Abstract

Portfolio optimization encompasses the optimal assignment of limited capital to different available financial assets to achieve a reasonable trade-off between profit and risk. This paper focuses on a portfolio selection model with interval-typed random parameters considering risk measures as value-at-risk (VaR). The value-at-risk is expressed by means of the interval-typed of random parameters and associated with Markowitz’s model. The purpose of this opinion is to design an interval mean-VaR portfolio optimization model with the objective of minimization of VaR. A methodology is developed to obtain an efficient investment strategy using interval analysis with the parametric representation of the interval. The theoretical developments are illustrated based on a historical data set taken from the National Stock Exchange, India.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

The portfolio optimization aims to find the best option among all the alternatives for the investors. For this, Markowitz [55] initiated the portfolio optimization (known as mean-variance \((\mathbf{MV})\) model), which consists of picking the best stock either one to maximize the future return for a fixed risk or minimize variance for a fixed return. The fundamental idea behind the mean-variance model is that the portfolio’s expected return is considered the investment return, and the variance of the portfolio return is used as a risk measure. Thereafter, several portfolio selection methodologies are established considering other parameters related to the financial market (such as different types of risks [53], transaction costs [8, 9, 46], liquidity [22, 66], etc.), which also affect the portfolio selection process. Due to the mean-variance model’s computational difficulty, somewhat different methods have been proposed, particularly to characterize risk measures for assets’ return. For example, the mean absolute deviation risk measure [35, 36], semi absolute deviation [62, 63], semi-variance risk measure [54], minimax risk measure [14] and the VaR [6, 17, 18, 25].However, the VaR measure disregards the loss beyond VaR and contempt the existence of subadditivity and convexity [3]. Moreover, asset selection and allocation of total investment with a VaR measure is computationally difficult [21]. Nevertheless, VaR has become an essential measure of risk for a securities portfolio among various financial markets’ risk measures. At present, it has become a vital tool for risk management and part of automated regulatory mechanisms in the financial industry. Therefore, a considerable number of researchers have been studied in recent years about the development of a portfolio optimization model based on the concept of VaR, such as [7, 15, 19, 23, 59, 61], etc. Some research work is briefly described further. A methodology to obtain optimal investment strategies is introduced by Campbell et al. [15] for the maximizing expected return of portfolio subject to a downside risk constraint rather than standard deviation alone. In addition, Alexander and Baptista [1, 2] examined the mean-VaR model’s economic implications for portfolio selection by making connections of value-at-risk with mean-variance analysis and showed that higher variance portfolios might have lower VaR. Gaivoronski and Pflug [23] presented a technique for calculating efficient portfolios, which provides the minimum VaR for a specified expected return. They have also found that resulting efficient frontiers are relatively different from mean-variance efficient frontier. Mansini et al. [52] have studied linear programming problem based mean-conditional value at risk portfolio selection model. Considering the more realistic factor of a financial market with downside risk measure, Baixauli-Soler et al. [5] and Babazadeh and Esfahanipour [4] have formulated the mean-VaR model introducing the minimum transaction cost, non-linear cost structure, etc., as constraints, and proposed a solution technique based on the multi-objective genetic algorithm. Many fuzzy portfolio selection models[10, 34, 51, 58] are formulated too in different aspects in which the parameters (such as expected return, variance, VaR, entropy, etc.) of it are assumed either as fuzzy triangular numbers or as fuzzy trapezoidal number. Although Lwin et al. [50] proposed an efficient learning hybrid evolutionary algorithm to solve the mean-VaR portfolio optimization problem with realistic constraints such as cardinality, quantity, pre-assignment, round-lot, and class constraints.

Due to the incomplete information provided by the financial market and human subjective judgments, the uncertain return rates are often problematic to present precisely. Therefore, to describe and analyze such types of uncertainties in some parameters of the existing portfolio optimization models (as given in the above-mentioned articles) such as expected returns, risk, liquidity, etc., probability theory or fuzzy set theory or possibility theory, etc., are generally used. For which, the distribution function or membership function or possibility distribution is to be assumed in advance [57]. In reality, it is too complicated to categorize such functions. However, an investor can easily state these parameters in the form of an interval whose lower and upper bound can be found either from historical data or based on the expert’s knowledge. As a result, a portfolio optimization problem becomes an interval optimization problem and can be dealt using interval analysis. In the previous two decades, many researchers [28, 29, 31, 37, 43, 57] have used the closed interval to describe and analyze uncertain parameters of the portfolio optimization problem. In this perspective, quite a lot of portfolio selection models associated with interval parameters have been developed such as [16, 24, 30, 33, 38, 43, 45], etc. An interval portfolio selection model [43, 60] has established and developed a methodology based on partial order relationship to obtain an efficient portfolio as a linear interval programming problem. Ida [30] considered the returns’ variances, covariances and the expected return of assets as interval and has proposed a mean-variance model in the form of multi-objective programming problem using interval uncertainty. Giove et al. [24] have applied the minimax regret approach based on a regret function to find an efficient solution for portfolio optimization model with interval parameters. A possibilistic portfolio selection model is established by Li and Xu [45], in which the expected rates of return of assets are treated as fuzzy or possibilistic variables. To express these parameters, they used closed intervals and converted the portfolio selection model into a nonlinear goal programming problem. They also obtained a satisfactory solution using a genetic algorithm. Furthermore, considering the mean-absolute deviation risk measure, Liu [47] introduced a portfolio selection model in which an interval represents the return of assets. In the same way, Tan [64] developed a portfolio selection model with interval parameters by taking into consideration of liquidity as a constraint in the mean-variance model. However, Wu et al. [65] have obtained a non-inferior solution of an interval portfolio selection model that improves and generalizes Markowitz’s \(\mathbf{MV}\) model. A portfolio rebalancing model is presented by Kumar et al. [39], where the parameters such as return of assets, the covariance of returns, and transaction costs are in the form of intervals. Bhurjee et al. [11, 13] formulated an optimal Sharp ratio model as an interval fractional programming problem and found the bound of the objective function. The multiperiod portfolio selection problem with parameters (such as returns, risk, liquidity, etc.) of securities in terms of intervals is proposed by [48, 49, 56, 67, 68]. Li and Jin [44] established a portfolio optimization model associated with interval number and interval type random variable, where the probabilistic risk measure is flexible for investors with different risk tolerance. Kumar et al. [40, 41] have formulated single and multiple objective portfolio selection models with interval parameters and interval decision variables, respectively. A stochastic technique is proposed by Kumar et al. [42] to solve the portfolio selection problem with minimax risk measure and bounded parameters. Recently, a multi-objective interval portfolio selection is developed based on investment decisions under different risk assumptions in [27]. One can observe from the above mentioned brief literature review of the portfolio optimization model with interval parameters that the majority of the models focus either on addressing semi-absolute deviation or variance as a risk measure, only a few focus on minimax risk measures. It is also seen that in the current scenario, downside risk measure as value at risk is receiving more attention from researchers, market analysts, and the financial institution. However, no one has described and analyzed VaR in the portfolio selection associating with the interval parameters in the model.

The accurate prediction of VaR is a crucial task in applied financial risk management. Even though significant progress has been documented in the financial econometrics field of study over the last decades, these approaches are not applicable in the financial industry due to the complexity that such approaches involve. Traditionally, the value of VaR is presumed to be a real number. However, this value is not necessarily estimated precisely because of ambiguity in the data set due to human error, complexity in the environment, a limited numerical representation capability of digital computers, etc. For example, most of VaR’s rational value (for any confidence level) as 1/3, 1.67839, 2.20347, etc., have infinite digits in their decimal representation computer work with rounded floating-point numbers. Algebraic operations on floating points numbers might be accumulated errors that may be significant. A way to work with this type of error is to understand real-interval spaces better [20]. In the literature, it is observed that VaR’s value also depends on the information about the expected return of the portfolio. Expected returns are usually estimated using given periods of recorded returns of all the assets; the data fluctuations might be altered due to some influences such as time and external environment. Such influences are too complicated to be appropriately described. Therefore, one may use interval numbers to represent these uncertain parameters (see [57]) to successfully overcome the ambiguity mentioned above in the data set.

