Abstract

This paper uses vector autoregression and Bayesian vector autoregression techniques to forecast the Indian Re/US dollar exchange rate. It extends the Dua and Ranjan (2010, 2012) model by including the domestic–foreign differential of the rate of return in stock prices as well as global oil prices as determinants of the exchange rate in addition to monetary model fundamentals (i.e. differential in money supply, interest rate and inflation), forward premium, volatility of capital flows, order flows and central bank intervention. The estimation period is July 1996–January 2017, while an analysis of the out-of-sample forecasting performance is undertaken from February 2017 to January 2019. The main findings are as follows: (i) Granger causality tests reveal that the exchange rate is granger caused by all the determinants considered, including differential of the rate of return of stock prices and global oil prices. (ii) Forecast accuracy of the extended model that includes stock market information and global oil prices is somewhat better than Dua and Ranjan (2010, 2012) model, especially at the longer end. (iii) Bayesian vector autoregressive models generally outperform their corresponding VAR variants. (iv) Turning points are difficult to predict.

Access provided by Autonomous University of Puebla. Download chapter PDF

Similar content being viewed by others

Keywords

JEL Classification

1 Introduction

Movements in exchange rates have important implications for the economy’s business cycle, trade and capital flows and are therefore crucial to understanding financial developments and changes in economic policy. Thus, timely forecasts of exchange rates can provide valuable input to policymakers and stakeholders in the sphere of international finance and trade. Nevertheless, the empirical literature is sceptical about the possibility of accurately predicting exchange rates. The seminal paper by Meese and Rogoff (1983) has shown that models based on economic fundamentals are unable to outperform a naïve random walk. Empirical research undertaken since then have provided mixed evidence on the success of economic models to predict exchange rates. No particular model seemed to have worked best uniformly at all times/horizons. Further, the volatility of exchange rates also at times have weakened the link between macroeconomic fundamentals and the exchange rate. The weak link between the fundamentals and the exchange rate has been termed “an exchange rate disconnection puzzle” (Engel, 2000).

Dua and Ranjan (2010, 2012), however, have found that macroeconomic fundamentals contribute significantly towards forecasting the INR/USD exchange rate. The underlying model includes the differential between the domestic and foreign counterparts of the following: money supply; output; interest rate; inflation; trade balance. In addition, it includes capital inflows, volatility of capital flows, order flows, forward premium and central bank intervention. The best fitting empirical model includes, besides the monetary model fundamentals (i.e. differential in money supply, output and interest rate), volatility of capital flows, order flows, forward premium and central bank intervention. The study finds that the inclusion of these additional variables, besides the monetary model fundamentals, improves the forecasts of the exchange rate.

This paper extends Dua and Ranjan (2010, 2012) study in two ways. First, based on Hau and Rey (2006); Aggarwal (1981); Branson (1986) and Sahoo et al. (2018), this paper extends the model estimated by Dua and Ranjan (2010, 2012) to include the differential of rate of return in stock prices and global oil prices as additional variables that can influence the exchange rate. With increasing integration with the global economy, changes in the stock market conditions may have an influence on the exchange rate. Global oil prices have a significant impact on exchange rates and also improve the forecasts of the exchange rates (Salisu et al., 2021). Second, Dua and Ranjan (2010, 2012) estimate the model using monthly data from July 1996 to December 2006 while out-of-sample forecasting performance is evaluated from January 2007 to June 2008. This paper extends the time period of estimation from July 1996Footnote 1 to January 2017, with the out-of-sample forecasting performance evaluated from February 2017 to January 2019.

Estimation is conducted in a VAR framework as well as in a Bayesian VAR (BVAR) model. The study also compares the forecast performance of the VAR model with the BVAR model. The rest of the paper is organised as follows. Section 2 reviews the exchange rate models. Section 3 explains the empirical model used in the study. Section 4 enumerates the econometric methodology, while Sect. 5 gives the empirical results. Section 6 concludes the paper.

2 Exchange Rate Models

2.1 Purchasing Power Parity, Monetary and Portfolio Balance Models

The literature on the modelling of the exchange rate ranges from the traditional PPP theory, monetary models and portfolio balance models to models incorporating capital flows and intervention by the central bank to the more recent models based on the microstructure of the foreign exchange markets. Dua and Ranjan (2010, 2012) document a comprehensive review of the evolution of models explaining exchange rate determination. The description below is based on the review in Dua and Ranjan (2010, 2012).

The earliest and simplest model of exchange rate determination, known as the purchasing power parity (PPP) theory, represented the application of the “law of one price”. This states that arbitrage forces will lead to the equalisation of goods prices internationally once the prices are measured in the same currency. It was observed initially that there were deviations from PPP in the short-run, but in the long-run PPP holds in equilibrium. Reasons for the failure of PPP, however, have been attributed to heterogeneity in the baskets of goods considered for construction of price indices in various countries, presence of transportation cost, imperfect competition in the goods market and increase in the volume of global capital flow particularly during the last few decades.

The failure of PPP models gave way to monetary models, which took into account the possibility of capital/bond market arbitrage apart from the goods market arbitrage assumed in the PPP theory. In the monetary models, it is the money supply in relation to money demand in both home and foreign countries, which determines the exchange rate. The prominent monetary models include the flexible and sticky-price monetary models of exchange rates as well as the real interest differential model and Hooper–Morton’s extension of the sticky-price model. In this class of asset market models, domestic and foreign bonds are assumed to be perfect substitutes.

The flexible-price monetary model (Frenkel, 1976) assumes that prices are perfectly flexible. Consequently, changes in the nominal interest rate reflect changes in the expected inflation rate. A relative increase in the domestic interest rate compared to the foreign interest rate implies that the domestic currency is expected to depreciate through the effect of inflation, which causes the demand for the domestic currency to fall relative to the foreign currency. In addition to flexible prices, the model also assumes uncovered interest parity, continuous purchasing power parity and the existence of stable money demand functions for the domestic and foreign economies.

In the sticky-price monetary model (originally due to Dornbusch, 1976), changes in the nominal interest rate reflect changes in the tightness of monetary policy. When the domestic interest rate rises relative to the foreign rate of interest, it is because there has been a contraction in the domestic money supply relative to the domestic money demand without a matching fall in prices. The higher interest rate at home attracts a capital inflow, which causes the domestic currency to appreciate. Since PPP holds only in the long-run,Footnote 2 an increase in the money supply does not depreciate the exchange rate proportionately in the short-run. This model retains the assumption of stability of the money demand function and uncovered interest parity, but replaces instantaneous purchasing power parity with a long-run version.

Frankel (1979) argued that a drawback of the Dornbusch (1976) formulation of the sticky-price monetary model was that it did not allow a role for differences in secular rates of inflation. He develops a model that emphasises the importance of expectation and rapid adjustment in capital markets. The innovation is that it combines the assumption of sticky prices with that of flexible prices with the assumption that there are secular rates of inflation. This yields the real interest differential model.

Hooper and Morton (1982) extend the sticky-price formulation by incorporating changes in the long-run real exchange rate. The change in the long-run exchange rate is assumed to be correlated with unanticipated shocks to the trade balance. Accordingly, they introduced the trade balance in the exchange rate determination equation. A domestic (foreign) trade balance surplus (deficit) indicates an appreciation (depreciation) of the exchange rate.

The four models discussed above can be derived from the following equation specified in logs with starred variables denoting foreign counterparts:

where e = price of foreign currency in domestic currency

m = money supply.

y = real output.

i = nominal interest rate.

π = inflation.

tb = trade balance.

The alternative testable hypotheses are as follows:

Flexible price model: δ > 0, α > 0, ϕ < 0, β = η = 0.

Sticky-price model: δ > 0, α < 0, ϕ < 0, β = η = 0.

Real interest differential model: δ > 0, α < 0, ϕ < 0, β > 0, η = 0.

Hooper–Morton model: δ > 0, α < 0, ϕ < 0, β > 0, η < 0.

