Abstract

The global financial crisis of 2007–08 has been one of the most difficult financial and economic episodes for the world economy. This chapter investigates changes in the impact of monetary policy on some key macroeconomic variables in pre-and post-global financial crisis of 2007–08. We estimate a reduced form Vector Autoregressive model of five variables: money, output, prices, interest rates and the exchange rates for pre-and post-crisis periods. The empirical evidence suggests that monetary policy shocks have expected effect on output and prices. However, the monetary policy transmission lags are significantly reduced in post crisis period. The peak effect on output and prices are felt with a lag of 5 and 12 months which were 13 and 23 months respectively in pre-crisis periods.

Access provided by CONRICYT-eBooks. Download conference paper PDF

Similar content being viewed by others

Keywords

JEL Classification

1 Introduction

Monetary policy affects macroeconomic variables such as real gross domestic product (GDP) and inflation through a mechanism called monetary policy transmission mechanism (MPTM). MPTM entails the entire process through which monetary policy actions are transmitted into the ultimate objectives of monetary policy . The Reserve Bank’s mandate for monetary policy is clearly enunciated in the Preamble of the Reserve Bank of India Act, 1934 as: “to regulate the issue of Bank notes and the keeping of reserves with a view to securing monetary stability in India and generally to operate the currency and credit system of the country to its advantage”. Thus the primary goal of the RBI is to ensure monetary stability in terms of preserving the purchasing power of the rupee. Ultimately, this can only be ensured when the prices are low and stable.

With the amendment of the Reserve Bank of India Act, 2016 the primary objective of monetary policy is to maintain price stability while keeping in mind the objective of economic growth . For the Reserve Bank to achieve its mandate effectively, the Monetary Policy Committee (MPC) has been constituted under the amended RBI Act to determine the policy repo rate in order to achieve the specified medium-term inflation target of 4%, within a band of 2%. Since price stability alone not necessarily can ensure financial stability, the latter being another important objective of monetary policy . Most of the literature on the transmission of monetary policy has focused on four key channels: the interest rate channel, the credit channel, the exchange rate channel and the asset price channel. In most of the countries, central banks use a short-term interest rate as their primary instrument of monetary management. Given inflexibility of prices and wages in the short-run, a shift in monetary policy rate leads to changes in market interest rates which in turn affects households and firms saving and investment behavior and ultimately real activity and inflation .

It is however, increasingly realized that the impact of monetary policy shocks on the macroeconomic variables may vary both across country as well as within the same country over time. The global financial crisis of 2007–08 has been one of the most difficult financial and economic episodes for the world economy. In recent research work, Friedman and Kuttner (2010) have demonstrated that developments since the 2008 crisis have made it necessary to reassess the impact of monetary policy shocks on macroeconomic variables where the changes have been very significant. Furthermore, they argued that use of both quantity (size of balance sheets) and price instruments (policy rate) by the central banks represent a fundamental departure from decades thinking of the scope of central bank actions. Financial environment in which monetary policy is conducted in the emerging market economies (EMEs) has changed over the past decade in terms of increasing role of debt markets relative to banks, globalization of debt markets and behavior of long term interest rates (Mohanty and Kumar 2016). Against this backdrop, the objective of this chapter is to provide evidence on the effect of monetary policy on the key macroeconomic variables in India . The main focus of the study is to test the hypothesis whether the response of macroeconomic variables to unexpected monetary policy shocks have changed significantly in post crisis years in comparison to pre-crisis period. The chapter employs a Vector Autoregression (VAR) methodology for empirical investigation of the monetary policy effects on some key macroeconomic variables . Vector Autoregression (VAR) models have been extensively used in the empirical analysis of monetary policy issues.

The remainder of this chapter is organized as follows: Section 3.2 presents literature review on monetary policy analysis based on VAR models. Section 3.3 gives a brief account of monetary policy operating procedure of the RBI. Section 3.4 specifies the reduced form VAR model consisting of five variables and dataset. Section 3.5 reports the results of Chow structural break test. Section 3.6 provides empirical evidence of the effects of monetary policy on macroeconomic variables in pre-and post-crisis from impulse responses and variance decompositions. Section 3.7 presents the concluding remarks.

