Abstract

Blockchain technology is predicted to reshape existing business models of the financial services industry. But although blockchain is often seen as a strategic technology, research focusing on its impact on business models is still rare. This research derives a hypotheses model that connects IT innovations with the three generic value disciplines of banks “operational excellence”, “customer intimacy” and “product leadership” as well as the four generic elements of business models “what”, “who”, “how” and “value”. A business model acts as a mediator for IT innovation. To test the hypothesis model data provided from an international survey of 104 financial services institutions and start-up companies was applied. The results support the hypothesis that all three value disciplines might be impacted by blockchain technology in the future. The regression analysis reveals that especially banks’ operations could be significantly changed. With these results, this research contributes to the emerging literature on blockchain and business models and the strategic use of IT.

Similar content being viewed by others

Explore related subjects

Discover the latest articles, news and stories from top researchers in related subjects.Avoid common mistakes on your manuscript.

1 Introduction

Blockchain has most often been associated with the cryptocurrency Bitcoin, as its underlying technology which was first introduced in 2008 in a white paper by Satoshi Nakamoto (2008). This technology has been said to “change market paradigms” (Gumsheimer et al. 2016), to be able to “reverse the fortunes of the post-crisis financial sector” (Grewe and Bosch 2016), and is predicted to be the technology “most likely to change the next decade of business” across all industries (Tapscott and Tapscott 2016a). Despite the fact that it can be applied across industries, public attention has mainly focused on the financial industry in the last years. One of the reasons is that blockchain’s first application Bitcoin is one that is related to financial services. Furthermore, a recent report states that 42% of all blockchain applications that are currently tested by firms are from financial institutions (Hileman and Rauchs 2017). Among the various examples are trading platforms for digital assets or trade finance platforms.

A considerable amount of research was conducted in the short period of time, since Bitcoin’s introduction in 2008, that was driven by the attention that the topic has received. Most of the existing literature concentrates on technical issues related to scalability (Croman et al. 2016), security (Eyal and Sirer 2013), and privacy (Fabian et al. 2016; Zyskind et al. 2015) or around Bitcoin (Ingram and Morisse 2016; Connolly and Kick 2015). But although blockchain is often mentioned as a strategic technology to change entire business models, research on this topic is still rare, especially in the field of its strategic impact. Conversely, many studies show that companies across all industries consider blockchain as a technology that has a strategic impact on their existing business models (Holotiuk et al. 2017; Iansiti and Lakhani 2017; Morkunas et al. 2019).

Literature has developed the concept of the business model in the context of digitalization to analyse the impact of technology on a company (Al-Debei and Avison 2010). This paper extends existing research by focusing on the potential impact of blockchain on banks’ business models. To answer this research question, the paper derives 11 hypotheses that are tested using an international survey, directed at the upper management of banks, and non-banks. The paper has the objective to thoroughly examine how the technology may influence banks’ business models including business processes, capabilities, channels, cost structure, revenue models, product and service offerings and customer intimacy as relevant elements of analysis. A secondary objective of this study is to explore differences in standpoints of the respondents, i.e. if banks and non-banks have contrary opinions.

This paper contributes to the existing literature in two areas. First, it connects blockchain technology research with business model research by demonstrating how the financial services industry is affected. Second, the results of the research indicate that blockchain technology itself might have an important impact on future business models which can be shown at the example of banks in all areas.

The remainder of this paper is structured as follows: The next section discusses the relevant theoretical background of blockchain technology and business models. Section 3 expands the hypotheses model development. The subsequent section describes the research method, including sample selection and sample description. Section 5 focuses on the presentation of the results, while Sect. 6 discusses them in more detail. Finally, Sect. 7 outlines the main findings and research limitations.

2 Theoretical background

2.1 Prior research on blockchain and business models

Blockchain can be defined as: “(…) a type of distributed ledger, comprised of unchangeable, digitally recorded data in packages called blocks. These digitally recorded “blocks” of data are stored in a linear chain. Each block in the chain contains data (e.g. Bitcoin transaction), is cryptographically hashed. The blocks of hashed data draw

upon the previous block in the chain, ensuring all data in the overall “blockchain” has not been tampered with and remains unchanged.” (BlockchainTechnologies.com 2018, para. 3). Five core elements constitute the major elements of blockchain technology (Gupta 2017):

-

Distributed database The data is not controlled by a single party. The complete database, including its history are transparent for each participant of a blockchain. Participants can by themselves validate the records of their transaction partners.

-

Peer-to-peer (p2p) transactions Peers communicate directly with each other rather than through a central node and each node keeps and forwards data to all other nodes.

-

Transparency with pseudonymity Transactions are observable by any allowed node. Each node can keep its identity anonymous, or alternatively provide evidence of its identity.

-

Immutability of records When a transaction has occurred, its record is immutable since it’s “chained” to all prior transactions.

-

Computational logic Algorithms and rules can be created to trigger transactions automatically (e.g., smart contracts).

These distinctive features may generate new business models across all industries (Iansiti and Lakhani 2017). One of the most recent examples are smart contracts. As firms and their relationships with other companies are built on contract-based structures, the digitalization and automation of these contracts could have an enormous impact on value chains, hierarchies and processes. But despite the opportunities that the blockchain technology may have for businesses, research on the relationship between blockchain and business models is still not widespread. Existing literature on blockchain revolves primarily around Bitcoin and cryptocurrencies (Godsiff 2015; Lindman et al. 2017). Kazan et al. (2015) have identified six archetypal business model configurations in the Bitcoin space. In addition, researchers have analysed the behaviour of specific actors in the ecosystem around Bitcoin. This includes studies on entrepreneurs (Ingram et al. 2015; Ingram and Morisse 2016) and organizational adopters (Connolly and Kick 2015). Dhillon (2016) and Brenig et al. (2015) investigate Bitcoin’s role as an aid for money laundering and other criminal activities. A vast body of research focuses on digital currencies as a substitute for payment systems (e.g., Ali et al. 2014; Kazan et al. 2014). Beck et al. (2016) have developed a proof of concept prototype aimed at improving trust-based payment solutions at coffee shops. Others explore Bitcoin’s ability to serve as a substitute for fiat money (e.g., Glaser et al. 2014; Lo and Wang 2014), Bitcoin as an investment vehicle (Hur et al. 2015; Dyhrberg 2016), and the role of central banks in a world of cryptocurrencies (Barrdear and Kumhof 2016). Another research focus is on technical aspects. For example, research has been published on the technical issues related to scalability (Croman et al. 2016), security (Eyal and Sirer 2013), and privacy (Fabian et al. 2016; Zyskind et al. 2015).

Most recently, scholars increasingly center their research on blockchain applications that reach beyond digital currencies. Brenig et al. (2016) for example offer a framework to evaluate the economic value of decentralized consensus systems for information-based industries. Glaser and Bezzenberger (2015) provide a taxonomy for decentralized consensus systems. Wörner et al. (2016) categorise blockchain use cases across industries and discuss their disruptive potential. Further research focuses on the impact of blockchain in the banking industry. Topics include the penetration of Bitcoin in the context of retail banking (Geng 2016), and new technology-enabled value chains (Liebenau et al. 2014). In addition, Beck and Müller-Bloch (2017) develop a framework for how incumbent banks can incubate and accelerate blockchain innovations. But although this research touches the impact of blockchain on banks’ business models, most of it has experimental character and empirical data about the potentials does not exist as the before mentioned research primarily concentrates on concepts and frameworks.

2.2 Business models in banking

In literature, publications on the relationship between strategic questions and IS emerged already in the 1970s (Siegal 1975; McLean et al. 1977). Especially the cases of the SABRE booking system and the Baxter Healthcare online ordering system demonstrated that IS can generate competitive advantage and thus can be fundamental for a company’s business model as a ‘competitive weapon’ (Ives and Learmonth 1984; Porter 1985; Galliers 1993a). But in many of these cases research could show that many strategic applications were due more to serendipity than formal planning approaches (Ciborra 1994; Senn 1992). That is why later research emphasized the importance of organizational requirements (Galliers 1993b) and that ‘‘IT alone is not enough’’ (Powell and Dent-Micallef 1997). In recent years, the concept of ‘‘digital business” terms the fusion between IT and business strategy which indicates an increasingly blurring line between the two fields (Bharadwaj et al. 2013; Galliers 2011). In this view, IS has a direct impact on business models and can be used to shape customer interaction, business operations, and products and services (Al-Debei and Avison 2010). In this paper a business model “(…) defines “who” a firm’s customers are, “what” this firm is selling, “how” it produces its offering, and why its business provides “value”. The ‘why’ dimension is used interchangeably with the term ‘value’. The four dimensions “who”, “what”, “how” and “value” describe a business model of which the first two (“who” and “what”) address its external aspects and the second two (“how” and “why”) address its internal dimensions.” (Gassmann et al. 2014).