In view of the facts mentioned above, motivated to fill this void in the portfolio optimization problem, in this paper,

-

a portfolio optimization model with bounded parameters is dealt with by introducing the risk measure as VaR using an interval-typed random rate of assets return. The VaR is here allied with the \(\mathbf{MV}\) analysis, and a portfolio optimization model with interval parameters is formulated, namely the interval mean-VaR model.

-

The proposed model sets up as an interval non-linear programming problem, where the objective function is to minimize the portfolio’s VaR for a specified level of return of total investments. A methodology is developed with the help of interval optimization using the parametric definition of the interval and obtained efficient investment strategy by transforming the primary model into an equivalent deterministic model.

-

Empirical results based on the historical data set taken from National Stock Exchange, India demonstrate that the quality of the suggested approach’s solutions is better than that of the existing other models.

The rest of the paper is planned as follows: we present preliminary of interval analysis and introduction of interval- typed random variable in Sect. 2. In Sect. 3, VaR is formulated by making connections with \(\mathbf{MV}\) analysis and designed the mean-VaR model using an interval form of the parameters. A solution methodology is also developed in this section with its existence. Section 4 presents a numerical analysis based on a case study using the data from the National Stock Exchange, India. Finally, concluding remarks is given in Sect. 5.

2 Preliminary

The basic concepts and properties of interval analysis are presented in this section.

-

A closed interval \({\mathbf {A}}\) with lower bound \((a^L)\) and upper bound \((a^U)\) is denoted by bold capital letter (\({\mathbf {A}}\)) and represented by \({\mathbf {A}}=[a^L,a^U]\) i.e. \(a^L\le a^U\). If \(a^L= a^U\), then \({\mathbf {A}}\) is called degenerate interval. The set of all closed intervals on \(\mathbb {R}\) is denoted by \(\mathbb {I(R)}\). A closed interval is said to be non-negative if \(a^L\ge 0\).

-

An interval can also be expressed in terms of a parameter in several ways. Any point in \({\mathbf {A}}\) may be expressed as \(a_t\), where \(a_t=a^L+t(a^U-a^L),t\in [0,1].\) Throughout this paper, a specific parametric representation of an interval is considered as \({\mathbf {A}}=[a^L,a^U]=\{a_t\mid t\in [0,1]\}.\)

-

\((\mathbb {I(R)})^k\)= The product space \(\underbrace{\mathbb {I(R)}\times \mathbb {I(R)}\times \cdots \times \mathbb {I(R)}}_{k ~{\text{ times }}}\).

-

\({\mathbf {C}}_v^k\in (\mathbb {I(R)})^k\) represents interval vectors of \(k-\)dimesinional i.e., \({\mathbf {C}}_v^k=({\mathbf {C}}_1,{\mathbf {C}}_2,\ldots ,{\mathbf {C}}_k)^T\), where each \({\mathbf {C}}_j=[c^L_{j},c^U_{j}],~j\in \Lambda _k;~\Lambda _k=\{1,2,\ldots ,k\}.\) The parametric form of \({\mathbf {C}}_v^k\) is the set

$$\begin{aligned} \nonumber \Big \{c_t|~c_t=(c_{t_1}^1,c_{t_2}^2,&\ldots ,c_{t_k}^k)^T,~ c_{t_j}^j=c_j^L+t_j(c_j^U-c_j^L),\\&~t=(t_1,t_2,\ldots ,t_k)^T,~0\le t_j \le 1, j\in \Lambda _k\Big \}. \end{aligned}$$(1) -

The interval matrix \({\mathbf {A}}_m \in (\mathbb {I(R)})^{p\times q}\) of order \(p\times q\) and \({\mathbf {A}}_m=({\mathbf {A}}_{ij})_{p\times q}\), \({\mathbf {A}}_{ij}=[a^L_{ij},a^U_{ij}],i\in \Lambda _p,~j\in \Lambda _q.\) \({\mathbf {A}}_m\in (\mathbb {I(R)})^{p\times q}\) is the set of real matrices,

$$\begin{aligned} \nonumber \Big \{A(t)|~A(t)=(a^{ij}_{t_{ij}})_{p\times q}, a^{ij}_{t_{ij}}=&a_{ij}^L+t_{ij}(a_{ij}^U-a_{ij}^L),\\&~0\le t_{ij} \le 1, i\in \Lambda _p,j\in \Lambda _q\Big \}. \end{aligned}$$(2)

The binary operation \(\circledast\) between two closed intervals \({\mathbf {A}}=[a^L,a^U]\) and \({\mathbf {B}}=[b^L,b^U]\) in \(\mathbb {I(R)}\) is defined to be \({\mathbf {A}}\circledast {\mathbf {B}}\) \(=\) \(\{a *b: a\in {\mathbf {A}}, b \in {\mathbf {B}}\}\), where \(*\in \{+,-,\cdot ,/\}\). These interval operations can also be performed with respect to parameters as follows:

Hence, we have

The set of closed intervals, \(\mathbb {I(R)}\) is not a totally ordered set. Several partial order relations exist on \(\mathbb {I(R)}\) in the literature (see [32, 57]). Here we consider a partial ordering due to Bhurjee and Panda [12] defined as follows:.

Definition 1

[12] For \({\mathbf {A}},{\mathbf {B}}\in \mathbb {I(R)}\), \(a_t\in {\mathbf {A}}\) and \(b_t\in {\mathbf {B}}\)

Note that \({\mathbf {A}}\preceq {\mathbf {B}}\) is not same as \({\mathbf {B}}\ominus {\mathbf {A}}\succeq {\mathbf {0}}.\) For example \([3,5] \preceq [4,9]\), but \([4,9] \ominus [3,5]=[-1,6]\nsucceq {\mathbf {0}}.\)

Interval valued function: Many researchers (see [26, 57]) have defined an interval valued function in different ways. In this paper, we consider the definition of the same as defined by Bhurjee and Panda [12].

Definition 2

For \({\mathbf {c}}_t\in {\mathbf {C}}_v^k,\) let \(f_{{\mathbf {c}}_t}:\mathbb {R}^n\rightarrow \mathbb {R}\). For a given interval vector \({\mathbf {C}}_v^k\in \mathbb {I}^k\), define an interval valued function \({\mathbf {F}}_{{\mathbf {C}}_v^k}:\mathbb {R}^n\rightarrow \mathbb {I}\) by

For every fixed x, if \(f_{{\mathbf {c}}_t}(x)\) is continuous in t then \(\min \limits _{t\in [0,1]^k}f_{{\mathbf {c}}_t}(x)\) and \(\max \limits _{t\in [0,1]^k}f_{{\mathbf {c}}_t}(x)\), exist. In that case

If \(f_{{\mathbf {c}}_t}(x)\) is linear in t then \(\min _{t\in [0,1]^k}f_{{\mathbf {c}}_t}(x)\) and \(\max _{t\in [0,1]^k}f_{{\mathbf {c}}_t}(x)\) exist in the set of vertices of \({\mathbf {C}}_v^k.\) If \(f_{{\mathbf {c}}_t}(x)\) is monotonically increasing in t, then \({\mathbf {F}}_{{\mathbf {C}}_v^k}(x)=[f_{{\mathbf {c}}_0}(x),f_{{\mathbf {c}}_1}(x)]\).

2.1 Interval-typed random variable

The definition of an interval-typed random variable due to Li and Jin [44] is given as follows: A variable \(\varvec{\chi }= [\chi ^L, \chi ^U]\) is said to be an interval-typed random variable if both lower bound \(\chi ^L\) and upper bound \(\chi ^U\) are random variables, and the mathematical expectation \(\mathbf{E}(\chi ^L) \le \mathbf{E}(\chi ^U)\).

