Abstract

The interest to assessing the shale gas resources in the USA has increased at the turn of the twentieth to twenty-first centuries. The success of the US oil and gas companies in commercial scale production spurred the efforts on verification of the data about the available shale gas resources. The shale gas production has created a surge in development of production base and evolvement of new technologies, making the USA the leader in the gas industry. With considerable shale gas reserves, the USA may claim to secure the leading positions and to influence significantly the formation of the world gas market.

Access provided by CONRICYT-eBooks. Download chapter PDF

Similar content being viewed by others

Keywords

1 Introduction

The USA possesses considerable shale gas resources, the interest to which has grown since the 1970s. However, regardless of a rather long history of shale gas production, there are only rough estimates of the shale gas resources [1–3].

The Department of Energy contributed much to surveying the shale gas plays in the USA. In the 1970s–1980s, DOE invested around US$ 100 million into prospecting and development of shale gas plays. The money were used mostly for development of the horizontal drilling technology, improvement of the drilling technique, application of multistage fracking technology and water-based reagents, and development of the techniques to draw up 3D maps on the basis of microseismic data (Fig. 1) [4]. The greater interest to development of technologies and investigation of plays was rewarded later on when the horizontal drilling technologies that had been developed earlier were applied in practical work.

{kind=link}

The governmental policy in taxation also played its role. It granted privileges to the companies engaged in unconventional gas production. The respective act was passed in 1980 which opened way for small oil and gas companies that initiated surveys of plays and search of means to improve shale gas production. As a result of persistent efforts, in 1999 the Barnett play, Texas, that for 18 years had been the testing ground for production technique perfection yielded the first commercial shale gas flow. Therefore, nearly two decades were required to develop the effective technology of horizontal drilling with hydraulic fracking.

2 Preparation for the “Shale Revolution”

The “shale revolution” was preceded by substantial and long efforts to study shale plays and to conduct exploratory drilling that should have provide data on the shale gas reserves available in the country. Moreover, the gas recovery from unconventional sources, such as shales, was closely connected with the US energy policy. For several decades the USA developed its policy with regard to its long-time interests and the available technologies. Thus, in 1975 the interdepartmental committee for raw materials was established in the USA that focused on formation of a reliable chain “exploration – production – processing – consumption – use of raw material wastes.” That time the USA also announced six national programs, one of which envisaged development of its own resource base. One of such resources was shale gas [5].

The first results of shale play development permitted to expect growth of the shale gas production, although initially the shale gas production was much lower than production of traditional gas. Thus, gas concentration in shale plays of the USA ranged from 0.2 to 3.25 bcm per square kilometer. With the yield rate of 20%, the recoverable gas reserves were assessed at 0.04–0.6 bcm per square kilometer, which is 50–100 times less than for the traditional gas fields. In addition, the commercial development of the shale gas plays required extensive geological surveys and drilling of dozen thousand wells during 7–10 years. Nevertheless, the oil and gas companies engaged in shale gas development continued their business.

Experience of the USA in shale development has shown that each shale formation requires individual approach, possesses unique geological conditions and operational peculiarities, and faces different problems that may arise in the course of production.

