Abstract

We examine whether an increase in ETF ownership is accompanied by a decline in pricing efficiency for the underlying component securities. Our tests show an increase in ETF ownership is associated with (1) higher trading costs (bid-ask spreads and market liquidity), (2) an increase in “stock return synchronicity,” (3) a decline in “future earnings response coefficients,” and (4) a decline in the number of analysts covering the firm. Collectively, our findings support the view that increased ETF ownership can lead to higher trading costs and lower benefits from information acquisition. This combination results in less informative security prices for the underlying firms.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Traditional noisy rational expectations models with costly information feature agents who expend resources to become informed. These informed agents earn a return on their information acquisition efforts by trading with the uninformed, and as they do so, the information they possess is incorporated into prices.Footnote 1 In many of these models, the supply of uninformed traders adjusts to provide just sufficient reward for costly efforts in information acquisition and processing. The equilibrium between cost constraints faced by informed traders and gains from trading against the uninformed is reflected in the level of informational efficiency of security prices in the market. The inherent tension between the efficiency with which firm-specific information is incorporated into stock prices and the incentives needed to acquire that information and disseminate it is central to understanding the informational role of security prices (e.g., Hayek 1945; Grossman 1989).

This paper employs exchange traded fund (ETF) ownership data to examine the economic linkages between the market for firm-specific information, the market for individual securities, and the role of uninformed traders. Specifically, we investigate whether an increase in ETF ownership is associated with a decline in the informational efficiency (or “pricing efficiency”) of the individual component securities underlying the fund.Footnote 2 In frictionless markets, a firm’s ownership structure should have little to do with the informational efficiency of its share price. However, as we argue below, market frictions related to information acquisition costs can cause ownership by ETFs to be a significant economic event, with direct consequences for the informational efficiency of the underlying securities.

Our central conjecture is that ETF ownership can influence a stock’s informational efficiency through its impact on the number of underlying shares available for trading to individual investors and the supply of uninformed traders willing to trade these securities. As ETF ownership grows, an increasing proportion of the outstanding shares for the underlying security becomes “locked up” (held in trust) by the fund sponsor. Although these shares are available for trade as part of a basket transaction at the ETF level, they are no longer available to traders who wish to transact on firm-specific information. Even more importantly, ETFs offer an attractive alternative investment vehicle for uninformed (or “noise”) traders, who would otherwise trade the underlying component securities.Footnote 3 As ETF ownership increases, some uninformed traders in the underlying securities migrate toward the ETF market. Over time, this migration creates a steady siphoning of firm-level liquidity, which in turn generates a disincentive for informed traders to expend resources to obtain firm-specific information.

We propose and test two hypotheses. First, we posit that as ETFs become larger holders of a firm’s shares, trading costs for the underlying securities will increase. This increase in trading costs is associated with a decrease in available liquidity for the component securities owned by ETFs. Second, we posit that the increased trading costs will lead to a general deterioration in the pricing efficiency of the underlying securities. Specifically, we posit that the increased trading costs will deter traders who would otherwise expend resources on information acquisition about that stock. In other words, for firms that are widely held by ETFs, the incentive for agents to seek out, acquire, and trade on firm-specific information will decrease. Over time, this will result in a general deterioration in the firm’s information environment and a reduction in the extent to which its stock price can quickly reflect firm-specific information.Footnote 4

To test these hypotheses, we conduct a series of analyses using a panel of U.S. firm-year observations between 2000 and 2014.Footnote 5 Specifically, for each stock in the panel we collect end-of-year ETF ownership data and examine the effect of changes in ETF ownership on the component securities’: (1) trading costs and (2) various proxies of firm-level pricing efficiency.Footnote 6

In our trading cost tests, we follow prior literature (Goyenko et al. 2009; Corwin and Schultz 2012; Amihud 2002) in using two proxies of firm trading costs—the relative bid-ask spreads, HLSPREAD, and an adjusted measure of the price impact of trades, ILLIQ_N.Footnote 7 After controlling for firm size, book-to-market ratio, share turnover, return volatility, and overall level of institutional ownership, we find that an increase in ETF ownership is associated with an increase in average daily bid-ask spreads of the component securities, measured over the next year. In addition, we show an increase in ETF ownership is associated with lower market liquidity in the underlying securities over the next year.

Our tests show a one percentage point increase in ETF ownership is associated with an increase of 1.6% in the average bid-ask spreads over the next year. At the same time, a one percentage point increase in ETF ownership is associated with an increase of 2% in average absolute returns over the next year. These findings are consistent with those of Hamm (2014), who reports that increased ETF ownership is associated with an increase in the “Kyle Lambda” (a stock illiquidity measure) for the underlying component securities owned by these funds.Footnote 8

To test the information-related effects of ETF ownership, we examine the effect of ETF ownership on two proxies for the extent to which stock prices reflect firm-specific information: (1) stock return synchronicity, SYNCH (the extent to which variation in firm-level stock returns is attributable to movements in market and related-industry returns), and (2) future earnings response coefficient, FERC (the association between current firm-specific returns and future firm earnings). In addition, we examine whether an increase in ETF ownership is associated with a decline in the number of analysts covering the firm.Footnote 9

Our results are broadly consistent with the information-related hypothesis. Specifically, we find that an increase in ETF ownership is accompanied by a decline in the pricing efficiency of the underlying component securities, as measured by either SYNCH or FERC. Our results indicate that a one percentage point increase in ETF ownership is associated with approximately a 9 percentage point increase in the average annual change in return synchronicity. Furthermore, firms experiencing a one percentage point increase in ETF ownership also experience a 14% reduction in the magnitude of their future earnings response coefficients. These results are robust to various model perturbations as well as the inclusion of controls for institutional ownership and a host of other variables prescribed by the literature (Roll 1984; Durnev et al. 2003; Piotroski and Roulstone 2004; Ettredge et al. 2005; Choi et al. 2011). Finally, we also find that an increase in ETF ownership is accompanied by a decline in the number of analysts covering the firm.

