Abstract

Real prices for metals seem to have developed at a constant price level over a long period of time, up to 100 years. Based on real prices for 28 metals, using the US Producer Price Index as a deflator, we have defined long-term and short-term low-price benchmarks. The results show that real prices which developed in cycles or reacted to shocks normally returned to a certain floor price, defined as the long-term low-price benchmark in this study. Using long-term low-price benchmarks as a price signal is a useful tool for investors and buyers to act anticyclically between cycles or shocks, either to secure long-term offtake agreements or to farm into new mining assets at a low price. A combined analysis with average real total cash cost data for 11 mineral raw materials supports the low-price benchmark approach and leads to a discussion whether the lessons of the past hold true for the future. We propose that these learning effects still take place and, in consequence, the long-term real price benchmarks may be extrapolated into the next decade. However, it is possible that the cost pressure to retain or obtain the social licence to operate increases to such a degree that technical rationalization cannot keep up with the cost increases. Consequently, the operating costs at mines and the ratio of the established long-term low-price benchmark to the total cash costs are important aspects to monitor.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

It is common knowledge that metal prices fluctuate. The capacities of producers and the demand of consumers are rarely in equilibrium. Therefore, the metal markets mostly fluctuate between buyer’s and seller’s markets. Prices for metals either move cyclically due to changes in global economic growth (Tilton 2003; Roberts 2009; Humphreys 2010; Bräuninger et al. 2013; Wellmer et al. 2018) or are a result of unexpected changes in market fundamentals caused by supply or demand shocks (Kilian 2009; Stürmer 2018).

Companies usually have a hard time to figure out when the peak or trough in prices is reached and when is a good time to invest in commodity assets or to procure metals. We have, therefore, established low-price benchmarks for 28 metals based on up to 100 years of monthly real price data. The established price benchmarks help companies to invest or procure in an anticyclical way mainly to achieve floor prices and to avoid price peaks.

For investors in the mining business, it is of great interest to identify such floor prices. Experience shows that in low-price phases (termed a “buyer’s market”), the prices for advanced projects tend to be cheap, whereas high-price phases are often associated with exorbitant premiums (termed a “seller’s market”) (Fig. 1). Identifying long-term low-price benchmarks over several hog cycles, describing the normal interaction between supply and demand and prices of raw materials, helps to determine the best time for farming into a project or buying metals. However, experience shows that investors often place an investment at the highest points of demand and at high prices because these phases attract the attention of a range of investors. During high-price phases, high premiums have to be paid for exploration projects and exploration rights, especially for metals which are “en vogue” at that time.

Schematic model for anticyclical investments in mining and exploration assets. Premium for promising exploration projects in relation to the phases of a raw material hog cycle (modified from Wellmer et al. 2018, with permission by Stürmer and acatech)

For traders and procurement departments in manufacturing companies, it is also of great interest to identify floor prices. Procurement departments have to secure a steady and secure flow of metals to their factories. They normally buy metals physically, have a short-term view of market developments of less than 1 to 3 years and often have to act in periods of highly volatile prices. Using short-term low-price benchmarks helps buyers to act at the lowest prices within a hog cycle. Buyers normally use offtake agreements, hedging instruments, or the spot market. On account of their short-term view of markets, they have to monitor market developments much more frequently than long-term oriented investors in order to place the right order at the right time.

In general, poor timing of investment or purchase in the metal sector could lead to heavy losses, reduced competitiveness, or even bankruptcy. Thus, understanding price movements over time is fundamental to decision-making. Our study helps long-term investors and buyers, as well as short-term buyers, to act at the right time. However, the study does not provide any guidance on the future outlook for metal prices.

The current literature does not systematically address long-term low-price benchmarks in combination with cash cost data. Rather, it normally covers average price trends over longer time periods, including correlation analysis with a wide range of economic indicators. Many studies have addressed the formation of supercycles (e.g., Jerrett and Cuddington 2008; Erten and Ocampo 2013) and hog cycles in different market environments (e.g., Hanau 1928; Ezekiel 1938; Rosenau-Tornow et al. 2009; Bräuninger et al. 2013) or analyzed price peaks (e.g., in Wellmer et al. 2018). There is also a wealth of literature on the character and lengths of commodity price cycles (e.g., Roberts 2009; Chen 2010; Rossen 2015) as well as on price forecasts (Drachal 2018 and references therein). Additionally, numerous publications cover charting techniques and technical analysis of price movements, e.g., using bar charts that define resistance and support planes, double tops and bottoms testing either market highs or market lows etc. (Government of Alberta 2019).

For our approach, we use long-term historical real prices and real cash cost data to derive possible benchmarks as a tool for acting anticyclically in the metal markets. The strength of this method is its use of data spanning up to 100 years, comparing a large number of metals, and combining the real price data with cash cost data (cf. “Database” section). When using metal price fluctuations as a tool to establish low-price benchmarks, it is essential to understand the dynamics of hog cycles, shock events, and fundamental changes in technological trends. These dynamics are briefly described in our methodological approach (cf. “Searching for low-price benchmarks—the approach” section). Based on this concept, the results show that the established low-price benchmarks could be a useful tool to provide an orientation on how a future floor prices might develop (cf. “Results” section). Finally, an indication about today’s situation in relation to the established benchmark prices is given (cf. “Discussion” section).

Database

From 1918 to 2017—up to 100 years of real price data

We are considering the real prices of metals over a period of up to 100 years. Prior to World War I, prices in real terms had remained on a high level (Tilton et al. 2018; Wellmer et al. 2018). After World War I, there was a significant break in metal price trends. Consequently, our analysis covers the period after the end of World War I. The likely reason that post-war price levels did not recover to pre-war levels was the coincidence with technological advances in the mining industry after World War I. The main technological breakthroughs were bulk-mining open-pit technology with big shovels first introduced in the copper mines of Bingham/USA and Chuquicamata/Chile, the flotation technology (Julihn 1932; Luyken and Bierbrauer 1931; Arrington and Hansen 1963; Lagos personal communication 2018), and other improvements in beneficiation like the Dorr rake classifier (Lynch 2018).

The price and cash cost data

The basic data for our real price time series are monthly nominal price data. The data has been compiled for research purpose over many decades at the Federal Institute for Geosciences and Natural Resources (BGR, German Geological Survey). Historic price data have been taken from magazines, journals, the London Metals Exchange, the World Bank Global Economic Commodities database, and the United States Geological Survey. Some of the earliest time series start around the middle of the nineteenth century. However, for most metals, the time series start around 1910, 1930, 1950, or late in the 1970s (cf. Tables 1, 2, 3, 4, and 5 and Plates 1, 2, 3, 4, and 5). In an attempt to standardize each time series, the data were adjusted to the same unit value (cf. Bräuninger et al. 2013 for further data sources and description of specifications). The unit value US$ was used for all metals. Where applicable, currency conversions were carried out for British Pound Sterling, the Deutsche Mark, and the Euro. The selected unit value for the weight was tonne (metric tonne, “t”), kilogram for V2O5 and Ta2O5, and ounce (troy ounce, “oz”) for precious metals. Weight conversions were carried out for short tonne (907.1847 kg), long tonne ((1016.0469 kg), metric tonne unit (1% unit value, 10 kg), and pound (0.4535 kg). Several breaks in the time series are attributed to the change in data sources and specifications. Breaks in specifications, which occurred at various times, were left as they were documented originally. For the purpose of this paper, the breaks in data sources and specifications are not considered to be critical to the results of this study (for comparison see vertical line in Plates 1, 2, 3, 4, and 5 indicating the data breaks). Normally, these breaks refer to technological changes combined with new manufacturing processes and materials which required technical adjustments of grades for similar applications.

