Abstract

This paper considers contemporaneous spillover effects between Germany and four peripheral European countries that were most affected by the European Debt Crisis, and provides evidence of bidirectional spillovers among these equity markets. We document that there is asymmetry and time variation in contemporaneous spillovers. Particularly, contemporaneous return spillovers from Germany to the peripheral equity markets is higher than the other way around. We show that European Debt Crisis led to a decrease in the contemporaneous spillover effects.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

The sovereign debt crisis has been one of the toughest challenges for the Euro Area (Kosmidou et al. 2015; Bhanot et al. 2014). Although the Euro Area (EA) is a single currency market with a common monetary policy, it consists of diverse countries in terms of economic growth, and their financial markets are different with regard to depth and development (Louzis 2015). The European Debt Crisis (EDC) highlighted these differences among the EA countries, as shown by the various challenges that each country faced in meeting their obligations from the Stability and Growth Pact and the Maastricht Treaty, such as government deficits of less than 3% of GDP and public debt levels limited to 60% of GDP. While the crisis originated in Greece, it rapidly spread to several Eurozone countries, such as Italy, Portugal and Spain. Unable to fund their deficits, these countries sought financial assistance to avoid default or a return to pre-Euro national currencies. The responses to the crisis, namely, the European governments’ willingness to rescue Greece from the sovereign default by providing financial support in May 2010, the establishment of the European Financial Stability Facility program in June 2010 and the European Central Bank’s (ECB) policies,Footnote 1 aimed to avoid the transmission of shocks across the European countries and markets (Ehrmann and Fratzscher 2017). To gauge the success of the programmes and future ones, it is therefore important to investigate the relations and spillovers among European financial markets.

While a few studies address the relations and spillovers among the EA sovereign debt markets (Ludwig 2014; Gómez-Puig and Sosvilla-Rivero 2013; De Santis 2014; Alter and Beyer 2014; Blatt et al. 2015), the EDC also affected European equity markets (Gentile and Giordano 2014; Stracca 2015; Louzis 2015). These equity-related studies show that news in the sovereign debt market for a given country has significant impacts on another country’s stock markets, and there are spillover effects among these markets. For instance, Bhanot et al. (2014) find that news regarding Greece’s downgrades negatively affected European equity markets, whereas Kosmidou et al. (2015) show that the approval of financial support programs positively affected the Greek capital market. Furthermore, Louzis (2015) identifies the stock markets, rather than bond markets, as the key transmitters of shocks across the EA markets. The above findings suggest that further investigation of spillover effects among European equity markets is important.

Given that European equity markets trade simultaneously, transmission of shocks among these markets can occur instantaneously. Therefore, taking into consideration these contemporaneous spillover effects is essential. Currently, a clear understanding of how the contemporaneous effects change over time, especially during financial crises, together with what drives their dynamics, is limited in European equity markets. For instance, it is yet to be documented whether there is asymmetry and time variation in contemporaneous spillover effects, and whether financial crises, financial assistance programs and credit rating downgrades influence their dynamics. To address these issues, identifying the shocks to individual equity markets is fundamental. Existing studies on spillover effects in financial markets usually either apply standard vector autoregression (VAR) models which focus on lead–lag relations or assume a priori that transmission of shocks occurs in one or another direction. However, such an assumption may not be reasonable and attempts should be made to detect the direction of causality, i.e., whether shocks occurring in one market affects another market or vice versa. Moreover, lead–lag relations may not entirely capture the contemporaneous spillover effects given the high level of integration among the EA markets.Footnote 2

As an alternative solution to identify the direction of causality among financial markets, Rigobon (2003) proposes the “identification through heteroskedasticity” approach, and more recently, Lütkepohl (2013) and Lanne and Lütkepohl (2010) propose a similar approach through shifts in the volatility of the residuals. The former approach has been implemented by several studies (Andersen et al. 2007; Ehrmann et al. 2011; Ehrmann and Fratzscher 2017) which show the existence of contemporaneous spillover effects among financial markets.

In this paper, we examine the instantaneous transmission of return shocks, namely, contemporaneous spillover effects. Using a structural VAR and the approaches of Lütkepohl (2013) and Lanne and Lütkepohl (2010) to identify contemporaneous relations, we investigate these effects that occur between the German equity market and the peripheral Greek, Italian, Portuguese and Spanish (GIPS) equity markets.Footnote 3 By investigating the contemporaneous spillovers, we make the following contributions. First, we analyze the instantaneous transmission of shocks across the German and GIPS equity markets taking into consideration the EDC, as well as the Global Financial Crisis (GFC). Specifically, we split our sample into four periods: the period prior to the GFC, the GFC period, the first phase of the EDC and the second phase of the EDC. We then estimate contemporaneous relations for each of these periods. In addition, we investigate the time variation in contemporaneous spillover effects using a rolling-windows estimation. Second, we assess how the financial assistance programs and credit rating downgrades contribute to spillover effects. In doing so, our approach differs from the works of Bhanot et al. (2014) and of Kosmidou et al. (2015), who investigate the impacts of similar events on equity markets rather than spillover effects. Our paper also differs from Ehrmann and Fratzscher (2017) who examine contemporaneous spillover effects between the EA bond markets. Third, from an empirical perspective, we use Lütkepohl’s (2013) and Lanne and Lütkepohl’s (2010) approaches which allow us to address the simultaneity issue without imposing restrictions on the direction of spillover effects. By using this method, our paper differs from the existing studies on spillover effects across the European equity and bond markets, such as Gentile and Giordano (2014), Louzis (2015) and Stracca (2015), who analyze spillover effects by either imposing a priori assumptions on what country the shocks originate from or concentrating on lead–lag dynamics.

Our investigation leads to several important findings. First, we show that there are asymmetric contemporaneous spillover effects, where the contemporaneous return spillover from the German to the GIPS equity markets is higher than the other way around. This implies that return shocks originating from Germany have stronger effects on each of the GIPS returns than the other way around. Second, we find that while the GFC led to an increase in the magnitude of the contemporaneous spillovers, the first phase of the EDC caused a decrease in their magnitude. During the second phase of the EDC, we observe an increase in the return spillover from Germany to GIPS stock markets and a similar magnitude as in the first phase of EDC of the return spillover effects the other way around. These findings are in line with Ehrmann and Fratzscher (2017), Caporin et al. (2018) and Claeys and Vasicek (2014) who examine the transmission of shocks among European bond markets. Third, we highlight the impact that financial assistance programs and credit rating downgrades have on the contemporaneous spillover effects. We find that financial support programs have reduced the spillover effects from GIPS equity markets to the German equity market and in most cases increased their magnitude the other way around. Credit rating downgrades, e.g., of Portugal and Italy, decreased contemporaneous spillover effects. De Santis (2014) provides similar evidence regarding the impacts of these events on European bond markets.

