Abstract

Emphasizing customer satisfaction as a strategic lever for enhancing business performance is a widespread business practice. However, just over 25 years of empirical studies by academic researchers has produced evidence that is sometimes contradictory. Hence, greater academic clarity and improved managerial understanding could result from a meta-analysis of the customer satisfaction-business performance relationship. To that end, the authors analyzed 251 correlations from 96 studies published between 1991 and 2017. While the satisfaction-performance relationship is positive and statistically significant on average (r = .101), more meaningful insights emerge from the explication of moderating and mediating relationships. Illustrative of these insights is the finding that satisfaction is more appropriately depicted as mediating the effects of selected marketing strategy variables on firm performance outcomes. Moreover, when satisfaction is viewed in the right setting using the right satisfaction and performance measures, a most favorable contingencies (MFC) perspective, the estimated correlation is reasonably strong (r = .349).

Similar content being viewed by others

Explore related subjects

Discover the latest articles, news and stories from top researchers in related subjects.Avoid common mistakes on your manuscript.

"Friendly service, clean rooms, comfortable surroundings, every time. If you’re not satisfied, we don’t expect you to pay. That’s our commitment and your guarantee.” –Hampton Inn

"We know each and every purchase is special, whether it's your next challenging puzzle or a gift for someone special. That's why we make the complete satisfaction of every customer our number one priority.” –Springbok Puzzles

It is not surprising that brands, both large and small, emphasize the importance of customer satisfaction in their marketing strategies. In fact, it is brand promises such as the above that lend support for the notion that customer satisfaction is important to firm performance. Indeed, multiple theoretical perspectives seemingly support the pivotal role of satisfaction in a firm’s marketing strategy. These include contagion perspectives (i.e., satisfied customers buying adjacent offerings and further motivating others to purchase through word-of-mouth; e.g., Barger and Grandey 2006), affective-state perspectives (i.e., satisfied customers developing positive affinities and enhanced product and brand loyalties leading to future purchases; Szymanski and Henard 2001), risk-reduction perspectives (i.e., guarantees of satisfying experiences moving additional consumers to purchase; Johnson et al. 2006), market-force perspectives (i.e., earned reputation for satisfying customers creating barriers to entry for non-incumbents leading to market share gains and additional scale effects; Rego et al. 2013), and market-signaling perspectives (i.e., promises of satisfaction making tangible the customer-centric culture valued by consumers; Singh and Sirdeshmukh 2000). Fornell et al. (2016a) even go so far as to assert that customer satisfaction is central to an economy. They emphasize a healthier economy and a healthier company are both characterized as having more, highly satisfied consumers.

The widespread practice of emphasizing satisfaction goals plus the multiple theoretical perspectives supporting this strategic emphasis would imply that the empirical evidence on the satisfaction-performance relationship should consistently support a positive relationship. However, a qualitative review of the literature reveals that evidence on the satisfaction-performance relationship is instead quite inconsistent. Weak and strong, positive and negative, statistically significant and non-significant satisfaction-performance effects characterize the literature. As a result, questions have been raised as to the role customer satisfaction actually plays in firm performance. They include (i) whether satisfaction-performance effects are generalizable (Jacobson and Mizik 2009; Lehmann and Reibstein 2006), (ii) whether customer satisfaction is indeed critical to firm performance (Kumar 2016), (iii) whether satisfaction is more critical to selected performance metrics than others (Bharadwaj and Mitra 2016), (iv) whether satisfaction is more appropriately depicted as a mediator of strategic marketing effects rather than being depicted as another exogenous determinant of firm performance (e.g., Homburg et al. 2014; Rubera and Kirca 2017), and (v) whether the satisfaction-performance field itself is in a state of limbo (Fornell et al. 2016a). Bharadwaj and Mitra (2016) further question whether the next primary replication or extension study can hope to effectively address these multiple, research issues. They also question whether other substantive issues might be overlooked when primary research is focused on bringing closure to the current set of conflicting results. Arguably, they implicitly question whether the area could benefit more today from a meta-analysis of the satisfaction-performance evidence. To that end, a meta-analysis would provide needed insights on central tendencies and relevant moderators of satisfaction-performance effects. A meta-analysis would also provide a needed empirical baseline for positioning and motivating future research on the satisfaction-performance relationship that would include examinations of satisfaction’s mediating effects with regard to marketing strategy as well as firm and industry variables.

The conceptual rationale favoring the satisfaction-performance relationship, the empirical evidence that is conflicting, and the resulting questions arguing for future research to synthesize and add clarity to current thinking all serve to motivate this meta-analysis on the satisfaction-performance relationship. After approximately a quarter century of empirical research in marketing dating back to Fornell (1992) and Rust and Zahorik (1993), taking stock of the satisfaction-performance evidence is needed to identify a common body of analytical knowledge emerging from, or embedded in, the extant data. This resulting knowledge base can center on the (i) expected strength of the satisfaction-performance relationship, (ii) circumstances under which satisfaction effects are expected to be stronger or weaker, and (iii) appropriate modeling of satisfaction’s role amongst other strategic drivers of firm performance. Our meta-analysis addresses these three facets of understanding by drawing on the cumulative evidence for its foundation (Grewal et al. 2018). To accomplish our goals, we proceed with a discussion of the conceptual meaning of satisfaction, the conceptual relationship between satisfaction and its performance outcomes, the potential moderators of the satisfaction-performance relationship, and the likely mediating role of satisfaction amongst other determinants of firm performance. The methodology used for the meta-analysis is then described. The presentation of the findings and their discussion, as well as a discussion of limitations and directions for future research, conclude the meta-analysis.

Conceptualizing customer satisfaction

Oliver (2010) provides a much needed dictionary-based definition of satisfaction. Dating back to the first edition of his book in 1997, Oliver defines satisfaction as the post-consumption consumer judgment of whether the good or service provided a pleasurable level of overall usage-related fulfillment. In this definition, consumers’ fulfillment assessments and existing sense of pleasure are viewed as keys to understanding the process behind customer satisfaction formation. Succeeding conceptualizations of satisfaction have in turn focused on explicating the process for assessing satisfaction levels in the context of disconfirmation, affect, equity, expectations, and/or product performance. Dominant among the process-based investigations is the disconfirmation paradigm, which views satisfaction as resulting from consumers’ comparing outcomes to expectations (e.g., Churchill and Surprenant 1982). Szymanski and Henard (2001), for example, find positive disconfirmation, along with consumer affect and buyer equity, as positively influencing consumers’ level of satisfaction. Ultimately, satisfaction levels are shown to positively impact consumers’ word-of-mouth, loyalty, and behavioral intentions.

In consideration of satisfaction’s central role in the aforementioned processes, Oliver (2010) further delineates between temporal and aggregate components of satisfaction. For one, satisfaction can represent a real-time assessment (i.e., during the buying process, but before purchase) in addition to a post-purchase assessment (i.e., information from memory reflective of satisfaction with prior buying situations) of the buying experience. The expectation is that the post-purchase assessment will be the bigger influencer of the purchase decision since it is more strongly rooted in final outcomes. Second, the post-purchase assessment can be reflective of transactional satisfaction (i.e., satisfaction with a single experience) or cumulative satisfaction (i.e., satisfaction reflective of multiple experiences) (Jones and Suh 2000). Here, the expectation is that cumulative assessments will be more influential. They are likely to be influential because they permit an assessment of the central tendencies of the purchase experiences that had occurred in the past, and because these cumulative data provide consumers with a broader foundation for predicting future consumption experiences. All told, this further recognition of satisfaction’s multiple facets has led researchers to distinguish among current satisfaction, lagged satisfaction, transactional satisfaction, and cumulative satisfaction in their respective investigations (e.g., Williams and Naumann 2011). As discussed next, researchers have also addressed these dimensions of satisfaction in the context of multiple metrics of firm performance.

