Abstract

Despite the potential promises that blockchain technology (BT) offers to the financial services sector, its large-scale implementations are still in a nascent stage. There is no consensus on what benefits BT may bring, and there is always a possibility of difference between expected benefits and experienced real-world impact. Since the actual impact can be assessed only after large-scale implementations by financial institutions, there is little empirical evidence available in the literature. In this context, this research seeks to explore the potential impact of BT by developing and empirically testing a model. For this purpose, we have identified four dimensions of BT, namely, Decentralization, Transparency, Trustlessness, and Security. The impact of BT on innovation, service quality, and firm performance is assessed based on the extent to which these dimensions are present in the organization. The linkages of the latent constructs are estimated by analyzing the primary data collected from senior managers of various banks in India. The findings of this study provide several important considerations regarding the implementation of BT.

Access provided by Autonomous University of Puebla. Download conference paper PDF

Similar content being viewed by others

Keywords

1 Introduction

Blockchain technology (BT) is identified as a disruptive innovation of the Internet era. This technology promises to bring revolutionary transformations in the way we transact over the internet, with prospective applications in various domains (Swan 2015; Huckle et al. 2016; Tapscott and Tapscott 2016; Beck et al. 2017). A blockchain is a distributed, decentralized, and immutable database, consisting of a growing sequence of blocks containing timestamped transactions, which is shared among a peer-to-peer network by a consensus mechanism. BT has got promising application prospects in the banking and financial services industry, especially in payment clearing and settlement systems, bank credit information systems, trade finance, etc. (Guo and Liang 2016; Peters and Panayi 2016; Treleaven et al. 2017). By way of decreasing transaction costs and by improving operating efficiency, BT offers the potential to be the core, underlying technology of the future financial services sector.

Despite the potential promises that this technology offers, large-scale BT implementations in the banking sector are still in the nascent stage. There is always a possibility of difference between expectations and experienced real-world impact of BT since the actual impact can only be assessed after large-scale implementations by financial institutions. While there are several initiatives offering blockchain solutions, especially by financial service providers and FinTechs, so far, no application has achieved large-scale recognition. It is necessary to be aware of the potential impacts resulting from the use of blockchain technology to real-world applications to foster the adoption of this technology at a larger scale. But there is no consensus on what benefits BT may really bring (Halaburda 2018).

Numerous conceptual studies are published focusing on BT. However, only a limited number of studies are available in literature, which is analytical and empirical in nature. Further, the focus of most of the research available on BT deals with technical, computational, and engineering aspects of blockchain. BT has not yet been thoroughly investigated from a strategic and managerial perspective by both academicians and practitioners. This gap has created exciting research avenues, especially from the perspective of managerial challenges and implications. A set of characteristics of BT are identified for this study, considering the above into account. Further, these characteristics are grouped into four dimensions of BT. Using these dimensions, we explore blockchain and related technologies from different perspectives, including strategic as well as managerial. A theoretical model is developed and empirically tested to explain the potential impact of BT on innovation, service quality, and firm performance in the context of the banking industry.

The rest of the paper is organized as follows: The research model and hypotheses are presented in sect. 2. This is followed by a discussion on the data and methodology in sect. 3. Section 4 presents the analysis and findings. Finally, the concluding remarks are given in sect. 5.

2 Research Model and Hypotheses

In order to understand the underlying concept of BT and to derive a distinct set of characteristics, a rigorous literature review is performed. One of the significant reasons for the interest in BT is its characteristics that provide security, anonymity, and data integrity without the need for any third party in control of the transactions (Yli-Huumo et al. 2016). BT can be leveraged to overcome the drawbacks that are associated with trusting a central authority by enabling reliable transactions on the blockchain without knowing or trusting the peer dealt with. Some authors have pointed out that BT enables a secure trust-free transaction system (Beck et al. 2016). Shared and distributed storage of information is mentioned as another characteristic of BT which enhances the transparency of the blockchain system (Garman et al. 2014; Cai and Zhu 2016). Seebacher and Schüritz (2017), in their work, identified trust and decentralization as the key characteristics of BT. Transaction security and immutability in the blockchain network achieved through public-key cryptography and peer verification process are also discussed in the literature (Cucurull and Puiggalí 2016; Weber et al. 2016; Zhao et al. 2016). An in-depth review and synthesis of these literature have revealed a set of characteristics that facilitate implementation of BT in an organization. From these four principal characteristics are identified for BT, namely, Decentralization, Transparency, Trustlessness, and Security. Using these dimensions, we explore BT from a strategic as well as managerial perspective. Further, we examine the potential impact of BT on innovation, service quality, and firm performance in the context of banking industry.