Our results have several implications. First, for financial markets, our findings highlight the influential role of the German stock market for the GIPS stock markets since shocks to German returns have greater impacts on GIPS markets than the other way around. Second, our model provides a useful tool that can be used to monitor the contemporaneous spillover effects which are of considerable importance to investors, as well as policy makers. Knowledge of these spillover effects is relevant for policies aiming to strengthen the stability of the EA markets and improve their ability to reduce the transmission of shocks among financial markets. As such, our findings provide insights for a country’s financial stability and implementation of adequate policy actions (Louzis 2015). For instance, our findings show that the EDC has led to a reduction in contemporaneous spillover effects rather than an increase in their magnitude, which occurred during the GFC. While on the one hand, this reduction was preferable since it hampered a more systemic crisis in the Euro Area, on the other hand, it has posed challenges for policy makers given that it has led to unequal transmission of policies across Euro Area (Ehrmann and Fratzscher 2017).

The rest of the paper is organized as follows. Section 2 discusses the studies on spillover effects among financial markets and how our work contributes to existing studies. Section 3 presents the empirical setting. Section 4 discusses the data and Sect. 5 presents the results. We conclude in Sect. 6.

2 Literature review

This paper investigates the contemporaneous spillovers among European equity markets and the impact of financial assistance programs, credit rating downgrades and financial crises to these spillovers. Hence, our study connects two strands of literature; namely, the spillover effects among financial markets and the impact of these events on financial markets. While each of these concepts have been studied independently in the literature, to our knowledge there are no studies which explore the relation between spillovers among equity markets and the announcement of financial assistance programs and credit rating downgrades. Moreover, despite significant research on bond markets, there are only few studies which focus on the European equity markets. Using vector autoregressive (VAR) models, Granger Causality tests and vector error correction (VEC) models, these studies concentrate on the lead–lag dynamics, and the impact of financial support programs and credit rating downgrades on equity markets. As such, there is limited evidence with regard to the instantaneous transmission of shocks among European equity markets. We start this section by discussing the papers that focus on bond markets and the impact of financial assistance programs and credit rating downgrades on these markets. We then show that there are spillover effects between the bond and equity markets within and outside the EA. Finally, we discuss the few studies that assess the impact of financial assistance programs and credit rating downgrades on equity markets rather than on the spillovers among markets.

There is a large body of literature that explores the relations among the European bond markets (e.g., Ehrmann and Fratzscher 2017; Gorea and Radev 2014; Ludwig 2014; Arghyrou and Kontonikas 2012; Giordano et al. 2013; Alter and Beyer 2014; Gómez-Puig and Sosvilla-Rivero 2013). The majority of these studies concentrate on the drivers that facilitate the transmission of shocks across bond markets, with the banking system, trade and debt holdings playing an important role. Other studies consider the role of news announcements, namely, bailout programs and credit rating downgrades, in the transmission of shocks across EA bond markets. For instance, Mink and De Haan (2013) examine the impact of general news about Greece and the Greek bailout program on European bank stock prices and bond markets in 2010. They find that news about Greece’s bailout program had a significant impact even on stock prices of banks without exposure to Greece, Ireland, Portugal and Spain. However, general news about Greece did not affect bank stock prices but had an impact on the sovereign bond prices of Portugal, Spain, Ireland. Similarly, De Santis (2014) investigates the impact of Troika’s (European Commission/ECB/International Monetary Fund) bailout programs and credit rating downgrades on bond markets in several EA countries.Footnote 4 He finds that while Greece’s and Portugal’s credit rating downgrades led to an increase in the sovereign spreads of EA countries, news announcements associated with Greece’s, Portugal’s and Ireland’s bailout packages triggered a decline in bond prices. These studies suggest that news announcements have significant impacts on the European bond markets.

The closest paper to ours in terms of methodology and issues addressed by previous studies on bond markets, is that of Ehrmann and Fratzscher (2017). Using the “identification through heteroskedasticity” approach of Rigobon (2003) they examine the contemporaneous spillover effects across several EA countries, which are interpreted as integration, fragmentation and contagion.Footnote 5 Their findings show that the EDC actually led to a reduction in the return spillover effects from German bond market to other bond markets compared to the GFC. Their observation suggests that while before the EDC, bond markets were integrated, since the start of the EDC bond markets experienced fragmentation. The exceptions were Italian and Spanish yields, which experienced an increase in their bidirectional spillovers and were less affected by the German shocks. Consistent with this view, the studies of Battistini et al. (2014), Caporin et al. (2018) and Claeys and Vasicek (2014) also provide evidence of fragmentation in the bond markets. Our study differs from Ehrmann and Fratzscher (2017) by exploring the time-varying contemporaneous spillovers between Germany and GIPS equity markets and the impacts of financial assistance programs and credit rating downgrades on these spillovers.

Given that European countries are related to each other by the joint monetary policy transmission mechanism and shared default risk via the European Financial Stability Facility and European Stability Mechanism programs (Alter and Beyer 2014), one would expect shocks to be transmitted from bond to equity markets. Indeed, several papers have investigated the relations between these markets and show that the EDC has affected not only European bond markets, but also equity markets in EA and even non-EA countries. For example, Louzis (2015) applies the generalized forecast error variance decomposition framework in investigating the return (price) and volatility (uncertainty) spillovers among the equity, bond, foreign exchange and the money markets in Europe.Footnote 6 He shows that Greek bond market volatility spills over to the other European markets. Moreover, he finds that during the EDC the periphery EA stock markets have the highest degree of spillover to the other markets. In addition, Stracca (2015) examines the global implications of the EDC on the equity, bond and foreign exchange markets outside Europe. Considering 40 non-EA countries of which 19 belong to the OECD, the author documents that the EDC led to an increase in the global risk aversion, as shown by the movements of the VIX, respectively, a decrease in financial stocks which dropped by half a percentage point. The main drivers of the EDC’s international transmissions are found to be the trade exposure to the EA, countries’ financial integration with the EA and financial development.

It has further been documented that the GFC and EDC had different effects on both European bond and equity markets. For instance, Gentile and Giordano (2014) examine the number of short- and long-run connections, and their direction in European sovereign bond spreads and stock returns applying Granger causality tests and a VEC model.Footnote 7 They show that during the GFC and EDC there was an increase in the transmission of shocks and the direction of causality was different in bond and equity markets. Specifically, in the case of stock markets (bond markets), during the GFC, Germany and France (Germany, Ireland and Portugal) influenced the other EA markets, whereas during the EDC, Greece, Italy and Portugal (Germany and Spain) affected the EA markets. Similarly, Samitas and Tsakalos (2013) provide evidence of increased correlations between the equity markets in Greece and several EA countries during both the GFC and the Greek debt crisis.Footnote 8 However, they argue that the Greek debt crisis had a lower than expected impact on the correlation between the Greek stock market and European stock markets. These findings are contrary to those of other studies (Ehrmann and Fratzscher 2017; Caporin et al. 2018; Claeys and Vasicek 2014) which showed that the EDC in fact led to either a decrease or no change in the transmission of shocks among European equity markets.