These models can be further extended to incorporate portfolio choice between domestic and foreign assets.Footnote 3 The portfolio balance model assumes imperfect substitutability between domestic and foreign assets and introduces current account in the exchange rate equation. It is a dynamic model of exchange rate determination that allows for the interaction between the exchange rate, current account and the level of wealth. For instance, an increase in the money supply is expected to lead to a rise in domestic prices. The change in prices would affect net exports, implying changes in the current account of the balance of payments. This, in turn, affects the level of wealth (via changes in the capital account) and consequently, the asset market and exchange rate behaviour. Under freely floating exchange rates, a current account deficit (surplus) is compensated by accommodating transactions in the capital account, i.e. capital account surplus (deficit). This has implications for the demand and supply of currency in the foreign exchange market, which can lead to appreciation (depreciation) of the exchange rate. Thus, the coefficient of the current account differential in the exchange rate model is hypothesised to have a positive sign. The theoretical model can be expressed (as a hybrid model) as follows:

where ca denotes current account balance and θ > 0

2.2 Capital Flows, Volatility of Capital Flows, Forward Premium

With an increase in liberalisation and opening up of the capital accounts world over, capital flows have become increasingly important in determining exchange rate behaviour.Footnote 4 The relation between capital flows and exchange rates is hypothesised to be negative (with the exchange rate defined as the price of foreign currency in domestic currency) with inflow implying purchase of domestic assets by foreigners leading to appreciation of the domestic currency when there is no government intervention in the foreign exchange market or if there is persistent sterilised intervention and vice versa for outflows.

Dua and Sen (2009) developed a model which examines the relationship between the real exchange rate, level of capital flows, volatility of the flows, fiscal and monetary policy indicators and the current account surplus and find that an increase in capital inflows and their volatility lead to an appreciation of the exchange rate. The theoretical sign on volatility can, however, be positive or negative.

The forward premium measured by the difference between the forward and spot exchange rate can provide useful information about future exchange rates.Footnote 5 According to covered interest parity, the interest differential between two countries equals the premium on the forward contracts. Thus, if domestic interest rates rise, the forward premium on the foreign currency will rise and the foreign currency is expected to appreciate. The exchange rate defined as the price of foreign currency in domestic currency and the forward premium are therefore expected to be positively related.

2.3 Microstructure Framework

The microstructure theory provides an alternative view to the determination of exchange rates. Unlike macroeconomic models that are based on public information, micro-based models suggest that some agents may have access to private information about fundamentals or liquidity that can be exploited in the short-run. A distinctive feature of the microstructure models is the central role played by transactions volume or order flows in determining nominal exchange rate changes (Medeiros, 2005; Bjonnes and Rime, 2003).

Order flow is the cumulative flow of transactions, with a positive or negative sign depending on whether the initiator of the transaction is buying or selling. An increase in order flow (i.e. an increase in the volume of positively signed transactions) will generate forces in the foreign exchange market such that there is pressure on the domestic currency to depreciate. Hence, the order flow and the exchange rate are positively related. The explanatory power or information content of order flow depends on the factors that cause it. Order flow is most informative when it is caused due to dispersion of private information amongst agents with respect to macroeconomic fundamentals (Evans and Lyons, 2005), whereas it is less informative when it is caused due to management of inventories by the foreign exchange dealers in response to liquidity shocks.

If the dealers of foreign exchange are heterogeneous and there exists information asymmetry in the market, then order flow will capture the reaction of the market (obtained from aggregating the different reactions of the dealers having different information sets) to changes in macroeconomic fundamentals and news related to changes in economic conditions. Another aspect of microstructure theory that has drawn attention is the liquidity effect of order flow. Studies in the literature have empirically tested whether the relationship between order flow and exchange rates is due to liquidity effects that are temporary in nature, such as the herding behaviour of foreign exchange dealers (Breedon and Vitale, 2004).

2.4 Intervention

With the growing importance of capital flows in determining exchange rate movements in most emerging market economies, intervention in foreign exchange markets by central banks has become necessary from time to time to contain volatility in foreign exchange markets and as a result plays an important role in influencing exchange rates in countries that have managed floating regime.

The motive of central bank intervention may be to align the current movement of exchange rates with the long-run equilibrium value of exchange rates; to maintain export competitiveness; to reduce volatility and to protect the currency from speculative attacks.Footnote 6

Intervention can be sterilised or non-sterilised. In case of non-sterilised intervention, purchase of foreign exchange (to prevent appreciation) increases money supply which reduces the rate of interest and increases demand. This leads to capital outflow on one hand and an increase in import demand on the other. All these lead to an increase in the demand for foreign currency, and hence, the exchange rate depreciates. Thus, non-sterilised intervention and exchange rates are positively related.

While non-sterilised intervention directly influences the exchange rate through the monetary channel, sterilised intervention also influences exchange rate through different channels—by changing the portfolio balance, through the signalling channel where sterilised purchase of foreign currency will lead to a depreciation of the exchange rate if the foreign currency purchase is assumed to signal a more expansionary domestic monetary policy and more recently, the noise-trading channel, according to which, a central bank can use sterilised interventions to induce noise traders to buy or sell currency. Hence, the overall effect of sterilised intervention on exchange rates is ambiguous.

Based on the above frameworks, Dua and Ranjan (2010, 2012) derive the following theoretical model:

where

capt = capital inflow.

volt = volatility of capital flows.

fdpmt = 3-month forward premia.

oft = order flow.

intt = central bank intervention.

The additional signs are as follows: θ > 0; ν < 0; ρ > or < 0; ω > 0; ψ > or < 0; and ξ > or < 0.

3 Empirical Models—Dua and Ranjan (2010, 2012) Model and Its Extension

Based on the above considerations, Dua and Ranjan (2010, 2012) estimate the following best-fit empirical model:

For variables that are nonstationary and endogenous, the signs correspond to those obtained in the cointegrating equation. In the case of exogenous variables (e.g. order flow and intervention, which are also stationary) signs and significance are determined in a vector error correction framework. The empirical signs of all the variables conform to economic theory.

The objective of the current study is to forecast INR/USD exchange rate by using the model developed by Dua and Ranjan (2010, 2012) and its extension that includes differential of rate of return on stock prices and global oil prices to examine whether the additional information on stock prices and global oil prices improve the forecast performance. Both the models are estimated from July 1996 through January 2017, and the out-of-sample forecast performance of the models is evaluated from February 2017 to December 2019.

The advantage of using the stock return differential as a predictor of exchange rates is that the stock price data is readily available. Unlike macroeconomic data,Footnote 7 there is no time lag in the publication and they are not subjected to revisions. Inclusion of oil prices is likely to improve the predictability of exchange rates as it may contain useful information for forecasting the movements in the exchange rate (Qiang et al., 2019; Salisu et al., 2021).

3.1 Exchange Rate and Stock Prices

According to the available literature, there are two main types of theoretical models that analyse the linkages between exchange rates and stock prices. The traditional approach based on “flow-oriented” models (Dornbusch and Fischer, 1980)Footnote 8 suggests that causality runs from the exchange rate to the stock prices, whereas the portfolio approach based on “stock-oriented” models (Branson, 1983; Frankel, 1983) suggests the opposite. In the first case, assuming that the Marshall–Lerner condition holds, a more competitive exchange rate will improve the trade position of an economy and stimulate the real economy through firm profitability and stock market prices (Caporale et al., 2014; Granger et al., 2000). However, there will be an increase in production costs by domestic firms that import inputs, leading to a reduction in the firms’ sales and their earnings, which in turn will lead to a decline in their stock prices. Hence, the impact of exchange rates on stock prices can be either positive or negative.

The portfolio approach (Branson, 1986, Frankel, 1983) is also called the “stock” approach. The portfolio balance theory (PBT) states that a relative increase in the stock prices of the home economy will increase the wealth of the domestic investors. This will increase the demand for money in the home economy, leading to an increase in the rate of interest. This will then lead to an inflow of foreign funds and the domestic currency will appreciate. In this case, causality flows from stock prices to the exchange rate, wherein a strong equity market is associated with currency appreciation. (Granger et al., 2000; Kollias et al., 2012; Salisu and Ndako (2018); Chen and Hsu, 2019).