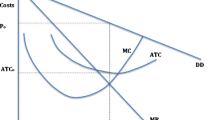

Relation between short-term low-price benchmark (black broken line), long-term low-price benchmark (black line), and average total cash costs for copper (annual, gray line). The long-term low-price benchmark is defined by the average of the lowest real prices indicated by the circles, the short-term low-price benchmark is defined by the average of values defined by the dotted circles. The line or marker for the average total cash costs (gray broken line) normally lies below the line of the long-term low-price benchmark (data sources: monthly real price data, BGR; annual real total cash cost data; calculation based on 2017 US PPI in US$/t; nominal cash costs data used with kind permission by S&P Global Market Intelligence (2018))

Iron, steel, and base metals. Real prices, lower and upper real price benchmarks, and real total cash costs (solid line for real price, solid horizontal line for lower real price benchmark, dashed line for upper real price benchmark, gray line for real total cash costs, real prices and cash costs deflated by using US PPI, basis 2017, vertical dashed line indicates break in price specification)

Ferroalloying metals. Real prices, lower and upper real price benchmarks, and real total cash costs (solid line for real price, solid horizontal line for lower real price benchmark, dashed line for upper real price benchmark, gray line for real total cash costs, real prices and cash costs deflated by using US PPI, basis 2017, vertical dashed line indicates break in price specification)

Minor metals. Real prices, lower and upper real price benchmarks (solid line for real price, solid horizontal line for lower real price benchmark, dashed line for upper real price benchmark, real prices deflated by using US PPI, basis 2017, vertical dashed line indicates break in price specification)

Precious metals. Real prices, lower and upper real price benchmarks, and real total cash costs (solid line for real price, solid horizontal line for lower real price benchmark, dashed line for upper real price benchmark, gray line for real total cash costs, real prices and cash costs deflated by using US PPI, basis 2017, vertical dashed line indicates break in price specification) Light metals. Real prices, lower and upper real price benchmarks (solid line for real price, solid horizontal line for lower real price benchmark, dashed line for upper real price benchmark, real prices deflated by using US PPI, basis 2017, vertical dashed line indicates break in price specification)

Cash cost data over a period of 26 years (1991 to 2017) were available for 11 metals (S&P Global Market Intelligence 2018, used with kind permission).

The choice of the deflator

Frequently, the Consumer Price Index (CPI) of a country is chosen as a deflator to derive real prices (Wellmer et al. 2008). Svedberg and Tilton (2006, p. 511) state: “The major consideration favoring the use of the CPI, however, is the fact that it reflects the real price of copper in terms of a representative basket of consumer goods and services. As a result, it more accurately assesses the impact of commodity price trends on the welfare of society - that is, consumer or people in general - than other deflators.” In addition they state that long-term trends in the real price of primary commodities are inflation biased and need to be inflation-bias-corrected (Svedberg and Tilton 2006; Cuddington 2010; Svedberg and Tilton 2011; Fernandez 2012; Gleich 2014).

For our investigation, however, the authors have chosen to use a Producer Price Index (PPI), specifically the US PPI (base December 2017; applied to nominal prices and cash cost data). The main arguments for applying the US PPI are given below.

We are considering the interest of investors in mining properties as well as of traders and procurement departments. These are mostly producers and manufacturers or their service providers. They are more interested in the real growth of output rather than in changes in the cost of living. The primary use of the PPI is to deflate revenue streams in order to measure the real growth of production costs, whereas the primary use of the CPI is to adjust income and expenditure streams to changes in the cost of living (BLS - Bureau of Labor Statistics 2014). In terms of goods, the PPI tracks change in manufacturing selling prices for consumer food, consumer energy goods, consumer durable goods, and consumer non-durable goods other than food and energy. The PPI includes sales to business as inputs to production, including capital investment, but not the CPI. In contrast to the CPI, the PPI currently does not have a complete coverage of services (only 72%). Nearly 63% of the world currency reserves are held in US$ (Leong 2018) and most of the commodities are traded in US$. For this reason, we have used the US PPI and not other producer price indices.

Searching for low-price benchmarks—the approach

Long-term low-price benchmarks

To establish long-term low-price benchmarks, an understanding of hog cycles is fundamental. The term “hog cycle” was developed by Hanau (1928) for agriculture and later transferred to mineral economics (Wellmer and Hagelüken (2015) and references therein). From the hog cycle, Ezekiel (1938) developed the cobweb theorem, describing the pendulum which swings between alternating phases of excess demand and supply. The hog cycle describes the interaction between supply, demand, and prices of raw materials. It is the oscillation between buyer’s and seller’s market. For the development of cyclicity, the aspect of time lag is important. When the demand increases, prices rise, and a boom period develops, the demand cannot be met immediately. For hogs, this is the time of breeding or even building new pigsties, while in the case of mining, it takes time to enlarge production capacities or to build a new mine.

A good example is the China boom between 2003 and 2012. Investment activities of mining and investment companies were particularly high when project costs reached record levels and high premiums for mining and exploration projects were paid. Within that period, mining share prices tripled relative to the broader market (Connolly and Orsmond 2011). The German Raw Materials Alliance (Rohstoffallianz) in 2012, at the height of the price cycle, is a good example where newcomers to the mining business had great difficulty in making a reasonable investment. Therefore, acting anticyclically is a better strategic option, but a longer-term perspective is required. After the mining boom ended in 2015, the top 40 mining companies had impairments of 53 billion US$ and written-off the equivalent of 32% of capex spent since 2010 (PricewaterhouseCoopers 2016). Many mining companies restructured their business, put projects “on ice,” sold marginal projects, or even disposed high-quality assets.

The prices before and after such hog cycles define a long-term low-price benchmark or floor price, a level to which real prices generally return. Defining long-term low-price benchmarks or floor prices is a simple concept. The long-term low-price benchmark for a metal is defined as the average of local troughs in a long-term real price time series. The local troughs are visually determined (Fig. 2). Each benchmark should continue over 10 to 20 years to cover at least one or two price cycles or shock events. Wherever the lowest real price points deviate 30 to 50% from the defined price plateau, a new long-term low-price benchmark can be established. Each benchmark is calculated by averaging the lowest real price points. Based on monthly real price data, 5 to 10 low points are sufficient to define the long-term low-price benchmark with confidence. Visual control and expert opinion provide sufficient accuracy as the benchmarks are intended to be used only as a guideline.

Light metals. Real prices, lower and upper real price benchmarks (solid line for real price, solid horizontal line for lower real price benchmark, dashed line for upper real price benchmark, real prices deflated by using US PPI, basis 2017, vertical dashed line indicates break in price specification)

Our results show that these low-price benchmarks have remained stable over a long time horizon and over several hog cycles or shock events. An explanation for this is that new ore deposits are continually being discovered and that the real costs of mining and processing a tonne of mineral concentrate or metal have not significantly changed. In addition, there is a long-term effect whereby declining grades or reserve levels are offset by technological improvements in mining or processing, commonly linked to economies of scale (Schwerhoff and Stürmer 2016).