Besides studies that assess the impacts of financial crises on the transmission of shocks, several studies investigate the impact of financial support programs and credit rating downgrades on European equity markets. Kosmidou et al. (2015), for example, show the impact of credit rating downgrades and rescue programs on the banking, financial and real sectors of the Greek capital market. They indicate that the credit rating announcements had negative impacts on the returns of Greek banking sector firms. In contrast, Troika’s bailout programs had positive impacts on both the financial and real economy of the Greek capital market. The importance of these events is also documented in Bhanot et al. (2014) who analyze the relation between the GIPS stock markets and Greek sovereign yield spreads around these events and during the Greek debt crisis. They conclude that an increase in the yield spread of Greek bonds led to a decline in stock market returns, which was driven by the Greek rating downgrades, whereas news about bailout possibilities had positive effects on the stock markets.

The extant literature investigates the impacts of financial crises on the spillover effects among European financial markets, and announcement of financial assistance programs and credit rating downgrades on these markets. These studies show that the GFC and EDC affected the transmission of shocks from one market to other markets differently. While some studies show that these crises increased the spillover effects, other studies demonstrate that there was a decrease in spillovers. One important aspect, however, which is not taken into consideration and may be one of the reasons for this disagreement is that European markets are highly integrated and trade simultaneously. Thus, the transmission of shocks may occur instantaneously in addition to having a delayed effect. Our study extends the above studies and contributes to the literature in that we explore the contemporaneous spillover effects in equity markets. Moreover, we assess the contribution of financial assistance programs and credit rating downgrades on the return spillovers from Germany to GIPS and the other way around, rather than only on equity markets. From an empirical perspective, we use the structural VAR (SVAR) and, the approaches of Lütkepohl’s (2013) and Lanne and Lütkepohl’s (2010) which allow us to estimate the direction of causality among the German and GIPS equity markets. In addition, the use of a rolling window estimation provides us with a better understanding of the transmission of return shocks across European equity markets over time, and especially during the GFC and EDC.

3 Model

In this study, we examine the spillover effects between Germany (GE) and Greece (G), Italy (I), Portugal (P) and Spain (S).Footnote 9 We apply a structural VAR (SVAR) model that is well suited to investigate the transmission of shocks, especially during the GFC and EDC, among these stock markets. The main challenge in the estimation of the SVAR model is the identification of the contemporaneous relations among equity markets without imposing restrictions on the direction of these relations. To achieve identification, we employ the approach of Lütkepohl (2013), and specifically Lanne and Lütkepohl (2010) which relies on the heterogeneity of the volatility in equity returns.

We compute weekly returns for all markets, i.e., \( R^i_{t}= \log (P^i_{t})-\log (P^i_{t-1})\), where \(P^i_{t}\) is the weekly price for country i. We model the returns using a SVAR process:

where \(R_{t}\) is a (\(2\times 1\)) vector representing the weekly returns, i.e.,

where \({R_{t}}^{GE}\) consists of the German equity returns and \(\textit{j}\) represents either the Greek, Italian, Portuguese or Spanish stock market.Footnote 10 The coefficient c is a (\(2\times 1\)) vector of constants and \(\mathbf {\Phi (L)}\) is a (\(2\times 2\)) matrix capturing lagged effects. The (\(2\times 2\)) matrix \(\mathbf {A}\) captures the contemporaneous relations among returns, i.e.,

where \(\alpha _{12}\) captures the spillover effect from market j to the German stock market, and \(\alpha _{21} \) captures the spillover effect from the German stock market to each of the GIPS stock markets j. The other parameters are defined likewise.

The starting point for the identification of \(\mathbf {A}\) is to estimate the reduced form VAR between Germany and each of the GIPS countries separately by premultiplying Eq. (1) by \(\mathbf A ^\mathbf -1 \):

The coefficients of Eq. (4) can be estimated by OLS and are related to the structural coefficients by: \( c^{*}= \mathbf {A^{-1}}c, \mathbf {\Phi (L)}^{*}=\mathbf {A^{-1}}\mathbf {\Phi (L)}, u_{t}=\mathbf {A}^\mathbf {-1}\varepsilon _{t} \), where and \(u_{t}\sim N(\mathbf {0}, \mathbf {\Omega })\) where \(\mathbf {\Omega } = \mathbf {A^{-1}} \mathbf {\Sigma }\)\(\mathbf {A^{-1^{'}}}\), where \(\mathbf {\Sigma }\) is the covariance matrix of the residuals \(\varepsilon _t\).

When analyzing these contemporaneous relations among markets, we face an endogeneity problem. That is, the transmission of return shocks between Germany and GIPS equity markets could occur instantaneously. Traditionally, this endogeneity problem is often resolved through use of sign restrictions for the identification of the matrix \(\mathbf {A}\) or by assuming that changes in one variable can affect the other variable immediately, but not vice versa, i.e., by making use of Choleski factorization (e.g., Alter and Beyer 2014; Louzis 2015; Antonakakis and Vergos 2013). However, in this paper, we make use of the “identification through heteroskedasticity” approach.

To solve the simultaneity problem, Lanne and Lütkepohl (2010) propose an approach based on heteroskedasticity in variances of the reduced form VAR.Footnote 11 Following Lanne and Lütkepohl (2010), we assume that the residuals of the reduced form VAR, \(u_{t}\) in Equation (4) are from a mixture of two independent Normal distributions, i.e.,

where we assume that \(\mathbf {\Omega _1} \ne \mathbf {\Omega _2}\). To identify \(\mathbf {A}\), we impose two further restrictions. First, we assume that structural shocks, \(\varepsilon _{t} \) from Eq. (1) are uncorrelated, i.e., the variances of \(\mathbf {\varepsilon }_{t}\), \(\mathbf {\Sigma _{1}}\) and \(\mathbf {\Sigma _{2}}\) are diagonal matrices. Moreover, given that \(\mathbf {A}\) is chosen such that its diagonal elements are unrestricted, we normalize the structural variances in the first regime, i.e., \(\mathbf {\Sigma _{1}} = \mathbf {I}\), and \(\mathbf {\Sigma _{2}} = \mathbf {\Phi }\). Second, the parameters from Eq. (4) are time invariant.Footnote 12 If these assumptions hold, then we can decompose \(\mathbf {\Omega }\) such that matrix \(\mathbf {A}\) is uniquely identified,

where \(\mathbf {\Psi }\) is a (\(2\times 2\)) diagonal matrix with distinct elements showing the change in variance from the \(\mathbf {\Omega }_{\mathbf {1}}\) to \(\mathbf {\Omega }_{\mathbf {2}}\).

