Abstract

Efficient markets should guarantee the existence of zero spreads for total return swaps. However, real estate markets have recorded values that are significantly different from zero in both directions. Possible explanations might suggest non-rational behaviour by inexperienced market players or unusual features of the underlying asset market. We find that institutional characteristics in the underlying market lead to market inefficiencies and, hence, to the creation of a rational trading window with upper and lower bounds within which transactions do not offer arbitrage opportunities. Given the existence of this rational trading window, we also argue that the observed spreads can substantially be explained by trading imbalances due to the limited liquidity of a newly formed market and/or to the effect of market sentiment, complementing explanations based on the lag between underlying market returns and index returns.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

In this paper, we examine the evolving UK market for total return swaps based on the Investment Property Databank index. The total return swaps market is the first actively traded commercial real estate derivatives market and is part of a global trend to create hedging and derivatives vehicles for the real estate market. As at the end of 2009, IPD had recorded over 2,100 transactions with a notional value in excess of $35billion since the market’s initiation in 2004. Total return swaps involve an exchange of returns based on IPD returns and returns based on LIBOR plus or minus a margin or spread.

In contrast to the spreads found in, for example, equity index swaps, the spreads for real estate total return swaps have been large, hundreds of basis points. This paper, developing prior research for the Investment Property Forum (Baum et al. 2006), explores the reasons for such spreads. Are they a result of pricing inefficiencies and uncertainties in an immature market, or are they rational, given the nature of the underlying asset market and the problems involved in creating a self-financing arbitrage portfolio? To preview our findings, we will show that lagging effects, transaction costs and heterogeneity results in there being a rational “trading window” around the expected zero spread over LIBOR. Actual trades should occur within that window, with the position of the “consensus” trade depending on the balance between those seeking long and those seeking short positions which, in turn, is linked to asset market sentiment. As the market grows to achieve critical mass and liquidity, one might expect the width of the trading window to shrink.

We begin with a brief introduction to the total returns swap market, looking at the structure of the swap vehicle and at trading volumes. Next, we consider pricing principles in swaps markets and their applicability to the real estate market. We set out some of the reasons why the spread might vary from the expected zero spread and consider whether spreads might be time varying. Section four sets out our pricing model. We then present empirical results before drawing some general conclusions.

The Total Return Swaps Market

Commercial real estate was arguably, until recently, the only major asset class without a well-developed derivatives market. Early attempts to establish such a market in the United Kingdom were unable to achieve critical mass or trading volume. In particular, in the property forwards markets created on London FOX in 1991, lack of trading led to insider deals and cross-trading to present the illusion of activity.Footnote 1 The failure of FOX was damaging for the development of a market for property derivatives, blighting attitudes of investors and regulators alike. Allied to regulatory constraints and unfavourable tax treatment which, in large measure, excluded institutional investors from participating in such markets, this meant that there was little activity during the 1990s, despite the work of energetic advocates from the industry.

In 1994 BZW launched Property Index Certificates (PICs), later rebranded as Property Linked Notes. PICS are structured as Eurobonds and, if acquired at par, effectively replicate IPD returns (less dealing fees and spreads), although any exit before maturity may result in a tracking error. Trading volumes were modest. The UK property industry continued to seek a derivative vehicle that would facilitate strategic and tactical portfolio management and enable investors to alter their exposure to real estate quickly and without incurring high transaction costs or being exposed to public market price volatility. However, attempts were hamstrung by regulatory restrictions, tax treatment and by concerns about the nature of the underlying property market indices.

Industry groups continued to lobby the Government for a relaxation of the constraints on investment in, and trading of, commercial real estate derivatives, making progress at the turn of the century. In 2002, the Financial Services Authority confirmed that life insurance companies could use property derivatives for efficient portfolio management. Taxation issues were largely resolved in 2003, when the Inland Revenue announced that property derivatives would fall into the ‘standard’ derivatives regime, confirmed in the 2004 Finance Act. Finally, the 2004 FSA collective investment scheme sourcebook allowed authorised retail and non-retail funds to hold property derivatives as investments. By 2005 most of the regulatory restrictions on the development of a property derivatives market had been lifted.

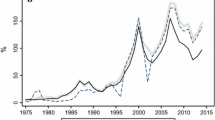

Commercial real estate index total return swaps have been traded in the UK since early 2005, once regulatory issues for institutional investors were resolved. During this period, a degree of standardisation of commercial terms has occurred. It is the standard form of total return swap commonly traded in the inter-bank market which is the focus of analysis in this paper. The UK market grew very rapidly, with outstanding notional principal passing the £1billion mark by the end of 2005, £6billion by the end of 2006, £9billion by the end of 2007 and £11billion by the end of 2008 (Fig. 1). By Q4 2009, over 2,000 trades had been executed with a notional value in excess of £22bn. Although trading volume fell as underlying asset market conditions worsened, there were still over 800 trades in 2008 and around 450 in 2009. In 2009, an IPD-based property futures contract has been listed on Eurex, although reported volumes are low.

UK total return swaps trading volumes

Developments in the UK form part of a wider global move towards the creation of property derivatives. In the US market, the development of derivative products in the real estate market is also quite recent, although the first real estate-linked swap was launched in 1991. Fisher (2005) describes a total return swap announced and to be offered by Credit Suisse First Boston (CSFB) in the USA. NCREIF index swap closing levels are now available on-line but, anecdotally, trading volumes remain thin. In 2006 Real Capital Analytics and MIT announced a set of indices tracking US commercial property prices which were designed to be the basis for derivative trading. CMBS Swaps have existed for some time, based on the Bank of America CMBS indices. In 2006, the S&P CME housing futures and options contracts were launched in Chicago, based on the Shiller-Weiss indices. More recently, it was announced that US real estate index trading would not be subject to the Foreign Investment in Real Property Tax Act, opening up the possibility of more active non-US trading. There is an active Listed Property Trust futures contract on the Australian Stock Exchange, there are exchange traded products based on the EPRA indices, residential property derivatives have been traded in Switzerland and Sweden and commercial real estate total return swaps based on IPD indices have been traded in Australia, Canada France, Germany and Japan.

The basic structure of the UK property return swap is as an over the counter contract for difference where parties swap an annual Investment Property Databank (IPD) commercial real estate total return index for an interest rate product. In the initial development of the total return swaps market, the standard contract was based on 3 month LIBOR plus or minus a spread (or margin) expressed in basis points. The IPD leg accrued over a calendar year and settled on the last business day of the March following the year end. The LIBOR leg accrued over a 3 month period corresponding to calendar quarters settling on the last business day of the quarter (that is, the last business days of March, June, September or December). More recently, there has been a shift towards a simplified annual contract / fixed interest basis but here we analyse the original contract since the spreads reported in the market place reflect that structure.Footnote 2

Deviations from these cashflows may occur at the start of a swap. The initial index level used to calculate the first IPD cashflow is, by market convention, the most recently published IPD monthly estimate of the annual total return. These indices are typically published two weeks after the end of each month. This has the effect of giving the swaps a retrospective start date of between 2 and 6 weeks. The LIBOR leg starts to accrue on the same date as the IPD leg. To fit with standard quarterly settlements, the first LIBOR payment may be in the form of a 1 or 2 month short-stub or, very occasionally when a payment would be due before the trade date, a 4 month long-stub. In these cases the relevant 1, 2 or 4 month LIBOR rate is used.