3 Shale Gas Reserves

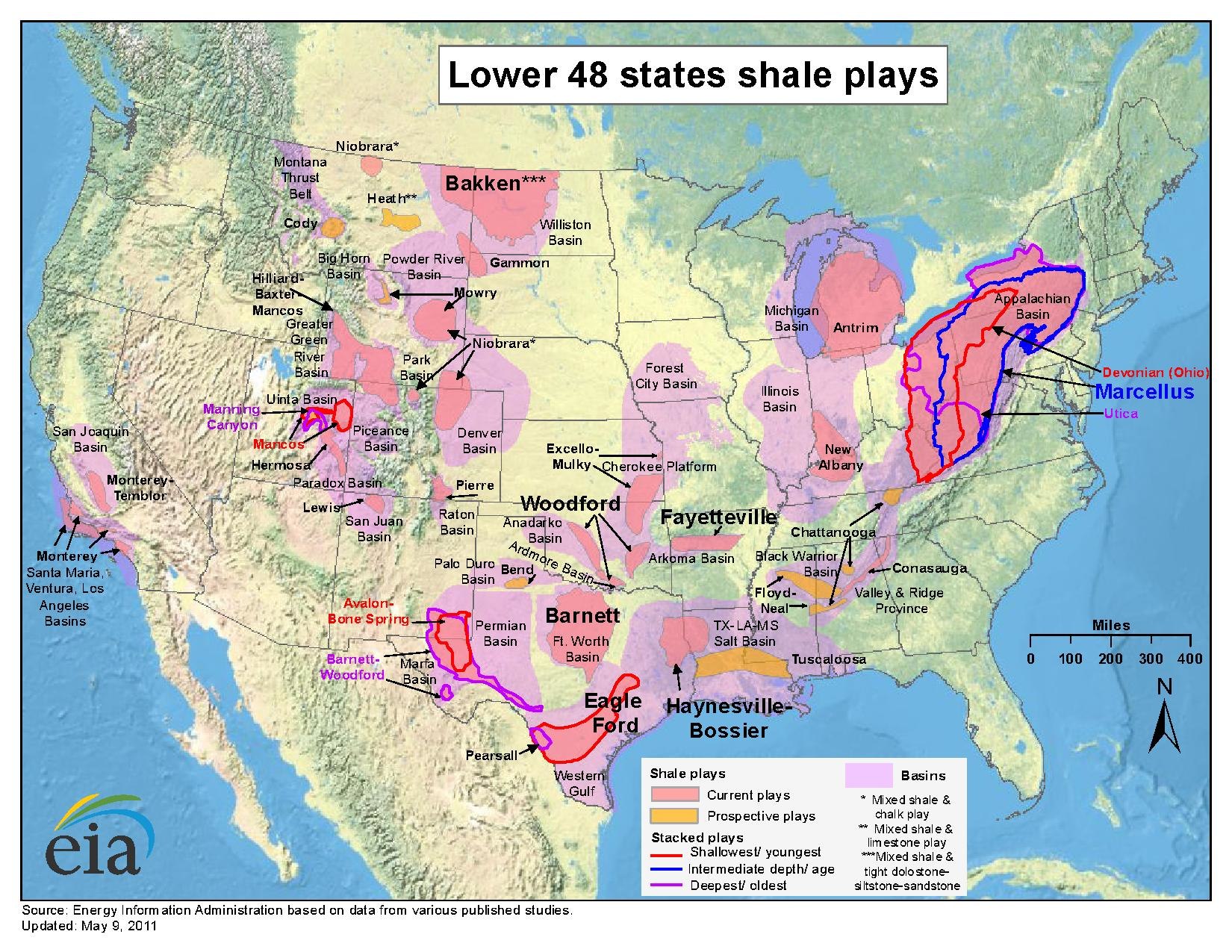

In the 1970s during the energy crisis and aggravation of the energy security issues, the US government seeking the likely way out recollected once again about the shales. As a result of prospecting works, there were four major shale formations found – Barnett (Texas), Haynesville (northwest of Louisiana and Eastern Texas), Fayetteville (Arkansas), and Marcellus (Pennsylvania, West Virginia, New York, and Maryland) as well as others covering dozens of thousand square kilometers and containing enormous shale gas reserves (Fig. 2). The main shale plays are described in the Table 1.

Major shale gas formation in the USA (http://www.ehelpfultips.com/shale%20gas%20map%20of%20the%20united%20states.gif)

{kind=link}

As the parent land of the shale gas production is the USA, the attention of everybody was focused, quite naturally, on the reserves of this hydrocarbon in the USA. In 2008 according to the assessments of the Energy Information Administration (EIA) of the US Department of Energy, the proved reserves of shale gas in the country made 866.6 bcm.

According to the report of the International Energy Agency (IEA) presented in 2009, after improvement of the applied technologies, the recoverable shale gas reserves in the USA have shown the 51% growth. As a result, EIA assessed the proved gas reserves in the USA at 58.7 tcm. However, in December 2010 EIA after respective adjustments decreased, the proved shale gas reserves in the country and, as of the late 2009, they made only 1.63 tcm.

The US Potential Gas Committee consisting of specialists in shale gas production announced about fundamental reassessment of the natural gas reserves in the USA, having increased them from 36.8 to 52.0 tcm, out of which nearly a third of the projected reserves accounted for shale gas (12–17 tcm). In 2009 this committee issued a new comprehensive report about the amount of gas trapped in the shales where the shale gas reserves were evaluated at 51.9 tcm. The US Department of Energy in its report projected the increase of the shale gas production to 113 bcm in the nearest future.