The banking business is especially affected by the direct impact of IT on business models as the industry has the highest percentage of IT spending concerning its revenues as it is an information based business whose products almost exclusively rely on data and IT has greatly enhanced bank performance (Davamanirajan et al. 2002, 2006). Most recently, the threats that banks face from innovative banking models from financial technology (fintech) start-up firms such as peer-to-peer lending or robo-advisors in some cases have even disintermediated traditional banks entirely (McKinsey and Company 2018). That is why many banks currently analyse their status quo as well as if and how they have to adapt to new business models with regard to these evolving new technologies (Libert et al. 2016).

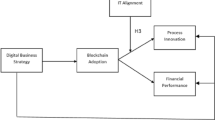

One prominent way to describe business models in banking is using the value disciplines typology devised by Treacy and Wiersema (1995) which was confirmed in later research (Palmer and Markus 2000; Weill and Ross 2004; Tallon 2008). Following this typology, firms can focus either on “operational excellence” which is centred around low cost, reliability, accuracy, and availability, on “customer intimacy”, meaning service quality or “product leadership”, which puts emphasis on innovative products and services. The model suggests focusing on just one of these three value disciplines following the concept of core competencies. A value discipline is not equivalent to a strategic vision, but it defines what a firm does and consequently structures every decision made (Treacy and Wiersema 1995). Although the three value disciplines show generic patterns of banks’ business models, they do not give guidance on how firms can adapt their business models to technological changes like those induced by blockchain. Previous literature notes the importance of distinguishing between the perception of the impact of an IT innovation and practical adoption like this is the case in the “Unified Theory of Acceptance and Use of Technology” (short: UTAUT2) (Venkatesh et al. 2003; Jasperson et al. 2005). But IT innovations per se do not lead to any value—thus the business model is the relevant mediator, for which we chose a similar approach as (Tallon 2010). Through the business model, an IT innovation is positively related to the three value disciplines as well as business processes which indirectly impact the value chain. Figure 1 connects the consequences of IT innovations on the banking business model elements and allows a more specific view on how financial services institutions can adapt their business models because of technological changes. In addition, it maps the hypotheses which are derived in the next section to the nodes (H1–H4c) between the banking and generic business model elements.

Research model

A business model innovation occurs once a minimum of two of the four generic business model elements are changed and launches a novel logic of how a company “creates value and captures value.” One key driver of change is technology, which is known to either initiate or allow business model innovation. Yet, it is important to note that simply utilizing a new technology won’t automatically generate value, the key is to comprehend the economic potential of it and to use it in a manner that creatively reforms a business (Gassmann et al. 2014). A standalone technology is deemed “worthless”, until the moment it is commercialized by becoming part of a business model. There are two ways technology can reach this stage. First, new technology can simply make use of the existing business model of the firm. Second, the firm might not have a business model suited for applying the new technology. If so, a new business model must be developed making optimized use of the technology (Chesbrough 2010).

Due to the deep-rooted beliefs and legacy systems of the banking industry, to utilize blockchain’s potential is a complex undertaking. Currently, banks are built on a centralized business model, with central ledgers—which is the custodian of the data. Blockchain technology gives rise to the possibility of the renovation of existing financial services’ business models. Apart from an infinite number of blockchain applications, the blockchain by itself—as a platform technology—already alters the business model by effectively removing redundant intermediaries. The predicted step forward for banks is to replace or accompany their centralized model in place with blockchain and network centred methods (Libert et al. 2016). The promise of a distributed ledger is represented by the robustness of the new network configurations, where a number of entities are linked and work in a collaborative manner. Therefore, blockchain requires banks to rethink their future business models (Finextra Research 2016).

3 Hypotheses model development

3.1 Derivation of hypotheses for operational excellence impact

Firms adhering to “operational excellence” offer reliable products or services, at the best price, with the least inconvenience at delivery (Treacy and Wiersema 1995). This value discipline puts emphasis on quality, reliability, an optimised supply chain and efficient and low-cost operations (Tallon 2010). In the centre of this view is “how” a firm’s products and services are produced including the processes, activities, resources, partners and competencies and is what defines the value chain (Gassmann et al. 2014). Specifically, back-office transaction processes could be drastically transformed by eliminating redundancies and settlement times (Underwood 2016). For example, a process for setting up a syndicated loan currently involves several attorneys and financial institutions, dealing with contracts and interaction of several parties, taking up to 20 days to settle (Fanning and Centers 2016). By means of blockchain, safe and almost immediate payments, data transfer, accurate trade records, and smart contracts allow for time reduction and improved quality of this process (Judd 2016). Another area of blockchain application in operations is regulation, where reporting, transparency and the diffusion of data could be optimized (Fanning and Centers 2016). To verify if there is believed to be a significant influence from blockchain on the operational excellence value discipline, the first hypothesis states:

Hypothesis 1

Blockchain is believed to have the highest impact on the operational excellence value discipline in banks.

A more specific view on banking processes shows that blockchain has a great potential to drive simplicity and efficiency through the establishment of new financial services infrastructure and processes. The areas that are positively affected are operational simplification, regulatory efficiency improvement, counterparty risk reduction, clearing and settlement time reduction, liquidity and capital improvement and fraud minimization (WEF 2016). While this view considers generic process optimization as the main benefits of blockchain, other research identifies improvement potentials in payments by the use of distributed payment platforms (Lindman et al. 2017) or sales related processes like the storage of online channel customer data in blockchain-based systems (Frey et al. 2016). The expected improvement of banks’ processes, capabilities and channels is part of the following hypothesis:

Hypothesis 2a

Blockchain is expected to improve banks’ processes, capabilities and channels.

Although process improvements are an important field of blockchain, the disruptive effect of the technology has been part of discussions in research and practice, especially in the area of peer-to-peer networks (Greiner and Hui 2015). Disruptive innovations can be seen from two perspectives. First as a threat, causing well-established firms to become antiquated, or worse—becoming wiped out. Second, as providing positive enhancements to some actors (Baiyere and Salmela 2015). The processes that accompany a radical innovation like blockchain, are usually unfamiliar to incumbent firms and call for comprehension, originating from external sources, along with traditional organizational knowledge (Hill and Rothaermel 2003). Firms are required to move outside of their traditional know-how to improve their capabilities to deal with radical innovation. Thus, they must engage with various market partners and experts from different domains (Christensen et al. 2001). In 2016, 13% of financial services firms in EMEA stated fear of disruption, as a reason for exploring blockchain, while 11% said it was due to competitive pressure, and only 2% said due to fear of FinTechs (Kocianski 2017). This view is shared also by other authors (e.g., Joichi et al. 2017). Summarized, these arguments culminate in the following hypothesis:

Hypothesis 2b

Blockchain is believed to lead to disruption of banks’ traditional operations.

Blockchain is capable of bringing cost savings for banks. One major reason for this, is that banks operate on heterogeneous IT applications that are siloed not only within banks but also between them. A recent study identified a potential to decrease operating costs for the worldwide banking industry and cut banks’ infrastructure costs for cross-border payments, securities trading and regulatory compliance amounting to US$15–20 billion per year (Lee 2016). This number shows that there might be a high potential to share a mutualized common infrastructure that previously was kept separately and runs independently by every market participant (Lee 2016). This means that blockchain can decrease transaction costs on both at an intra-organizational and at an inter-organizational level (Beck and Müller-Bloch 2017). This leads to the following hypothesis:

Hypothesis 2c

Blockchain is expected to enable significant cost savings.

