Abstract

Background

South Korea is unique in that it leads global markets in R&D as well as production of biosimilar products and was the first market into which some biosimilar products were introduced. We analyzed the time trend of market penetration and simulated saved spending by biosimilars in South Korea.

Methods

We pulled Korean National Health Insurance claims data from January 2012–December 2018 for second-generation biologics, including infliximab, rituximab, and trastuzumab, and examined the time trends of expenditure, utilization in defined daily dose, and price. We also assessed market penetration by biosimilars and simulated expenditure savings gained due to their introduction. We comparatively examined time trends and spending savings during the same period for selected small-molecule generic drugs to understand any specifics limited to biosimilars for time trends of market share and quantity-standardized prices.

Results

The market share for infliximab biosimilar plateaued at over 30%, which is smaller than the market penetration of esomeprazole (over 60%), a small-molecule comparator. Despite a shorter observation period, rituximab and trastuzumab biosimilars also showed larger utilization rates (12.89% and 13.93%, respectively) than infliximab (9.05%) in their second year after market entry. Infliximab was associated with approximately US $82–114 million expenditure savings over 6 years after its biosimilar entry to the market. Rituximab and trastuzumab biosimilars each also resulted in reduction in total spending by approximately US $9–14 million, in less than 2 years.

Conclusion

Biosimilars captured the market rapidly, despite a heterogeneous uptake rate by product in South Korea. However, expansion of biosimilar use in the market and consequent expenditure savings need to be supported by pre-emptive policy measures to encourage price competition and boost utilization.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

The second-generation biosimilars overall captured the market rapidly at an early stage after market entry. |

In the medium term, the second-generation biosimilars plateaued at a lower level of market share than small-molecule generics. |

Expenditure savings gained from the introduction of biosimilars were substantial, but the lack of more price reduction confined the magnitude of savings. |

Pre-emptive policy measures may be needed to ensure expenditure savings following expansion of biosimilar use in the market. |

1 Introduction

Rising healthcare expenditure is a global concern. The total pharmaceutical expenditure across OECD countries was more than US $800 billion in 2015 [1]. Technology advancement in the pharmaceutical industry particularly leads to innovative biological drugs such as cancer immunotherapy or cell therapeutics, which are highly priced in general [2, 3]. However, recent patent expirations of high-priced biologics and ensuing introduction of biosimilar products onto the market may reduce costs of such high-end drugs [4,5,6,7,8].

For traditional small-molecule drugs, cost savings by generic entry to the market has been investigated widely in the previous literature [9,10,11,12,13,14,15,16,17,18]. However, there has been little evidence presented on savings from the entry of biosimilars, generic versions of biologics. Several budget impact analyses have projected the potential cost savings from biosimilars such as infliximab, rituximab, and trastuzumab for autoimmune diseases and breast cancer, particularly in European countries [6, 19,20,21,22,23,24]. Biosimilars were projected to reduce spending in the USA on biologic drugs by US $54 billion (3% of total estimated biologics spending) from 2017 to 2026 [8], despite the biosimilar infliximab having only 5% market penetration in 2018 [25]. The reduction of the average medication cost for infliximab was found to be 30% in Korea [26], where several leading pharmaceutical companies have vigorously led research and development (R&D) of biosimilar products [14, 26]. Despite such evidence, our understanding about the financial impact of market entry of biosimilars remains limited, since the available data are scarce due to the relatively small number and short history of those products.

The mechanism of cost savings from the use of biosimilars is similar to that of cost-saving from generics of small-molecule drugs. First, biosimilars, whose R&D costs are less than those of the original products, enter the market at lower prices. Second, the emergence of alternative treatments weakens the monopoly status of original products, which also can lead to a drop in prices. However, the introduction of generic medicines might expand the market in some treatment areas [14], and the prices are rigid, all of which would hinder expected cost savings by generic entries to the market. Therefore, whether the emergence of biosimilars contributes to cost savings is an empirical question to be answered by assessing the market share of biosimilars and the extent of decrease in the average price.

Pharmaceutical expenditure is contextual and influenced by the healthcare system, including insurance schemes for pharmaceuticals. Such contextual heterogeneity within a given market raises the need for evidence from a specific healthcare system to effectively and comprehensively design measures for rational pharmaceutical use and spending. Korea is unique in that it leads the global market in R&D as well as production of biosimilar products, despite its overall pharmaceutical industry being relatively weak. A biosimilar for infliximab, the first biosimilar product in the world, was developed by a firm in Korea, which also developed biosimilars for rituximab, trastuzumab, and etanercept. Korea is the first market in which those products were released. Thus, analyzing market penetration and price movement of those biosimilars in Korea would contribute to global evidence.