Regardless of the uncertainties concerning reserve estimates, many international organizations in the USA persisted that the USA possessed from 17 to 108 tcm of shale gas. The proved shale gas reserves make 24 tcm, out of which 3.6 tcm are technically recoverable, while the consumption of natural gas in the USA is equal to around 650 bcm per year.

According to the EIA’s 2011 Annual Energy Outlook, the shale gas reserves made 72 tcm, out of which 24 tcm were technical recoverable reserves. However, later on the forecast for the technically recoverable shale gas reserves was decreased to 13.6 tcm.

In early 2012 the Energy Information Administration (EIA) of the US Department of Energy lowered its assessments of the shale gas reserves to be extracted by 40%. In the same year IEA published new assessments of the shale gas reserves, putting them at 208 tcm. While speaking about the shale gas reserves, the total geological reserves or technically recoverable reserves are often meant. And here no reference is made to the proved shale gas reserves.

The major explored shale hydrocarbon resources are found in the North America: in Texas (Barnett play, Eagle Ford oil play), North Dakota (Bakken oil play), Montana, Michigan, Oklahoma, Alabama, and Arkansas. The resources of the shale gas (recoverable) in the surveyed basins are estimated at 13.5 tcm of gas and 4.5 billion tons of oil.

The recent surveys of the shale gas plays in 48 states of the USA have shown that the technically recoverable reserves are estimated from 7.1 to 24.4 tcm. The wide scatter of figures indicates that regardless of long-time investigations, the reserves are assessed only roughly.

4 Shale Gas Production

The shale gas production got its start in the late 1990s and has increased gradually by the first decade of the twenty-first century. Survey and prospecting works lasted for several years. In 1998 the USA produced 8.3 bcm of shale gas. The development of the Barnett Shale play in the north of Texas went on. The geological reserves were assessed at 590 bcm, while the proved recoverable reserves were at 59 bcm [6]. Company Chesapeake Energy, the operator of this play, had invested around US$ 30–40 billion into its development.

The conducted surveys have shown that the shales occur here at a depth of 450–2,000 m covering an area of 13,000 km2. The layer thickness varies from 12 to 270 m. The methane level in the play amounts to about 0.3%.

In 2002 the US company Devon Energy drilled the first horizontal well in the Barnett play, thus, launching the shale gas production at scale in the USA based on the new technology [7]. In the same year, the shale gas production technology was upgraded to combine vertical and directional drilling. Combining the two processes – vertical and directional drilling – with the multistage fracking became the new achievement in the shale gas production which permitted to lower the cost of production and to increase the attractiveness of shale play development.

The US companies learned gradually how to handle the shale structures and acquired new experience of working in shale plays. In 2003 there were produced 14.7 bcm of shale gas, permitting the US companies engaged in this hydrocarbon production to make projections of future production volumes.

From 2005 the shale gas production in the USA had increased sharply, and the shale gas contributed much to the gas production growth in the USA. Around 70% of the shale gas was extracted in the Barnett play. Already in 2006 the production of shale gas in the Barnett play from 6,080 wells made 20 bcm, and in 2007 the USA produced 34 bcm of shale gas.

In 2008 there was a real breakthrough in the shale gas production in the USA which was facilitated by the following factors: First, on the eve of the world financial crisis, the hydrocarbon prices reached their maximum. The natural gas production in the USA has surged all at once, demonstrating the highest growth rates for the recent quarter of the century. And the shale gas gave the greatest growth. Second, the effect of accrued investments in the shale production sector and reduction of the traditional gas potential came into action. Third, the improvement of production technologies and application of new materials allowed for cost reduction. Therefore, the “shale revolution” in the USA started, in fact, not after appearance of the really important advanced technologies but after the gas cost reached nearly 500 US dollars per thousand cubic meters. So, the production of shale gas became economically beneficial [7].

Owing to the vigorous increase of the shale gas production, called in mass media the “gas revolution,” the USA in 2009 became the world leader in gas production extracting 745.3 bcm, and the unconventional sources (methane from coal formations and shale gas) provided over 40% of this output.

