays in the interval \([u^*,v^*]\). More explicitly if \(X(0-)=x\) then

where \(L(t,u^*)\) (respectively \(L(t,v^*)\)) is the local time push of the process X at the boundary \(u^*\) (respectively \(v^*\)).

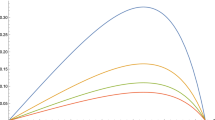

Value function and optimal policies: \(f(x)=1, g(x)=3\) for \(x\ge 0.\)

For the first numerical experiment we take \(b=3, c=2, \sigma =1\) in (3.1). Let \(\delta =0.05\), and \(f(x)=1,g(x)=3\) for all \(x\ge 0\). Figure 1 shows the value function V(x) as a function of the initial population x and provides optimal policies, with 1 denoting harvesting, \(-1\) denoting seeding, and 0 denoting no harvesting or seeding. It can be seen from Fig. 1 that the optimal policy is a barrier strategy. There are levels \(L_1\) and \(L_2\) such that \([0, L_1)\) is the seeding region, \([L_1, L_2)\) is the diffusion region where there is no control of the population, and \([L_2, U]\) is the harvesting region. Because of the benefit from seeding, \(V(0)>0\). These observations agree with those in the analogous financial setting (Jin et al. 2013; Scheer and Schmidli 2011).

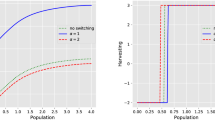

Next, suppose that g takes very large values. In particular, we take \(g(x)=50, x\ge 0\). In this case, one can observe that there is no seeding; see Fig. 2. In other words, because the cost of seeding is very high, the optimal strategy does not benefit from seeding.

To explore how noise impacts the problem, we explore what happens when \(\sigma =1000\) and keep the other coefficients the same. The results are shown on Fig. 3. It turns out, as expected, that if the noise is very large, the value function is close to the current harvesting potential \(J(\cdot , Y_0, Z_0)\) and no seeding is needed. This is because the large noise will drive the species extinct with probability 1 and, therefore, the optimal strategy is to immediately harvest all individuals. We refer the reader to the works by Alvarez and Shepp (1998), Tran and Yin (2016), Hening et al. (2019), Alvarez and Hening (2018) for more insight regarding how noise impacts harvesting.

Value function and optimal policies: \(f(x)=1, g(x)=50\) for \(x\ge 0\)

Value function and optimal policies: \(f(x)=1, g(x)=3, \sigma (x)=1000\) for \(x\ge 0.\)

Value function versus initial population for a two-species competitive model

3.2 Two-species ecosystems

Example 3.2

Consider two species competing according to the following stochastic Lotka-Volterra system

and suppose that \(\delta =0.05\), \(f_1(x)=1\), \(f_2(x)=2\), \(g_1(x)=4, g_2(x)=4\) for all \(x\in [0, \infty )^2\). We take \(U = 5\). In addition, set

Figure 4 shows the value function V as a function of initial population sizes (x, y). Figure 5 provides the optimal harvesting-seeding policies, with “1” denoting harvesting of species 1, “\(-1\)” denoting seeding of species 1, “2” denoting harvesting of species 2, “\(-2\)” denoting seeding of species 2 and “0” denoting no harvesting or seeding. It can be seen from Fig. 5 that when population size of each species is larger than a certain level, it is optimal to harvest. However, for a very large region, harvesting of species 1 is the first choice. Moreover, one can observe that it is never optimal to seed species 1 (Fig. 6). As shown in Fig. 7, if we assume both species abundances are 0 initially, we should only seed species 2. This tells us that the benefits obtained from species 2 are larger than those from species 1 due to its higher price; i.e, \(f_2(x)=2>1=f_1(x)\).

Optimal harvesting-seeding strategy versus population size for a two-species competitive model

Optimal harvesting-seeding strategy versus population size for a two-species competitive model: the case \(y=0\) (the left picture) and \(x=0\) (the right picture)

Value function versus initial population for a two-species predator–prey model

Optimal harvesting-seeding strategy versus population size for a two-species predator–prey model

Example 3.3

Consider a predator–prey system modelled by the stochastic Lotka–Volterra system

Conditions for the coexistence and extinction of the different species can be found in Hening and Nguyen (2018). Suppose that \(\delta =0.05\), \(f_1(x)=1\), \(f_2(x)=1\), \(g_1(x)=6, g_2(x)=6\) for all \(x\in [0, \infty )^2\). We take \(U = 5\). In addition, let

Optimal harvesting-seeding strategy versus population size for a two-species predator–prey model: the case \(y=0\) (the left picture) and \(x=0\) (the right picture)

Figure 7 shows the value function V as a function of initial population (x, y). Figure 8 provides the optimal harvesting-seeding strategies, with “1” denoting harvesting on species 1, “\(-1\)” denoting seeding on species 1, “2” denoting harvesting on species 2, “\(-2\)” denoting seeding on species 2 and “0” denoting no harvesting or seeding. We see in Fig. 9 that, as expected, since the predator goes extinct if there is no prey, the optimal strategy is to immediately harvest all the predators at time \(t=0\).