The purpose of this study was to analyze the time trend of market penetration of and the saved spending from three second-generation biosimilars available for at least 1 year in South Korea between 2012 and 2018: infliximab, rituximab, and trastuzumab. In order to understand any specifics limited to biosimilars, we also selected small-molecule generic drugs to compare time trends and spending savings during the same period. The small-molecule generics of interest were listed in the same time window as the biosimilars of interest and each treatment, including the originator and the generic products, reimbursed 100 billion Korean Won (KRW) or higher during the analysis period. This work will provide insights into what policy changes on biosimilars are needed to increase biosimilar use and savings.

2 Methods

2.1 Data

We used claims data from the National Health Insurance Service (NHIS) for the present study. NHIS is the only public health insurer, with all Koreans and legal foreign residents as compulsory beneficiaries, and all medical providers are mandatory participants. The prescribers can choose whether to use the originator or the generic drugs without restriction in South Korea. This is the same for the biologic medicines regardless of the context of the medical practice: hospital, outpatient, and prescribed medicines. The NHIS claims data is built on insurance claims from healthcare providers, and it contains detailed prescription information including brand name, administration dosage, and frequency. Therefore, we can assume that our data represent literally all utilization of the selected drugs in South Korea. We pulled all claims for drugs of interest from January 2012 to December 2018.

Biosimilars of first-generation biologics have been available for some time in the fields of hematology and supportive cancer care [27]. More recently, biosimilars of more complex, second-generation biologicals, such as monoclonal antibodies, have been approved for treatment of rheumatoid arthritis (RA), other immune-related inflammatory diseases, and cancers [28]. In Korea, the emergence of second-generation biosimilars began in 2012, and infliximab, trastuzumab, rituximab, and etanercept are currently available (as of June 2019). The current study included only infliximab, rituximab, and trastuzumab among the four second-generation biologicals in order to analyze at least a 12-month trajectory of market behaviors. All utilization data, including inpatient use and dispensed medicines are analyzed for these three medicines.

Infliximab, the first second-generation biosimilar, is a treatment for chronic inflammatory autoimmune diseases, and is indicated for RA and inflammatory bowel disease (IBD) [6]. The original infliximab (Remicade®) was listed in 2001 in the NHIS, and 3645 patients per month were treated on average in 2017 in South Korea. Original rituximab (Mabtera®), which is widely used for oncology, hematology, rheumatology, and nephrology, was introduced in 1998 in the national formulary, and 2437 patients were treated with it per month in 2017 [29]. Trastuzumab is approved for the treatment of early breast cancer, advanced breast cancer, and metastatic gastric cancer [30]. The original trastuzumab (Herceptin®) was listed in 2000 in the NHIS, and 2052 patients were treated with it monthly in 2017. Etanercept has been mainly used for RA since 2004, and 2313 patients were treated per month in 2017 in South Korea [31].

In April 2012, the NHIS enacted a drastic pricing policy for drugs in the formulary, which enforces a price drop to the level of 53.55% of the off-patent price for small-molecule originators and 70–80% for the price of biologics once corresponding generics are listed. At the same time, the list price of the biosimilars and generics are capped at the lowered originators’ price [32]. Given that the first second-generation biosimilar product, infliximab, was listed in December 2012 in the national formulary (after the enforced price cut in April 2012), it is important to select small-molecule treatments as comparators that were exposed to the same pharmaceutical policy change. Among generics listed after the price reform in 2012, we selected imatinib, esomeprazole, and entecavir, which are used in the areas of hemato-oncology, gastroenterology, and hepatology, respectively. All utilization data, including inpatient use and dispensed medicines, are analyzed for these three medicines. All of the generics of the selected small-molecule drugs were listed in the national formulary in a similar time window to those of the biosimilars of interest. The annual spending on each of these treatments has been recorded as being over 100 billion KRW (approximately US$91 million); therefore, the budget impact of them on the NHIS is significant.

2.2 Variables

The main outcome variables are spending, utilization, and unit price of each treatment. Spending of each drug was measured as monthly total expenditure, which includes the cost subsidized by NHIS as well as out-of-pocket costs. Utilization was measured as monthly quantity used in defined daily dose (DDD), a standardized quantity per day to maintain efficacy for its main indication in adults [33]. Because no definitions of DDDs are available for rituximab, trastuzumab, and imatinib, we used the maintenance dose for main indications of each product approved by Ministry of Food and Drug Safety in Korea as a proxy measure of DDDs for those products. For unit price, we used cost divided by DDD of each treatment as the standardized measure [34]. The cost per DDD or quantity-adjusted unit cost represents the daily cost per treatment when the standard maintenance dose was applied.