As a result, already in 2010 the shale gas production made 132 bcm. In the 2003–2010 timeframe, more than 190 thousand wells were drilled in the USA, out of which nearly the half were abandoned due to their unsuccessful results. However, the oil and gas companies continued drilling works, and by 2009 there were drilled 1,658 horizontal wells [8] which permitted to increase the shale gas extraction. Moreover, some amendments were made in the subsoil use act that removed constraints for application of the hydraulic fracturing technology with the use of chemical agents without which the companies were unable to cut their costs.

The major US companies, such as Chesapeake, Apache, Devon Energy, and Noble Energy, were the leaders in the shale gas production (Fig. 3). In 2012 Chesapeake extracted 32 bcm. The main asset of this company is the Barnett play as well as Haynesville and Marcellus plays. The company Apache produced 24 bcm followed by Devon Energy and Noble Energy [9].

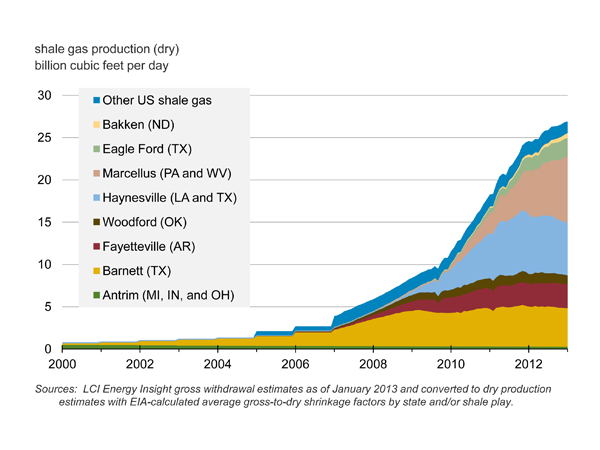

Shale gas production in the USA by geologic formation (https://upload.wikimedia.org/wikipedia/commons/2/27/US_Shale_Gas_Production.jpg)

{kind=link}

The rapid increase of the shale gas production in the US territory was facilitated by numerous factors, such as the enormous economic potential, the immense reserves and vast sparsely populated areas, the availability of well surveyed plays, the permanently improving drilling technologies, the proximity to gas consumption locations, the preferential taxation, the developed gas transportation infrastructure, and the strong endeavor to attain energy security based on its own resources. A powerful stimulus for shale gas production in the USA was preferential taxation that is not found in Europe.

Having sharply increased the shale gas production, the US companies lowered the gas prices, thus, putting themselves in a complicated situation. This led to significant changes in the country-wise distribution of the world gas market and by early 2010 to excessive shale gas supply in the market.

Regardless of these complications, the US companies continued shale gas production. According to the Energy Information Administration (EIA) of the US Department of Energy, the shale gas production in 2010 had grown to 132 bcm. In 2011 the shale gas production was assessed at 150 bcm, or 15% of the cumulative gas output in the world. In 2012 there were produced 260 bcm of shale gas, in 2013 it reached 319 bcm, and in 2014 it reached 350 bcm [10]. As a result, the USA was the only country in the world that started gas extraction from shales at industrial scales. In 2012 the shale gas provided around 30% of the total gas output in the USA.

There are fundamental reasons why the “shale revolution” in the USA became possible. Comparing the dynamics of gas production in the USA with the adopted solutions for stimulation of the unconventional gas production, it becomes clear that the achievements in the shale gas production are rooted in the decisions taken by the US authorities in the 1970s–1980s. And the key factor here is the tax legislation – the oil and gas companies engaged in shale gas production were granted the tax credit. In fact, this allowed for considerable reduction of the production costs and, accordingly, attraction of additional investments into development of shale gas plays.

The shale gas production spurred the development of the gas transport infrastructure. In 2008 the pipeline system designed to supply shale gas from the Fort Worth basin to the gas pipelines on the Mexican Gulf coast of the USA accounted for 11% of all new gas transportation capacities. In 2009 the capacity of gas pipelines connected with the shale gas plays continued its growth. The projects were implemented that ensured better conditions for shale gas delivery. In 2013–2015 the growing shale gas production encouraged further development of adjacent productions involved in development shale gas plays.

5 Forecast of the Shale Gas Production

The USA is persistent in its endeavor to keep its leadership in the shale gas production in the next decade. In the 2011 Annual Energy Outlook the shale gas, for the first time since its production has been launched, was given great credibility. The first projections based on the growth rates of the shale gas production that were made – in two decades its production in the USA shall double and reach 473 bcm and by 2035 – 45% of all gas produced in the USA will be extracted from shale plays [11].