Suppose \(\chi ^L\) and \(\chi ^U\) follow a normal distribution with mean \(\mathbf{E}(\chi ^L)\), \(\mathbf{E}(\chi ^U)\) and standard deviation \(\sigma _{\chi ^L}\), \(\sigma _{\chi ^U}\); in short \(\chi ^L\sim {\mathcal {N}}(\mathbf{E}(\chi ^L),\sigma _{\chi ^L}^2)\), \(\chi ^U\sim {\mathcal {N}}(\mathbf{E}(\chi ^U),\sigma _{\chi ^U}^2)\), respectively. Also, if \(\mathbf{E}(\chi ^L)= \mathbf{E}(\chi ^U)\) and \(\sigma _{\chi ^L}=\sigma _{\chi ^U}\), then \([\chi ^L, \chi ^U]\) degenerate a traditional normally distributed random variable.

Clearly, based on the above definition if \(\varvec{\chi }_1\) and \(\varvec{\chi }_2\) are two interval-typed random variables then addition and constant multiplication are well defined as follows:

-

\(\varvec{\chi }_1 \oplus \varvec{\chi }_2\) = \(\Big [\min \limits _{t_1,t_2\in [0, 1]}(\chi _{t_1} + \chi _{t_2}),~\max \limits _{t_1,t_2\in [0, 1]}(\chi _{t_1}+\chi _{t_2})\Big ]\) \(\equiv [\chi _1^L+\chi _2^L, \chi _1^U+\chi _2^U].\)

-

For \(~k\in \mathbb {R}\), \(k \varvec{\chi }= \{k \chi _t~|~t\in [0,1]\}\equiv \left[\min \limits _{t\in [0, 1]}(k \chi _t),~\max \limits _{t\in [0, 1]}(k \chi _t)\right]\equiv [k\chi ^L, k\chi ^U]\), \(k\ge 0\).

Property 1

Let \(\varvec{\chi }_1, \varvec{\chi }_2,\ldots ,\varvec{\chi }_n\) be the n number of interval-typed random variables, where \(\chi _i^L\sim {\mathcal {N}}\Big (\mathbf{E}(\chi _i^L), \sigma _{\chi _i^L}^2 \Big )\), \(i= 1,2,\ldots ,n,\) and \(\chi _i^U\sim {\mathcal {N}}\Big (\mathbf{E}(\chi _i^U), \sigma _{\chi _i^U}^2 \Big )\), \(i= 1,2,\ldots ,n.\) The lower bounds \(\chi _1^L, \chi _2^L,\ldots , \chi _n^L\) are mutually independent with each other, the upper bounds \(\chi _1^U, \chi _2^U,\ldots , \chi _n^U\) are also mutually independent with each other. Thus,

is an interval-typed random variable with \(\varvec{\chi }^L\sim {\mathcal {N}}\Big (\sum \limits _{i=1}^n\mathbf{E}(\chi _i^L), \sum \limits _{i=1}^n\sigma _{\chi _i^L}^2\Big )\) and \(\varvec{\chi }^U\sim {\mathcal {N}}\Big (\sum \limits _{i=1}^n\mathbf{E}(\chi _i^U), \sum \limits _{i=1}^n\sigma _{\chi _i^U}^2\Big )\).

Property 2

If \(\varvec{\chi }\) is an interval-typed random variable then the cumulative distribution function for \(\varvec{\chi }\) is an extension of the traditional cumulative distribution function as follow:

where \(F(x_t)=\mathbf{Pr}[\chi _t \le x_t]\), for all \(t \in [0, 1]\).

3 Interval mean-value-at-risk model

As mentioned earlier in this paper, we formulate an interval parameter portfolio optimization problem with risk measure as value-at-risk and called it interval mean-value-at-risk model (\(\mathbf{IMVAR}\)). the following notations are used throughout the paper to formulate the model.

H | Total number of time period |

\(r_{jh}\) | Rate of return of the \(j{th}\) stock at time h, for \(j=1,2,\ldots ,n\) and \(h=1, 2,\ldots H\). |

\(\mu _j\) | Expected rate of return of the \(j{th}\) stock, i.e. \(\mu _j=\frac{1}{H}\sum _h^H r_{jh}\). |

\(\varvec{\mu }_j=[\mu _{j}^L,~\mu _{j}^U]\) | Interval rate of return of the \(j{th}\) stock with lower bound \(\mu _{j}^L\) and upper bound \(\mu _{j}^U\). |

\({\varvec{\mu }_p}\) | Interval expected rate of return of the portfolio. |

\(\mu _p^L\) | Lower bound of expected rate of the return of the portfolio. |

\(\mu _p^U\) | Upper bound of expected rate of the return of the portfolio. |

\(\varvec{\sigma }_{ij}=[\sigma _{ij}^L,~\sigma _{ij}^U]\) | represents an interval form of covariance between \(i{th}\) and \(j{th}\) stocks. |

\(\varvec{\sigma }_{p}=[\sigma _{p}^L,~\sigma _{p}^U]\) | Standard deviation of the portfolio in the form of interval. |

\(\sigma _p^L\) | Lower bound of standard deviation of the portfolio. |

\(\sigma _p^U\) | Upper bound of standard deviation of the portfolio. |

\(x_{j}\in [0,1]\) | Proportion of total investment of \(j{th}\) stock, \(j=1,2,\ldots,n\). |

3.1 Model formulation

Suppose an investor aims to allocate his/her wealth into \(n\ge 2\) numbers of risky stocks for a fixed time period H of the investment. The interval \(\varvec{\mu }_j\) is the mean of rate of return of \(j{th}\) stocks, \(j =1, 2,\ldots ,n\). Denote \(\mathbf{x} = (x_1, x_2,\ldots ,x_n)^T\) is a portfolio of the investor, in such a way that \(\sum _{j=1}^n x_j=1\). Thus the expected rate of return of the portfolio is \(\mu _p=\sum _{j=1}^n\mu _jx_j\). Assume that the expected rate of return of a stock lies in the closed interval, the expected rate of the portfolio will also be contained in an interval \([\mu _p^L, \mu _p^U]\), and correspondingly variance will \([\sigma _p^L,\sigma _p^U]\). Following is the definition of value-at-risk of the portfolio if the rate of return of a portfolio is an interval.

Definition 3

Let \(\varvec{\chi }\) be the interval-typed random variable representing return of a portfolio, and \(\mathbf{F}(.)\) be its interval form of the cumulative distribution function. For a given period of time, the VaR at a confidence level \(\alpha \%, \alpha \in (0.5, 1)\) of a portfolio is defined as:

where \(\mathbf{F}(\mathbf{R})=\mathbf{Pr}[\varvec{\chi }\preceq \mathbf{R}]\), \(\mathbf{R}\) represents an interval rate of return over a given time period.

In particular, consider \(\mathbf{V}\) represents an interval rate of return of a portfolio over the given time period, then the VaR at the \(\alpha \%\) confidence level is \(\mathbf{V}\) with the intent that \(\mathbf{F}(-\mathbf{V })=1-\alpha\).