Innovation is generally considered as an essential component for organizations to obtain competitive advantage and superior performance (Cooper and Kleinschmidt 1987; Mone et al. 1998; Gunday et al. 2011). As per the definition given in the OECD Oslo manual 2005, product innovation can be viewed as the introduction of a new or significantly improved good or service. Process innovation is the implementation of a new or significantly improved production or delivery method. Organizational innovation is the implementation of a new organizational method in the firm’s business practices, and it is strongly related to administrative efforts (OECD 2005). Product and process innovations are closely related to technological developments (Gunday et al. 2011). Further, considerable research has been conducted on the relationship between innovation and service quality (Verhees and Meulenberg 2004; Parasuraman 2010) and also on service quality and firm performance (Roth and Jackson III 1995; Kaynak 2003; Yee et al. 2010).

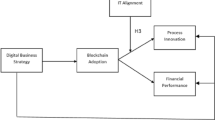

While there are many conceptual studies that suggest that BT will have a positive impact on the firm’s performance, there is no empirical evidence published so far. Similarly, there are only a limited number of studies focusing on BT and service quality, and again there is no empirical evidence in the literature. In the context of the banking industry, BT is expected to decrease transaction costs and improve operating efficiency. In this study, we aim to explore the impact of the dimensions of BT on firm performance through innovation by examining the product, process, and administrative innovations, as well as through service quality in the context of the banking industry. Figure 1 represents the conceptual framework of the study.

Conceptual framework of the study. Source: author’s own study

A structural model is developed for testing the following hypothesis:

-

H1: The four dimensions of blockchain technology (i) trustlessness, (ii) decentralization, (iii) transparency, and (iv) security are positively related with the three dimensions of innovation, (a) product innovation, (b) process innovation, and (c) administrative innovation

-

H2: The four dimensions of blockchain technology (i) trustlessness, (ii) decentralization, (iii) transparency, and (iv) security are positively related with service quality

-

H3: The three dimensions of innovation (a) product innovation, (b) process innovation, and (c) administrative innovation are positively related with service quality

-

H4: Service quality is positively related with firm performance

3 Data and Methodology

The linkages of the latent constructs are estimated by analyzing the primary data collected from senior managers of various banks in India by applying Structural Equation Modeling (SEM). A scale for BT is developed for this study with Trustlessness, Decentralization, Transparency, and Security as multidimensional constructs. Measures of innovation (Jiménez-Jiménez and Sanz-Valle 2011), service quality (Parasuraman et al. 1988), and firm performance (Jiménez-Jiménez and Sanz-Valle 2011) are adapted from previous literature. All these constructs are measured using a five-point Likert scale, measured from strongly disagree to strongly agree. A draft questionnaire is pre-tested to check the content validity and hence modified accordingly. Questionnaires containing items measuring BT, innovation, service quality, and firm performance were distributed to 200 senior managers of various banks in India. A total of 167 responses were obtained, out of which 11 responses were with missing values and those were excluded from the final sample.

4 Analysis and findings

The data revealed that all the constructs are having high item communalities, hence the concern of sample size adequacy is satisfied. Descriptive statistics of indicators of all the latent constructs are shown in Table 1.

Individual confirmatory factor analysis (CFA) is performed by considering each latent construct one by one, and the results are explained in Table 2. All the nine constructs are having statistically significant (p < 0.001) factor loadings (≥ 0.5), and the value of Average Variance Extracted (AVE) exceeds the recommended minimum value of 0.50. Again, Cronbach’s alpha and composite reliability of all the constructs are greater than the recommended threshold of 0.70 (Hair et al. 2011; Fornell and Larcker 1981), and R2 values above 0.5 (Easterby-Smith, 1991), indicates evidence for convergent validity.

The results from Table 3 confirm that the intercorrelation values of the exogenous variables are well below 0.85 and AVE values are greater than squared intercorrelation values, and hence indication for discriminant validity (Hair et al. 2011; Fornell and Larcker 1981).

Table 4 shows that the values for NFI, IFI, TLI, and CFI are well above the recommended threshold of 0.90 (Hu and Bentler 1999; Hair et al. 2011; Hooper et al. 2008). Hence unidimensionality of all the latent constructs are verified. Therefore, it is evident that there are no cross loadings, or the indicators are reflecting only the corresponding construct.

The VIF values for all the four predictor variables are less than 5, with tolerance levels greater than 0.2, indicating the fact that there is no multicollinearity issue in the data set. Figure 2 represents the structural model used in this study. According to the results summarized in Table 5 the overall fit of the structural model is good, with a χ2 value of 1153.695 and CMIN/DF value of 2.303, which is well below 5.0 (Marsh and Hocevar 1985). NFI, IFI, TLI, and CFI are above 0.90 (Hair et al. 2011; Hu and Bentler 1999; Hooper et al. 2008). All these results suggest that the overall fit of the structural model is good.