2 Review of Literature

VAR models have been used in standard literature for studying the dynamic relationship among macroeconomic variables . The use of VARs to estimate the impact of monetary policy on the real economic activity was pioneered by Sims (1972, 1980). Sims (1972) studied the role of money stock in explaining business cycles in the United States during inter-World War and post-World War. In another study (1980), he estimated the VAR model for different countries in order to examine the role of money as a good indicator of monetary policy . In most fascinating study, Bernanke and Blinder (1992) found the US federal funds rate as extremely informative about future movements of real macroeconomic variables . After estimating three variable VAR model with fund rate, log of CPI and prime age [25–54] male unemployment, they found inflation shocks drive up the fund rate with the peak effect coming 5–10 months and then decaying very slowly, while unemployment shocks push the fund rate in the opposite direction but with somewhat longer lags and smaller magnitude.

A number of studies have been conducted in India using VAR models especially after the structural and macroeconomic reforms of the early 1990s. Therefore, it appears that VAR assumptions throw light on theorization of monetary policy transmission effects in India . To examine the implications of structural reforms (April 1992 to March 1997) on monetary policy transmission, Ray et al. (1998) establish the importance of both interest rate and exchange rate channel in the monetary transmission in post liberalization era. They found that money, income , prices and exchange rates are cointegrated and interest rate and exchange rate which were exogenous in the pre-reforms period became endogenous variables in post reforms periods. This evidence suggests of shift in monetary policy transmission. Applying VAR models in the vector error correction form, Al-Mashat (2003) demonstrates that the interest rate channel and exchange rate channel are most important while bank lending channel is found weak reflecting low pass-through of changes in policy rate to lending rates.

In order to explore the channels of monetary transmission the RBI (2004) estimated a five variables recursive VAR model. These variables are log of index of industrial production (LIIP), log of WPI (LWPI), Bank rate (BRATE), log of broad money (LM3) and log of exchange rate (LEXCH). Empirical evidence of transmission channels shows that monetary policy shocks have the expected effect on output and prices. Interest rate and exchange rate as financial variables are found more effective than earlier. Bhattacharya and Ray (2007) present both narrative analysis of monetary policy stance as well as empirical evidence based on Vector autoregression model with three variables output, prices and “measure” of monetary policy stance. Their findings indicate that monetary policy had been more effective in controlling inflation vis-a-vis stimulating output growth. Moreover, the results are quite robust and remain consistent despite changing the ordering of variables. Using quarterly data from 1996 to 2007, Aleem (2010) examines monetary policy transmission channels. The VAR results support the importance of the bank lending channel in a bank based Indian economy. While both asset price channel and exchange rate channel are not found significant which, he argued, are consistent with lower market capitalization of listed companies and massive interventions by the Reserve bank of India in foreign exchange market respectively.

Based on structural vector autoregression (SVAR) model, Mohanty (2012) provides the empirical evidence of interest rate channel of monetary policy transmission in India . Using quarterly data, the results show that monetary contraction has a negative effect on output with a lag of two quarters while impact on inflation with a lag of three quarters. The overall impact persists through eight to ten quarters. After finding a structural break at a time ofLiquidity Adjustment Framework (LAF) introduction, Sengupta (2014) examines the changes in transmission channels of monetary policy in pre-LAF and post-LAF periods. Using vector autoregressionmodel with monthly data from April 1993 to March 2012, the study finds that the bank lending channel although has weakened still remains an important channel of monetary transmission. Moreover, the interest rate and asset price channels have become stronger while the exchange rate channel though weak, shows a mild improvement in the post-LAF period. Mishra et al. (2016) examine the empirical evidence of the strength of monetary transmission in India using the structural vector autoregression (SVAR) method. While the pass-through from the policy rate to bank lending rates is in right direction, it is not complete. The responses of real activity (IIP) and prices (WPI) are not found significant following monetary policy shocks. The estimated effect may reflect either weakness in monetary transmission or the limitations of empirical methodology. Overall, the empirical results do provide a mixed message on the effectiveness of monetary policy in India . Mohanty and Kumar (2016) reviewed the recent changes in financial intermediation in Emerging Market Economies (EMEs) and its implications on the monetary transmission.