Suppose \(\alpha ^*\in (0, \infty )\), such that cumulative distribution function of standard normal distribution \(\varvec{\Phi }(-\alpha ^*)=1-\alpha ,\) for \(\alpha \in (0.5,1)\). Let \(\mathbb {Z}\) be the set of interval-typed random variable with normally distributed lower and upper bound. According to Definition 3, the VaR of portfolio \(\mathbf{x}\) at the \(100\alpha \%\) confidence level is \(\mathbf{V}\equiv -\mathbf{F}^{-1}(1-\alpha )\). Since for \(-\mathbf{V},\)

Thus an interval function \(\mathbf{V}:(0.5,~1)\times {\mathbb {Z}} \rightarrow \mathbb {I(R)},\) defined as

\(\forall \, (\alpha , {\mathcal {R}}_p(\mathbf{x}))\in (0.5,~1)\times {\mathbb {Z}}\) gives the bounds of VaR at \(100\alpha \%\) confident level of normally distributed random rate of return of portfolio \({\mathcal {R}}_p(\mathbf{x})\). Based on the above interval function (4) refers to VaR of the portfolio, the formulation of the mean-VaR portfolio optimization model for the fixed tolerance level of expected rate return \({\varvec{\mu }_{fix}}\) is given as follows:

where \(\varvec{\sigma }_p(\mathbf{x})\) and \(\varvec{\mu }_p(\mathbf{x})\) are defined as follows:

\({\mathbf {A}}_m=[\varvec{\sigma }_{ij}]_{n\times n}\) represents interval matrix with components as interval form of covariance between \(i{th}\) and \(j{th}\) stocks; \({\varvec{\mu }}_v^n=({\varvec{\mu }}_1, {\varvec{\mu }}_2,\ldots ,{\varvec{\mu }}_n)^T\). Hence mean-VaR model (5-7) becomes as follows:

In order to find lower \((\sigma _p^L)\) and upper \((\sigma _p^U)\) bound of the standard deviation of a portfolio in \(\mathbb {R}\) with \((\sigma _p^L) \le (\sigma _p^U)\) for \(\mathbf{IMVAR}\) can be easily evaluated using variance of the portfolio \(\mathbf{x}\), so as to find

Using the partial orderings defined in Sect. 2, the feasible region of above problem can be expressed as,

where \(t_p\in [0,1]\) and \(\Big \{A(t)|~A(t)=(\sigma ^{ij}_{t_{ij}})_{n\times n}, a^{ij}_{t_{ij}}= a_{ij}^L+t_{ij}(a_{ij}^U-a_{ij}^L), ~0\le t_{ij} \le 1, i\in \Lambda _n,j\in \Lambda _n\Big \}\).

The equivalent parametric form of \(\mathbf{IMVAR}\) is given as follows:

where \({\mathbf {t}}=(t_p,t^{\prime })\in [0,1]^{1+n}\).

Due to complexity of an interval inequality and interval uncertainty in the objective function, the classical optimization technique could not be directly applicable to solve nonlinear programming problems. Therefore \(\mathbf{IMVAR}_t\) is further transformed into a deterministic optimization problem (which is denoted by \(\mathbf{IMVAR}^\prime\)) as follows:

where \(w:[0,1]^{1+n}\rightarrow R_+\), \(\mu _{t^\prime }\in {\varvec{\mu }}_{v}^n\), \(d{\mathbf {t}}=dt_pdt_1^{\prime }dt_2^{\prime }\ldots dt_n^{\prime }\). This model is a deterministic nonlinear programming problem and can be solved by using Karush-Kuhn-Tucker (KKT) conditions with the help of any optimization software like Lingo, Mathematica, etc.

3.2 Existence of solution of interval mean VaR optimization problem

Definition 4

A point \(\mathbf{x}^*\in \varvec{\bigtriangleup }\) is called as an efficient solution of \(\mathbf{IMVAR}\) if there is no \(\mathbf{x}\in \varvec{\bigtriangleup }\), \(\mathbf{x}\ne \mathbf{x}^*\) such that \(S_{VaR}(\mathbf{x})\le {\mathcal {S}}_{VaR}(\mathbf{x}^*)\) and \({\mathcal {S}}_{VaR}(\mathbf{x})\ne {\mathcal {S}}_{VaR}(\mathbf{x}^*)\).

Definition 5

\(\mathbf{x}^*\) is called an properly efficient solution of \(\mathbf{IMVAR}\) if \(\mathbf{x}^*\in \varvec{\bigtriangleup }\) is an efficient solution of \(\mathbf{IMVAR}\) and there is a real number \(\lambda > 0\) so that for some \({\mathbf {t}}\in [0,1]^{1+n}\) and every \(\mathbf{x}\in \varvec{\bigtriangleup }\) with \({\mathcal {S}}_{VaR}(\mathbf{x},{\mathbf {t}}) < {\mathcal {S}}_{VaR}(\mathbf{x}^*,{\mathbf {t}})\), at least one \({\mathbf {t}}^\prime \in [0,1]^{1+n}\), \({\mathbf {t}}\ne {\mathbf {t}}^\prime\) exists with \({\mathcal {S}}_{VaR}(\mathbf{x},{\mathbf {t}}^\prime ) > {\mathcal {S}}_{VaR}(\mathbf{x}^*,{\mathbf {t}}^\prime )\) and

Note 1

Every properly efficient solution for a problem is an efficient solution to the problem. However, the converse is not true.

Theorem 1

A point \(\mathbf{x}^*\in \varvec{\bigtriangleup }\) is an optimal solution of \(\mathbf{IMVAR}^\prime\) then \(\mathbf{x}^*\) is a properly efficient solution of \(\mathbf{IMVAR}\).

Proof

Let \(\mathbf{x}^*\) be an optimal solution of \(\mathbf{IMVAR}^\prime\). Assume that \(\mathbf{x}^*\) is not a properly efficient solution of \(\mathbf{IMVAR}\). So for some \({\mathbf {t}}\in [0,1]^{1+n}\) and some \(\mathbf{x}\in \varvec{\bigtriangleup }\) with \({\mathcal {S}}_{VaR}(\mathbf{x},{\mathbf {t}}) < {\mathcal {S}}_{VaR}(\mathbf{x}^*,{\mathbf {t}})\). Select a weight function \(w:[0,1]^{1+n}\rightarrow \mathbb {R}_{+}\) which is continuous. Then we choose \(\lambda = \max \Big \{\frac{w({\mathbf {t}}^\prime )}{w({\mathbf {t}})}\Big \}\), \({\mathbf {t}}\ne {\mathbf {t}}^\prime\), \({\mathbf {t}},{\mathbf {t}}^\prime \in [0,1]^{1+n}\), \(w({\mathbf {t}}) > 0\) satisfying

and for all \({\mathbf {t}}^\prime \in [0,1]^{1+n}\) with \({\mathcal {S}}_{VaR}(\mathbf{x},{\mathbf {t}}^\prime ) > {\mathcal {S}}_{Var}(\mathbf{x}^*,{\mathbf {t}}^\prime )\).

This gives

After integrating on both sides with respect to the parameter \({\mathbf {t}}\) and \({\mathbf {t}}^\prime\), we have

which is a contradiction that \(\mathbf{x}^*\) is an optimal solution of \(\mathbf{IMVAR}^\prime .\) Hence \(\mathbf{x}^*\) is a properly efficient solution of \(\mathbf{IMVAR}\). \(\square\)

4 Numerical example

The efficacy of the above-developed model and its solution methodology is explained as a case study using the historical data collected from the National Stock Exchange, India. Firstly, a step-by-step procedure is explained to estimate and implement the above-developed methodology. This algorithm will help for obtaining optimal bounds of the VaR with efficient investment strategies, which is given as follows:

4.1 Algorithm

-

Step 1:

Input

-

(a)

Number of stocks(n).

-

(b)

Collect historical opening(\(p_{jh}^{open}\)), maximum(\(p_{jh}^{max}\)), minimum(\(p_{jh}^{min}\)), and closing(\(p_{jh}^{close}\)) prices of each stock for a given time period(H).

-

(c)

Fix the values of \(\alpha \) and \(\alpha ^*\).

-

Step 2:

(a) Calculate rate of return corresponding to each price using the formula \(r_{jh}^{price}=\frac{{p_{jh}^{price}-p_{jh-1}^{price}}}{p_{jh-1}},\) where \(price\in \{opening,maximum,minimum,closing\}.\)

-

(b)

Calculate \(\mu _j^{price}=\frac{1}{H}\sum _{h=1}^{H}r_{jh}^{price}\), for \(j=1,2\dots n.\)

-

(c)

Estimate, for all \(j=1,2,\dots ,n\), \(\mu _j^L=\min \{\mu _j^{open}, \mu _j^{max}, \mu _j^{min}, \mu _j^{close}\}\) and \(\mu _j^U=\) \(\max \{\mu _j^{open},\) \(\mu _j^{max},\) \(\mu _j^{min}, \mu _j^{close}\}\) .