It is instructive to compare and contrast our results with the findings reported in a recent working paper by Glosten et al. (2016). Like us, Glosten et al. examine the effect of ETF trading on the informational efficiency of underlying securities. However, they document an increase in information efficiency for firms with increased ETF trading. This evidence suggests that an increase in ETF ownership improves pricing efficiency in the underlying stock. At first blush, these findings seem at odds with ours. However, using the same filtering rules as Glosten et al., we can replicate their findings and reconcile them with our own.

A key difference in the research design between the two studies is in the timing of the ETF trades. While we examine the effect of past changes in ETF ownership on future earning response coefficients (FERCs), Glosten et al.’s tests are focused on the effect of contemporaneous ETF trading on current quarter earnings-response coefficients (ERCs). In other words, they focus the effect of contemporaneous increases in ETF ownership on the market’s ability to incorporate same-quarter earnings. However, we focus on longer-term implications of changes in ETF ownership for the informational environment of the firms.

Their research design is motivated by price discovery theory in market microstructure. A number of studies in that literature suggest trading associated with the ETF-arbitrage mechanism can improve intraday price discovery for the underlying securities (Hasbrouck 2003; Yu 2005; Chen and Strother 2008; Fang and Sang 2012; Ivanov et al. 2013), particularly if the individual securities are less liquid than the ETF. The idea is that traders can respond to earnings news (especially the macro-related component of earnings) more quickly by trading the lower cost ETF instrument. As a result, the price of the ETF may lead the price of the underlying securities in integrating this type of news. Hasbrouck (2003) provides some empirical evidence for this phenomenon using index futures. Glosten et al.’s findings are consistent with this idea in that increases in ETF ownership in a given quarter are associated with higher same-quarter ERCs.

Applying the same data filters as Glosten et al., we also find a positive contemporaneous relation between increases in ETF ownership and the market’s ability to incorporate same-quarter earnings. However, we go further and show that this positive relation holds only when all three variables (stock returns, ETF changes, and earnings) are measured in the same quarter. As we lengthen the time lag between ETF changes and future earnings, the relation turns negative. Moreover, as we increase the time lag between past ETF changes and current returns, the negative relation becomes stronger. In other words, while same-quarter ETF trading seems to improve pricing efficiency, the more salient result over the longer run is that increases in ETF ownership lead to a deterioration in pricing efficiency for the underlying securities.

We also provide some evidence on the differential impact of changes in ETF ownership on the incorporation of “macro-based” versus “firm-specific” components of earnings news. Glosten et al. posit that increased ETF trading can enhance price discovery for information embedded in macro-based component of firm earnings. The idea is that, for this type of earnings news, informed traders would prefer to trade through the ETF, which is low cost venue. To test this conjecture, they parse the earnings of each firm into a macro-based component and a firm-specific component. Their results show that increases in ETF ownership primarily improve the market’s ability to integrate macro-based earnings news. In their tests, the effect of changes in ETF ownership on the association between firm-specific component of earnings and stock returns, ERC, is insignificant.

In contrast, our main hypothesis is that the cost of information arbitrage will increase with ETF ownership. While this effect should reduce firm-specific FERC, it could also reduce the macro-based FERC. This is because as ETF ownership increases, all investors (both informed and uninformed) face higher trading costs and consequently have less incentive to acquire and analyze information about the underlying securities. Therefore, over time, we would expect increased ETF ownership to be associated with lower FERCs on both the macro-based and firm-specific components of earnings.

Our results largely support this hypothesis. First, we replicate the Glosten et al. result using a panel of U.S. firm-quarter observations between 2000 and 2014. Second, we show that in periods following increases in ETF ownership, the correlation between returns and future period macro-based and firm-specific components of earnings is lower. In fact, we find that the negative impact of increased ETF ownership on firms’ FERC is generally more pronounced for the firm-specific component of earnings. Taken together, our findings confirm the Glosten et al.’s finding that ETF trading improves price discovery for the same-quarter macro-based component of a firm’s earnings. However, we also show this positive effect is short-lived. Over the longer term, the primary effect of increases in ETF ownership is to lower both macro-based and firm-specific FERCs. This effect is particularly strong with respect to the firm-specific component of earnings.

Our findings contribute to a growing literature on the economic consequences of basket or index-linked products. The rapid increase in index-linked products in recent years has attracted the attention of investors, regulators, and financial researchers.Footnote 10 A number of prior studies suggest that trading associated with the ETF-arbitrage mechanism can improve intraday price discovery for the underlying stocks (Hasbrouck 2003; Yu 2005; Chen and Strother 2008; Fang and Sang 2012; Ivanov et al. 2013). Other studies highlight concerns related to the pricing and trading of these instruments, including the more rapid transmission of liquidity shocks, higher return correlations among stocks held by same ETFs (Da and Shive 2013; Sullivan and Xiong 2012), greater systemic risk (Ramaswamy 2011), and elevated intraday return volatility (Ben-David et al. 2015; Broman 2013; Krause et al. 2014), particularly during times of market stress (Wurgler 2000).