3 Reserve Bank’s Current Monetary Policy Operating Procedure

Based on the recommendations of the Committee on Banking Sector Reforms (Narasimham Committee II 1998), RBI had adopted an Interim Liquidity Adjustment Facility (ILAF) as its operating procedure in April 1999. The Interim LAF was transitioned towards full-fledged LAF in June 2000. The modified new operating framework (Reserve Bank of India 2011) has allowed banks to manage their daily liquidity more efficiently and reduced volatility in money market.

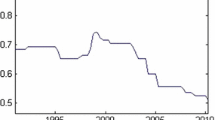

According to which liquidity injections are done at the Marginal Standing FacilityFootnote 1 (MSF) and liquidity absorptions are through fixed reverse repo rate. The fixed overnight repo rate is the single monetary policy rate and has been placed in the middle of the corridor, with the reverse repo rate 25 basis points below it and the MSF rate 25 basis points above it. The weighted average call money rate (WACMR) is the new operating target of monetary policy . The main objective of the liquidity management is to anchor the weighted average call money rate (WACMR) around the policy rate (Fig. 3.1).

Source Handbook of Statistics on the Indian Economy, 2015–16

Some key policy rates.

4 Methodology and Data Set

We estimate a reduced-form vector autoregression (VAR), as proposed by Sims (1980), to examine the response of macroeconomic variables to unexpected monetary policy shocks. In a reduced form VAR, each variable is expressed as a linear function of its own lagged values, lagged values of all other variables and a serially uncorrelated error tem. Thus a reduced form VAR is a system of equations and can be written in matrix form as:

where Yt is vector of macroeconomic variables included in our model. A0 is a vector of constants. A is the matrix of coefficients. L is lag operator. And ut is a vector of serially uncorrelated disturbances that have zero mean and time invariant covariance. In our VAR specification, the vector Yt consists of five macroeconomic variables : index of industrial production (LIIP), wholesale price index (LWPI), weighted average call money rate (CMR), Broad money (LM3) and Rupee per US dollar exchange rate (LEXR):

For estimating VAR model, one important issue is the identifying assumption. Since monetary policy actions are endogenous response to current developments in the economy; therefore these actions must be separated from exogenous policy shocks. The dynamic analysis of the VAR system may produce reliable estimates of the effects of monetary policy only when this fundamental identification problem is solved (Bagliano and Favero 1998). Therefore, following Christiano et al. (1999), we identify monetary policy shocks by a standard choleski-decomposition with the order of variables as given in the vector Yt. In other words, monetary policy reacts to development in real economy contemporaneously but does not affect output and prices contemporaneously (i.e. in the same period). Accordingly, real variables like output and prices have been placed before monetary policy instrument in the model. Given the monthly data, this identifying assumption seems reasonable.