References

Alvarez LHR (2000) Singular stochastic control in the presence of a state-dependent yield structure. Stoch Process Appl 86:323–343

Alvarez LHR, Shepp LA (1998) Optimal harvesting of stochastically fluctuating populations. J Math Biol 37:155–177

Alvarez LH, Lungu E, Øksendal B (2016) Optimal multi-dimensional stochastic harvesting with density-dependent prices. Afrika Matematika 27(3–4):427–442

Alvarez ELH, Hening A (2018) Optimal sustainable harvesting of populations in random environments. arXiv preprint arXiv:1807.02464

Asmussen S, Taksar M (1997) Controlled diffusion models for optimal dividend payout. Insur: Math Econ 20(1):1–15

Bass RF (1998) Diffusions and elliptic operators. Springer, New York

Benaim M (2018) Stochastic persistence. arXiv preprint arXiv:1806.08450

Benaïm M, Schreiber SJ (2018) Persistence and extinction for stochastic ecological difference equations with feedbacks. arXiv preprint arXiv:1808.07888

Braumann CA (2002) Variable effort harvesting models in random environments: generalization to density-dependent noise intensities. Math Biosci 177/178:229–245. Deterministic and stochastic modeling of biointeraction (West Lafayette, IN, 2000)

Budhiraja A, Ross K (2007) Convergent numerical scheme for singular stochastic control with state constraints in a portfolio selection problem. SIAM J Control Optim 45(6):2169–2206

Dickson DCM, Waters HR (2004) Some optimal dividends problems. ASTIN Bull 34(1):49–74

Du NH, Nguyen NH, Yin G (2016) Conditions for permanence and ergodicity of certain stochastic predator–prey models. J Appl Probab 53(1):187–202

Evans SN, Ralph PL, Schreiber SJ, Sen A (2013) Stochastic population growth in spatially heterogeneous environments. J Math Biol 66(3):423–476

Freidlin MI (2016) Functional integration and partial differential equations, vol 109. Princeton University Press, Princeton

Gard TC (1984) Persistence in stochastic food web models. Bull Math Biol 46(3):357–370

Gard TC (1988) Introduction to stochastic differential equations. Marcel Dekker, New York

Haussmann UG, Suo W (1995a) Singular optimal stochastic controls I: existence. SIAM J Control Optim 33(3):916–936

Haussmann UG, Suo W (1995b) Singular optimal stochastic controls II: dynamic programming. SIAM J Control Optim 33(3):937–959

Hening A, Nguyen D (2018) Coexistence and extinction for stochastic Kolmogorov systems. Ann Appl Probab 28(3):1893–1942

Hening A, Nguyen DH, Ungureanu SC, Wong TK (2019) Asymptotic harvesting of populations in fluctuating environments. J Math Biol 78(1–2):293–329

Hofbauer J (1981) A general cooperation theorem for hypercycles. Monatshefte für Mathematik 91(3):233–240

Hofbauer J, So JW-H (1989) Uniform persistence and repellors for maps. Proc Am Math Soc 107(4):1137–1142

Hofbauer J, Sigmund K (1998) Evolutionary games and population dynamics. Cambridge University Press, Cambridge

Hutson V (1984) A theorem on average Liapunov functions. Monatshefte für Mathematik 98(4):267–275

Jin Z, Yang H, Yin G (2013) Numerical methods for optimal dividend payment and investment strategies of regime-switching jump diffusion models with capital injections. Automatica 49(8):2317–2329

Kulenko N, Schmidli H (2008) Optimal dividend strategies in a Cramer–Lundberg model with capital injections. Insur: Math Econ 43(2):270–278

Kushner HJ (1990) Numerical methods for stochastic control problems in continuous time. SIAM J Control Optim 28(5):999–1048

Kushner HJ, Martins LF (1991) Numerical methods for stochastic singular control problems. SIAM J Control Optim 29(6):1443–1475

Kushner HJ, Dupuis PG (1992) Numerical methods for stochastic control problems in continuous time. Springer-Verlag, New York

Lande R, Engen S, Sæther B-E (1995) Optimal harvesting of fluctuating populations with a risk of extinction. Am Nat 145(5):728–745

Lande R, Engen S, Ther BS (2003) Stochastic population dynamics in ecology and conservation. Oxford University Press, Oxford

Li X, Mao X (2009) Population dynamical behavior of non-autonomous Lotka–Volterra competitive system with random perturbation. Discrete Contin Dyn Syst Ser A 24(2):523–545

Lions P-L, Sznitman A-S (1984) Stochastic differential equations with reflecting boundary conditions. Commun Pure Appl Math 37(4):511–537

Lungu EM, Øksendal B (1997) Optimal harvesting from a population in a stochastic crowded environment. Math Biosci 145(1):47–75

Lungu EM, Øksendal B (2001) Optimal harvesting from interacting populations in a stochastic environment. Bernoulli 7(3):527–539

Mao X, Yuan C (2006) Stochastic differential equations with Markovian switching. Imperial College Press, London

Radner R, Shepp L (1996) Risk vs. profit potential: a model for corporate strategy. J Econ Dyn Control 20(8):1373–1393