-

Step 3:

(a) Compute \(\sigma _{ij}^L\) and \(\sigma _{ij}^U\) for all \( i= 1,2,\dots , n\), \(j=1,2,\ldots ,n\) as follow:

$$\begin{aligned} \sigma _{ij}^L=&\frac{1}{H-1}\sum _{t=1}^{H}(\tilde{r}_{ih}-\mu _i^L)(\tilde{r}_{jh}-\mu _j^L) \text{ and } \end{aligned}$$(9)$$\begin{aligned} \sigma _{ij}^U=&\frac{1}{H-1}\sum _{t=1}^{H}(\hat{r}_{ih}-\mu _i^U)(\hat{r}_{jh}-\mu _j^U), \end{aligned}$$(10)where \(\tilde{r}_{it}\) denotes the return of \(i{th}\) stock at time t, for every i, t, corresponding to the sample returns of \(i{th}\) stock from which the lower bound of expected return \(\mu _i^L\) is obtained. Similarly, \(\hat{r}_{it}\) denotes value of sample return of \(i{th}\) stock at time t which is associated with the sample return from which the upper bound of expected return \(\mu _i^U\) is obtained.

-

(b)

If \(\sigma _{ij}^L>\sigma _{ij}^U\), then arrange \(\sigma _{ij}^L=\sigma _{ij}^U\) and \(\sigma _{ij}^U=\sigma _{ij}^L\) and vice-versa.

-

Step 4:

(a) Choose \(\alpha ^* \in (0,\infty )\) and weight function \(w(\mathbf{t})\) in such way that

$$\begin{aligned} \underbrace{\int _0^1\int _0^1\dots \int _0^1}_{1+n}w(\mathbf{t})d\mathbf{t}=1. \end{aligned}$$ -

(b)

Make deterministic model \({\mathcal {S}}_{VaR}(\mathbf{x})\).

-

Step 5:

Evaluate efficient portfolio \(\mathbf{x^*}\) by solving the model formulated in previous Step 4 (b) for given values of \(\alpha ^*\) and \(\varvec{\mu }_{fix}\) with the help of any software, which supports non-linear optimization problem.

-

Step 6:

Obtain the bound of value at risk for the portfolio \(\mathbf{x^*}\).

In order to explain the above-given step by step procedure, we collect firstly (Step 1: (a) and (b) of the algorithm 4.1) the data sets of the daily, opening price, maximum price, minimum price, and closing price of fifty stocks listed in National Stock Exchange(NSE), India, for a time period January 1, 2017, to December 31, 2019. The name of all 50 stocks is given in Table 1.

Based on each type of price, we calculate each stock’s rate of return according to Step 2: (a). Using Step 2: (b) and (c), the bound of the expected return of each stock has been calculated, which are listed in Table 2.

In Step 3, bounds of covariance between two stocks have also been evaluated using the technique explained in the expression (9) and (10).

In Step 4, the estimated bounds of the expected rate of return of each stock and covariance between the stocks (which are obtained in Step 2 and Step 3, respectively) have considered in the terms of the input data for developed portfolio selection model to find the optimum bounds of value-at-risk of the portfolio. Simultaneously, we select three different values of \(\alpha ^*=4.50, 3.55, 1.88\), and individually evaluate optimal investment strategies for a given tolerance level of the rate of the expected return of portfolio \(\varvec{\mu }_{fix}\). For this, we construct first deterministic model by choosing \(w(\mathbf{t})=1\) based on the Step 4 (a), and then obtain the efficient portfolios with each of the three values of \(\alpha ^*\), for all the values of \(\varvec{\mu }_{fix}=[0.010\), 0.012], [0.0120, 0.0140], [0.0140, 0.0160], [0.0160, 0.0180], [0.0180, 0.0200], [0.0200, 0.0220], [0.0220, 0.0240] and [0.0240, 0.0260] using LINGO 11 software as explained in Step 5. Finally, the bounds of VaR for each portfolio is calculated in Step 6. A complete list of the efficient portfolios for each value of \(\alpha ^*\) at all values of \(\varvec{\mu }_{fix}\) are given in Tables 3, 4 and 5.

The result of Table 3 gives the details of the lower and upper bound of VaR, standard deviation, and the expected return of the portfolio for fixed \(\alpha ^*=4.50\), corresponding to each the tolerance range of \(\varvec{\mu }_{fix}\). These results are obtained through the equivalent deterministic model \({\mathcal {S}}_{VaR}(\mathbf{x})\) of \(\mathbf{IMVAR}\). One may also observe from Table 3 that the efficient bound of VaR changes as the lower bound of \(\varvec{\mu }_{fix}\) changes, simultaneously the optimal investment strategies stuff happens the different for all the possible tolerance levels of expected return. Similarly, Table 4 and Table 5 describe the same type of result as given in Table 3 for the values of \(\alpha ^*=3.50\) and \(\alpha ^*=1.88\), respectively. One can also see from the results obtained in Tables 3, 4, and 5 that a group of the same stocks is obtained for different values of \(\alpha ^*\) conforming to each lower bound \(\mu _{fix}^L\). Although the proportions of the total investment for each value of \(\mu _{fix}^L\) are different with different ranges of VaRs. The portfolios obtained based on three different value of \(\alpha ^*\) in Tables 3, 4, and 5 are also represented graphically in Figs. 1 and 2. From these figures, one can be shown that the portfolios obtained for different values of \(\alpha ^*\) are different and changed with the different values of \(\mu _{fix}^L\).

The graph between \(\mu _{fix}\) and the bounds of VaR corresponding to \(\alpha ^*=\)4.50, 3.50, and 1.88

VaR-\(\sigma\) graph for each value of \(\alpha ^*=\)4.50, 3.50, and 1.88

Next, a single tolerance level of the expected return of portfolio \(\varvec{\mu }_{fix}=[0.02, 0.22]\) is selected and obtained an efficient portfolio varying the value of \(\alpha ^*\) in Step 5. Accordingly, the optimal investment strategy has been acquired using LINGO 11 software for each value of \(\alpha ^*=\) 1.85, 2.05, 2.25, 2.45, 2.65, 2.85, 3.05, 3.25, and 3.45, respectively.

The optimal bounds of VaR of portfolios with the proportion of the total investment on stocks corresponding to each value of \(\alpha ^*\) for a fixed \(\varvec{\mu }_{fix}=[0.02,0.022]\) are given in Table 6. The values of \(\sigma _p^L\), \(\sigma _p^U\), \(\mu _p^L\), \(\mu _p^U\), \(\mathrm{VaR}^L\) and \(\mathrm{VaR}^U\) are evaluated via the proportions of the total investment for each portfolio. All these values are also given in the table. One can observe from Table 6 that as the confidence level increases, the upper bound of VaR increases; that is, the range of VaR increases. This can be clearly seen in Fig. 3, where x-axis indicates different values of \(\alpha ^*\) and y-axis indicates values of VaR. The lower bound of the VaRs represents VaR’s possible acceptable value for the worst scenario of the market. Thus it is the same for all values of \(\alpha ^*\). However, the upper bound of VaRs represents the optimistic value of VaR when everything in the financial market goes in the right way.

VaR-\(\alpha ^*\) graph

Based on Table 6, another graph is drawn to explain the relation between upper bounds of VaR \((\mathrm{VaR}^U)\) (last rows in the table) and upper bound of standard deviations \((\varvec{\sigma _p^U})\) of the portfolio, where x-axis indicates different values of \(\varvec{\sigma _p^U}\) and the y-axis indicates values of \(\mathrm{VaR}^U\). This is given in Fig. 4. From this figure, one can see that the value of \(\varvec{\sigma _p^U}\) decreases, the value of \(\mathrm{VaR}^U\) increases, which means that lower value of standard deviation, a higher value of VaR.

The graph between upper bound of VaR \((\mathrm{VaR}^U)\) and standard deviation \((\varvec{\sigma _p^U})\) of the portfolios for different values of \(\alpha ^*\) at fixed tolerance level of expected return

Based on the above discussion, we observe that one can obtain a suitable investment policy of investment by solving \(\mathbf{IMVAR^\prime }\) for a fixed value of \({\varvec{\mu }}_{fix}\) and a confidence level (i.e., \(\alpha ^*\)). Selecting the values of the parameters \({\varvec{\mu }}_{fix}\) and \(\alpha ^*\) (according to the investors’ frame of mind), the investor might be accomplished a preferred portfolio investment policy.