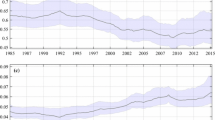

We have used Index of Industrial Production as a proxy variable for GDP output data as the monthly data of GDP output is not available in India . Monetary policy rate is proxied by overnight weighted average call money rate (CMR) because it is also the operating target of the Reserve Bank. For price index, the headline wholesale price index (WPI) has been selected. For quantity variable, I have taken monthly data of broad money (M3) in real terms by deflating correspondingly monthly WPI index and rupee per US dollar for exchange rate. In general, estimation of any VAR model requires long time series data. Accordingly, the model has been estimated using monthly data running from 2000–01 April to 2015–16 March. The entire sample is divided into two sub-sample for pre-crisis (April, 2000–August, 2008) and post-crisis (October, 2008–March, 2015). The data set has been taken from the Reserve bank’s site: http://dbie.rbi.org.in and also from Handbook of Statistics on Indian Economy: 2015–16. All the variables except the policy interest rate are seasonally adjusted using X–12 ARIMA and are transformed into natural logarithms. The Augmented Dickey-Fuller test results indicate that all the variables except call money rate are non-stationary. As differencing of series throws away important information and does not improve asymptotic efficiency, the VAR model has been estimated in levels (RBI 2004). The appropriate lag length in our VAR model has been decided on the basis of various information criteria: Akaike Information Criteria (AIC), Schwarz Criteria (SC), Hannan-Quinn (HQ), Final Prediction Error (FPE). All these information criteria except SC indicate the appropriate lag length of two (Appendix table). Thus our VAR model includes only two lags of variables (Fig. 3.2).

The time series variables included in VAR analysis (for all the graphs X axis shows months and Y axis units)

5 Test of Structural Break: Chow Test

To check the presence of structural break in the sample, we estimate one of the VAR equations of broad money in terms of output, prices, interest rate and exchange rates. In a span of eight months from September 2008 and April 2009, the Reserve Bank followed unprecedented policy activism. Therefore it does make sense to check whether there is a structural break between this period. Table 3.1 shows the results of Chow test when we choose September 2008 as break point. Clearly, we can reject the null hypothesis of no structural break at September 2008 for the above equation. Thus we find a structural break at September 2008 and therefore we will estimate the VAR model for pre and post crisis periods.

6 Empirical Evidence

-

(i)

Impulse Response FunctionsFootnote 2:

Figure 3.3 depicts the dynamic responses of output, prices, overnight call money rate and exchange rate to a positive two standard deviation call money rate shock in the pre-crisis period. An exogenous monetary policy shock- corresponding to a 1% (100 basis points) rise in call money rate- has the expected negative effect on output with the peak effect occurring around 13 months after the shock and output declines to 0.35% below the base line. In the subsequent months, output gradually returns to the baseline approximately in 40 months. Following unexpected monetary tightening, prices also decline to a low level of almost 0.20% below the base line. The peak of effect on price occurs almost in 23 month after the shock to the interest rate and does not return to the base line even after 45 months. More important, it is clear from the graph that there is no price puzzle and thus the included variables correctly specify the model. The response of the exchange rate shows that it depreciates following exogenous monetary shock. The peak effect occurs around six months after the shock and takes almost three years (34 months) to return to baseline.

Impulse responses of output, prices and exchange rate to interest rate shock (pre-crisis)

We now repeat the interpretation of impulse response functions for post-crisis period. From Figure 3.4, it is clear that a positive shock to call money rate (0.8% rise in CMR) leads output to decline to a low level of 0.24% below the baseline after five months. In almost 22 months, output gradually returns to the baseline. The maximum negative effect on prices (0.28%) occurs in almost 12 months and remains below the baseline even after three years. The response of the exchange rate shows that it depreciates following monetary tightening shock with the maximum effect at 5 months.

Impulse responses of output, prices and exchange rate to interest rate shock (post-crisis)

-

(ii)

Variance Decomposition analysis:

Variance decomposition analysis examines the variance of output and prices that can be explained by monetary policy and other shocks in the economy.

The empirical results (Table 3.2) indicate that the proportion of output at 48 months ahead horizon, due to interest rate and broad money shocks is 3% in pre-crisis periods and 4% in post crisis periods respectively. Looking at forecast error variance of prices, shocks to interest rate and broad money explain almost 4 and 9% of volatility in prices in pre-crisis periods and 10 and 1% in post crisis periods respectively. Similarly, interest rate and broad money shocks explain only a small proportion of variance in exchange rate. Moreover, the innovations to exchange rate explain almost 56 and 59% of total variance in output and prices in pre-crisis period which declined significantly in post crisis periods to 17 and 7%. Overall, a significant proportion of both output and price volatility is not on account of monetary policy shocks. In other words, innovations to interest rate and broad money explain only a small proportion of output and price variance in both pre- and post-crisis periods. This low explanatory power of monetary policy shocks in terms of both interest rate and broad money for output and price variance however does not imply that monetary policy does not matter. VAR framework focuses on non-systematic component of monetary policy shocks. Thus major source of fluctuations in output and prices may be due to systematic component of monetary policy shocks (Christiano et al. 1999; Boivin and Giannoni 2002; RBI 2004).