Our results also show that fundamental technological changes in the mining industries may shift the benchmarks in the long-term to lower or higher real prices. This could result from breakthrough technologies leading to lower-cost mining or processing. Legislative changes in particular countries or required by international treaties may lead to substitution and efficiency effects in the manufacturing industry reducing demand and leading to a dramatic fall in the price of certain metals (Wellmer and Hagelüken 2015), thus lowering the price benchmarks. Examples are discussed in the “Results” section. The “Discussion” section includes an analysis of the price situation in March 2019 for all investigated metals in relation to the long-term low-price benchmarks. Possible actions for long-term investors and buyers are suggested.

Short-term low-price benchmarks

To establish short-term low-price benchmarks, it is important to observe price fluctuations within a hog cycle. The mean length of a cycle period lies between 53 and 84 months for a wide variety of commodities (Roberts 2009). This time period matches with the shortest lead time for new mine projects, which is commonly 3 to 7 years (Wellmer and Dalheimer 2012). Within such a cycle, metal prices are often highly volatile. Our observation of past cycles shows that prices often quickly revert to a level which is higher than the long-term low-price benchmark but much lower than the average price of the peak phase. Thus, determining short-term low-price benchmarks might be a useful tool for traders and buyers who need to act carefully within a hog cycle. A good example is silver. Between 1974 and the late 1980s, the Hunt Brothers stockpiled large amounts of silver and tried to control the silver market (Fey 1982). Large fluctuations in the market and several peak prices due to the cartel were characteristic of that period. Buying or hedging silver in 1978 or 1979 for 2 years at the short-term low-price benchmark would have saved the buyers a lot of money. When the Hunt Brothers filed for bankruptcy in 1988, the real price for silver returned to the former floor price—a logical reaction to destruction of the cartel.

Short-term low-price benchmarks are defined using local troughs during sustained periods of high and volatile prices. The local troughs are visually determined. However, defining local troughs or price trends within a price cycle, especially in highly volatile markets, remains challenging (cf. also Cortez et al. 2018; He et al. 2015; Radetzki and Wårell 2017, and references therein for future perspectives on prices).

A short-term low-price benchmark cannot be established for times which are characterized by short-term shock events. These shocks are a special type of price-forming event. Most are accompanied by price peaks which usually last less than 1 to 2 years before prices fall back to the old level. Price peaks can occur for various reasons. For example, sudden interruptions of supply can occur due to strikes or wars like the cobalt price peak in 1978 caused by the Shaba crisis. Perceived shortages and hype can also give rise to price peaks: a good example is the tantalum price peak that occurred during the IT boom followed by the dotcom bubble at the beginning of the twenty-first century (Damm 2018). Technological breakthroughs in the manufacturing industry may also create price peaks, for example, sudden new demand for germanium in the fiber and infrared optics industry at the end of the 1990s (Melcher and Buchholz 2014).

Problems created by price peaks can generally be overcome relatively fast by industry operating in a market economy. A good example is the extreme price peak of rare earth elements in 2011/2012 which resulted from increased demand and export restrictions imposed by China, the largest producer of rare earth elements. When manufacturers reduced and substituted rare earth elements in their applications and a WTO-court case against China was launched, prices collapsed in 2013/2014 and fell back close to their former level (Wellmer et al. 2018, cf. Fig.5.2 therein).

The ratio between the short-term/long-term low-price benchmark

The ratio between the short-term and long-term low-price benchmarks indicates at which minimum surplus price buyers could procure a metal within a hog cycle. The higher this ratio, the higher the price that has to be paid for a metal during a hog cycle in comparison to the long-term low-price benchmark. A good example of this is copper (Plate 1). The ratio is between 1.41 and 1.43 for past hog cycles covering the period 1953 to 2003, and 1.71 for the period 2004 to 2017. This range is based on 64 years of market data and may help buyers to better estimate at which level minimum surplus prices may lie in a future hog cycle. The results for all metals studied, shown in Plates 1, 2, 3, 4, and 5, are described briefly in the “Results” section and interpreted in the “Discussion” section.

Use of cash cost curves

Cash costs per unit metal produced are typically calculated in three ways (S&P Global Market Intelligence 2018):

-

(i)

Total cash costs: total mine site costs, cash operating costs including transport costs of concentrates to the smelter, smelting and refining charges as well as royalty and production taxes

-

(ii)

All-in costs: total cash costs, all-in-sustaining costs, development and expansion capex, interest charges, extraordinary cash charges and other all-in costs

-

(iii)

Total production costs: total cash costs, reclamation and closure provision, depreciation, deferred stripping amortized, inventory change

For our study, we use deflated average total cash costs in real terms (weighted average of all covered mines, deflator US PPI; data based on nominal cash costs, S&P Global Market Intelligence 2018), mainly because exploration and capex costs as well as depreciation and inventory changes are flexible costs which during low-price phases may be deferred to later periods. Cash costs normally rise and fall along with rising or falling metal prices. However, at a given time, the cash costs define a lower marker for metal prices, because many mines and mine projects are no longer profitable below the average cash cost line (gray broken line, Fig. 2, average values given in Tables 1, 2, and 4).

The ratio between the long-term low-price benchmark/total cash costs

The ratio between the long-term low-price benchmark and the average cash costs shows how far the real price benchmark is from the average cash cost level. This ratio can be used as a predictor for the future development of low-price benchmarks. The closer this ratio is to 1, the closer the mining industry operates at its operating margins. If the ratio is approximately 1, a number of mines that operate at the average cash costs level would theoretically barely survive. Mines at the lower side of the cash cost curve would make a profit, while mines at the upper side of the cash cost curve would have to close sooner or later. If the ratio is > 1, mines that operate at the average cash cost level would make a good profit. If the ratio is < 1, many mines would have to close in times of falling prices, and thus, global mine output would shrink. In this case, metal prices would have to increase to make good this deficiency. In consequence, real prices for metals may not systematically fall below the average real cash costs. In fact, the metal prices have to be significantly above the real cash costs in order to allow mining companies to generate profit and reinvest in exploration. The results are visualized in Plates 1, 2, 3, 4, and 5, will be described briefly in the “Results” section, and interpreted in the “Discussion” section.

Results

Steel, iron ore, and base metals

Real prices for steel, iron ore, and base metals generally have a flat trend (Plate 1, Table 1).

For steel, two major breaks in the real price time series can be identified. The first break is between 1949 and 1958 when real prices doubled from a 500 US$ to a 1000 US$ long-term low-price benchmark. The reason for this price increase was strong demand for steel in connection with the Marshall Plan and strong global economic growth combined with heavy investments in infrastructure and building. The second break was between 1979 and 1982 at the beginning of the steel crisis of the 1980s. Real prices collapsed to a 400 US$ long-term low-price benchmark and have remained at about the same level up to the present time (steel, merchant rebar, world, and EU prices).

Iron ore is characterized by one long-term low-price benchmark lasting 90 years. In 2010, long-term price contracts for iron ore were phased out by major mining companies and prices rose dramatically. However, when global economic growth slowed in 2015, prices for iron ore dropped to the former floor price of around 48 US$/tonne.