There are a number of significant differences between this structure and most other forms of financial market swap. Most notable is the retro start. This is necessary, as there will always be a delay between the index date and the publication of the index for property whereas in equities or rates the initial index can be set at the moment that the trade is done. The settlement of the IPD leg is also affected by the delay in publication of property indices. The standard settlement for the IPD leg was at the end of March, reflecting the publication of the annual results.

Another significant difference is that the cashflows were not settled with the same frequency (see Fig. 2). There will be a number of LIBOR payments made before the first IPD payment is due. This does, in principle, give rise to both pricing and counterparty credit issues although most trades, while OTC, are backed by investment banks as the “effective” counterparties.Footnote 3

Total property swap structure. Typical buyer’s 2-year TRS structure representing positive (arrows going up) and negative (arrows going down) cash flows. This contract reflects the initial modus operandi of the UK market where the interest rate leg is linked to a variable interest rate (LIBOR) and a spread which, in this example, is set to be equal to 50 bps

The remainder of the paper focuses on the spreads above or below LIBOR. These have fluctuated considerably over the short life of the UK total return swap (Fig. 3 shows the evolution of margins across 2007 and 2008 as the market turned) and are increasingly treated as a forward indicator of property market returns. This is not the case for equity market index swaps where the spreads over LIBOR are very close to zero. Are the differences observed in real estate markets a function of the particular characteristics of the underlying asset class or do they represent some mispricing of risk and return in the initial development of the market?

Indicative UK IPD total return swap spreads over LIBOR

Swap Pricing Principles and Real Estate Markets

The starting point for a consideration of swap pricing comes from the literature on the pricing of interest rate swaps, which developed from the 1980s. Most contemporary pricing models are based on an arbitrage-free efficient market model where the price reflects the ability to create a self-financing arbitrage portfolio. Swaps are thus typically modelled as a portfolio of “swaplets”—typically either as a series of short-term interest forward contracts or FRAs or by the investors going long in a floating bond and short in a fixed rate bond (see reviews in Minton 1997, or Klein 2004, for example). Two broad interrelated controversies emerge from the literature: one concerning the extent to which swap prices are consistent with interest forward and future prices, the other concerned with counter-party risk.

Analysis typically draws on price data from interest rate forward and futures markets. These turn out to be incomplete in explaining swap prices. The gaps in explanation have been attributed to differential counterparty default risk (which, in turn, has been related to the “comparative advantage” explanation of the added value of swap contracts)—for example in Jarrow and Turnbull (1995). The relevance of counterparty risk has been disputed and dismissed (see, for example, Litzenberger 1992; Collin-Dufresne and Solnik 2001). The loss on default from a swap is low compared to the underlying asset, since no principal is exchanged and treatment of swaps in default is favourable. Further, swaps are generally brokered by a market maker, who stands between the parties and, de facto, offers a guarantee. Swap prices are set at market levels and lower credit risk parties do not pay different rates to higher rated parties (although their access to the market may be constrained) ‘quoted swap rates do not reflect credit rating differences between the counterparties; i.e firms do not pay up to do swaps with highly rated counterparties’ (Litzenberger, op cit.). Credit risk differences are accommodated in a credit service annex and there is little variation in spread for similarly dated contracts.

The difference between swap rates and interest future rates has been explained in terms of differences in the cash settlement procedures of the two instruments. For example, Gupta and Subrahmanyam (2000) explain differences in the Eurocurrency futures curve and swap curves as resulting from a ‘convexity bias’ caused by marking to market adjustments in the futures market (which causes correlation between overnight interest rates and futures prices). After adjusting for these factors, the appropriate fixed rate for a swap contract eliminates any arbitrage opportunities, producing zero net present values on a risk adjusted basis. It should be noted that the pricing anomalies found by researchers with respect to convexity biases (and, indeed, counterparty default risk, if this is accepted) are very small.

Swaps are brokered, and the market maker will charge a small fee for setting up the deal and matching parties, for warehousing deals, for accepting inventory risk and to cover the (average) risk of counterparty default. The same applies to currency swaps, which, in principal, could be replicated with a series of currency forward agreements or futures. Arbitrage principles ensure that the spreads are very low.

In considering financial market swaps—for example, parties swapping returns based on an equity market index for LIBOR-based interest rate payments—the same arbitrage principles apply. While the equity market expected return might be higher than forward expectations of interest rates, the existence of an investible underlying asset anchors spreads around LIBOR to very low numbers. The investor receiving LIBOR can use the cashflow to support borrowing that, in turn, can be used to acquire the appropriate index tracking equity portfolio. Given that this is a riskless portfolio, the price of the interest rate leg should be set to ensure that the swap does not generate abnormal returns. There are transaction costs in acquiring the matching portfolio and carry costs in managing the portfolio, but, amortised over the life of the swap, these will be marginal.

A common principle here is that a riskless, self-financing portfolio can in practice be created by an investor. In all cases, a perfectly matched long/short position can be acquired with reasonably low transaction costs. As a result, expected cashflows can be discounted at the risk free rate, and differences in risk between the swapped assets become irrelevant. More importantly, differences in expected returns also become irrelevant. The only reason for a spread, then, relates to the costs involved in creating the position.

This principle forms the basis of the theoretical models of real estate derivative pricing introduced by Titman and Torous (1989), Buttimer et al. (1997), Bjork and Clapham (2002) and Clapham et al. (2006). Such models produce low to zero spreads over the matching interest rate return. Other authors have noted that drawing direct analogies with interest rate and equity index swaps is problematic. Park and Switzer (1996) note problems of basis risk (when the assembled portfolio does not track the market index); Okata and Kawaguchi (2003) note problems of swap pricing in incomplete markets where the underlying asset is indivisible, has high transaction costs, limited liquidity and unobservable fundamental prices. Patel and Pereira (2008) reintroduce the idea of counterparty risk: while Fabozzi et al. (2010) discuss forecast uncertainties and pricing.

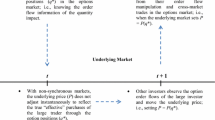

Of more direct relevance to this paper is Geltner and Fisher (2007)—hereinafter GF—who consider pricing issues for swap contracts based on real estate indices. They argue that real estate indices differ from conventional financial market indices since they are based on appraisals and because investors cannot hold the underlying portfolio. They suggest that the appraisals have two impacts on the index—introducing noise and lagging effects. Noise comes from random deviation between reported index values and the “true” prices of the underlying market—this is said to add short-run volatility to the index and to induce some negative autocorrelation. Lagging effects are more significant in their model—they present a standard appraisal adjustment model which smoothes market volatility, causes the index to lag behind actual property prices perhaps resulting in momentum effects. Given that the underlying index cannot be traded, they argue that these factors must be accounted for in any equilibrium pricing model. Their pricing model starts by examining the pricing of a forward contract. They show that standard pricing results rely on the index reflecting the current equilibrium expected returns in the underlying market and the ability to hold an arbitrage portfolio—conditions that do not hold in real estate markets with appraisal based index number series. They also note that the index risk premium may be lower than the required risk premium in the underlying asset market, due to smoothing effects. Further, momentum effects may mean that the short- to medium-term expected return on the index may differ from its equilibrium required real return.

