Abstract

Background There is over 10 years of clinical experience and evidence to show that biosimilar medicines can be used as safely and effectively in approved therapeutic indications as their originator biological medicines. In Ireland, biosimilar medicine uptake has been very slow, and savings to the health service will only be realised through fostering a competitive biological medicine market. Objective The objective of this study was to investigate the utilisation of biosimilars following a ‘best-value biological’ medicine initiative for adalimumab and etanercept in the Irish healthcare setting. Methods Data was extracted from the National High Tech claims database and High Tech ordering and management hub for the following drugs; adalimumab (Humira®, Amgevita®, Hulio®, Idacio®, and Imraldi®) and etanercept (Enbrel® and Benepali®). Main outcome measure: uptake of the best-value biological medicines. Results In June 2019, just over 90 patients had been initiated on, or switched to a best-value biological for adalimumab or etanercept. Over the next 12 months this increased to over 8500 patients. With the best-value biologicals accounting for approximately 50 % of market share in June 2020, the combined estimated savings and avoided costs are €22.7 million to date. The gain-share prescribing incentive has raised over €3.6 million for the specialties to invest back into patient care. Conclusion Against the background of a finite healthcare budget, this study shows that increasing use of biosimilars can create the financial savings and space to invest in new innovative therapies for the benefit of many patients.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Impacts on practice

-

The ‘best-value biologic’ initiative incentivises clinicians to prescribe biosimilars for adalimumab and etanercept, as opposed to their originator medicines.

-

This initiative has been successful, and has resulted in savings of €22 million to date, thus allowing space for investing in new therapies within the clinical specialty.

.

Introduction

In Ireland ‘High Tech’ medicines are usually prescribed and initiated in the hospital setting and include agents such as antineoplastic and immunomodulatory drugs, anti-infectives for systemic use and modulatory drugs for the treatment of cystic fibrosis. These drugs are expensive and although they represent just 1% of the 77.5 million prescription items dispensed in Ireland each year they account for approximately one third of total drug expenditure, exceeding €800 million per annum in 2018 [1]. Biological medicines containing tumour necrosis factor-alpha (TNF-α) inhibitors are the highest expenditure category on the High Tech (HT) Drug Arrangement, accounting for approximately €224 million in 2018 with adalimumab (Humira®) and etanercept (Enbrel®) making up over 86 % of this expenditure. TNF-α inhibitors are licensed for the treatment of a variety of inflammatory conditions including rheumatoid arthritis, psoriatic arthritis, juvenile idiopathic arthritis, inflammatory bowel disease, axial spondyloarthritis and plaque psoriasis. Therefore, they are predominantly used in the clinical specialties of dermatology, gastroenterology and rheumatology.

A biosimilar medicine (biosimilar) is defined as a biological medicine that contains a version of the active substance of an already authorised biologic (known as the reference biologic). This means that the candidate biosimilar must establish similarity to the key characteristics of the molecular and biological activity of the reference product and will be expected to have similar clinical outcomes in terms of safety and efficacy [2]. The availability of biosimilars for Humira® and Enbrel® was seen as an opportunity to significantly reduce expenditure on TNF-α inhibitors (since 2010, expenditure on Humira® and Enbrel® has exceeded € 1.3 billion), thereby enabling the funding of other new innovative medicines.

However, reducing expenditure is dependent on the uptake of biosimilars and whilst the etanercept biosimilar, Benepali® has been available in Ireland since September 2016 its uptake was negligible in the first 2 years, accounting for under 2% of the etanercept market share. This very low uptake of Benepali® and the availability of biosimilar products for adalimumab prompted the Health Service Executive-Medicines Management Programme (HSE-MMP) to publish its roadmap for the prescribing of best-value biological (BVB) medicines in December 2018 [3]. The MMP indicated that it would be issuing prescribing and cost guidance for relevant therapeutic areas, prescriber and patient support materials in addition to the identification of what it considered the BVB medicine(s).