Among the base metals analyzed, the longest low-price benchmarks are for zinc and lead spanning periods of 100 years and 65 years, respectively. For the other base metals, several shorter low-price benchmarks were identified which fluctuate more frequently. Despite short- to medium-term high-price phases lasting 3 to 5 years, for example in the 1970s and 1980s, real prices always fell back close to the identified long-term low-price benchmarks and rarely slipped below that marker. The period between 1982 and 2003 is generally characterized by a very low long-term low-price benchmark. The main reason is a collapse in global economic growth from 5.35 to 0.39% between 1976 and 1982 followed by a period of volatile growth (World Bank Group 2019). During that period, prices for example for lead dramatically dropped additionally as a consequence of internationally applied new environmental regulations calling for a reduction of lead in gasoline, paints, solders, and water systems (Plunkert and Jones 1999). Another example is tin. Real prices for tin significantly decreased in 1986 after the International Tin Cartel finally collapsed in 1985.

As for steel and iron ore, the real prices of base metals were strongly influenced by the economic boom in China between 2003 and 2016. Except for copper and lead, the real prices fell back to, or near to, the estimated long-term low-price benchmark. In fact, they actually fell below the average real price of the total period (Table 1). For copper and lead, it is difficult to establish a low-price benchmark for the period 2005 to 2017. The real prices have not yet fallen to the previously established low-price benchmark and it seems that a new benchmark level needs to be established (broken line; cf. further discussion in Chapter 5).

Within this group of commodities, the average ratio between the short-term and long-term low-price benchmark generally varies between 1.25 for tin and 1.46 for copper. This ratio shows that even during high-price phases, a good purchase price can be achieved. An exception is iron ore, which has an average ratio of 1.61. The ratio between the long-term low-price benchmark and the average real total cash costs varies between 1.01 for zinc and 1.65 for iron ore.

Ferroalloying metals

Real prices for the ferroalloying metals nickel, cobalt, and tungsten generally have a flat trend indicating a stable long-term low-price benchmark which continues over more than eight decades (Plate 2, Table 2). The real prices always returned to levels close to the low-price benchmarks, even at times when prices dramatically increased due to shocks or economic booms (e.g., cobalt peaks during the first and second Congo wars in Zaire and the DRC in the 1990s/early 2000s; growth in demand due to the China boom between 2003 and 2016). For tungsten, it is difficult to say whether the existing long-term low-price benchmark could be extrapolated towards 2017 (broken line). The real prices have not yet fallen to the established benchmark level (cf. further discussion in the “Discussion” section).

In contrast to the long lasting low-price benchmarks for nickel, cobalt, and tungsten, real prices for ferroalloys, such as ferromolybdenum, ferrochrome, and ferromanganese, tend to have systematically shifted towards lower real prices, starting from around 1975 to 1982 and continuing to the present day. The price erosion between 1975 and 1982 reflects a shift in ferroalloy production from higher-cost to lower-cost locations, new steelmaking processes, increased use of recycled materials, and improved operating efficiencies for ferroalloy production. During this period, open hearth furnaces were phased out and replaced by basic oxygen and electric arc furnaces. For example, due to efficiency and substitution gains, the manganese unit consumption per tonne of crude steel production was reduced from around 7.2 to 6.4 kg of manganese (de Linde 1995). At the same time, steel prices collapsed, particularly between 1979 and 1982, when the annual world crude steel production decreased about 100 million tonnes, from 750 to 650 million tonnes. It seems that the efficiency gains for ferroalloys had a long lasting effect on lowering the real prices.

Real prices for ferrotitanium and vanadium have a flat trend corresponding to one long-term low-price benchmark at around 4200 US$/tonne and 19 US$/kg (V2O5), respectively. However, the time series are relatively short, spanning a period of only 37 years.

For the ferroalloying metals, the ratio between the short-term and long-term low-price benchmarks generally varies between 1.62 for ferromanganese and 3.72 for ferromolybdenum. In general, it is much higher than those for the base metals. The ratio between the long-term low-price benchmark and the real total cash costs for nickel, cobalt, and ferromolybdenum varies between 0.71 for cobalt and 1.34 for ferromolybdenum.

Minor metals

In general, real prices for the minor metals also have a flat trend (Plate 3, Table 3). With the exception of lithium (lithium carbonate), the established long-term low-price benchmarks cover a period of more than 40 years. Although minor metal prices frequently have sharp price peaks, for example indium, tantalum, or cadmium, real prices always drop back to the established long-term low-price benchmark levels.

Major breaks in long-term low-price benchmarks are found for bismuth and germanium. Between 1950 and the end of the 1970s, the time series for bismuth starts with a long-term low-price benchmark of around 33,000 US$/tonne. During this time, the price for bismuth was controlled by major producers. Actually, the demand for bismuth as a metallurgical additive to aluminum, iron, and steel dramatically increased in the 1970s (Carlin 2013). This increase in demand caused a massive rise in global refined production. Subsequently, a strong oversupply, combined with weakening consumption, caused a collapse of real prices in the early 1980s. Since then, real prices have stayed at a much lower benchmark level of around 10,000 US$/tonne.

For germanium, the time series starts with a long-term low-price benchmark of around 2.1 million US$/tonne covering the period from 1950 to 1966. During this period, real prices remained at a relatively high level, with a major price peak occurring between 1953 and 1956. At that time, germanium was in great demand for use as a semiconductor in crystal diodes, transistors, and other electronic parts. However, from 1965 to 1970 and onwards, a new low-price benchmark of around 0.7 million US$/tonne was established because germanium had continuously been substituted by electronic grade silicon. In fact before 1970–1980, germanium was only used in small quantities and in special applications in the military and aerospace sectors but had little commercial use in mass products. Subsequently, however, new technologies such as fiber optics and infrared night vision systems were developed leading to greatly increased demand for germanium. This, in turn, led to a massive built up in refined germanium production followed by a large surplus in production capacity. As a consequence, real prices for germanium fell back to the previously established low-price benchmark level.

Real prices for lithium carbonate were relatively stable between 1977 and the mid-1990s. New low cost brine-based supplies in South America (< 2500 US$/tonne), especially in Chile and Argentina (Ober 1999), caused a drop in real prices from a 6200 US$/tonne long-term low-price benchmark to a new benchmark of about 3200 US$/tonne (note that the sharp price drop in 1998 in Plate 3 is due to restricted availability of reliable price data for the time from 1996 to 2000). Real prices increased from 2006 onwards to a new long-term low-price benchmark of around 5800 US$/tonne which was a result of increased global demand for lithium in lithium ion batteries (Ober 2007).

For minor metals, the ratio between the short-term and long-term low-price benchmarks varies between 1.69 for tantalum and 3.32 for selenium. Because minor metals commonly form sharp price peaks, short-term low-price benchmarks are difficult to define. In addition, our time series only starts in 1950 or during the 1970s and are not, therefore, as reliable as for other metals analyzed in this study.

Precious metals

Between 1918 and 2000, real prices for the precious metals silver, platinum, and palladium generally have a flat trend. The established long-term low-price benchmarks cover a period of six to nine decades (Plate 4, Table 4).

Real prices for gold have, however, developed very differently. After World War II, gold prices were fixed by the Bretton Woods System (World Gold Council 2019). In 1971, when the Bretton Woods System began to collapse, gold prices shifted to a much higher benchmark level. In 2006, the gold price started to dramatically increase again and real prices appear to have shifted away from the long-term low-price benchmark of around 500 US$/oz that was established during the 1970s and 1980s. It is difficult to determine whether the existing long-term low-price benchmarks could be extrapolated towards 2017 (broken line) or whether a new low-price benchmark can be established. Real prices for all the precious metals have not yet fallen to the established long-term low-price benchmark level (cf. further discussion in the “Discussion” section).