Our study adds a longer-term informational perspective to this debate. Adopting key insights from information economics (Rubinstein 1989; Subrahmanyam 1991; Gorton and Pennacchi 1993; Bhattacharya and O’Hara 2016; Cong and Xu 2016), we present empirical evidence on how incentives in the market for information can affect pricing in the market for the underlying securities. Our results suggest that ETF ownership can lead to increased trading costs for market participants, which has further consequences for the amount of firm-specific information incorporated into stock prices. While the benefits of ETFs to investors are well understood (Rubinstein 1989), far less is known about other (unintended) economic consequences they may bring to financial markets. Our findings help highlight a potentially undesirable consequence of ETFs.

Evidence presented in this study also provides support for a long-standing prediction of the noisy rational expectations literature. A number of models in this literature (Grossman and Stiglitz 1980; Hellwig 1980; Admati 1985; Diamond and Verrecchia 1981; Verrecchia 1982; Kyle 1985, 1989) predict that, when information is costly to acquire and process, informational efficiency of security prices will vary with the supply of uninformed investors willing to trade these securities. Using the emergence of ETFs, we link the siphoning of firm-level liquidity and an increase in trading costs to a reduction in the incentives for information acquisition and hence lower pricing efficiency.

Lee and So (2015) argue that the study of market efficiency involves the analysis of a joint equilibrium in which all markets need to be cleared simultaneously. Specifically, supply must equal demand in the market for information about the underlying security as well as in the market for the security itself. Our findings provide support for this view and bring into sharp relief the close relationship between the market for component securities and that for information about these securities.

The remainder of our study is organized as follows. In the next section, we provide institutional details on ETFs and describe the link between noise trading and ETFs. In section 3, we develop our main hypotheses and outline our research design. In Section 4, we report the empirical findings, and in section 5, we conclude.

2 Exchange traded funds and noise traders

2.1 Exchange traded funds (ETFs)

In the United States, ETFs are registered under the Investment Company Act of 1940 and are classified as open-ended funds or as unit investment trusts (UITs). Like open-end index funds, in a typical ETF, the underlying basket of securities is defined with the objective of mimicking the performance of a broad market index. But ETFs differ in some important respects from traditional open-end funds. For example, unlike open-end funds, which can only be bought or sold at the end of the trading day for their net asset value (NAV), ETFs can be traded throughout the day much like a closed-end fund.Footnote 11 In addition, ETFs do not sell shares directly to investors. Instead, they only issue shares in large blocks called “creation units” to authorized participants (“APs”) who effectively act as market-makers.

Only the ETF manager and designated APs participate in the primary market for the creation/redemption of ETF shares. At the inception of the ETF, APs buy an appropriate basket of the predefined securities and deliver them to the ETF manager, in exchange for a number of ETF creation units. Investors can then buy or sell individual shares of the ETF from APs in the secondary market on an exchange. Shares of the ETF trade during the day in the secondary market at prices that can deviate from their net asset value (NAV), but the difference is kept in line through an arbitrage mechanism in the primary market. For example, when an ETF is trading at a premium to an AP’s estimate of value, the AP may choose to deliver the creation basket of securities in exchange for ETF shares, which in turn it could elect to sell or keep.

Note that the creation/redemption mechanism in the ETF structure allows the number of shares outstanding in an ETF to expand or contract based on investor demand. As Madhavan and Sobczyk (2014) observe, this creation/redemption mechanism means that “liquidity can be accessed through primary market transactions in the underlying assets, beyond the visible secondary market.” This additional element of liquidity means that trading costs of ETFs are determined by the lower bound of execution costs in either the secondary or primary markets, a factor especially important for large investors” (p. 3). In other words, unlike open-end funds, APs interested in accessing the assets represented by the ETF can now choose to trade either in the secondary ETF market (buy/sell the ETF shares directly) or in the primary market (buy/sell the basket securities).

For other (non-APs) investors, ETFs offer the convenience of a stock (ETFs can be bought and sold throughout the day, like common stocks) along with the diversification of a mutual fund or index funds. (They give investors a convenient way to purchase a broad basket in a single transaction.) Unlike open-end index funds (or other basket securities), ETFs do not require investors to deal directly with the fund itself. The most popular ETFs also tend to be much more liquid than the underlying securities, making them useful instruments for speculators and traders.Footnote 12 Finally, adding to their appeal to traders, ETF shares can also be borrowed and sold short.

In sum, ETFs possess many of the characteristics of what Rubinstein (1989) calls an “ideal market basket vehicle.” In particular, ETFs have a continuous market through time of basket sales and purchases (i.e., they provide reliable cash-out prices prior to commitment to trade) and have low creation costs (i.e., trade execution costs incurred in the original purchase of components of the underlying basket and organization costs). They also enhance tax benefits obtained from positions in the individual components of the basket. Unlike open-end mutual funds, which typically fund shareholder redemptions by selling portfolio securities, ETFs usually redeem investors in-kind. As a result, there is no taxation of unrealized profits from ETF holdings. Additionally, ETFs are offered in small enough units to appeal to small investors (not just to large institutional investors), and they remove all basket-motivated trading away from the individual securities or risks comprising the basket.