2.3 Analysis

First, we addressed the trend of unit cost and share of generic spending on a yearly basis. Then we assessed the penetration patterns of generics by comparing the DDD patterns of originator and corresponding generics on a monthly basis.

Second, we conducted simulations on the cost savings gained from the introduction of generics based on various assumed price changes but fixed share of utilization of generics as observed in the data. These simulations are intended to help understand past cost savings yielded from biosimilar enlisted in the NHIS, not to project future cost savings. In the first simulation, we assumed no price change of the originators regardless of the entry of biosimilars to the market. In fact, as discussed above, the NHIS enforced a price cut from the initial listed price at the level of 70–80% for the original biologics and 53.55% for the original small-molecule medicines. We calculated simulated expenditure of the originators as the multiplication of the prices of originators before the entry of biosimilars to actual utilization amounts of originators. In the second simulation, we supposed no biosimilar entry in the market and that originators take the observed biosimilar shares; the prices of originators are naturally taken as the initial list-prices, since we assumed no biosimilar entry to the national formulary. Both simulations were also conducted for comparator small-molecule generics of interest in order to understand any similarities or differences between biologics and small-molecule drugs in terms of time trends of market share and quantity-standardized prices.

We used SAS (version 9.4; SAS Institute, Cary, NC, USA) for data processing and analyses, and Microsoft Excel (version 2010) was used for simulations.

3 Results

Table 1 shows the entry dates and therapeutic indications of biosimilars and small-molecule comparators for the current study. Biosimilar products of infliximab, rituximab, and trastuzumab were entered in the national formulary in December 2012, April 2017, and June 2017, respectively. The small-molecule generics of imatinib, esomeprazole, and entecavir were listed in September 2013, October 2014, and October 2015, respectively. Only two to three manufacturers for biosimilars of interest in Korea were identified, whereas 12–89 manufacturers were found for small-molecule generic comparators based on actual claims to the NHIS in 2018 (Table 1).

The time trend of standardized price as in price per DDD (referred to interchangeably as unit cost hereafter) for each product is presented in Table 2. The unit cost (price per DDD) for original biologics diminished for all investigated products: the unit cost for original infliximab decreased by 30.1% after 2 years from biosimilar entry to the national formulary; the corresponding decreases were 20.8% for rituximab and 21.2% for trastuzumab. Small-molecule comparators showed a larger reduction of unit cost following generic entry than biologics to the extent of 48.6% for imatinib, 46.7% for esomeprazole, and 45.8% for entecavir in the third year of generic entry. However, no further reduction of unit cost was observed particularly for infliximab, imatinib, and esomeprazole, which have longer periods of observation after the entry of their generic products. Moreover, the unit costs of generics and biosimilars were only slightly lower than originators, and even slightly higher for esomeprazole (Table 2).

Table 3 shows the yearly time trend of total expenditure and share of biosimilars or generics for each investigated treatment, which shows a heterogeneous pattern by drug category. Total expenditure for infliximab and esomeprazole showed an upward trend over years, whereas expenditure for trastuzumab, imatinib, and entecavir presented a downward trend over years. The spending share for infliximab biosimilar reached over 30% in the sixth year from its initial entry to the national formulary. Even though only 2-year follow-up data were available for biosimilars of rituximab and trastuzumab, each showed larger utilization rates (12.89% and 13.93%, respectively) than infliximab (9.05%) for the corresponding period. A large variation in the growth rate of spending share was observed for small-molecule generic drugs of interest given that the share during the second year was almost a half (47.21%) for esomeprazole, whereas it was only 15.45% for entecavir and 1.17% for imatinib. The spending share for imatinib generics remained negligible even in the sixth year from its initial market entry (Table 3).

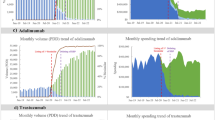

We also depicted a monthly trend of utilization in DDD and share of biosimilars and generics in each biologics and small-molecule treatment. For infliximab, biosimilar products penetrated markets rapidly during the early phase following market entry in December 2012, reaching approximately 30% in 48 months. The utilization shares of biosimilars for rituximab and trastuzumab also showed steep increases, each reaching approximately 20% in 12 months, though data for further years are not yet available (Fig. 1a). Generic esomeprazole infiltrated the market very rapidly to the maximum of 66.9%, but remained stagnant thereafter. Generic entecavir also showed only a quarter of total utilization at the maximum during the observed time periods, and generic imatinib rarely subverted the originals in the market share, even several years after its entry (Fig. 1b).