Within the group of precious metals, the ratio between the short-term and long-term low-price benchmark generally varies between 1.86 for platinum and 2.67 for palladium. The ratio between the long-term low-price benchmark and the average real total cash costs varies between 0.71 for palladium and 1.15 for gold.

Light metals

For aluminum and magnesium, a systematic drop in the established long-term low-price benchmarks can be observed starting in 1940 (Plate 5, Table 5).

Between 1918 and 1947, a long-term low-price benchmark of around 4600 US$/tonne can be identified for aluminum. During the 1940s, the real price dramatically decreased when the demand for military components declined, price controls by producers were abandoned, production capacities were expanded, and new applications for aluminum were developed, for example in the fields of construction and infrastructure (Kramer 2013; Bray 2013). Based on these developments, a new low-price benchmark of around 2600 US$/tonne can be traced over three decades ending in 1982. From then until the present day, real prices again systematically dropped to a new low-price benchmark of around 1900 US$/tonne. The latest reduction in the benchmark price can be attributed to major reductions in the cost of aluminum production that have occurred in China during that period.

Between 1948 and 1992, real prices for magnesium stayed at a long-term low-price benchmark of around 3400 US$/tonne. However, this price level actually lasted for only short periods, in particular around 1973, 1993, and 1998, with much higher real prices prevailing for longer time intervals. Magnesium prices periodically increased strongly due to a combination of high energy costs, rising inflation rates, and the increased use of magnesium in aluminum beverage cans (Kramer 2013). From 2000 onwards, real prices for magnesium significantly dropped to a new low-price benchmark of around 2500 US$/tonne when global magnesium production shifted towards low-cost production sites in China using the Pidgeon process via silicothermic reduction (Roskill Information Services Ltd. 2016).

The ratio between the short-term and long-term low-price benchmarks is around 1.31 for aluminum and 1.37 for magnesium. It should be noted that these ratios can only be established for the periods 1923 to 1940 (aluminum) and 1974 to 1991 (magnesium), with no ratios identified for more recent years.

Discussion

For the 28 metals investigated, our study shows that real prices have fluctuated markedly over time, but that they normally returned to a certain floor price, defined here as the long-term low-price benchmark. Where price data are available, a long-term low-price benchmark, or several low-price benchmarks, with a total duration of 80 to 100 years can be established for certain metals such as iron ore, copper, zinc, nickel, cobalt, tungsten, antimony, silver, platinum, and palladium.

It is remarkable that real prices have stayed relatively stable over such a long period of time. According to the total cash cost curves of the past 26 years, it seems that operating mines produced metals at similar costs over time (with production costs moving up and down with metal prices). New innovations and efficiency gains in exploration, mining, and processing have continuously reduced costs to inflation level (Schwerhoff and Stürmer 2016; Wellmer et al. 2018). Even during the last major cycle, the China Boom, when industrial growth stimulated metal prices in a dramatic way, prices in real terms fell to the level before the cycle started. This observation may lead to the conclusion that the China boom, an economic boom with the strongest effect on metal prices in modern history, had no sustaining effect towards higher real prices.

Compared to previous years, real prices for ferromolybdenum, ferrochrome, and ferromanganese dropped significantly to a lower long-term low-price level around 1979 to 1985. Since then, their floor prices have remained at that level. Although global demand for these ferroalloys has strongly increased, production costs, efficiency gains, and scaling effects in manufacturing processes have contributed to this long-term price drop. Aluminum and magnesium show similar trends.

If we trust in human innovation capability, future discoveries and further efficiency gains in mining and processing will be made. Thus, we suggest that the long-lasting low-price benchmarks could, with minor movements up or down, be extrapolated into the next decade. However, for copper, lead, tungsten, and the precious metals, it is clear that their real prices have not yet fallen to the established benchmark level. Therefore, it is difficult to say for these metals whether the existing long-term low-price benchmarks can be extrapolated towards 2017 and beyond, or whether the higher real prices are sustainable in the future. The experience of past real price trends shows that real prices in the long run have always dropped to, or near to, the long-term low-price benchmark.

A good marker for defining the long-term low-price benchmarks could be the ratio of the long-term low-price benchmark and the average real total cash cost marker:

-

For copper, iron ore, and ferromolybdenum, the ratio is > 1 and it appears that there is still potential for real prices to drop close to the average real total cash cost marker. In the event of a forthcoming global financial or economic crisis, we suggest that real prices for copper and iron ore would fall to or near the long-term low-price benchmark. High investments in copper mining will lead to new mine production possibly at today’s average real total cash cost level. In consequence, copper prices in the long run should come back to the calculated long-term low-price benchmark. Another example is lithium. Prices have peaked in 2017 because the e-mobility boom is currently driving lithium carbonate prices to levels significantly greater than 10,000 US$/tonne. Mining companies around the globe are making major investments in new mines and mine extensions (Schmidt 2017). Current total cash costs of brine-based mining in salt lakes are around 2500 US$/tonne and for hard rock mining around 3000 US$/tonne to 4000 US$/tonne (Deutsche Bank 2016). Thus, we propose that the current peak prices will not last for long and real prices may swing back to near the estimated long-term low-price benchmark.

-

Cobalt, silver, platinum, and palladium have a ratio < 1, which means that mining on average is not very profitable. It also means that the former real price benchmark might be too low and a new benchmark at a higher price level should be considered. However, this depends on whether the future market is bullish or bearish for a longer period of time (whereby bullish describes a market sentiment that prices will rise; bearish is the opposite). In fact, the cobalt price dramatically dropped near to the old benchmark level in 2018 after the market was overheated by the e-mobility boom. However, the cobalt benchmark probably needs to rise to compensate the enormous investment costs for cobalt in the mining sector. Platinum and palladium prices are also following current technological trends in the automotive sector. Since the diesel scandal, prices for palladium have almost doubled, whereas the platinum price has fallen. Any new political decisions regarding the future of diesel cars, consumer behavior, and technological innovations will affect both raw material markets. The low ratios of < 1 point to the fact that either mining costs have dramatically increased or that more cost-intensive deposits (e.g., lower grade zones) were mined just because of high market prices. For the platinum group metals, both effects are probably responsible for these low ratios. Therefore, it is necessary to continuously monitor cash cost developments at mines as well as developments in the automotive industry and the investment sector. If the sales volumes of diesel cars continue to fall, the demand for platinum will decrease and prices may fall to the long-term low-price benchmark level. A decrease in the size of the market for diesel cars would lead to increased demand for gasoline cars, which would, in turn, support the demand for palladium because palladium is predominantly used in catalytic filters in gasoline cars. In consequence, the benchmark for palladium would rise. In the long run, electric cars may replace conventional cars using an internal combustion engine. Consequently, the demand for, and prices of, both, platinum and palladium, may fall significantly, unless the platinum group elements become widely used in other new technologies such as fuel cells.