We posit these characteristics make ETFs attractive to noise (uninformed) traders who would otherwise trade the underlying securities. Our main conjecture is that, with the rise in ETFs, some noise traders will gravitate to ETFs and away from the underlying stocks, with attendant consequences for the trading costs and pricing efficiency of the underlying securities.

2.2 Noise traders and ETFs

Although noise (uninformed) traders play a prominent role in analytical models, surprisingly little is known about why they trade. The typical noisy rational expectations model (e.g., Kyle 1985; Verrecchia 1982; Admati 1985) abstracts away from this question. In these models, noise traders trade for exogenous reasons unrelated to information. Because their motive is non-informational, noise traders in this literature are also often referred to as “liquidity traders.” This moniker suggests they trade either for consumption or for portfolio-rebalancing reasons, neither of which would necessarily change with the rise of ETFs.

Our analysis can be accommodated within a standard noisy rational expectations (NRE) framework. The key assumption needed is that the cost of becoming informed in a security is increasing with its ETF ownership. As ETF ownership increases, we assert—and our tests show—that the cost of informational arbitrage will also increase. Given increased information costs, NRE models (e.g., Verrecchia 1982; Grossman and Stiglitz 1980) predict a decrease in the security’s pricing efficiency. This robust prediction of the NRE literature is the basis of our main hypothesis.Footnote 13 Note, however, that because the NRE framework provides no motivation for noise trading, it has little to say about why noise trading might migrate to ETFs, rather than to index funds. To address this question, we need to impose additional structure on noise trading.

The noise traders we have in mind are closer to those featured by Black (1986). According to Black, noise traders engage in non-informational trades not primarily for liquidity reasons, but because they either mistakenly think they have superior information or because they find utility from trading itself. In his words: “Noise trading is trading on noise as if it were information. People who trade on noise are willing to trade even though from an objective point of view they would be better off not trading. Perhaps they think the noise they are trading on is information. Or perhaps they just like to trade” (Black 1986, p. 531). This form of noise trading, Black argues, is needed to rationalize the high volume of trading we observe in individual stocks.

With the rise of ETFs, we posit some noise (uninformed) traders who formerly traded the underlying stocks will migrate to these basket instruments instead. They do so because ETFs still allow them to express a view on certain stocks (or stock baskets/substitutes) but at much lower costs. A key difference between ETFs and passive index funds is that ETFs allow noise traders to satisfy their desire to trade (or engage in speculation), while passive index products, by and large, do not. If Black is correct and noise traders do not trade primarily for consumption reasons, ETFs can offer “transactional utility” to these traders in ways that passive index funds cannot.

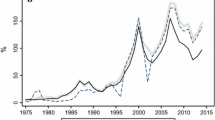

Recent empirical evidence suggests such a migration is indeed taking place. Sullivan and Xiong (2012) find that the average annual growth rate of passively managed assets since the early 1990s is double that of actively managed assets. In recent years, much of this increase has been in the form of ETFs. More importantly, the total value of trading in ETFs far outstrips their share ownership. Figure 1 shows that ETF ownership averaged around 5.5% for our sample firms in recent years. However, as Pisani (2015) observed, total ETF trading is now close to 28% of the total daily value traded on US equity exchanges. In other words, the daily turnover in ETF shares is approximately five times larger than the turnover in the shares of a typical stock. These findings show ETFs are now serving as common trading vehicles and not merely as a way to secure a passive index return.

ETF ownership by year. This chart plots, by fiscal year, the average percentage of shares outstanding held by ETFs for firms in our sample. The horizontal axis indicates the year, and the vertical axis indicates the magnitude of ETF ownership. Our methodology for calculating ETF ownership is outlined in Section 4 of the paper

3 Hypothesis development and research design

The primary goal of this study is to investigate whether an increase in the proportion of firm shares held by ETFs is associated with a decline in the pricing efficiency of the underlying component securities. To address this question, we identify two central dimensions of a firm’s information environment: (1) transactions costs of market participants and (2) the extent to which stock prices reflect firm-specific information. We then predict the effects of ETF ownership on each of these dimensions and construct tests to evaluate these predictions.

We first posit that ETFs serve as attractive substitutes to the underlying component securities for uninformed traders. Because of the trading benefits offered by ETFs, especially to uninformed investors, we expect uninformed investors to gravitate toward ETFs and away from the underlying stocks (Milgrom and Stokey 1982; Rubinstein 1989). As uninformed traders shift toward trading ETFs and away from the underlying securities, transactions costs for trading the those component securities will increase (Subrahmanyam 1991; Gorton and Pennacchi 1993; Madhavan and Sobczyk 2014). The increase in transactions costs will deter market participants from engaging in firm-specific information gathering and will lead to less informative stock prices in the firm-specific component (Grossman and Stiglitz 1980; Admati 1985). Based on the reasoning outlined above, we offer the following hypotheses.

-

H1 : An increase in ETF ownership is associated with higher trading costs for the underlying component securities.

-

H2 : An increase in ETF ownership is associated with deterioration in the pricing efficiency of the underlying component securities.