The TNF-α inhibitors BVB initiative commenced in January 2019 after the MMP highlighted the criteria that would be considered when identifying the best-value agents. Manufacturers were invited to submit documentation in accordance with the criteria to support their application for BVB medicine status. The MMP published its recommendations in May 2019 indicating that Imraldi® and Amgevita® (should clinicians wish to prescribe a citrate-free formulation) were the BVBs for adalimumab and Benepali® for etanercept [4]. Another important development was the introduction of a gain-share incentive on the 1st June 2019 which offered the relevant clinical service €500 for each patient initiated on, or switched to a BVB medicine. This funding can be invested to further enhance service delivery for patients.

Aim of the study

The aim of this study was to outline the impact of the MMP BVB initiative in enhancing the uptake of biosimilars for adalimumab and etanercept in the Irish healthcare setting.

Ethics approval

As the pharmacy claims data used in this study was anonymised, ethical approval was not required in order to comply with ethical standards.

Methods

The HT Drug Arrangement is administered by the HSE through the Primary Care Eligibility Reimbursement Service (HSE-PCERS). HT medicines are purchased by the HSE and supplied through community pharmacies for which pharmacists are paid a patient care fee by the HSE-PCERS, with the cost of the medicines being paid by the HSE-PCERS directly to the manufacturer or wholesaler. Information on the number of HT prescriptions dispensed and number of individual patients is collected in the HT claims database therefore the data included in this study is representative of the Irish population.

The prescribing of biological medicines is monitored through the HT medicines ordering and management hub (HTH) introduced in December 2017. This HTH enables prescribers to register patients for HT medicines and generate prescriptions for those patients. The HTH collects data on the number of patients commenced on/switched to a BVB medicine, the number of BVBs prescribed according to specialty, the gain-share earned and this enabled the estimated savings from the HSE-MMP BVB initiative to be calculated since its introduction on the 1st June 2019.

Data was extracted from the HT claims database and HTH for the following drugs; adalimumab (Humira®, Imraldi®, Amgevita®, Hulio® and Idacio®) and etanercept (Benepali® and Enbrel®). We investigated:

-

1.

the utilisation of originator and biosimilar adalimumab and etanercept in terms of number of prescriptions and number of patients.

-

2.

estimates of State expenditure on biosimilar adalimumab and etanercept and potential cost-savings and avoided costs associated with the BVB initiative.

The quantity of biosimilar adalimumab and etanercept (i.e. number of pre-filled pens and syringes) that was supplied to patients for each of the BVB medicines since the 1st June 2019 was extracted from the HT claims database. The difference in cost between originator and biosimilar adalimumab and etanercept was calculated. The difference in cost was then multiplied by the quantity of biosimilar adalimumab and etanercept supplied to patients to obtain the estimated savings to date from the BVB medicine initiative. It should be noted that the estimated savings includes both savings realised from switching patients from originator to biosimilar adalimumab and etanercept, and avoided costs in patients who are commenced treatment on biosimilar adalimumab and etanercept, as opposed to the originator.

Results

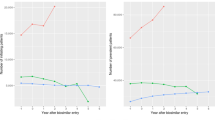

In May 2019, prior to the introduction of the TNF-α inhibitor BVB initiative, 8163 people were being treated with Humira® and 166 patients with an adalimumab biosimilar. In May 2019, 4208 people were being treated with Enbrel® and just 104 patients with an etanercept biosimilar. Twelve months after the introduction of the TNF-α inhibitor BVB initiative, in May 2020, over 3400 people were being treated with an adalimumab BVB, and over 1800 people being treated with an etanercept BVB. By July 2020, over 8500 patients were prescribed an adalimumab or etanercept BVB (Fig. 1). The highest prescribing of BVBs per specialty was in rheumatology (74%) followed by gastroenterology (14%) and dermatology (12%).

The number of patients with an adalimumab or etanercept BVB prescription generated, according to the HTH

The fall in the number of patients being treated with the originator products Humira® and Enbrel® in addition to the increase in the number of patients on their biosimilars is shown in Fig. 2. With the BVBs now accounting for approximately 50% of market share, the estimated savings are €22.7 million to date. The gain-share has raised over €3.6 million for the specialties to invest back into patient care.