3.2 Derivation of hypotheses for customer intimacy impact

Blockchain could improve service by increased transparency and trust between counterparties. The beneficial features of a blockchain based system are the absence of trust issues and improved transparency and security (Beck et al. 2016). Thus, a better-quality service offered to the banks’ customers could be achieved. In addition to service quality, blockchain could allow banks to reach new customer(s) (segments) and entering new markets. Potential areas in this context could for instance be international trade finance or new platforms for issuing digital assets. In addition, blockchain technology could also be the answer to include new customers from the vast unbanked markets, experiencing financial omission with no connection to a financial institution. At present, the number of unbanked customers amounts to 15% of the population in OECD countries. In fact, in Mexico 73% are unbanked, and in the U.S. the figure reaches 15% (of persons above 15 years old) meaning 37 million people are affected (Tapscott and Tapscott 2016b). The total amount of people globally in this potential customer segment is approximately over 2 billion. Due to the challenges of geographical division, mobile money suppliers lack a suitable strategy enabling them to achieve network effects, required for long-term survival. The promise lies in blockchain becoming the underlying structure to succeed in breaking the currently closed circle of mobile money services, allowing interoperability both locally and internationally. Furthermore, popularity of smartphone adoption in emerging countries is already a movement towards involving the unbanked segment. Hence, blockchain allows banks to reach the unbanked via smartphone applications, offering financial services based on blockchain technology (Gencer 2016). Blockchain technology could therefore allow banks to enter new markets and serve new customer segments. This leads to the following hypothesis:

Hypothesis 3a

Blockchain could have a positive impact on banks’ customer intimacy.

Although blockchain is often discussed in the context of achieving cost savings in operations rather than as a source for additional revenues, future revenue potentials could be leveraged by new blockchain applications with which banks are likely to offer services to customers (Macheel 2016). This is in line with a typical effect of disruptive innovations which say that an innovation will initially target niche markets and later progress to the mainstream markets, suggesting new revenue models are likely to develop (Govindarajan and Kopalle 2006). Examples for new sources of revenue for banks are new services like know-your-customer or personal data storage services which are implemented based on blockchain technology and which banks could provide as trusted advisors. In addition, banks’ sales processes today are centred around client advisors and in many cases still do not allow online processes. With blockchain based applications, novel online sales processes including different stakeholders in so called digital ecosystems become possible. An example would be a digital trade system that allows firms to provide and use compliance data without redundancy across different providers. Overall, these arguments form the basis for the following three hypotheses:

Hypothesis 3b

Blockchain is assumed to enable new revenue models.

Hypothesis 3c

Blockchain is believed to lead to the disruption of banks’ sales processes.

Hypothesis 3d

Banks could react against disintermediation by acquiring competitors, or self-develop the technologies required.

3.3 Derivation of hypotheses for product leadership impact

From a wider perspective, an innovation can be “the generation, acceptance, and implementation of new ideas, processes, products or services.” (Thompson 1965, p. 2). To alter, or to improve products and business models is the goal of an innovation process (Wörner et al. 2016; Bucherer et al. 2012). Moreover, Christensen et al. (2001) state the following about disruptive technologies: “In effect, they offer consumers products and services that are cheaper, better, and more convenient than ever before” (p. 81). According to Mougayar (2016) “You should not just see the Blockchain as a problem-solving technology. Rather, it is a technology that lets you innovate and target new opportunities.” (p. 146). In addition, Govindarajan and Kopalle’s (2006) disruptive innovation criterion number (2) explains that it should present new value propositions to entice new customers. Thus, banks could transform and create new value propositions which are attractive to customers. In investment banking for instance, new products become available for targeting mass-markets for the first time as they become profitable, thanks to the reduction in administrative costs (Robeco 2016). An example are novel platforms for digital assets which can be used by private investors to invest in start-up companies. Summarized, these arguments support the hypothesis of blockchain technology as an instrument for product and service innovation. Thus, the following three hypotheses can be derived.

Hypothesis 4a

Blockchain could have a positive impact on product leadership within the banking sector.

Hypothesis 4b

Blockchain is expected to lead to a redesign of existing products and services.

Hypothesis 4c

Blockchain is assumed to enable new products and services.

4 Research method

4.1 Data collection

To draw valid conclusions about blockchain’s potential in the banking industry and to generate a realistic sample set, we applied a systematic sampling approach with knowledgeable candidates.Footnote 1 The attitude of the respondents relied on predicting IT acceptance and usage on the job, including the perceived usefulness and ease of use (Venkatesh et al. 2003). The data for supporting the research model were gathered using the online survey tool SurveyMonkey. The survey consisted of three distinct parts: questions about the participant’s background and the core questions directly related to the hypotheses. The survey targeted two groups: banks and blockchain start-ups. The data set includes a list of 266 banks from Switzerland which is provided by the Swiss National Bank, and from which contact information of top management and executives was extracted manually. This list was chosen as the authors had good contact relationships to many of these banks. Furthermore, a list of 100 international banks was collected from the list of the top 100 global banks provided by S&P Global Market Intelligence (Mehmood and Chaudhry 2018). This resulted in a list of 366 banks in total. The second subject group targeted was non-banks, mainly start-ups with a blockchain focus. Non-financial blockchain start-ups were omitted. The mapping of blockchain start-ups was accomplished by web search. The four most prominent sources were the global, and open database Blockchain Angels’ Start-up Tracker curated by Outlier Ventures, CBINSIGHTS’s list of top 95 Bitcoin & Blockchain Startups In One Market Map, Blockchain startups by AngelList and The Crypto Valley Association’s corporate member directory (AngelList 2017; CBINSIGHTS 2017; Outlier Ventures 2017; The Crypto Valley Association 2017). This led to a total of 300 different non-banks which have a blockchain focus on financial services. The survey was open for a period of 3 months and reminders were sent out to improve the participation rate.

4.2 Data description

Overall, 104 responses were received, corresponding to a response rate of 15.4%. The sample size is consistent with similar research based on surveying the upper hierarchy of companies on the topic of company operations (Klassen and Jacobs 2001; Zahra 1991). The response rate is also what is to be expected in comparable studies, stating that 10–12% is common (Sieger et al. 2013, p. 12). The sample characteristics of the respondents are presented in Table 1.

4.3 Data analysis

Various statistical analysis methods were used to summarize the results of the survey, to test the hypotheses and to draw conclusions. The software tool IBM SPSS Statistics was used to perform all the statistical analysis. First, the results of the survey were evaluated in terms of descriptive statistics. This included performing a univariate analysis strengthened by inferential statistics by means of a t test, a multivariate analysis technique—the principal component analysis.Footnote 2 Second, inferential statistics were performed to reveal contrasting opinions between banks and non-banks. Finally, a linear regression was run on a selected variable. The results are presented in the next section.

5 Research results and discussion

5.1 Univariate analysis

A univariate analysis was performed to draw valid conclusions for our sample set, analysing the data in terms of central tendency and dispersion. Furthermore, a t-test to test the significance of difference between the sample means and four (indicating a neutral and/or an undecided opinion) was conducted. From the t-statistics, p values were derived. In tables 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12 highly statistically significant p values (two tailed) of p < 0.001 are indicated by ***, p values of p < 0.01 by ** and not significant p values are abbreviated by ns. To test our first hypothesis (H1), respondents were asked to rate the impact of blockchain on the three different value disciplines. The Likert scale ranged from no impact = 1, to very high impact = 7 (Table 2).

The first hypothesis is considered valid for our sample with 69.23% of respondents stating high or very high impact on operational excellence by blockchain. The customer intimacy value discipline contrasting scores only (N = 28, 26.93%) in this category, while (N = 38, 36.54%) of voters expect a moderate impact. Additionally, it can be observed that the value discipline product and service innovation closely follow with 60.54%, making it very likely to experience a high impact as well. As evidenced by the t-statistics in Table 2, the hypothesis is further supported as the sample mean was significantly larger than four for all value disciplines, but the biggest difference is found for the operational excellence value discipline (t-statistic = 13.49; p < 0.001).

The respondents were asked to rate six possible operational consequences, ranging from strongly disagree = 1 to strongly agree = 7, with 4 being equivalent to undecided. Please bear in mind the middle value is prone to influencing the analysis, when interpreting the results (Table 3).

In conclusion, hypothesis H2a yielded an agreeing trend for all six statements as illustrated in Table 3. A distinctive strongly agree was scored for the following three statements:

-

Blockchain is expected to enhance banks’ transaction-oriented back office processes and capabilities (N = 44, 42.31% and a t-statistic of 16.60; p < 0.001)

-

Blockchain is expected to require new financial infrastructure and new governance models (N = 40, 38.46% and a t-statistic of 12.56; p < 0.001)

-

Blockchain is expected to open new channels for banks (N = 34, 32.69% and a t-statistic of 11.42; p < 0.001)

To evaluate the potential of blockchain to disrupt banks, the respondents were asked to rate two potential scenarios ranging from strongly disagree = 1 to strongly agree = 7 and 4 if undecided (Table 4).