To test H1, we analyze the relation between changes in ETF ownership and changes in two proxies of liquidity that capture trading costs: (1) bid-ask spreads and (2) an adjusted measure of the price impact of trades (Goyenko et al. 2009). To investigate the relation between changes in ETF ownership and changes in bid-ask spreads, we estimate the following regression.Footnote 14

In Eq. (1), the ∆ operator indicates a change in the value of a particular variable. For example, ∆HLSPREAD it is the difference between firm i’s measure of HLSPREAD during year t and its value in year t-1. HLSPREAD it is the Corwin and Schultz (2012) annual high-low measure of bid-ask spread for firm i over year t. Corwin and Schultz (2012) derive this estimator from the observation that the ratio of high to low observed stock prices (\( \frac{H_t^o}{L_t^o}\Big) \)in a particular period is a function of the bid-ask spread (S), which is a fixed amount, and the “true” unobservable range of high (\( {H}_t^A\Big) \) and low (\( {L}_t^A\Big) \) stock prices, which themselves are functions of the underlying variance of the stock price that varies with the time horizon:

This distinction enables estimation of the spread by using a system of equations in which spread is constant but the time horizon (and consequently the variance) changes. The result spread estimator (S) is defined by the following set of expressions.

We use this measure of bid-ask spread as a proxy for trading costs because it is much less time and data-intensive to calculate than intraday bid-ask spread measures and because Corwin and Schultz (2012) demonstrate that it outperforms the Roll (1984), Lesmond et al. (1999), and Holden (2009) techniques for measuring bid-ask spreads.

The variable of interest in Eq. (1), ∆ETF it − 1, is the change in the percentage of firm i’s shares held by all ETFs from the end of year t-2 to the end of year t-1. Our first hypothesis (H1) predicts that the coefficient β 1 is positive, indicating that, ceteris paribus, increases in ETF ownership are associated with increases in bid-ask spreads. Change in ETF ownership may be correlated with overall change in institutional ownership and prior research suggests there might be a relation between institutional ownership and bid-ask spreads.Footnote 15 To isolate the effect of change in ETF ownership on stock liquidity and ensure our results are not confounded by the relation of ETF ownership with institutional ownership, we include ΔINST it − 1 directly in Eq. (1) as an additional control variable. ΔINST it − 1 is the change in the percentage of firm i’s shares held by all institutions from the end of year t-2 to the end of year t-1. Footnote 16

In Eq. (1), Controls it − 1 represents a vector of firm- and industry-related control variables nominated by the literature. The vector includes the change in the log of market value of equity [∆LN(MVE)] during year t-1 because larger firms generally have smaller bid-ask spreads. Prior studies also find that bid-ask spreads increase with the return volatility and decrease with the share turnover (Copeland and Galai 1983). Accordingly, we control for the change in the annualized standard deviation of daily returns during year t-1 [∆STD(RET)] and the change in average share turnover from year t-2 to year t-1 (∆TURN). We also include the change in book to market ratio (∆BTM) during year t-1 as a control for the effect of financial distress, growth opportunities, or both on bid-ask spreads (Fama and French 1992; Lakonishok et al. 1994). Finally, to control for time and industry trends in bid-ask spreads, we include year and industry fixed effects.Footnote 17 The industry fixed effects are defined based on the 48 Fama and French (1997) industry classification.

As an additional test of H1, we examine the association between changes in ETF ownership and another proxy of a firm’s market liquidity or trading costs: an adjusted measure of the price impact of trades from Amihud (2002). The Amihud (2002) measure of the price impact of trades, also known as the illiquidity ratio, ILLIQ, is the ratio of average daily absolute returns to average daily dollar volume. While ILLIQ is a well-accepted proxy for the price impact of trades (Goyenko et al. 2009), in the context of this paper, using ILLIQ as originally defined to test H1 complicates our analyses. The literature (Hasbrouck 2003; Yu 2005; Chen and Strother 2008; Fang and Sang 2012; Ivanov et al. 2013) shows that ETF ownership can affect both the numerator of the illiquidity ratio (the average daily absolute returns) and its denominator (the average daily dollar volume). In particular, changes in ETF ownership can mechanically induce greater trading volume without conferring an overall improvement in liquidity on the underlying stock (Ben-David et al. 2015). Indeed, during our sample period, the range of changes in volume is an order of magnitude larger than the range of changes in absolute returns. Hence constraining the two components of the illiquidity ratio to share a single coefficient is not appropriate in our study.

To mitigate this problem, we decompose ILLIQ into two components (the numerator and the denominator) and estimate the following regression.

ILLIQ_N it is the daily absolute return for firm i averaged over all the trading days in year t. The dependent variable in Eq. (2), ΔILLIQ_N it , is the change in ILLIQ_N it from year t-1 to year t. ILLIQ_D it is the daily dollar volume for firm i averaged over all the trading days in year t and ΔILLIQ_D it is the change in ILLIQ_D it from year t-1 to year t. ΔETF it − 1 and ΔINST it − 1 are defined above. ΔControls it − 1 denotes several control variables measured as of the end of year t-1. Specifically, it includes the log of market value of equity [LN(MVE)] as of the end of year t-1, because we expect larger firms to exhibit smaller price impact of trades. In addition, ΔControls it − 1 contains the change in book-to market-ratio (ΔBTM) during year t-1 to control for the effects of financial distress, growth opportunities, or both on ΔILLIQ_N it . In our estimation of Eq. (2), we also include year and industry fixed effects. Our hypothesis predicts that the coefficient β 1 is positive, indicating that ceteris paribus increases in ETF ownership are associated with increases in absolute returns (and hence lower liquidity or higher trading costs for market participants).