They then determine a feasible trading range by considering the position of a bullish investor taking a long position and a bearish investor taking a short position. The investor going long may expect higher growth in the index than would be necessary to deliver the equilibrium return: thus the bullish investor will be prepared to pay LIBOR plus the additional growth anticipated plus (or minus) any lag effects from the index construction process. The investor going short may hold a portfolio which she believes could deliver positive alpha—returns greater than those delivered by the index. She too will have a growth expectation which may differ from that of the bullish investor. The two trading conditions define a feasible trading window. If both parties have the same expectations, then the only feasible trading price is a point which is defined by the underlying interest rate and the index lag effect. But if growth expectations differ or if the investor shorting the market feels that her portfolio can deliver alpha, then a range of feasible positions emerge. The paper implicitly suggests that the contract price will be a rate that is a midpoint between the minimum and maximum prices in the trading range, after allowing for a bid-ask spread to pay for brokerage and other dealing costs.

Baum et al. (2006) made very similar arguments, concluding that the spread from property index total return swaps should, in principle, be close to zero but that underlying asset market efficiencies make trading at non-zero spreads rational—that is, there are motivations and real gains for going long or short in real estate using a derivative rather than trading in the underlying market. While the margins should not reflect return differentials between LIBOR and expected real estate returns once risk is accounted for, there are rational reasons why margins should exist. Are these asset market differences sufficient to explain the large spreads (and their changes in signs) observed in practice?

The starting point for our conceptual model of swap pricing builds from GF’s (2007) lag model and starts from four basic principles. First, that the equilibrium spread does not reflect differences in expected returns. This is consistent with swap pricing in other markets—although the anecdotal evidence in Baum et al. (2006) suggests that many market participants based their investment decisions on return differentials and forecasts of property market performance. Second, that arbitrage and covered trades should ensure that “normal” spreads are zero (or no more than the difference between LIBOR and the borrowing costs of the representative investor). Third, that swap contracts are not negotiated between counterparties, but are arranged by a swap dealer, such that counterparty risk issues are dealt with outside the swap contract and, hence, do not affect spreads. Fourth, any non-zero spreads reflect underlying real estate asset market distortions and inefficiencies. The focus, then, is on the nature of the underlying real estate market and its impact on the ability to construct a self-financing arbitrage portfolio.

We analyse a number of constraints facing an investor operating in the underlying real estate market. These are the existence of high transaction costs in the private market (for UK direct real estate acquisitions, round trip costs of around 7.5% can be assumed with higher entry costs than exit costs due to up front tax costs through stamp duty); execution time (acquiring (and selling) real estate involves a search process which could easily take 6 months, and a time to transaction which is also lengthy); tracking error and basis risk (due to lot size issues and heterogeneity, it is very difficult to track the underlying index; indirect real estate vehicles which may reduce some of the liquidity and transaction cost problems may be subject to greater tracking error); and differences in cashflow timing between the underlying portfolio and the swap contract.

Finally, we note that an actual arbitrage portfolio would be subject to management obligations and costs which should be, but are not necessarily, reflected in the published IPD returns and that—other than the total returns swaps under consideration—there are no effective ways to short the commercial real estate market. Taken together, these factors mean that, in the absence of a simple to construct, reliable self-financing arbitrage portfolio, the institutional characteristics of the underlying asset market may be significant in determining traded spreads.

These characteristics of the underlying asset market are neither symmetrical nor time invariant. Some appear symmetrical—the tracking error / basis risk problem faces buyer and seller, the portfolio management obligations are a symmetrical cost and saving. Others are quasi-symmetrical. Both parties would face round trip transaction costs, but the acquirer faces higher initial costs than the seller (hence the NPV of the buyer would be less than that of the seller). Heterogeneity creates asymmetry. Sellers cannot recover their original portfolio, a risk not faced by a buyer. Asymmetries in relation to execution time vary over the market cycle. In a rising market, the buyer, unable to get into the market, faces a loss of upside return. In a falling market, the illiquidity facing a seller locks in losses and poor returns.

One other reason for the existence of margins is the belief on the part of investors that their portfolio can generate abnormal returns or alpha. GF include this in their formulation of a fair trading range. If the investor does believe that her held portfolio can generate positive risk-adjusted returns despite adverse market conditions, she may chose to short the market while retaining the real estate assets: she will be prepared to pay a premium up to the value of alpha to hedge market real estate returns. While the market remains wedded to the concept of alpha, empirical evidence of its existence is weak—for example, Bond and Mitchell (2008) found no strong statistical evidence of persistent or significant fund manager out-performance in an analysis of UK professional fund managers.

The lagging issue identified in GF is clearly significant for short time horizons, particularly in a US context with the stale appraisal problem evident in the NCREIF index, but may be less of an issue in the UK swaps market with annual based contracts and an annual sample that is 100% valued each period. How predictable, though, are UK IPD commercial real estate returns and how significant are the lagging effects? The IPD index does, indeed, exhibit serial correlation—over the 1981–2007 period, the all property index has a first order autocorrelation of 0.357, which is just statistically significantly different from zero and indicates that around 13% of the variation in current returns can be explained by the previous year’s returns, but that is around half the serial correlation exhibited by NCREIF over the same period. Given that the lagging effect is well known, one might expect that it would reflected in short-run forecasts of property market performance. However, examination of the Investment Property Forum’s consensus forecasting service shows that the accuracy of forecasts 1 and 2 years out is poor—for 2003–2007, the mean absolute error for the 1 year out forecast is 10.9%, rising to 11.4% for the 2 year out forecast (see Fig. 4).

Real estate market forecast accuracy

The implication of these imperfections in the underlying market is that it may be rational at certain points in the market for a party in a real estate total return swap to pay a margin above (or below) LIBOR even in the absence of lagging effects. Thus a property owner, wishing to reduce exposure to the real estate market for a period, but also wishing to retain their assembled portfolio might be prepared to pay IPD and receive LIBOR minus a margin to avoid both transaction costs, delays in execution of sales and the problems of rebuilding the portfolio. An investor wishing to gain short term exposure to UK real estate may be prepared to pay LIBOR plus a margin to avoid round trip transaction costs, and that margin might be higher if they are confronted with difficulties in gaining exposure in the underlying market through supply constraints or long execution times.

What this implies is that there is a rational trading window around the zero spread equilibrium position. Actual trades should occur within the trading window and, if there is critical mass, liquidity and a balance between buyers and sellers of the IPD leg, one would expect that trades would occur close to the zero spread. However, in a nascent swaps market that is immature, with restricted liquidity and, critically, with an underlying asset that is cyclical in nature, that balance between buyers and sellers (those wishing to go long versus those wishing to short the market) is likely to be disturbed. As a result the shape and position of the trading window will shift over time. It should be emphasised that this is not (primarily) as a result of differences in return expectations, but rather results from changes in the numbers of participants prepared to pay a premium over LIBOR to those prepared to accept a discount to LIBOR. In this restricted sense alone, the spread observed will reflect market sentiment and return forecasts.

In the remaining sections of the paper, we seek to estimate the size of the window using a cashflow-driven model that makes plausible assumptions about the behaviour of the underlying market. In this, we recognise that many of the characteristics of fully efficient markets used in theoretical swap pricing models (that generate closed form solutions) are violated. Underlying cashflows are discrete, not continuous; there are high costs in trading, the underlying asset is not (easily) divisible, it is not possible to perfectly replicate portfolios and it is not easy to short-sell the underlying asset. We next set out the pricing model used (and the assumptions made) before reporting empirical results.

