Abstract

The rapid increase of the shale gas production in the USA has influenced significantly the global energy market. Primarily, this is connected with a sharp decrease of natural gas import by the USA. Moreover, the scenarios of the US shale gas supply to the European market that turned out to be under strong impact of the “shale revolution” have been discussed actively. Other world countries possessing shale gas reserves are also planning to increase its production. Although the first results of export of the “shale revolution” have shown that quite unlikely the US experience of this area will be repeated in the next decade, but, still, with regard to the volumes of the shale gas production the global energy market is already altering notably.

Access provided by CONRICYT-eBooks. Download chapter PDF

Similar content being viewed by others

Keywords

1 Introduction

The rapid growth of the shale gas production in the USA has brought this hydrocarbon into the focus of attention practically in all world countries. The publication of data on availability of some fantastic reserves led to appearance of a wealth of projections about future scenarios of development of the global energy market as well as particular regional markets. Moreover, the first results of the “shale revolution” provoked a new round of geopolitical rivalry for the European gas market.

With good reason, the US efforts to move the “shale revolution” to Europe may be considered as a geopolitical project targeted to attain the long-time objectives. In July 2011, the James A. Baker III Institute for Public Policy at the Rice University published the report entitled “Shale Gas and U.S. National Security” where the shale gas was considered as an important instrument for extending the US geopolitical influence. The authors of this report marked that the growing supply of shale gas had already involved its geopolitical consequences being the key factor in weakening the possibilities of Russia to use its “energy weapon” against its European users by increasing the alternative deliveries to Europe of liquefied gas ousted from the US market [1].

In different world regions, the development of shale gas plays causes rivalry among countries. This factor affects the promotion of some pipeline projects that turn into the instrument in the struggle for gas markets.

2 The European Policy Got into the Shale Flow

The plans to develop shale gas plays in Europe stirred new discussions about the fate of future pipeline projects. In particular, the European countries stressed high dependence on the Russian pipeline gas imports. This factor influences the development of foreign policy by some European countries. It is also used in negotiations with Russia on supplied gas price. However, different approaches of the EU countries to reduction of dependence on the Russian gas mostly suppose cutting of the volumes of the Russian gas imports. Such stand of European countries is formed, to a great extent, under the USA influence.

The USA persist in promoting the idea of diversification of the Europe energy sources by extending the shale gas supply to the European market. In this, the USA is facilitated by considerable dependence of some European countries in their foreign policy. It is not accidental that in the recent decade the EU has been discussing whether it is feasible to implement the costly projects on construction of pipelines from the Caspian region and Central Asia or may it’s better to wait some time for implementation of the shale gas projects [2].

Receiving news from the USA about increase of the shale gas production, the EU becomes more doubtful whether the pipeline projects are needed. The most well-known project that the EU has tried to accomplish since 2002 is the gas line Nabucco. This project has been discussed for about 10 years; it should be an additional solution for diversification of the EU gas supply, in particular, from Central Asia and Iraq. In July 2009, the intergovernmental agreement for this project was signed by Turkey, Romania, Bulgaria, Hungary, and Austria. It was aimed both to reduce dependence of Europe on the Russian gas and to creation of new transit routes for the Caspian resources, thus, consolidating the political ties of the Caspian countries with the EU. According to the official statements, this project was not accomplished due to its high cost and lack of free gas resources. At the same time, the “shale factor” also affected the promotion of this EU project [3]. Moreover, with the extension of the shale gas production the likely scenarios of its alternative supply to Europe were developed; consequently, it became more unclear whether the Nabucco project would take geopolitical or commercial dimensions in the future [4].

3 Potential Participants of the “Shale Revolution”

In the recent decade, the main attention was focused on the USA that increased the shale gas production and had already influenced the global gas market. The EU is in the focus of the US policy as it is considered one of the potential regions for export of shale gas from the USA.

Apart from the European countries possessing considerable shale gas reserves, the USA pays much attention to other regions and countries (Fig. 1). Thus, significant shale gas plays were found in such Canadian provinces as British Columbia, Alberta, and Quebec and the largest of them are Horn River and Monti [5]. In general, the proved shale gas reserves in Canada are assessed at 11 tcm. The most perspective of them is the Utica Shale play (Quebec) containing 113 bcm of shale gas [6].

Potential shale gas reserves in the world (http://cdn.energytribune.com/wp-content/uploads/MAP2.jpg)

{kind=link}

In Australia, the shale plays are found in the Cooper, Canning, Maryborough, and Perth basins. The total shale gas reserves are estimated at 11.2 tcm. In 2011, the first shale gas was extracted in the Cooper play. However, the main constraints for the growth of shale gas production are transportation problems and high labor cost.