The number of patients receiving adalimumab or etanercept, by product. Note there is currently no biosimilar of Enbrel® solution for injection in a vial and patients receiving this product are not shown in this graph

Discussion

The availability of biosimilars for adalimumab in 2018 provided the impetus to enhance biosimilar uptake as expenditure on Humira® had reached over €137 million per annum at that time. The poor uptake of Benepali®, the biosimilar for etanercept, which had been available since September 2016 highlighted the task ahead of the HSE-MMP. The publication of the MMP roadmap in December 2018 was the first step in the process outlining the criteria for the identification of BVB medicines. The criteria included drug acquisition cost, therapeutic indications, product range including pack sizes and strengths available, product stability including storage requirements, administration devices, patient factors including patient support programmes, clinical guidelines, ability to supply the Irish market in addition to expenditure in the therapeutic area and the potential for savings. This culminated in the identification of the two adalimumab biosimilars (Imraldi® and Amgevita®) in addition to Benepali® as an alternative to Enbrel®. This process included communication with clinicians particularly through the clinical programmes in dermatology, gastroenterology and rheumatology as these represent the main prescribers. The MMP published prescribing and cost guidance in addition to patient support materials [5]. In conjunction with the HSE-PCERS, it also provided prescribers with information in relation to the BVB medicines and on the registration and prescribing using the HTH, which was another key component to facilitating the prescribing and monitoring of biosimilars; this included undertaking site visits nationally to engage with clinical teams at their place of work. The support of the clinical programmes for the BVB initiative has been pivotal to its success.

The introduction of the prescribing incentive in the form of a gain-share of €500 per patient initiated or switched to one of the BVBs was also an important contributor to the significant increase in biosimilar use. Financial incentives may certainly impact on prescribing behaviour but success can depend on clarity of purpose and aligning incentives with professional values [6]. In this case the BVB initiative promoted safe, effective and cost-effective prescribing in addition to providing much needed investment for the specialties involved. This is not the first example of a prescribing incentive scheme in Ireland as the Indicative Drug Target Savings Scheme (IDTSS), introduced in 1993, provided for the use of savings derived from projected prescribing targets to further general practice infrastructure on the basis that 50% of the savings would be made available to the individual prescriber for investment in specific practice developments [7]. The IDTSS was successful in enhancing the use of generic medicines and providing savings for investment in general practice. The BVB gain-share incentive has also been successful in ensuring significant uptake of low-cost, equally efficacious alternatives to Humira® and Enbrel®.

Further developments that enhanced BVB uptake in the first year included the addition of two more adalimumab biosimilar products (Hulio® and Idacio®) to the BVB medicine list in January 2020 as they satisfied the criteria outlined above. In addition, the HSE announced a policy change which was introduced on the 1st February 2020. This confirmed that reimbursement of adalimumab and etanercept under the High Tech Arrangement would only be supported for the BVB medicines in adult patients commencing such therapy. This is operationalised through the HTH; should prescribers wish to use the originator product a case needs to be made to the MMP outlining why the originator should be used in preference to the BVB, very few applications have been made to date.

In Ireland the cost-effectiveness of all medications is considered prior to reimbursement. This is a two stage process, conducted by the National Centre for Pharmacoeconomics (NCPE) which involves a rapid review of the particular product which is completed in 4–6 weeks and is followed by a full Health Technology Assessment (HTA) where necessary [8]. Of course, drug acquisition cost is an important consideration; the introduction of biosimilar versions of adalimumab in Denmark resulted in a reduction of costs of approximately 80%, with the National Health Service in the United Kingdom achieving a four-fold reduction in costs [9, 10]. A similar reduction in costs would be expected in Ireland, and therefore a full HTA of the BVBs is not required. As biosimilars do not have to undergo a formal cost-effectiveness assessment they can readily access the market.

The biosimilar market in Europe is the largest worldwide and many policy recommendations have been adopted to increase biosimilar uptake [11]. A review of 20 EU Member States plus Iceland, Norway, Russia and Serbia demonstrated that approximately half had incentives targeting physicians to prescribe biosimilars. These included supplementary remuneration for French physicians, a prescribing rate of at least 20% for treatment naïve patients in Belgium and biosimilar quotas with regionally negotiated targets in Germany [12]. Most countries in the review discuss budgetary restrictions as playing a role in policy changes encouraging biosimilar prescribing. Experience from Denmark demonstrates the impact a well-planned biosimilar implementation strategy can have. Treatment recommendations from the Danish Medicines Council that adalimumab biosimilars should be used for all indications following patent expiration of the adalimumab originator (Humira®) had an immediate impact. The recommendations included the switching of patients from the originator to the biosimilars resulting in the proportion of biosimilars increasing to over 95% and a reduction in expenditure exceeding 82% in just 2 months [9]. The Danish model for the rapid and safe implementation of infliximab and etanercept biosimilars has also been successful [13].