For the verification of the results obtained from our developed model \(\mathbf{IMVAR}\), we consider the results obtained based on the deterministic mean-value-at-risk model \((\mathbf{DMVAR})\), Markowitz’s mean-variance model (\(\mathbf{MV}\)), and mean-absolute deviation model (\(\mathbf{MAD}\)); which have been developed by Alexander and Baptista [1]) Markowitz [55], and Konno & Yamazaki [36], respectively. To evaluate the optimal investment strategies of all \(\mathbf{DMVAR}\), \(\mathbf{MV}\) and \(\mathbf{MAD}\) models, the same data sets for the same period has been used. Among the data, only the closing price of all the 50 stocks is used to estimate each stock’s expected rate of return and variance/covariance between stocks. Using these estimated parameters as inputs, we create an efficient portfolio of all three models for each of the given expected return of portfolio \((\mu _{fix})\), viz., 0.0100, 0.0120, 0.0140, 0.0160, 0.0180, 0.0200, 0.0220 and 0.0240. The proportion of total investment in each stock of the portfolios obtained based on the \(\mathbf{DMVAR}\) model with optimally calculated variance for \(\alpha ^*=4.50\) are given in Table 7. The optimal variance of each portfolio of the \(\mathbf{MV}\) model with the proportion of total investment of each stock is given in Table 8. The proportion of total investment in each stock of the portfolios obtained based on the \(\mathbf{MAD}\) model with calculated expected return and variance are given in Table 9.

With the help of results obtained in Table 8, the efficient frontier for Markowitz’s mean-variance model is given in Fig. 5.

Risk-return graph of the Markowitz’s mean-variance model

Next, a comparative study of the outcomes found based on the \(\mathbf{IMVAR}\), \(\mathbf{DMVAR}\), \(\mathbf{MV}\) and \(\mathbf{MAD}\) models are presented, which are mentioned in Tables 3, 7, 8 and 9, respectively. One may observe in Table 6 that the proportion of the total investment obtained in each stock from \(\mathbf{IMVAR}\) for all tolerance levels of the expected return of the portfolio for \(\alpha ^* =4.50\) is different for different \(\mu _{fix}^L\). For example, if \(\mu _{fix}^L=0.01,\) then the portfolio consists 20 stocks, viz., A3, A10, A12, A13, A14, A15, A16, A17, A23, A24, A28, A29, A30, A36, A40, A41, A42, A43, A45 and A47 with proportion of the total investment 0.02148, 0.02398, 0.00346, 0.00167, 0.00578, 0.04598, 0.03464, 0.08257, 0.03702, 0.06186, 0.08519, 0.18126, 0.02332, 0.09098, 0.07326, 0.00460, 0.13819, 0.04115, 0.00202 and 0.04158, respectively. Correspondingly the calculated upper- and lower-bound of standard deviation of portfolio are 0.00066 and zero, respectively. While, the portfolio consists of 18 stocks for \(\mu _{fix}^L=0.020\), viz., A10, A11, A12, A13, A14, A16, A17, A18, A23, A24, A28, A29, A36, A40, A41, A42, A43 and A47 with proportion of the total investment 0.07277, 0.01439, 0.03216, 0.02170, 0.01714, 0.04780, 0.04902, 0.07061, 0.05982, 0.07292, 0.06399, 0.18588, 0.00060, 0.09446, 0.01502, 0.07200, 0.02468 and 0.08505, respectively, accordingly the calculated range of optimal \(\varvec{\sigma }_p= [0, 0.00087]\).

However, one can see that the portfolios which are obtained by using both the \(\mathbf{DMVAR}\) and \(\mathbf{MV}\) model consists 15 stocks for the fixed value of expected return \(\mu _{fix}=0.010\), viz., A3, A9, A10, A12, A15, A16, A17, A19, A23, A25, A26, A28, A29, A42 and A43 with the proportion of the total investment 0.02787, 0.02519, 0.03151, 0.03361, 0.05773, 0.08080, 0.07439, 0.02048, 0.11765, 0.11177, 0.10642, 0.08554, 0.02134, 0.15403 and 0.05168, respectively with variance 0.00033. For the fixed value of expected return \(\mu _{fix}=0.020\), the portfolio contains only 13 stocks, viz., A10, A12, A16, A17, A23, A24, A25, A26, A28, A29, A35, A41 and A43 with proportion of the total investment 0.02290, 0.05547, 0.10004, 0.10140, 0.08323, 0.01138, 0.09408, 0.13826, 0.10059, 0.15876, 0.05166, 0.00122 and 0.08100, respectively with variance 0.00063. Similarly, the portfolio obtained (using \(\mathbf{MAD}\) model) in Table 9 consists 12 stocks for the fixed value of expected return \(\mu _{fix}=0.010\), viz., A3, A9, A10, A12, A15, A16, A17, A23, A26, A28, A29 and A42 with proportion of the total investment 0.03808, 0.05431, 0.02925, 0.00438, 0.11331, 0.07607, 0.09263, 0.06557, 0.14277, 0.05337, 0.16198 and 0.16828, respectively with the calculated optimal \(\varvec{\sigma }_p= 0.00068\). While, for the fixed value of expected return \(\mu _{fix}=0.020\) the portfolio contains 13 stocks, viz., A10, A12, A15, A16, A17, A23, A26, A28, A29, A35, A41, A42 and A43 with proportion of the total investment 0.03712, 0.02569, 0.07567, 0.13014, 0.04944, 0.05515, 0.11475, 0.04521, 0.20129, 0.13951, 0.03531, 0.06904 and 0.02168, respectively with the calculated range of optimal \(\varvec{\sigma }_p= 0.00082\). Hence, the \(\mathbf{IMVAR}\) model provides a more diversify portfolio as compared to the other methods \((\mathbf{MV}, \mathbf{DMVAR} \text{ and } \mathbf{MAD})\), which helps to reduce the risk of the portfolio.

Although, the efficient portfolios obtaining from the \(\mathbf{MV}\) model are different for all given expected returns of the portfolio in Table 8. But the results obtained by the \(\mathbf{DMVAR}\) model are the same as the results obtaining by the \(\mathbf{MV}\) model as given in Tables 7 and 8. All efficient portfolios (obtaining in Table 3) of \(\mathbf{IMVAR}\) are different from the efficient portfolio obtained from the \(\mathbf{MV}\) (in Table 8), \(\mathbf{DMVAR}\) ( in Table 7)) and \(\mathbf{MAD}\) (in Table 9) models for all possible value of \(\mu _{fix}\). It can also be seen that the efficient frontier drawn between the calculated variance and the expected return of each portfolio relative to all models is different except the efficient frontier of \(\mathbf{MV}\) model and \(\mathbf{DMVAR}\) model. This can be easily viewed in Fig. 6. In this figure, the x-axis represents the calculated variance of the portfolio and the y-axis represents the expected return \(\mu\) of the portfolio.

The relation between expected return and standard deviation of the portfolios obtained based on all three models \(\mathbf{IMVAR}^\prime\), \(\mathbf{DMVAR}\), \(\mathbf{MV}\) and \(\mathbf{MAD}\)

In Fig. 6, two curves DMVAR and MV represent the relation between the values of \(\sigma _p\) and \(\mu _p\), which are given in the last and the first row of Table 7, and the second and the first row of Table 8 respectively. Similarly, the relation between the values of \(\sigma _p^U\) with values of \(\mu _p^L\) and \(\mu _p^U\) of Table 3 is represented by two curves IMVAR(Lower) and IMVAR(Upper), respectively in the figure. The curve MAD represents the efficient frontier making from the last two rows (\(\mu _p\) and \(\varvec{\sigma }_p^2\)) of Table 9. One may observe from the figure that curves DMVAR and MV coincide with each other, while MAD, IMVAR(Upper), and IMVAR(Lower) are inside of the curve. All the efficient frontiers are inside of the feasible region of \(\mathbf{MV}\) efficient set. However, the efficient set obtained using VaR as a measure of risk is smaller than the mean-variance efficient group. Still, then again, we find that the efficient portfolio obtained by the mean-VaR model is economically better diversified than the efficient portfolio obtained by other models, which are described below.