Overall, most respondents (N = 54, 52.28% and a t-statistic of 8.27; p < 0.001) agree or strongly agree that blockchain is believed to enable non-banks to disintermediate banks and they agreed, but to a lesser degree (N = 34,32.69% and a t-statistic of 5.21; p < 0.001) about the second scenario, that blockchain is believed to lead to circumvention of banks. The hypothesis H2b is validated for our sample as seen in Table 4, the respondents confirm the possibility of non-banks disintermediating banks and hence disrupting the banks’ traditional operations.

The respondents were asked to rate the significant cost savings enabled for four different processes by strongly disagree = 1 to strongly agree impact = 7, and the middle value of 4 if undecided (Table 5).

Table 5 concludes that the hypothesis H2c is validated for the sample, with strongly agree for significant cost savings in transaction oriented back office processes and inter-bank processes (t-statistic of 18.75; p < 0.001 and 17.68; p < 0.001 respectively), and with agree for significant cost savings in support oriented back office processes (t-statistic of 7.56; p < 0.01). However, the hypothesis does not hold for significant cost savings in front office processes, for which the difference from the neutral/undecided opinion is not significant (t-statistic of 0.41).

Hypothesis H3a aims to find out if there is a positive relationship between blockchain and banks’ customer intimacy. The respondents were asked to rate five statements related to customer intimacy by strongly disagree = 1 to strongly agree impact = 7 and the middle value of 4 if undecided. While all statements showed a trend to agree to various extents as shown in Table 6, the following two statements stood out with many respondents strongly agreeing:

-

Enable peer-to-peer interaction among customers without intermediaries (N = 36, 34.62 and a t-statistic of 15.57; p < 0.001)

-

Improved quality of banks’ services by increased trust and transparency (N = 17, 16.35% and a t-statistic of 7.84; p < 0.001) (Table 6).

Hence, hypothesis H3a is validated for the sample, and blockchain could have a positive impact on banks’ customer intimacy value discipline. The respondents were asked to rate two statements regarding new revenue models by strongly disagree = 1 to strongly agree impact = 7 and the middle value of 4 if undecided. The results are shown in Table 7 and Table 8.

Most respondents (N = 68, 65.39% and a t-statistic of 19.84; p < 0.001) agree or strongly agree with the statement, confirming the hypothesis H3b (Table 8).

Overall, most respondents (N = 57, 54.81% and a t-statistic of 11.90; p < 0.001) agree or strongly agree that blockchain is believed to lead to a redesign of existing revenue models. This would imply disruption of the banks’ sales processes, and thus H3c is validated. As the statement “Blockchain is believed to lead to a redesign of existing revenue models” indirectly means new revenue models, it represents a control question for H3b above. Thus, given the similarity of the descriptive statistics for both statements our hypothesis H3b that blockchain is assumed to enable new revenue models is confirmed twice for the sample.

For the hypothesis H3d the respondents were asked to rate two already predicted scenarios by strongly disagree = 1 to strongly agree impact = 7 and the middle value of 4 if undecided (Table 9).

As noted in Table 9, overall, most respondents (N = 61, 58.65% and a t-statistic of 12.26; p < 0.001) agree, or strongly agree with the first scenario. For the second scenario, the trend was also that most respondents (N = 51, 49.04% and a t-statistic of 8.87; p < 0.001) agree, or strongly agree. In conclusion, the first scenario which is a common business practice, had more than double the number of respondents that strongly agree, compared to the second scenario. Thus, our hypothesis H3d stating—Banks could react against disintermediation by acquiring competitors, or self-develop the technologies required—is validated for our sample. In addition, we discover the second scenario is a plausible one too as the inferential statistics results also show that the hypothesis is supported.

Furthermore, the respondents were asked to rate the following statement: Blockchain is believed to lead banks to take on more R&D and boost product and service innovation to offer customers leading-edge products and services (Table 10).

The opinion between the two groups differs as revealed in the t-tests. The mean scores significantly differed for banks and non-banks, 5.12 and 5.79 respectively.Footnote 3 Consequently, non-banks agree with the statement more than banks. As seen in Table 10, overall, most respondents (N = 58, 55.77% and a t-statistic of 12.10; p < 0.001) agree or, strongly agree and so we consider the hypothesis H4a validated for the sample.

Hypothesis H4b stated that blockchain is expected to lead to a redesign of existing products and services. The respondents were asked to rate the degree of impact of blockchain on existing products and services from no impact = 1 to high impact = 7. They were then asked to rate the impact on five different existing products and service areas by strongly disagree = 1 to strongly agree = 7 and 4 if undecided. The results are reported in Table 11.

Most respondents (N = 55, 52.89% and a t-statistic of 9.43; p < 0.001) expect the impact on existing products and services to be high or very high. Thus, our respondents tend to agree that blockchain is expected to have a significant impact on banks’ existing products and services. Next, we verify which of the existing products and service areas will be affected due to blockchain. As most respondents (N = 70, 67.30% and a t-statistic of 15.40; p < 0.001) agree or strongly agree, our sample concludes that existing products and services in payments is believed to be impacted by blockchain. Also, most respondents (N = 56, 53.85% and a t-statistic of 8.41; p < 0.001) agree or strongly agree that existing products and services in investments is believed to be impacted by blockchain. In addition, most respondents (N = 63, 60.57% and a t-statistic of 8.23; p < 0.001) agree or strongly agree blockchain is believed to have an impact on existing products and services in financing. In terms of advisory, the difference from the mean is insignificant (− 0.12; not significant), thus the undecided choice dominates (N = 25, 24.04%) and as many people that agree as disagree (both N = 19,18.27%). Therefore, for our sample, it is unclear if blockchain is expected to have an impact on existing products and services in advisory. Overall, the trend is for respondents to agree existing products and services in cross-processes are expected to be impacted as (N = 56, 53.49% and a t-statistic of 11.06 p < 0.001) agree or strongly agree.

The opinion between the two groups differs as revealed in the student test,Footnote 4 the mean scores significantly differ between banks and non-banks for all points above except for payments. To summarize, the hypothesis H4b is validated for the sample: blockchain is expected to lead to a redesign of existing products and services and this involves impact on all existing product and services areas mentioned, expect for the field of advisory .

Hypothesis H4c states that blockchain is assumed to enable new products and services. The respondents were asked to rate this statement from strongly disagree = 1 to strongly disagree = 7 and 4 if undecided. They were then asked to rate the statement regarding five different products and service areas by the same scale. The results are shown in Table 12.

The opinion between the two groups differ as the means significantly differs for banks and non-banks for all abovementioned points.Footnote 5 The respondents scored very similarly to the previous hypothesis H4b about redesign of existing products and services. In terms of the modes, all points were equal expect for payments which were bimodal with 6 and 7 in H4b. To summarise, the hypothesis H4c is also validated for the sample as the sample mean for five areas is significantly larger than four (all p values < 0.001): blockchain is assumed to lead to new products and services, and this involves new products and services in all areas mentioned, expect for the field of advisory (t-statistic 1.37; not significant).

5.2 Principal component analysis

A multivariate method is used, the principal component analysis (PCA), to allow us to detect the linear components of our set of variables (Field 2009, p. 792). The technique achieves a data reduction from 37 variables down to four principal ones that explain 50.18%Footnote 6 of the variance within this data set.Footnote 7 The elbow rule states that only components above the elbow in the scree plot graph should be retained. A clear break is visible in Fig. 2 below at component number four, after which the curve begins to flatten. This indicates that all remaining components after the fourth make up for decreasing amounts of the total variance (UCLA 2017a.). Thus, the first four components are extracted for our PCA.

Screen plot graph of PCA

As shown in Table 13, the first principal component is strongly correlated with four of the original variables. This component is highly linked to the observations agreeing blockchain is expected to lead to new products and services in the area of investments and is expected to have an impact on existing products and services in the area of investments. Moreover, the component is connected to the blockchain impacting existing products and services overall and leading to new products and services overall. Hence, the first principal factor can be represented as: change in product and service offerings. This means banks will adapt their existing offerings to utilize benefits of blockchain, as well as develop entirely new products to cover the opportunities opened up by blockchain. Special emphasis is put on products and services in investments.