Conceptualizing the performance effects of customer satisfaction

Customer satisfaction has been construed in the literature as a market-based asset that is relevant to the efficient and effective orchestration of firm resources and the enhancement of firm performance (Beckers et al. 2017; Rubera and Kirca 2017). Dominant among such investigations, and therefore important for the meta-analysis to examine, is the study of satisfaction with respect to certain accounting measures of financial performance (e.g., profit), market measures of financial performance (e.g., stock price), and marketing measures of performance (e.g., market share and revenue).Footnote 1 Common rationale for satisfaction impacting these performance outcomes often derives from satisfaction’s role in driving a firm’s costs, margins, cash flow, and prospects for future growth. Anderson et al. (1994), for example, emphasize the positive association among satisfaction, word-of-mouth, and loyalty as being impactful for reducing price elasticities (e.g., improving retention and cash flow when prices increase), lowering transaction costs (e.g., lower costs of retaining customers relative to acquiring new customers, and lower marketing expenditures as a result of positive word-of-mouth effects), and increasing the firm’s share of its customers’ wallet (e.g., satisfied customers purchasing more of their total needs as well as buying more of the firm’s current, adjacent, and new offerings). Furthermore, they emphasize the value of satisfaction for reducing cross elasticities (e.g., insulating companies from competitive actions such as price wars that could adversely impact margins and cash flow) and/or increasing reputational effects (e.g., retaining current customers, attracting new customers). In all likelihood, these positive outcomes of positive satisfaction levels are likely to positively influence the firm’s accounting and market measures of financial performance, as well as its marketing performance outcomes. Selected financial and marketing performance effects are reviewed next.

A market measure of financial performance that has been the focus of empirical studies in the context of customer satisfaction is stock prices. Since market share, revenue, and profit improvements are widely viewed as indicators of greater firm attractiveness, theories of efficient markets suggest satisfaction and stock prices would move in the same direction. For example, the previously discussed process perspective of satisfaction suggests that satisfaction’s positive effects on consumer word-of-mouth, loyalty, and lifetime value should positively affect performance predictability, stability, and prospects for growth, all of which should be valued by the firm’s stakeholders (Fornell et al. 2016b). Anderson et al. (2004) also discuss satisfaction and stock market effects from a competitive forces perspective. That is, firms having satisfied and loyal customers should be more attractive and less risky partner companies (e.g., more stable sales, finances, and favorable growth prospects). These more stable and less risky partners should in turn be in a preferred position to extract favorable terms of trade (e.g., lower unit costs and higher volume orders) from channel members and business associates to further improve multiple performance metrics. For example, when markets are efficient, the positive outcomes from establishing favorable business partnerships should be evidenced in abnormal stock returns (e.g., Fornell et al. 2006; Sorescu and Sorescu 2016). Hence, satisfaction and stock prices are expected to be positively related. A similar positive relationship is expected for satisfaction with market share as discussed next.

The negative relationship sometimes evidenced for market share with profits emphasizes the fact that while increased satisfaction levels can be manifested in more sales and market share gains, gaining market share can also accrue at the expense of margin reductions or cost increases to the firm (Szymanski et al. 1993). More specifically, market share gains frequently result from increasing investments in advertising (Tellis 1988) and the sales force (Gatignon and Hanssens 1987), lowering prices in the context of penetration and experience curve pricing policies, and investing resources to improve quality and sales of the offering (Buzzell and Wiersema 1981), all of which can lower margins. Strategies for providing consumers with broader product lines (Robinson 1988) and increasing R&D expenditures necessary for creating a wider portfolio of innovative offerings (Blundell et al. 1999) can also characterize a firm’s efforts to gain additional market share. All told, customers (i) being more informed and better served as marketing efforts increase, (ii) selecting from a wider assortment of higher quality, innovative offerings that can better match changing needs (Robinson 1988), and (iii) shopping among baskets of superior and more affordable offerings (i.e., whenever greater firm market power does not translate into higher consumer prices; Cotterill and Putsis 2000) should create the necessary utility to positively impact customer satisfaction and customer retention and firm market share (Rust and Zahorik 1993). Therefore, assuming firms can expand offerings as their customer base becomes more heterogeneous (Rego et al. 2013), the expectation is that satisfaction levels and a firm’s market share performance would be positively related (Beckers et al. 2017; Morgan and Rego 2006).

Framework for the investigation

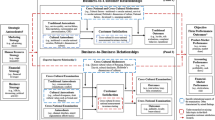

The preceding discussion on the conceptualization of customer satisfaction and its performance effects provides the backdrop for Fig. 1, which guides the meta-analysis. Figure 1 provides an integrative perspective on the potential moderating role of elements related to both satisfaction and performance, many of which have not yet been the focus of systematic modeling efforts. One set of moderating elements included in the model is the nature of the performance metric (i.e., measures of marketing performance, and accounting and market measures of financial performance). A second set of moderating variables modeled in Fig. 1 are factors that define the setting for the investigation, how satisfaction was captured, and which facets of satisfaction were considered. Bharadwaj and Varadarajan (2004), in their integrated model of business performance, highlight strategy and performance, firm resources and performance, and industry structure and performance as three major streams of research (spanning industrial organization economics, strategic management, and strategic marketing) focused on understanding, explaining, and predicting business performance. Therefore, also modeled in Fig. 1 are marketing strategy factors, firm factors, and industry factors delineating their direct effects on business performance outcomes, and effects mediated by customer satisfaction. In turn, the following meta-hypothesis (i.e., main-effect hypothesis), which is grounded in the dominant perspective of satisfaction and performance being positively related (Oliver 2010), provides the necessary reference for proposing that satisfaction-performance effects could be stronger or weaker on average in the presence of the moderating factors (as will be discussed below):

Conceptual framework for the meta-analysis

H1:

On average, customer satisfaction will have a positive and statistically significant effect on pooled, firm performance, all else held constant.

Moderators

Contextual moderators

Services versus goods

The intangibility, heterogeneity, inseparability and simultaneity (IHIP) characteristics of services (Parasuraman et al. 1985) suggest that satisfaction could play a stronger role in a services versus goods context (Edvardsson et al. 2000). First, the considerably greater potential for variability in the quality of services relative to goods suggests that firms which consistently and closely meet customers’ service expectations would be rewarded with more repeat purchases from satisfied customers (Reichheld and Sasser 1990). Second, since services are simultaneously produced and consumed and cannot be inventoried (e.g., an unoccupied seat on a departing flight of a commercial airline generates zero revenue; a hotel room that is unoccupied on a given night generates zero revenue) lowering prices to balance supply and demand, a common practice in service industries, can result in margin erosion. Against this backdrop, the use of yield management software for revenue maximization through dynamic pricing (i.e., lowering and raising prices in response to demand and supply), and price discrimination (e.g., charging business travelers a higher price and leisure travelers a lower price) is quite pervasive in a number of service industries. All else being equal, the need to lower prices to balance supply and demand will be lower for service firms that engender greater customer loyalty and repeat purchases by delivering consistently superior customer satisfaction experiences. As Edvardsson et al. (2000) demonstrate, customers loyal to a service can be more profitable than customers loyal to a good. The expectation therefore is that satisfied customers will be more loyal and more profitable in services than goods businesses. Formally, we predict:

H2:

The customer satisfaction-performance relationship will be stronger for services relative to both goods and hybrids of goods and services, all else equal.

Non-retailing versus retailing

Retailing is often characterized as more complex than other types of businesses for several reasons. For one, the scope of operations can often be vast as retailers can be responsible for selling many thousands of stock keeping units from a multitude of manufacturers. The number of relationships to effectively manage on the supply side can therefore be considerable and can complicate efforts to coordinate product availability and product assortments with consumer demand (Adjei et al. 2009). Second, relative to business-to-business (B2B) firms, retailers can be faced with a considerably larger base of customers on the demand side. This can make it more challenging for retailers to get product assortments right, maintain proper inventory levels, develop strong customer relationships, and effectively serve a multitude of suppliers and end users. Effectively satisfying end users may therefore be more challenging for retailers (Cai 2010; Koschat 2008), especially in consideration of the greater challenges of executing an omni-channel strategy of online and bricks-and-mortar retailing (Verhoef et al. 2015). Indeed, retailing can be further characterized as highly competitive with offerings often assuming commodity status. Therefore, the capability to distinguish the firm on superior goods satisfaction leading to superior firm performance could represent a key strategic obstacle diminishing the strength of the satisfaction-performance relationship for retailers compared to non-retailers, all else equal. Stated formally:

H3:

The customer satisfaction-performance relationship will be stronger for non-retailers relative to retailers, all else held constant.