Our second hypothesis (H2) states that an increase in ETF ownership is associated with deterioration in pricing efficiency of the underlying component security. We test this hypothesis using two proxies for the extent to which stock prices reflect firm-specific information: (1) stock return synchronicity, SYNCH, and (2) future earnings response coefficient, FERC. SYNCH is a measure of the extent to which variation in firm-level stock returns is explained by movements in market and related-industry returns. Roll (1984) posits that, when greater relative levels of firm-specific information are being impounded into stock prices, the magnitude of the stock return synchronicity measure decreases. Wurgler (2000), Durnev et al. (2003), Durnev et al. (2004), and Piotroski and Roulstone (2004) use this insight and provide evidence in support of it in a variety of settings. Because stock return synchronicity relates negatively to the amount of firm-specific information embedded in stock price, based on H2, we predict that changes in ETF ownership lead to positive changes in stock return synchronicity.

To estimate firm-specific measures of stock return synchronicity, SYNCH it , we follow the methodology outlined by Durnev et al. (2003). First, for each firm-year observation we obtain the adjusted coefficient of determination (adjusted R 2) by regressing daily stock returns on the current and prior day’s value-weighted market return (MKTRET) and the current and prior day’s value-weighted Fama and French 48-industry return (INDRET):

In Eq. (3), RET id is firm i’s stock return on day d, MKTRET d is the value-weighted market return on day d, and INDRET d is the value-weighed return of firm i’s industry, defined using the Fama-French 48 classifications, on day d. Footnote 18 Eq. (3) is estimated separately for each firm-year, using daily returns for firm i over the trading days in year t, with a minimum of 150 daily observations.

Next, for each firm-year observation, we calculate the annual measure of stock return synchronicity, SYNCH it , as the logarithmic transformation of \( {R}_{it}^2 \) to create an unbounded continuous measure of synchronicity (Piotroski and Roulstone 2004; Gow et al. 2010; Crawford et al. 2012; Hutton et al. 2009)Footnote 19: \( {SYNCH}_{it}=\mathit{\log}\left(\frac{R_{it}^2}{1-{R}_{it}^2}\right) \). High values of the SYNCH it measure indicate that a greater fraction of variation in firm-level stock returns is explained by variations in market and related-industry returns.

To test whether an increase in ETF ownership is accompanied by a decline in the amount of firm-specific information that is being impounded into stock prices, we estimate the following equation.

In Eq. (4), ∆SYNCH it is the difference between firm i’s measure of SYNCH during year t and its value in year t-1. ΔControls it − 1 indicates several annual change measures that research suggests are associated with changes in stock return synchronicity. Following Jin and Myers (2006), we control for changes in the skewness of firm i’s returns over year t-1 (ΔSKEW). In addition, since Li et al. (2014) show that synchronicity is often confounded with systematic risk, we include the annual change in CAPM beta as a control for a firm’s systematic risk. As additional controls, we include annual changes during year t-1 in the log of market value of equity [ΔLN(MVE)], book-to-market ratio (ΔBTM), average share turnover (ΔTURN), and year and industry fixed effects. ΔETF it − 1 and ΔINST it − 1 are defined and measured as in Eqs. (1) and (2). Our second hypothesis predicts that the coefficient β 1 is positive, indicating that, ceteris paribus, increases in ETF ownership are associated with increases in stock return synchronicity.

Our second proxy for the extent to which stock prices reflect firm specific information is the future earnings response coefficient, which measures the extent to which current stock returns reflect future firm earnings. To test whether an increase in ETF ownership is accompanied by a decline in the extent to which firm-level stock returns reflect future firm earnings, we follow the literature (e.g., Kothari and Sloan 1992; Collins et al. 1994; Choi et al. 2011) and estimate several versions of the following regression model.

In Eq. (5), RET it represents firm-level stock returns during year t, and EARN it − 1, EARN it , and EARN it + 1 denote firm-level net income before extraordinary items during years t−1, t, and t + 1, scaled by market value of equity. The coefficient β 3 measures the relation between current firm-level stock returns and future firm earnings; prior research refers to this coefficient as the “future earnings response coefficient” (FERC) and offers it as a measure of the extent to which current stock returns reflect/predict future firm earnings (Lundholm and Myers 2002; Ettredge et al. 2005; Choi et al. 2011). To address our main research question, we include as explanatory variables the level of ETF ownership (ETF it − 1) at the end of year t - 1 as well as the interaction between the level of ETF ownership and past, current, and future earnings (ETF it − 1 × EARN it ± j ). Our second hypothesis predicts that the coefficient on the interaction of ETF ownership with current and future firm earnings is negative, indicating that FERCs are lower for firms with higher ETF ownership (i.e., β 7 and, more importantly, β 8 are negative).

As in previous equations, Controls it denotes a number of control variables suggested by research. Following Collins et al. (1994), we control for future firm-level stock returns, RET it + 1, to address the potential measurement error induced by using actual future earnings as a proxy for expected future earnings. In addition, to account for the effect of a firm’s growth on the ability of its stock returns to reflect future earnings, we control for total asset growth from year t-1 to year t, ATGROWTH t . Also, we control for the possibility that firms experiencing losses may have lower FERCs by including an indicator variable, LOSS t , that equals 1 if the firm experiences a loss in year t + 1 (i.e., EARN it + 1 < 0) and 0 otherwise. Controls it also includes the natural logarithm of market value of equity at the end of year t.