Structural Model. Source: Primary data

Table 6 shows the results of hypothesis testing. The first hypothesis (H1) is developed for testing the relationship between four dimensions of BT and three dimensions of innovation. H2 tests the relationship between BT and service quality. Further, H3 tests the relationship between innovation and service quality. Finally, H4 tests the relationship between service quality and firm performance.

The results of the study generally support theoretical predictions, and some interesting findings also emerged. The results reveal that there is a significant positive relationship between trustlessness and process innovation, trustlessness and administrative innovation, decentralization and product innovation, decentralization and process innovation, transparency and process innovation, security and product innovation, and security and process innovation. However, trustlessness was found to have an insignificant relationship with product innovation. Banking, being a service industry, this result has important implications. From the three dimensions of innovation, both product and process innovation are positively and significantly related to service quality. Further, consistent with the findings of existing literature, the relationship between service quality and firm performance was found to be positive.

Another significant finding and consequent implication of this study is that except security, all other dimensions of BT are positively and significantly related to service quality. Contrary to the proposed benefits on service quality aspects expected from BT’s heavy reliance on cryptographic security mechanisms (Dubovitskaya et al. 2017; Schlegel et al. 2018), our results indicate that the security dimension is having an insignificant relationship with service quality. Since processing speed plays a significant role in achieving superior service quality and faster banking transactions is one of the key advantages expected from BT, this result should be read along with some of the previous studies investigating the security-speed trade-offs in blockchain protocols when it comes to tackling scalability (Kiayias and Panagiotakos 2015). Research on this area is still immature. Extensive research on different aspects of BT, primarily related to security, speed, and scalability in delivering financial services, is required to overcome the challenges hindering its large-scale adoption. Importantly, the significance of the results lies in the fact that it reveals that an in-depth understanding of security aspects of blockchain systems will be needed when considering large-scale implementations in the banking sector.

5 Conclusions

In this work, we have attempted to foster a general understanding of the impact of blockchain technology from a managerial perspective. A theoretical model is developed and empirically tested to explain the potential impact of BT on innovation, service quality, and firm performance in the context of banking industry. This study makes several significant contributions to theory and practice. It is the first of its kind to shed light on the various dimensions of blockchain technology and its impact on innovation, service quality, and firm performance. The findings of this study provide several important considerations to the decision makers regarding implementation of BT in their organizations. The results provide a better understanding of why banking industry might want to invest in using blockchain-based technologies. Further, this study corroborates prior research relating service quality and performance. Finally, given the little empirical research on blockchain technology, future research across various other industries would help determine if the findings are more generalizable.

References

Beck, R., Avital, M., Rossi, M., & Thatcher, J. B. (2017). Blockchain technology in business and information systems research. Business & Information Systems Engineering, 59(6), 381–384.

Beck, R., Stenum Czepluch, J., Lollike, N. & Malone, S. (2016). Blockchain–the gateway to trust-free cryptographic transactions. In 24th European Conference on Information Systems (ECIS). Istanbul.

Cai, Y., & Zhu, D. (2016). Fraud detections for online businesses: a perspective from blockchain technology. Financial Innovation, 2(20), 1–10.

Cooper, R. G., & Kleinschmidt, E. J. (1987). New products: what separates winners from losers? Journal of Product Innovation Management, 4(3), 169–184.

Cucurull, J. & Puiggalí, J. (2016). Distributed immutabilization of secure logs. In International Workshop on Security and Trust Management, pp. 122–137. Springer.

Dubovitskaya, A., Xu, Z., Ryu, S., Schumacher, M. & Wang, F. (2017). Secure and trustable electronic medical records sharing using blockchain. In AMIA annual symposium proceedings. American Medical Informatics Association, pp. 650–659.

Easterby-Smith, M. (1991). Management research: An introduction. London: Sage Publications.

Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research, 18(1), 39–50.

Garman, C., Green, M. & Miers, I. (2014). Decentralized Anonymous Credentials. In NDSS, pp. 17–30.

Gunday, G., Ulusoy, G., Kilic, K., & Alpkan, L. (2011). Effects of innovation types on firm performance. International Journal of Production Economics, 133(2), 662–676.

Guo, Y., & Liang, C. (2016). Blockchain application and outlook in the banking industry. Financial Innovation, 2, 24.

Hair, J. F., Black, W. C., Babin, B. J., Anderson, R. E., & Tatham, R. L. (2011). Multivariate Data Analysis (6th ed.). New Jersey: Pearson Prentice Hall.

Halaburda, H. (2018). Blockchain revolution without the blockchain? Communications of the ACM, 61(7), 27–29.

Hooper, D., Coughlan, J., & Mullen, M. R. (2008). Structural equation modelling: Guidelines for determining model fit. Electronic Journal of Business Research Methods, 6(1), 53–60.