The Pricing Model

GF explicitly consider the appropriate margin for a real estate swap in the context of an appraisal-based index and without assuming a perfect arbitrage situation, where the returns from the index are reproducible (or, equivalently, where the reported index returns reflect the equilibrium in the underlying property market). Their representation starts with a covered trade where the investor taking the long position in real estate holds a bond or cash position that generates LIBOR and the investor taking the short position holds a real estate portfolio that comprises properties similar to those in the index. They consider a swap which is based on a capital appreciation index: here, we reproduce their argument, but for a total return swap. The starting position is the standard, risk neutral, position that the required (fixed) interest rate on the swap F is equal to the risk free or LIBOR rate i. However, the F = i equality may not hold where the index is appraisal-based.

The equilibrium return for the average property tracked by the reference index is:

where E E represents an equilibrium expectation, i is the risk free or LIBOR rate and RP p is the risk premium for the property. If the index were to track the underlying property then, in expectations, the index return r n :

However, if the index is appraisal based, then lagging and smoothing become issues. Specifically, the moving average nature of the appraisal-based index return results in lower risk, such that:

In equilibrium, E(r n ) = E E (r p ), so that the differences vary over time but equalise in the long run. GF argue that the same lag biases that cause risk differences also create momentum effects so that E(r n ) can differ from E(r p ) and hence from E E (r n ) at any given time. The sum of the lag effects is given as:

where M is a transient, time-varying momentum term.

Given these momentum effects, GF are able to derive feasible trading positions for the long and short positions. Without reproducing the derivations, they show that the trading condition for the holder of the long position is:

where L is the lag effect from the appraisal smoothing and B L represents the belief that the holder of the long position has about “abnormal” return.Footnote 4 Clearly, if L = B L = 0 then F = i, which is the standard risk neutral, fair price representation. In similar fashion, the trading condition for the holder of the short position is given by:

Where α is the short investor’s belief that her portfolio will earn abnormal return (alpha) and BS is her expectation of abnormal negative growth in the returns index.Footnote 5 As before, with L = α = B S = 0, then F = i. Overall, then, this creates a trading window:

If the owner of real estate has no expectation of alpha and there are no differences in expectation of abnormal growth, the interest rate for the short leg will be equal to the risk free rate plus the lag or smoothing effect. The average value of alpha must be zero (and, strictly, an investor taking the long position might also have a belief that their investment skills could “add alpha” to a directly held portfolio which they forgo by taking the long position in the swap).

GF then discuss the impact of bid-ask spreads and the willingness of investors to pay them. In a liquid and mature market, competition between intermediaries will drive down margins. They also note that there are circumstances where investors on one side of the swap will be more prepared to accept larger spreads than those on the other—as an example, they cite a situation where the holder of the short position is only willing to pay 50 bps, perhaps because they are concerned about noise in the index and basis risk, while the holder of the long position is prepared to pay 100 bps: the net effect is that the midpoint would now be 25 bps above the equilibrium margin. These effects would occur where there are imbalances in supply and demand, a greater (or lesser) proportion of investors seeking to hold the short position rather than the long position. Thus situations where F is significantly different from i could result from either lag/momentum effects or from market sentiment effects in markets that are not fully liquid—or a combination of both of these factors. In their model, the observed margins are mid-point trading prices, that is

Our paper extends this model by focussing on the trading window effects that result from market frictions in real estate. We argue that holders of long and short positions have incentives to pay (receive) margins that result from the structure of the market and that are independent of the lag and momentum effects. Specifically, we examine three issues: transaction costs, execution time and timing of cashflow. If the impacts of these factors were symmetric then they would cancel and the appropriate interest rate (in the absence of systematic alpha or systematic differences between B S and B L ) would be \( F = i + L \). However, we argue that there are asymmetric effects that alter this conclusion.

First, consider transaction costs. Buying and selling real estate incurs substantial transaction costs. In the UK, it is standard to assume round trip costs of 7.5%. However, these are asymmetric: acquisition costs of 5.5% and sales costs of 2.0% for example. The investor taking the long position saves these costs when compared to buying the underlying asset; the holder of the short position saves the costs compared to the sale and repurchase of the underlying assets.Footnote 6 Since the present value of the savings made in the long position exceed those made in the short position, the neutral position is shifted towards a higher value of F. For the long and short investors, respectively we have:

where TC L is the present value of the round trip transaction costs from gaining exposure to real estate over the swap period and TC S is the present value of the round trip costs of reducing exposure to real estate over the swap period, TC L > TC S . Thus, on average, F is shifted above i+L.

Execution time effects result from the fact that investment in private real estate is illiquid and may require a long period of time to be executed. Research from Bond et al. (2006) shows that the execution time (for sales) in a normal market is equal to 6 months to fix the price and another 3 months to complete the transaction, a total of 9 months. In a growing market, this would result in a loss of return for the buyer (and gain for the seller), with the converse true in a falling market. Suppose the property market is expected to deliver a return of 4.5% per quarter (3% capital growth and 1.5% income return). An investor acquiring real estate assets directly would miss out on 6 months of capital growth and 9 months of income return (while presumably receiving a cash return on the capital to be invested). An investor taking a long position in a swap contract, by contrast, receives instant exposure. The converse is true for the seller who receives (or is exposed to) 6 months of real estate growth and 9 months of income return, forgoing interest payments over this period . Since the losses and gains are largely offsetting, any asymmetries will relate to long run average growth and, on a time-varying basis, to the lag and momentum effects. Hence for long and short positions:

where ExC L and ExC S are the costs associated with time to execute for buyer and seller respectively. With no trending or momentum effects, ExC L = –ExC S and there is no impact on F. With long run capital growth and no momentum, ExC L is negative, ExC S is positive and F is higher than i. Momentum effects will be sign dependent.

Cash flow timing may be important where a mismatch between swap contracts and private investment in real estate exists. A swap contract pays a total return at the end of each year, while a private real estate investment generates a quarterly in advance cash flow (under the standard UK commercial lease contract), while the capital gain is only realised when the property is sold (notionally when the swap contract ends). These cashflows create effects that operate in opposite directions. First, in a TRS, income-type cash flows are pushed backwards in time at the end of the year (resulting in a negative effect for the long position and a positive one for the short position). Second, however, the cash flow related to the capital gain (which is, on average, positive) is pushed backward if a player invests directly in real estate (i.e. a swap contract would generate capital gains/losses every year). These effects respectively tend to diminish and increase (in absolute terms) as the length of the contract increases. The nature of this double impact (trade-off) does not allow us to make any inference as to the expected sign of the spread.

To see the impact of these effects, we start by assuming that L = 0 and focus on the trading window that relates to frictions and inefficiencies. We then reintroduce smoothing effects. We utilise a risk-adjusted cashflow model that is akin to a certainty equivalent approach.Footnote 7 To our knowledge, few articles have applied the certainty equivalence approach in a real estate context, for example to estimate systematic risk (Brown 1988), to examine portfolio allocation decisions (Fugazza et al. 2009) and for real estate development pricing (Sing 2001). Other studies in the derivatives literature have already used the concept of certainty equivalence to price different products, such as firms in business damage cases (Boudreaux et al. 2000), weather derivatives (Lee and Oren 2009), and volatility swaps (Grasselli and Hurd 2007).Footnote 8

Our basic model to price total return swaps—with the main assumptions reported in Table 1—refers to the initial standard contract with a quarterly LIBOR cashflow (negative for the buyer and positive for the seller) and an annual total return cashflow for property (positive for the buyer and negative for the seller). The Net Present Value (i.e. NPV from now onwards) can then be represented as follows:

where:

-

NPV swapB = net present value of a swap contract for a buyer;

-

CE[TR i ] = certainty equivalent annual total return at time i;

-

LIBOR i-1,i = quarterly LIBOR rate between time i-1 and i;

-

SwapFee = annual fee for the swap contract (expressed as a percentage of the contract value)Footnote 9;

-

Spread = annual spread to be added/subtracted to the LIBOR rate (i.e. price of the swap contract as reported in financial markets);

-

NV = nominal value of the swap contract.