The empirical literature in this regard includes Ulku and Demirci (2012) that examines PBT for eight European emerging markets and finds validity for the same. The results are based on daily and monthly data for the period January 2003 to October 2010. Salisu and Ndako (2018) lend support to the portfolio balance theory for the full OECD, the Euro area and the non-Euro area for the period May 2004–June 2017.Footnote 9

The theoretical link between stock return differential and exchange rate can also be explained by the uncovered equity parity (UEP). According to the UEP, when foreign equity holdings outperform their domestic counterparts, domestic investors are exposed to the higher exchange rate and hence repatriate some of the foreign equity to mitigate their exchange rate risk (Curcuru et al., 2014). This rebalancing usually results in the selling of foreign currency, thus, leading to foreign currency depreciation. UEP theory suggests that a strong equity market is associated with currency depreciation because of portfolio rebalancing (Chen and Hsu, 2019).

Some empirical studies provide evidence in support of the UEP.Footnote 10 The paper by Hau and Rey (2006) develops an empirical model that integrates analysis of exchange rates, equity prices, and equity portfolio flows. This study uses daily data on 17 OECD countries relative to the USA for the period 1980–2001. The study provides empirical evidence that suggests that a strong equity market is associated with currency depreciation in line with UEP theory contradicting the conventional wisdom of currency appreciation under exuberant equity market.

Curcuru et al. (2014) also find support for the UEP hypothesis when they analyse the data on U.S. investors’ monthly equity positions across 42 markets for the period January 1990 to December 2010. They show that U.S. investors rebalance away from equity markets that recently performed well and move into equity markets just prior to relatively strong performance, suggesting tactical reallocations to increase returns rather than reduce risk.

Chen and Hsu (2019) examine daily exchange rate predictability with stock return differentials using the seven most-traded currencies, the USD, EUR, JPY, GBP, AUD, CHF and CAD. USD is used as the numeraire. The results of the study are also consistent with UEP theory. They provide evidence that exchange rate changes are predictable with stock return differentials.

Empirical literature examines the causality link between stock prices and the exchange rate. Studies report either unidirectional or bidirectional causal relationship between exchange rate and stock prices.Footnote 11 Xie et al. (2020) examine the exchange rate-stock price nexus for a group of advanced and emerging countries. They employ bootstrapped panel Granger non-causality tests and find that the stock prices are helpful for predicting the exchange rates, but not vice versa.

The empirical literature supports strong correlation between stock prices and exchange rate in advanced and developed economies as suggested by Curcuru et al. (2014); Hau and Rey (2006); Melvin and Prins (2015); Chen and Hsu (2019). However, the evidence for the emerging markets is weak.Footnote 12 Bahmani–Oskooee and Sujata Saha (2015), Lin (2012) shows that where capital mobility is low, economic integration acts as the cause of the linkage, and thus, it supports the flow-orientated model. But where capital mobility is more, financial integration acts as the cause of the linkage which in turn favours the stock-oriented model. They also suggest that the relationship between exchange rate and stock prices is sensitive to the frequency of data used, study period chosen, the country considered, and other macro variables included in the model. Lin (2012) also finds that the co-movement between exchange rates and stock prices becomes stronger during crisis periods when compared with relatively normal periods.

Thus, empirical evidence suggests that relationship between the exchange rate markets and the stock markets are not homogeneous across all the economies examined. The sign of the correlation between stock return differentials and exchange rate movements is ambiguous in theory. The portfolio balance approach suggests that strong equity markets are associated with exchange rate appreciation, while UEP suggests that strong equity markets are associated with exchange rate depreciation. Nevertheless, empirical literature provides an indication about exchange rate predictability using information from stock markets.

3.2 Exchange Rate and Oil Prices

The exchange rate is one of the important channels through which the effect of international crude oil price shock is passed to the financial markets and the economy. According to the theoretical literature, the link between oil price and the exchange rate is analysed from different channels.Footnote 13 First, according to the terms of trade channel an oil price increase will be followed by a depreciation of currencies in those countries with large oil dependence in the tradable sector since the price level in those countries will increase.Footnote 14 Second, through the wealth and portfolio channels an increase in oil prices, leads to transfer of wealth to oil exporting countries, and this is reflected in an improvement in the current account balance, so that currencies of oil exporting countries are expected to appreciate while currencies of oil importers are expected to depreciate after an oil price increase.

However, as explained by Turhan et al. (2014) and Qiang et al. (2019), the link between the oil exchange rates may be positive or negative, and it may also change from one period to another. Turhan et al. (2014) examines the dynamic relationship between oil prices and exchange rates in G20 countries and find a negative correlation between oil prices and exchange rates. Ju et al. (2014) study the macroeconomic effects of China’s international crude oil price shocks and empirically find that oil price shocks have a negative impact on China’s GDP and exchange rate.

Qiang et al. (2019) discuss different channels through which an oil shock can affect an oil-importing country. An increase in international oil price leads to a commodity price rise and hence inflation in the economy. This increases the cost of exporting goods in the economy; lower the cost of importing goods and will eventually cause a decline in export foreign exchange earnings and an increase in the foreign exchange expenditure, thus leading to rise in exchange rate of foreign currency and fall in the exchange rate of the local currency. Inflation will also reduce the country’s real interest rates, causing capital outflows and ultimately leading to the depreciation of the national currency.

Qiang et al. (2019) concluded that international crude oil price fluctuations can also affect the exchange rate of oil-importing countries through the balance of payments, speculative trading, and expectations. However, the influence level depends on the relative degree of dependence of the country on oil imports, which cannot be generalised.

In the light of the above discussion, the empirical model estimated by Dua and Ranjan (2010, 2012)—Model 1 below—is augmented as follows:

Model 1

Model 2

The expected signs of the additional variables in the augmented model are given in Table 2.

The present study evaluates whether Model 2 can improve the forecast accuracy of Model 1 in predicting the Re/$ exchange rate.

Rates of return are computed from stock prices of India and U.S. The Indian stock prices are measured by CNX Nifty 50 index computed as average values of every month with base Nov. 1995 = 1000, and the U.S. stock prices are taken on the basis of S&P 500 index which is computed as average values of every month with base Nov. 1995 = 1000. The rate of return of Indian and US stock prices is calculated as log of average value of stock prices in the current period minus log of average value of stock prices in the previous time period. Oil prices are calculated as log difference of monthly global oil prices.

Data definitions and the sources of the variables are given in Table 14 in the appendix.

4 Econometric Methodology

This study employs vector autoregressive (VAR), VECM and Bayesian vector autoregressive (BVAR) models to estimate the Dua and Ranjan (2010, 2012) model and its augmented variant as described previously. Tests for nonstationarity are first conducted followed by tests for cointegration and Granger causality. Finally, VAR and Bayesian vector autoregressive (BVAR) models are estimated and tested for out-of-sample forecast accuracy. This section briefly describes the tests for nonstationarity, VAR and BVAR modelling, cointegration and Granger causality and tests for out-of-sample forecast accuracy.

4.1 Testing for Nonstationarity

The first econometric step in the exercise is to test whether the series is nonstationary or whether they contain a unit root. We focus on Dickey–Fuller generalised least squares (DF-GLS) test proposed by Elliot et al. (1996) and the KPSS test proposed by Kwiatkowski et al. (1992). The presence of unit roots in time series has implications for statistical inference in the classical framework, since the OLS estimators and the corresponding statistics do not have the standard asymptotic distributions. Bayesian methods are generally preferred when the testable hypothesis is the presence of a unit root. This is because traditional tests have extremely low power, especially against trend stationary alternatives (Nankervis et al., 1988). Sims (1988) therefore argues that Bayesian theory provides a more reasonable procedure for inference than classical hypothesis testing. Hence, the study also conducts the Bayesian unit root test.

According to Dua and Mishra (1999), Bayesian methods take the data as given but assume that the true parameter is random. Classical methods, on the other hand, regard the true parameter of interest as unknown and fixed and examine the behaviour of the estimator in repeated samples. Bayesian inference depends on the given sample and the posterior distribution which varies with the product of the likelihood function and the prior distribution.

According to Dua and Mishra (1999), if the model is given as \(y_{t} = \rho y_{t - 1} + \varepsilon_{t} ,{ }\) the test statistic is the square of the conventional t-statistic for \(\rho = 1\) and is compared with the Schwarz criterion, which has an asymptotic Bayesian justification and is considered as the asymptotic Bayesian critical value. This is approximately given as

where \(\sigma_{\rho }^{2} = \sigma^{2} /\sum y_{t - 1}^{2}\), \(\sigma^{2}\) is the variance of et and for monthly data s = 12.