In Ireland there will likely be a focus on interchangeability and the switching of patients from reference biologics to biosimilars. In our study over 4300 patients successfully switched therapy from the reference biologic (Humira® or Enbrel®) to the BVBs, in keeping with the literature which reports safety and efficacy associated with switching [14, 15]. This is consistent with the view of the Health Products Regulatory Authority (HPRA) in Ireland who consider that biosimilars can be used interchangeably with the reference product or with other biosimilar medicines of that reference product, under supervision of a physician [16]. Whether we see the introduction of automatic substitution remains to be seen, as this is currently prohibited under Irish legislation [17]. The uptake of biosimilars for agents such as infliximab in the hospital setting in Ireland has been published and highlighted the significant time lag between regulatory approval and clinical acceptance [18].

There are several limitations to this study; the data available to us did not include patient characteristics, such as age and gender. Further, the database does not include any efficacy, outcomes or indication data. However, to our knowledge, this is the first study to describe the nationwide uptake and expenditure associated with BVB initiative in Ireland.

Conclusions

The BVB initiative outlined here has been focused on the community setting to date and in view of the significant uptake of biosimilars for the TNF-α inhibitors, it will likely serve as a template for the future, particularly in view of the increasing number of biosimilar approvals in Europe [19]. Against the background of a finite healthcare budget the increasing use of biosimilars could create the financial space to enable us to invest in new innovative therapies for the benefit of many patients.

Availability of data and material

The data that support the findings of this study are available from the HSE-PCRS but restrictions apply to the availability of these data, which were used under licence for the current study, and so are not publicly available.

Code availability

Data analyses were carried out using custom code (SAS® 9.4) and Microsoft Excel.

References

PCRS—reporting menu. https://www.sspcrs.ie/portal/annual-reporting/report/annual. Accessed 06 Aug 2020.

NMIC. NMICB December 2015—update on biosimilar medicines.pdf. http://www.stjames.ie/GPsHealthcareProfessionals/Newsletters/NMICBulletins/NMICBulletins2015/NMIC%20Bulletin%20December%202015 %20-%20Update%20on%20Biosimilar%20Medicines.pdf. Accessed 06 Aug 2020.

MMP. MMP roadmap for the prescribing of best-value biological (BVB) medicines in the Irish healthcare setting. https://www.hse.ie/eng/about/who/cspd/ncps/medicines-management/best-value-biological-medicines/mmp-roadmap-for-the-prescribing-of-best-value-biological-bvb-medicines-in-the-irish-healthcare-setting.pdf. Accessed 06 Aug 2020.

MMP. Best-value biological medicines: tumour necrosis factor-α inhibitors on the high tech drug scheme. https://www.hse.ie/eng/about/who/cspd/ncps/medicines-management/best-value-biological-medicines/mmp%20report%20bvb%20medicines%20tnf%20alpha%20 inhibitors%20may%202019.pdf. Accessed 06 Aug 2020.

MMP. Best-value biological medicines—Medicines Management Programme. HSE.ie. https://www.hse.ie/eng/about/who/cspd/ncps/medicines-management/best-value-biological-medicines/best-value-biological-medicines.html. Accessed 06 Aug 2020.

Roland M, Campbell S. Successes and failures of pay for performance in the United Kingdom. N Engl J Med. 2014;370(20):1944–9. https://doi.org/10.1056/NEJMhpr1316051.

Walley T, Murphy M, Codd M, Johnston Z, Quirke T. Effects of a monetary incentive on primary care prescribing in Ireland: changes in prescribing patterns in one health board 1990–1995. Pharmacoepidemiol Drug Saf. 2000;9(7):591–8. https://doi.org/10.1002/pds.544.