The back-office enhancements are assigned to the second principal component. The second principal component's most correlated variables are reported in Table 14. As banks acquire or reproduce the technologies required, they enhance transaction oriented back office processes and capabilities, which in turn improves the support oriented back office processes and capabilities as well as the security and reliability of the entire system.

The third principal component can be defined as potential changes in the financial infrastructure and governance models. The third principal component's most correlated variables are listed in Table 15. From the perspective of non-banks this is a desirable scenario, giving them a competitive edge against the banks who must carry the cost of implementing large scale changes. By not doing so, banks would risk disruption of their traditional operations i.e. disintermediation and circumvention .

The fourth principal component is improved customer centric services expected to be enabled by the blockchain. The links between the three variables in Table 16 is logical: the improved customer centricity will bring new customers into the bank and offer better service to existing customers. However, the relatively low correlation parameters suggest that respondents are somewhat pessimistic about the positive impact happening in this field.

The sample can be summarized with these four principal components that lead to the following conclusions:

-

Component 1 indicates a change in product and service offerings, in particular in investments.

-

Component 2 shows that specifically back office operation enhancements are targeted by blockchain.

-

Component 3 reveals potential changes in the financial infrastructure and governance models.

-

Component 4 shows improvements in customer centricity (customer access and new customer segments).

5.3 Inferential statistics

To reveal whether the opinions of the two respondent groups, banks vs. non-banks, opinions varied significantly, an independent samples t-Test was conducted (Table 17).Footnote 8 The test investigates the following hypotheses:

H 0

The opinions of banks and non-banks are not different.

H 1

The opinions of banks and non-banks differ.

Table 17 summarizes all variables that are statistically significant (p value < 0.05).

There are eight groups of variables where disagreements arose. In all of these cases, the non-banks had higher means than the banks, indicating that they voted farther out at the higher end of the scale. It can be assumed that:

-

Banks might be more conservative than start-ups.

-

Non-banks are possibly more involved about future effects of blockchain.

-

An optimism typical for start-ups is present.

The assumed explanation is banks confidence in their present products assuring leadership without necessarily relying on innovative products based on blockchain but being open to the idea. For natural reasons the non-banks will rely entirely on an innovative product offering to achieve product leadership using blockchain.

5.4 Regression analysis

In the following section a linear regression is conducted which might uncover hidden relationships in the sample. For this, a variable from hypothesis H2b is selected, as it is the most representative of measuring blockchain’s impact on the banking industry, and it considers the opinions of the two respondent groups. Hypothesis H2b states that blockchain is believed to lead to disruption of banks’ traditional operations. The dependent variable for which the regression is run is: blockchain is believed to enable non-banks to disintermediate banks. The goal is to discover which variables influence this statement. As it is unclear which variables will be deterministic for this statement. The backward variable selection method is used where predictors remain until reaching the ideal R2 (Field 2009, p. 213). In this case, the selection took 28 steps to reach the optimal R2. As can be seen in Table 19, 9 significant independent variables could be identified that show relationships with the dependent variable.Footnote 9 This method inserts all predictors (independent variables) in the model and assesses the influence of each predictor by evaluating the significance value of the t-test for each one. It is then compared with a dismissal criterion—in this case the adjusted R2. The model is re-estimated for the following table which provides a summary of the model.Footnote 10 The R value is 0.802 and denotes the simple correlation, which points to a high degree of correlation. The R squared (R2) value illustrates that 64.3% of the total variation in the target variable, is explained by the nine independent variables—which is considerable (Laerd Statistics 2013). The adjusted R2 is 0.608, which is close to the value of R2, a difference of 0.035, suggesting the cross-validity of the model is good. Thus, if the model was to be generalized i.e. derived from the population, it would represent 3.5% less variance in the outcome (Field 2009, p. 236).

The ANOVAFootnote 11 describes the appropriateness of the regression equation for the data. As the p value of the Fischer test,—the statistical significance value (p value here below)—is less than alpha (0.05), the regression model statistically significantly forecasts the target variable (Laerd Statistics 2013). As summarized in Table 18, the result is a significant regression model of: (F(9,94) = 18.776, p = 0.000), with a R2 of 0.643.

The following 9 predictor variables have a statistically significant impact on the statement: the blockchain is believed to enable non-banks to disintermediate banks. The beta stands for the change in the statement caused by one unit change in the predictor (Field 2009, p. 259). The constant or the so-called y-intercept of the regression—is the expected value of the statement when all other variables are equal 0 (UCLA 2017b). For this, each variable is analysed regarding its relationship to the statement. The results are shown in Table 19.

-

1.

Blockchain is expected to improve security and reliability of banks’ system (from H2a)

Specifically, there is a negative relation between the variable and the statement. For every one point score increase on the Likert scale about this variable—there is a 0.186 increase in the score for the statement. This indicates that a respondents’ positive view on blockchain improving both security and reliability of banks systems, will positively impact their expectation of non-banks disintermediating banks too.

-

2.

Blockchain is expected to enable significant cost savings in transaction oriented back office processes (from H2c)

The model predicts a positive association. For a one score increase on the Likert scale, about the following variable, there is a 0.25 increase in the score for the statement. We can assume significant cost saving brought about by increased productivity and efficiency in the processes, does lead to a competitive advantage for non-banks who already possess the technology. Banks would need to go through a costly and time consuming process of replacing solutions in place today with blockchain based processes, which needs to be integrated with other systems as well within the bank. Non-banks will be able to ‘run faster’ implementing tailored processes, helping them to disintermediate banks.

-

3.

Blockchain is expected to enable new revenue models (H3b)

For each one point increase on the Likert scale for this variable, there is a 0.518 decrease in the score for the statement. We can infer the more respondents agree with this variable, the more they recognize that a new revenue model is the basis for succeeding with the introduction of massive use of blockchain, where banks are in a stronger position due to their knowledge about the market and organisation in place. This would make it less likely to witness disintermediation of banks.

-

4.

Blockchain is expected to improve the quality of banks services by increased trust and transparency (from H3a)

For each one point increase on the Likert scale for this variable, there is a 0.185 decrease in the score for the statement. This reveals respondents’ opinion that improved trust and transparency in banks would counteract the opportunity to disintermediate them.

-

5.

Blockchain is expected to enable peer-to-peer interaction among customers without intermediaries (from H3a)

For each one point increase on the Likert scale for this variable, there is a 0.253 increase in the score for the statement. This show coherence, the respondents who agree with this variable e.g. customers have various alternative offerings on the market e.g. new apps that can be used without the involvement of banks, the more they will agree the blockchain is expected to enable non-banks to disintermediate banks. This is an indicator of banks traditionally weak interest to get involved in P2P business, leaving it wide open for competitors.

-

6.

Blockchain is expected to have an impact on existing products and services in advisory (from H4b)

For each one point increase on the Likert scale for this variable, there is a 0.253 increase in the score for the statement. This suggests respondents don’t think banks will be able to reform their existing advisory systems to properly utilize blockchain leaving this area to non-bank competitors.

-

7.

Blockchain is expected to enable new products and services (H4c)

For each one point increase on the Likert scale for this variable, there is a 0.44 increase in the score for the statement. This positive relationship indicates that since developing new products and services is a golden opportunity for non-banks, it can result in disintermediating banks’ traditional offerings.

-

8.

Blockchain is expected to lead to new products and services in advisory (from H4c)

For each one point increase on the Likert scale for this variable, there is a 0.18 decrease in the score for the statement. A similar reasoning to point 6. can be applied. The motivation to replace manned processes with automated ones in this field is controversial at banks.

-

9.

Blockchain is expected to lead to circumvention of banks (from H2b)

For each one point increase on the Likert scale for this variable, there is a 0.517 increase in the score for the statement. This show coherence, the respondents who agree the blockchain is believed to lead to circumvention of banks e.g. as customers have access to various alternative offerings e.g. new apps, security, efficiency, and lower costs, the more they agree the blockchain could enable non-banks to disintermediate banks.

6 Discussion of results

The results of the descriptive and inferential statistics analysis confirmed that all hypotheses of the survey are validated. Table 20 outlines the research results.

The descriptive statistics analysis then narrowed down the findings to four principal components. Thus, the underlying structure of the data set is made up of these key components summarized in Table 21.