‘Alpha’ gives the prior probability on the stationary part of the prior; the remaining probability is concentrated on \(\rho = 1\). The choice of the prior weight can have a significant effect on the statistic given above. “Marginal Alpha” is the value for alpha at which the posterior odds for and against the unit root are even. A higher value of “marginal alpha” favours the presence of unit root. Since the first and last terms in the expression for the critical value are constant for a given prior and data, a small \(\tau\) favours no unit root. Therefore, if t2 is greater than \( \tau\), we reject the null hypothesis of a unit root.

Sims (1988) considers a non-informative prior in the unit root test proposed under Sims (1988).Footnote 15

If two of these three tests indicate nonstationarity for any series, we conclude that the series has a unit root.

4.2 VAR, BVAR and VECM Modelling

A vector autoregressive (VAR) model offers an approach, particularly useful for forecasting purposes. This method is multivariate and does not require specification of the projected values of the exogenous variables. Economic theory is used only to determine the variables to include in the model.

Although the approach is “atheoretical”, a VAR model approximates the reduced form of a structural system of simultaneous equations. VAR model does not totally differ from a large-scale structural model. Rather, given the correct restrictions on the parameters of the VAR model, they reflect mirror images of each other.

The VAR technique uses regularities in the historical data on the forecasted variables. Economic theory only selects the economic variables to include in the model. An unrestricted VAR model (Sims, 1980) is written as follows:

where y = an (n × 1) vector of variables being forecast;

A(L) = an (n × n) polynomial matrix in the back-shift operator L with lag length p, i.e. \(AL = A_{1} L + A_{2} L^{2} + \ldots \ldots \ldots . + A_{p} L^{p}\).

C = an (n × 1) vector of constant terms; and

e = an (n × 1) vector of white noise error terms

The model uses the same lag length for all variables. There is one serious drawback of the VAR model that over parameterisation produces multicollinearity and loss of degrees of freedom that can lead to inefficient estimates and large out-of-sample forecasting errors. One solution excludes insignificant variables/lags based on statistical tests.

An alternative approach to overcome over-parameterisation uses a Bayesian VAR model is used as described in Litterman (1981), Doan et al. (1984), Todd (1984), Litterman (1986), and Spencer (1993). Instead of eliminating longer lags and/or less important variables, the Bayesian technique imposes restrictions on these coefficients on the assumption that these are more likely to be near zero than the coefficients on shorter lags and/or more important variables. If, however, strong effects do occur from longer lags and/or less important variables, the data can override this assumption. Thus, the Bayesian model imposes prior beliefs on the relationships between different variables as well as own lags of a particular variable. If these beliefs (restrictions) are appropriate, the forecasting ability of the model should improve. The Bayesian approach to forecasting, therefore, provides a scientific way of imposing prior or judgmental beliefs on a statistical model. Several prior beliefs can be imposed so that the set of beliefs that produces the best forecasts is selected for making forecasts. The selection of the Bayesian prior, of course, depends on the expertise of the forecaster.

The restrictions on the coefficients specify normal prior distributions with means zero and small standard deviations for all coefficients with decreasing standard deviations on increasing lags, except for the coefficient on the first own lag of a variable that is given a mean of unity. This so-called Minnesota prior was developed at the Federal Reserve Bank of Minneapolis and the University of Minnesota.

The standard deviation of the prior distribution for lag m of variable j in equation i for all i, j, and m–S(i, j, m) can be expressed as function of a small number of hyper parameters: w, d, and a weighting matrix f(i,j). This allows the forecaster to specify individual prior variances for a large number of coefficients based on only a few hyperparameters. The standard deviation is specified as follows:

The term si equals the standard error of a univariate autoregression for variable i. The ratio si/sj scales the variables to account for differences in units of measurement and allows the specification of the prior without consideration of the magnitudes of the variables. The parameter w measures the standard deviation on the first own lag and describes the overall tightness of the prior. The tightness on lag m relative to lag 1 equals the function g(m), assumed to have a harmonic shape with decay factor d. The tightness of variable j relative to variable i in equation i equals the function f(i, j).

To illustrate, assume the following hyperparameters: w = 0.2; d = 2.0; and f(i, j) = 0.5. When w = 0.2, the standard deviation of the first own lag in each equation is 0.2, since g(1) = f(i, j) = si/sj = 1.0. The standard deviation of all other lags equals 0.2[si/sj{g(m)f(i, j)}]. For m = 1, 2, 3, 4, and d = 2.0, g(m) = 1.0, 0.25, 0.11, 0.06, respectively, showing the decreasing influence of longer lags. The value of f(i, j) determines the importance of variable j relative to variable i in the equation for variable i, higher values implying greater interaction. For instance, f(i, j) = 0.5 implies that relative to variable i, variable j has a weight of 50%. A tighter prior occurs by decreasing w, increasing d, and/or decreasing k. Examples of selection of hyperparameters are given in Dua and Ray (1995), Dua and Smyth (1995), Dua and Miller (1996) and Dua and Mishra (1999), Dua and Ranjan (2010, 2012).

The BVAR method uses Theil’s (1971) mixed estimation technique that supplements data with prior information on the distributions of the coefficients. With each restriction, the number of observations and degrees of freedom artificially increase by one. Thus, the loss of degrees of freedom due to overparameterisation does not affect the BVAR model as severely.

The above description of the VAR and BVAR models assumes that the variables are stationary. If the variables are nonstationary, they can continue to be specified in levels in a BVAR model because as pointed out by Sims et al. (1990, p.136) “……the Bayesian approach is entirely based on the likelihood function, which has the same Gaussian shape regardless of the presence of nonstationarity, [hence] Bayesian inference need take no special account of nonstationarity”. Furthermore, Dua and Ray (1995) show that the Minnesota prior is appropriate even when the variables are cointegrated.

In the case of a VAR, Sims (1980) and others, e.g. Doan (2018), recommend estimating the VAR in levels even if the variables contain a unit root. The argument against differencing is that it discards information relating to comovements between the variables such as cointegrating relationships. The standard practice in the presence of a cointegrating relationship between the variables in a VAR is to estimate the VAR in levels or to estimate its error correction representation, the vector error correction model, VECM. If the variables are nonstationary but not cointegrated, the VAR can be estimated in first differences.

The possibility of a cointegrating relationship between the variables is tested using the Johansen and Juselius (1990) methodology. The concept of Granger causality can also be tested in the VECM framework. For example, if two variables are cointegrated, i.e. they have a common stochastic trend, causality in the Granger (temporal) sense must exist in at least one direction (Granger, 1986; 1988). Since Granger causality is also a test of whether one variable can improve the forecasting performance of another, it is important to test for it to evaluate the predictive ability of a model.

4.3 Evaluation of Forecasting Models

Evaluation of the forecasting models is based on RMSE, Theil’s U (Theil, 1966), and the Diebold–Mariano (1995) test. The models are initially estimated using monthly data over the period July 1996 to January 2017 and tested for out-of-sample forecast accuracy from February 2017 to January 2019. Recursive forecasts are generated from one-through twelve-months-ahead and out-of-sample forecast accuracy of estimated models is assessed. The forecast accuracy of the VAR technique versus the BVAR method is also evaluated.

4.3.1 Thiel’s Inequality Coefficient: Quadratic Loss Criteria

To test for accuracy, the Theil coefficient that implicitly incorporates the naïve forecasts as the benchmark is used. If At+n denotes the actual value of a variable in period (t + n), and tFt+n the forecast made in period t for (t + n), then for T observations, the Theil U-statistic is defined as follows:

The U-statistic measures the ratio of the root mean square error (RMSE) of the model forecasts to the RMSE of naive, no-change forecasts (forecasts such that tFt+n = At). The RMSE is given by the following formula:

A comparison with the naïve model is, therefore, implicit in the U-statistic. A U-statistic of 1 indicates that the model forecasts match the performance of naïve, no-change forecasts. A U-statistic > 1 shows that the naïve forecasts outperform the model forecasts. If U is < 1, the forecasts from the model outperform the naïve forecasts. The U-statistic is, therefore, a relative measure of accuracy and is unit-free.