-

N = duration of the contract

The above equation—which represents our base case scenario—shows that, at each time i, the buyer of a swap contract will receive the net payment of the total return as recorded by the IPD index (i.e. once a year) minus the LIBOR rate, a swap fee (normally equal to 0.05% of the nominal value) and a spread, which represents the price agreed between the two parties. The net cashflows are then discounted at the LIBOR rate, which is the rate at which we discount certainty equivalent cashflows (with risk-free assets which do not need any certainty equivalence adjustment) assuming LIBOR is the proxy for our risk-free rate (RFR). We also decide to exclude counterparty default risk spreads because they are normally settled in a separate contract and they would also contradict the assumption of market efficiency.

Furthermore, we can represent the NPV of a swap contract from the seller’s point of view as follows:

where NPV swapS = net present value of a swap contract for a seller, with remaining terms as previously specified;

Consistent with market efficiency, the expectation, in the absence of market imperfections, is that the NPVs will be zero and that neither short or long party gain from the transaction. In our modelling exercise, we opt to use the certainty equivalence of annual total returns in a discrete time framework and manage to replicate the results of zero NPVs with efficient markets as for the continuous time model previously used in real estate literature. Our approach is more intuitive and easy to understand and apply in a new market. It also avoids assumption of a continuous time, frame which, cannot be maintained given the nature of the underlying market and the structure of swap contracts (especially for products linked to subsectors of the overall real estate market, e.g. sectoral or regional indices).

We can now prove that, under the assumption of market efficiency, we obtain a zero spread. Firstly, we know that the certainty equivalent cashflow can be proxied by the difference between annual total return (TR) and a risk premium (RP)—because TR = RFR + RP. This measure would consequently be equal to a riskless cashflow that can be proxied by LIBOR and Eq. 2 is reduced as follows:

For this to equal zero, the swap fee and the spread need to be zero—which is what would be assumed to hold in an efficient market. In practice the swap dealer will require a return for matching clients, warehousing risk and any counterparty risk costs. However, without market inefficiencies, our expectation would be for the spread to be equal to zero. This discrete time result is consistent with the continuous time results found in, for example, Buttimer et al. (1997) or Bjork and Clapham (2002).

The principle here follows GF in assuming a covered trade. However, when investors buy private real estate, the net cashflow of their investment will differ for some factors we need to price in order to understand the spread a buyer/seller would be willing to pay/receive to bypass these market inefficiencies. In our analysis, we will investigate the impact of these inefficiencies on the ‘rational’ spreads of real estate total return swaps.

Transaction Costs

The first factor we consider is the existence of high transaction costs for private real estate investments (5.5% acquisition fee at the beginning of the investment and 2.0% selling fee at the end). The NPV from a buyer (or seller)’s point of view can then be represented as follows:

where:

-

NPV pretcB = net present value of private real estate investment (i.e. pre) including transaction costs (i.e. tc) for a buyer;

-

NPV pretcS = net present value of private real estate investment (i.e. pre) including transaction costs (i.e. tc) for a seller;

-

CE(TR i ) = annual total return at time i;

-

LIBOR i-1,i = quarterly LIBOR rate between time i-1 and i;

-

NV = nominal value of the investment in direct real estate (assumed to be equal to the nominal value of the swap contract).

-

SellFee = selling fee when the investor sells the investment (expressed in percentage of the investment value);

-

CE(CG 0,N ) = cumulative capital growth for the entire investment period (assuming a compounding effect on the nominal value to compute the selling fee);

-

AcqFee = acquisition fee when the investor buys the investment (expressed in percentage of the contract value);

-

N = duration of the contract

The difference between the buyer and the seller’s cashflow (apart from the inverted signs for the LIBOR and total return components) comes from asymmetry in timing of transaction costs and the 350 basis point difference between acquisition and sale costs. This factor becomes more significant the shorter the length of the swap contract.

In order to identify the boundaries within which it would be rational for an investor to trade, we simply equate Eqs. 1 and 3 for the buyer (or 2 and 4 for the seller) and solve for Spread.

Execution Time

Investments in private real estate is illiquid and execution periods can be lengthy. Research from Bond et al. (2006) shows that the execution time (for sales) in a normal market is equal to 6 months to fix the price and another 3 months to complete the transaction. From a financial point of view, in a growing market, this would result in a loss of return for the buyer (and gain for the seller), and, in a falling market, we would observe a loss of return for the seller (and gain for the buyer).

For example, suppose the market is expected to show a total return of 18% during the coming year. For simplicity we assume this performance is evenly spread throughout the year, giving us a total return around ~4.5% each quarter (composed of a 1.5% income return and 3% capital growth). If, at the beginning of the year, investors decide to buy a property, it will take them around 6 months to fix the price (during this time investors do not receive either income return or capital growth) and another 3 months to complete the deal. Investors would then have to suffer a loss of total return for 6 months and loss of income return for a further 3 months after the price has been fixed, somewhat offset by cash returns on the capital to be invested.

Consequently, since the effect of execution time on the swap contract pricing should be apportioned across the duration of the contract (through the annual spread), this factor will, once again, have a bigger impact for shorter contracts. When we account for the time to complete a transaction in private real estate markets, the NPV of a buyer (or seller) will be computed as follows:

where:

-

NPV preetB = net present value of private real estate investment (i.e. pre) considering execution time (i.e. et) for a buyer;

-

NPV swapS = net present value of private real estate investment (i.e. pre) considering execution time (i.e. et) for a seller;

-

LIBOR i-1,i = quarterly LIBOR rate between time i-1 and i;

-

NV = nominal value of the swap contract;

-

p = time necessary to fix the price (expressed in quarters);

-

k = execution time (expressed in quarters and including both period to fix the price and period to complete).

Cashflow Timing

The third factor differentiating the cashflows of a total return swap and the underlying investment in private real estate is their timing. If investors buy private real estate, they obtain a quarterly cashflow for the income part (i.e. rents minus costs) and will only cash in the capital gain at the end of the investment period (when they sell the property). Correspondingly, if investors were to sell private real estate (assuming they could do so by taking a short position), they would only have to pay (forego) quarterly cashflows for the income part (rents minus costs) and will only need to contribute the capital gain (if positive) at the end of the investment period. Furthermore, the annual total return payment (and hence the capital growth component) made on the swap is calculated on the fixed notional principal sum.

Consequently we can identify two effects, an income effect and a capital growth effect. With the former, for the direct property investment, income is brought forward since, in UK lease contracts rent is paid quarterly in advance. Thus the NPV should be higher for direct property than the long position in the swap, implying a negative spread. The nominal impact increases as contract lengths increase, but the marginal effect decreases over time due to discounting effects (i.e. we expect a negative annual spread decreasing in absolute values over time). The position of the seller of a swap contract would be mirroring the one just described for the buyer.