Scheer N, Schmidli H (2011) Optimal dividend strategies in a Cramer–Lundberg model with capital injections and administration costs. Eur Actuar J 1(1):57–92

Schreiber SJ, Benaïm M, Atchadé KAS (2011) Persistence in fluctuating environments. J Math Biol 62(5):655–683

Smith HL, Thieme HR (2011) Dynamical systems and population persistence, vol 118. American Mathematical Society, Providence

Song Q, Stockbridge RH, Zhu C (2011) On optimal harvesting problems in random environments. SIAM J Control Optim 49(2):859–889

Tran K, Yin G (2015) Optimal harvesting strategies for stochastic competitive Lotka–Volterra ecosystems. Automatica 55:236–246

Tran K, Yin G (2016) Numerical methods for optimal harvesting strategies in random environments under partial observations. Automatica 70:74–85

Tran K, Yin G (2017) Optimal harvesting strategies for stochastic ecosystems. IET Control Theory Appl 11(15):2521–2530

Turelli M (1977) Random environments and stochastic calculus. Theor Popul Biol 12(2):140–178

Acknowledgements

KT was supported in part by Vietnam National Foundation for Science and Technology Development (NAFOSTED) under Grant 101.03-2017.23. GY was supported in part by the National Science Foundation under Grant DMS-1710827.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendices

Appendix A: Properties of value functions

This section is devoted to several properties of the value function. Particularly, the lemma below will be helpful in proving the boundedness of the value function.

Lemma A.1

Suppose that Assumption 2.3 holds, (Y, Z) is an admissible control policy yielding the process X, and \(\Phi (\cdot )\in C^2(\mathbb {R}^d)\). Then for any \(s\ge 0\), there exist \({\widehat{X}}(s)\in \mathbb {R}^d\) and \({\widetilde{X}}(s)\in \mathbb {R}^d\) such that \({\widehat{X}}(s)\le X(s)\), \({\widetilde{X}}(s)\le X(s)\), and

Proof

Without loss of generality, we suppose that \(\Delta Y_i(s)> 0\) for \(i=1, \dots , k\) and \(\Delta Y_i(s)=0\) for \(i=k+1, \dots , {d}\), where \(k\le d\). Define

By the admissibility of (Y, Z), \(\Delta Z_i(s)= 0\) for \(i=1, \dots , k\) and \(\Delta Y_i(s)=0\) for \(i={k+1}, \dots , d\). We can check that

By the mean value theorem, there is a point \({\widehat{X}}(s)\le X(s)\) on the line segment connecting X(s) and \({X}^*(s)\) such that

Similarly, there is a point \({\widetilde{X}}(s)\le X(s)\) on the line segment connecting \({X}(s-)\) and \({X}^*(s)\) such that

The conclusion follows from (A.1) and (A.2). \(\square \)

Theorem 2.11

Let Assumption 2.3 be satisfied. Suppose that there exists a function \(\Phi : {{\bar{S}}}\mapsto [0, \infty )\) such that \(\Phi \in C^2({{\bar{S}}})\) and that \(\Phi (\cdot )\) solves the following coupled system of quasi-variational inequalities

where \(({\mathcal {L}}-\delta )\Phi (x)={\mathcal {L}}\Phi (x)-\delta \Phi (x)\). Then the following assertions hold.

- (a):

-

We have

$$\begin{aligned} V(x)\le \Phi (x)\quad \text {for any } x\in {S}. \end{aligned}$$(2.13) - (b):

-

Define the non-intervention region

$$\begin{aligned} {\mathcal {C}}= \left\{ x\in S: f_i(x)<\dfrac{\partial \Phi }{\partial x_i}(x)<g_i(x) \right\} . \end{aligned}$$Suppose that

$$\begin{aligned} ({\mathcal {L}}-r)\Phi (x)=0, \end{aligned}$$(2.14)for all \(x\in {\mathcal {C}}\), and that there exists a harvesting-seeding strategy \(\big (\widetilde{Y}, \widetilde{Z}\big ) \in {\mathcal {A}}_{x}\) and a corresponding process \(\widetilde{X}\) such that the following statements hold.

- (i):

-

\(\widetilde{X}(t)\in \overline{{\mathcal {C}}}\) for Lebesgue almost all \(t\ge 0.\)

- (ii):

-

\(\int \nolimits _0^{t} \left[ \nabla \Phi (\widetilde{X}(s))- f(\widetilde{X}(s))\right] \cdot d\widetilde{Y}^c(s)=0\) for any \(t\ge 0\).

- (iii):

-

\(\int \nolimits _0^{t} \Big [g(\widetilde{X}(s))-\nabla \Phi (\widetilde{X}(s)) \Big ] \cdot d\widetilde{Z}^c(s)=0\) for any \(t\ge 0\).

- (iv):

-

If \(\widetilde{X}(s)\ne \widetilde{X}(s-)\), then

$$\begin{aligned} \Phi (\widetilde{X}(s))-\Phi (\widetilde{X}(s-))=- f(\widetilde{X}(s-)) \cdot \Delta \widetilde{Z}(s). \end{aligned}$$ - (v):

-

\(\lim \limits _{N\rightarrow \infty }E_{x}\Big [e^{-rT_N}\Phi (\widetilde{X}(T_N))\Big ]=0\), where for each \(N=1, 2, \dots \),

$$\begin{aligned} \beta _N:=\inf \{t\ge 0: |X(t)|\ge N\},\quad T_N: = N \wedge \beta _N. \end{aligned}$$(2.15)

Then \(V(x)=\Phi (x)\) for all \(x\in S\), and \(\big (\widetilde{Y},\widetilde{Z}\big )\) is an optimal harvesting-seeding strategy.