Since the U-statistic is a relative measure, it is affected by the accuracy of the naïve forecasts. Extremely inaccurate naïve forecasts can yield U < 1, falsely implying that the model forecasts are accurate. This problem is especially applicable to series with trend. The RMSE, therefore, provides a check on the U-statistic and is also reported.

4.3.2 Modified Diebold Mariano (DM) Test

The Diebold–Mariano test compares the forecast performance of alternative models; i.e., it tests the null hypothesis of no difference in the accuracy of two competing forecasts. Let \(\mathop Y\limits^{ \wedge }_{1t}\) and \(\mathop Y\limits^{ \wedge }_{2t}\), where t = 1,2…n, be a pair of h-step ahead forecasts of Yt and e1t and e2t be the associated forecast errors. If g(e) be a function (e.g. mean square error) of the forecasts errors, then the null hypothesis of equality of expected forecast performance is: E[g(e1t)–g(e2t)] = 0. Define dt = g(e1t)–g(e2t); t = 1,2,…n. For optimal h-step ahead forecasts, the sequence of forecasts errors follows a moving average process of order h–1. Therefore, it is assumed that for h-step ahead forecasts, all autocorrelations of order h or higher of the sequence dt are zero. Then, the variance of \(\overline{d} \;( = n^{ - 1} \sum\limits_{t = 1}^{n} {d_{t} )}\) is asymptotically,

where \(\gamma_{k}\) is the kth autocovariance of dt. This autocovariance can be estimated by

The Diebold–Mariano test statistic is given by

where \(\mathop V\limits^{ \wedge } (\overline{d} )\) is the estimated variance of \(\overline{d}\). Under the null hypothesis, Diebold–Mariano test statistic has an asymptotic standard normal distribution.

Harvey et al. (1997) note that the Diebold–Mariano test could be seriously over-sized as the prediction horizon, h, increases. They therefore provide a modified Diebold–Mariano test statistic

Harvey et al. also recommend a further modification of comparing the statistics with critical values from the student’s t distribution with (n–1) degrees of freedom, rather than from the standard normal distribution.

5 Empirical Results

The empirical estimation is initiated by testing the variables for stationarity. Tests for the existence of cointegrating relationship(s) and granger causality are conducted. To estimate VAR models, if all variables are nonstationary and integrated of the same order, the Johansen test is conducted for the presence of cointegration. If a cointegrating relationship exists, the VAR model can be estimated in levels. The concept of Granger causality can also be tested in the VECM framework. BVAR models are also estimated, and the out-of-sample forecast accuracy is tested.

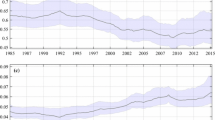

A statistical analysis of the exchange rate over the period under consideration shows the volatility of the exchange rate. Table 3 reports the summary statistics of the exchange rate over the full period and sub-periods. The summary statistics reveal that while standard deviation in the estimation period (July 1996–Jan. 2017) is 8.33 and in the out-of-sample forecasting period (Feb. 2017–Jan. 2019) is 3.06, the standard deviation for the entire period is as high as 9.57 indicating volatility of the exchange rate. The forecasting period is further divided into two sub-periods (refer Fig. 1), which is February 2017–January 2018 (sub-period 1) and February 2018–January 2019 (sub-period 2). Table 3 also shows that volatility in the first sub-period is 0.92 as compared to the second sub-period, showing volatility of 2.99. This volatility is reflected in the full out-of-sample forecasting period–Feb 2017 to January 2019.

Exchange rate-Re/$

5.1 Testing for Nonstationarity

The first step in the estimation of the models is to test for nonstationarity. Three alternative tests are used, i.e. the Dickey–Fuller generalised least squares test, the KPSS test and a Bayesian unit root test based on Sims (1988).Footnote 16

If at least two of the three tests show the existence of a unit root, the series is considered as nonstationary. Tables 4 and 5 report the results for the Bayesian unit root test and the inference drawn from the classical and Bayesian unit root tests, respectively. The results suggest that apart from order flow, intervention, difference of rate of return on Indian and US stock prices and global oil prices, all other variables are nonstationary.

The Bayesian unit root test presents the following picture. The test statistic for the exchange rate, interest rate differential, differential between Indian and foreign output; differential between Indian and foreign money supply, when compared with the asymptotic Schwarz limit fails to reject the null of a unit root process. The marginal alpha’s for these variables is also high indicative of a unit root process. On the other hand, the test statistic for the order flows, central bank intervention and difference of rate of return on Indian and US stock prices and global oil prices does not reject the null of stationarity with high values of the test statistic when compared with the Schwarz limit and low values of marginal alphas.

5.2 Testing for Cointegration

We use Johansen’s FIML technique to test for cointegration between the exchange rate, interest rate differential, money supply differential, output differential, volatility of capital inflows, the forward premium and first difference of order flows and central bank intervention based on our empirical specification (Model 1). Since order flows and the official intervention are stationary, they are treated as exogenous variables in the first specification when testing for the presence of a cointegrating relationship. We then extend the model and include the difference in the rates of return on Indian and US stock prices and global oil prices as additional exogenous variables (Model 2). The appropriate order of VAR in case of Model 1 is 2 as suggested by the lag specification test. The cointegrating vector is given below. The long-run relationship captured by the cointegrating vector shows that empirical signs of all the variables conform to economic theoryFootnote 17 Footnote 18

For Model 2, the cointegrating relationship is as follows and the empirical signs of the variables conform to the economic theory.Footnote 19

Following the estimation of the error correction equations, we test for Granger causality using the vector error correction model (VECM).

The Granger causality tests, undertaken for both Models 1 and 2 using the VECM, show that all variables, namely interest rate differential, money supply differential, output differential forward premium, volatility of capital flows, order flows, central bank intervention significantly Granger cause INR/USD exchange rate. The difference between rates of return in stock prices and global oil prices also significantly Granger cause the exchange rate. Results on Granger Causality are reported in Table 6. These results thus justify the inclusion of all the variables that Granger causes the exchange rate, since these variables can potentially improve the predictive performance of the model.

Models 1 and 2 are estimated both in VAR and in BVAR frameworks, and their predictive ability is evaluated over three out-of-sample periods, viz. February 2017 through January 2018, February 2017 through January 2019 and the whole period, February 2017–January 2019. As noted earlier, the sub-period February 2017–January 2018 is relatively more stable than the other periods. Results for this period are therefore examined in detail.

5.3 Empirical Results: Out-Of-Sample Forecasts-February 2017–January 2018

5.3.1 VAR Models: February 2017–January 2018

The forecast accuracy statistics for the VAR models are reported in Table 7. The results suggest that:

-

Both models exhibit a rise in RMSE as forecast horizon increases till 6 months ahead and fluctuate after that, suggesting a decrease in forecast accuracy at least for the initial horizons.

-

3-month average Theil U-statistic consistently falls for both models. Theil U-statistic is generally lower for Model 2 as compared to Model 1, indicating that inclusion of stock market information and oil prices may produce better forecasts.

-

Modified DM test (Table 8) suggest that Model 2 performs better than Model 1 for all short-term forecast horizons and at the long-end, thus, providing some evidence in support of the fact that information on stock markets and global oil prices produces more accurate forecasts.

5.3.2 BVAR Models: February 2017–January 2018

The hyperparameter in the prior has been set as w = 0.2, d = 1, k = 0.7 for all except volatility of capital flows and differential in rate of return in stock prices, which have a tighter interaction parameter of 0.3 and 0.2, respectively.Footnote 20

Forecast accuracy statistics for the BVAR models are reported in Table 9. The modified DM test results are in Table 10.

The main findings that emerge from the BVAR framework are as follows:

-

RMSE declines towards the longer end for Model 1 and Model 2. This suggests generally forecast accuracy increases in BVAR framework with an increase in the forecast horizon.

-

3-month average Theil U-statistic generally falls with an increase in the forecast horizon.

-

Modified DM test suggests that Model 2 generally performs better than Model 1 for shorter and longer forecast horizon, implying that information on stock markets and global oil prices produces more accurate forecasts at the shorter and longer end.

