Abstract

Despite the extensive advancement of knowledge in the field of empirical asset pricing, little is known about how this literature applies to asset classes beyond common stocks and bonds. In this paper we apply recent developments in financial economics, which posit an important role for limited market participation and financial intermediaries, in understanding real estate returns. The risk factors motivated by these theories have significant explanatory power for the cross-section of REITs. However, this relationship is the opposite of what we expected, and the results point to a more complex set of findings that are difficult to reconcile with risk-based explanations. Our results suggest systematic mispricing of real estate assets that is heavily influenced by investor sentiment.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

We investigate whether a broad class of limited market participation models, including the intermediary asset pricing model, offer useful insights for real estate investors given the success of the models in asset classes beyond equities. For example, He et al. (2017) and Lettau et al. (2019) have shown that the equity capital ratio of primary dealers and the capital share of income, respectively, have significant explanatory power for U.S. stocks, treasury and corporate bonds, options, credit default swaps, commodities, and foreign currencies. Past attempts to apply standard asset pricing models to real estate have had mixed success.

In a frictionless economy described by Lucas (1978), households can perfectly diversify away idiosyncratic risk by trading in the financial market. As a result, a household’s consumption reacts only to systematic shocks to the economy; and consumption growth, which is perfectly correlated across households, provides a sufficient statistic of systematic risk that prices financial assets. While it is theoretically elegant and intuitively appealing, Lucas’s representative-agent consumption-based CAPM fails to a large extent to explain asset prices in empirical studies.

The failure of the standard consumption-based CAPM is not too surprising because the real economy is not frictionless. It is difficult to perfectly diversify away idiosyncratic labor income shocks because we cannot trade human capital. While an individual can borrow (save) when there is a negative (positive) labor income shock, most households face borrowing constraints. In addition, a large fraction of U.S. households own no stocks, directly or indirectly.

Guo (2004) incorporates these market frictions, i.e., idiosyncratic labor income shocks, borrowing constraints, and limited stock market participation, in an otherwise standard consumption-based CAPM.Footnote 1 Guo shows that the modified heterogeneous-agent consumption-based CAPM provides a coherent explanation for several well-known stock market stylized facts such as the equity premium puzzle, stock market return predictability, and excess volatility puzzle.Footnote 2 Shareholders are marginal investors in the limited participation model, and stocks are priced by shareholders’ consumption rather than by aggregate consumption.

Malloy et al. (2009) and Aït-Sahalia et al. (2004) find that shareholders’ consumption and luxury-goods consumption, respectively, provide a better explanation for the cross-section of stock returns than aggregate consumption.Footnote 3 While these empirical findings are encouraging, it is a challenging task to test the limited stock market participation model empirically because it is difficult to measure the consumption of marginal shareholders who are likely to be very wealthy and underrepresented in the Consumer Expenditure Surveys (CEX) used by Malloy, Moskowitz, and Vissing-Jorgensen (2002) advocate using the capital share of income to measure limited participation risk factor.

The intermediary asset pricing model is built on the premise that a financial intermediary is the marginal investor whose “consumption” sets asset prices. For example, in He and Krishnamurthy’s (2013) model, only sophisticated investors, i.e., financial intermediaries, can trade risky assets. Unsophisticated investors, i.e., households, can invest in risky assets only through a financial intermediary. While this assumption is clearly unrealistic, it might hold approximately, especially for complex assets. In addition, as in Guo’s (2004) limited participation model, He and Krishnamurthy (2013) assume that financial intermediaries cannot fully diversify away liquidity shocks because of borrowing constraints.

Limited participation models likely provide a better explanation for commercial real estate than the standard representative-agent consumption-based CAPM. Commercial real estate investment requires sophisticated and specialized knowledge, and is typically undertaken by institutional investors or high net-worth investors rather than retail investors. We investigate this conjecture using the empirical risk factors proposed by Vissing-Jorgensen (2002), Aït-Sahalia et al. (2004), Adrian et al. (2014), He et al. (2017), and Lettau et al. (2019). We also compare the limited participation models with traditional stock market factor models. To the best of our knowledge, this test has not been performed in the extant literature.

Much of the literature on real estate asset pricing has focused on equity REIT returns because of data availability and comparability to existing research methodology in financial economics. Following standard research practice established by Fama and French (1992), REITs along with other financial companies, are excluded from empirical asset pricing studies. This practice provides an opportunity to consider the extent to which recent advances in asset pricing can be applied to real estate. Furthermore, researchers have been able to exploit the unique regulatory requirements of the REIT structure to gain insight into real asset markets in a way that studies of common stocks do not permit (see Hartzell et al., 2010, Bond and Chang 2013 for discussion on this parallel markets concept).Footnote 4 Hoesli and Oikarinen (2012) also show the close connection between REIT markets and private real estate markets, which suggests that REIT asset pricing studies might be informative for real assets.

To preview our results, we find the financial intermediary risk factor, measures of limited stock market participation and traditional stock market factors are significantly priced in the cross-section of real estate returns. Moreover, these factors have a strong commonality; their economic information about REIT returns are subsumed by the luxury consumption factor of Aït-Sahalia et al. (2004). However, the sign of all these risk factors suggests a negative price for risk, which is the opposite of that expected.

Our explanation for this puzzling finding is that investor sentiment is an important driver of the REIT market. When investor sentiment is strong, stocks with lower past returns, low returns on assets, and negative earnings surprises are overvalued compared with stocks with high past returns, high returns on assets and positive earnings surprises. Because of short sale constraints, the mispricing is not corrected until the sentiment subdues. Our findings are consistent with those documented by Baker and Wurgler (2006), Stambaugh et al. (2012), and others that investor sentiment and short sale constraints jointly explains major stock market anomalies.

Our results also accord with recent theoretical result by Kozak et al. (2018). In the absence of near-arbitrage opportunities, sentimental demand can have significant effects on stock prices if it comoves with a systematic factor. Moreover, the risk price of investor sentiment can be positive or negative. Consistent with Kozak, Nagel, and Santosh’s conjecture, Stambaugh and Yuan (2017) show that mispricing factors explain the cross-section of stock returns. As we discuss in the next section, an extensive literature on real estate returns also points to investor sentiment as being a pervasive factor.

Section 2 reviews the related literature. Section 3 describes data. Section 4 presents empirical results. Section 5 discusses economic explanations of main findings. Section 6 offers some concluding remarks.

Related literature on REITs

The literature on REIT asset pricing has greatly expanded in recent years. Bond and Xue (2017) apply the investment-based asset pricing model to the REIT market. They show the importance of profitability and investment factors in both the time series and cross-section of returns. Van Nieuwerburgh (2019) considers the exposure to stock and bond factors in the time series of real estate returns. He also studies the HKM factor in the time series of REIT returns and finds that it provides little explanation for returns beyond that of the Fama and French (1992) five-factor model.