According to the Ernst & Young forecasts, by 2035 the shale gas production in the USA will reach the level of 342 bcm or demonstrate a nearly fourfold increase compared to 2009 [12]. Here EIA assumed that by 2030 the shale gas would take only 7% of the global gas market. As a result, EIA believes that the escalation of the shale gas production in the next 25 years could only offset the reduction of its inflow from other sources.

6 Shale Gas Attracted Big Business

In the USA the gas trapped in the shale formations was extracted mostly by small independent companies – classical venture companies implementing risky innovative projects. However, having developed and applied in practice the advanced technologies of directional drilling and hydraulic fracturing (fracking), these companies succeeded to increase sharply the shale gas production at a relatively low, as was asserted by the representatives of these companies, cost, and big business rushed into this sector. The large oil and gas corporations that earlier preferred to observe the actions of Chesapeake Energy and its colleagues as bystanders started moving to this business.

In 2009 British BP invested 1.3 billion US dollars for 50% interest in the joint venture that intended to extract the shale gas in the Haynesville play. Italian Eni also invested into the US companies engaged in the shale gas production. In the same year ExxonMobil, the world’s largest oil and gas corporation, purchased the US company XTO Energy possessing technologies and professionals for 41 billion US dollars, including covering of debts for 10 billion US dollars, which was the second largest producer of shale gas in the USA which reserves were estimated at over 1.5 tcm.

In 2010 the French Total established the joint venture for developing the Barnett Shale play with the leader in this business – company Chesapeake Energy. They extended their services keeping in mind that in the future the backup and maintenance services may guarantee profits for them for many years ahead. The French company paid around 2.25 billion US dollars for 25% interest. Earlier other oil and gas giants, such as British Petroleum and Nordic Statoil Hydro, entered into the partnership agreements with Chesapeake. Norway invested 3.4 billion US dollars. In February 2010 the Japanese company Mitsui Bussan invested 5.4 billion US dollars into development of the Marcellus Shale play in Pennsylvania. This project is evaluated at 25 billion US dollars. Summing up the above, only in the first half of 2010 the largest world fuel companies spent 21 billion US dollars for purchase of the assets in the shale gas production field [13]. Over 2005–2010 period, the transactions related to merger and takeover of companies involved in the shale gas production projects earned 100 billion US dollars [14].

In mid-2011 the largest mining company BHP Billiton (Britain and Australia) announced about purchase of the US corporation Petrohawk Energy for 12.1 billion US dollars. These assets were purchased to get access to the shale gas reserves in Texas and Louisiana. Earlier, in February 2011, BHP purchased the interest in the shale gas play in Arkansas of Chesapeake Energy for 4.75 billion US dollars.

The interest of large oil and gas companies to the shale gas production was enhanced by the data on this hydrocarbon production. In 2014–2015 the USA was the leader in shale gas production that as before remained one of the main factors influencing the global gas market.

7 Shale Gas Cost

One of the key issues faced by all oil and gas companies engaged in the shale gas production is the cost of shale gas. The US companies promoting widely their success in the shale gas production focused on the low cost of this gas. The US second largest producer of natural gas specializing in shale gas extraction – company Chesapeake Energy – made public the shale gas production costs making, on the average, US$ 99 per 1,000 cu. m. Such declarations promised the real “shale revolution” in the gas market. Such costs allowed for making projections of the shale gas export to the foreign markets. Adding here the costs of gas liquefaction and transportation to Europe, the total gas price reached US$ 200 per 1,000 cu. m which was economically efficient [15].

Meanwhile, the experience of the shale gas production shows that the situation in this business is not so cloudless. Moreover, the costs of the shale gas production call many questions, which is the reason to doubt the reliability of the supplied data.

The assessments of the shale gas plays should take into account the fact that the amount of accessible gas in the shales is directly proportionate to the shales thickness. The most economically effective are considered the “fragile” shales with a high level of silicon dioxide. These plays contain natural bends and fractures. This very fact explains why the Barnett play is highly productive. In fragile shales the less intensive fracking is possible.