McCullagh L, Barry M. The pharmacoeconomic evaluation process in Ireland. Pharmacoeconomics. 2016;34(12):1267–76. https://doi.org/10.1007/s40273-016-0437-5.

Jensen TB, Kim SC, Jimenez-Solem E, Bartels D, Christensen HR, Andersen JT. Shift from adalimumab originator to biosimilars in Denmark. JAMA Intern Med. 2020. https://doi.org/10.1001/jamainternmed.2020.0338.

England NHS. NHS England » NHS set to save record £300 million on the NHS’s highest drug spend. https://www.england.nhs.uk/2018/11/nhs-set-to-save-record-300-million-on-the-nhss-highest-drug-spend/. Accessed 06 Aug 2020.

Moorkens E, Vulto AG, Huys I, Dylst P, Godman B, Keuerleber S, et al. Policies for biosimilar uptake in Europe: an overview. PLoS ONE. 2017;12(12):e0190147. https://doi.org/10.1371/journal.pone.0190147.

Policy recommendations for a sustainable. biosimilars market: lessons from Europe—GaBI Journal. http://gabi-journal.net/policy-recommendations-for-a-sustainable-biosimilars-market-lessons-from-europe.html. Accessed 06 Aug 2020.

Jensen TB, Bartels D, Sædder EA, Poulsen BK, Andersen SE, Christensen MM, et al. The Danish model for the quick and safe implementation of infliximab and etanercept biosimilars. Eur J Clin Pharmacol. 2020;76(1):35–40. https://doi.org/10.1007/s00228-019-02765-3.

Jørgensen KK, Olsen IC, Goll GL, Lorentzen M, Bolstad N, Haavardsholm EA, et al. Switching from originator infliximab to biosimilar CT-P13 compared with maintained treatment with originator infliximab (NOR-SWITCH): a 52-week, randomised, double-blind, non-inferiority trial. Lancet. 10 2017;389(10086):2304–16. https://doi.org/10.1016/S0140-6736(17)30068-5.

Glintborg B, Loft AG, Omerovic E, Hendricks O, Linauskas A, Espesen J, et al. To switch or not to switch: results of a nationwide guideline of mandatory switching from originator to biosimilar etanercept. One-year treatment outcomes in 2061 patients with inflammatory arthritis from the DANBIO registry. Ann Rheum Dis. 2019;78(2):192–200. https://doi.org/10.1136/annrheumdis-2018-213474.

HPRA. Guide to biosimilars for healthcare professionals. http://www.hpra.ie/homepage/about-us/publications-forms/guidance-documents/item?id=e6d50326-9782-6eee-9b55-ff00008c97d0&t=/docs/default-source/publications-forms/guidance-documents/guide-to-biosimilars-for-healthcare-professionals-v3. Accessed 06 Aug 2020.

Electronic I. S. Book (eISB). Electronic Irish statute book (eISB). http://www.irishstatutebook.ie/eli/2013/act/14/enacted/en/html. Accessed 06 Aug 2020.

Biosimilar infliximab introduction into the gastroenterology care pathway in a large acute Irish teaching hospital: a story behind the evidence—GaBI Journal. http://gabi-journal.net/biosimilar-infliximab-introduction-into-the-gastroenterology-care-pathway-in-a-large-acute-irish-teaching-hospital-a-story-behind-the-evidence.html. Accessed 06 Aug 2020.

Top developments in biosimilars during 2019—GaBI Journal. http://gabi-journal.net/top-developments-in-biosimilars-during-2019.html. Accessed 06 Aug 2020.

Acknowledgements

We would like to acknowledge the HSE-PCRS for facilitating access to the data.

Funding

No specific funding was received for this research.

Conflicts of interest

The authors declare that they have no conflict of interest.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher’s note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

About this article

Cite this article

Duggan, B., Smith, A. & Barry, M. Uptake of biosimilars for TNF-α inhibitors adalimumab and etanercept following the best-value biological medicine initiative in Ireland. Int J Clin Pharm 43, 1251–1256 (2021). https://doi.org/10.1007/s11096-021-01243-0

Received:

Revised:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11096-021-01243-0