-

Nickel, zinc, lead, and gold are close to a ratio of about 1 which suggests that real prices will not drop below the defined long-term low-price benchmark (e.g., dashed benchmark line for gold, Plate 4). In fact, at lower price levels, mining of these metals would be marginal or unprofitable. Whenever demand rises and average real cash costs cross the long-term low-price benchmark, this is normally a signal of extremely bullish markets (cf. for example Plate 1, zinc; Plate 2, nickel, cobalt, ferromolybdenum; Plate 4, precious metals). Therefore, metals near the ratio of 1 need to be monitored closely. For example, gold became a major monetary asset class during the global financial crisis of 2008–2009, which still has not been completely resolved (World Bank Group 2018). High government debts in many countries, including EU member states and China, and “bad banks” still exist and have increased demand for gold as a safe haven. We thus propose that gold prices might stay at a high level until the effects of the financial crisis have been minimized. Accordingly, the long-term low-price benchmark for gold should probably be shifted upwards.

Monitoring average real total cash costs appears to be a useful tool to establish future low-price benchmarks. Total cash costs in the mining industry normally increase or decrease with increasing or decreasing prices. However, if total cash costs increase or decrease for a longer period of time, this could be a signal for rising or falling real prices forming new benchmarks.

The main factors which may increase operational costs at mines are (i) financial internalization of stronger environmental measures; (ii) financial internalization of a fairer involvement of local communities; (iii) increase in interest rates; and (iv) a trend to greater involvement of governments in mining.

Factors which may decrease operating costs in the mining industry are (i) technological breakthroughs in exploration such as the squid magnetic survey which enables mining and exploration companies to find high-grade metal deposits at depths of 1.000 m below ground; (ii) technological breakthroughs in mining such as full automatization in open pit and underground operations; (iii) micro mining methods deployed in narrow stratiform but high-grade deposits; (iv) improved shaft sinking methods at lower costs; breakthroughs related to beneficiation and extractive metallurgy such as micro grinding, advanced heap or tank bioleaching or other leaching techniques.

A more general observation is that the market power of companies seem to have an effect on the low-price benchmarks. In the past whenever key market players have enforced price controls and when these controls eventually came to an end, real prices then collapsed. Notable examples include bismuth in the late 1970s (producer controls); silver in the late 1980s (Hunt Brothers); and tin, for which the price decreased in 1986 after the International Tin Council collapsed in 1985. In contrast, real prices for gold increased between 1973 and 1976 after the price controls of the Bretton Woods System were abandoned.

Substitution is another factor that may have influenced changes in the benchmark price levels. One example is the lead price which dropped in the early 1980s when lead was largely substituted after strong environmental restrictions limiting its use were implemented globally (Plunkert and Jones 1999, Halme et al. 2012).

Applying the long-term low-price benchmark method to a given market situation, Table 6 shows an example for metal prices of March 2019 and suggests actions for long-term investment or purchase. At the price level of March 2019, there is a good or strong indication for long-term investment or purchase for cobalt, indium, bismuth, cadmium, aluminum, and magnesium. A good or strong indication for long-term investment or purchase is given when prices are close to the established long-term low-price benchmark with a ratio ≤ 1–1.2. Steel, tin, ferrochrome, ferrotitanium, germanium, selenium, and platinum may be placed on a watch list. For the rest of the metals, prices are relatively high in relation to the established benchmark levels. Investors and buyers may adjust the suggested categorization according to their experience and needs.

In contrast to the long-term low-price benchmarks, short-term low-price benchmarks can be used differently. These are of greater interest to buyers in purchasing departments, who have a shorter view on markets and who seek to secure a steady and secure flow of metals to their factories. The data show that identifying short-term low-price benchmarks within a hog cycle could lead to a good purchase signal. The observed ratio short-term/long-term benchmark varies a lot among the metals studied. Some metals, for example antimony, ferromolybdenum, tungsten, and vanadium, have a ratio > 2.0 or even > 3. This means that buyers had to pay very high prices throughout the whole cycle period. For other metals, with a ratio of < 2.0, extremely high prices can be avoided and a reasonable purchase price achieved either before or between price peaks.

Conclusion

In our study, we established low-price benchmarks for 28 metals. Our results show that there are metal specific lower price bounds over long periods of time. This helps investors and buyers to act anticyclically in between cycles, either to secure long-term offtake agreements or to farm into new mining assets at the right time. Short-term low-price benchmarks may be a helpful tool for buyers who operate to a short timescale and wish to purchase metals during a hog cycle.

For most of the metals studied, the long-term low-price benchmark can be tracked for many decades, up to 100 years. Over a period of such great length, learning effects have taken place which have helped to balance the supply and demand sides. We propose that these learning effects are still taking place and, in consequence, the long-term low-price benchmarks may, with minor deviations, be extrapolated at least into the next decade.

While real prices for most metals have not increased in the past, this may not necessarily hold for the future when it is likely that more environmental and social costs will have to be internalized. The “social licence to operate” (Prno 2013; Parsons and Moffat 2014) may become the most serious challenge for mining, smelting, and refining in the future (acatech 2018; Wellmer et al. 2018). In their annual risk radar of the top ten risk factors in the natural resources industry, the consulting company EY classified the social licence to operate as the greatest risk for 2019 (EY 2019). It is possible that the cost pressure to retain or obtain a social licence to operate will increase to such a degree that technical rationalization will be unable to keep up with the cost increases. As a result, there would be a need for prices to rise in real terms. Consequently, it would become important to continue to closely monitor real total cash costs and the ratio of the established long-term low-price benchmarks to the real total cash costs. Furthermore, price control actions, substitution, and recycling trends, as well as technological breakthroughs on the supply and demand side, need to be reviewed on a regular basis.

The most effective measures to secure metal supplies at low costs on a long-term basis are either to secure long-term offtake agreements or to farm into mining assets at the right time. As exploration and mining are a risky business and a secure supply is strategic for the manufacturing industry as well as for governments, several countries have taken action to support their manufacturing and mining industries. If manufacturing companies want to farm into advanced exploration projects or even to buy mining properties, at least by taking over a minority shareholding, this strategy calls for shrewd anticyclical action. Our long-term low-price benchmark method might be a good tool to detect low-price periods and to support decision-making.

Governments can help reduce the risk and capital burden. For example, the German Government subsidizes research and provides financial guarantees for untied project loans, i.e., through the state-owned promotional KfW Bank (BMWi 2018). Between 1970 and 1990, the German Government also encouraged German companies to invest in backward integration through an exploration support program (“Measures to improve the supply of mineral natural resources to the Federal Republic”). It succeeded in supporting German companies to acquire significant shares in foreign mines and, thus, to develop a robust backward integration of their business. A similar exploration support program was restarted by the German Government in 2013 but discontinued in 2015 due to a general relaxation of the metal markets and lack of engagement in mining activities by German industry (Wellmer et al. 2018).

Countries with a more proactive mineral resources strategy include China, the USA, and Japan. Especially in China and Japan, state mining companies are very active in securing mineral and metal supplies for their industries. The main organization in Japan is the Japan Oil, Gas and Metals National Corporation (JOGMEC) (Hilpert and Mildner 2013, Reuters 2016). JOGMEC provides financial assistance to Japanese companies helping to reduce the risk involved in exploration and mine development. Normally, this is done by concluding joint ventures with foreign mining companies. For example, in the case of the steel alloying metal niobium, JOGMEC works with the most important niobium producer worldwide, the Cia. Brasileira de Metalurgia e Mineração in Brazil. As a result of the activities of JOGMEC, major Japanese companies have been able to secure minority shares in many productive new deposits and thus ensured secure long-term supplies for Japanese industry.