5.3.3 VAR Versus BVAR Models: February 2017–January 2018

The modified Diebold Mariano test results for the comparison of VAR and BVAR for Models 1 and 2 are reported in Table 11.

-

BVAR Models 1 and 2 generally perform better than the corresponding VAR model, especially at longer and shorter horizons.

-

Figs. 4a through 4c in the appendix illustrate the 3, 6 and 9-month ahead out-of-sample forecasts made using both VAR and BVAR versions of Model 1. Likewise, Fig. 5a through 5c in the appendix report the same on the basis of Model 2. The differences between the direction of forecasts made using Model 1 and Model 2 are not obvious from the graphs. However, Fig. 5b and 5c show that in case of Model 2, both 3-month and 9-month ahead forecasts produced by BVAR framework are closer to the actual exchange rate values. The benefits of including stock market information and oil prices emerges more clearly in the Diebold–Mariano test.

-

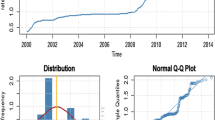

We also examine the direction of forecasts made around a turning point. This is illustrated by using Model 2 to forecast made in November 2017. The forecasts are shown in Fig. 2 and highlight that forecaster tend to miss the turning point in October 2017.

Fig. 2

Multi-period forecasts made in November 2017

5.3.4 Summary: February 2017–January 2018

-

Inclusion of stock market information and oil prices improves the accuracy of forecasts.

-

BVAR models yield more accurate forecasts than VAR models.

5.4 Empirical Results: Out-Of-Sample Forecasts-February 2018–January 2019

The forecasting performance of VAR and BVAR empirical models for Model 1 and Model 2 is compared using RMSE and Theil’s U for the second sub-period February 2018–January 2019. Forecast accuracy statistics for both VAR and BVAR are provided in Tables 12 and 13, respectively.

Results suggest the following:

-

For VAR, RMSE for both models rise with an increase in the forecast horizon implying a deterioration in forecast accuracy. Theil’s U values are greater than one indicating that VAR forecasts are worse than naïve.

-

For BVAR, RMSE increases for both the models up to 12-months ahead implying a decrease in forecast accuracy. Theil’s U values are greater than 1 implying that BVAR forecasts are worse than naïve forecasts.

-

For both VAR and BVAR models, RMSEs and Theil Us are higher than those for the sub-period February 2017–January 2018.

-

Since VAR and BVAR models yield Theil’s U greater than 1, the DM test is not reported for Model 1 versus Model 2.

-

Since in general, this sub-period exhibits inaccurate forecasts, the comparison between VAR and BVAR framework is not considered.

-

Inaccuracy of the forecast may be attributed to the high volatility in exchange rate in this period as denoted by high standard deviation. It may be noted that in 2018, a combination of rising US interest rates, a stronger dollar and the intensification of trade tensions between USA and China led to market pressures and portfolio outflows in some emerging market economies including India causing depreciation and high volatility in currency markets.

-

This period includes a turning point in July 2018. We examine the direction of forecasts made around a turning point. This is illustrated by using Model 2 to forecast from August 2018 up to January 2019. Forecasts are shown in Fig. 3 and highlight that forecaster tend to miss the turning point. Forecasts exhibit a downward trend, while the series has moved upwards.

Multi-period forecasts made in August 2018

5.5 Empirical Results: Out-Of-Sample Forecasts-February 2017–January 2019

The out-of-sample forecast period is finally considered for the full period from February 2017–January 2019.Footnote 21

-

In VAR model, RMSE increases consistently with the forecast horizon, resulting in Theil’s U greater than 1. This implies that forecast accuracy decreases with an increase in forecast horizons.

-

For BVAR models, RMSE increases consistently with forecast horizon, resulting in Theil’s U greater than 1. This further implies a decrease in forecast accuracy as the forecast horizon increases.

-

For both VAR and BVAR models, RMSEs and Theil Us are higher than those for the sub-period February 2017–January 2018.

6 Conclusion

This study forecasts INR/USD exchange rate based on two models, viz. the model estimated in Dua and Ranjan (2010, 2012) and an augmented version of the model that incorporates the differential of the rate of return in stock prices and global oil prices applying VAR and Bayesian VAR framework. The study also evaluates the forecast performance of these two frameworks. Dua and Ranjan (2010, 2012) employed a hybrid model that includes the fundamentals of the monetary and portfolio balance models as well as capital inflow volatility, forward rate, order flows, official intervention. In addition, keeping in mind the increasing linkages between stock markets across the globe, the difference between the rates of return in stock prices is included in the model. Moreover, given the dependency of the economy on oil imports and the linkages of oil with dollars and hence the exchange rate, the model also includes global oil prices. The results of the exercise suggest a cointegrating relationship between the exchange rate, money supply differential, interest rate differential, output differential, forward rate, volatility of the capital inflows. The coefficients in the cointegrating relationship are supported by theory. The error correction equation for the exchange rate also indicates that the exchange rate adjusts to move the system to the long-run relationship. Tests of Granger causality also indicate that all the variable Granger cause the exchange rate. In a similar manner, the inclusion of the difference between the rates of return in the stock prices and oil prices also yields a cointegrating relationship between the variables under study. The coefficients in the cointegrating relationship are supported by theory.

The study firstly examines whether the model augmented by difference between the rates of return on the stock prices and oil prices improves the forecast accuracy of the model given by Dua and Ranjan (2010, 2012). Secondly, the study evaluates the forecasting performance of a VAR model versus a BVAR model. The main findings of the study are as follows:

-

1.

Forecast accuracy of the model can be improved by including stock market information and global oil prices in the model.

-

2.

Information on stock prices and oil prices helps to improve forecasts, especially on the longer end.

-

3.

BVAR models outperform their corresponding VAR variants.

-

4.

Inaccuracy of forecasts in 2018 can be attributed to the high volatility in the exchange rate in this period. In 2018, a combination of factors such as rising US interest rates, a stronger dollar and the intensification of trade tensions between the US and China led to market pressures and portfolio outflows in some emerging market economies including India causing depreciation and high volatility in currency markets.

-

5.

Turning points are difficult to predict as shown using Model 2 with predictions made in November 2017 and August 2018

Notes

- 1.

The starting period is based on availability of data for all the series.

- 2.

- 3.

- 4.

- 5.

- 6.

- 7.

- 8.

- 9.

See Salisu and Ndako (2018) for a review of literature on portfolio balance approach.

- 10.

- 11.

Some studies have found unidirectional causality from exchange rates to stock prices (Bhutto and Chang, 2019 and the references cited therein), or from stock prices to exchange rates (Liang et al., 2013, Wong 2017 and references cited therein). There are few studies that have also found bidirectional causality between exchange rate and stock prices (See Bahmani-Oskooee and Saha (2015) and the references cited therein for a review of different studies).

- 12.

Kim (2011), Ulku and Demirci (2012), Baur and Miyakawa (2013), Aftab et al. (2018) provide evidence for failure of the UEP hypothesis in emerging markets. Also see, Bahmani-Oskooee and Sujata Saha (2015), Lin (2012) for reasons for weak correlation between stock prices and exchange rate in emerging markets.

- 13.

- 14.

- 15.

- 16.

DF-GLS AND KPSS tests are reported in the appendix in Table 15.

- 17.

- 18.

The coefficient of the error correction term (−0.004) is negative and less than one in absolute value in the equation for the exchange rate. The t-statistic (−3.74) with a p-value of 0.00. This implies that the exchange rate adjusts to the discrepancy from the long-run relationship to ensure that the system moves towards the long-run relationship.

- 19.

The coefficient of the error correction term (−0.005) is negative and less than one in absolute value with a p-value of 0.001. This implies that the exchange rate adjusts to the discrepancy from the long-run relationship to ensure that the system moves towards the long-run relationship.

- 20.

To estimate the BVAR model, a grid search is undertaken over the period February 2017–January 2018 to select the optimal prior, i.e. the combination of hyper parameters that yields the most accurate forecasts. The comparison of results from the optimal prior, i.e. w = 0.2, d = 1, k = 0.7 for all except k = 0.3 for volatility of capital flows and k = 0.2 for differential in rate of return in stock prices are reported in Table 16 in the appendix along with results from alternative priors.