Trend of monthly utilization in defined daily dose (DDD) and utilization share of biosimilars (a) and small-molecule generics (b). The dotted vertical lines indicate entry date of each biosimilar product

Lastly, we show simulation results in Fig. 2a, b. Assuming that there were no biosimilars and generics introductions to the market, the discrepancy between real and simulated spending is the retrenched budget from generic entry to the market. Among biosimilars, infliximab showed the largest savings among the three groups of biologics investigated in the study, with approximately US $82–114 million over the 6 years since its generic entry to the market, depending on the simulation scenarios. Biosimilar rituximab and trastuzumab also resulted in reduction in total spending by approximately US $9 and US $14 million, respectively, for less than 2 years (19 months for rituximab and 17 months for trastuzumab), at the maximum (Fig. 2a). For small-molecule comparators, entry of the generic imatinib in the national formulary prompted enforced reduction of original imatinib and consequently led to a reduction in total spending by US $231 million, despite the generic version having barely penetrated the market. The maximum budget savings by generic esomeprazole and entecavir were also estimated as US $291 and US$233 million, respectively (Fig. 2b).

Simulation results on saved spending by introduction of biosimilars (a) and small-molecule generics (b). The first scenario represents no price cut due to entry of biosimilar or small-molecule generics in the market. The second scenario represents no price reduction of originator despite the introduction of biosimilar or small-molecule generics. The blue and orange areas represent the saved spending due to the introduction of biosimilar of small-molecule generics, respectively, under each scenario

4 Discussion

The current study investigated the trend of market penetration and the cost saving gained from the use of biosimilar products for infliximab, rituximab, and trastuzumab in comparison to selected generic drugs for small-molecule products. Our findings show that biosimilars acquired market share at a relatively similar rate to that of some of the generics of the selected small-molecule drugs, as they occupied almost one-fifth of the total utilization within a year from market entry. Given that the first-generation biosimilars, including epoetin, filgrastim, and somatropin, gained approximately 10% of the total market within 1 year from their entry in Europe [35, 36], the market share growth in a year for the biosimilars from the current study is much higher. Among small-molecule generics, imatinib exhibited a distinctive pattern, with little market penetration for generics despite a significant drop in price, possibly due to safety and efficacy issues of the generic versions in other countries [37,38,39,40]. In the USA, by contrast, the prescription share of generic imatinib has increased to 74% amid slow price drops since original imatinib’s patent had expired [41]. Additionally, it is worth noting that the generic having the most manufacturers, esomeprazole, had the highest market share and the generic with the least manufacturers, imatinib, had the lowest market share. Also, the generic with arguably the least severe indications, esomeprazole, had the highest market share.

Studies have cast doubt on the proposition that biosimilars can command a market share as easily as generic small-molecule drugs [42]. A stronger preference for branded biologics than for small-molecule pharmaceutical products also has been reported [43,44,45], driven by the ongoing concerns over interchangeability between biologics and their generic versions, unlike the established standards for general pharmaceuticals [28, 46, 47]. Such uncertainty about the equivalence between original biologics and biosimilar products restrains physicians from switching to biosimilars from brand biologics [43, 44, 48, 49]. Furthermore, due to high technology barriers, R&D of biosimilars is known to be much pricier, to the magnitude of approximately 100× in financial resources and 2–3× in time to success, than generics for small-molecule pharmaceuticals [42, 50,51,52]. Such product characteristics for biologics restrict the competitiveness of biosimilars in terms of price. Therefore, in order to increase biosimilar market penetration, it is important to produce and inform of clinical evidence of the possibility of substitution.

According to the NHIS claims data, total pharmaceutical expenditure can be separated into the amounts used for hospitalized patients, outpatient clinics, and dispensed prescriptions by community pharmacies. Generally, the pharmaceutical spending for hospitalization, outpatients, and dispensed prescriptions accounted for 14%, 16%, and 70%, respectively, in 2018 [53]. For biologic medicines in this analysis, however, these proportions were 16%, 75%, and 9%, respectively, in 2018, which indicates that biologics have been consumed more in the hospitals and clinics than in community pharmacies. This consumption pattern may explain the lower uptake of biosimilars in the market. The treatments that are used for more severe disease conditions tend not to be replaced for the generic versions.

Biosimilar infliximab was the front-runner for biosimilars in South Korea and showed a slower capture of the market than the two small-molecule generic drugs esomeprazole and entecavir in the current study. However, biosimilar latecomers for rituximab and trastuzumab exhibit a faster penetration of the market than did infliximab in South Korea. This may indicate improved value for bioequivalence for latecomer biosimilars partly due to real-world evidence for their effectiveness in European markets [6, 19, 20]. Future studies need to continue to monitor the market performance of biosimilars as medium- to long-term data are accumulated for late-coming biosimilars.