7 Conclusions

This research aimed to examine how blockchain’s elements might change banks’ existing business models in the future. The hypotheses model was derived by fusing generic business model elements “what”, “who, “how” and “value” with the bank specific value disciplines “product leadership”, “customer intimacy” and “operational excellence.” The 11 hypotheses were tested by issuing a global survey resulting in a total of 104 respondents, which represent the upper management of both banks and non-banks. The main conclusions derived from this analysis can be summarized in three major aspects.

Firstly, the revelations suggest that blockchain technology, impacts all elements of banks’ business models (who-what-how-why). As the criteria for business model innovation is, that at least two elements are changed, blockchain might lead to new business models in banking and thus challenging the status quo. In addition, the four components predict significant changes in all four elements of banks business models, too. This view is consistent with many analyses from other research that is not based on empirical data (e.g., Iansiti and Lakhani 2017; Joichi et al. 2017; McKinsey and Company 2018). First studies of the evolving alternative finance sector in addition shows that a variety of novel business model approaches currently emerges in parallel to the existing ones (Rauchs et al. 2018). Among the examples are mining approaches for cryptocurrencies, digital custody services or hardware manufacturers which provide a variety of tools for different purposes (e.g. storage devices, mining infrastructure, etc.). If and how banks will adopt to these new emerging business models is yet open as none of the incumbents already started to apply them.

Second, the inferential statistics results revealed significantly contrasting opinions between banks and non-banks for 25 of the 37 variables. In these instances, the non-banks scored higher i.e. stronger agree/higher impact. It can

be assumed that banks are more conservative than start-ups, and non-banks are possibly more involved in researching future effects of blockchain, as well as have more optimism for the new models to be successful. While the start-up industry has been very dynamic in recent years in exploring novel blockchain concepts, the opposite can be said about the incumbents. Although banks tried to adapt blockchain for their existing models, only small steps could be observed. An example is the area of trade finance for which banks formed international consortia. The existing gap between the incumbents and the start-ups might be one explanation why the start-ups evaluate the future potential higher than the incumbents. Another argument which supports this hypothesis is regulation. The existing regulation regimes in many countries is often not flexible enough to allow incumbents novel business model approaches.

Third, the different statements that the respondents made regarding blockchain’s significance and its potential revealed that the technology is still in a very early phase of development. The statements for example included: one of many technologies as part of a toolbox, a disruptive technology, a foundational technology and a revolutionary technology. Although blockchain is expected to provide several specific features like efficiency, decentralization, transparency, trust and security, banks do not very proactively explore the opportunities in areas like product innovation or novel service offerings by enhancing back office processes and by improving their customer focus. But for this, changes in the financial market infrastructure and governance models are required. New business models in banking based on blockchain therefore require not only technological adaptations, but primarily rely on organizational and cultural changes in the applying firms.

Although, this analysis revealed new insights about the future potentials of blockchain regarding the technology’s impact on banks’ business models, this research has some limitations. First, a larger sample size would enhance the insights obtained from the survey. Second, while the analysis made some logical assumptions of the potential relationships, it would have been valuable to obtain a richer insight about why respondents answered in these particular ways. In-depth case studies could contribute to this. Third, a more in-depth perspective on geographical and country specifics might also lead to interesting findings, especially as regulations often address issues of national interest. Further research could address these limitations and further explore the potential opportunities of blockchain for enabling new business models in banking.

Notes

See Appendix 1 for additional respondent information.

See Appendix 2.

See Table 17.

See Table 17.

See Table 17.

See “Component matrix” in Appendix 2.

See “Total variance explained” in Appendix 2.

See Appendix 3 for full independent samples test, independent sample test with sig. variables and the complete group statistics table.

See “Model summary” in Appendix 4.

See “Coefficients tables: model 1 and model 29” in Appendix 4.

See “ANOVA table” in Appendix 4.

References

Al-Debei MM, Avison D (2010) Developing a unified framework of the business model concept. Eur J Inf Syst 19:359–376

Ali R, Barrdear J, Clews R, Southgate J (2014) Innovations in payment technologies and the emergence of digital currencies. Bank Engl Q Bull 54(3):1–14

AngelList (2017) Blockchains startups. AngelList.co. https://angel.co/blockchains. Accessed 30 June 2017

Baiyere A, Salmela H (2015) Wicked yet empowering - when IT innovations are also disruptive innovations. ICIS 2015 proceedings. http://aisel.aisnet.org/cgi/viewcontent.cgi?article=1656&context=icis2015. Accessed 1 Nov 2017

Barrdear J, Kumhof M (2016) The macroeconomics of central bank issued digital currencies. Staff working paper (605), Bank of England. www.bankofengland.co.uk/research/Documents/workingpapers/2016/swp605.pdf. Accessed 12 Dec 2017

Beck R, Müller-Bloch C (2017) Blockchain as radical innovation: a framework for engaging with distributed ledgers as incumbent organization. In: HICSS 2017 proceedings 2017, pp 5390–5399. http://scholarspace.manoa.hawaii.edu/bitstream/10125/41815/1/paper0666.pdf. Accessed 6 Nov 2017

Beck R, Stenum Czepluch J, Lollike N, Malone S (2016). Blockchain—the gateway to trust-free cryptographic transactions. In: ECIS 2016, pp 1–14. https://pure.itu.dk/ws/files/81041470/ECIS_Format_Blockchain_paper_160330.pdf. Accessed 8 Apr 2017

Bharadwaj A, El Sawy O, Pavlou P, Venkatraman N (2013) Digital business strategy: toward a next generation of insights. MIS Q 37(2):471–482

BlockchainTechnologies.com (2016) Blockchain explained—distributed ledgers and blockchain technology. http://www.blockchaintechnologies.com/blockchain-definition. Accessed 6 Mar 2017

Brenig C, Accorsi R, Müller G (2015) Economic analysis of cryptocurrency backed money laundering. In: ECIS 2015 proceedings. http://aisel.aisnet.org/ecis2015_cr/20. Accessed 6 Nov 2017

Brenig C, Schwarz J, Rückeshäuser N (2016) Value of decentralized consensus systems—evaluation framework. In: ECIS 2016 proceedings. http://aisel.aisnet.org/ecis2016_rp/75/. Accessed 6 Nov 2017

Bucherer E, Eisert U, Gassmann O (2012) Towards systematic business model innovation: lessons from product innovation management. Creat Innov Manag 21(2):183–198

CBINSIGHTS (2017) Ledger fever: 95 Bitcoin & blockchain startups in one market map. CB insights research. https://www.cbinsights.com/research/bitcoin-blockchain-startup-market-map/. Accessed 27 Mar 2017

Chesbrough H (2010) Business model innovation: opportunities and barriers. Long Range Plan 43(Business Models):354–363. https://doi.org/10.1016/j.lrp.2009.07.010

Christensen C, Craig T, Hart S (2001) The great disruption. Foreign Aff 80(2):80–95

Ciborra C (1994) From thinking to tinkering: the grassroots of IT and strategy. In: Ciborra C, Jelessi T (eds) Strategic information systems: a European perspective. Wiley, Chichester, pp 70–83

Connolly A, Kick A (2015) What differentiates early organization adopters of Bitcoin from non-adopters? In: AMCIS 2015 proceedings. http://aisel.aisnet.org/amcis2015/AdoptionofIT/GeneralPresentations/46

Croman K, Decker C, Eyal I, Gencer AE, Juels A, Kosba A, Miller A, Saxena P, Shi E, Sirer EG, Song D, Wattenhofer R (2016) On scaling decentralized blockchains. In: Financial cryptography and data security lecture notes in computer science, pp 106–125

Davamanirajan P, Mukhopadhyay T, Kriebel CH (2002) assessing the business value of information technology in global wholesale banking: the case of trade services. J Organ Comput Electron Commer 12(1):5–16

Davamanirajan P, Kauffman RJ, Kriebel CH, Mukhopadhyay T (2006) Systems design, process performance and economic outcomes in international banking. J Manag Inf Syst 23(2):67–92

Dhillon G (2016) Money laundering and technology enabled crime: a cultural analysis. In: AMCIS 2016 proceedings. http://aisel.aisnet.org/amcis2016/ICTs/Presentations/17/

Dyhrberg AH (2016) Hedging capabilities of Bitcoin. Is it the virtual gold? Finance Res Lett 16:139–144

Eyal I, Sirer E (2013) Majority is not enough: Bitcoin mining is vulnerable. Cornell University Library. http://arxiv.org/abs/1311.0243. Accessed 4 Dec 2017