The efficacy of the investment strategy obtained from all models is examined by evaluating the portfolios’ actual monthly return obtained from all the models mentioned above, including the interval parameter semi-absolute portfolio selection model (developed by Lai et al. [43]).

The proportions of total investment used to calculate the actual monthly return of portfolios are listed in Table 10. The proportions of the total investment based on the model of Lai et al. [43] are obtained using the same data sets (where \(w_1=0.08\), \(w_2=0.09\)) that have been used for our method. The actual returns of all stocks (listed in Table 1) are evaluated using the monthly closing prices from January 1, 2020, to December 31, 2020. The actual monthly return of the portfolios are calculated for every nine monthly returns corresponding to all \(\mathbf{IMVAR},\) \(\mathbf{DMVAR,}\) \(\mathbf{MV}\), \(\mathbf{MAD}\) and Lai et al.’s models. The actual return of portfolio corresponding to each model are listed in Table 11.

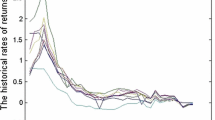

The graphical representations of actual monthly returns of all five models are given in Fig. 7, where \(x-\)axis represents months of the portfolio and \(y-\)axis means actual returns. The months Feb, Mar, Apr, May, Jun, Jul, Aug, Sep, and Oct, are denoted as 1, 2, 3, 4, 5, 6, 7, 8, and 9, respectively, in the figure. It is clear from Table 10 that the total amount is distributed in more stocks by our model \(\mathbf{IMVAR}\) compared to other models. That means the \(\mathbf{IMVAR}\) model is provided a more diversified portfolio than the existing model.

Actual monthly returns

From Fig. 7, it can be seen that actual returns of the portfolio related to our model \(\mathbf{IMVAR}\) gives negative return only on two months Feb and Mar. It is very close to zero as compared to another one. However, the portfolio’s actual monthly returns corresponding to the other four models give negative returns on three months (Feb, Mar and Apr). These all returns are a bit far away from zero compared to our model. If we are assumed Zero expected return as a baseline, then returns obtained by our method are more consistent than returns received by \(\mathbf{DMVAR,}\) \(\mathbf{MV}\), \(\mathbf{MAD}\) and Lai et al.’s methods. Hence, \(\mathbf{IMVAR}\) provides a well-diversified portfolio with less risk.

5 Conclusion

This paper deliberated the VaR risk measure of the portfolio optimization problem under interval uncertainty by defining interval-type random parameters. The mean-VaR model is formulated with parameters expected return and risk in the form of intervals. A solution technique is developed by transforming the \(\mathbf{IMVAR}\) model into a classical deterministic nonlinear model \(\mathbf{IMVAR}^\prime\) using the parametric definition of interval. The existence of an optimal investment strategy for an optimal range of VaR is discussed. The mean-VaR model is also analyzed through a case study based on the National Stock Exchange of India’s data set. Characterization of the existence of an optimally weighted combination of stocks with an optimal range of VaR of the \(\mathbf{IMVAR}\) shows that for an obtainable objective minimum VaR, one must be careful in selecting the confidence level and fixing a tolerance level of expected return. Suppose the tolerance level of the expected return at which VaR is computed is sufficiently large. In that case, the minimum VaR portfolio may not exist, and the mean-VaR efficient set may be empty. The computational results show that the \(\mathbf{IMVAR}\) provides better investment strategies with minimum VaR to the risk aversion of an investor using interval data.

References

Alexander, G.J., Baptista, A.M.: Economic implications of using a mean-var model for portfolio selection: a comparison with mean-variance analysis. J. Econ. Dyn. Control 26(7–8), 1159–1193 (2002)

Alexander, G.J., Baptista, A.M.: A comparison of var and cvar constraints on portfolio selection with the mean-variance model. Manag. Sci. 50(9), 1261–1273 (2004)

Artzner, P., Delbaen, F., Eber, J.M., Heath, D.: Coherent measures of risk. Math. Finance 9(3), 203–228 (1999)

Babazadeh, H., Esfahanipour, A.: A novel multi period mean-var portfolio optimization model considering practical constraints and transaction cost. J. Comput. Appl. Math. 361, 313–342 (2019)

Baixauli-Soler, J.S., Alfaro-Cid, E., Fernandez-Blanco, M.O.: Mean-var portfolio selection under real constraints. Comput. Econ. 37(2), 113–131 (2011)

Basak, S., Shapiro, A.: Value-at-risk-based risk management: optimal policies and asset prices. Rev. Financial Stud. 14(2), 371–405 (2001)

Benati, S., Rizzi, R.: A mixed integer linear programming formulation of the optimal mean/value-at-risk portfolio problem. Eur. J. Oper. Res. 176(1), 423–434 (2007)

Best, M.J., Hlouskova, J.: Portfolio selection and transactions costs. Comput. Optim. Appl. 24(1), 95–116 (2003)

Best, M.J., Hlouskova, J.: An algorithm for portfolio optimization with transaction costs. Manag. Sci. 51(11), 1676–1688 (2005)

Bhattacharyya, R., Chatterjee, A., Kar, S., et al.: Uncertainty theory based novel multi-objective optimization technique using embedding theorem with application to r & d project portfolio selection. Appl. Math. 1(03), 189 (2010)

Bhurjee, A., Kumar, P., Panda, G.: Optimal range of sharpe ratio of a portfolio model with interval parameters. J. Inf. Optim. Sci. 36(4), 367–384 (2015)

Bhurjee, A.K., Panda, G.: Efficient solution of interval optimization problem. Math. Methods Oper. Res. 76(3), 273–288 (2012)

Bhurjee, A.K., Panda, G.: Multi-objective interval fractional programming problems: an approach for obtaining efficient solutions. Opsearch 52(1), 156–167 (2015)

Cai, X., Teo, K.L., Yang, X., Zhou, X.Y.: Portfolio optimization under a minimax rule. Manag. Sci. 46(7), 957–972 (2000)

Campbell, R., Huisman, R., Koedijk, K.: Optimal portfolio selection in a value-at-risk framework. J. Bank. Finance 25(9), 1789–1804 (2001)

Chatterjee, K., Hossain, S.A., Kar, S.: Prioritization of project proposals in portfolio management using fuzzy ahp. Opsearch 55(2), 478–501 (2018)

Chen, F.Y.: Analytical var for international portfolios with common jumps. Comput. Math. Appl. 62(8), 3066–3076 (2011)

Chen, S.X., Tang, C.Y.: Nonparametric inference of value-at-risk for dependent financial returns. J. Financial Econ. 3(2), 227–255 (2005)

Consigli, G.: Tail estimation and mean-var portfolio selection in markets subject to financial instability. J. Bank Finance 26(7), 1355–1382 (2002)

Costa, T., Chalco-Cano, Y., Lodwick, W.A., Silva, G.N.: Generalized interval vector spaces and interval optimization. Inf. Sci. 311, 74–85 (2015)

Cui, X., Zhu, S., Sun, X., Li, D.: Nonlinear portfolio selection using approximate parametric value-at-risk. J. Bank. Finance 37(6), 2124–2139 (2013)

Fang, Y., Lai, K.K., Wang, S.Y.: Portfolio rebalancing model with transaction costs based on fuzzy decision theory. Eur. J. Oper. Res. 175(2), 879–893 (2006)

Gaivoronski, A.A., Pflug, G.: Value-at-risk in portfolio optimization: properties and computational approach. J. Risk 7(2), 1–31 (2005)

Giove, S., Funari, S., Nardelli, C.: An interval portfolio selection problem based on regret function. Eur. J. Oper. Res. 170(1), 253–264 (2006)