Pharmaceutical products traditionally show inelastic demand particularly for drugs for severe diseases, which circumscribes price competition between original drugs and their generic versions [43, 44, 54]. Therefore, imposing price cuts for pharmaceutical products has been actively used in various countries such as Australia or Norway [2], as well as in South Korea, as a policy measure to contain drug expenditure. Our findings demonstrate that contribution of generic versions to expenditure containment is mostly derived from the enforced price reduction of originals entailed by entry of generics to the market [55, 56]. However, the real-world utilization data show almost no additional voluntary reduction of the list price for either biological originators or biosimilars after the imposed price cut, which limited the magnitude of expenditure savings through biosimilar use. The same was observed for small-molecule treatments. To facilitate further price competition and market uptake of generic drugs, more proactive policy measures are needed.

We also show that total spending for investigated products expands due to the increase in quantity used, despite the price reduction caused by biosimilar and generic entries to the market. This “balloon effect” [57] was particularly observed for infliximab and esomeprazole, which implies ineffectiveness of current price cuts for containment of total spending. At the same time, the increased utilization may imply that patients could access those drugs more easily due to the price reduction and wider choices as a result of the biosimilar or generic entry. WHO reported that approximately 30% of the global population still has difficulties accessing essential drugs for treatment, which could be alleviated by entry of generics to the market [58].

This study is built on the previous literature and advances it by assessing the market uptake of biosimilars and comparing it to that of generic small-molecule drugs over the medium term. Our findings would contribute to building global evidence on understanding market performances of biosimilars in terms of similarities and differences compared to traditional small-molecule drugs. However, our findings may not be generalizable to overall biosimilar products and the global market due to the limited number of biosimilars available in the current data. We confined our data 2012–2018, considering the drastic price cut imposed on all listed drugs in the national formulary in South Korea in April 2012. This restricted the observation periods of rituximab and trastuzumab to 2 years. We also note that DDDs of rituximab, trastuzumab, and imatinib were estimated based on their approved indications due to the lack of global measurement of DDD by the WHO. The focus of this study, however, was to investigate the time trend of utilization, and, thus, we could explore the market penetration properly as long as the same DDD definition was applied for both biological originators and corresponding biosimilars. Lastly, the observed differences in savings between small-molecule generics and biosimilars could vary depending on the selection of different small-molecule compounds as comparators. The pharmaceutical market depends on its therapeutic field, such as disease severity, epidemiology, and the availability of treatment options. Future studies need to consider and categorize the characteristics of markets and explore generalized patterns.

5 Conclusion

Biosimilars captured the market rapidly in the early stages and plateaued at a lower level than some generics in Korea. Simulation results of this study also showed significant cost savings due to the introduction of biosimilars; however, the level of saving was lower than that with generic drugs. Our findings imply that expansion of biosimilar use in the market and consequent expenditure savings need to be supported by pre-emptive policy measures to encourage price competition and boost utilization.

Data availability statement

Data are from the National Health Insurance Service, and the authors obtained the data after a confidentiality agreement for restrictive use of the data. Queries on the dataset and software codes should be directed to the corresponding author.

References

Organisation for Economic Co-operation and Development. Health at a Glance 2017. In: OECD Indicaors. OECD Publishing, Paris. 2017. https://www.oecd-ilibrary.org/social-issues-migration-health/health-at-a-glance-2017_health_glance-2017-en. Accessed 28 Jun 2019.

Belloni A, Morgan D, Paris V. Pharmaceutical expenditure and policies: past trends and future challenges. OECD Health Working Paper No. 87. Paris: Organisation for Economic Co-operation and Development; 2016.

Organisation for Economic Co-operation and Development. Pharmaceutical innovation and access to medicines. In: OECD Health Policy Studies. OECD Publishing, Paris. 2018. https://www.oecd-ilibrary.org/content/publication/9789264307391-en. Accessed 28 Jun 2019.

Araujo FC, Goncalves J, Fonseca JE. Pharmacoeconomics of biosimilars: what is there to gain from them? Curr Rheumatol Rep. 2016;18(8):50. https://doi.org/10.1007/s11926-016-0601-0.

Haustein R, de Millas C, Hoer A, Haussler B. Saving money in the European healthcare systems with biosimilars. Generics Biosimilars Initiative J. 2012;1(3–4):120–6.