We estimate the parameters of our SVAR using Quasi-Maximum Likelihood (QML), where the log-likelihood function is given as,

where \(\gamma \) is the mixture probability, \(0<\gamma <1\). Given the fact that the elements of matrix \(\mathbf {A}\) vary freely, we normalize the estimated matrix \(\mathbf {A}\) such that its diagonal elements are one. In this case, its off diagonal elements can be written as:

The t-statistics for the \(\widehat{\alpha _{12}}\) and \(\widehat{\alpha _{21}}\) are computed using the Bollerslev-Wooldrige standard errors.

4 Data

In line with the extant literature (Savva and Aslanidis 2010; Guidi and Ugur 2014; Baele and Inghelbrecht 2010; Baele et al. 2007; Caporale and Spagnolo 2011) we employ weekly data covering the period from January 2003 to December 2014.Footnote 13 The data are obtained from Thomson Reuters DataStream and consist of the Morgan Stanley Capital International (MSCI) equity return indices for Greece, Italy, Portugal, Spain and Germany.

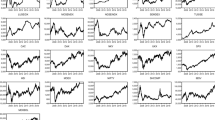

European stock market indices. Note: This figure shows the MSCI indices for Germany, Greece, Italy, Portugal and Spain. We cover the period from January, 2003 to December, 2014. a Germany. b Greece. c Italy. d Portugal. e Spain.

In Fig. 1, we provide time series plots of the equity indices. We notice a sharp decline in the equity markets due to the GFC in September 2008 and smaller declines over the period January 2010 to December 2012 related to the EDC. The figure clearly highlights that the EDC affected equity markets to varying degrees.

Table 1 presents summary statistics for equity returns in Germany and each of the GIPS countries. As can be seen, the highest variability of the returns based on minimum and maximum is in Germany and Italy, while the highest volatility is in Greece. The negative skewness on returns suggests that negative shifts in the German and GIPS stock markets occur more often than positive shifts. The presence of excess kurtosis in all countries implies that large shifts occur more often than is the case of normally distributed series.

Table 2 reports the event dates regarding financial assistance programs and both credit rating downgrades to and close to non-investment grade. The main reason for taking into account the bailout packages is that financial markets might consider these events as a signal of European governments’ willingness to use public funds to protect private investors (Mink and De Haan 2013). At the same time, financial support could also be understood as evidence that other countries might receive financial support. Further, there are two reasons for taking into consideration the credit rating downgrades. First, credit rating downgrades provide information about a country’s ability to meet its debt obligations. Therefore, these downgrades are important for investors who might take them into consideration when estimating the discount rate and expected flow of dividend from stocks, affecting stock valuations. Second, a credit rating downgrade might affect a country’s ability to borrow in international markets, and thus contribute to a credit crunch, which negatively impacts the stock market (Ferreira and Gama 2007). We present the credit rating downgrades as reported by Standard and Poor’s (S&P), Moody’s Investors Service (Moody’s) and Fitch’s agencies. Particularly, we take into consideration the announcement for Greece’s, Portugal’s and Spain’s downgrades to non-investment grade and rescue programs. Given that Moody’s downgrade of Spain refers to the downgrade to junk status of it’s five biggest regions, i.e., Catalonia, Andalucia, Castilla-La Mancha, Extremadura and Muricia, we also consider Spain’s downgrade close to non-investment grade by Standard and Poor’s. We include Italy’s downgrade close to non-investment grade as it has been the first Italian revision since 2006 by Standard and Poor’s.

5 Results

In this section, we begin by presenting evidence on the contemporaneous relations over the full sample period. We then show the impacts of GFC and EDC on these relations by estimating the model presented in Sect. 3 for each of the four periods, i.e., pre-GFC, GFC and, first and second phase of the EDC. Further, we estimate the time-varying contemporaneous relations. Finally, we assess whether the financial assistance programs and credit ratings downgrades affected the dynamics of contemporaneous spillover effects between the German and GIPS equity markets.

5.1 Contemporaneous relations

We start our analysis with the estimation of the reduced form VAR model using Eq. (4) over the full sample period and all four subperiods as defined below. We estimate these reduced for VARs, with a lag length of five, which is the optimal lag length over the whole sample period as suggested by the Akaike Information Criterion. The first subperiod is from January 2005 to August 2008. The second subperiod uses Lehman Brothers’ collapse as the starting date of GFC and lasts from September 2008 until September 2009.Footnote 14 The third subperiod covers the \(\text {EDC}^\text {first phase}\), when most of the austerity measures started to be implemented and lasts from October 2009 until September 2012. The start date for the \(\text {EDC}^\text {first phase}\) coincides with investors’ concerns regarding the quality of Greek sovereign debt, which were followed shortly after, on November, by the Greek government announcement of a budget deficit twice of the previous estimates (Bhanot et al. 2014). The fourth subperiod, the \(\text {EDC}^\text {second phase}\), covers October 2012–December 2014. The starting date of this subperiod coincides with the ECB’s announcement of the Outright Monetary Transactions program and is in line with Ehrmann and Fratzscher (2017). We then use the residuals from the reduced form VAR and approaches of Lütkepohl’s (2013) and Lanne and Lütkepohl’s (2010), which allow us to identify the responses of the German stock market to changes in the returns of each peripheral European stock markets, i.e., Greece, Italy, Portugal and Spain and vice versa, the return spillover effects from Greece, Italy, Portugal and Spain to Germany.

Table 3 presents contemporaneous relations for the entire sample period, the period before the GFC, the period during the GFC and the periods during the first and second stage of the EDC. These relations have initially negative signs as they are captured by matrix \(\mathbf {A}\) which is on the left-hand side of Eq. (1). When taken to the right-hand side, the signs of the contemporaneous relations become positive. As such, an increase in the German stock market returns leads to an increase in the Greek, Italian, Portuguese and Spanish stock market returns and the other way around.Footnote 15

Analyzing the contemporaneous relations for the entire sample period (reported in Panel A), we find high and positive contemporaneous spillovers with values ranging between 0.51 and 0.70 from the German returns to GIPS returns. The coefficients suggest that a 1% increase in the German returns leads to a contemporaneous increase between 0.51 and 0.70% in GIPS returns. Vice versa, a 1% increase in GIPS returns causes a smaller increase in German returns than the other way around, varying from approximately 0.17–0.27%. These results highlight the important role of Germany in transmitting shocks to the GIPS countries. The relatively large magnitudes of these spillovers highlight the economic significance of the transmission of these shocks.