Certain shale gas reserves are found in Britain. In June 2013, the governmental report was published where it was asserted that around 3.7 bcm of shale gas was found in the north of the country.

The Mexican government develops plans on the shale gas production. By developing the Eagle Ford shales, Mexico is expecting to extract up to 14 bcm of shale gas by 2026. If the La Casita shale play will be also developed, then the projections should rise to 34 bcm of shale gas [7]. According to unconfirmed data, considerable shale gas reserves may be found in India.

Substantial shale gas reserves are contained in Ukraine, although there are no accurate assessments. The shale formations found in Ukraine take their origin in Poland, pass across four western regions of Ukraine – Lvovsky, Ivanovo-Frankovsky, Zakarpatsky, and Chernovitsky – and reach its central part in the Donetsk – Pre-Dnieper Depression. Ukraine focuses its attention on the shale gas plays Yuzovsky (Donetsk and Kharkov regions) with the reserves of 4 tcm and Odessky (Lvov and Ivanovo-Frankovsky regions) with the reserves estimated at 2.98 tcm.

Therefore, many countries possessing potentially significant shale gas reserves make attempts to develop them. In all likelihood, this will require some decades when the forecasts of reserves are verified, less hazardous production technologies are developed, and the industrial base required for development of shale plays is created. In addition, the countries should make not a simple choice between production of hydrocarbons and water resources whose deficit gives rise to internal and interstate conflicts [8].

The political consequences of the shale boom will not be reduced to the changed alignment of forces in the global gas market. Many countries have to make adjustments in their energy diplomacy in view of the fact that more and more gas will be offered at prices which with time on can compete successfully with traditional natural gas. In the recent decade, such tendency has been gaining strength, but so far it has created potential threat to traditional gas exporting countries, such as Russia, Iran, and Near East countries. At the same time, the importing countries in Europe and Asia are free to choose gas producers.

The progress in shale gas production will change the energy policy of China. The need to import oil and gas will force China to extend cooperation with the countries taking special place in the global politics. In particular, availability of enormous gas resources in Iran may push China to widening the political and economic contacts with this country in order to ensure the energy security of China.

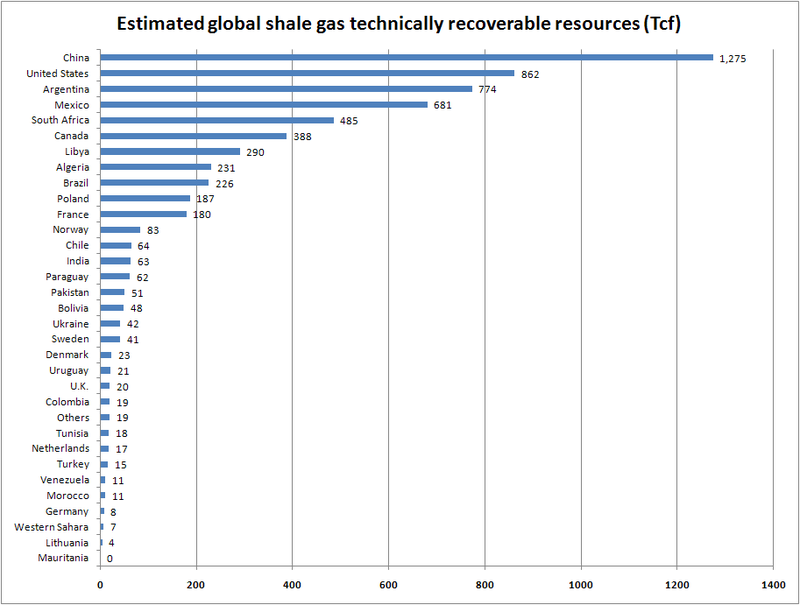

At the same time, if China managed to organize its own shale gas production, then it may reduce the gas import. The first results of shale play development have shown that China cannot repeat the US “shale revolution.” However, the stage-by-stage development of this hydrocarbon will help China to decrease the gas import (Fig. 2).

Shale gas technically recoverable resources by countries (http://3.bp.blogspot.com/-vBaFLDhKINA/TZ0bdlzQZZI/AAAAAAAAHG4/JRTIpiIv5-Y/s1600/worldnatgas.png)

{kind=link}

4 Russia Under the Shale Gas Pressure

So far, we are witnessing the virtual rivalry between Russian pipeline gas supply to Europe and export of US shale gas progressing in view of depletion of traditional gas sources. Prior to the “shale revolution,” it was expected that gas production in the USA, Canada, and in the North Sea would drop significantly which might lead either to the growing share of Russian gas in the European market or gas produced in other regions. In any case, it meant greater dependence of European users on export.