Satisfaction measurement moderators

Cumulative versus transactional satisfaction

The satisfaction-performance relationship is expected to be stronger on average when satisfaction is operationalized as cumulative (i.e., multiple encounters) rather than transactional (i.e., a single encounter) satisfaction. Research has shown that there is a greater likelihood that cumulative satisfaction weighs more heavily in relationship formation (Bolton 1998) and is more diagnostic and more indicative of the firm’s past, present, and future performance (Anderson et al. 1994). Taking into account the greater likelihood that consumers are more firmly loyal and less price sensitive, and thereby willing to pay more in consideration of high cumulative satisfaction levels (Homburg et al. 2005), we predict that satisfaction effects on performance will be stronger when the focus is cumulative satisfaction, all else equal. Formally:

H4:

The customer satisfaction-performance relationship will be stronger when satisfaction is operationalized as cumulative relative to when satisfaction is operationalized as transactional, all else held constant.

Lagged versus same-period satisfaction

Conceptually, it can be argued that consumer purchase decisions would be influenced both by real-time (i.e., current) satisfaction assessments as well as post-purchase (i.e., lagged) satisfaction assessments (Oliver 2010). Empirically, however, satisfaction effects on performance have sometimes been found to be stronger for lagged versus current satisfaction levels (Terpstra and Verbeeten 2014). An explanation for the greater effect of previous period assessments is that lagged satisfaction allows for a full accounting of the effects of consumers’ word-of-mouth on firm performance. Hence, we posit that while both current and lagged satisfaction levels can significantly impact firm performance, performance effects are likely to be stronger for lagged customer satisfaction. Stated formally:

H5:

The customer satisfaction-performance relationship will be stronger for lagged satisfaction relative to same-period satisfaction, all else constant.

Top-box versus not top-box satisfaction

Morgan and Rego (2006) posit that a focus on the top one or two most positive satisfaction scale responses could lead to stronger estimates of the satisfaction-performance relationship. The rationale for this posited effect includes top-box respondents being the firm’s most profitable customers due to the effects of satisfaction on the willingness of loyal customers to pay price premiums and their likelihood of buying again. Hurley and Estelami (1998), for example, find stronger relationships between service quality and sales growth among top-box versus bottom-box respondents. De Haan et al. (2015) further document that top-box customer satisfaction performs best for predicting customer retention, which inarguably is a critical driver of firm performance. Consequently, we would expect to find a stronger association for satisfaction with performance when satisfaction reflects top-box scores and all else is held constant. Thus, we predict:

H6:

The customer satisfaction-performance relationship will be stronger for top-box satisfaction relative to not top-box satisfactions, all else held constant.

ACSI versus non-ACSI measures

The American Customer Satisfaction Index (ACSI) scores are thought to better capture the underlying level of customer satisfaction among respondents (Fornell 1992). ACSI scores capture satisfaction levels at a granular level (e.g., scores ranging from 1 to 100) and then indexes them as a composite latent variable with partial least squares used to estimate importance weights. ACSI scores also reflect national sentiments over an array of products, firms, industries, and consumer groups. This broader and larger sample of consumers and offerings can reduce sampling error and delimit biases from regional differences in satisfaction tendencies (Mittal et al. 2004). Minimizing these biases can reduce noise and allow for a stronger estimate of the satisfaction-performance relationship to emerge from the analysis. The expectation therefore is that stronger satisfaction-performance effects would be evidenced when the database is national (including Swedish and Norwegian databases [Anderson et al. 1994; Keiningham et al. 2008]) and the ACSI approach is used for database construction. This positive effect is likely when such data are contrasted to either satisfaction data grounded in other multi-item scales (i.e., non-national data absent the ACSI approach) or satisfaction data gathered using single-item measures, and especially when single-item measures are used for capturing more abstract constructs like customer satisfaction (Bergkvist and Rossiter 2007; Loo 2002). Formally, we predict:

H7:

The customer satisfaction-performance relationship will be stronger, on average, for ACSI-type measures compared to other multi-item and single-item measures of satisfaction, all else held constant.

Performance measurement moderators

Comparisons across performance measures

Prior literature suggests that market measures of financial performance of the firm (e.g., stock prices) are superior to both accounting measures of financial performance (e.g., profits) and marketing measures of performance (e.g., market share and revenues). This stronger effect is likely because differences in accounting practices across firms can render comparisons of profit performance (which is often based on revenue measures) problematic (Anderson et al. 2004). Therefore, satisfaction-performance effects can be stronger for market measures than accounting measures of financial performance due to there being less noise in the data. Research further suggests that the increased costs associated with strategies designed to capture additional market share can have a detrimental effect on firm profits. Szymanski et al. (1993) in their meta-analysis of the market share-profitability relationship find that the two firm performance metrics, market share and profits, are negatively correlated on average. Consequently, the expectation for the meta-analysis is that satisfaction effects will be strongest for stock prices compared to market share, profit, and revenue measures of performance. Therefore:

H8:

On average, the customer satisfaction-performance relationship will be strongest for stock prices compared to market share, profit, and revenue measures of firm performance, all else equal.

Methodology

Database development

Search process

The search for satisfaction-performance studies relevant to the meta-analysis starts with the seminal studies of Fornell (1992) and Rust and Zahorik (1993), and includes the broader search for more recent or earlier studies (Wiley 1991) on this topic. This search incorporated multiple outlets (i.e., published and unpublished studies) to minimize publication bias, multiple disciplines to minimize familiarity bias (i.e., focusing only on domains of researcher expertise), multiple methods (e.g., citation reviews, manual searchers, electronic databases) to minimize availability bias (i.e., focusing on easily identifiable studies; Rothstein and Hopewell 2009), and multiple key words for satisfaction (e.g., consumer, customer, and buyer satisfaction) and performance (e.g., financial, market share, profitability, and stock price performance) to minimize the likelihood of missing additional studies capturing the same constructs. The search also spans multiple disciplines and sub-disciplines that included behavioral accounting, computer science, consumer behavior, economics, engineering, finance, hospitality management, information systems, marketing strategy, operations management, organizational psychology, services marketing, and strategic management. Finally, prior to concluding the search process in July 2017, 25 authors of satisfaction-performance studies were contacted and asked for any working papers they may have or know about on this topic.

Inclusion criteria

The final set of satisfaction-performance studies ultimately judged relevant to our meta-analysis were those using both objective measures to capture firm performance and overall measures to capture satisfaction and firm performance levels. The focus on objective performance measures stems from research demonstrating that managers’ subjective performance assessments can represent imprecise proxies of actual firm performance. Ailawadi et al. (2004), for example, report a mean correlation of only .30 between objective and subjective sales agent performance measures, and Wall et al. (2004) report a mean correlation of just .48 between subjective and objective profit measures. Findings such as these have led to an advocacy in the literature for objective performance measures due to their greater accuracy, capability to reduce common-method bias, and appropriateness for making within and between business comparisons given that objective measures are inherently absolute. Second, the validity of combining effects across studies requires combining effects at similar levels of aggregation. Therefore, studies relevant to the meta-analysis needed to report satisfaction and performance as overall customer satisfaction (either transactional or cumulative overall satisfaction levels) and overall business performance (i.e., overall market share, revenue, profit, or stock price performance levels) rather than satisfaction or performance with a single attribute of the offering (e.g., price) or a specific aspect of the business (e.g., salesforce or supply chain).