Panel B, which documents the contemporaneous relations prior to GFC, shows that shocks to German stock returns are transmitted to GIPS stock returns, with spillover coefficients ranging between around 0.40 and 0.70. In particular, a 1% increase in German returns leads to an increase in Greek, Italian, Portuguese and Spanish returns of 0.72, 0.39, 0.55 and 0.73%, respectively. These findings suggest that GIPS equity markets are moving together in response to German stock market shocks. Vice versa, GIPS returns have smaller impacts on the German returns, ranging from approximately 0.12 to 0.40. These findings indicate that the German returns are less sensitive to GIPS return shocks than the other way around.

When we consider Panel C, the spillover effects during the GFC, we notice that the magnitude of return spillover effects between Germany and GIPS is higher than in the pre-GFC period. Specifically, we find that shocks to the German returns lead to higher comovement across GIPS returns than in the opposite direction. For instance, while a 1% increase in German returns leads to an increase ranging from 0.57% in Portuguese returns to 0.80% in Greek returns, the responses of German returns to shocks in GIPS stock market returns are much smaller, with the spillover coefficients varying between 0.30 and 0.40. In sum, we conclude that the GFC has led to an intensification in the transmission of shocks between the German stock market and GIPS stock markets. This finding is somewhat in line with Claeys and Vasicek (2014) and Louzis (2015) who show that the GFC also increased the spillover effects among European bond and equity markets.

When investigating the contemporaneous relations during \(\text {EDC}^\text {first phase}\) in Panel D, we find that shocks to German stock market led to less comovement across GIPS stock markets than during the GFC. In particular, a 1% increase in German returns causes an increase in GIPS returns equal to 0.66, 0.52, 0.55 and 0.68%, respectively. Since German returns have the standard deviation of 0.03, these findings also imply that during the \(\text {EDC}^\text {first phase}\) there is an increase in GIPS returns of 1.98, 1.56, 0.65 and 2.04%. Vice versa, we find that spillover effects from GIPS returns to German returns are mostly insignificant and smaller in magnitude compared with the GFC period, with values around 0.10. The exception is the return spillover from Spain to Germany which is 0.24. These results are in line with Ehrmann and Fratzscher (2017), who interpret this decrease in the magnitude of the return spillover effects from Germany to GIPS compared to the GFC as evidence that GIPS markets are less integrated with the German market. This decline in degree of integration might be related with the fact that between 2007 and 2013 there was a reduction in the exports from peripheral countries to Germany and imports of peripheral countries from Germany (Esposito 2016; Simonazzi et al. 2013). Chambet and Gibson (2008) shows that a decrease in trade openness leads to a decrease financial integration. Moreover, while the Economic and Monetary Union membership has made the GIPS countries attractive investment destinations and led to large capital inflows, especially from Germany, during the EDC there has been a reduction in these inflows (Batavia and Nandakumar 2016; Esposito 2016). As such, it is not surprising that the GIPS equity markets are less integrated with the German equity market. In addition, when considering the correlations between German returns and GIPS returns in “Appendix 2”, we observe that during \(\text {EDC}^\text {first phase}\) there is a higher decrease in correlations than during the GFC.

When we analyze Panel E, the contemporaneous effects during the \(\text {EDC}^\text {second phase}\), we observe that German return shocks have become more important for GIPS equity market returns. For example, a 1% increase in the German returns induces an increase in Italian and Portuguese returns equal to 0.76 and 0.63%, respectively. The return spillover effects from Germany to Greece and Spain are higher than during both GFC and \(\text {EDC}^\text {first phase}\) with the values around 0.90. This increased transmission of German return shocks to Greek and Spanish returns indicates that the Greek and Spanish stock markets are more sensitive to German shocks than the other peripheral markets. When exploring the spillover effects from GIPS returns to German returns, we notice that their magnitude is, most of the time, statistically insignificant, once again, this finding is in line with Ehrmann and Fratzscher (2017).

On the whole, our analysis so far shows that the magnitude of contemporaneous spillover effects among the German and GIPS equity markets has changed considerably during the GFC and EDC. Moreover, we provide evidence of asymmetry in these relations, where contemporaneous return spillover from German stock market to GIPS stock markets is higher than the other way around. Particularly, we find that while the GFC has led to an increase in the contemporaneous spillover effects between these markets; the first phase of the EDC has actually led to a decrease in their magnitude. During the second phase of the EDC we notice an increase in the return spillover effects from Germany to GIPS. Vice versa, the return spillover effects from GIPS to Germany are similar with those during the first phase of EDC. In sum, our findings reveal the existence of asymmetry and time variation in contemporaneous relations.

5.2 Contemporaneous relations over time

To gain further insights into the contemporaneous relations, we apply a rolling window estimation. Specifically, we estimate our model for a two year window or 104 observations and roll this window forward one week at a time.Footnote 16

Figure 2 presents the time-varying contemporaneous relations between the German and GIPS equity markets covering the period from January, 2005 to December, 2014. The patterns in Fig. 2 are in line with those in Table 3. Specifically, during the GFC, we document the existence of a considerable increase in the return spillover effects between Germany and GIPS equity markets. The high magnitude of the spillover effects is persistent in the early stage of the EDC and well into 2011. In response to the German return shocks, the Greek and Italian returns started to decrease in the summer of 2011, soon followed by those of Portugal and Spain. These results emphasize the fact that during the first phase of the EDC, GIPS equity markets are less affected by the German equity market. Claeys and Vasicek (2014) and Caporin et al. (2018) find a similar pattern when investigating transmission of shocks among the European bond markets. Contrary to the findings in Table 3, Fig. 2 shows that during both phases of the EDC there are periods when shocks to German returns have high impacts on GIPS returns, and the GIPS return shocks cause a decrease in German returns. For instance, in response to German return shocks, we observe an increase in Greek returns around the beginning of 2011 and an increase in Greek, Portuguese and Spanish returns in the summer of 2013. Further, we find that an increase in the Greek returns in the summer of 2011 and 2014, and Italian returns in the summer of 2011 and summer of 2013 until the end of our sample period leads to a decrease in German stock market returns. According to Ehrmann and Fratzscher (2017) these findings indicate the existence of a “flight-to-safety” effects toward Germany. These effects from Fig. 2 are not evident in Table 3, which reflects the overall picture of the contemporaneous effects over the entire sample and each of the four periods.