The shale gas has changed the course of events giving rise to rivalry among energy companies engaged in shale gas production and countries exporting pipeline gas. So far, this rivalry concerns largely the technologies as one of the key factors that may make shale gas more attractive is its relative low cost. It is meant here the improved fracking technology using longer than before horizontal wells and injection of the greater volume of water for fracturing. Owing to this already in 2015, the US companies expected to lower the production costs [9]. This fact may also explain the campaign unrolled in 2015 on promotion of shale gas and appearance of new forecasts stating that in one or two decades the shale gas production in the USA should demonstrate the three to fourfold rise. The USA is expecting to attain such goal by improving the shale gas production technologies.

In this context, the growth of the shale gas production in the USA may have certain consequences for the geopolitical and economic interests of Russia. And very important here will be the decision of the USA on development of export of liquefied natural gas (LNG). The growing supply to international gas markets will create additional pressure on Russian gas supply to Europe and Asia. It should be also remembered that in the long-time perspective the cost of Russian gas will grow as Russia will have to develop new fields located in complicated climatic conditions of the North, including in offshore areas [10].

In the USA, the consequences of the shale gas production are already visible – the terminals for LNG import are idling and the likelihood of the USA growing dependence on import becomes less and less. Moreover, the growing production of shale gas in the USA means that LNG from Qatar will be directed to the European market.

The persistent effort of the USA to thrust the “shale revolution” on other countries positioning it as allegedly universal means for attaining energy independence is a poorly disguised endeavor to cut by any means the oil and gas revenues of Russia. This will inhibit the strategic perspective of dynamic development of technological upgrading of economics and military–industrial complex of Russia – the process capable to return Russia its lost status of superpower.

5 US Energy Policy

Promoting the “shale revolution” in Europe, the USA continues to do everything possible and impossible to maintain its influence in the traditional oil and gas regions in Near East, Middle East as well as in Central Asia and in the Caspian region.

This policy got additional impulse after breakdown of the USSR when the new geopolitical processes started gaining strength. The close attention of the USA to Central Asia and Caspian region was dictated by the enormous hydrocarbon potential there. This factor determined the US approaches to pursuance of its multi-aspect and multi-faceted polity in the Caspian region, thus, shaping a new model of international relations after the end of the cold war period [11].

Hydrocarbon resources, pipeline projects, and shale gas production became the important factors of the US energy policy. The energy aspect is the key issue in the system of US foreign policy actions [12].

The fall of the oil prices observed in 2014–2015 can make adjustments in the shale gas production in the USA proper. And the more so as in such situation the shale play development becomes less attractive. Persistence of low oil prices will lead to an abrupt reduction of drilling in the USA and production decrease. The safety margins of US companies engaged in shale play development are rather limited and the considerable debts and profit reduction should be added here.

The USA was always an active player in the world gas trade. The US “shale revolution” permitted the country to change orientation from import of Canadian pipeline gas and LNG from Near East to gas export [13]. However, in North America the “shale revolution” is only unwinding, while in other world countries it has not been commenced as yet. There are different reasons obstructing the shales development: inability to use technologies, technical difficulties, underdeveloped infrastructure, and inadequate legislative base. Accordingly, no one can say when this “shale revolution” will occur in other countries and whether this is possible at all [14].

So far, the USA has not succeeded to export its “shale revolution.” Many countries are not ready to spend much money and to face environmental risks [15]. Thus, the “shale revolution” in China, unlike the USA, did not happen owing to more complicated geological structure of local shales, and water and energy shortage required for shales development. The European shale boom was stopped not in the least by ecologists [16]. Consequently, according to forecasts, by 2025 Europe will produce the insignificant volume of shale gas as its reserves and conditions of extraction differ radically from the US plays [5]. In general, according to projections of the International Energy Agency, the shale gas production by 2030 will not exceed 7% of the total world production.

Nevertheless, it should be noted that the shale gas production in the USA influenced perceptibly the US economy. Thus, the shale gas has changed completely the US petrochemical industry. It is widely used not only in production of polymers, but of mineral fertilizers, too [17].

6 Conclusions

Considerable growth in the recent decade of the shale hydrocarbon production (oil and gas) gave a powerful impulse to alterations in the global gas market. Simultaneously, the interest to development of new technologies called to reduce the costs of shale gas and oil production has also increased.