Search outcomes and coding of findings

The outcome from the search for relevant satisfaction-performance studies was the identification of 96 empirical studies (67 published and 29 unpublished studies at the time of the review) examining the relationship between overall customer satisfaction and objective, overall firm performance. The Pearson correlation coefficient, or data that could be converted to correlations (Borenstein et al. 2009), was the most common metric reported. In total, 251 satisfaction-performance correlations were coded from the 96 studies. These correlations form the basis for our meta-analysis.

Overview of data analyses

As is traditional to meta-analysis (Borenstein et al. 2009; Schmidt and Hunter 2015), our empirical analysis begins with the univariate estimation of the central tendency of the satisfaction-performance correlation and its variance. Random-effects rather than fixed-effects modeling is used throughout the meta-analysis to account for observed variance among the Pearson correlations (Becker 2009). Preliminary analyses further supported the analysis of the Pearson correlation compared to its Fisher-z transformed value. Schmidt and Hunter (2015) argue that any negative bias from r-based estimates is highly preferable to the resulting positive bias inherent in Fisher-z estimates. We also found the estimates from our analysis of the r-based correlations were indeed more conservative. Hence, the Pearson correlation is the metric used in all subsequent phases of the meta-analysis, including both the bivariate (i.e., comparisons of mean effects by subcategories of the proposed moderator) and multivariate analyses of moderators. Specific to the multivariate analysis of moderators, we specify a restricted maximum likelihood (REML) model with Knapp-Hartung (K-H) variance estimators. REML is advocated for the fact that it tends to be unbiased, efficient, and avoids over-fitting (Harbord and Higgins 2008). K-H confidence intervals are also more conservative estimates that have been shown to perform better than z-based intervals (Hartung et al. 2011; Röver et al. 2015).

Finally, the empirical analysis concludes with estimating the meta-analytic structural equation model (MASEM) for satisfaction with performance. MASEM is advocated in meta-analysis for (i) capturing associations not fully addressed in the literature, (ii) examining relationships grounded in the cumulative evidence that more closely approximate true effects (see central limit theorem), and (iii) addressing effects within the broader, nomological framework that describes the variables of interest (Jak 2015). Our MASEM focuses on examining the likely mediating effects of satisfaction on performance with regard to several classical marketing strategy (i.e., advertising, R&D, and scope of served market) and firm and industry (i.e., firm size, industry concentration, and market growth) variables. Not only are these core variables modelled widely in the marketing literature, (i) they are connected in theory to both satisfaction and performance, and (ii) they are elements for which a complete or nearly complete correlation matrix can be developed from this literature (Palmatier et al. 2006).

Meta-analytic results

Central tendency of the satisfaction-performance relationship

As stressed in our introduction, the considerable disparity in size, direction, and statistical significance of the 251 satisfaction-performance correlations challenges researchers and managers alike to assess central tendency and identify relevant contingencies through a qualitative review of the data. Specifically, the correlations range from -.59 to .99 with little evidence to indicate that effect sizes have gotten appreciably stronger or weaker with time (r = .173, p < .05, for effect size with study publication date).Footnote 2 Moreover, 55 of the 251 correlations are negative, 10 of the negative-signed correlations are statistically significant (p < .05), and four more correlations are reported in the literature as having a value of .00. While 192 of the 251 correlations are indeed positive, only half (n = 96) of these correlations are statistically significant (p < .05). Thus, a meta-analysis is necessary to clarify the satisfaction-performance relationship as well as identify why the reported estimates differ so greatly.

Our meta-analysis of the 251 satisfaction-performance correlations finds the mean correlation to be both positive and statistically significant as predicted in H1. Specifically, the mean correlation (i.e., mean adjusted for sample size and scale reliability) for customer satisfaction with pooled performance (i.e., regardless of performance metric) is equal to .101 (95% CI of .075 to .127). Although the mean is relatively modest in size, it does display desirable statistical properties. For one, the large fail-safe N of 1793 (i.e., number of missing, null effects to render the mean non-significant) for satisfaction with performance indicates the estimate is absent meaningful publication bias. Second, funnel-plots using the trim and fill method and sensitivity analysis using bootstrapping further suggest no meaningful satisfaction-performance effects are absent in the database and no meaningful outliers are present in the database. For example, bootstrapping (i.e., withholding one case and re-estimating the mean) shows the range of .097 to .103 for the revised mean correlation is well within rounding of .101. Third, there is no indication of meaningful dependency in the database from conducting an effect-level (i.e., each effect within the study) versus a study-level (i.e., one effect per study) analysis of the correlations. The mean effect-level (M = .101, 95% CI of .075 to .127) and study-level (M = .121, 95% CI of .081 to .161) correlations for satisfaction with performance are not statistically different, the intra-class correlation of .005 is near zero, and the design effect of 1.008 is well below the cutoff of 2.0 for suggesting clustering is warranted (Romano and Kromrey 2009). These data clearly indicate that dependency is not a meaningful issue. Nonetheless, we adjusted the standard errors by the square root of the design effect to ensure subsequent findings are conservative (Shackman 2001).

Moderators of the satisfaction-performance relationship

While the overall estimate of the satisfaction-performance correlation is statistically significant and positive, the wide variance in reported effects combined with the modest strength of the mean relationship compared to other strategic factors (e.g., M = .248 across all strategic variables as reported in Eisend (2015)) leads one to question whether the strength of the satisfaction-performance relationship is substantially stronger under certain conditions. In this context, analysis shows the Q statistic is statistically significant (Q = 3850, p < .05), indicating meaningful heterogeneity across the reported effects, and the estimated I2 value of 93.51% exceeds the 75% threshold level, indicating that a high percentage of variance between the correlations is due to heterogeneity rather than chance (Higgins et al. 2003). These findings, in turn, provide a necessary statistically-based justification for examining moderator effects within the context of the satisfaction-performance relationship. Our initial moderator findings, which are presented in Table 1 and discussed next, also point to elements for which satisfaction-performance effects can generalize (i.e., non-significant moderator effects with due caution to Type II error).

Study setting characteristics

Consistent with H2, the data in Table 1 show the mean satisfaction-performance correlation is significantly stronger for services (M = .144; 95% CI of .092 to .196) compared to goods (M = .049; 95% CI of .016 to .083). The bivariate findings do not however support H3, which predicts satisfaction effects as stronger for non-retailers. Rather, satisfaction-performance effects appear to generalize across retailers and non-retailers. The mean satisfaction-performance correlation of .115 (95% CI of .087 to .143) for non-retailers is greater than the mean effect of .070 for retailers (95% CI of .019 to .120), but the difference in mean correlations is not statistically significant.

Satisfaction measures

The findings from Table 1 also fail to support H4, which proposes a meaningful difference between cumulative and transactional satisfaction effects. The mean correlation for cumulative satisfaction (M = .086; 95% CI of .064 to .107) is not significantly different from the mean correlation for transactional satisfaction (M = .145; 95% CI of .074 to .214), implying that satisfaction-performance effects can generalize across cumulative and transactional assessments. The satisfaction-performance correlation also apparently generalizes between the use of lagged satisfaction measures (M = .128; 95% CI of .057 to .199) and satisfaction measures that are not lagged (M = .097; 95% CI of .070 to .124), and thus, H5 is not supported. Likewise, the data in Table 1 fail to support H6. That is, though satisfaction-performance effects are slightly stronger on average for top-box scores (M = .181; 95% CI of .102 to .258) compared to when the complete scale is used to score satisfaction (M = .092; 95% CI of .065 to .119), the difference in means is not statistically significant. Finally, the bivariate findings in Table 1 do not support H7 The estimated means for ASCI-type measures (M = .108; 95% CI of .073 to .144), multi-item scales (M = .061; 95% CI of .015 to .107), and single-item scales (M = .156; 95% CI of .100 to .213) are not statistically distinct from one another.

Performance measures

The findings in Table 1 do however lend partial support for H8. The average satisfaction-performance relationship is stronger on average when performance is operationalized as stock price (M = .113; 95% CI of .072 to .153) compared to market share (M = -.019; 95% CI of -.105 to .68). The relationship is also stronger on average when the performance metric is profit (M = .127; 95% CI of .091 to .165) instead of market share. Thus, the bivariate findings offer insights into certain moderators of satisfaction-performance effects and the conditions under which satisfaction effects are likely to generalize. Critical moderator insights are also generated through the following multivariate (REML) findings presented in Table 2, which consider the unique contributions and profile nature of the contingency effects.