We also examine how FERCs vary with changes in ETF ownership by decomposing the level of ETF ownership at the end of period t-1 into the sum of the level of ETF ownership at the end of period t-2 and the change in ETF ownership during period t-1: ETF t − 1 = ETF t − 2 + ΔETF t − 1

Thus we re-estimate Eq. (5) using ETF t − 2 and ΔETF t − 1 in lieu of ETF t − 1:

In estimating Eq. (6), we expect that β 7 and β 8 – the coefficients on the interactions of lagged levels of ETF ownership with current and future firm earnings (i.e., ETF t − 2 × EARN t and ETF t − 2 × EARN t + 1) – as well as β 10 and β 11 – the coefficients on the interactions of lagged changes in ETF ownership with current and future firm earnings (i.e., ΔETF t − 1 × EARN t and ΔETF t − 1 × EARN t + 1) − are negative.

The consequences of changes in ETF ownership on stock pricing efficiency may differ for “macro-based” (systematic or aggregate) and “firm-specific” (or idiosyncratic) components of earnings. To test this conjecture, we follow the procedure of Glosten et al. and decompose total earnings into “macro-based” and “firm-specific” components by estimating the following regression.

In Eq. (7), EARNMKT t is the size-weighted average of year t earnings before extraordinary items for all firms with available earnings information in Compustat. EARNIND t is the size-weighted average of year t earnings before extraordinary items for all firms with the same Fama-French 48-industry classification.

For each firm-year, we define the systematic or aggregate portion of earnings (EARNAGG it ) as the fitted value from the annual estimation of Eq. (7). The residual portion is defined as the idiosyncratic or firm-specific portion of earnings (EARNFIRM it ). Using these components of earnings, we estimate the following modified version of Eq. (5).

With the exception of EARNAGG it and EARNFIRM it , all variables in Eq. (8) remain as defined in Eq. (6). H2 predicts that the coefficients on the interaction of lagged ETF ownership measures with current and future macro-based and firm-specific earnings will be negative (i.e., β 10, β 11, β 16, and β 17 for macro-based earnings; β 13, β 14, β 19, and β 20 for firm-specific earnings).

As an additional test of H2, we examine how ETF ownership relates to the number of analysts covering the firm during a year. H2 predicts that higher ETF ownership will lead to lower incentives for information acquisition for the underlying securities. To the extent that analysts are drawn to firms that are more attractive to individual investors, we expect that firms with increases in ETF ownership will experience reductions in analyst coverage. To test this conjecture, we estimate several versions of the following equation.

In Eq. (9), ΔANALYST it is the change from year t-1 to year t in the number of unique analysts on I/B/E/S providing forecasts of firm i’s one-year-ahead earnings. As before, ΔControls it − 1 represents annual changes in a number of control variables, measured as the change in the level of each variable from year t-2 to year t-1, which are suggested by the literature. Barth et al. (2001) demonstrate that firms with large research and development expenses or intangible assets experience greater analyst coverage. Accordingly, we include the annual change in the proportion of research and development expenses, relative to total operating expenses (ΔRD_F it-1 ), and the annual change in the proportion of intangible assets, relative to total assets (ΔINTAN_F it-1 ), as controls. Following Lang and Lundholm (1996), we also control for annual change in return volatility [ΔSTD(RET) it-1 ]. To capture the effect of stock return momentum on levels of analyst coverage, we control for prior firm-level six-month equity returns (MOM it-1 ), measured as of the end of year t-1. Eq. (9) also includes controls for firm size [LN(MVE)], change in book-to-market ratio (ΔBTM), and change in share turnover (ΔTURN). Our second hypothesis predicts that the coefficient β 1 is negative, indicating that, ceteris paribus, changes in ETF ownership are associated with decline in number of analysts covering a firm.

To control for potential time-series as well as cross-sectional correlations between firm-specific measures, we base our inferences from all equations on t-statistics calculated using standard errors clustered by both firm and year (e.g., Gow et al. 2010). All variables used in the estimation of Eqs. (1) to (9) are also defined in Appendix Table 8.Footnote 20

4 Empirical analyses

4.1 Sample construction and descriptive statistics

We determine year-end ETF ownership by first using CRSP, Compustat, and OptionMetrics databases to identify all ETFs traded on the major U.S. exchanges. Specifically, we identify ETFs as securities on CRSP with a share code of “73” and securities on Compustat or OptionMetrics with an issue type of “%.” After identifying candidate ETFs, we obtain for each ETF the reported equity holdings from the Thomson Financial S12 database. For some ETFs, the Thomson Financial S12 database does not provide regular reporting of equity holdings. In these instances, we hand collect additional holdings data from Bloomberg Financial. ETFs without any reported holding data in the Thomson Financial database or Bloomberg Financial are excluded from the sample. This process yields a sample of 443 unique ETFs. Appendix Table 9 provides a list of the 10 largest ETFs in our sample, ranked based on the average assets under management.

Using the annual panel of holdings for each ETF we define, for every stock in a given year, the ETF ownership variable (ETF) as the aggregate number of shares held by all ETFs divided by total number of shares outstanding in that year. We repeat this process for every firm-year between 2000 and 2014 to construct our panel. Our sample begins in 2000 because it is the first year with sufficient variation in ETF ownership to conduct our analyses. Our sample ends in 2014 due to data availability constraints. All firm-years with no reported ETF ownership during the sample period are included in the sample with ETF it = 0.