- 21.

The results are not given here for brevity and can be obtained from the author upon request.

References

Aftab, M., Ahmad, R., & Ismail, I. (2018). Examining the uncovered equity parity in the emerging financial markets. Research in International Business and Finance, 45, 233–242.

Aggarwal, R. (1981). Exchange rates and stock prices: A study of us capital markets under floating exchange rates. Akron Business and Economics Review, 22(2), 7–12.

Bahmani-Oskooee, M., & Saha, S. (2015). On the relation between stock prices and exchange rates: A review article. Journal of Economic Studies.

Baur, D. G., & Miyakawa, I. (2013). International investors, exchange rates and equity prices. FIRN Research Paper.

Bhutto, N. A., & Chang, B. H. (2019). The effect of the global financial crisis on the asymmetric relationship between exchange rate and stock prices. High Frequency, 2(3–4), 175–183.

Bjønnes, G. H., & Rime, D. (2003). Dealer behavior and trading systems in foreign exchange markets, WP. Norges Bank.

Bohn, H., & Tesar, L. L. (1996). US equity investment in foreign markets: Portfolio rebalancing or return chasing? The American Economic Review, 86(2), 77–81.

Branson, W. H. (1983). Macroeconomic determinants of real exchange risk. In R. J. Herring (Ed.), Managing foreign exchange risk. Cambridge: Cambridge University Press.

Branson, W. H. (1984). A model of exchange rate determination with policy reaction: Evidence from monthly data. In P. Malgrange, & P. A. Muet (Eds.), Contemporary macroeconomic modelling. Oxford.

Branson, W. H. (1986). The limits of monetary coordination as exchange rate policy. Brookings Papers on Economic Activity, 1986(1), 175–194.

Breedon, F., & Vitale, P. (2004). An empirical study of liquidity and information effects of order flow on exchange rates, paper no. 4586. Centre for Economic Policy Research.

Caporale, G. M., Hunter, J., & Ali, F. M. (2014). On the linkages between stock prices and exchange rates: Evidence from the banking crisis Of 2007–2010. International Review of Financial Analysis, 33, 87–103.

Cenedese, G., Payne, R., Sarno, L., & Valente, G. (2016). What do stock markets tell us about exchange rates? Review of Finance, 20(3), 1045–1080.

Chen, S. S., & Hsu, C. C. (2019). Do stock markets have predictive content for exchange rate movements? Journal of Forecasting, 38(7), 699–713.

Clarida, R. H., & Taylor, M. P. (1997). The term structure of forward exchange premiums and forecastability of spot exchange rates: Correcting the errors. Review of Economics and Statistics, 70, 508–511.

Curcuru, S. E., Thomas, C. P., Warnock, F. E., & Wongswan, J. (2014). Uncovered equity parity and rebalancing in international portfolios. Journal of International Money and Finance, 47, 86–99.

de Medeiros, O. R. (2005). Order flow and exchange rate dynamics in Brazil. Brazil: Universidad de Brasília.

Della Corte, P., Sarno, L., & Tsiakas, I. (2007). An economic evaluation of empirical exchange rate models, paper 6598. CEPR.

Dellas, H., & Tavlas, G. (2013). Exchange rate regimes and asset prices. Journal of International Money and Finance, 38, 85–94.

Diebold, F. X., & Mariano, R. S. (2002). Comparing predictive accuracy. Journal of Business & economic statistics, 20(1), 134–144.

Doan, T. A. (2018). RATS user’s manual, version 10. Estima.

Doan, T. A., Litterman, R. B., & Sims. (1984). Forecasting and conditional projection using realistic prior distributions. Econometric Reviews, 3, 1–100.

Dooley, M., & Isard, P. (1982). A portfolio balance rational expectations model of the dollar mark exchange rate. Journal of International Economics, 12, 257–276.

Dornbusch, R. (1976). Expectations and exchange rate dynamics. Journal of Political Economy, 84, 1161–1176.

Dornbusch, R., & Fischer, S. (1980). Exchange rates and the current account. The American economic review, 70(5), 960–971.

Dua, P., & Ray, S. C. (1995). A BVAR model for the Connecticut economy. Journal of Forecasting, 14, 217–227.

Dua, P., & Miller, S. M. (1996). Forecasting Connecticut home sales in a BVAR framework using coincident and leading indexes. The Journal of Real Estate Finance and Economics, 13(3), 219–235

Dua, P., & Mishra, T. (1999). Presence of persistence in industrial production: The case of India. Indian Economic Review, 23–38.

Dua, P., Raje, N., & Sahoo, S. (2003). Interest rate modelling and forecasting in india. Department of Economic Analysis and Policy, Reserve Bank of India.

Dua, P., & Sen, P. (2009). Capital flow volatility and exchange rates: The case of India. In Macroeconomic Management and Government Finances, Asian Development Bank. Oxford University Press.

Dua, P., & Ranjan, R. (2010). Exchange rate policy and modelling in India, DRG Study No. 33. Reserve Bank of India.

Dua, P., & Ranjan, R. (2012). Exchange rate policy and modelling in India. Oxford University Press.

Elliott, G., Rothenberg, T. J., & James, H. (1996). Stock. Efficient tests for an autoregressive unit root. Econometrica, 64(4), 813–836.

Engel, C. (2000). Comments on Obstfeld and Rogoff's "The six major puzzles in international macroeconomics: Is there a common cause?"

Evans,M. D. D., & Lyons, R. K. (2007). How is macro news transmitted to exchange rates? NBER.

Evans, M. D., & Lyons, R. K. (2005). Meese-Rogoff redux: Micro-based exchange-rate forecasting. American Economic Review, 95(2), 405–414.

Frankel, J. A. (1979). On the mark: A theory of floating exchange rates based on real interest differentials. American Economic Review, 69, 610–622.

Frankel, J. A. (1983). Monetary and portfolio-balance models of exchange rate determination, In J.S. Bhandari and B. H. Putnam (eds.), Economic Interdependence and Flexible Exchange Rates, MIT Press: Cambridge, 84–115.

Fratzscher, M., Schneider, D., & Van Robays, I. (2013). Oil prices, exchange rates and asset prices. CESifo Area Conference on Macro.

Frenkel, J. A. (1976). A monetary approach to the exchange rate: doctrinal aspects and empirical evidence. Scandinavian Journal of Economics, 78, 200–224.

Granger, C.W.J. (1986). Developments in the study of cointegrated economic variables. Oxford Bulletin of Economics and Statistics 48, 213–228.

Granger, C.W.J. (1988) Some Recent Developments in a Concept of Causality, Journal of Econometrics 39:199-211.

Granger, C. W., Huang, B. N., & Yang, C. W. (2000). A bivariate causality between stock prices and exchange rates: Evidence from recent asianflu. The Quarterly Review of Economics and Finance, 40(3), 337–354.

Griffin, J. M., Nardari, F., & Stulz, R. M. (2004). Are daily cross-border equity flows pushed or pulled? Review of Economics and Statistics, 86(3), 641–657.

Harvey, D., Laybourne, S., & Newbold, P. (1997). Testing the equality of prediction mean squared errors. International Journal of Forecasting, 13, 281–291.

Hau, H., & Rey, H. (2006). Exchange rates, equity prices, and capital flows. The Review of Financial Studies, 19(1), 273–317.

Hooper, P., & Morton, J. (1982). Fluctuations in the dollar: A model of nominal and real exchange rate determination. Journal of International Money and Finance, 1, 39–56.

Isard, P. (1980). Lessons from an empirical model of exchange rates. IMF Staff Papers, 34, 1–28.

Johansen, S., & Juselius, K. (1990). Maximum likelihood estimation and inference on cointegration with applications to money demand. Oxford Bulletin of Economics and Statistics 52, 169–210.

Ju, K., Zhou, D., Zhou, P., & Wu, J. (2014). Macroeconomic effects of oil price shocks in China: An empirical study based on Hilbert-Huang transform and event study. Applied Energy, 136, 1053–1066.

Kim, H. (2011). The risk adjusted uncovered equity parity. Journal of International Money and Finance, 30(7), 1491–1505.

Kohli, R. (2001). Real exchange rate stabilisation and managed floating: Exchange rate policy in India, WP 59. ICRIER.