Jha A, Upton A, Dunlop WC, Akehurst R. The Budget Impact of Biosimilar Infliximab (Remsima(R)) for the treatment of autoimmune diseases in five European countries. Adv Ther. 2015;32(8):742–56. https://doi.org/10.1007/s12325-015-0233-1.

Manova M, Savova A, Vasileva M, Terezova S, Kamusheva M, Grekova D, et al. Comparative price analysis of biological products for treatment of rheumatoid arthritis. Front Pharmacol. 2018;9:1070. https://doi.org/10.3389/fphar.2018.01070.

Mulcahy AW, Hlavka JP, Case SR. Biosimilar cost savings in the United States: initial experience and future potential. Rand Health Quart. 2018;7(4):3.

Fraeyman J, Van Hal G, De Loof H, Remmen R, De Meyer GR, Beutels P. Potential impact of policy regulation and generic competition on sales of cholesterol lowering medication, antidepressants and acid blocking agents in Belgium. Acta Clin Belg. 2012;67(3):160–71. https://doi.org/10.2143/ACB.67.3.2062650.

Luo J, Seeger JD, Donneyong M, Gagne JJ, Avorn J, Kesselheim AS. Effect of generic competition on atorvastatin prescribing and patients’ out-of-pocket spending. JAMA Intern Med. 2016;176(9):1317–23. https://doi.org/10.1001/jamainternmed.2016.3384.

Nador A, Pratt JL, Rix E. The Canadian Competition Bureau releases benefitting from generic drug competition in Canada: the way forward. Health Law Can. 2009;29(3):54–5.

Puig-Junoy J. Impact of European pharmaceutical price regulation on generic price competition: a review. Pharmacoeconomics. 2010;28(8):649–63. https://doi.org/10.2165/11535360-000000000-00000.

Sheingold S, Nguyen NX. Impacts of generic competition and benefit management practices on spending for prescription drugs: evidence from Medicare’s Part D benefit. Medicare Medicaid Res Rev. 2014. https://doi.org/10.5600/mmrr.004.01.a01.

Kim SC, Choi N-K, Lee J, Kwon K-E, Eddings W, Sung Y-K, et al. Utilization of the first biosimilar infliximab since its approval in South Korea. Arthritis Rheumatol. 2016;68(5):1076–9.

Jung Sowon, Lee Tae-Jin, Cho Byung-Hee. Market competition after patent exprity of original medicines. Korean J Health Econ Pol. 2008;14(2):1–25.

Bae G, Park C, Lee H, Han E, Kim D-S, Jang S. Effective policy initiatives to constrain lipid-lowering drug expenditure growth in South Korea. BMC Health Serv Res. 2014;14(1):100. https://doi.org/10.1186/1472-6963-14-100.

Son K-B, Bae S. Patterns of statin utilisation for new users and market dynamics in South Korea: a 13-year retrospective cohort study. BMJ Open. 2019;9(3):e026603. https://doi.org/10.1136/bmjopen-2018-026603.

Kwon H-Y, Yang B-M. Do generics really create savings on drug expenditures? Korean J Health Econ Pol. 2011;17(4):1–20.

Cesarec A, Likic R. Budget impact analysis of biosimilar trastuzumab for the treatment of breast cancer in Croatia. Appl Health Econ Health Pol. 2017;15(2):277–86. https://doi.org/10.1007/s40258-016-0285-7.

Gulacsi L, Brodszky V, Baji P, Rencz F, Pentek M. The rituximab biosimilar CT-P10 in rheumatology and cancer: a budget impact analysis in 28 European countries. Adv Ther. 2017;34(5):1128–44. https://doi.org/10.1007/s12325-017-0522-y.

Kanters TA, Stevanovic J, Huys I, Vulto AG, Simoens S. Adoption of biosimilar infliximab for rheumatoid arthritis, ankylosing spondylitis, and inflammatory bowel diseases in the EU5: a budget impact analysis using a Delphi panel. Front Pharmacol. 2017;8:322. https://doi.org/10.3389/fphar.2017.00322.

Araújo F. Biosimilar DMARDs: what does the future hold? Drugs (New York, NY). 2016;76(6):629–37. https://doi.org/10.1007/s40265-016-0556-5.

Brodszky V, Baji P, Balogh O, Péntek M. Budget impact analysis of biosimilar infliximab (CT-P13) for the treatment of rheumatoid arthritis in six Central and Eastern European countries. Eur J Health Econ. 2014;15(1):65–71. https://doi.org/10.1007/s10198-014-0595-3.

Whitehouse J. The cost saving potential of utilizing biosimilar medicines in biologic naive severe rheumatoid arthritis patients. Value Health. 2013. https://doi.org/10.1016/j.jval.2013.08.1547.