Contemporaneous relation between returns. Note: this figure shows the rolling window estimates for the contemporaneous relations of the equity markets. As our data start January 2003 and we choose the window for the rolling estimation to be 2 years, we present the spillover effects from January 2005 to December 2014. a The relations between \(R_{t}^{G}\) and \(R_{t}^{GE}\). b The relations between \(R_{t}^{I}\) and \(R_{t}^{GE}\). c The relations between \(R_{t}^{P}\) and \(R_{t}^{GE}\). d The relations between \(R_{t}^{S}\) and \(R_{t}^{GE}\)

In sum, Fig. 2 highlights the impacts of the GFC and EDC on the contemporaneous spillover effects and the importance of taking into consideration their time variation. The next section further investigates the drivers of these dynamics in the contemporaneous relations context.

5.3 Explaining the contemporaneous relations

In previous sections, we emphasized the relevance of taking into account the time variation in contemporaneous spillovers and the differences in their magnitudes that are observed over time and especially during the GFC and EDC. In this section, we focus on explaining the impact of financial support programs and credit rating downgrades on the time-varying contemporaneous spillover effects shown in Fig. 2. In particular, we first calculate the mean of contemporaneous spillover effects six weeks before and after each of these events. We then use these findings and compute the absolute change in contemporaneous relations as the difference between the mean of contemporaneous spillover effects after and before each of the financial support programs and credit rating downgrades. Finally, we provide the \(\textit{t}\)-statistics which are computed by dividing the absolute change in contemporaneous relations by their sum of standard deviations six weeks before and after the events. Table 4 shows the absolute change in contemporaneous relations after each of the GIPS’s credit rating downgrade and financial assistance program as given in Table 2.

Examining the impact of financial support programs on these contemporaneous effects, we observe that Greece’s first financial assistance program has led to a significant decrease in the spillover effects from GIPS returns to German returns, and increases in the spillover effects from German returns to Italian, Portuguese and Spanish returns. This is in line with the patterns of spillover effects in Fig. 2 and indicates that in the early stage of the EDC, the Greek financial support program affected the transmission of return shocks to peripheral EA countries since these countries were confronted with similar circumstances. We find that Greece’s second financial support program significantly decreased the return spillover from Greece to Germany with − 0.006 and the spillovers from German returns to Portuguese and Spanish returns with − 0.019 and − 0.017, respectively. Portugal’s and Spain’s financial assistance programs have caused a decrease in the transmission of return shocks from GIPS equity markets to German equity market. Vice versa, the spillover effects from German returns to GIPS returns experienced a significant increase after both Portugal’s and Spain’s financial support programs. The exceptions are the return spillovers from Germany to Italy and Spain, which have decreased by − 0.007 and − 0.027, respectively, after Spain’s bailout and which also correspond with the implementation of Outright Monetary Transactions program. These results are in line with Ehrmann and Fratzscher (2017) who show that under this program there is a reduction in the return spillovers from the German bond market to the Italian and Spanish bond markets. Additionally, Altavilla et al. (2016) find that Italian and Spanish yields declined under the Outright Monetary Transactions program. Overall, our results suggest that while the transmission of GIPS return shocks to Germany’s returns decrease after the rescue programs, the transmission other way around increases. These findings are in line with De Santis (2014) who, focusing on Greece’s and Portugal’s financial assistance programs, shows that these events led to a decline in the EA sovereign yields.

We further investigate the impact of credit rating downgrades on the transmission of return shocks between German and GIPS equity markets. We find a significant decrease in the transmission of GIPS return shocks to German returns and an increase in the transmission the other way around, after Greece’s downgrades. These results are consistent with those from Panel D of Table 3, which show that during the \(\text {EDC}^\text {first\;phase}\) shocks occurring in GIPS equity market returns have smaller impacts on German equity market returns than shocks originating during the GFC. Moreover, Greece’s downgrades explain the high magnitude of return spillovers from Germany to GIPS during the early stage of the EDC, as shown in Fig. 2. On the contrary, while contemporaneous spillover effects did not change significantly after Portugal’s first downgrade, these spillovers significantly declined after the following two downgrades and Italy’s downgrade. This indicates that investors already anticipated Portugal’s and Italy’s downgrades leading to a decrease in the magnitude of contemporaneous spillover effects. Instead, Spain’s credit rating downgrades, which occurred at the end of 2012 led to an increase in contemporaneous spillover effects between German and GIPS equity market returns. These findings are consistent with those from Panel E of Table 3, which indicate that during the \(\text {EDC}^\text {second\;phase}\) there is an increase in the transmission of return shocks between Germany and GIPS, compared to the transmission during \(\text {EDC}^\text {first\;phase}\).

Overall, we find that although European governments’ willingness to provide support to Greece, Spain and Portugal has decreased the transmission of return shocks from peripheral countries to Germany, has mostly led to an increase in the transmission of German return shocks to GIPS equity markets. We show that Greece’s credit rating downgrades led to an increase in spillover effects from Germany to GIPS returns and a decrease in return spillovers the other way around. Finally, we document that while Portugal’s and Italy’s downgrades led to a decrease in contemporaneous spillover effects, Spain’s downgrades caused an increase in contemporaneous spillovers. In sum, based on the statistics in Table 4, it is evident that financial support programs and credit rating downgrades affected the contemporaneous spillovers between German and GIPS stock markets.

6 Conclusion

In this paper, we examine the contemporaneous spillover effects between the German and GIPS equity markets. Using Lütkepohl’s (2013) and Lanne and Lütkepohl’s (2010) approaches and, a rolling window estimation, we explain the extent to which these relations vary over time, especially during financial crises. Moreover, we investigate the impact of financial assistance programs and credit rating downgrades on the time-varying contemporaneous spillover effects at the return level.

Our analyses yield several interesting findings. First, we document the existence of asymmetric contemporaneous spillover effects. We find that an increase in German returns had a greater impact on GIPS returns than the other way around. Second, we observe that while during the GFC there was an increase in the magnitude of contemporaneous spillover effects, during the first phase of the EDC there was a decrease in their magnitude. In line with Ehrmann and Fratzscher (2017), this reduction in the spillover effects indicates that GIPS equity markets are less integrated with the German equity market. Importantly, however, during the second phase of the EDC, we notice an increase in return spillover from Germany to GIPS equity markets. Third, we show the impacts that financial support programs and credit rating downgrades had on the direction of return spillover effects among our stock markets. We notice that financial assistance programs have decreased the return spillovers from GIPS to Germany and in most cases increased the spillovers the other way round. Credit rating downgrades, e.g., of Portugal and Italy, reduced the contemporaneous spillovers, indicating that investors have anticipated the downgrades to occur.