Proof

(a) Fix some \(x \in S\) and \((Y, Z)\in {\mathcal {A}}_{x}\), and let X denote the corresponding harvested process. Choose N sufficiently large so that \(|x|<N\). For

by the admissibility of (Y, Z), we have

Then Dynkin’s formula leads to

It follows from (2.12) that

where \(\Delta \Phi (X(s))=\Phi (X(s))-\Phi (X(s-))\). By virtue of Lemma A.1, the monotonicity of \(f(\cdot )\), \(g(\cdot )\), and (2.12), we obtain

Since \(\Phi (\cdot )\) is nonnegative, it follows from (A.4) and (A.5) that

Letting \(N\rightarrow \infty \), it follows from (A.3) and the bounded convergence theorem that

Taking supremum over all \((Y, Z)\in {\mathcal {A}}_{x}\), we obtain \(\Phi (x)\ge V(x)\).

(b) Let (i)–(v) be satisfied. Then Dynkin’s formula leads to

By (i), \(({\mathcal {L}}-\delta )\Phi (\widetilde{X}(s))=0\) for almost all \(s\ge 0\). This, together with (ii) and (iv), implies that

Letting \(N\rightarrow \infty \) and using (iv), we obtain

This, together with (a), implies that \(\Phi (x)=V(x)\) for any \(x\in S\) and \((\widetilde{Y}, \widetilde{Z})\) is an optimal harvesting strategy. \(\square \)

Next, we establish the continuity of the value function.

Proposition 2.5

Let Assumption 2.3 be satisfied. Then the following assertions hold.

- (a):

-

For any \(x, y\in {{\bar{S}}}\),

$$\begin{aligned} V(y)\le V(x) - f(x)\cdot (x-y)^++g(x)\cdot (x-y)^-. \end{aligned}$$(2.6) - (b):

-

If \(V(0)<\infty \), then \(V(x)<\infty \) for any \(x\in {{\bar{S}}}\) and V is Lipschitz continuous.

Proof

(a) Fix \((Y, Z)\in {\mathcal {A}}_{y}\). Define

Then \(({\widetilde{Y}}, {\widetilde{Z}})\in {\mathcal {A}}_{x}\). Let \({\widehat{X}}\) denote the process satisfying (2.2) with \({\widehat{X}}(0-)=x\) and strategy (Y, Z). Let \({\widetilde{X}}\) denote the process satisfying (2.2) with \({\widetilde{X}}(0-)=y\) and strategy \(({\widetilde{Y}}, {\widetilde{Z}})\). Then we have \({\widehat{X}}(t)={\widetilde{X}}(t)\) for any \(t> 0\). Consequently, it follows that

Since \(V(x)\ge J(x, {\widetilde{Y}}, {\widetilde{Z}})\), we have

from which, (2.6) follows by taking supremum over \((Y, Z)\in {\mathcal {A}}_{y}\).

(b) Similar to (2.6), we have

In view of (2.6) and (A.6), if \(V(0)<\infty \), then \(V(x)<\infty \) for any \(x\in {{\bar{S}}}\). Moreover,

Thus, \(V(\cdot )\) is Lipschitz continuous. \(\square \)

Using Theorem 2.11, we proceed to present an easily verifiable condition for the finiteness of the value function.

Proposition 2.7

Let Assumption 2.3 be satisfied. Moreover, suppose that there is a positive constant C such that

Then there exist a positive constant M such that

Proof

Define

where M is a positive number to be specified. We can check that \(\Phi (\cdot )\) solves the system of inequalities (2.12) for sufficiently large M. By virtue of Theorem 2.11, \(V(x)\le \Phi (x)\) for any \(x \in S.\) The details are omitted for brevity. \(\square \)

Throughout the rest of this section, we aim to characterize the value function as a viscosity solution of an associated system of quasi-variational inequalities. Our approach is motivated by Asmussen and Taksar (1997), Song et al. (2011). However, the results and proofs below are nontrivial extensions because we have interacting species as well as seeding. We use the following notation and definitions. For a point \(x^0\in S\) and a strategy \((Y, Z)\in {\mathcal {A}}_{x^0}\), let X be the corresponding process with harvesting and seeding. Let \(B_\varepsilon (x^0)=\{x\in S: |x-x^0|<\varepsilon \}\), where \(\varepsilon >0\) is sufficiently small so that \(\overline{B_\varepsilon (x^0)}\subset S\). Let \(\theta =\inf \{t\ge 0: {X}(t)\notin B_\varepsilon (x^0) \}\). For a constant \(r>0\), we define \(\theta _r=\theta \wedge r\).