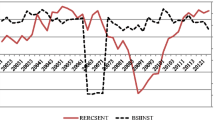

In terms of supporting the use of limited participation models for REITs, Chan et al. (1998) provide early evidence that institutional investors are more active in REITs than in common stocks. This represented a reversal of ownership patterns observed in the early 1990s. We provide updated evidence in Figs. 1 and 2, showing greater representation in terms of the number and percentage of institutional owners in REITs relative to common stocks. In particular, Fig. 2 shows that in 2016 the average percentage of institutional ownership for REITs is almost 80% whereas a sample matched on size and book-to-market for common stocks is around 65%. In both cases, the percentage ownership by institutional investors has accelerated since the early 2000s.

Number of Institutional Investor in REITs and Common Stocks. Notes: The solid line is the average number of institutional investors holding REITs stocks. The dashed line is the average number of Institutional investors that hold matched common stocks. For each REIT stock, one common stock is selected by the propensity score based on the market capitalization and the book-to-market equity ratio. The sample spans the 1987 to 2016 period

Percent of Institutional Investor in REITs and Common Stocks. Notes: The solid line is the average fraction of institutional investors that hold REIT stocks. The dashed line is the average fraction of institutional investors that hold matched common stocks. For each REIT, one common stock is selected by the propensity score based on the market capitalization and the book-to-market equity ratio. The sample spans the 1987 to 2016 period

Another set of literature has developed since the financial crisis that considers the tail risk of financial markets as a risk factor. Van Nieuwerburg (2019) examines the probability of disaster from Siriwardane (2015) and the financial fragility factor of Giglio et al. (2016). He finds that REITs load positively on the tail risk factor although the effect is reduced when standard factors such as size, value and momentum are included. Alcock and Andrilikova (2018) shows that a measure of asymmetric dependence is priced in the cross-section of REIT returns. In a contemporary paper, Boudry et al. (2019) show that REITs offer a hedge against the flight to safety risk of Baele et al. (2020).

A final related development in real estate asset pricing points to the role of sentiment as an important factor beyond traditional risk-based explanations for asset returns. Early works by Clayton and MacKinnon (2003) and Gentry et al. (2004) extended the literature on sentiment in closed-end fund discounts to REITs pricing relative to net asset value. Ling et al. (2014) find a positive relationship between measures of investor sentiment for private real estate markets and subsequent period real estate returns. However, long-horizon regressions show this sentiment is associated with possible mispricing. Das et al. (2015) show that the sentiment of institutional investors “spills over” from private real estate markets to public markets and highlights the role of economic conditions in determining the direction of this spillover.

Data and Methodology

The sample used in this paper consists of all equity REITs listed in the CRSP/Ziman database. The sample includes 436 distinct REITs traded on the NYSE, Amex, and Nasdaq exchanges from 1987 to 2016. In our sample, the market capitalization of all equity REITs grew from 8.5 million dollars to one trillion dollars and the number of REITs grew from 87 to 188. Data on REIT returns are from CRSP and the accounting data are from COMPUSTAT. Following Fama and French (1992), we construct REIT-based versions of the Fama-French three factors. Following Hou et al. (2015), we construct REIT-based investment and profitability factors. We obtain the Fama and French (1992) five factors and the risk-free rate from Kenneth French at Dartmouth College.

We construct the intermediary asset pricing factors following Adrian et al. (2014) and He et al. (2017). HKM is the He et al. (2017) equity capital ratio factor defined as the ratio of total market equity to total market assets (book debts plus market equity) of primary dealers. AEM is the Adrian et al. (2014) leverage ratio factor and is defined as the ratio of total financial assets to the difference between total financial assets and total liabilities of brokers and dealers.

Three empirical limited participation risk factors are employed in the empirical analysis. LUXCON is the year-over-year log changes in luxury sales that we construct following Aït-Sahalia et al. (2004). SHCON is shareholders’ consumption growth following Malloy et al. (2009). CS4 is year-over-year changes in the capital share of income proposed by Lettau et al., 2019).

For comparison, we also include several commonly used financial and macroeconomic risk factors. Unless otherwise indicated, these factors are constructed using the data from the FRED database hosted by the Federal Reserve Bank of St. Louis. Table 1 lists acronyms of all risk factors. We provide detailed descriptions of data sources and construction methods in the appendix.

Table 2 reports summary statistics for the main risk factors that we consider in the paper over the 1987Q1 to 2016Q4 period. MKT is the excess stock market return. REIT is the excess REIT market return. ΔDEF is the change in the default spread. ΔDIV is the change in the aggregate REIT dividend price ratio. SMB, HML, RMW, and CMA are the Fama and French (1992) factors. SMB is the return difference between small and large capitalization stocks. HML is the return difference between high and low book-to-market equity ratio stocks. RMW is the return difference between high and low profitability stocks. CMA is the return difference between low and high asset growth stocks.

Luxury consumption growth has a higher mean and higher volatility than shareholder consumption growth, and the correlation between the two series is as low as 0.065. Their correlations with the capital share of income are also weak. Similarly, the two financial intermediary factors HKM and AEM also have a low correlation, as HKM is constructed by using the market value of equity and AEM is constructed by using the book value of equity.

Table 3 reports the summary statistics of returns on REIT hedging portfolios. At the beginning of each month, we sort all equity REITs into five portfolios base on SIZE (market capitalization), BM (book-to-market ratio), MOM (past returns), AG (asset growth), ROE (return on equity), or SUE (earnings surprises). We calculate the value-weighted portfolio returns for each firm characteristic and take the return difference between the first and fifth quintiles.

Consistent with Chui et al. (2003a, b), Price et al. (2012), and Bond and Xue (2017), we find that MOM, ROE, and SUE are significantly positive. SIZE, BM, and AG are positively but economically small and statistically insignificant. There is a strong positive correlation between MOM, ROE and SUE. The REIT hedging portfolios also correlate with their common stock counterparts, the correlation coefficients are 0.13, 0.28, 0.56, 0.19, and 0.36 for SIZE, BM, MOM, AG, and ROE, respectively (untabulated).

Main Empirical Findings

Financial Intermediary Models

In Table 4, we report the univariate Fama and MacBeth (1973) cross-sectional regression results. For each risk factor, we estimate the univariate model using 30 portfolios that consist of six groups of quintile portfolios formed on size, book-to-market, momentum, asset growth, return on equity, and earnings surprises.

Specifically, for risk factor j (fjt) we first estimate the betas of each portfolio using the time-series regression

where βij is the beta of portfolio i on risk factor j, ei, t is the pricing error, and N is the number of test portfolios. We then run the cross-sectional regression of the excess portfolio returns on the estimated betas:

where γi, t is the risk price for factor j in quarter t and εi, t is the pricing error.