Sarpatwari A, Barenie R, Curfman G, Darrow J, Kesselheim AS. The US biosimilar market: stunted growth and possible reforms. Clin Pharmacol Ther. 2019;105(1):92–100.

Kim J, Ha D, Song I, Park H, Lee S-W, Lee E-K, et al. Estimation of cost savings between 2011 and 2014 attributed to infliximab biosimilar in the South Korean healthcare market: real-world evidence using a nationwide database. Int J Rheumatic Dis. 2018;21(6):1227–36.

Grabowski H, Guha R, Salgado M. Biosimilar competition: lessons from Europe. Berlin: Nature Publishing Group; 2014.

Schellekens H, Smolen JS, Dicato M, Rifkin RM. Safety and efficacy of biosimilars in oncology. Lancet Oncol. 2016;17(11):e502–9.

Candelaria M, Gonzalez D, Gómez FJF, Paravisini A, García ADC, Pérez L, et al. Comparative assessment of pharmacokinetics, and pharmacodynamics between RTXM83™, a rituximab biosimilar, and rituximab in diffuse large B-cell lymphoma patients: a population PK model approach. Cancer Chemother Pharmacol. 2018;81(3):515–27.

Verrill M, Declerck P, Loibl S, Lee J, Cortes J. The rise of oncology biosimilars: from process to promise. Future Oncol. 2019. https://doi.org/10.2217/fon-2019-0145.

Weaver AL, Lautzenheiser RL, Schiff MH, Gibofsky A, Perruquet JL, Luetkemeyer J, et al. Real-world effectiveness of select biologic and DMARD monotherapy and combination therapy in the treatment of rheumatoid arthritis: results from the RADIUS observational registry. Curr Med Res opin. 2006;22(1):185–98.

Kwon H-Y, Kim H, Godman B, Reich MR. The impact of South Korea’s new drug-pricing policy on market competition among off-patent drugs. Exp Rev Pharmacoecon Outcomes Res. 2015;15(6):1007–14. https://doi.org/10.1586/14737167.2015.1083425.

World Health Organization Collaborating Centre for Drug Statistics Methodology. Guidelines for ATC classification and DDD assignment 2019. Oslo, Norway; 2018.

Rovira J, Espin J, Garcia L, de Labry AO. The impact of biosimilars’ entry in the EU market. Andalusian School Public Health. 2011.

Remuzat C, Dorey J, Cristeau O, Ionescu D, Radiere G, Toumi M. Key drivers for market penetration of biosimilars in Europe. J Market Access Health Pol. 2017;5(1):1272308.

Morton FMS, Stern AD, Stern S. The impact of the entry of biosimilars: evidence from Europe. Rev Ind Organ. 2016;53:173–210. https://doi.org/10.1007/s11151-018-9630-3.

de Lemos ML, Kyritsis V. Clinical efficacy of generic imatinib. J Oncol Pharm Pract. 2015;21(1):76–9.

Canada CMLSo. Generic tyrosine kinase inhibitors (TKIs) arrive in Canada. Chronic Myelogenous Leukemia Society of Canada. 2014. http://cmlsociety.org/generic-tyrosine-kinase-inhibitors-tkis-arrive-in-canada/. Accessed 29 Apr 2019.

International G-GS. Generic Gleevec. GIS-GIST Support International. 2013. http://gistsupport.medshelf.org/Generic_Gleevec. Accessed 29 Apr 2019.

Goubran HA. Failure of a non-authorized copy product to maintain response achieved with imatinib in a patient with chronic phase chronic myeloid leukemia: a case report. J Med Case Rep. 2009;3(1):7112. https://doi.org/10.1186/1752-1947-3-7112.

Cole AL, Dusetzina SB. Generic price competition for specialty drugs: too little, too late? Health Aff (Millwood). 2018;37(5):738–42. https://doi.org/10.1377/hlthaff.2017.1684.

van de Vooren K, Curto A, Garattini L. Biosimilar versus generic drugs: same but different? Appl Health Econ Health Pol. 2015;13:125–7. https://doi.org/10.1007/s40258-015-0154-9.

Sullivan E, Piercy J, Waller J, Black CM, Kachroo S. Assessing gastroenterologist and patient acceptance of biosimilars in ulcerative colitis and Crohn’s disease across Germany. PLoS One. 2017;12(4):e0175826. https://doi.org/10.1371/journal.pone.0175826.