Fabian B, Ermakova T, Sander U (2016) Anonymity in Bitcoin? The users’ perspective. In: ICIS 2016 proceedings

Fanning K, Centers DP (2016) Blockchain and its coming impact on financial services. J Corp Account Finance 27(5):53–57. https://doi.org/10.1002/jcaf.22179

Field A (2009) Discovering statistics using SPSS and sex and drugs and rock ‘n’ roll. SAGE, Los Angeles

Finextra Research (2016) Banking on blockchain: charting the progress of distributed ledger technology in financial services, 1st edn, Finextra Research, pp 5–26. https://www.ingwb.com/media/1609652/banking-on-blockchain.pdf. Accessed 10 June 2017

Frey RM, Wörner D, Ilic A (2016) Collaborative filtering on the blockchain: a secure recommender system for e-commerce. In: AMCIS proceedings

Galliers RD (1993a) IT strategies: beyond competitive advantage. J Strateg Inf Syst 2(4):283–291

Galliers RD (1993b) Towards flexible information architecture: integrating business strategies, information systems strategies and business process redesign. Inf Syst J 3(3):199–213

Galliers RD (2011) Further developments in information systems strategising: unpacking the concept. In: Galliers RD, Currie WL (eds) The Oxford handbook of management information systems: critical perspectives and new directions. Oxford University Press, Oxford, pp 329–345

Gassmann O, Frankenberger K, Csik M (2014) The business model navigator: 55 models that will revolutionise your business. Pearson, Harlow

Gencer M (2016) Blockchain can bring the unbanked into the global economy. Am Banker 181(145):1

Geng D (2016) Data analytics on consumer behavior in omni-channel, retail banking, card and payment services. In: PACIS 2016 proceedings. http://aisel.aisnet.org/pacis2016/186

Glaser F, Bezzenberger L (2015) Beyond cryptocurrencies - a taxonomy of decentralized consensus systems. In: ECIS 2015 proceedings. http://aisel.aisnet.org/ecis2015_cr/57/. https://doi.org/10.18151/7217326

Glaser F, Zimmermann K, Haferkorn M, Weber MC, Siering M (2014) Bitcoin-asset or currency? Revealing users’ hidden intentions. In: ECIS 2014 proceedings. http://aisel.aisnet.org/ecis2014/proceedings/track10/15. Accessed 1 Dec 2017

Godsiff P (2015) Bitcoin: bubble or blockchain? www.nemode.ac.uk/wp-content/uploads/2015/10/Godsiff-2015-KES-AMSTA.pdf. Accessed 1 Dec 2017

Govindarajan V, Kopalle PK (2006) The usefulness of measuring disruptiveness of innovations ex post in making ex ante predictions. J Prod Innov Manag 23(1):12–18. https://doi.org/10.1111/j.1540-5885.2005.00176.x

Greiner M, Hui W (2015) Trust-free systems—a new research and design direction to handle trust-issues in P2P systems: the case of Bitcoin. In: AMCIS 2015 proceedings

Grewe I, Bosch R (2016) Can the financial services industry master cryptofinance? BearingPoint Institute. http://www.bearingpoint.com/ecomaXL/files/BearingPoint-Institute_006-01_Can-the-financial-services-industry-master-cryptofinance.pdf&download=0. Accessed 1 Dec 2017

Gumsheimer T, Felden F, Schmid C (2016) Recasting IT for the digital age, BCG perspectives, The Boston Consulting Group. https://www.bcgperspectives.com/content/articles/technology-innovation-recasting-it-for-the-digital-age

Gupta V (2017) The Promise of blockchain Is a world without middlemen. Harvard business review digital articles, pp 2–5. https://hbr.org/2017/03/the-promise-of-blockchain-is-a-world-without-middlemen. Accessed 28 Mar 2017

Hileman G, Rauchs M (2017) Global blockchain benchmarking study. University of Cambridge, Cambridge

Hill CL, Rothaermel FT (2003) The performance of incumbent firms in the face of radical technological innovation. Acad Manag Rev 28(2):257–274. https://doi.org/10.5465/AMR.2003.9416161

Holotiuk F, Pisani F, Moormann J (2017) The impact of blockchain technology on business models in the payments industry. In: Leimeister JM, Brenner W (Hrsg) Proceedings der 13. internationalen Tagung Wirtschaftsinformatik (WI 2017), St. Gallen, S. pp 912-926. https://wi2017.ch/images/wi2017-0263.pdf. Accessed 10 July 2017

Hur Y, Jeon S, Yoo B (2015) Is Bitcoin a viable e-business? Empirical analysis of the digital currency’s speculative nature. In: ICIS 2015 proceedings. http://aisel.aisnet.org/icis2015/proceedings/eBizeGov/18. Accessed 3 Dec 2017

Iansiti M, Lakhani KR (2017) The truth about blockchain. Harv Bus Rev 95(1):118–127

Ingram C, Morisse M (2016) Almost an MNC: Bitcoin entrepreneurs’ use of collective resources and decoupling to build legitimacy. In: HICSS 2016 proceedings. http://ieeexplore.ieee.org/document/7427692. Accessed 3 Dec 2017

Ingram C, Morisse M, Teigland R (2015) ‘A bad apple went away’: exploring resilience among Bitcoin entrepreneurs. In: ECIS 2015 proceedings. http://aisel.aisnet.org/ecis2015_rip/31

Ives B, Learmonth G (1984) The information system as a competitive weapon. Commun ACM 27(12):1193–1201

Jasperson JS, Carter PE, Zmud RW (2005) A comprehensive conceptualization of post-adoptive behaviors associated with information technology enabled work systems. MIS Q 29(3):525–557

Joichi I, Narula N, Ali R (2017) The blockchain will do to the financial system what the internet did to media. Harvard business review digital articles, pp 2–5. https://hbr.org/2017/03/the-blockchain-will-do-to-banks-and-law-firms-what-the-internet-did-to-media. Accessed 27 Mar 2017

Judd E (2016) Breaking down blockchain. Indep Bank 66(3):102–103

Kazan E, Tan C-W, Lim ET (2014) Towards a framework of digital platform disruption: a comparative study of centralized & decentralized digital payment providers. In: ACIS 2014 proceedings. http://hdl.handle.net/10292/8052. Accessed 3 Dec 2017

Kazan E, Tan C-W, Lim ET (2015) Value creation in cryptocurrency networks: towards a taxonomy of digital business models for Bitcoin companies. In: PACIS 2015 proceedings. http://aisel.aisnet.org/pacis2015/34. Accessed 3 Dec 2017

Klassen RD, Jacobs J (2001) Experimental comparison of web, electronic and mail survey technologies in operations management. J Oper Manag 19(6):713–728

Kocianski S (2017) The blockchain in banking report: the future of blockchain solutions and technologies. http://uk.businessinsider.com/blockchain-in-banking-2017-3?r=US&IR=T. Accessed 30 Mar 2017

Laerd Statistics (2013) One-way ANOVA in SPSS Statistics: understanding and reporting the output. Statistics.laerd.com. https://statistics.laerd.com/spss-tutorials/one-way-anova-using-spss-statistics-2.php. Accessed 19 Oct 2017

Lee P (2016) Banks take over the blockchain. Euromoney 47(566):92–99

Libert B, Beck M, Wind JY (2016) How blockchain technology will disrupt financial services firms. http://knowledge.wharton.upenn.edu/article/blockchain-technology-will-disrupt-financial-services-firms/. Accessed 8 Apr 2017

Liebenau JM, Elaluf-Calderwood SM, Bonina CM (2014) Modularity and network integration: emergent business models in banking. In: HICSS 2014 proceedings. http://ieeexplore.ieee.org/document/6758750

Lindman J, Tuunainen VK, Rossi M (2017) Opportunities and risks of blockchain technologies: a research agenda. In: HICSS 2017 proceedings. http://aisel.aisnet.org/hicss-50/da/open_digital_services/3. Accessed 3 Dec 2017

Lo S, Wang CW (2014) Bitcoin as money? Current policy perspectives (14-4), Federal Reserve Bank of Boston. www.bostonfed.org/publications/current-policy-perspectives/2014/bitcoin-as-money.aspx. Accessed 3 Dec 2017