We report the estimated risk price and its t-values in Table 4. The t-value constructed using the Fama and MacBeth (1973) standard error and the t-value constructed using the Shanken (1992) corrected standard error are in parentheses and brackets, respectively. We mainly rely on the Shanken corrected standard error for inference because the Shanken correction is quite substantial for risk factors constructed using macrovariables.

Following Jagannathan and Wang (1996), we define the cross-sectional R2 as

where \({\mathrm{Var}}_c\left(\overline{r_i}\right)\) is the cross-sectional variance of mean portfolio returns and \({\mathrm{Var}}_c\left(\overline{\varepsilon_i}\right)\) is the cross-sectional variance of mean portfolio pricing errors. As in Lettau and Ludvigson (2001), we also report the adjusted, cross-sectional \({\overline{R}}^2=1-\left[\frac{\left(1-{R}^2\right)\left(N-1\right)}{N-J-1}\right]\), where N is the number of test assets and J is the number of risk factors.

He and Krishnamurthy (2013) argue that a decrease in primary dealers’ equity, for example, during the 2008 financial crisis, increases the marginal utility of primary dealers who are the marginal investors. If an asset performs poorly when primary dealers’ equity decrease, it should have a positive risk premium. Consistent with this theoretical implication, He et al. (2017) find that the aggregate equity capital ratio factor, HKM, has a positive risk price for many asset classes.

Table 4 shows that HKM is significantly priced at the 5% level for REIT portfolios. However, its estimated risk price is negative. The puzzling result reflects the fact that while MOM, ROE, and SUE are significantly positive, they correlate negatively with HKM (Table 3). In particular, Fig. 3 shows that HKM decreases drastically in 2008Q4, while MOM is about 22%. Results are similar for ROE and SUE (untabulated).

Equity Capital Ratio Factor and REIT Momentum Factor. Notes: The solid line is the He, Kelly, and Manela (2017) equity capital ratio factor defined as the ratio of total market equity to total market assets (book debts plus market equity) of primary dealers. The dashed line is the momentum factor constructed using REIT data. Quintile momentum portfolios are sorted on the past 2 to 12 month return. The sample spans the 1987 to 2016 period

Adrian and Shin (2014) conjecture that a decrease in brokers and dealers’ leverage, for example, during 2008 financial crisis, reduces funding liquidity. Assets that do poorly when the leverage decreases thus require a positive risk premium. Consistent with this implication, Adrian et al. (2014) find that the AEM factor has a significantly positive risk price for common stock portfolios formed by size, book-to-market, and momentum.

By contrast, Table 4 shows that the risk price of AEM is negative albeit statistically insignificant for REIT portfolios. The result reflects the fact that while MOM, ROE, and SUE are significantly positive, they correlate negatively with AEM (untabulated). For example, Fig. 4 shows that AEM decreases drastically in 2008Q4, while MOM is about 22%.

Leverage Ratio Factor and Momentum Factor Returns. Notes: The solid line is the Adrian, Etula, and Muir (2014) leverage ratio factor and is defined as the ratio of total financial assets to the difference between total financial assets and total liabilities of brokers and dealers. The dashed line is the momentum factor constructed using REIT data. Quintile momentum portfolios are sorted on the past 2 to 12 month returns. The sample spans the 1987 to 2016 period

Conceptually, the equity capital ratio used in He et al. (2017) is the reciprocal of the leverage used in Adrian et al. (2014). That is, He and Krishnamurthy (2013) and Adrian and Shin (2014) have opposite predictions on the price of the intermediary risk factor. It is perplexing that He et al. (2017) and Adrian et al. (2014) document opposite signs for the financial intermediary risk factor. As we have mentioned above, both HKM and AEM decrease substantially in 2008Q4. Obviously, the two studies use different source data and methodologies to construct their intermediary risk factors. Our findings appear to suggest that the equity capital ratio has more pervasive effects on REITs.Footnote 5

Limited Market Participation Models

In this subsection, we explore whether limited market participation models explain the cross-section of REIT returns. As in the standard consumption-based CAPM, the consumption growth of marginal investors should have a positive risk price.

We consider three measures of limited stock market participation risk factors. The first factor is luxury consumption growth, LUXCON. Because luxury consumption exhibits strong seasonal variation, we use the year-over-year growth. For example, for 2000Q1, LUXCON is the log change in luxury consumption between 2000Q1 and 1999Q1.

We estimate loadings on luxury consumption growth in two ways. First, we regress the quarterly portfolio return of 2000Q1 on LUXCON of 2000Q1, and this is the specification LUXCON in Table 4. Second, we regress the portfolio return over 1999Q2 to 2000Q1 on LUXCON of 2000Q1, and this is the specification of LUXCON4. As a robustness check, we also construct LUXCON8 as the growth rate from 1998Q1 to 2000Q1, and use the return over the 1998Q2 to 2000Q1 to estimate loadings. This is the specification LUXCON8.Footnote 6

We find that luxury consumption growth is significantly priced and accounts for a large variation (for example, 60% for LUXCON) of the cross-section of REIT portfolio returns. However, contrary to the prediction of limited participation theory, its risk price is negative. Results are qualitatively similar for LUXCON4 and LUXCON8. To conserve space, we mainly use LUXCON in the remainder of the paper.

The second limited stock market participation risk factor is the change in the capital share of income proposed by Lettau et al. (2019). Because top shareholders finance their consumption primarily out of capital income, changes in the capital share of income are likely to track top shareholders’ consumption growth closely. As in Lettau et al. (2019), we use the year-over-year change, CS4, and estimate loadings using the return over the corresponding four quarters period. Table 4 shows that contrary to the implication of limited stock market participation theory, the risk price is negative albeit statistically insignificant.

The last limited stock market participation risk factor is shareholders’ consumption growth, ΔSHCON. We follow Malloy et al. (2009) and construct this variable using data from the Consumption Expenditure Survey. Table 4 shows that the risk price of ΔSHCON is positive, albeit statistically insignificant at the 10% level.

Other Commonly Used Risk Factors

In Table 4, we also consider commonly used risk factors. The CAPM stipulates that loadings on excess market returns explain the cross-section of stock returns. We use MKT (excess stock market returns) and REIT (excess REIT market returns) as proxies for excess market returns. We find that contrary to CAPM, the risk price is significantly negative for both MKT and REIT.

As in Van Nieuwerburgh (2019), we also investigate the effect of bond returns on REITs. Table 4 shows that the risk price of excess Treasury bond returns (TB) is positive and marginally significant. However, TB accounts for less than 40% of the cross-section of expected REIT portfolio returns. Untabulated results show that the explanatory power of excess Treasury bond returns vanishes when we control for loadings on MKT or REIT in bivariate regressions. We also find that excess corporate bond returns (CB) has negligible explanatory power for the cross-section of REIT returns.