Goh, J.W., Lim, K.G., Sim, M., Zhang, W.: Portfolio value-at-risk optimization for asymmetrically distributed asset returns. Eur. J. Oper. Res. 221(2), 397–406 (2012)

Hansen, E., Walster, G.W.: Global Optimization Using Interval Analysis: Revised and Expanded, vol. 264. CRC Press, Amsterdam (2003)

Henriques, C.O., Coelho, D.: A multiobjective interval portfolio formulation approach for supporting the selection of energy efficient lighting technologies. In: Proceedings of 2017 6th International Conference on Environment, Energy and Biotechnology (ICEEB2017) (2017)

Ida, M.: Generation of efficient solutions for multiobjective linear programming with interval coefficients. In: Proceedings of the 35th SICE Annual Conference. International Session Papers, pp. 1041–1044. IEEE (1996)

Ida, M.: Multiobjective optimal control through linear programming with interval objective function. In: Proceedings of the 36th SICE Annual Conference. International Session Papers, pp. 1185–1188. IEEE (1997)

Ida, M.: Portfolio selection problem with interval coefficients. Appl. Math. Lett. 16, 709–713 (2003)

Ida, M.: Solutions for the portfolio selection problem with interval and fuzzy coefficients. Reliable Comput. 10(5), 389–400 (2004)

Ishibuchi, H., Tanaka, H.: Multiobjective programming in optimization of the interval objective function. Eur. J. Oper. Res. 48(2), 219–225 (1990)

Jong, Y.: Optimization method for interval portfolio selection based on satisfaction index of interval inequality relation. arXiv preprint arXiv:1207.1932 (2012)

Kar, M.B., Kar, S., Guo, S., Li, X., Majumder, S.: A new bi-objective fuzzy portfolio selection model and its solution through evolutionary algorithms. Soft Comput. 23(12), 4367–4381 (2019)

Konno, H.: Piecewise linear risk function and portfolio optimization. J. Oper. Res. Soc. Japan 33(2), 139–156 (1990)

Konno, H., Yamazaki, H.: Mean-absolute deviation portfolio optimization model and its applications to tokyo stock market. Manag. Sci. 37(5), 519–531 (1991)

Kumar, P., Bhurjee, A.: An efficient solution of nonlinear enhanced interval optimization problems and its application to portfolio optimization. Soft Computing pp. 1–14

Kumar, P., Panda, G.: Solving nonlinear interval optimization problem using stochastic programming technique. Opsearch 54(4), 752–765 (2017)

Kumar, P., Panda, G., Gupta, U.: Portfolio rebalancing model with transaction costs using interval optimization. Opsearch 52(4), 827–860 (2015)

Kumar, P., Panda, G., Gupta, U.: An interval linear programming approach for portfolio selection model. Int. J. Oper. Res. 27(1–2), 149–164 (2016)

Kumar, P., Panda, G., Gupta, U.: Multiobjective efficient portfolio selection with bounded parameters. Arab. J. Sci. Eng. 43(6), 3311–3325 (2018)

Kumar, P., Panda, G., Gupta, U.: Stochastic programming technique for portfolio optimization with minimax risk and bounded parameters. Sādhanā 43(9), 149 (2018)

Lai, K.K., Wang, S., Xu, J., Zhu, S., Fang, Y.: A class of linear interval programming problems and its application to portfolio selection. IEEE Trans. Fuzzy Syst. 10(6), 698–704 (2002)

Li, C., Jin, J.: A new portfolio selection model with interval-typed random variables and the empirical analysis. Soft Comput. 22(3), 905–920 (2018)

Li, J., Xu, J.: A class of possibilistic portfolio selection model with interval coefficients and its application. Fuzzy Optim. Decision Making 6(2), 123–137 (2007)

Liu, S., Wang, S., Qiu, W.: Mean-variance-skewness model for portfolio selection with transaction costs. Int. J. Syst. Sci. 34(4), 255–262 (2003)

Liu, S.T.: The mean-absolute deviation portfolio selection problem with interval-valued returns. J. Comput. Appl. Math. 235(14), 4149–4157 (2011)

Liu, Y.J., Zhang, W.G., Wang, J.B.: Multi-period cardinality constrained portfolio selection models with interval coefficients. Ann. Oper. Res. 244(2), 545–569 (2016)

Liu, Y.J., Zhang, W.G., Zhang, P.: A multi-period portfolio selection optimization model by using interval analysis. Econ. Model. 33, 113–119 (2013)

Lwin, K.T., Qu, R., MacCarthy, B.L.: Mean-var portfolio optimization: a nonparametric approach. Eur. J. Oper. Res. 260(2), 751–766 (2017)

Majumder, S., Kar, S., Pal, T.: Mean-entropy model of uncertain portfolio selection problem. In: Multi-Objective Optimization, pp. 25–54. Springer (2018)

Mansini, R., Ogryczak, W., Speranza, M.G.: Conditional value at risk and related linear programming models for portfolio optimization. Ann. Oper. Res. 152(1), 227–256 (2007)

Mansini, R., Ogryczak, W., Speranza, M.G.: Twenty years of linear programming based portfolio optimization. Eur. J. Oper. Res. 234(2), 518–535 (2014)

Markovitz, H.: Portfolio Selection: Efficient Diversification of Investments. John Wiley, NY (1959)

Markowitz, H.: Portfolio selection*. J. Finance 7(1), 77–91 (1952)

Moghadam, M.A., Ebrahimi, S.B., Rahmani, D.: A constrained multi-period robust portfolio model with behavioral factors and an interval semi-absolute deviation. Journal of Computational and Applied Mathematics 374, (2020)

Moore, R.: Interval Analysis. Prentice Hall, Hoboken (1966)

Qin, Z., Kar, S., Li, X.: Developments of mean-variance model for portfolio selection in uncertain environment. J. Comput. Appl. Math. (2009)

Ranković, V., Drenovak, M., Urosevic, B., Jelic, R.: Mean-univariate garch var portfolio optimization: actual portfolio approach. Comput. Oper. Res. 72, 83–92 (2016)

Şerban, F., Costea, A., Ferrara, M.: Portfolio optimization using interval analysis. Economic Computation and Economic Cybernetics Studies and Research, ASE Publishing 48(1), 125–137 (2015)

Sheng, Z., Benshan, S., Zhongping, W.: Analysis of mean-var model for financial risk control. Syst. Eng. Proc. 4, 40–45 (2012)

Speranza, M.G.: Linear programming models for portfolio optimization. Finance 14, 107–123 (1993)

Speranza, M.G.: A heuristic algorithm for a portfolio optimization model applied to the milan stock market. Comput. Oper. Res. 23(5), 433–441 (1996)

Tan, M.y.: Interval number model for portfolio selection with liquidity constraints. In: Fuzzy engineering and operations research, pp. 31–39. Springer (2012)

Wu, M., Kong, D.w., Xu, J.p., Huang, N.j.: On interval portfolio selection problem. Fuzzy Optimization and Decision Making 12(3), 289–304 (2013)

Yan, X.S.: Liquidity, investment style, and the relation between fund size and fund performance. J. Financial Quant. Anal. 43(3), 741–767 (2008)

Zhang, P.: An interval mean-average absolute deviation model for multiperiod portfolio selection with risk control and cardinality constraints. Soft Comput. 20(3), 1203–1212 (2016)

Zhang, P.: Multiperiod mean semi-absolute deviation interval portfolio selection with entropy constraints. J. Ind. Manag. Optim. 13(3), 1169–1187 (2017)

Acknowledgements

The authors would like to thanks the referees for their comments and suggestions that led the paper into the current form.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors declare that they have no conflict of interest.

Ethical approval

This article does not contain any studies with human participants or animals performed by any of the authors.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

About this article

Cite this article

Kumar, P., Behera, J. & Bhurjee, A.K. Solving mean-VaR portfolio selection model with interval-typed random parameter using interval analysis. OPSEARCH 59, 41–77 (2022). https://doi.org/10.1007/s12597-021-00531-7

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s12597-021-00531-7