Proposition A.2

Let Assumption 2.3 be satisfied and suppose that \(V(x)<\infty \) for all \(x\in {{\bar{S}}}\). The value function V is a viscosity subsolution of the system of quasi-variational inequalities

That is, for any \(x^0\in S\) and any function \(\phi \in C^2(S)\) satisfying

for all x in a neighborhood of \(x^0\), we have

Proof

For \(x^0\in S\), consider a \(C^2\) function \(\phi (\cdot )\) satisfying \(\phi (x^0)=V(x^0)\) and \(\phi (x)\le V(x)\) for all x in a neighborhood of \(x^0\). Let \(\varepsilon >0\) be sufficiently small so that \(\overline{B_\varepsilon (x^0)}\subset S\) and \(\phi (x)\le V(x)\) for all \(x\in \overline{B_\varepsilon (x_0)}\), where \(\overline{B_\varepsilon (x_0)}=\{x\in S: |x-x^0|\le \varepsilon \}\) is the closure of \(B_\varepsilon (x^0)\).

Choose \((Y, Z)\in {\mathcal {A}}_{x^0}\) such that \(Y(0-)=Z(0-)=0\), \(Y(t)=Y(0)\) and \(Z(t)=Z(0)\) for any \(t\ge 0\), \(|\Delta Y(0)|+|\Delta Z(0)|\le \eta \), where \(\eta \in [0, \varepsilon )\). Thus, there are only jumps at time \(t=0\). Let X be the corresponding harvested process with initial condition \(x^0\) and strategy (Y, Z).

Note that the chosen strategy (Y, Z) guarantees that X has at most one jump at \(t=0\) and remains continuous on \((0, \infty )\). This, together with the fact that \(\eta \in [0, \varepsilon )\), implies that \({X}(t)\in \overline{B_\varepsilon (x^0)}\) for all \(0\le t\le \theta \). By virtue of the dynamic programming principle, we have

By the Dynkin formula, we obtain

A combination of (A.9) and (A.10) leads to

First, we take \(\eta =0\); that is, \(Y(t)=Z(t)=0\) for any \(t\ge 0\). Then \(\theta >0\) almost surely (a.s.) and (A.11) can be rewritten as

We suppose that \(({\mathcal {L}}-\delta )\phi (x^0)>0\). Then we can choose a sufficiently small \(\varepsilon >0\) such that \(({\mathcal {L}}-\delta )\phi (x)>0\) for any \(x\in B_\varepsilon (x^0)\). Note that we can find such an \(\varepsilon \) while still making sure that the condition from the beginning of the proof holds - one just needs to take the minimum of the two small numbers. As a result, \(({\mathcal {L}}-\delta )\phi (X(s))>0\) for any \(t\in [0, \theta )\). It follows that \(\int _0^{\theta _r} e^{-\delta s} ({\mathcal {L}}-\delta ) \phi ({X}(s))ds>0\) and therefore,

which contradicts (A.12). This proves that

Next, we fix \(i\in \{1, \dots , d\}\) and take \(\eta \in (0, \varepsilon )\), \(Y_i(t)=Y_i(0)=\eta \) for all \(t\ge 0\), and \(Y_j(t)=Z_i(t)=Z_j(t)=0\) for all \(j\ne i\) and \(t\ge 0\). Then (A.11) reduces to

Now sending \(r\rightarrow 0\), we have

By dividing the above inequality by \(\eta \) and letting \(\eta \rightarrow 0\), we obtain

Now we take \(\eta \in (0, \varepsilon )\), \(Z_i(t)=\eta \) for all \(t\ge 0\), and \(Z_j(t)=Y_i(t)=Y_j(t)=0\) for all \(j\ne i\) and \(t\ge 0\). Then (A.11) reduces to

Now sending \(r\rightarrow 0\), we have

Finally, dividing the above inequality by \(\eta \) and letting \(\eta \rightarrow 0\), we arrive at

Now (A.8) follows by combining (A.13), (A.14), and (A.15). \(\square \)

Lemma A.3

Suppose (Y, Z) is an admissible strategy and let X be the resulting population process. Define the random variable \(\lambda \) as follows. If \(X(\theta )=X(\theta -)\) then \(\lambda =0\), while if \(X(\theta )\notin \overline{B_\varepsilon (x^0)}\), then let \(\lambda \) be a positive number in (0, 1] such that

Then there is a positive number \(\kappa _0>0\) such that

where \({\hbox {1{}1}}(x)=(1,\dots ,1)'\) for all \(x\in {\bar{S}}\).