REIT companies have high leverage, and their performance is significantly affected by interest rate changes. TED is the spread between the 3-month LIBOR rate and the 3-month Treasury rate. DEF is the credit spread between BAA and Aaa-rated corporate bonds. An increase in these variables indicate an increase in borrowing costs. An asset that performs poorly when funding costs increase should have a positive risk premium. Contrary to this conventional wisdom, we show in Table 4 that risk price is positive for both ΔTED and ΔDEF. We also consider the stochastically detrended risk-free rate (ΔRREL) and the spread between the long-term and short-term Treasury bonds (ΔTERM). Neither variable has a significant risk price, however.

Because investors are risk averse, an increase in stock market variance corresponds to a deterioration in investment opportunities. Consistent with this conjecture, Ang et al. (2006) show that stocks with higher loadings on changes in stock market variance have lower expected returns.Footnote 7 Following Ang et al. (2006), we use options-implied stock market variance. However, Table 4 shows that changes in stock market variance, ΔMV, has a significantly positive price of risk.

In Campbell’s (1993) intertemporal CAPM, risk factors are state variables that forecast stock market returns. Campbell (1996) includes the aggregate dividend price ratio as a risk factor because of its strong predictive power for excess stock market returns. In Table 4, ΔDIV is the first difference of the log aggregate REIT dividend price ratio. We find that it is significantly priced with a positive price of risk. However, because ΔDIV has a strong negative correlation with REIT (Table 2), untabulated results show that its explanatory power becomes insignificant when we control for loadings on REIT in the cross-sectional regression.

Lastly, we consider the Fama and French (1992) risk factors and the momentum factor, MOM, constructed using common stocks in univariate regressions. We show in Table 4 that common stock MOM and RMW have significantly positive risk prices in the REIT market. These results reflect the fact that MOM, ROE, and SUE constructed using REITs correlate positively with common stock MOM or RMW (untabulated).

Multivariate Cross-Sectional Regressions

We find that that many risk factors are significantly priced in the univariate Fama and MacBeth (1973) regression. In Table 5, we compare their explanatory power in multivariate regressions. We first estimate factor loadings or betas using the time-series regression:

where N is the number of test portfolios, βij is the beta of portfolio i on risk factor j, ei, t is the pricing error, and J is the number of risk factors. We then run the cross-sectional regression of the excess portfolio returns on the estimated betas:

where γj, t is the risk price for factor j in quarter t and εi, t is the pricing error. Following the existing empirical asset pricing literature, we calculate the cross-sectional R2 using eq. (3).

Column 1 of Table 5 shows that REIT subsumes the information content of MKT in explaining the cross-section of REIT portfolio returns. Untabulated results show that REIT drives out other risk factors except ΔDEF and LUXCON. Column 2 shows that REIT and ΔDEF have similar explanatory power, and column 3 shows that LUXCON drives out REIT. Columns 4–6 show that LUXCON drives out ΔDEF, ΔDIV and HKM, respectively.

MKT, REIT, ΔDEF, ΔDIV, and HKM have significant explanatory power for REIT portfolio returns in the univariate regression (Table 3). Bivariate regression results in Table 5 suggest that their economic information content is similar to, albeit noticeably weaker than, that of LUXCON possibly because of measurement errors. We test this conjecture in two ways.

First, we construct the first-principle component, FPC, of MKT, REIT, ΔDEF, ΔDIV, and HKM. Column 9 of Table 5 shows that FPC is only marginally significant at the 10% level in the bivariate regression, while LUXCON is significant at the 1% level. Second, we construct tracking portfolios for both HKM and LUXCON. We regress HKM or LUXCON on a constant and two extreme REIT portfolios of each characteristic, and use the fitted value as the risk factor. Column 10 shows that the results with tracking risk factors are similar to those reported in column 9. These results indicate that LUXCON is a pervasive factor in the REIT market.

In Table 6, we compare LUXCON with common stock risk factors. Column 1 reports the results of the Fama and French, 1992three-factor model. MKT is negatively priced at the 10% level. Column 2 reports the Fama and French three-factor model augmented by the momentum factor. MOM is positively priced at the 1% level, while the other factors are insignificant at the 10% level. Column 3 reports the Fama and French (2015) five-factor model. CMA is positively priced at the 10% level. As we have mentioned above, common stock MOM and CMA are priced because of their positive correlations with the hedging REIT portfolios formed on past returns, profitability, and earnings surprise. Interestingly, when we control for LUXCON in columns 4–6, the common stock risk factors become insignificant, while LUXCON is statistically significant at the 1% level. These results confirm that LUXCON is a pervasive factor.

In Table 7, we compare LUXCON with risk factors constructed using REITs. In column 1, the three-factor model (REIT, SIZE, and BM) accounts for 53% of cross-sectional variation in REIT portfolio returns, and REIT is negatively priced at the 1% level. When we add LUXCON as a risk factor in column 2, the R2increases to 72%, and LUXCON is statistically significant at the 1% level. By contrast, the REIT factors are insignificant at the 5% level.

We augment the three-factor model with MOM in column 3 of Table 7. The R2 increases to 60% from 53% in column 1. In addition, MOM is significant at the 1% level, while REIT becomes insignificant at the 10% level. The results should not be too surprising. We include the REIT portfolios used to construct MOM as test portfolios. In addition, MOM correlates strongly with ROE and SUE (Table 3), and portfolios formed on ROE and SUE are also used as test portfolios. Nevertheless, these results indicate that MOM has a pervasive effect on REITs. Column 4 shows that LUXCON remains significant at the 1% level when we control for the four factors. The R2 also increases to 72% from 60% in column 3. By contrast, the explanatory power of MOM is noticeably weaker than that in column 3. It is significant only at the 5% level.

Column 5 of Table 7 shows that the five-factor model (REIT, SIZE, BM, AG, and ROE) has good explanatory power for the cross-section of REIT portfolio returns. The R2 of 78%, and ROE is significant at the 1% level. In addition, we show in column 6 that the explanatory power of LUXCON becomes negligible when controlling for the five factors. By contrast, ROE remains significant at the 1% level. These results indicate that the explanatory power of LUXCON reflect its close correlations with REIT factors. To further illustrate this point, we show in column 7 that the tracking portfolio for LUXCON is significant at the 1% level, even when we control for the five factors.

To summarize, LUXCON, a macrovariable, has a significant relation with the cross-section of REIT portfolio returns. This novel finding helps us to identify the economic driving force in the REIT market.