Capital growth effects are more complex. For direct property investment, the capital gain is only paid on sale of the building at the end of the holding period. By contrast, the swap contract pays total return annually, the total return including the capital growth component. This might seem to benefit the holder of the swap contract. However, the swap contract pays total return on the nominal or notional principal of the swap contract, which is fixed. Growth for the direct holder of the real estate is compound (and, indeed, the income return is based on the capital value at the start of the year, so there is a gain when markets are trending upwards). Where capital returns fluctuate above and below zero, effects will vary. The swap contract benefits when there is a recovery after declining capital values (since capital growth is based on the fixed notional principal, not on the reduced capital value) and, relatively, from a negative return following a positive return (since the cash fall is magnified for the property owner by the prior growth). In a declining market, the holder of the swap experiences capital value falls based on the initial notional value; the property holder experiences falls based on the reducing capital value.Footnote 10

However, if we assume the reinvestment of realised capital growth on the swap contract, the holder of the long position can reinvest the capital to recreate the same position as the holder of direct real estate (for example buying a long position in another swap expiring at the same time). The swap buyer will then obtain both capital growth and income return on the capital component.Footnote 11 Consequently, the two effects of compounding capital growth and income return computed on the either larger or smaller capital value for direct property investment are cancelling and the only remaining effect is the one noted earlier—the differences in cashflow timing of the income component in the property investment than in a swap contract.

It is important to remember that in standard UK lease contracts the rent (and we also assume costs) is paid in advance. So the NPV of a buyer (or seller)’s point of view can then be represented as follows:

where:

-

NPV precftB = net present value of private real estate investment (i.e. pre) considering cashflow timing (i.e. cft) for a buyer;

-

NPV precftS = net present value of private real estate investment (i.e. pre) considering cashflow timing (i.e. cft) for a seller;

-

CE(IR i ) = quarterly income return at time i;

-

LIBOR i-1,i = quarterly LIBOR rate between time i-1 and i;

-

NV = nominal value of the investment in direct real estate (assumed to be equal to the nominal value of the swap contract).

-

CE(CG 0,N ) = cumulative capital growth for the entire investment period (assuming a compounding effect on the nominal value to compute the selling fee);

-

N = duration of the contract.

Smoothing Effects

If real estate markets were efficient and indices constructed using periodically recorded prices (i.e. same properties transacted at each measurement point in time), we may have observed asset prices moving as a random walk. Consequently, we determine the impact of considering a true random walk in the underlying market, as opposed to a smoothed total return (as from the IPD index series). When we account for the smoothing and momentum effects as in GF—the NPV of a buyer (or seller) will be computed as follows:

where:

-

NPV presmeB = net present value of private real estate investment (i.e. pre) considering the smoothing effect (i.e. sme) for a buyer;

-

NPV presmeS = net present value of private real estate investment (i.e. pre) considering the smoothing effect (i.e. sme) for a seller;

-

CE(unsmTR i ) = unsmoothed quarterly total return at time i;

-

LIBOR i-1,i = quarterly LIBOR rate between time i-1 and i;

-

NV = nominal value of the investment in direct real estate (assumed to be equal to the nominal value of the swap contract).

-

N = duration of the contract.

Since the effect of this inefficiency can only be seen if returns are not assumed to be deterministic, results accounting for smoothing effects are presented in a stochastic framework below, where the model used to (un)smooth real estate indices is described.

Empirical Results

Our analysis is based on a standardised, hypothetical contract with a nominal value of 1,000. This is analysed for different maturities from 1 to 10 years. We assume contracts are made and timed to begin at the start of a year. The main assumptions are set out in Table 1. Our modelling strategy aims to adopt a comparative static approach to isolate the impact of the individual institutional characteristics of the underlying market on the swap spread, before combining the factors together. We introduce a stochastic component for the underlying market values in a Monte Carlo framework based on real estate capital growth and income returns set to long run IPD (UK) averages with volatility and correlation structures based on historic performance. Within each run of the simulation, we smooth the index on which the swap is based, replicating the situation faced by an investor weighing the derivative and underlying market performance.

In developing the stochastic models, we assume that both real estate return and LIBOR rate follow a geometric Brownian motion (GBM). Total returns have an initial value of 100, average growth rate of 10.3% with a standard deviation of 10%.Footnote 12 The corresponding figures for LIBOR are 5.75%, 0% and 2%. Given the nature of the real estate (and swap) cashflows, we use a discrete time version of GBM:

where S t is the value of the asset at time t, Δt represents the discrete measurement period (i.e. a quarter in our case), and μ and σ respectively represent the annual expected rate of return for either total return or LIBOR and its annual volatility; and ε represents a single draw from the standard normal distribution taken in every discrete time increment Δt.

We assume that that the GBM generates an unsmoothed, but unobservable, version of the total return index. Consequently we use a standard first order auto-regressive filter to smooth the GBM path and compute the index values to be used in the simulation. Quan and Quigley (1989) defined the simple model from which Geltner (1989) derived the FOARF model applied empirically by Booth and Marcato (2004) to UK sub-annual returns. We follow this procedure and obtain smoothed total returns as follows:

where α refers to the autocorrelation coefficient, and unsmTR t and smoothTR t respectively represent the unsmoothed and smoothed total return at time t. Based on historic data, quarterly α is set to 0.65 with the immediately preceding returns set to the average return for annual or quarterly periods. We then run 1,000 simulations of this model for 1 to 10 year swaps and record the 5th and 95th percentiles and mean spread for each distribution.

As Fig. 5 shows, the behaviour of smoothed and unsmoothed series is similar, but with the unsmoothed values being clearly being more volatile. On average, the direct effects of smoothing dissipate quickly in stable market conditions. Even with a smoothing parameter of 0.65 on a quarterly basis, average buyer required premia for momentum effects alone fall to around 30 bp in the fourth year, with seller premia showing a similar sharp fall and never exceeding 81 bp. However, there is a considerable spread of possible values around those averages. Figure 6 shows two of the 1,000 simulations: the smoothing/momentum effects vary markedly, while the transaction cost effects are relatively stable. Momentum effects may be more pronounced in cyclical rising and falling markets.

Example of Unsmoothing Effect on Total Returns. Panel a GBM of Total Return Index vs. Smoothed Index. Panel b Smoothed vs. Unsmoothed Total Returns The simulation randomly chooses geometric Brownian motion patterns for the real estate index. However, to correct for lagging and momentum issues the resulting patterns are smoothed. a reports the outcome of one of these simulations showing the difference of the smoothing process if either a quarterly or an annual index is considered. The analysis discussed in the paper refers to the quarterly frequency. b reports the same outcome represented in a, but showing returns rather than index levels with a quarterly frequency

Examples of smoothing effect on transaction costs pricing. The graphs above represent the impact of two different inefficiencies (smoothing and transaction costs) on the swap spreads. For each inefficiency we reported two separate outcomes of our simulation (graphs to the right and left) to show the different impact market cycles may have on the spread: transaction costs have a constant effect which is only slightly determined by the different market cycle; smoothing, instead, depends very much on the current phase of the cycle and the prediction of market players

Figure 7 shows the impact of transaction costs for both buyers and sellers. The impact is strongly related to the maturity of the contract. For a short dated swap, the impact of transaction costs is very pronounced: for a 1 year swap (that is, for an investor wishing to increase their exposure to real estate for a very short period), the ‘rational spread’ for a buyer may be as high as 800 bp. However, spreads fall sharply as tenor increases. Note that spread boundaries are asymmetric, reflecting higher initial acquisition costs in UK markets. The results show that ii is rational to trade within the “trading window” defined by the upper (buyer) and lower (seller) boundaries, with different investors prepared to accept margins between the two limits, the consensus spread reflecting the balance of supply and demand.