Proof

Recall that \(\theta _r=\theta \wedge r\) for any positive number r. Define

It can be seen that \(X_\lambda ^r\in \overline{B_\varepsilon (x^0)}\) for any \(r>0\). We consider the function \({\widetilde{\Phi }} (x)= |x-x^0|^2-\varepsilon ^2\) for \(x \in B_\varepsilon (x^0)\). It follows that

Since \({\widetilde{\Phi }}(\cdot ), b(\cdot )\), and \(\sigma (\cdot )\) are continuous, it is obvious that

for some positive constant K. Note that K depends only on \(x^0, \varepsilon , \delta \) and bounds on \(b(\cdot ), \sigma (\cdot )\). Let \(K_0=\dfrac{1}{K+2\varepsilon }\) and define \(\Phi (x)=K_0 {\widetilde{\Phi }}(x)\) for \(x\in B_\varepsilon (x^0)\). Then it follows immediately that

Moreover, we have

By virtue of the Dynkin formula, we have

By virtue of (A.18), we have

where P(s) is a point on the line connecting X(s) and \(X(s-)\). Hence it follows from (A.17)–(A.20) that

We also have

where \(P_0\) is a point on the line segment connecting \({X}(\theta _r-)\) and \({X}_\lambda ^r\). Thus,

Combining (A.21) and (A.23), we have

By letting \(r\rightarrow \infty \), we arrive at

If \({{\mathbb {P}}}(\theta =\infty )>0\), then \({{\mathbb {E}}}e^{-\delta \theta }\Phi ({X}_\lambda )=0\). Otherwise, \(\theta <\infty \) a.s. and in that case, since \(\Phi ({X}_\lambda )\in \partial B_\varepsilon (x^0)\), \(\Phi ({X}_\lambda )=0.\) Also, it is clear that \(\Phi (x^0)= -K_0 \varepsilon ^2.\) Thus, we obtain

Set \(\kappa _0:=K_0\varepsilon ^2\) and note that the above establishes (A.16). \(\square \)

Proposition A.4

Let Assumption 2.3 be satisfied and assume that \(V(x)<\infty \) for \(x\in {{\bar{S}}}\). The value function V is a viscosity supersolution of the system of quasi-variational inequalities (A.7); that is, for any \(x^0\in S\) and any function \(\varphi \in C^2(S)\) satisfying

for all x in a neighborhood of \(x^0\), we have

Proof

Let \(x^0\in S\) and suppose \(\varphi (\cdot )\in C^2(S)\) satisfies (A.26) for all x in a neighborhood of \(x^0\).

We argue by contradiction. Suppose that (A.27) does not hold. Then there exists a constant \(A>0\) such that

Let \(\varepsilon >0\) be small enough so that \(\overline{B_\varepsilon (x^0)}\subset S\) and for any \(x\in \overline{B_\varepsilon (x^0 )}\), \(\varphi (x)\ge V(x)\) and

Let \((Y, Z)\in {\mathcal {A}}_{x^0}\) and X be the corresponding harvested process. Recall that \(\theta =\inf \{t\ge 0: {X}(t)\notin B_\varepsilon (x^0) \}\) and \(\theta _r=\theta \wedge r\) for any \(r>0\). It follows from the Dynkin formula that

By virtue of Lemma A.1, for any \(s\in [0, \theta _r)\), there exist \({\widehat{X}}(s)\in \mathbb {R}^d\) and \({\widetilde{X}}(s)\in \mathbb {R}^d\) such that \({\widehat{X}}(s)\le X(s)\), \({\widetilde{X}}(s)\le X(s)\), and

This, together with the monotonicity of the functions f, g, and equation (A.29) imply that

Hence it follows from (A.29) and (A.30) that

Therefore,

We are in a position to apply Lemma A.3. To this end, recall from Lemma A.3 that \(\lambda \) is a random variable such that if \(X(\theta )=X(\theta -)\), then \(\lambda =0\); and if \(X(\theta -)\ne X(\theta )\), then \(\lambda \) is the positive number in (0, 1] such that

Note that \(\lambda \) is independent of r. Also recall that

Using the same argument as the one in Lemma A.1, we obtain

Combining (A.32) and (A.33), we have

Since \({X}_\lambda ^r\in \overline{B_\varepsilon (x^0)}\), \(\varphi ({X}_\lambda ^r)\ge V({X}_\lambda ^r)\). On the other hand, it follows from (2.6) that

By (A.34) and (A.35) we note that

Letting \(r\rightarrow \infty \), we have

Using (A.16) and (A.37), we arrive at

Taking the supremum over \((Y, Z)\in {\mathcal {A}}_{x^0}\), it follows that

In view of the dynamic programming principle, (A.39) can be rewritten as

which is a contradiction. As a result (A.27) has to hold, i.e. V is viscosity supersolution of (A.7). \(\square \)

Summarizing what have obtained thus far, we state the following result.

Theorem A.5

Let Assumption 2.3 be satisfied and suppose \(V(x)<\infty \) for \(x\in {S}\). The value function V is a viscosity subsolution and also a viscosity supersolution, and hence a viscosity solution, of the system of quasi-variational inequalities (A.7).

Appendix B: Numerical algorithm

1.1 B.1: Transition probabilities and local consistency

We use the notation defined in Sect. 2.1. To proceed, we state one more assumption below, which will be used to ensure the validity of transition probabilities \(p^h(x, y|\pi )\). However, it is not an essential assumption. There are several alternatives to handle the cases when Assumption B.1 fails. We refer the reader to page 1013 in the book by Kushner (1990) for a detailed discussion. Define for any \(x\in {\bar{S}}\) the covariance matrix \(a(x)= \sigma (x)\sigma '(x)\).