Alternative Measures of Luxury Consumption

Table 8 reports two alternative measures of luxury consumption proposed by Aït-Sahalia et al. (2004). JW is consumption growth on Jewelry and Watches. BA is consumption growth on boats and aircrafts. For comparison, we also include the growth rate of aggregate consumption measured by nondurable goods and services, NDS, which is widely used to test the standard consumption-based CAPM. In the univariate regression, the risk price of BA and JW is significantly negative at the 10% level and 5% level, respectively. The risk price of NDS is also significantly negative at the 10% level. When we compare the explanatory power of these alternative measures with that of LUXCON, LUXCON remains significant.

Systematic Risk Factor versus Systematic Mispricing Factor

We find that many risk factors are significantly priced in the cross-section of REIT portfolio returns. Their information content is subsumed by that of LUXCON. Our result suggests that LUXCON is a pervasive systematic factor in the REIT market. However, the risk prices of these factors have the opposite signs to these stipulated by the theories that motivate them. It is very difficult to reconcile our results with a risk-based explanation. It is very hard to understand why a hedging portfolio that performs well during the financial crisis should have a high expected return. In this Section, we explore a hypothesis that our results reflect systematic mispricing associated with investor sentiment.

The sentiment hypothesis follows closely the behavioral asset pricing theory articulated by Baker and Wurgler (2006, 2007), which builds on two key assumptions. First, the REIT market is influenced by investor sentiment. Second, the mispricing is not immediately arbitraged away because of short sale constraints. When sentiment is strong, REITs with lower past returns, low returns on assets, and negative earnings surprises (hereafter we refer to these REITs as weak REITs) are overvalued compared with stocks with high past returns, high returns on assets and positive earnings surprises (hereafter we refer to these REITs as robust REITs). Because of short sale constraints, the mispricing is not corrected until the sentiment subsides. As a result, REITs that are more sensitive to investor sentiment have lower average returns.

Short sale constraints are not a necessary condition for mispricing to have a significant effect on asset prices. Kozak et al. (2018) point out that investor sentiment is a priced risk factor even in the absence of near-arbitrage opportunities. Sentiment-induced mispricing is not immediately arbitraged away because bets against the mispricing are not risk free if the sentiment correlates with a systematic REIT factor, e.g., business cycles. Improvement in future business conditions would further fuel the sentiment and widen the mispricing.

Stambaugh and Yuan (2017) use the sentiment hypothesis to explain systematic mispricing in common stocks. However, there is an interesting difference between sentiment in the common stock market and sentiment in the REIT market. Stambaugh and Yuan show that the Baker and Wurgler (2006) sentiment measure, which by construction is orthogonal to business cycles, is priced in common stocks. By contrast, the REIT market sentiment appears to have a strong comovement with business cycles. As we show in Table 8, standard business cycle measures, e.g., the industrial production index and the Chicago Fed National Activity index are negatively priced in the cross-section of REIT portfolio returns at the 5% level. In addition, the information content is completely subsumed by LUXCON in the case of the activity index while industrial production remains significant along with the significance of LUXCON. These results are consistent with Kozak et al. (2018) conjecture.

Our sentiment hypothesis has the following implications. First, weak stocks have stronger comovement with sentiment than robust stocks. This explains why weak stocks have lower average returns than robust stocks, because the former is more susceptible to overpricing. Second, MOM, ROE, and SUE have higher returns mainly during the period when sentiment decreases. Similarly, in the cross-sectional regression, the coefficient on LUXCON loadings is more pronounced when sentiment subdues.Footnote 8 Last, with the increase in the share of institutional investors in the REIT market over our sample, the explanatory power of sentiment for REIT has become weaker. Our results are consistent with these implications.

In Table 9, we investigate the relation between investor sentiment and REIT returns. We consider three standard investor sentiment measures, the Michigan consumer sentiment index (MICHIGAN), the confidence indicator constructed by the Organization for Economic Cooperation and Development (OECD) and the Conference Board consumer confidence index (CCI). As a robustness check, we also include two housing market sentiment measures, the NAHB Wells Fargo National Housing Market Index from National Association of Home Builders (HMI) and house start permits (PERMIT4). These variables are also closely watched by market participants to gauge aggregate economic activity.

As conjectured, the sentiment measures are negatively priced at least at the 5% level in the univariate regression. Moreover, except CCI, their explanatory power becomes negligible when we control for LUXCON, which is significant at least at the 5% level. Similarly, CCI becomes less significant in the bivariate regression. These results are consistent with the first implication that investor sentiment is an important driver of the REITs market. Untabulated results show that the Baker and Wurgler (2006) sentiment measure is not priced in the REITs market, indicating an important difference between common stocks and REITs.

To investigate the second implication, we construct a sentiment dummy variable, DUM. It equals 1 for the quarters of the lowest ΔCCI quartile and 0 otherwise. In panel A of Table 10, we show that MOM and ROE are positive only in quarters of the lowest ΔCCI quartile. Similarly, SUE is much larger when CCI declines sharply. In panel B, we include LUXCON, DUM, and their interaction term LUXCON*DUM as explanatory variables in cross-sectional regressions. As expected, the coefficient on the interaction term is significantly negative at the 1% level. These results indicate that the mispricing is more pronounced when sentiment is high.

Additional analysis lends further support to the asymmetric effect of investor sentiment on REITs. The sentiment hypothesis implies that CCI correlates negatively with future REIT market returns. Moreover, if weak REITs are overvalued relative to robust REITs when sentiment is strong, robust REITs outperforms weak REITs when the sentiment eventually subdues.Footnote 9 We expect that CCI correlates positively with MOM, ROE, and SUE. Table 11 shows that that CCI negatively and significantly forecast excess REIT market returns and R2 increases from 12% for the one-quarter horizon to 22% for the eight-quarter horizon. In addition, CCI positively forecasts MOM, ROE, and SUE constructed using REITs, and the relation is statistically significant for MOM and ROE at the 2-year forecast horizon according to the one tail test.

In Table 12, we investigate the explanatory power of LUXCON in two subsamples. The 2008 financial crisis has pronounced effects on both HKM and the REIT market (Figs. 3 and 4). To ensure that our main findings are not sensitive to this episode, the first subsample spans the 1987Q1 to 2007Q4 period. The 1993 regulatory changes have attracted institutional investors to enter the REIT market (Figs. 1 and 2). The second subsample spans the 1994Q1 to 2016Q4.

HKM and LUXCON are significantly priced in the first subsample at the 5% level, indicating that our main findings are not sensitive to the 2008 financial crisis. By contrast, HKM is insignificant in the second half sample and the evidence is also mixed for LUXCON. LUXCON4 is significantly priced in the second subsample; however, its explanatory power in terms of R2 is much weaker than that in the first subsample. The evidence is consistent with the conjecture that the increase in institutional ownership alleviates mispricing, although it may also reflect sampling errors due to the small sample size of the two subsamples.