Macheel T (2016) Blockchain promises cost cuts, but what about revenue? Retrieved from https://www.americanbanker.com/news/blockchain-promises-cost-cuts-but-what-about-revenue. Accessed 10 May 2017

McKinsey & Company (2018) Banks in the changing world of financial intermediation. https://www.mckinsey.com/industries/financial-services/our-insights/banks-in-the-changing-world-of-financial-intermediation

McLean E, Soden J, Steiner G (1977) Strategic planning for MIS. Wiley, New York

Mehmood JZ, Chaudhry S (2018) The world’s 100 largest banks. S&P Global Market Intelligence. www.spglobal.com/marketintelligence/en/news-insights/research/the-world-s-largest-banks. Accessed 3 Oct 2017

Morkunas VJ, Paschen J, Boon E (2019) How blockchain technologies impact your business model. Bus Horiz

Mougayar W (2016) The business blockchain: promise, practice, and application of the next Internet technology. Wiley, Hoboken

Nakamoto S (2008) Bitcoin: a peer-to-peer electronic cash system. http://bitcoin.org/bitcoin.pdf. Accessed 1 Dec 2017

Outlier Ventures (2017) Tracking startup ecosystem live. Outlierventures.io. https://outlierventures.io/startups/browse/. Accessed 27 June 2017

Palmer JW, Markus MI (2000) The performance impacts of quick response and strategic alignment in specialty retailing. Inf Syst Res 11(3):241–259

Porter ME (1985) Competitive advantage: creating and sustaining superior performance. Free Press, New York

Powell TC, Dent-Micallef A (1997) Information technology as competitive advantage: the role of human, business, and technology resources. Strateg Manag J 18(5):375–405

Rauchs M, Blandin A, Klein K, Pieters G, Recanatini M, Zhang B (2018) 2nd global cryptoasset benchmarking study, University of Cambridge. https://www.jbs.cam.ac.uk/fileadmin/user_upload/research/centres/alternative-finance/downloads/2018-12-ccaf-2nd-global-cryptoasset-benchmarking.pdf

Robeco (2016) Distributed ledger technology for the financial industry. Blockchain administration 3.0, 1st edn, Robeco—The investment engineers, pp 1–25. https://www.robeco.com/media/0/4/b/04bf42beda332cd32ab89a21cec8110a_201605-distributed-ledger-technology-for-the-financial-industry_tcm26-3491.pdf

Senn JA (1992) The myths of strategic system. Inform Sys Manag 9(3):7–12

Siegal P (1975) Strategic planning of management information systems. Mason and Lips Comp. Publishers, New York

Sieger P, Zellweger T, Aquino K (2013) Turning agents into psychological principals: aligning interests of non-owners through psychological ownership. J Manag Stud 50(3):361–388

Tallon PP (2008) A process-oriented perspective on the alignment of information technology and business strategy. J Manag Inf Syst 24(3):231–272

Tallon P (2010) A service science perspective on strategic choice, IT, and performance in U.S. banking. J Manag Inf Syst 26(4):219–252

Tapscott D, Tapscott A (2016a) The impact of the blockchain goes beyond financial services, Harvard Business Review. https://hbr.org/2016/05/the-impact-of-the-blockchain-goes-beyond-financial-services

Tapscott D, Tapscott A (2016b) Blockchain revolution. How the technology behind Bitcoin is changing money, business, and the world. New York Portfolio/Penguin

The Crypto Valley Association (2017) Members—crypto valley. Crypto Valley. https://cryptovalley.swiss/member-directory/. Accessed 30 June 2017

Thompson A (1965) Bureaucracy and innovation. Adm Sci Q 1:1. https://doi.org/10.2307/2391646

Treacy M, Wiersema F (1993) Customer intimacy and other value disciplines. Harvard Business Review. https://hbr.org/1993/01/customer-intimacy-and-other-value-disciplines

Treacy M, Wiersema F (1995) The discipline of market leaders. Basic Books, New York

UCLA (2017a) Principal components analysis | SPSS annotated output. https://stats.idre.ucla.edu/spss/output/principal_components/

UCLA (2017b) SPSS annotated output regression analysis. https://stats.idre.ucla.edu/spss/output/regression-analysis/

Underwood S (2016) Blockchain beyond Bitcoin. Commun ACM 59(11):15–17. https://doi.org/10.1145/2994581

Venkatesh V, Morris M, Davis G, Davis F (2003) User acceptance of information yechnology: toward a unified view. MIS Quarterly 27:425–478

Weill P, Ross JW (2004) IT Governance: how top performers manage IT decision rights for superior results. Harvard Business School Press, Boston

World Economic Forum (2016) The future of financial infrastructure. An ambitious look at how blockchain can reshape financial services, 1st edn, World Economic Forum, pp. 1–130. http://www3.weforum.org/docs/WEF_The_future_of_financial_infrastructure.pdf

Wörner D, von Bomhard T, Schreier Y, Bilgeri D (2016) The Bitcoin ecosystem: disruption beyond financial services? pp 1–16. https://www.alexandria.unisg.ch/248647/1/2201_ECIS_Bitcoin_Ecosystem_Final.pdf

Zahra SA (1991) Predictors and financial outcomes of corporate entrepreneurship: an exploratory study. J Bus Ventur 6(4):259–285

Zyskind G, Nathan O, Pentland A (2015) Decentralizing privacy: using blockchain to protect personal data. In: SPW 2015 proceedings, IEEE Xplore. http://ieeexplore.ieee.org/document/7163223

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendices

Appendix 1: Additional respondent data

1.1 Complete list of respondents’ job titles

Respondent’s job title | Bank | Non-bank | Total |

|---|---|---|---|

CEO (Chief Executive Officer) | 8 | 25 | 33 |

CTO (Chief Technology Officer) | 2 | 2 | 4 |

CIO (Chief Information Officer) | 2 | 2 | 4 |

CFO (Chief Financial Officer) | 0 | 1 | 1 |

CDO (Chief Digitization Officer) | 4 | 0 | 4 |

Other (please specify): | 36 | 22 | 58 |

Assistant | 1 | 1 | |

Associate Director of Innovation | 1 | 1 | |

BA | 2 | 2 | |

Business Development | 1 | 1 | |

Business Development Manager | 1 | 1 | |

Business Manager | 1 | 1 | |

CFO/CRO/COO | 1 | 1 | |

Chief Enabler | 1 | 1 | |

Chief Investment Officer | 1 | 1 | |

Chief Product Officer | 1 | 1 | |

Chief Strategy Officer | 1 | 1 | |

CMO | 1 | 1 | |

COO (Chief Operations Officer) | 2 | 2 | 4 |

Digital Business Developer | 1 | 1 | |

Digital Business Executive | 1 | 1 | |

Director | 1 | 1 | 2 |

Div CTO | 1 | 1 | |

Executive Director | 1 | 1 | |

Global Head Products and Services | 1 | 1 | |

Head Business Development | 1 | 1 | |

Head of Business Development and Support | 1 | 1 | |

Head of digital and Distribution IT | 1 | 1 | |

Head of DLT and Blockchain | 1 | 1 | |

Head of Innovation | 1 | 1 | |

Head of Innovation Center | 1 | 1 | |

Head of Product Switzerland | 1 | 1 | |

Head of project management | 1 | 1 | |

Head of Transaction Banking | 1 | 1 | |

Head of Venture Capital | 1 | 1 | |

Head Project Management | 1 | 1 | |

Innovation | 1 | 1 | |

Innovation/Digital | 1 | 1 | |

Innovation Manager | 1 | 1 | |

Investment Advisor | 1 | 1 | |

kaufm. angestellter | 1 | 1 | |

Manager | 1 | 1 | |

Managing Director | 1 | 1 | |

Marketing Manager | 1 | 1 | |

MD, Head Trading IT | 1 | 1 | |

Member of the board | 1 | 1 | |

Member of the executive board | 1 | 1 | |

Member of the Executive Board, Head Corporate Finance | 1 | 1 | |

Operations Director | 1 | 1 | |

Owner | 1 | 1 | |

Principal | 1 | 1 | |

Private banker | 1 | 1 | |

Project Manager | 1 | 1 | |

Research Manager | 1 | 1 | |

Risk officer | 1 | 1 | |

Salesmanagement Private Banks | 1 | 1 | |

Senior Project Manager | 1 | 1 | |

VP for Corporate Alliances | 1 | 1 | |

Wealth manager | 1 | 1 |

1.2 Examples of respondent profiles

-