A similar concept for Germany has been discussed as a policy option in a recent position paper within the research project “Energy Systems of the Future” (ESYS) by the three German science academies (acatech 2018; Wellmer et al. 2018). One of these policy options is the “establishment of a state-subsidized German metals company, which acts anticyclically and operates internationally.”

In order to act anticyclically with private or public money, certain guidelines are necessary. The real price benchmarks presented in this paper are one such tools for acting anticyclically in the metal markets. To make favorable investment or purchase agreements, the management of these companies has to have leeway for decisions to act or not to act. This paper may help companies to develop guidelines for establishing threshold prices, defined as prices where the manager could buy or sell metals or place investments in mining. These threshold prices, which could be the long-term low-price benchmarks developed here, could also be used for decision-making to increase stockpiles at the right time.

References

acatech (2018) National Academy of Science and Engineering, German National Academy of Sciences Leopoldina, Union of the German Academies of Sciences and Humanities Raw materials for the energy transition—securing a reliable and sustainable supply. Position paper, Schriftenreihe Energiesysteme der Zukunft, Munich, Berlin (acatech), 100 p https://www.acatech.de/Publikation/raw-materials-for-the-energy-transition-securing-a-reliable-and-sustainable-supply/. Accessed 30 July 2018

Arrington LJ, Hansen GB (1963) “The Richest Hole on Earth”—a history of the Bingham copper mine. Utah State University Press, Monograph Series, Vol XI, 1, 103 p

BLS - Bureau of Labor Statistics (2014) Comparing the Producer Price Index for Personal Consumption with the U.S. All Items CPI for All Urban Consumers. https://www.bls.gov/ppi/ppicpippi.htm. Accessed 25 August 2018

BMWi (2018) Federal Ministry for Economics and Energy: Garantien für Ungebundene Finanzkredite. https://www.bmwi.de/Redaktion/DE/Artikel/Aussenwirtschaft/garantien-fuer-ungebundene-kredite.html. Accessed 28 August 2018

Bräuninger M, Leschus L, Rosen A (2013) Ursachen von Preispeaks, −einbrüchen und –trends bei mineralischen Rohstoffen. DERA Rohstoffinformationen 17, Deutsche Rohstoffagentur (DERA) in der Bundesanstalt für Geowissenschaften und Rohstoffe (BGR), Berlin: 123 p

Bray EL (2013) Aluminium. Metal prices in the United States through 2010. Scientific Investigations Report 2012–5188. U.S. Geological Survey, Reston, pp 2–6

Carlin JF Jr (2013) Bismuth. Metal prices in the United States through 2010. Scientific Investigations Report 2012–5188. U.S. Geological Survey, Reston, pp 17–18

Chen MH (2010) Understanding world metal prices—returns, volatility and diversification. Res Policy 35:127–140

Connolly E, Orsmond D (2011) The mining industry: from bust to boom. Reserve Bank of Australia, Conference 2011, Chapter 4.2.4, https://www.rba.gov.au/publications/confs/2011/connolly-orsmond.html. Accessed 5 October 2018

Cortez CAT, Saydam S, Coulton J, Sammut C (2018) Alternative techniques for forecasting mineral commodity prices. Int J Min Sci Technol 28(2 March 2018):309–322

Cuddington JT (2010) Long-term trends in the real real prices of primary commodities: inflation bias and the Prebisch-Singer hypothesis. Resour Policy, Elsevier 35(2):72–76

Damm, S (2018) Rohstoffrisikoanalyse Tantal. DERA-Rohstoffinformationen 31, Deutsche Rohstoffagentur (DERA) in der Bundesanstalt für Geowissenschaften und Rohstoffe (BGR), 85 p. https://www.deutsche-rohstoffagentur.de/DE/Gemeinsames/Produkte/Downloads/DERA_Rohstoffinformationen/rohstoffinformationen-31.pdf?__blob=publicationFile&v=4. Accessed 02 July 2019

Deutsche Bank (2016) Industry Lithium, 101, Sydney, p. 177 http://www.metalstech.net/wp-content/uploads/2016/07/17052016-Lithium-research-Deutsche-Bank.compressed.pdf. Accessed 02 July 2019

Drachal K (2018) Some novel Bayesian model combination schemes: an application to commodities prices. Sustainability 10(2801):1–27 https://www.researchgate.net/publication/326883169_Some_Novel_Bayesian_Model_Combination_Schemes_An_Application_to_Commodities_Prices. Accessed 02 July 2019

Erten B, Ocampo JA (2013) Super cycles of commodity prices since the mid-nineteenth century. World Dev 44:14–30

EY (2019) Business risks facing mining and metals 2018–2019. https://assets.ey.com/content/dam/ey-sites/ey-com/global/topics/mining-metals/mining-metals-pdfs/ey-top-10-business-risks-facing-mining-and-metals-in-2019-20.pdf. Accessed 25 January 2019

Ezekiel M (1938) The cobweb theorem. Q J Econ 52(1):255–280

Fernandez V (2012) Trends in real commodity prices: how real is real. Res Policy 37(1):30–47

Fey S (1982) The great silver bubble. Hodder & Stoughton General Division, London 275 p

Gleich B (2014) Der Preis mineralischer Rohstoffe: Zeittrend und Einflussfaktoren. Neue empirische Antworten auf eine alte Fragestellung mit Implikationen für Wirtschaft und Gesellschaft. Dissertation, Cuvillier Verlag Göttingen, 324 p

Government of Alberta (2019) How to use charting to analyse commodity markets. http://www1.agric.gov.ab.ca/$department/deptdocs.nsf/all/sis10136. Accessed 16 May 2019

Halme K, Piirainen KA, Vekinis G, Sievers Eu, Viljamaa (2012) Substitutionability of critical raw materials. Policy Department A: Economic and Scientific Policy, Directorate General for Internal Policies (eds), PE 492.448, Brussels, 100 p https://www.researchgate.net/publication/262198504_Substitutionability_of_Critical_Raw_Materials. Accessed 15 January 2019

Hanau A (1928) Die Prognose der Schweinepreise. Vierteljahreshefte zur Konjunkturforschung, Sonderheft Vol 7. Institut für Konjunkturforschung, Berlin 44 p

He K, Lu X, Zou Y, Lai KK (2015) Forecasting metal prices with a curvelet based multiscale methodology. Res Policy 45(C):144–150

Hilpert HG, Mildner SA (eds) (2013) Nationale Alleingänge oder internationale Kooperation? Analyse und Vergleich der Rohstoffstrategien der G20-Staaten. Stiftung Wissenschaft und Politik, Bundesanstalt für Geowissenschaften und Rohstoffe, Berlin/Hannover. https://www.bgr.bund.de/DE/Themen/Zusammenarbeit/TechnZusammenarbeit/Politikberatung_SV_MER/Downloads/SWP-studien_2013-S01.pdf?__blob=publicationFile&v=1. Accessed 29 August 2018

Humphreys D (2010) The great metals boom: a retrospective. Res Policy 35:1–13

Jerrett D, Cuddington JT (2008) Broadening the statistical search for metal price supercycles to steel and related metals. Res Policy 33:188–195