Our findings have several important implications. First, for regulatory authorities, central banks and governments, our findings provide a better understanding of the transmission of shocks and thus, useful information on a country’s financial stability. Second, our methodology can be used as a tool for monitoring the spillovers among markets. This can assist policy makers to implement and coordinate their policy actions that aim at controlling the transmission of shocks (Louzis 2015). Finally, the fact that financial support packages have reduced the transmission of return shocks from peripheral countries to Germany indicates that these programs have, to some degree, restored market participants’ confidence in the EA. On the whole, our analyses highlight the relevance of taking into consideration the asymmetry and time variation in contemporaneous spillovers.

Notes

The European Financial Stability Facility program was created as a temporary solution to the EDC. Starting from October 2012, the European Stability Mechanism is the permanent rescue mechanism that safeguards financial stability in Europe by providing financial assistance to the European countries. The ECB’s policies refer to its decision to purchase the government debt of the troubled EA countries under its Securities Markets Program, adopted in May 2010 and replaced by the Outright Monetary Transactions program in October 2012.

An alternative approach to examine time variation in stock market interdependence builds on the work of Manner and Candelon (2010), who use copulas to capture stock market interdependence and a sequential breakpoint test algorithm to identify time variation in interdependence.

There are several reasons for the choice of the German equity market and GIPS equity markets. First, these markets are integrated and related through trade, banking system and debt holdings which facilitate the transmission of shocks among them, especially during the European crisis (Stracca 2015). For instance, German banks have invested heavily in Greek bonds. As such, it is important to investigate whether or not the magnitude of the spillover effects has changed with the ongoing EDC. Second, Ehrmann and Fratzscher (2017) show there are relatively little spillovers in bond yields among the peripheral countries (Greece, Italy, Portugal, Spain and Ireland), except the bidirectional spillovers between Italy and Spain. They document that bond yields of the peripheral countries strongly co-move with the German bond market, and are also more affected by shocks to their own bond market. Third, Germany is an important member of the European Union which has been less affected by the EDC and has highly contributed to the European Financial Stability Facility program (now European Stability Mechanism). This has led to an increase in its influence with regard to the implementation of different policies across the Euro Area. These policies (e.g., the financial support programs, OMT program) have affected and have mainly focused on the GIPS countries, the origin of the debt crisis. In addition, the GIPS’s credit ratings have been downgraded several times between 2010 and 2012. These credit rating downgrades might negatively affect their stock markets as well as the German stock market. As such, it is essential to explore the relations between the German and GIPS returns and also to what extent the EDC has influenced them. Specifically, it is relevant to examine to what extent the GIPS markets moved away from Germany and the other way around.

Belgium, Netherlands, Finland, Austria, France, Ireland and GIPS.

Their analysis includes three core countries (Germany, France and the Netherlands) and five peripheral countries of the EA (GIPS and Ireland).

See also, the studies of Antonakakis and Vergos (2013) and of Claeys and Vasicek (2014) who use this method of a VAR model proposed by Diebold and Yilmaz (2012). The study of Louzis (2015) considers the EONIA rate, EUR/USD exchange rate, Ireland and GIPS bond markets and the equity markets in GIPS countries, Ireland, France, Belgium, Austria, Netherland, US and Germany.

Their investigation includes GIPS, Ireland, France, UK and Germany.

Countries included Germany, France, UK and peripheral counties, i.e., GIPS and Ireland.

In line with Cappiello et al. (2006) the German equity market can be seen as the benchmark of the EA equity markets. Moreover, Germany is one of the major European contributors to the financial assistance programs. Additionally, Germany is a leading member of EA with an influential role regarding the European politics (e.g., the implementation of austerity measures), especially during the EDC.

The use of a large multivariate specification encapsulating all markets would be ideal. However, estimation of such a large system is quite cumbersome, even more so when estimating the system over rolling windows to obtain time-varying contemporaneous spillovers, where we could expect no convergence in the likelihood due to the size of the model. This motivates us to focus on bivariate systems where we model equity returns from the peripheral countries vis-a-vis the German market.

Various methods have been put forward to use heteroskedasticity in the data for identification of structural parameters. Rigobon (2003) uses volatility regimes over different periods of time, while Ehrmann et al. (2011) and Andersen et al. (2007) use a rolling-windows approach to identify volatility regimes. Lütkepohl’s (2013) further suggests an approach based on a GARCH model, and a Markov-switching model to capture heterogeneity in the data. While all these approaches can potentially be used to achieve identification of the structural parameters, the approach of Lanne and Lütkepohl (2010) seems most flexible in our setting as we estimate the model on a rolling window to extract time-varying parameters.

Note that the assumption of time invariance only applies to the estimation window. When we take the model to the data, we estimate the structural parameters over various subsamples (pre- and post-crisis) and on the basis of rolling windows to introduce time variation.

This frequency minimizes the effects of non-synchronous data which may arise when a market is closed in one country, while another market is open in another country. Moreover, the weekly frequency is characterized by less noise and is able to better analyze the transmission of return shocks over time and during financial crises.

In addition, we assess the stability and statistical significance of contemporaneous relations using the breakpoint test based on Qu and Perron (2007), Blatt et al. (2015), and Bataa et al. (2013) (we report the Wald-type statistic as per Equation (4) of Bataa et al. (2013) as our break dates are known). “Appendix 1” reports these statistics. We show that generally the null hypotheses of constant contemporaneous spillover effects can be rejected for the structural breaks due to both GFC and EDC. In sum, Wald’s test emphasizes the relevance of considering contemporaneous relations over the pre-GFC, GFC, \(\text {EDC}^\text {first phase}\) and \(\text {EDC}^\text {second phase}\) periods.

As a robustness check, we also use a window of 78 observations (a period of one and a half year). We find that the results are very similar to those presented in this paper.