Waller J, Sullivan E, Piercy J, Black CM, Kachroo S. Assessing physician and patient acceptance of infliximab biosimilars in rheumatoid arthritis, ankylosing spondyloarthritis and psoriatic arthritis across Germany. Patient Preference Adherence. 2017;11:519.

Berndt ER, Aitken ML. Brand loyalty, generic entry and price competition in pharmaceuticals in the quarter century after the 1984 Waxman–Hatch legislation. Int J Econ Business. 2011;18(2):177–201.

Kurki P, van Aerts L, Wolff-Holz E, Giezen T, Skibeli V, Weise M. Interchangeability of biosimilars: a European perspective. BioDrugs. 2017;31(2):83–91.

O’Callaghan J, Barry SP, Bermingham M, Morris JM, Griffin BT. Regulation of biosimilar medicines and current perspectives on interchangeability and policy. Eur J Clin Pharmacol. 2019;75(1):1–11.

Cohen H, Beydoun D, Chien D, Lessor T, McCabe D, Muenzberg M, et al. Awareness, knowledge, and perceptions of biosimilars among specialty physicians. Adv Ther. 2016;33(12):2160–72.

Menditto E, Orlando V, Coretti S, Putignano D, Fiorentino D, Ruggeri M. Doctors commitment and long-term effectiveness for cost containment policies: lesson learned from biosimilar drugs. ClinicoEcon Outcomes Res. 2015;7:575–81. https://doi.org/10.2147/CEOR.S88531.

Blackstone EA, Joseph PF. The economics of biosimilars. Am Health Drug Benefits. 2013;6(8):469–78.

Crommelin D, Bermejo T, Bissig M, Damiaans J, Kramer I, Rambourg P. Pharmaceutical evaluation of biosimilars: important differences from generic low-molecular-weight pharmaceuticals. Eur J Hosp Pharm Sci. 2005;11(1):11–7.

Garattini L, Curto A, van de Vooren K. Western European markets for biosimilar and generic drugs: worth differentiating. Eur J Health Econ. 2015;16:683–7. https://doi.org/10.1007/s10198-015-0684-y.

Health Insurance Review and Assessment Service. Statistics for Pharmaceutical Reimbursement Claims. In: Statistics for Pharmaceutical Reimbursement Claims by Utilization Type. Health Insurance Review and Assessment Service, Wonju. 2018. http://kosis.kr/common/meta_onedepth.jsp?vwcd=MT_OTITLE&listid=354_354004. Accessed 2 Oct 2019.

Aladul MI, Fitzpatrick RW, Chapman SR. Patients’ understanding and attitudes towards infliximab and etanercept biosimilars: result of a UK web-based survey. BioDrugs. 2017;31(5):439–46. https://doi.org/10.1007/s40259-017-0238-1.

Yazdany J, Dudley RA, Lin GA, Chen R, Tseng CW. Out-of-pocket costs for infliximab and its biosimilar for rheumatoid arthritis under medicare part D. JAMA. 2018;320(9):931–3. https://doi.org/10.1001/jama.2018.7316.

Mestre-Ferrandiz J, Towse A, Berdud M. Biosimilars: how can payers get long-term savings? Pharmacoeconomics. 2016;34(6):609–16.

Mrazek M. Comparative approaches to pharmaceutical price regulation in the European Union. Croatian Med J. 2002;43(4):453–61.

Brems Y, Seville J, Baeyens J. The expanding world market of generic pharmaceuticals. J Generic Med. 2011;8(4):227–39.

Woori Bank. Average exchange rate by period. Seoul. 2018. https://spot.wooribank.com/pot/Dream?withyou=FXXRT0016. Accessed 10 Dec 2019.

Author information

Authors and Affiliations

Contributions

EH and HJL conceived the study. HJL performed data cleaning and analyses and EH verified the analytical methods. HK performed the literature review. EH and HJL drafted the manuscript. All authors discussed the results and commented on the manuscript.

Corresponding author

Ethics declarations

Conflict of interest

Research support from the Korea National Research Foundation [Grant number 2019R1A2C1003259] is gratefully acknowledged. The content is solely the responsibility of the authors and does not necessarily represent the official view of the Korea National Research Foundation. The Korea National Research Foundation had no involvement in preparation and submission of this manuscript. The authors declare that they have no competing interests.

Rights and permissions

About this article

Cite this article

Lee, HJ., Han, E. & Kim, H. Comparison of Utilization Trends between Biosimilars and Generics: Lessons from the Nationwide Claims Data in South Korea. Appl Health Econ Health Policy 18, 557–566 (2020). https://doi.org/10.1007/s40258-019-00547-7

Published:

Issue Date:

DOI: https://doi.org/10.1007/s40258-019-00547-7