At the same time, the low gas concentration in rocks explains the quick decline of drilled wells. As a result, the optimistic forecasts underestimate the shale field decline rates. The shale gas is extracted in great quantities only in the first year of drilling, while later on the production declines and is maintained at a lower level. To keep the gas production at a stable level, the companies should permanently drill new wells. In the largest shale gas play Barnett in Texas, the well decline rate by the second year of production made 37%, on the average, and by the third year 50% compared to the first year. This means that the efficiency of shale gas production requires permanent drilling of new wells and maintaining the operating parameters of the drilled wells. As a result, the real cost of the shale gas production with regard to all expenses on land site lease, drilling of a great number of wells which yield declined sharply already in a year, and creation of the respective infrastructure is evaluated at 242–282.5 US dollars per 1,000 cu. m. So, the data on the shale gas production costs for companies vary within a wide range – from 130 to 400 US dollars per 1,000 cu. m.

8 Conclusions

In the 2013–2015 timeframe, the shale gas production rates in the USA remained high. Moreover, the quicker than it was assumed, earlier growth of the shale gas production in the USA led to spot price collapse on the American continent and in Europe. The gas underdelivered to the USA due to the domestic consumption growth was redirected to Europe that affected the deliveries of the Russian company “Gazprom” which prices exceeded significantly the market quotations.

The shale gas and oil production in industrial scales is conducted only in four world countries: the USA, Canada, China, and Argentina. But in the last three countries, the volumes of production are meager. Thus, the USA is the only country producing significant amounts of unconventional hydrocarbons. According to British Petroleum estimates, by 2030 the USA will produce 63% of gas from shale and coal formations, and by forecasts of the International Energy Agency by 2035, this figure should grow to 71%.

The increase of the shale gas production will permit the USA to minimize the import of natural gas and to purchase it only from Canada. The terminals for the imported liquefied gas available in the USA may be used to cover the current needs during seasonal maximums, while the accomplishment of the US strategy to supply shale gas to the European market could become an additional stimulus for extension of this hydrocarbon production.

References

Soeder DJ (2012) Shale gas development in the United States. In: Al-Megren H (ed) Advantages in natural gas technology. InTech, Rijeka, p 542

Modern Shale Gas. Development in the United States. 2009

The Economic and Employment Contributions of the Shale Gas in the United States. Prepared for America’s Natural Gas Alliance. 2011

Matishov GG, Paroda SG (2015) Shale gas production by the hydraulic fracturing technology: present state, risks and threats. Geol Geophys S Russ 1:42 (in Russian)

Karpova NS, Lavrov SN, Simonov AG (2014) International gas projects of Russia: European alliance and strategic alternatives. TEIS, Moscow, pp 87–88 (in Russian)

Orekhin P (2015) Great play with shales. Round World 2:95–98 (in Russian)

Motyashov VP (2011) The gas and geopolitics: the chance for Russia. Book and Business, Moscow, 350 p (in Russian)

Khaitun AD (2011) The shale revolution has not yet come. NG-Energia. January 11 (in Russian)

Karpova NS, Lavrov SN, Simonov AG (2014) International gas projects of Russia: European alliance and strategic alternatives. TEIS, Moscow, p 98 (in Russian)

Atepaeva E (2015) EIA: the shale gas and oil production 2014. Oil Gas Vert 2:14 (in Russian)

Khegai AM (2011) The effect of the shale gas development on the U.S. gas industry. USA and Canada 7:63–76 (in Russian)

Ernst & Young (CIS) Report “Shale Gas in Europe: Revolution or Evolution?” 2014. p 1

Vedomosti. 2010. October 06 (in Russian)

USA and Canada. 2011. No. 7. pp 63–76 (in Russian)

Kulikov S (2011) The Europeans inflate new bubbles. Nezavisimaya gazeta. October 13. C. 4 (in Russian)

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2016 Springer International Publishing Switzerland

About this chapter

Cite this chapter

Zhiltsov, S.S., Zonn, I.S. (2016). Shale Gas Production in the USA. In: Zhiltsov, S. (eds) Shale Gas: Ecology, Politics, Economy. The Handbook of Environmental Chemistry, vol 52. Springer, Cham. https://doi.org/10.1007/698_2016_51

Download citation

DOI: https://doi.org/10.1007/698_2016_51

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-319-50273-1

Online ISBN: 978-3-319-50275-5

eBook Packages: Earth and Environmental ScienceEarth and Environmental Science (R0)