Hu, L. T., & Bentler, P. M. (1999). Cutoff criteria for fit indexes in covariance structure analysis: Conventional criteria versus new alternatives. Structural Equation Modeling: A Multidisciplinary Journal, 6(1), 1–55.

Huckle, S., Bhattacharya, R., White, M., & Beloff, N. (2016). Internet of things, blockchain and shared economy applications. Procedia computer science, 98, 461–466.

Jiménez-Jiménez, D., & Sanz-Valle, R. (2011). Innovation, organizational learning, and performance. Journal of Business Research, 64(4), 408–417.

Kaynak, H. (2003). The relationship between total quality management practices and their effects on firm performance. Journal of Operations Management, 21(4), 405–435.

Kiayias, A. & Panagiotakos, G. (2015). Speed-Security Tradeoffs in Blockchain Protocols. IACR Cryptology ePrint Archive.

Marsh, H. W., & Hocevar, D. (1985). Application of confirmatory factor analysis to the study of self-concept: First-and higher order factor models and their invariance across groups. Psychological Bulletin, 97(3), 562–582.

Mone, M. A., McKinley, W., & Barker, V. L., III. (1998). Organizational decline and innovation: A contingency framework. Academy of Management Review, 23(1), 115–132.

OECD and Eurostat. (2005). Oslo manual: Guidelines for collecting and interpreting innovation data. Paris.

Parasuraman, A. (2010). Service productivity, quality and innovation: Implications for service-design practice and research. International Journal of Quality and Service Sciences, 2(3), 277–286.

Parasuraman, A., Zeithaml, V. A., & Berry, L. L. (1988). Servqual: A multiple-item scale for measuring consumer perceptions of service quality. Journal of Retailing, 64(1).

Peters, G. W., & Panayi, E. (2016). Understanding modern banking ledgers through blockchain technologies: Future of transaction processing and smart contracts on the internet of money. In Banking beyond banks and money, 239–278.

Roth, A. V., & Jackson, W. E., III. (1995). Strategic determinants of service quality and performance: Evidence from the banking industry. Management Science, 41(11), 1720–1733.

Schlegel, M., Zavolokina, L. & Schwabe, G. (2018, January). Blockchain Technologies from the Consumers’ Perspective: What Is There and Why Should Who Care?. In Proceedings of the 51st Hawaii International Conference on System Sciences.

Seebacher, S. & Schüritz, R. (2017, May). Blockchain technology as an enabler of service systems: A structured literature review. In International Conference on Exploring Services Science, pp. 12–23. Springer.

Swan, M. (2015). Blockchain: Blueprint for a new economy. Inc: O'Reilly Media.

Tapscott, D., & Tapscott, A. (2016). Blockchain revolution: How the technology behind bitcoin is changing money, business, and the world. Penguin.

Treleaven, P., Brown, R. G., & Yang, D. (2017). Blockchain technology in finance. Computer, 50(9), 14–17.

Verhees, F. J., & Meulenberg, M. T. (2004). Market orientation, innovativeness, product innovation, and performance in small firms. Journal of Small Business Management, 42(2), 134–154.

Weber, I., Xu, X., Riveret, R., Governatori, G., Ponomarev, A., & Mendling, J. (2016, September). Untrusted business process monitoring and execution using blockchain. In International Conference on Business Process Management (pp. 329–347). Cham: Springer.

Yee, R. W., Yeung, A. C., & Cheng, T. E. (2010). An empirical study of employee loyalty, service quality and firm performance in the service industry. International Journal of Production Economics, 124(1), 109–120.

Yli-Huumo, J., Ko, D., Choi, S., Park, S., & Smolander, K. (2016). Where is current research on blockchain technology? A systematic review. PLoS One, 11(10), e0163477.

Zhao, J. L., Fan, S., & Yan, J. (2016). Overview of business innovations and research opportunities in blockchain and introduction to the special issue. Financial Innovation, 2(28), 1–7.

Author information

Authors and Affiliations

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2021 The Author(s), under exclusive license to Springer Nature Switzerland AG

About this paper

Cite this paper

Rekha, A.G., Resmi, A.G. (2021). An Empirical Study of Blockchain Technology, Innovation, Service Quality and Firm Performance in the Banking Industry. In: Bilgin, M.H., Danis, H., Demir, E., Vale, S. (eds) Eurasian Economic Perspectives. Eurasian Studies in Business and Economics, vol 16/1. Springer, Cham. https://doi.org/10.1007/978-3-030-63149-9_5

Download citation

DOI: https://doi.org/10.1007/978-3-030-63149-9_5

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-030-63148-2

Online ISBN: 978-3-030-63149-9

eBook Packages: Economics and FinanceEconomics and Finance (R0)