Meta-regression findings

The REML findings continue the support throughout the meta-analysis for H1, which posits a positive and statistically significant effect of satisfaction on performance. As reported in Table 2, the grand mean (constant term) is positive, statistically significant, and equal to .127 (p < .05). The REML findings also suggest that while satisfaction-performance can generalize on average (with consideration given to Type II errors) between services and goods (H2), lagged and current satisfaction timeframes (H5), and composite and non-composite measures (H7), other setting and other measure factors moderate the estimate of the satisfaction-performance relationship. Specifically, the coefficients for non-retailing (B = .059, p < .10) and top-box satisfaction (B = .181, p < .05) are positive and statistically (p < .05) or marginally (p < .10) significant (see H3 and H6, respectively). The REML findings also indicate an effect for cumulative versus transactional satisfaction that is marginally significant (B = -.070, p < .10) and opposite to the positive effect predicted in H4. Finally, a pattern of stronger satisfaction-performance effects generally is found for stock price (i.e., negative coefficients are evidenced when stock price is the contrast measure in the REML model) as suggested in H8. In particular, the coefficient reported in Table 2 for market share is negative (B = -.148, p < .05), implying that satisfaction-performance effects are stronger on average for stock price relative to market share (i.e., stock price is the contrast category in the regression model).

In addition to these descriptive findings, predictive results derived from the REML findings also illuminate the hidden effects of satisfaction on performance (i.e., the predicted mean correlation under its most favorable contingencies [MFC]). When the setting is non-retailing (i.e., non-retailing equals one), satisfaction is transactional satisfaction (i.e., cumulative satisfaction equals zero), satisfaction is operationalized as top-box satisfaction (i.e., top-box satisfaction equals one), performance is operationalized as stock price (i.e., market share is zero), and all other coefficients in the model are set to zero, the predicted satisfaction-performance relationship is reasonably strong. The predicted mean correlation is .349, which is nearly a three-fold increase in strength compared to the grand mean of .127. According to Cohen (1988), a mean correlation of .349 is moderate to large in strength. Hence, it seems appropriate to state that, on average, satisfaction’s role in driving business performance can be meaningfully impactful when viewed in the context of its MFC—the right setting with the right measures. We now turn attention to the MASEM findings and the potential mediating role of satisfaction in the context of other factors that could be affecting firm performance levels.

Structural equation results

More recent satisfaction-performance studies have come to emphasize satisfaction’s performance effects within a partial-mediating framework (e.g., Homburg et al. 2014; Luo et al. 2012; Maiga et al. 2013; Rubera and Kirca 2017; Yu et al. 2013). Our focus in this MASEM portion of the meta-analysis therefore emphasizes whether a partial-mediating (PM) perspective is further supported in the cumulative data on the satisfaction-performance relationship. For one, our preliminary analysis of several performance metrics (i.e., pooled performance, market share, and profit) indicated that a full-mediating model (i.e., each exogenous factor directly impacting satisfaction and only satisfaction directly impacting performance) does not fit the cumulative satisfaction-performance data.Footnote 3 Second, the modification indices backed by theory point to a further modeling of multiple exogenous variables directly impacting both satisfaction and performance, which is supportive of a PM model. Thus, the more general PM model guiding MASEM estimation is presented in Fig. 2. The conceptual rationale in support of each PM model path is summarized in Table 3.

Illustrative findings for partial mediating model of the customer satisfaction and pooled performance relationship

The correlation matrix in Table 4 is used as input for PM model estimation (see Supplemental Material [Section II] for standard error and skewness statistics). Excessive numbers of missing correlations for revenue and stock price metrics (e.g., missing correlations with R&D, served market focus, and market growth) precluded PM model estimation for these two performance metrics. A complete matrix however was available for pooled performance and profit and a nearly complete matrix was available for market share (absent the correlation for market growth rate). Therefore, separate MASEMs are estimated for pooled performance, profit, and market share. Specifically, for pooled performance and profit, not all exogenous variables were indicated as significantly impacting performance. The non-significant performance effects are therefore not modeled in order to permit an assessment of model fit (i.e., these models are not saturated models). For market share, the indices and the resulting significant paths point to a saturated model (i.e., each of the available exogenous factors significantly impacts performance at p < .05). The findings from the estimation of the saturated market share model as well as the estimated pooled performance and profit models are presented in Table 5.

Pooled performance findings

As summarized in Table 5, the MASEM for pooled performance is non-significant (p = .68) with the RMSEA (0, 90% CI of .04 to .097), CFI (1.0), TLI (1.0) and SRMR (.006) indices further supporting the appropriateness of modeling satisfaction effects within the PM framework of Fig. 2. The data in Table 5 also reveal that (i) satisfaction is a statistically significant (p < .05) predictor of performance (β = .074), (ii) all three marketing strategy factors—advertising (β = .175), R&D expenditures (β = .157), and scope of served market (β = .096)—are significant predictors of satisfaction, (iii) the firm factor of firm size (β = −.121) is a statistically significant predictor of satisfaction, and (iv) three of the exogenous factors—advertising (β = .144), scope of served market (β = .066), and industry concentration (β = .211)—are statistically significant predictors of pooled performance. Finally, among the statistically significant (p < .05) total effects (i.e., direct plus indirect effects via satisfaction), the greatest impact on performance in absolute value is evidenced for industry concentration (β = .213), followed by advertising expenditures (β = .157) and R&D expenditures (β = .012). All told, these findings, and the findings that follow, support a PM perspective to modeling customer satisfaction with business performance.

Market share findings

As mentioned, the modification indices when estimating a FM model for satisfaction with market share point to the saturated model in Fig. 2 as the most descriptive of satisfaction-market share effects. In turn, PM model estimation (see Table 5) shows (i) the paths for advertising (β = .177), R&D (β = .156), scope of served market (β = .097), and firm size (β = −.122) with regard to satisfaction to be statistically significant (p ≤ .05), (ii) the satisfaction-performance path to be positive and significant (β = .041), and (iii) each marketing strategy factor and each industry factor to be a statistically significant predictor of market share performance. Regarding these market share effects, we find positive effects on market share for advertising (β = .131), firm size (β = .402), and industry concentration (β = .615), while greater R&D expenditures (β = −.133) and a narrower scope of served market (β = −.371) negatively impact market share levels. Finally, the total effects are statistically significant for each of the exogenous variables: advertising (β = .138), R&D (β = −.127), scope of served market (β = −.367), firm size (β = .397), and industry concentration (β = .616).

Profit findings

The findings in Table 5 also indicate that the PM model for satisfaction with profit fits the data well. The overall model is non-significant (p = .64) with RMSEA (0, 90% CI of .04 to .098), CFI (1.0), TLI (1.0) and SRMR (.008) indices lending support to the PM modeling of satisfaction with respect to firm profit. Regarding the individual paths in the model, (i) advertising (β = .175), R&D (β = .157), and scope of served market (β = −.121) emerge as statistically significant drivers of satisfaction levels, (ii) satisfaction is a statistically significant predictor of profit (β = .076), and (iii) both advertising expenditures (β = .178) and R&D expenditures (β = .093) are shown to positively and directly influence a firm’s level of profitability. The findings from the MASEM further document that the total effects for advertising (β = .191) and R&D (β = .105) with respect to firm profit are also statistically significant. The implications of these PM findings and the other findings from the meta-analysis are discussed next, particularly as they address selected gaps in the current satisfaction-performance literature.