References

Ait-Sahalia Y, Andritzky J, Jobst A, Nowak S, Tamirisa N (2012) Market response to policy initiatives during the global financial crisis. J Int Econ 87(1):162–177

Altavilla C, Giannone D, Lenza M (2016) The financial and macroeconomic effects of the OMT announcements. Int J Cent Bank 12(3):59–57

Alter A, Beyer A (2014) The dynamics of spillover effects during the European sovereign debt turmoil. J Bank Finance 42:134–153

Andersen TG, Bollerslev T, Diebold FX, Vega C (2007) Real-time price discovery in global stock, bond and foreign exchange markets. J Int Econ 73(2):251–277

Antonakakis N, Vergos K (2013) Sovereign bond yield spillovers in the Euro zone during the financial and debt crisis. J Int Financ Mark Inst Money 26:258–272

Arghyrou MG, Kontonikas A (2012) The EMU sovereign-debt crisis: fundamentals, expectations and contagion. J Int Financ Mark Inst Money 22(4):658–677

Baele L, Inghelbrecht K (2010) Time-varying integration, interdependence and contagion. J Int Money Finance 29(5):791–818

Baele L, Pungulescu C, Ter Horst J (2007) Model uncertainty, financial market integration, and the home bias puzzle. J Int Money Finance 26(4):606–630

Bataa E, Osborn DR, Sensier M, van Dijk D (2013) Structural breaks in the international dynamics of inflation. Rev Econ Stat 95(2):646–659

Batavia B, Nandakumar P (2016) Did EMU membership cause the “Dutch disease” in the PIGS nations? Glob Finance J 31:31–41

Battistini N, Pagano M, Simonelli S (2014) Systemic risk, sovereign yields and bank exposures in the euro crisis. Econ Policy 29(78):203–251

Bhanot K, Burns N, Hunter D, Williams M (2014) News spillovers from the Greek debt crisis: impact on the Eurozone financial sector. J Bank Finance 38:51–63

Blatt D, Candelon B, Manner H (2015) Detecting contagion in a multivariate time series system: an application to sovereign bond markets in Europe. J Bank Finance 59:1–13

Caporale GM, Spagnolo N (2011) Stock market integration between three CEECs, Russia, and the UK. Rev Int Econ 19(1):158–169

Caporin M, Pelizzon L, Ravazzolo F, Rigobon R (2018) Measuring sovereign contagion in Europe. J Financ Stab 34(2):150–181

Cappiello L, Engle RF, Sheppard K (2006) Asymmetric dynamics in the correlations of global equity and bond returns. J Financ Econom 4(4):537–572

Chambet A, Gibson R (2008) Financial integration, economic instability and trade structure in emerging markets. J Int Money Finance 27(4):654–675

Claeys P, Vasicek B (2014) Measuring bilateral spillover and testing contagion on sovereign bond markets in Europe. J Bank Finance 46:151–165

De Santis RA (2014) The euro area sovereign debt crisis: identifying flight-to-liquidity and the spillover mechanisms. J Empir Finance 26:150–170

Diebold F, Yilmaz K (2012) Better to give than to receive: predictive directional measurement of volatility spillovers. Int J Forecast 28:57–66

Ehrmann M, Fratzscher M (2017) Euro area government bonds—fragmentation and contagion during the sovereign debt crisis. J Int Money Finance 70:26–44

Ehrmann M, Fratzscher M, Rigobon R (2011) Stocks, bonds, money markets and exchange rates: measuring international financial transmission. J Appl Econom 26(6):948–974

Esposito P (2016) Trade creation, trade diversion and imbalances in the EMU. Econ Model 60:462–472

Ferreira MA, Gama PM (2007) Does sovereign debt ratings news spill over to international stock markets? J Bank Finance 31(10):3162–3182

Gentile M, Giordano L (2014) Financial contagion during the Lehman Brothers default and sovereign debt crisis. J Financ Manag Mark Inst 1(2):197–224

Giordano R, Pericoli M, Tommasino P (2013) Pure or wake-up call contagion? Another look at the EMU sovereign debt crisis. Int Finance 16(2):131–160

Gjika D, Horvath R (2013) Stock market comovements in Central Europe: evidence from the asymmetric DCC model. Econ Model 33:55–64

Gómez-Puig M, Sosvilla-Rivero S (2013) Granger-causality in peripheral EMU public debt markets: a dynamic approach. J Bank Finance 37(11):4627–4649

Gorea D, Radev D (2014) The euro area sovereign debt crisis: can contagion spread from the periphery to the core? Int Rev Econ Finance 30:78–100

Guidi F, Ugur M (2014) An analysis of South-Eastern European stock markets: evidence on cointegration and portfolio diversification benefits. J Int Financ Mark Inst Money 30:119–136

Kosmidou KV, Kousenidis DV, Negakis CI (2015) The impact of the EU/ECB/IMF bailout programs on the financial and real sectors of the ASE during the Greek sovereign crisis. J Bank Finance 50:440–454

Lanne M, Lütkepohl H (2010) Structural vector autoregressions with nonnormal residuals. J Bus Econ Stat 28(1):159–168

Louzis DP (2015) Measuring spillover effects in Euro area financial markets: a disaggregate approach. Empir Econ 49(4):1367–1400

Ludwig A (2014) A unified approach to investigate pure and wake-up-call contagion: evidence from the Eurozone’s first financial crisis. J Int Money Finance 48:125–146

Lütkepohl H (2013) Identifying structural vector autoregressions via changes in volatility. Adv Econom 32:169–203

Manner H, Candelon B (2010) Testing for asset market linkages: a new approach based on time-varying copulas. Pac Econ Rev 15(3):364–384

Mierau JO, Mink M (2013) Are stock market crises contagious? The role of crisis definitions. J Bank Finance 37(12):4765–4776

Mink M, De Haan J (2013) Contagion during the Greek sovereign debt crisis. J Int Money Finance 34:102–113

Qu Z, Perron P (2007) Estimating and testing structural changes in multivariate regressions. Econometrica 75(2):459–502

Rigobon R (2003) Identification through heteroskedasticity. Rev Econ Stat 85:777–792

Samitas A, Tsakalos I (2013) How can a small country affect the European economy? The Greek contagion phenomenon. J Int Financ Mark Inst Money 25:18–32

Savva CS, Aslanidis N (2010) Stock market integration between new EU member states and the Euro-zone. Empir Econ 39(2):337–351

Simonazzi A, Ginzburg A, Nocella G (2013) Economic relations between Germany and southern Europe. Camb J Econ 37(3):653–675

Stracca L (2015) Our currency, your problem? The global effects of the euro debt crisis. Eur Econ Rev 74:1–13

Syllignakis MN, Kouretas GP (2011) Dynamic correlation analysis of financial contagion: evidence from the Central and Eastern European markets. Int Rev Econ Finance 20(4):717–732

Author information

Authors and Affiliations

Corresponding author

Additional information

We thank participants at the 2017 Annual Conference of the Multinational Finance Society (MFS), 2017 Annual Conference of the Romanian Academic Economists from Abroad (ERMAS), 2016 Auckland Finance Meeting, 2016 SIRCA’s Pitching Research Symposium, the 2016 seminar at Queen’s University Belfast, the 2016 seminar Technical University of Dortmund and the 2016 seminar at University of Liverpool for helpful comments and suggestions.

Rights and permissions

About this article

Cite this article

Finta, M.A., Frijns, B. & Tourani-Rad, A. Time-varying contemporaneous spillovers during the European Debt Crisis. Empir Econ 57, 423–448 (2019). https://doi.org/10.1007/s00181-018-1480-1

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00181-018-1480-1