Julihn CE (1932) Copper: an example of advancing technology and the utilization of low-grade ores. In: Tyron FG, Eckel EC (eds) Mineral Economics, Chapter VI, A.I.M.E. Series. McGraw-Hill, New York, pp 111–136

Kilian L (2009) Not all oil price shocks are alike: Disentangling demand and supply shocks in the crude oil market. American Economic Review 99(3):1053–1069

Kramer JA (2013) Magnesium. Metal prices in the United States through 2010. Scientific Investigations Report 2012–5188, U.S. Geological Survey, Reston: 88–90

Leong R (2018) U.S. dollar share of global currency reserves fall further–IMF. https://www.reuters.com/article/uk-forex-reserves/u-s-dollar-share-of-global-currency-reserves-fall-further-imf-idUSKBN1JR21G. Accessed 25 August 2018

de Linde JP (1995) Ferroalloy markets. In: Tuset JK, Tveit H, Page IG (eds) Norwegian Ferroalloy Organization, Infacon 7, 11.-14. June 1995, Trondheim, Norway, pp 39–62

Luyken W, Bierbrauer E (1931) Die geschichtliche Entwicklung der Flotation. In: Luyken W, Bierbrauer E (eds) Die Flotation in Theorie und Praxis. Springer, Berlin, pp 2–19

Lynch A (2018) The eras of mineral processing. In: Wood D (2018) Geology and mining: an introduction and overview. SEG Newsletter, 115, 1: 9–21

Melcher F, Buchholz P (2014) Germanium. In: Gun G (ed) Critical metals handbook. Wiley, Chichester, pp 177–203

Ober JA (1999) Lithium in 1998. Minerals Yearbook, U.S. Geological Survey, United States Government Printing Office, Washington, DC 8 p

Ober JA (2007) Lithium in 2006. Minerals Yearbook, U.S. Geological Survey, United States Government Printing Office, Washington, DC 8 p

Parsons R, Moffat K (2014) Constructing the meaning of social licence. Soc Epistemol 28(3–4):340–363

Plunkert A, Jones TS (1999) Metal prices in the United States through 1998. U.S. Geological Survey, United States Government Printing Office, Washington, DC 179 p

PricewaterhouseCoopers (2016) Mine 2016—slower, lower, weaker… but not defeated. Review of global trends in the mining industry. Global Mining Leadership Team, PricewaterhouseCoopers 50 p. https://www.pwc.com/gx/en/mining/pdf/mine-2016.pdf. Accessed 15 Jan 2019

Prno J (2013) An analysis of factors leading to the establishment of a social licence to operate in the mining industry. Res Policy 38:577–590

Radetzki M, Wårell L (2017) A handbook of primary commodities in the global economy. Cambridge University Press, Cambridge 305 p

Reuters (2016) Japan passes law to allow JOGMEC to invest in foreign oil, gas firms. 11.11.2016. https://www.reuters.com/article/us-japan-jogmec-idUSKBN1360UC. Accessed 29 August 2018

Roberts MC (2009) Duration and characteristics of metal price cycles. Res Policy 34:87–102

Rosenau-Tornow D, Buchholz P, Riemann A, Wagner M (2009) Assessing long-term supply risks for mineral raw materials—a combined evaluation of past and future trends. Res Policy 34:161–175

Roskill Information Services Ltd (2016) Blast furnace iron production and usage of magnesium for desulphurization. International Magnesium Association Conference, Rome, Italy, May 15-17, unpublished presentation

Rossen A (2015) What are metal prices like? Co-movement, price cycles and long-run trends. Res Policy 45:255–276

S&P Global Market Intelligence (2018) Mine economics methodology—mine economics cost curves. S&P Global Market Intelligence, commercial access 5. October 2018

Schmidt, M (2017) Rohstoffrisikoanalyse Lithium. DERA-Rohstoffinformationen Nr. 33, Deutsche Rohstoffagentur in der Bundesanstalt für Geowissenschaften und Rohstoffe, 134 p https://www.deutsche-rohstoffagentur.de/DERA/DE/Downloads/Studie_lithium_2017.pdf?__blob=publicationFile&v=3. Accessed 02 July 2019

Schwerhoff G, Stürmer M (2016) Non-renewable resources, extraction technology, and endogenous growth. Federal Reserve Bank of Dallas Working Paper No. 1506, 38 p

Stürmer M (2018) 150 years of boom and bust: what drives mineral commodity prices? Macroecon Dyn 22(3):702–717

Svedberg P, Tilton JE (2006) The real, real price of nonrenewable resources: copper 1870-2000. World Dev 34(3):501–519

Svedberg P, Tilton JE (2011) Long-term trends in the real real prices of primary commodities: inflation bias and the Prebisch-Singer hypothesis. Res Policy 36(1):91–93

Tilton JE (2003) On borrowed time? Assessing the threat of mineral depletion. Resources for the Future, Washington, D.C., Routledge 158 p

Tilton JE, Crowson PCF, DeYoungJr JH, Eggert RG, Ericsson M, Guzmán JI, Humphreys D, Lagos G, Maxwell P, Radetzki M, Singer DA, Wellmer FW (2018) Public policy and future mineral supplies. Res Policy 57:55–60

Wellmer FW, Dalheimer M (2012) The feedback control cycle as regulator of past and future mineral supply. Mineral Deposita 47(7):713–729

Wellmer FW, Hagelüken C (2015) The feedback control cycle of mineral supply, increase of raw material efficiency, and sustainable development. Minerals 5:815–836

Wellmer FW, Dalheimer F, Wagner M (2008) Economic evaluations in exploration. Springer, Berlin 250 p

Wellmer FW, Buchholz P, Gutzmer J, Hagelüken C, Herzig P, Littke R, Thauer RK (2018) Raw materials for future energy supply. Springer, Berlin 255 p

World Bank Group (2018) Global economic prospects—the turning of the tide? World Bank Publications, The World Bank Group, Washington DC 184 p

World Bank Group (2019) GDP growth (annual %), World Bank national accounts data, and OECD National Accounts data files, 1965–2017, all countries. https://data.worldbank.org/indicator/NY.GDP.MKTP.KD.ZG?end=2017&start=1961&view=chart, Accessed 25 April 2019

World Gold Council (2019) The Bretton Woods system. https://www.gold.org/about-gold/history-of-gold/bretton-woods-system. Accessed 2 July 2019

Acknowledgments

This research was conducted with internal funds at the Federal Institute for Geosciences and Natural Resources (BGR, German Geological Survey). The research is part of the Raw Materials Monitoring System at the German Mineral Resources Agency (DERA) at the BGR. DERA was assigned by the Federal Ministry of Economics and Energy (BMWi) in 2013 to build up the monitoring system which was mandated by the German Government through the German coalition agreement of 2013 between the German parties CDU/CSU and SPD.

We would like to thank the reviewers of this paper for their valuable contributions and comments, Dr. Gus Gunn for proof-reading of the English language and helpful comments regarding individual metal markets, and colleagues at the BGR who compiled historic price data over previous decades.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher’s note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

About this article

Cite this article

Buchholz, P., Wellmer, FW., Bastian, D. et al. Leaning against the wind: low-price benchmarks for acting anticyclically in the metal markets. Miner Econ 33, 81–100 (2020). https://doi.org/10.1007/s13563-019-00199-y

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s13563-019-00199-y