The factor of “shale revolution” influenced greatly the energy policy of many countries exporting and importing oil and gas. Europe, Russia, and China have to respond to the quickly changing situation in the global hydrocarbon market.

The so-called shale revolution dealt a serious blow upon the system of oil and gas supply established in the recent five decades, and enhanced uncertainty in the supplier–consumer relationships. With all diversity of forecasts, it can be said with assurance that the formation of the shale segment continues its pressure on the world gas market that has really acquired the global dimensions.

The shale gas will affect most strongly the regional markets. The main attractiveness of shale gas is its closeness to the final user which cuts significantly the transportation costs.

The effect of shale gas on particular regional markets will differ greatly owing to the unique features of each market. All this may lead to significant geopolitical changes which will affect, in their turn, the world politics. At the same time, it is too early to speak about the decreased role of hydrocarbon supply via pipelines. Availability of considerable oil and gas reserves, developed infrastructure, and availability of efficient technologies remain the important factors that will keep pipeline projects feasible.

Shale hydrocarbon production is closely intertwined with food security and water resources. All three issues are closely interconnected and their solution requires an integrated approach and long-term planning by many world states [18].

Shale gas production alters the foreign policy of many countries provoking the new lines of competition and changing radically the alignment of forces in the world and regional energy markets. The extraction technology of shale gas whose reserves may be found in many world countries, including those that were earlier referred to gas producers, may result in cardinal change of the situation. And the more so as many countries, primarily, the main producers and consumers of hydrocarbons are involved in the shale gas production, directly or indirectly.

References

Zhiltsov SS (2013) Shale flash mob: technologies, ecology, politics. Vostochnaya kniga, p 176

Barysch K (2010) Shale gas and energy security of the European Union. Oil and Gas Vertical 18:26–29

Zhiltsov SS, Zonn IS (2011) The Caspian pipeline geopolitics “The East – the West”. M. “Intellekt”, 320 p (in Russian)

George JJ (2011) Coal, shale oil and costly mirage of the energy independence of Ukraine. Modern Tokyo Times (Japan), 7 Aug 2011

Magomet RD (2014) Shale gas production. In: Proceedings of the Mining Institute, Saint-Petersburg, vol 207, p 125–130

Tkachenko IY, Brilliantov ND (2012) Shale gas: the analysis of production development and prospects. Russ Foreign Economic bulletin 11:43

Tolstonogov AA (2014) Assessment of development of the shale gas production and processing. Samara State Technical University, Samara, p 35–46

Zonn IS, Zhiltsov SS (2008) Struggle for Water. Index of Security 14(3):49–62

Bashkatova AM (2015) New drop of oil prices may become critical for Russia. Nezavisimaya gazeta, 3 Sept 2015, p 4

Garanina OL (2013) Perspectives of shale gas production in EU and risks for Russia. Problems National strategy 2:123–140

Pisarev VD (1999) U.S. policy in the Caspian region. In: Europe and Russia: problems of southern direction. Mediterranean – Black Sea – Caspian, M. “Interdialect+”, p 376

Zhiznin SZ (2000) U.S. energy diplomacy. USA and Canada, No. 2, p 72–94

Karpova NS, Lavrov SN, Simonov AG (2014) International gas projects of Russia: European alliance and strategic alternatives. TEIS, p 94

Chater J (2014) Shale oil and gas transform America, but the rest world is not in a hurry. AC, No. 1, p 24–28

Orekhin P (2015) Great play in shales. Round World 2:95–98

Martynova A (2015) Obscure future/oil and gas. Izvestia, p 14–15

Peter Cox Technology (2014) Technologies – a major factor of the competition. Oil of Russia 1–2:45–49

Kutuzova M (2013) Global energy scenarios. Vlast, 16 Sept 2013, p 55–57

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2016 Springer International Publishing Switzerland

About this chapter

Cite this chapter

Zhiltsov, S.S., Semenov, A.V. (2016). The Role of Shale Gas in the Global Energy. In: Zhiltsov, S. (eds) Shale Gas: Ecology, Politics, Economy. The Handbook of Environmental Chemistry, vol 52. Springer, Cham. https://doi.org/10.1007/698_2016_85

Download citation

DOI: https://doi.org/10.1007/698_2016_85

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-319-50273-1

Online ISBN: 978-3-319-50275-5

eBook Packages: Earth and Environmental ScienceEarth and Environmental Science (R0)