Conclusion

We conduct a comprehensive analysis of REIT pricing using both recently proposed limited market participation models and traditional risk factors. We find that the stock market return, the REIT market return, the default spread, the dividend yield, the equity capital ratio by He et al. (2017) and luxury consumption growth by Aït-Sahalia et al. (2004) have significant explanatory power for cross-sectional REIT returns. Luxury consumption growth subsumes the information content of all the other factors. This finding is robust to subsamples and alternative luxury consumption measures Table 13.

Unlike the results for common stocks, the risk price associated with these factors is negative. This result contradicts risk-based asset pricing theory and suggests that real estate markets are heavily influenced by investor sentiment. This sentiment also has strong comovement with the business cycle. One implication is the weak REITs (REITs with low past returns, low return on assets and negative earnings surprises) get bid up in the price relative to robust REITs. Weak REITs have lower average returns than robust REITs because the mispricing is eventually corrected when sentiment subsides.

Our findings accord with recent theoretical results by Kozak et al. (2018), who argue that sentimental demand significantly affects asset prices if it correlates with a systematic factor. Even though arbitragers know that weak REITs are overvalued relative to robust REITs when sentiment is strong, it is not optimal for arbitragers to bet against the mispricing. This is because when the sentiment-induced mispricing comoves with a systematic factor, e.g., the business cycle, bets against the mispricing are not risk free. Improvement in future business conditions would further strengthen the sentiment and exacerbate the mispricing.

Notes

The representative-agent models by Campbell and Cochrane (1999) and Basal and Yaron (2004) also explain these stylized facts. However, unlike Guo (2004), these models do not explain the unstable relation between stock market volatility and the dividend yield documented by Schwert (1989). The empirical findings by Muir (2017) also pose challenges to the representative-agent models.

REITs are required to hold 75% of their assets in real property or loans secured on such assets. Further 75% of REIT annual gross income must be from real estate related sources. Also important is the requirement that REITs distribute 90% of its taxable income, which limits the ability to retain earnings within the organization.

Adrian et al. (2014) construct the broker and dealer leverage using the Flow of Funds data that are subject to regular revision. Tyler Muir posts both the original AEM factor used in Adrian et al. (2014) and an updated AEM factor constructed using a more recent vintage of the Flow of Funds data on his research website https://sites.google.com/site/tylersmuir/home/data-and-code. Unlike the original AEM factor, the updated version has negligible explanatory power for the cross-section of stock portfolio returns. Similarly, Guo and Pai (2020a, Guo and Pai, 2020b) show that revision of National Income and Product Accounts data has significant effects on empirical asset pricing tests. He et al. (2017) construct the equity capital ratio of primary dealers using Compustat data that are not subject to systematic revision.

The specifications LUXCON4 and LUXCON8 follow those used in Lettau et al. (2019).

We thank the anonymous referee for suggesting this implication.

References

Adrian, T., Etula, E., & Muir, T. (2014). Financial Intermediaries and the Cross Section of Asset Returns. Journal of Finance, 69(6), 2557–2596.

Adrian, T., & Shin, H. (2014). Procyclical leverage and value-at-risk. Review of Financial Studies, 27(2), 373–403.

Aït-Sahalia, Y., Parker, J., & Yogo, M. (2004). Luxury Goods and the Equity Premium. Journal of Finance, 59(6), 2959–3004.

Allen, F., & Gale, D. (1994). Limited Market Participation and Volatility of Asset Prices. American Economic Review, 84(4), 933–955.

Alcock, J., & Andrilikova, P. (2018). Asymmetric Dependence in Real Estate Investment Trusts: An Asset-Pricing Analysis. Journal of Real Estate Finance and Economics, 56(2), 183–216.

Ang, A., Hodrick, R. J., Xing, Y., & Zhang, X. (2006). The cross-section of volatility and expected returns. The Journal of Finance, 61(1), 259–299.

Basal, R., & Yaron, A. (2004). Risks for the Long Run: A Potential Resolution of Asset Pricing Puzzles. Journal of Finance, 59(4), 1481–1509.

Baele, L., Bekaert, G., Inghelbrecht, K., & Wei, M. (2020). Flights to Safety. Review of Financial Studies, 33(2), 689–746.

Baker, M., & Wurgler, J. (2006). Investor Sentiment and the Cross-Section of Stock Returns. Journal of Finance, 61(4), 1645–1680.

Baker, M., & Wurgler, J. (2007). Investor Sentiment in the Stock Market. Journal of Economic Perspectives, 21(2), 129–151.

Bond, S.A. and Q. Chang (2013). REITs and the Private Real Estate Market, in H.K. Baker and G. Filbeck (eds). Alternative Investments: Instruments, Performance, Benchmarks, and Strategies, Chapter 5, pp 79–97, The Robert W. Kolb Series in Finance. . John Wiley & Sons, Inc.

Bond, S. A., & Xue, C. (2017). The Cross-Section of Expected Real Estate Returns: Insights from Investment-based Asset Pricing. Journal of Real Estate Finance and Economics, 54, 403–428.

Boudry, W. I., Connolly, R. A., & Steiner, E. (2019). What Really happens during Flight to Safety: Evidence from Real Estate Markets. Real Estate Economics., 2019, 1–26.

Campbell, J. (1993). Intertemporal Asset Pricing without Consumption Data. American Economic Review, 83(3), 487–512.

Campbell, J. (1996). Understanding Risk and Return. Journal of Political Economics, 104(2), 298–345.

Campbell, J., & Cochrane, J. (1999). By Force of Habit: A Consumption Based Explanation of Aggregate Stock Market Behavior. Journal of Political Economy, 107(2), 205–251.

Campbell, J., Giglio, S., Polk, C., & Turley, R. (2018). An Intertemporal CAPM with Stochastic Volatility. Journal of Financial Economics, 128(2), 207–233.

Chan, S.H., Leung, W. K., & Wang, K. (1998). Institutional investment in REITs: Evidence and implications. The Journal of Real Estate Research, 16(3), 357–374.

Chui, A. C. W., Titman, S., & Wei, K. C. J. (2003a). Intra-industry momentum: the case of REITs. Journal of Financial Markets, 6(3), 363–387.

Chui, A. C. W., Titman, S., & Wei, K. C. J. (2003b). The Cross Section of Expected REIT Returns. Real Estate Economics, 31, 451–479.

Clayton, J., & MacKinnon, G. (2003). The Relative Importance of Stock, Bond and Real Estate Factors in Explaining REIT Returns. The Journal of Real Estate Finance and Economics, 27, 39–60.

Cuoco, D., & Basak, S. (1998). An Equilibrium Model with Restricted Stock Market Participation. Review of Financial Studies, 11(2), 309–341.

Das, P., Freybote, J., & Marcato, G. (2015). An Investigation into Sentiment-Induced Institutional Trading Behavior and Asset Pricing in the REIT Market. The Journal Real Estate Finance and Economics, 51(2), 160–189.