Discussion of the results

The essence of this meta-analysis is in the multi-step, multi-tiered processes of investigating the many findings on the satisfaction-performance relationship with the goal of providing beneficial generalizations and contingencies. Toward this end, we provide Table 6, which is designed to bring necessary closure to the empirical portion of the investigation by offering readers a summary of the findings. This summary concisely outlines possible generalizations and necessary caveats, and also offers suggested implications for theory and practice within the context of customer satisfaction and its role in driving firm performance. More broadly, the summary table offers necessary insights for first, concluding that satisfaction matters generally to firm performance outcomes, and then second, for concluding that satisfaction effects are more prominent when viewed from the lens of the various moderators and mediators that can come to describe the satisfaction-performance relationship. Therefore, it is with this summary and its supportive evidence in hand that the following discussion goes beyond a restating of the tabled information. Rather, the discussion which follows emphasizes the role of the meta-analytic findings within the context of selected gaps in the satisfaction-performance literature, i.e., issues debated, and research extensions articulated in previous researcher studies that are relevant to future academic research and business practice. These issues and extensions focus on the (i) generalizability of ACSI-based findings, (ii) identification of moderators of satisfaction effects, (iii) appropriate modeling of the satisfaction-performance relationship, and (iv) practical implications of satisfaction-performance findings for business decisions. Each of these methodological, modelling, and managerial gaps, and thus their implications, are discussed in turn below.

Implications for methods, models, and management

Presence versus absence of ACSI effects

As discussed previously, the ACSI approach is touted for its measurement properties when it comes to capturing satisfaction levels. However, questions have also been raised regarding the composition and representativeness of the firms in the ACSI database. For example, Morgan and Rego (2006) question whether (i) ACSI firms are representative of the U.S. economy in terms of industry coverage and (ii) ACSI findings generalize to smaller firms whose end-users are businesses instead of consumers since the ACSI database is comprised predominantly of large, consumer-based firms. In addition, Bharadwaj and Mitra (2016) question how firms are chosen for inclusion in the ACSI database and whether missing data abounds that would impact subsequent satisfaction estimates. Sorescu and Sorescu (2016), in turn, question whether the firms in the ACSI database are outliers (i.e., firms high on satisfaction that just so happen to be profitable). Finally, Fornell et al. (2016a) emphasize the need to document whether there exists an ACSI “inclusion effect,” (i.e., whether ACSI-based findings differ from findings from other databases). Being that the meta-analysis presented here includes satisfaction-performance findings derived from data of both ACSI and non-ACSI firms, the findings of this meta-analysis can begin to address whether or not an ACSI inclusion effect exists. What we find is evidence indicating the absence of such an inclusion effect. Our bivariate results from Table 1, for example, show the mean satisfaction-performance relationship does not differ significantly for ACSI versus non-ACSI derived measures of customer satisfaction. The multivariate findings from Table 5 also show that the ACSI vs. non-ACSI variable is not a significant moderator of the estimated strength of the satisfaction-performance relationship. Together, these data imply that measurement as well as sampling features distinct to ACSI-based investigations do not appear to meaningfully bias estimates of relationship strength. Rather, ACSI-based results are likely to be externally valid.

Identifying meaningful moderators

A second gap in the literature centers on the consistent call for the identification of additional moderators of the satisfaction-performance relationship. For example, Voss et al. (2010) present a relatively exhaustive list of relational (e.g., relationship duration, orientation, age, program, etc.) and marketplace (e.g., service quality, switching costs, convenience, competition, etc.) characteristics for consideration as moderators of the satisfaction-repurchase link. Gruca and Rego (2005) show context to be an important moderator of satisfaction effects and argue for more research on this topic. Mittal and Kamakura (2001), in turn, present research on the moderating effects of customer characteristics in regard to satisfaction and repurchase intent and repurchase behavior. Studies by Anderson et al. (2004) and Rego et al. (2013) more generally argue for subsequent investigations focusing on identifying critical moderators of satisfaction effects. With this call to research in mind, the findings from the meta-analysis add to our understanding of contingency effects through its modeling of multiple study settings, satisfaction measures, and performance measures as moderators of satisfaction-performance effects. What we find is that retail/non-retail setting, cumulative/transactional satisfaction, top-box/not top-box satisfaction, and stock price/market share performance emerge as critical distinctions for properly modeling and estimating satisfaction-performance effects. We also find services/goods setting, lagged/not lagged satisfaction, stock price/profit and revenue performance, as well as the ACSI/non-ACSI context (as previously mentioned) are not relevant moderators of satisfaction-performance effects. Hence, the meta-analysis expands the list of identified moderators documented in the literature. It also provides insights into those elements that can now be viewed as being less relevant in the context of moderators of satisfaction effects.

Appropriate modeling of satisfaction effects

In addition to the previous two methodological gaps, the meta-analysis addresses a theoretical gap centering on how to best model satisfaction effects. Though the question of alternative modeling is not always at the forefront of discussions in the satisfaction literature, generating insights into whether direct-effect specification, moderator specification, or mediating specification is most appropriate for capturing satisfaction effects in the context of firm performance is nonetheless implicit—if not explicit—among the considerations in academic pursuits of satisfaction knowledge. What the meta-analysis adds in this regard is a robust set of findings indicating that while main-effects are evidenced from the literature, the specification of more elaborate models is invariably more appropriate for capturing the true nature of the effect satisfaction has on firm performance. As mentioned above, satisfaction is evidenced as being stronger under selected conditions, which is further supportive of theory grounded in contingency perspectives. But moreover, a modeling of satisfaction as a partial mediator of satisfaction effects is both more reflective of the total influence of satisfaction on firm performance and more reflective of the total influence of marketing strategy and firm/industry factors on how well a firm performs in the marketplace. The MASEM findings lend support to the growing specification and estimation of satisfaction effects within a mediating framework (e.g., Homburg et al. 2014; Luo et al. 2012; Maiga et al. 2013; Rubera and Kirca 2017; Yu et al. 2013). Specifically, we find consistent support across the various performance metrics for suggesting that customer satisfaction can mediate the role of marketing strategy, firm, and industry factors in determining performance levels. This finding is important not only for properly conceptualizing satisfaction’s role in driving firm performance, it is important for explicating the total effects (i.e., direct plus indirect) of these strategic factors in determining how well the firm performs. A further recognition of total effects also ensures that the influence of these strategic factors is not being underestimated nor underappreciated. Thus, our partial-mediating findings, and their support in the context of estimating outcomes using cumulative data, are important for filling in conceptual and empirical gaps when it comes to both modeling satisfaction-performance effects and modeling strategic and firm/industry factors in consideration of customer satisfaction and firm performance.

Relevancy to business practice

The perceived value of satisfaction as a focal variable in managerial decision making stems from knowing that satisfaction is both statistically significant and practically relevant to firm performance. Primary studies, for example, have the benefit of being able to provide point estimates of satisfaction outcomes using specific model estimates benchmarked against firms in their respective databases. For example, Gruca and Rego (2005) find that a one-point increase in customer satisfaction scores translates into a $55 million increase in net operating cash for the average firm in their sample. Anderson et al. (2004) report that a 1% change in customer satisfaction scores leads to a 1.016% change in shareholder value for the average firm in their sample. Finally, Anderson et al. (1994) find that an annual, one-point increase in satisfaction scores over five years translates into a cumulative discounted return of $7.48 million or 11.5% of current ROI for the typical firm in their database. Because a meta-analysis of bivariate correlations does not provide the same the opportunity to reference a specific database of firms, an alternative focus for assessing practical relevance is necessary. One such focus results from estimating McGraw and Wong’s (1992) common language effect size (CLES). CLES can be interpreted as the probability that between randomly selected firms, the one which is higher on satisfaction will also be the firm that is higher on performance (the baseline probability is 50% when satisfaction and performance are uncorrelated). Our mean correlation of .349 (the MFC value) estimated for satisfaction with performance is equal to a CLES value of .702 (Dunlap 1999). Translated for managers and analysts alike, the CLES of .702 means that there is more than a 70% probability that the firm that is higher on customer satisfaction will also have a higher stock price. The improved predictive capability that this metric indicates further implies that satisfaction can have relevance to business practice and financial analysts’ decision making as illustrated next.