7 Concluding Remarks

In order to assess the changes in the impact of monetary policy on some key macroeconomic variables in pre- and post-crisis, we estimate a reduced form VAR model of five variables: money, output, prices, interest rates and the exchange rates. The empirical results are analyzed in terms of impulse response functions and variance decomposition. The empirical evidence shows that both output and prices respond negatively to unexpected monetary policy shock- in terms of two standard deviation shock to overnight call money rate. More importantly, we can notice that in response to monetary policy shock the decline in output precedes the decline in prices in both pre- and post-crisis periods. But the response of output and prices to monetary policy shock is sooner in post-crisis in comparison to pre-crisis periods. In other words, the monetary policy transmission lags are significantly reduced in post crisis period. The peak effect on output and prices are felt with a lag of 5 and 12 months which were 13 and 23 months respectively in pre-crisis periods. The response of exchange rate is however is not in right direction (a monetary tightening leads the exchange rate to depreciate) and which might be consistent with the finding of weak exchange rate channel (Mishra et al. 2016). Variance decomposition results show that innovations to interest rate and broad money explain only a small proportion of output and price variance in both pre- and post-crisis periods. For sensitivity of results, alternative ordering of variables has been undertaken but the impulse responses remain broadly unchanged.

Notes

- 1.

MSF is the rate at which scheduled commercial banks (SCBs) can borrow overnight without giving any collateral at their discretion up to 1% of their respective Net Demand and Time Liabilities (NDTL) at penal rate 25 basis points above the repo rate.

- 2.

For all the figures X axis shows months and Y axis units.

References

Aleem, A. (2010). Transmission mechanism of monetary policy in India. Journal of Asian Economics, 21, 186–197.

Al-Mashat, R. (2003). Monetary policy transmission in India: Selected issues and statistical appendix. Country Report No. 03/261, International Monetary Fund.

Bagliano, F. C., & Favero, C. A. (1998). Measuring monetary policy with VAR models: An evaluation. European Economic Review, 42, 1069–1112.

Bernanke, B. S., & Blinder, A. S. (1992). The federal funds rate and the channels of monetary transmission. The American Economic Review, 82(4), 901–921.

Bhattacharya, I., & Ray, P. (2007). How do we assess monetary policy stance? Economic and Political Weekly, 42(13), 1201–1210.

Boivin, J., & Giannoni, M. (2002). Assessing changes in the monetary transmission mechanism: A VAR approach. Federal Reserve Bank of New York Economic Policy Review, 8(1), 97–111.

Christiano, L. J., Eichenbaum, M., & Evans, C. L. (1999). Monetary policy shocks: What have we learned and to what end? In J. B. Taylor & M. Woodford (Eds.), Handbook of macroeconomics (Vol. 1A). Amsterdam: North-Hlland.

Friedman, B. M., & Kuttner, K. N. (2010). Implementation of monetary policy: How do central banks set interest rates? In: B. M. Friedman & M. Woodford (Eds.), Handbook of monetary economics (Vol. 3B). Amsterdam: North-Holland.

Khundrakpam, J. K., & Jain, R. (2012, June). Monetary policy transmission in India: A peep inside the black box. Reserve Bank of India Working paper Series WPS (DEPR): 11/2012.

Mishra, P., & Montiel, P. (2013). How effective is monetay transmission in developing countries? A survey of the empirical evidence. Economic Systems, 37(2), 187–216.