Assumption B.1

For any \(i=1, \dots , d\) and \(x\in {{\bar{S}}}\),

Let \({{\mathbb {E}}}^{h, \pi }_{x, n}\), \({\mathbb Cov}^{h, \pi }_{x, n}\) denote the conditional expectation and covariance given by

respectively. Our objective in this subsection is to define transition probabilities \(p^h (x, y | \pi )\) so that the controlled Markov chain \(\{X^h_n\}\) is locally consistent with respect to the diffusion (2.2) in the sense that the following conditions hold:

To this end, using the procedure introduced by Kushner (1990), we define the approximation to the first and the second derivatives of V by a finite difference method using the step size \(h>0\) for the state variable. Afterwards, we plug in all the approximations into the first part of system (A.7), combine similar terms and divide by the coefficient of \(V^h(x)\). The transition probabilities are the coefficients of the resulting equation. For \(x\in S_h\), define

where for a real number c, \(c^+=\max \{c, 0\}\), \(c^-=-\min \{0, c\}\); that is, \(c=c^+\) if \(c\ge 0\) and \(c=-c^-\) if \(c<0\). Set \(p^h (x, y|\pi =0)=0\) for all unlisted values of \(y\in S^h\). Assumption B.1 guarantees that the transition probabilities in (B.2) are well-defined. At the seeding and harvesting steps, we define

Thus, \(p^h (x, y|\pi =\pm i)=0\) for all nonlisted values of \(y\in S^h\). Using the above transition probabilities, we can check whether the locally consistent conditions of \(\{X^h_n\}\) in (B.1) are satisfied.

1.2 B.2: Continuous-time interpolation and time rescaling

The convergence result is based on a continuous-time interpolation of the chain, which will be constructed to be piecewise constant on the time interval \([t^h_n, t^h_{n+1}), n\ge 0\). For use in this construction, we define \(n^h(t)=\max \{n: t^h_n\le t\}, t\ge 0\). We first define discrete time processes associated with the controlled Markov chain as follows. Let \(Y^h_0=Z^h_0=B^h_0=M^h_0=0\) and define for \(n\ge 1\),

The piecewise constant interpolations, denoted by \((X^h(\cdot ), Y^h(\cdot ), Z^h(\cdot ), B^h(\cdot ), M^h(\cdot ))\) are naturally defined as

Define \({\mathcal {F}}^h(t)=\sigma \{X^h(s), Y^h(s), Z^h(s): s\le t\}={\mathcal {F}}^h_{n^h(t)}\). Using the representation of diffusion, harvesting, and seeding steps in (2.17), we obtain

This implies

Recall that \(\Delta t^h_m = h^2/Q_h(X^h_m)\) if \(\pi ^h_m=0\) and \(\Delta t^h_m = 0\) if \(\pi ^h_m\ge 1\) or \(\pi ^h_m\le -1\). It follows that

with \(\{\varepsilon _1^h(\cdot )\}\) being an \({\mathcal {F}}^h(t)\)-adapted process satisfying

We now attempt to represent \(M^h(\cdot )\) in a form similar to the diffusion term in (2.2). Factor

where \(P(\cdot )\) is an orthogonal matrix, \(D(\cdot )=\mathrm{diag}\{r_1(\cdot ), ..., r_d (\cdot )\}\). Without loss of generality, we suppose that \(\inf \limits _{x}r_i(x)>0\) for all \(i=1, ..., d\). Define \(D_0(\cdot )=\mathrm{diag}\{1/r_1(\cdot ), ..., 1/r_d (\cdot )\}\).

Remark B.2

In the argument above, for simplicity, we assume that the diffusion matrix (a(x)) is nondegenerate. If this is not the case, we can use the trick from (Kushner and Dupuis 1992, pp. 288–289) to establish equation (B.10).

Define \(W^h(\cdot )\) by

Then we can write

with \(\{\varepsilon _2^h(\cdot )\}\) being an \({\mathcal {F}}^h(t)\)-adapted process satisfying

Using (B.8) and (B.10), we can write (B.7) as

where \(\varepsilon ^h(\cdot )\) is an \({\mathcal {F}}^h(t)\)-adapted process satisfying

The objective function from (2.20) can be rewritten as

Time rescaling. Next we will introduce a “stretched-out” time scale. This is similar to the approach previously used by Kushner and Martins (1991) and Budhiraja and Ross (2007) for singular control problems. Using the new time scale, we can overcome the possible non-tightness of the family of processes \(\{Y^h(\cdot ), Z^h(\cdot )\}_{h>0}\).

Define the rescaled time increments \(\{\Delta \widehat{t}_n^h: n=0, 1, ...\}\) by

The time scale is stretched out by h at the seeding and harvesting steps.

Definition B.3

The rescaled time process \(\widehat{T}^h(\cdot )\) is the unique continuous nondecreasing process satisfying the following:

-

(a)

\(\widehat{T}^h(0)=0\);

-

(b)

the derivative of \(\widehat{T}^h(\cdot )\) is 1 on \((\widehat{t}^h_n, \widehat{t}^h_{n+1})\) if \(\pi ^h_n=0\), i.e., n is a diffusion step;

-

(c)

the derivative of \(\widehat{T}^h(\cdot )\) is 0 on \((\widehat{t}^h_n, \widehat{t}^h_{n+1})\) if \(\pi ^h_n\ne 0\), i.e., n is a seeding step or a harvesting step.