Spread boundaries with transaction costs in private real estate. The graph shows the maximum margin a buyer and a seller are willing to pay to enter a total return swap contract in order to avoid transaction costs: 5.5% acquisition costs and 2.0% selling costs. The spread is represented in basis points. The boundaries are given for 1 to 10 years long swap contracts

Figure 8 shows the rational spreads that emerge from execution times given normal property market conditions. The spreads are broadly symmetrical and fall with maturity as the impact of return differences in the early part of the contract are damped as the investment period increases: the required margin converges on a zero margin. For investors seeking to change their exposure to real estate in the short term (whether seeking to increase or decrease their exposure), it may be rational to accept a spread around LIBOR on a swap contract, when compared to activity in the underlying market.

Spread boundaries with execution time in private real estate. The graph shows the maximum margin a buyer and a seller are willing to accept to enter a total return swap contract in order to execute the transaction immediately (instead of waiting for the time needed to negotiate the price and to complete the deal). The spread is represented in basis points. The boundaries are given for 1 to 10 years long swap contracts

Figure 9 shows the impact of cashflow timing (recall that in our simulation model, we assume expected nominal capital growth of 4% and income return of 6.3% based on historic averages). As explained in section 4.3, if we assume capital growth components are reinvested, we are left with the income shift component.Footnote 13 Since for the direct property investment in the UK rent is paid quarterly in advance, income is then brought forward. Thus the NPV is higher for direct property than the long position in the swap, implying a negative spread. This can be seen clearly with the −21 bps spread for year one (both swap and owner receive capital growth at the same point). The impact increases as contract lengths increase, but the marginal effect decreases over time and it is equal to −16 bps for 10 year contracts.

Spread boundaries with cash flow timing in private real estate. The graph shows the maximum spread a buyer and a seller are willing to accept to enter a total return swap contract in order to adjust for differences in cash flow timing: quarterly income return and one-off capital appreciation. The spread is represented in basis points. The boundaries are given for 1 to 10 years long swap contracts

The results of combining the three real estate market characteristics of transaction costs, execution time and cashflow timing are shown in Fig. 10. The resultant window shows very wide plausible margins for short maturities (particularly at the very short end, 1 or 2 year contracts), strong asymmetry and a rapid convergence towards low margins as maturity increases. For short maturity contracts, transaction cost effects are very important with the buyer boundary indicating positive spreads. Cashflow impacts, however, become more significant with longer tenor contracts, with the buyer boundary falling below zero for contracts greater than 6 years.

Spread boundaries with combined effects (excluding smoothing effects). The graph shows the maximum spread that a buyer and a seller are willing to accept to enter a total return swap contract in order to avoid transaction costs (round trip 7.5%), to adjust for differences in cash flow timing, and to complete the transaction immediately. The spread is represented in basis points. The boundaries are given for 1 to 10 years long swap contracts

Figure 11 shows the combined effects of the various market inefficiencies, including appraisal smoothing allowing for stochastic returns and LIBOR. Panel A shows the average spreads for an investor buying IPD and an investor selling IPD, along with the area bounded by the 5% and 95% quantiles from the simulations. For short contracts, there is considerable disparity in the average values. However, there is equally considerable variation in required spreads for the short-traded contracts, creating sufficient overlap for trading to occur, even allowing for momentum effects. Required spreads, however, do converge quickly as maturity increases.

Combined Market Factor Effects with Stochastic Returns. Panel A: Average Spread and [5%–95%] quantiles. Panel B: Buyer and Seller Average Spreads and Mid-Point (including smoothing effect)

Panel B shows the average required spreads for both buyer and seller, with a “mid-point” spread shown. The mid-point would reflect the expected trading position if the market had frequent trades and a balance between investors seeking to buy and those seeking to sell. In practice, as the market evolves, the actual trading position is more likely to reflect imbalances in demand and might occur anywhere in the trading window. Panel B also demonstrates that the spread window is asymmetric: the buyer is prepared to pay a larger premium to avoid transaction costs and tracking error than the seller is prepared to concede to avoid having to sell and repurchase their reference portfolio. Required buyer spreads fall to less than 120 bp from the seventh year, while seller spreads reduce to close to zero over the same period. To some extent, such asymmetries will be institutionally determined, with UK commercial property transaction costs falling disproportionately on the buyer.

Conclusions

This paper examines the evolving total property return swaps market, focusing on the pricing of swaps and the margins above and below LIBOR that are observed in the market. These have been both volatile and large. Theoretical analyses of swap spreads and the experience of financial swap contracts (e.g. equity index swaps), by contrast, suggest that the expected margin should be zero or close to zero. Participants in the market have suggested that the high observed margins are a function of expectations about market returns (which thus explains the high negative spreads observed from the third quarter of 2007 and across 2008). However, this should present arbitrage opportunities for investors who can create an arbitrage portfolio in the underlying market (actually or synthetically).

This paper develops Geltner and Fisher’s (2007) model of a trading window, which, for them, reflects momentum effects and buyer-seller willingness to accept spreads that differ from the “fundamental” price of the swap. We develop that argument by suggesting that it is institutional characteristics in the underlying market that lead to the possibility of “rational” spreads around LIBOR, particularly for short maturity swaps. We show, using a certainly equivalent, cashflow approach, that transaction costs, execution times and, to a lesser extent, cashflow patterns in the underlying market mean that it may be rational for an investor seeking to change their exposure to real estate to pay a margin above (below) LIBOR rather than buying (selling) the underlying real estate asset. This result holds without making any assumptions about predictability of returns or tracking error. This creates a “rational” trading window with upper and lower bounds, within which individual investors might trade. The width of the window is large for short maturities, but quickly shrinks to the theoretically-expected low margins as maturities increase.

Given the existence of this rational trading window, we argue that the observed spreads can substantially be explained both by the short-run momentum effects suggested by Geltner and Fisher and by differences in the numbers of investors seeking to go long versus the numbers of investors wishing to short the market.Footnote 14 Imbalances will be a feature of an evolving market where there is restricted liquidity, lack of critical mass and restrictions . It will also be a feature of a market where there are periods of strong common market sentiment (which might also be linked to serial correlation and persistence in commercial real estate markets, exacerbated by the valuation-basis of the reference index in the market).

This paper, then, helps to reconcile theoretical research that suggests that the spread on a real estate total return swap should be zero or close to zero with the empirical observation that swap spreads are both large and volatile and the persistent market practitioner belief that the margins for different maturities reflect expected return differences and that they thus act as a forecast of property market performance. It is the balance between buyers and sellers within the rational trading window that drives the margin set in the market.

Notes

The move to a fixed interest rate does not alter the basis of our analysis since investors could easily have swapped out the floating LIBOR payments for fixed in the interest rate swaps market.

In the aftermath of the credit crunch, the counter-party risk posed by investment banks does raise issues that merit consideration. However these fall outwith the concerns of this paper.

The Geltner-Fisher representation solves for a capital appreciation only index and hence includes an income return term. As we are dealing with a total return swap, we omit this term for simplicity.

In GF, Bs is subtracted as it is expressed as an absolute magnitude (i.e. it is assumed that Bs is always negative). We generalise the result for the short seller.

In effect, the holder of the short position is laying off beta exposure: the swap allows this to be done in a more cost effective and efficient way than an underlying transaction—using the swap for portfolio value insurance. Thus they would be prepared to accept a spread that was lower than the fundamental F. We are grateful to David Geltner for this point.