Kollias, C., Mylonidis, N., & Paleologou, S. M. (2012). The nexus between exchange rates and stock markets: Evidence from the euro-dollar rate and composite European stock indices using rolling analysis. Journal of Economics and Finance, 36(1), 136–147.

Koop, G. (1992). Objective Bayesian unit root tests. Journal of Applied Econometrics, 7(1), 65–82.

Kwiatkowski, D., Phillips, P. C., Schmidt, P., & Shin, Y. (1992). Testing the null hypothesis of stationarity against the alternative of a unit root: How sure are we that economic time series have a unit root?. Journal of econometrics, 54(1–3), 159–178.

Liang, C. C., Lin, J. B., & Hsu, H. C. (2013). Re-examining the relationships between stock prices and exchange rates in ASEAN-5 using panel granger causality approach. Economic Modelling, 32, 560–563.

Lin, C. H. (2012). The co-movement between exchange rates and stock prices in the Asian emerging markets. International Review of Economics & Finance, 22(1), 161–172.

Litterman, R. B. (1981). A Bayesian procedure for forecasting with vector auto regressions, WP. Federal Reserve Bank of Minneapolis.

Litterman, R. B. (1986). Forecasting with Bayesian vector auto regressions–five years of experience. Journal of Business & Economic Statistics, 4, 25–38.

Meese, R. A., & Rogoff, K. (1983). Empirical exchange rate models of the seventies: Do they fit out of sample? Journal of International Economics, 14(1–2), 3–24.

Melvin, M., & Prins, J. (2015). Equity hedging and exchange rates at the London 4 pm fix. Journal of Financial Markets, 22, 50–72.

Nankervis, J. C., & Savin, N. E. (1996). The level and power of the bootstrap t test in the AR (1) model with trend. Journal of Business & Economic Statistics, 14(2), 161–168.

Orzeszko, W. (2021). Nonlinear causality between crude oil prices and exchange rates: Evidence and forecasting. Energies, 14(19), 6043.

Pagliari, M. S., & Hannan, S. A. (2017). The volatility of capital flows in emerging markets: Measures and determinants. International Monetary Fund.

Phillips, P. C. (1991). To criticize the critics: An objective Bayesian analysis of stochastic trends. Journal of Applied Econometrics, 6(4), 333–364.

Phylaktis, K., & Ravazzolo, F. (2005). Stock prices and exchange rate dynamics. Journal of International Money and Finance, 24(7), 1031–1053.

Qiang, W., Lin, A., Zhao, C., Liu, Z., Liu, M., & Wang, X. (2019). The impact of international crude oil price fluctuation on the exchange rate of petroleum-importing countries: A summary of recent studies. Natural Hazards, 95(1), 227–239.

Raza, N., Shahzad, S. J. H., Tiwari, A. K., & Shahbaz, M. (2016). Asymmetric impact of gold oil prices and their volatilities on stock prices of emerging markets. Resources Policy, 49, 290–301.

Salisu, A. A., & Ndako, U. B. (2018). Modelling stock price-exchange rate nexus in OECD countries: A new perspective. Economic Modelling, 74, 105–123.

Sahoo, A., Moharana, S., & Dash, M. (2018). Relationship between macroeconomic variables and stock market trend. Journal of Management (JOM), 5(3).

Salisu, A. A., Cuñado, J., Isah, K., & Gupta, R. (2021). Oil price and exchange rate behaviour of the BRICS. Emerging Markets Finance and Trade, 57(7), 2042–2051.

Salisu, A. A., Cuñado, J., Isah, K., & Gupta, R. (2020). Stock markets and exchange rate behaviour of the BRICS. Journal of Forecasting.

Sharma, N. (2017). Cointegration and causality among stock prices, oil prices and exchange rate: Evidence from India. International Journal of Statistics and Systems, 12(1), 167–174.

Sims, C. A. (1980). Macroeconomics and reality. Econometrica, 48, 1–48.

Sims, C. A. (1988). Bayesian skepticism on unit root econometrics. Journal of Economic dynamics and Control, 12(2–3), 463–474.

Sims, C. A., Stock, J. H., & Watson, M. W. (1990). Inference in linear time series models with some unit roots. Econometrica: Journal of the Econometric Society, 113–144.

Spencer, D. E. (1993). Developing a Bayesian vector autoregression forecasting model. International Journal of Forecasting, 9, 407–421.

Sui, L., & Sun, L. (2016). Spillover effects between exchange rates and stock prices: Evidence from BRICS around the recent global financial crisis. Research in International Business and Finance, 36, 459–471.

Theil, H. (1966). Applied Economic Forecasting, Amsterdam: North-Holland.

Todd, R. M. (1984). Improving economic forecasting with Bayesian vector autoregression. Quarterly Review (fall, pp. 18–29). Federal Reserve Bank of Minneapolis.

Turhan, M. I., Sensoy, A., & Hacihasanoglu, E. (2014). A comparative analysis of the dynamic relationship between oil prices and exchange rates. Journal of International Financial Markets Institutions and Money, 32, 397–414.

Ülkü, N., & Demirci, E. (2012). Joint dynamics of foreign exchange and stock markets in emerging Europe. Journal of International Financial Markets Institutions and Money, 22(1), 55–86.

Wen, D., Liu, L., Ma, C., & Wang, Y. (2020). Extreme risk spillovers between crude oil prices and the US exchange rate: Evidence from oil-exporting and oil-importing countries. Energy, 212.

Wong, H. T. (2017). Real exchange rate returns and real stock price returns. International Review of Economics & Finance, 49, 340–352.

Xie, Z., Chen, S. W., & Wu, A. C. (2020). The foreign exchange and stock market nexus: new international evidence. International Review of Economics & Finance, 67, 240–266.

Živkov, D., Balaban, S., & Djurašković, J. (2018). What multiscale approach can tell about the nexus between exchange rate and stocks in the major emerging markets? Czech Journal of Economics and Finance, 68(5), 491–512.

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Appendix

Appendix

See Tables 14, 15 and 16, Figs. 4 and 5

a Model 1: 3-Month ahead forecast: Feb 2017–Jan 2018, b 6-Month ahead forecast: Feb 2017–Jan 2018, c Model 1: 9-Month ahead forecast: Feb 2017–Jan 2018

a Model 2: 3-Month ahead forecast: Feb 2017–Jan. 2018, b Model 2: 6-Month ahead forecast: Feb. 2017–Jan. 2018, c Model 2: 9-Month ahead forecast: Feb. 2017–Jan. 2018

Questions to Think About

-

1.

This chapter shows that addition of stock prices in the exchange rate model helps in improving its predictability. What is the expected relationship between exchange rate and stock prices in (i) developed and (ii) developing economies?

Hint: Estimate the direction of relationship between stock prices and exchange rate in different economies and compare their results. Refer: Salisu et al. (2020).

-

2.

What are the various types of hyperparameters used for the Minnesota Prior? What are the implications of changing the hyperparameters for “overall tightness” and “Lag decay”?

Hint: Construct different combination of hyperparameters and analyse the result. Refer: Dua, Raje and Sahoo (2003).

-

3.

This chapter includes the domestic–foreign differential of the rate of return of stock prices as well of global oil prices as determinants of the exchange rate in addition to monetary model fundamentals (i.e. differential in money supply, interest rate and inflation), forward premium, volatility of capital flows, order flows and central bank intervention. Test the significance of these determinants of exchange rate in a cointegrating framework.

Rights and permissions

Copyright information

© 2023 The Author(s), under exclusive license to Springer Nature Singapore Pte Ltd.

About this chapter

Cite this chapter

Dua, P., Ranjan, R., Goel, D. (2023). Forecasting the INR/USD Exchange Rate: A BVAR Framework. In: Dua, P. (eds) Macroeconometric Methods. Springer, Singapore. https://doi.org/10.1007/978-981-19-7592-9_8

Download citation

DOI: https://doi.org/10.1007/978-981-19-7592-9_8

Published:

Publisher Name: Springer, Singapore

Print ISBN: 978-981-19-7591-2

Online ISBN: 978-981-19-7592-9

eBook Packages: Economics and FinanceEconomics and Finance (R0)