Thus \(\widehat{T}^h(\cdot )\) does not increase at the times t at which a harvesting step or a seeding step occurs. Define the rescaled and interpolated process \(\widehat{X}^h(t)= \xi ^h(\widehat{T}^h(t))\) and likewise define \(\widehat{Y}^h(\cdot )\), \(\widehat{Z}^h(\cdot )\), \(\widehat{B}^h(\cdot )\), \(\widehat{M}^h(\cdot )\), and the filtration \(\widehat{{\mathcal {F}}}^h(\cdot )\) similarly. It follows from (B.7) that

Using the same argument we used for (B.11) we obtain

with \(\widehat{\varepsilon }^h(\cdot )\) is an \(\widehat{{\mathcal {F}}}^h(\cdot )\)-adapted process satisfying

1.3 Convergence

Using weak convergence methods, we can obtain the convergence of the algorithms. The proofs to the following results are essentially the same as those given by Jin et al. (2013), Tran and Yin (2016) and we therefore omit the details.

Theorem B.4

Suppose Assumptions 2.3 and B.1 hold. Let the approximating chain \(\{X^h_n \}\) be constructed with transition probabilities defined in (B.2)–(B.3), \(\big (X^h(\cdot ), W^h(\cdot ), Y^h(\cdot ), Z^h(\cdot )\big )\) be the continuous-time interpolation defined in (B.4)–(B.5), (B.9), and \(\widehat{T}^h(\cdot )\) be the process from Definition B.3. Let \(\widehat{X}^h(\cdot ), \widehat{W}^h(\cdot ), \widehat{Y}^h(\cdot ), \widehat{Z}^h(\cdot )\) be the corresponding rescaled processes and denote

Then the family of processes \((\widehat{H}^h)_{h>0}\) is tight. As a result, \((\widehat{H}^h)_{h>0}\) has a weakly convergent subsequence with limit

We proceed to characterize the limit process.

Theorem B.5

Suppose Assumptions 2.3 and B.1 hold. Let \(\widehat{{\mathcal {F}}}(t)\) be the \(\sigma \)-algebra generated by

Then the following assertions hold.

- (a):

-

\(\widehat{W}(t)\) is an \(\widehat{{\mathcal {F}}}(t)\)-martingale with quadratic variation process \(\widehat{T}(t)I_d\).

- (b):

-

\(\widehat{Y}(\cdot )\), \(\widehat{Z}(\cdot )\), and \(\widehat{T}(\cdot )\) are nondecreasing and nonnegative.

- (c):

-

The limit processes satisfy

$$\begin{aligned} \widehat{X}(t)=x +\int _0^t b(\widehat{X}(s))d\widehat{T}(s)+\int _0^t \sigma (\widehat{X}(s))d\widehat{W}(s)-\widehat{Y}(t)+\widehat{Z}(t), \quad t\ge 0.\nonumber \\ \end{aligned}$$(B.17)

For \(t<\infty \), define the inverse \(R(t)= \inf \{s: \widehat{T}(s)>t\}\). For any process \(\widehat{\nu }(\cdot )\), define the time-rescaled process \(({\bar{\nu }}(t))\) by \({\bar{\nu }}(t)= \widehat{\nu }(R(t))\). Let \({\mathcal {{\bar{F}}}}(t)\) be the \(\sigma \)-algebra generated by \(\{{{\bar{X}}}(s), {{\bar{W}}}(s), {{\bar{Y}}}(s), {{\bar{Z}}}(s), {{\bar{R}}}(s): s\le t\}\). Let \(V^h(x)\) and \(V^U(x)\) be value the functions defined in (2.16) and (2.21), respectively.

Theorem B.6

Suppose Assumptions 2.3 and B.1 hold. The following assertions are true.

- (a):

-

\({\bar{R}}\) is right continuous, nondecreasing, and \({\bar{R}}(t)\rightarrow \infty \) as \(t \rightarrow \infty \) with probability 1.

- (b):

-

\({\bar{Y}}\) and \({\bar{Z}}\) are right-continuous, nondecreasing, nonnegative, and \(\mathcal {{\bar{F}}}(t)\)-adapted processes.

- (c):

-

\({\bar{W}}(\cdot )\) is a standard \(\mathcal {{\bar{F}}}(t)\) adapted d dimensional Brownian motion, and

$$\begin{aligned} {{\bar{X}}}(t)=x +\int _0^t b({\bar{X}}(s))ds+\int _0^t \sigma ({\bar{X}}(s))d{\bar{W}}(s)-{\bar{Y}}(t)+\bar{Z}(t), \quad t\ge 0.\nonumber \\ \end{aligned}$$(B.18) - (d):

-

For any \(x\in [0, U]^d\), \(V^h(x)\rightarrow V^U(x)\) as \(h\rightarrow 0\).

Rights and permissions

About this article

Cite this article

Hening, A., Tran, K.Q., Phan, T.T. et al. Harvesting of interacting stochastic populations . J. Math. Biol. 79, 533–570 (2019). https://doi.org/10.1007/s00285-019-01368-x

Received:

Revised:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00285-019-01368-x