The swap fee is always equal to zero unless the NPV for the swap contract is computed to assess the impact of transaction costs. In this case, the annual swap fee is assumed to be equal to 0.05%.

For example, for two consecutive years with 25% falls in value, with an initial value of 100, in year two the swap pays out −25, while the property (having fallen to 75) falls by −18.75. The swap holder benefits from any recovery and from any positive income return.

We note, for future research, that there are practical limitations to the reinvestment approach given the lack of critical mass in the market place: investors would find it difficult to obtain small value long or short swap contracts that reflected any delivered capital gain. It would also require active management of the contract. Although swap fees would be incurred, they will be small as a proportion of the overall contract value. In a risk-neutral world, the investors could, of course, invest proceeds at LIBOR.

Higher volatilities were also tested—results are available from the authors.

We also computed the cash flow timing effect without any reinvestment assumption (results available from authors). For our simulations, our model assumptions are consistent with historic average return performance, giving on average positive capital return. As a result, we expect to see negative spreads both for players holding long and short positions, relative to the underlying property market, with spreads increasing with the length of the swap contract. Cashflow timing effects will be reduced (and may be positive) when returns fluctuate between positive and negative (or, at least, are low relative to LIBOR). However, if the market is pro-cyclical, as might be expected given the cyclical behaviour of real estate and smoothing effects in real estate indices, cashflow effects in the absence of reinvestment drive expected negative spreads.

Particularly as some institutional investors are not permitted to hold short positions.

References

Alvarez, L. H. R., & Rakkolainen, T. A. (2009). Investment timing in presence of downside risk: a certainty equivalent characterization, Annals of Finance, Forthcoming.

Baum, A., Lizieri, C., & Marcato, G. (2006). Pricing property derivatives: an initial review, London, Investment Property Forum.

Bjork, T., & Clapham, E. (2002). A note on the pricing of real estate index linked swaps, SSE/EFI Working Paper Series in Economics and Finance, No. 492.

Bond, S., & Mitchell, P. (2008): Alpha and persistence in UK Real Estate Fund Performance, Paper presented to the MIT-Maastricht Property Seminar, Maastricht, NL, December 2008.

Bond, S., Crosby, N., Hwang, S., Key, T., Lizieri, C., McAllister, P., et al. (2006). Liquidity in Commercial Property Markets, London, Investment Property Forum.

Booth P., & Marcato G. (2004). The dependency between returns from direct real estate and returns from real estate shares (with P. Booth). Journal of Property Investment and Finance, 22(2), 147–161.

Boudreaux, D., Ferguson, W. L., & Boudreaux, P. (2000). Analysis and valuation of closely held firms involved in business damage cases and application of certainty equivalence. Journal of Legal Economics, 9(3), 1–18.

Brown, G. (1988). A certainty equivalent expectations model for estimating the systematic risk of property investments. Journal of Property Valuation and Investment, 6(1), 17–41.

Buttimer, R. J., Kau, J. B., & Slawson, V. C. (1997). A model for pricing securities dependent upon a real estate index. Journal of Housing Economics, 6, 6–30.

Case, K., Shiller, R., & Weiss, A. (1993). Index-based futures and options markets in real estate. Journal of Portfolio Management, 19, 83–92.

Clapham, E., Englund, P., Quigley, J. M., & Redfearn, C. L. (2006). Revisiting the past and settling the score: index revision for house price derivatives. Real Estate Economics, 34(2), 275–302.

Collin-Dufresne, P., & Solnik, P. (2001). On the term structure of default premia in the swap and LIBOR markets. Journal of Finance, 56, 1095–1115.

Ehrhardt, M. C., & Wachowicz, J. M. (2006). Capital budgeting and Initial Cash Outlay (ICO) uncertainty. Financial Decisions, 18(1), 27–42.

Fabozzi, F., Shiller, R., & Tunaru, R. (2010). Property derivatives for managing european real-estate risk. European Financial Management, 16, 8–26.

Fan, G., Huszár, Z., & Zhang, W. (2009). Implications of assets comovement on real asset price and liquidity risk, Working Paper, Available at SSRN: http://ssrn.com/abstract=1441260

Fisher, J. (2005). New strategies for commercial real estate investment and risk management. Journal of Portfolio Management, 32, 154–161.

Fugazza, C., Guidolin, M., & Nicodano, G. (2009). Time and risk diversification in real estate investments: assessing the ex post economic value. Real Estate Economics, 37(3), 341–381.

Geltner, D. (1989). Estimating real estate’s systematic risk from aggregate level appraisal-based returns. AREUEA Journal, 17(4), 463–481.

Geltner, D., & Fisher, J. (2007). Pricing and index considerations in commercial real estate derivatives. Journal of Portfolio Management, special issue, 99–118.

Grasselli, M. R., & Hurd, T. R. (2007). Indifference pricing and hedging for volatility derivatives. Applied Mathematical Finance, 14(4), 303–317.

Gupta, A., & Subrahmanyam, M. (2000). An empirical examination of the convexity bias in the pricing of interest rate swaps. Journal of Financial Economics, 55, 239–279.

Hazen, G. (2009). An extension of the internal rate of return to stochastic cash flows. Management Science, 55(6), 1030–1034.

Hennessy, D. A., & Lapan, H. E. (2006). On the nature of certainty equivalent functionals. Journal of Mathematical Economics, 43(1), 1–10.

Jarrow, R., & Turnbull, S. (1995). Pricing derivatives in financial securities subject to credit risk. Journal of Finance, 50, 53–85.

Klein, P. (2004). Interest rate swaps: reconciliation of models. Journal of Derivatives, 12, 46–57.

Kruschwitz, L., & Löffler, A. (2003). Certainty equivalent in capital markets, Working Paper dp-272, Wirtschaftswissenschaftlichen Fakultät der Universität Hannover.

Lee, Y., & Oren, S. S. (2009). An equilibrium pricing model for weather derivatives in a multi-commodity setting. Energy Economics, 31(5), 702–713.

Litzenberger, R. (1992). Swaps: plain and fanciful. Journal of Finance, 47, 831–850.

Minton, B. (1997). An empirical examination of basic valuation models for plain vanilla US interest rate swaps. Financial Economics, 44, 251–257.

Otaka, M., & Kawaguchi, Y. (2003). Hedging and pricing of real estate securities under market incompleteness, mimeo, Meikai University Working Papers Series.

Park, T., & Switzer, L. (1996). An economic analysis of real estate swaps. Canadian Journal of Economics, 29, S527–S533.

Patel, K., & Pereira, R. (2008). Pricing property index swaps with counterparty default risk. Journal of Real Estate Finance and Economics, 36, 5–21.

Quan, D. C., & Quigley, J. M. (1989). Inferring an investment return series for real estate from observations on sales. AREUEA Journal, 17(2), 218–230.

Sing, T. F. (2001). Optimal timing of a real estate development under uncertainty. Journal of Property Investment & Finance, 19(1), 35–52.

Syz, J. (2008). Property derivatives. Chichester: Wiley.

Titman, S. D., & Torous, W. N. (1989). Valuing commercial mortgages: an empirical investigation of the contingent-claims approach to pricing risky debt. Journal of Finance, 44(2), 345–373.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Lizieri, C., Marcato, G., Ogden, P. et al. Pricing Inefficiencies in Private Real Estate Markets Using Total Return Swaps. J Real Estate Finan Econ 45, 774–803 (2012). https://doi.org/10.1007/s11146-010-9268-x

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11146-010-9268-x