The improved practical relevance of satisfaction information to decision making and practice can be manifested in a number of ways. One application is with respect to investors’ use of marketing information. Luo and Homburg (2008), for example, present satisfaction as a customer-based asset, and specially an intangible firm asset, impacting firm performance and the value of the firm. Aksoy et al. (2008), in turn, point to studies indicating that even though satisfaction has come to be viewed as a customer-based asset, analysts apparently do not widely recognize customer satisfaction as one of the intangible assets they review when evaluating businesses. Possible explanations for the lack of emphasis placed on satisfaction information is the variability in the relationships reported in the literature and the lack of clarity on the nature of the central relationship. Grewal et al. (2010), for example, find that satisfaction heterogeneity delimits the translation of customer satisfaction into shareholder value. This meta-analysis begins to address the variability gap by providing information on the predictive ability of satisfaction levels as well as insights into central tendency and the explanations for the variance across the reported effects.

A second application of the greater predictability of stock prices in the face of satisfaction information is within the context of CEO compensation. For example, there is a growing emphasis on customer satisfaction as an explicit CEO performance metric (Luo et al. 2012). The fact that total shareholder return is increasingly emphasized in executive compensation plans, and is increasingly emphasized as a performance metric among institutional investors, accents the further need to better understand the mechanisms behind stock performance (Gruca and Rego 2005). In this context, the meta-analysis findings show satisfaction is one of the factors impacting share prices as well as one of the factors predictive of share price performance. Therefore, rewarding or incentivizing managers for satisfaction performance can be considered warranted in the context of creating shareholder value, all else equal. Moreover, the ability to consistently deliver superior customer satisfaction experiences is a firm capability that can be difficult for competitors to diagnose and/or replicate due to its tacit nature and embeddedness in organizational processes (Teece et al. 1997; Vorhies et al. 2009). Hence, achieving superior satisfaction and a reputation for superior satisfaction can therefore make marketing assets and capabilities difficult for competitors to match. With the contributions of the meta-analysis to marketing thought and managerial practice in mind, we now turn to future research issues worthy of empirical study that could not be addressed within the meta-analysis.

Implications for future research

The limitations of meta-analysis represent potential directions for future research. For example, meta-analysis is limited to factors examined in previous studies that also include elements central to research interests and inertia at any one point in time in a research stream’s evolution. While our meta-analysis spans research trends addressing issues relating to certain antecedents, outcomes, moderators, and mediators of satisfaction-performance effects, certain other factors not modeled or not modeled extensively enough in the literature could not be included in the meta-analysis. Hence, there is the call to examine yet other moderators and other elements relevant to developing a more comprehensive understanding of satisfaction effects. They include customer factors such as expertise, cognitive complexity, need for uniqueness, self-concept maintenance, consumer networks, and consumer contagion, product factors such as product complexity, firm factors such as organizational learning capability and corporate culture, macro environmental factors such as regulatory forces impacting business practices, and marketing strategy factors such as brand extensions, marketing alliances, digital strategies, customer prioritization, collaborative efforts, and promotional pricing. Similarly, modeling the moderating roles of additional contextual elements, as well as modeling the nonlinear and asymmetric effects of satisfaction and other factors on performance (see Luo and Homburg 2007; van Doorn and Verhoef 2008), could be critical for identifying the full menu of settings and functional forms for which satisfaction effects are their strongest. There was not sufficient research attention devoted to these issues to permit their examination within the context of our meta-analysis.

In addition, the respective studies over the years that have examined various components of a more complete satisfaction modeling with respect to performance point to the need for both a comprehensive conceptual modelling of satisfaction as well as the need for a mega-analysis that seeks to combine findings across previous meta-analyses in which satisfaction has been a component. An initial conceptual model of satisfaction that includes the many possible antecedents and outcomes of satisfaction and their interconnections by Thursyanthy and Tharanikaran (2017) illustrates how daunting of a task it may be to both conceptualize and then empirically model the totality of customer satisfaction effects. Likewise, the challenges of piecing together the correlation matrices across existing satisfaction meta-analyses looking at the antecedents of satisfaction (Szymanski and Henard 2001), employee satisfaction (Brown and Lam (2008), satisfaction effects in market channel relationships (Geyskens et al. 1999), etc., suggest that the many linkages necessary for constructing a truly complete correlation matrix may be an ambitious goal. Nonetheless, providing a pathway and an ambition for creating a more inclusive and comprehensive understanding of satisfaction can be notable for advancing academic understanding and managerial practice. Importantly, pursuit of this understanding is strongly encouraged given the promise demonstrated by both this meta-analysis and previous research on the customer satisfaction-business performance relationship.

Notes

Another market measure of financial performance that has been the focus of investigation in the satisfaction-performance literature is Tobin’s q. However, concerns have been raised recently by Bendle and Butt (2018) regarding the use and misuse of Tobin’s q in marketing (see Bendle and Butt 2018). Because of these concerns (brought to our attention by a reviewer for which we are grateful, and a reviewer’s related suggestion), the analysis of Tobin’s q is presented in the Supplemental Material.

A breakout of the mean satisfaction-performance correlation by time period (i.e., year of study publication) similarly fails to illuminate a meaningful pattern of ever increasing or decreasing effect sizes. Specifically, for studies published (i) before 1997, M = −.110 (95% CI of −.224 to .007, n = 15), (ii) during the period 1998–2002, M = .092 (95% CI of .046 to .138, n = 42), (iii) during the period 2003–2007, M = .097 (95% CI of .064 to .131, n = 66), (iv) during the period 2008–2012, M = .140 (95% CI of .089 to .191, n = 90), and (v) during the period 2013–2017, M = .112 (95% CI of .044 to .180, n = 38). Thus, while the respective means for the last four time periods are each significantly stronger than the mean estimate for the time period “before 1997” (note, the mean for “before 1997” is not statistically significant), it should be noted that the respective means for each of the four, more recent time periods are not significantly different from one another.

Prior to estimating the final PM models, a full mediating (FM) model (i.e., marketing strategy, firm, and industry factors only directly impacting satisfaction and satisfaction then directly impacting performance) was estimated to determine whether fit would be superior. The MASEM findings indicate that the FM model is a poor fitting model across the performance measure while the respective partial-mediating versions of those models can be considered to fit the data well. Regarding the FM pooled performance model, the χ2 (6) of 67.34 is significant (p < .05), the CFI of .57 and TFI of .04 are below the critical threshold of .95 suggestive of a good fit, the SRMR of .05 is reasonable, but values of zero represent perfect fit, and the RMSEA of .11 and its 90% CI having an upper bound that exceeds .10 (CI = .087 to .133) are further indicants of poor fit. Similarly, the FM model is a poor fit for market share. The Δχ2 (5) of 921.56 is significant (p < .05), the CFI is .06 and TFI is −1.06 (which is a non-normed value), the SRMR is .16, and the RMSEA of .48 with a 90% CI of .455 to .508 are also indicants of poor fit. Likewise, the FM model is a poor fit to the data when profit is the performance measure. The χ2 (6) of 36.83 is significant (p < .05), the CFI of .72 and TFI of .40 are below the threshold of .95, the SRMR of .04 is reasonable, but the RMSEA of .08 and its 90% CI having an upper bound that exceeds .10 (CI = .055 to .104) are indicative of poor model fit. The resulting modification indices (in the case of each of these three FM models) pointed to estimating a partial mediating model instead, with one or more of the exogenous factors further exerting a direct effect on the respective performance metric.

References

Adjei, M. T., Griffith, D. A., & Noble, S. M. (2009). When do relationships pay off for small retailers? Exploring targets and contexts to understand the value of relationship marketing. Journal of Retailing, 85(4), 493–501.

Ailawadi, K. L., Dant, R. P., & Grewal, D. (2004). The difference between perceptual and objective performance measures: an empirical analysis. Cambridge: Marketing Science Institute.

Aksoy, L., Cooil, B., Groening, C., Keiningham, T., & Yalcin, A. (2008). The long-term stock market valuation of customer satisfaction. Journal of Marketing, 72(4), 105–122.