Fama, E., & French, K. (1992). The Cross-Section of Expected Stock Returns. Journal of Finance, 47(2), 427–465.

Fama, E. F., & MacBeth, J. D. (1973). Risk, Return, and Equilibrium: Empirical Tests. Journal of Political Economy, 81(3), 607–636.

Gentry, W., Jones, C., Mayer, C. (2004). Do Stock Price Really Reflect Fundamental Values? The case of REITs. Working paper, Columbia University.

Giglio, S., Kelly, B., & Pruitt, S. (2016). Systemic Risk and the Macroeconomy: An Empirical Evaluation. Journal of Financial Economics, 119(3), 457–471.

Guo, H. (2004). Limited Stock Market Participation and Asset Prices in a Dynamic Economy. Journal of Financial and Quantitative Analysis, 39(3), 495–516.

Guo, H. (2006). Time-Varying Risk Premia and the Cross Section of Stock Returns. Journal of Banking and Finance, 30(7), 2087–2107.

Guo, H., Pai, Y. (2020a). Rediscovering the CCAPM Lost in Data Revision. Working paper, University of Cincinnati.

Guo, H., & Pai, Y. (2020b). Stock Market and Real Economy: Unwritten History Matters. Working paper. University of Cincinnati.

Guvenen, F. (2009). A Parsimonious Macroeconomic Model for Asset Pricing. Econometrica., 77(6), 1711–1740.

Hartzell, J. C., Muhlhofer, T., & Titman, S. D. (2010). Alternative benchmarks for evaluatin mutual fund performance. Real Estate Economics, 38(1), 121–154.

He, Z., & Krishnamurthy, A. (2013). Intermediary Asset Pricing. American Economic Review, 103(2), 732–770.

He, Z., Kelly, B., & Manela, A. (2017). Intermediary Asset Pricing: New Evidence from Many Asset Classes. Journal of Financial Economics, 126(1), 1–35.

Hoesli, & Oikarinen, E. (2012). Are REITs Real Estate? Evidence from International Sector Level Data. Journal of International Money and Finance, 31(7), 1823–1850.

Hou, K., Xue, C., & Lu, Z. (2015). Digesting Anomalies: An Investment Approach. Review of Financial Studies, 28(3), 650–705.

Jagannathan, R., & Wang, Z. (1996). The Conditional CAPM and the Cross-Section of Expected Returns. Journal of Finance, 51(1), 3–53.

Kiku, D., Bansal, R., Shaliastovich, I., & Yaron, A. (2014). Volatility, the Macroeconomy and Asset Prices. Journal of Finance, 69(6), 2471–2511.

Kozak, S., Nagel, S., & Santosh, S. (2018). Interpreting Factor Models. Journal of Finance., 73(3), 1183–1223.

Ling, D., Naranjo, A., & Scheick, B. (2014). Investor Sentiment, Limits to Arbitrage, and Private Market Returns. Real Estate Economics, 42(3), 521–577.

Lettau, M., & Ludvigson, S. (2001). Resurrecting the (C)CAPM: A Cross-Sectional Test When Risk Premia Are Time-Varying. Journal of Political Economy, 109(6), 1238–1287.

Lettau, M., Ludvigson, S., & Ma, S. (2019). Capital Share Risk in U.S. Asset Pricing. Journal of Finance., 74(4), 1753–1792.

Lucas, R. (1978). Asset Prices in an Exchange Economy. Econometrica, 46(6), 1429–1445.

Malloy, C. J., Moskowitz, T. J., & Vissing-Jorgensen, A. (2009). Long-run stockholder consumption risk and asset returns. The Journal of Finance, 64(6), 2427–2479.

Mankiw, G., & Zeldes, S. (1991). The Consumption of Stockholders and Nonstockholders. Journal of Financial Economics, 29, 97–112.

Muir, T. (2017). Financial Crises and Risk Premia. Quarterly Journal of Economic., 132(2), 765–809.

Price, S. M., Gatzlaff, D. H., & Sirmans, C. (2012). Information uncertainty and the post-earnings-announcement drift anomaly: Insights from REITs. The Journal of Real Estate Finance and Economics, 44(1–2), 250–274.

Schwert, W. (1989). Why Does Stock Market Volatility Change Over Time? Journal of Finance, 44(5), 1115–1153.

Stambaugh, R., & Yuan, Y. (2017). Mispricing Factors. Review of Financial Studies, 30(4), 1270–1315.

Stambaugh, R., Yu, J., & Yuan, Y. (2012). The Short of It: Investor Sentiment and Anomalies. Journal of Financial Economics, 104(2), 288–302.

Siriwardane, E. (2015). The Probability of Rare Disasters: Estimation and Implications. Harvard Business School Finance Working Paper (Vol. No. 16-061).

Van Nieuwerburgh, S. (2019). Why are REITS Currently So Expensive? Real Estate Economics, 47(1), 18–65.

Vissing-Jorgensen, A. (2002). Limited Stock Market Participation and the Elasticity of Intertemporal Substitution. Journal of Political Economy, 110(4), 825–853.

Acknowledgements

The authors would like to acknowledge a grant from the Real Estate Research Institute to complete this research. The authors also thank Robert Connolly, Jacob Sagi, Eva Steiner, Buhui Qiu, Chen Xue and seminar and conference participants at the University of Sydney, The Southern Methodist University, The University of Queensland, 2019 AREUEA-ASSA Annual Conference, and 2018 RERI Annual Conference for their helpful comments.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher’s Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix

Appendix

REITs Sample

We use the CRSP/Ziman Real Estate Data Series. The CRSP/Ziman database includes all REITs that traded on the three primary exchanges since 1980. We use equity REITs (RTYPE = 2) in the empirical analysis. The number of firms in CRSP/Ziman database ranges from 55 to 199 each year. We also compare our sample with the sample identified by the National Association of Real Investment Trusts (NAREIT). The firms covered in the two databases are very similar.

REITs Portfolio Construction

At the beginning of each month, we sort equity REITs equally into five portfolios based on a firm characteristic. For each portfolio, we first calculate the monthly portfolio return and then convert it into the quarterly portfolio return. We construct portfolio returns using the CRSP and COMPUSTAT data. We use the following six firm characteristics in the empirical analysis.

-

Market Equity (Size) is the share price times the number of shares outstanding. The market equity is calculated at the beginning of each month.

-

Book-to Market (B/M) is the book equity divided by market equity. The B/M is calculated in June each year. The book equity is from the end of last fiscal year. The market equity is from the end of last Calendar year.

-

Momentum (MOM) is measured as the cumulative return in the past t-12 to t-2 month.

-

Investment (I/A) is the annual growth rate in total non-cash asset. We assume that annual investment growth rate is known four months after fiscal year end.