Mishra, P., Montiel, P., & Sengupta, R. (2016). Monetary transmission in developing countries: Evidence from India. IGIDR; Working Paper, 2016-008.

Mohanty, D. (2011, September). How does the Reserve Bank of India conduct its monetary policy? Reserve Bank of India Bulletin.

Mohanty, D. (2012, May). Evidence of interest rate channel of monetary policy transmission in India. RBI Working Paper No. 6.

Mohanty, M. S., & Kumar, R. (2016). Financial intermediation and monetary policy transmission in EMEs: What has changed post-2008 crisis? Monetary and Economic Development, BIS Working Papers No. 546.

Mohanty, M. S., & Turner, P. (2008). Monetary policy transmission in emerging market economies: What has changed? BIS Papers, 35.

Ray, P., Joshi, H., & Saggsar, M. (1998). New monetary transmission channels: Role of interest rates and exchange rate in conduct of Indian monetary policy. Economic And Political Weakly, 33(44).

Reserve Bank of India. (2004). Monetary transmission mechanism. Report on Currency and Finance, 2003–04. Mumbai: Reserve Bank of India.

Reserve Bank of India. (2011). Report of the working group on operating procedure of monetary policy, chairman: Deepak Mohanty. Mumbai: Reserve Bank of India.

Reserve Bank of India. (2014). Report of the expert committee to revise and strengthen the monetary policy framework, Chairman: Urjit R. Patel. Reserve Bank of India: Mumbai.

Reserve Bank of India. (2015–16). Handbook of statistics on the Indian economy. Mumbai: Reserve Bank of India.

Sengupta, N. (2014). Changes in transmission channels of monetary policy. Economic and Political Weekly, XLIX(49), 62–71.

Sims, C. A. (1972). Money, income and causality. The American Economic Review, 62(4), 540–552.

Sims, C. A. (1980). Macroeconomics and reality. Econometrica, 48, 1–48.

Acknowledgements

The author is very grateful to Prof. Chetan Ghate and Dr. Jose Antonio Pedrosa Garcia for valuable comments and discussions in the International Conference on Economics and Finance, organized by BITS Pilani, KK Birla Goa Campus. Further, the author expresses sincere gratitude to Prof. U. Kalpagam (DPhil Supervisor) for extremely useful suggestions and encouragement all the time.

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Appendix

Appendix

VAR lag order selection criteria

Lag | Log L | LR | FPE | AIC | SC | HQ |

|---|---|---|---|---|---|---|

0 | 416.2659 | NA | 9.49e−09 | −4.284019 | −4.199189 | −4.249662 |

1 | 2073.012 | 3209.945 | 3.94e−16 | -21.28137 | −20.77239a | −21.07523 |

2 | 2131.920 | 111.0672a | 2.77e−16a | −21.63458a | −20.70145 | −21.25666a |

3 | 2147.914 | 29.32199 | 3.04e−16 | −21.54077 | −20.18348 | −20.99106 |

4 | 2158.157 | 18.24530 | 3.56e−16 | −21.38705 | −19.60561 | −20.66555 |

5 | 2173.813 | 27.07228 | 3.94e−16 | −21.28972 | −19.08412 | −20.39644 |

Rights and permissions

Copyright information

© 2018 Springer Nature Switzerland AG

About this paper

Cite this paper

Singh, G.P. (2018). Some Empirical Evidence on the Effects of Monetary Policy in India: A Vector Autoregressive Based Analysis. In: Mishra, A., Arunachalam, V., Patnaik, D. (eds) Current Issues in the Economy and Finance of India. ICEF 2018 2018. Springer Proceedings in Business and Economics. Springer, Cham. https://doi.org/10.1007/978-3-319-99555-7_3

Download citation

DOI: https://doi.org/10.1007/978-3-319-99555-7_3

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-319-99554-0

Online ISBN: 978-3-319-99555-7

eBook Packages: Economics and FinanceEconomics and Finance (R0)