Anderson, E. W., Fornell, C., & Lehmann, D. R. (1994). Customer satisfaction, market share and profitability: findings from Sweden. Journal of Marketing, 58(3), 53–66.

Anderson, E. W., Fornell, C., & Mazvancheryl, S. (2004). Customer satisfaction and shareholder value. Journal of Marketing, 68(4), 172–185.

Barger, P. B., & Grandey, A. A. (2006). Service with a smile and encounter satisfaction: emotional contagion and appraisal mechanisms. Academy of Management Journal, 49(6), 1229–1238.

Becker, B. J. (2009). Model-based meta-analysis. In H. Cooper, L. Hedges, & J. Valentine (Eds.), The handbook of research synthesis and meta-analysis (pp. 377–395). New York: Russell Sage Foundation.

Beckers, S. F., van Doorn, J., & Verhoef, P. C. (2017). Good, better, engaged? The effect of company-initiated customer engagement behavior on shareholder value. Journal of the Academy of Marketing Science, 45(3), 1–18.

Bendle, N. T., & Butt, M. N. (2018). The misuse of accounting-based approximations of Tobin’s q in a world of market-based assets. Marketing Science, 37(3), 484–504.

Bergkvist, L., & Rossiter, J. R. (2007). The predictive validity of multiple-item versus single-item measures of the same constructs. Journal of Marketing Research, 44(2), 175–184.

Bharadwaj, S. G., & Mitra, D. (2016). Satisfaction (Mis)pricing revisited: real? Really big? Journal of Marketing, 80(5), 116–121.

Bharadwaj, S. G., & Varadarajan, R. (2004). Toward an integrated model of business performance. In N. K. Malhotra (Ed.), Review of marketing research (pp. 207–243). Armonk: M. E. Sharpe.

Blundell, R., Griffith, R., & Van Reenen, J. (1999). Market share, market value and innovation in a panel of British manufacturing firms. The Review of Economic Studies, 66(3), 529–554.

Bolton, R. N. (1998). A dynamic model of the duration of the customer’s relationship with a continuous service provider: the role of satisfaction. Marketing Science, 17(1), 45–65.

Borenstein, S. (1991). Selling costs and switching costs: explaining retail gasoline margins. RAND Journal of Economics, 22(3), 354–369.

Borenstein, M., Hedges, L. V., Higgins, J. P. T., & Rothstein, H. R. (2009). Introduction to meta-analysis. Chichester: Wiley.

Bradburd, R. M., & Caves, R. E. (1982). A closer look at the effect of market growth on industries' profits. The Review of Economics and Statistics, 64(4), 635–645.

Brown, S., & Lam, S. (2008). A meta-analysis of relationships linking employee satisfaction to customer responses. Journal of Retailing, 84(3), 243–255.

Buzzell, R. D., & Wiersema, F. D. (1981). Modelling changes in market share: a cross-sectional analysis. Strategic Management Journal, 2(1), 27–42.

Cai, G. (2010). Channel selection and coordination in dual-channel supply chains. Journal of Retailing, 86(1), 22–36.

Camisón, C., & Forés, B. (2010). Knowledge absorptive capacity: new insights for its conceptualization and measurement. Journal of Business Research, 63(7), 707–715.

Churchill, G. A., & Surprenant, C. (1982). An investigation into the determinants of customer satisfaction. Journal of Marketing Research, 19(4), 491–504.

Cohen, J. (1988). Statistical power analysis for the behavioral sciences (2nd ed.). Hillsdale: Erlbaum.

Cotterill, R. W., & Putsis, W. P. (2000). Market share and price setting behavior for private labels and national brands. Review of Industrial Organization, 17(1), 17–39.

De Haan, E., Verhoef, P. C., & Wiesel, T. (2015). The predictive ability of different customer feedback metrics for retention. International Journal of Research in Marketing, 32(2), 195–206.

Doorley, T. L., & Donovan, J. M. (1999). Value-creating growth: how to lift your company to the next level of performance. San Francisco: Jossey-Bass.

Dunlap, W. P. (1999). A program to compute McGraw and Wong’s common language effect size indicator. Behavior Research Methods, Instruments, & Computers, 31(4), 706–709.

Edvardsson, B., Jognson, M. D., Gustafsson, A., & Strandvik, T. (2000). The effects of satisfaction and loyalty on profits and growth: products versus services. Total Quality Management, 11(7), 917–927.

Eisend, M. (2015). Have we progressed marketing knowledge? A meta-meta-analysis of effect sizes in marketing research. Journal of Marketing, 79(3), 23–40.

Falk, T., Hammerschmidt, M., & Schepers, J. J. L. (2010). The service quality-satisfaction link revisited: exploring asymmetries and dynamics. Journal of the Academy of Marketing Science, 38(3), 288–302.

Fornell, C. (1992). A national customer satisfaction barometer: the Swedish experience. Journal of Marketing, 55(1), 1–21.

Fornell, C., Mithas, S., Morgenson, F. V., III, & Krishan, M. S. (2006). Customer satisfaction and stock prices: high returns, low risk. Journal of Marketing, 70(1), 1–14.

Fornell, C., Morgeson, F. V., III, & Hult, G. T. M. (2016a). An abnormally abnormal intangible: stock returns on customer satisfaction. Journal of Marketing, 80(5), 122–125.

Fornell, C., Morgeson, F. V., III, & Hult, G. T. M. (2016b). Stock returns on customer satisfaction do beat the market: gauging the effect of a marketing intangible. Journal of Marketing, 80(5), 92–107.

Gatignon, H., & Hanssens, D. M. (1987). Modeling marketing interactions with application to salesforce effectiveness. Journal of Marketing Research, 24(3), 247–257.

Geyskens, I., Stenkamp, J., & Kumar, N. (1999). A meta-analysis of satisfaction in marketing channel relationships. Journal of Marketing Research, 36(2), 223–238.

Grewal, R., Chandrashekaran, M., & Citrin, A. (2010). Customer satisfaction heterogeneity and shareholder value. Journal of Marketing, 47(4), 612–626.

Grewal, D., Puccinelli, N., & Monroe, K. B. (2018). Meta-analysis: integrating accumulated knowledge. Journal of the Academy of Marketing Science, 46(1), 1–22.

Gruca, T., & Rego, L. (2005). Customer satisfaction, cash flow, and shareholder value. Journal of Marketing, 69(3), 115–130.

Harbord, R. M., & Higgins, J. P. (2008). Meta-regression in Stata. Meta, 8(4), 493–519.

Hartung, J., Knapp, G., & Sinha, B. K. (2011). Statistical meta-analysis with applications (Vol. 738). Hoboken: Wiley.

Higgins, J. P. T., Thompson, S. G., Deeks, J. J., & Altman, D. G. (2003). Measuring inconsistency in meta-analyses. BMJ [British Medical Journal], 327(7414), 557–560.

Homburg, C., Koschate, N., & Hoyer, W. D. (2005). Do satisfied customers really pay more? A study of the relationship between customer satisfaction and willingness to pay. Journal of Marketing, 69(2), 84–96.

Homburg, C., Allmann, J., & Klarmann, M. (2014). Internal and external price search in industrial buying: the moderating role of customer satisfaction. Journal of Business Research, 67(8), 1581–1588.

Hurley, R. F., & Estelami, H. (1998). Alternative indexes for monitoring customer perceptions for services quality: a comparative evaluation in retailing. Journal of the Academy of Marketing Science, 26(3), 209–221.

Jacobson, R., & Mizik, N. (2009). Rejoinder—customer satisfaction-based mispricing: issues and misconceptions. Marketing Science, 28(5), 836–845.

Jak, S. (2015). Meta-analytic structural equation modelling. New York City: Springer.

Johnson, M. S., Garbarino, E., & Sivadas, E. (2006). Influences of customer differences of loyalty, perceived risk and category experience on customer satisfaction ratings. International Journal of Market Research, 48(5), 601–622.

Jones, M. A., & Suh, J. (2000). Transaction-specific satisfaction and overall satisfaction: an empirical analysis. Journal of Services Marketing, 14(2), 147–159.