-

Profitability (ROE) is measured as quarterly return on equity, defined as income before extraordinary item dividend by one-quarter-lagged book equity. We assume that quarterly ROE is known on the earnings announcement day (RDQ).

-

Earnings Surprise (SUE) is measured as the standardized unexpected earnings. SUE is calculated as the change in the most recent quarterly earnings per share (EPSPXQ) from its value in the same quarter last year divided by the standard deviation of changes over the previous eight quarters. We assume that earnings surprise known on the earnings announcement day (RDQ).

Financial Factors and Dividend-Price Ratio

TED is the spread between the 3-month Libor and the 3-month Treasury bill. TERM is the spread between the 10-year Treasury bond and the 3-month Treasury bill. DEF is the spread between the Baa-rated and Aaa-rated corporate bonds. DIV is the aggregate quarterly dividend divided by aggregate market cap. Dividend data are from the CRSP event database, which records dividend per share ordered by ex-dividend day (DIVAMT). We include all ordinary dividend (DISTCD first digit = 1) and exclude year-end, extra dividend (DISTCD = 1262) and special dividend (DISTCD = 1272). The dividend price ratio is calculated as the ratio of the sum of dollar amount dividend (dividend per share multiply number of share outstanding) within each quarter to the total market capitalization at the end of each quarter.

Market Factor

MKT is the value weighted excess return of SP500 stocks. REIT_MKT is the value weighted excess return of all equity REITs identified by CRSP/Ziman database. TB is the excess Treasury bond return. CB is the excess corporate bond return. We MKT and the risk-free rate data from Kenneth French at Dartmouth College and obtain TB and CB data from Amit Goyal at the University of Lausanne. We construct REIT_MKT using the CRSP/Ziman database.

Limited Stock Market Participation Factors

Stockholder consumption growth

Following Malloy et al. (2009), we use the Consumer Expenditure Survey (CEX) data to construct stockholder consumption growth factor. CEX interviews 4000 ~ 8000 households each quarter. Each household is interviewed once every three months over four consecutive quarters. About 20% sample households are replaced for each interview. The first interview is a practice interview and the results are not report in the data. The interview data only includes result from interviews two to five.

The sample spans 1982 to 2016 period. CEX data for 1996 and after can be directly download from the Public-Use Microdata (PUMD) on the CEX website. The early sample 1982 to 1995 can be download from the ICPSR website.

We construct stockholder consumption growth (SHCON) in the following steps. First, we classify all types of expenditure into durable, nondurable and service by NIPA definition. All durable items are excluded. For service, we exclude all housing expense except house operation cost, medical and education cost, rental and finance expense for durable products (such as car finance). We also exclude all miscellaneous items because we have insufficient information to correctly classify them. Table A1 shows the UCC (six-digit codes that identify the consumption item) we use for calculating household consumption.

Second, we construct household consumption growth. Interviews are conducted and recorded in each month, and we calculate the quarterly consumption growth rate at a monthly frequency. For example, if a household has the third interview in May 2016, it reports its consumption in February, March, and April 2016. The household then would have the fourth interview in August 2016 and report its consumption in May, June, and July 2016. The household’s consumption growth in July 2016, i.e., the second quarter of 2016, is the difference between the natural logarithm of total consumption reported in the fourth interview and the natural logarithm of total consumption reported in third interview.

Third, we merge the household consumption growth data with household characteristics data. We clean the data by excluding following observations. (1) Households with less than four interviews. (2) Nonurban households (variable: BLS_URBN) and households residing in student housing (variable: CUTENURE). (3) Households with incomplete income response (variable: REPSTAT). (4) The consumption growth rates that are lower than −61% or greater than 161%.

Last, we identify the stockholder in our sample and calculate the stockholder consumption growth rate. In the fifth interview, households will be asked the amount of stock, bonds, mutual fund that they hold today and the amount they hold one year from today. We classify households with either positive holding today or positive holding one year ago as stockholders. SHCON is the average of stockholders’ consumption growth rates.

Luxury consumption

Following Aït-Sahalia, Parker, and Yogo (2004), we use the sales of the high-end luxury goods to construct the luxury consumption growth factor, LUXCON. The high-end luxury goods should not be considered as durable goods for the very rich since fashion is fickle.

We include sales of three luxury retailers, Gucci (GUC), Saks (SKS) and Tiffany (TIFF, TIF since 1986). The quarterly sales data are available from COMPUSTAT over the 1995 to 2004 period for Gucci, the 1991 to 1997 period for Saks, and the 1960 to 2016 period for Tiffany.

COMPUSTAT reports the quarterly sale (turnover) data for all public companies. COMPUSTAT segment reports the annual US sale and annual international sale data for all public companies. Using COMPUSTAT segment data, we can calculate the ratio of US retail to the total sale each year. Then, we multiply this ratio by the quarterly total sale to get quarterly US sale. Because of the seasonality in luxury sales, we use the year-over-year growth rate. For example, the 2016Q4 luxury consumption growth is the percentage change of the 2016Q4 luxury sales over the 2015Q4 luxury sales.

Intermediary Equity Capital Ratio

He, Kelly, and Manela (2017) creates the intermediary equity capital ratio, which is the aggregate equity capital ratio of the New York Fed’s Primary dealer. The intermediary capital ratio is denoted as aggregate value of market equity divided by aggregate market equity plus aggregate book debt. Their factor could be downloaded at http://www.zhiguohe.com/research.html

Intermediary Leverage Ratio

Adrian, Etula, and Muir (2014) constructs intermediary leverage ratio, which is the total financial assets divided by the difference between total financial assets and total liabilities. Adrian, Etula, and Muir use aggregate broker and dealer’s financial assets and liabilities data from Financial Accounts of the United States hosted by the Federal Reserve Board. They are free to download from the website https://www.federalreserve.gov/releases/z1/current/default.htm. Tyler and Muir also posts both the original data used in Adrian, Etula, and Muir (2014) and the updated data on his website https://sites.google.com/site/tylersmuir/home/data-and-code.

Capital Share of Income

We follow Lettau, Ludvigson, and Ma (2019) to construct the capital share of income. The relation between labor share (LS) and capital share (CS) is CS = 1-LS. Lettau, Ludvigson, and Ma calculate the labor share growth rate by taking the log difference of quarterly seasonally adjusted labor share index. The capital share growth rate is the labor share growth rate with the opposite sign. The labor share index are free to download from the FRED database hosted by the St. Louis Fed (http://research.stlouisfed.org/fred2/series/PRS85006173).

Rights and permissions

About this article

Cite this article

Bond, S., Guo, H. & Yang, C. Systematic Mispricing: Evidence from Real Estate Markets. J Real Estate Finan Econ (2022). https://doi.org/10.1007/s11146-021-09883-9

Accepted:

Published:

DOI: https://doi.org/10.1007/s11146-021-09883-9