Figure 1 reports the average ETF ownership across firms for each year of our sample. The figure reveals a significant increase in average ETF ownership over our sample period, from roughly 1% in 2000 to nearly 5.5% in 2014. This is consistent with the rapid increase in the dollar value of ETF trading as a percentage of total exchange dollar value traded. For example, during June 2015, the total value of ETF trading represented close to 28% of the total daily exchange value traded (Pisani 2015), which represents a 35% increase in percentage of value of ETF trading from June 2014. Clearly ETFs have quickly become an important vehicle for traders in the equity market.

We obtain market-related data on all US-listed firms from CRSP and accounting data from Compustat. To be included in our sample, each firm-year observation must have information on stock price, number of shares outstanding, and book value of equity. We also require sufficient data to calculate the standard deviation of daily returns and average share turnover within each firm year. We restrict our analyses to firms with nonnegative book-to-market ratios in every year of our sample period. This results in a sample of 39,863 firm-years and 5992 unique firms. In some of our analyses, we also require annual data on analyst coverage. In such analyses, our sample size is reduced to 29,562 firm-year observations and 4184 unique firms. The number of observations included in each regression varies according to data availability.

Panel A of Table 1 presents descriptive statistics for the main variables used in the analyses. Of particular interest for our analyses is the level of ETF ownership, measured as a percentage of total shares outstanding held by all ETFs, and changes in ETF ownership. The mean (median) percentage ETF ownership is 3.31% (2.52%). This is much lower than the level of institutional ownership, which has a mean (median) of 57.78% (62.50%). We also observe consistently larger annual changes in institutional ownership relative changes in ETF ownership. The mean (median) change in ETF ownership is 48 (27.7) basis points, while the mean (median) change in institutional ownership is 264 (109) basis points. The distributional statistics of both ETF and institutional ownership in our sample are consistent with the literature (Hamm 2014; Jiambalvo et al. 2002). Nevertheless, we expect the two measures to differ in many important respects and have different effects on measures of trading costs and pricing efficiency.

Panel A also reveals that ∆ILLIQ_N and ∆ILLIQ_D, the two components of changes in the Amihud (2002) illiquidity ratio, have notably different variances. ∆ILLIQ_N is very narrowly distributed with a standard deviation of 0.801, while ∆ILLIQ_D exhibits a significantly larger standard deviation of 15.661. This difference provides further support for our decision to decompose the Amihud (2002) ratio into its two components in an attempt to estimate the effect of changes in ETF ownership on ∆ILLIQ_N controlling for ∆ILLIQ_D.

Table 1, panels B and C, present Pearson and Spearman correlation coefficients between the key levels and changes of variables in our regression analysis. In our sample, ∆ETF is positively correlated with changes in book-to-market ratio (Pearson coef. = 0.022) and turnover (Pearson coef. = 0.07). Panel B reveals that ∆ETF is positively correlated with two proxies of changes in trading costs, ∆HLSPREAD (Pearson coef. = .171) and ∆ILLIQ_N (Pearson coef. = 0.193). Consistent with our hypotheses, ∆ETF is also positively correlated with ∆SYNCH (Pearson coef. = 0.080) and negatively correlated with ∆ANALYST (Pearson coef. = −0.005).

4.2 Testing H1: ETF ownership and trading costs of market participants

Tables 2 and 3 present regression summary statistics from the estimation of Eqs. (1) and (2), which are designed to test our first hypothesis using two measures of liquidity that capture trading costs and various model specifications.

Column 1 of Table 2 reveals that change in bid-ask spread, ΔHLSPREAD, exhibits the expected relations with our control variables. ΔHLSPREAD is negatively associated with increases in firm size (coef. = −0.044, t-stat. = −1.67), positively associated with increases in the book-to-market ratio (coef. = 0.051, t-stat. = 2.42), and positively associated with increases in return volatility (coef. = 0.001, t-stat. = 1.86). According to column 1 of Table 2, changes in ETF ownership are positively related to changes in bid-ask spreads (coef. = 0.016, t-stat. = −2.41). This finding supports our hypothesis that, ceteris paribus, the trading costs of market participants increase with changes in ETF ownership. To ensure that the results in column 1 are not confounded by the relation between changes in institutional ownership with ΔHLSPREAD and with ΔETF, we estimate column 1, controlling for ΔINST. Column 2 reveals that, consistent with H1, there exists a significantly positive association between changes in ETF ownership and changes in HLSPREAD (coef. = 0.017, t-stat. = 2.51). The average HLSPREAD in our sample is 1.07%. Thus these results show that a one percentage point increase in ETF ownership is associated with an increase of 1.6% in the average HLSPREAD over the next year. The coefficient on institutional ownership is slightly negative and not significantly different from 0 (coef. = −0.000, t-stat. = −0.58). These results are wholly consistent with the findings of Hamm (2014) and suggest that her findings extend to our longer horizon.

Results from estimating Eq. (2) are presented in Table 3 and provide evidence on the association between changes in of ETF ownership and another measure of changes in trading costs. Column 1 reveals that ΔILLIQ_N has a strong positive association with changes in book-to-market ratio (coef. = 0.172, t-stat. = 4.20) and changes in ILLIQ_D (coef. = 0.004, t-stat. = 5.38). The results in column 1 also reveal a strong positive relation between changes in ETF ownership and changes in ILLIQ_N (coef. = 0.042, t-stat. = 2.55), suggesting that increases in ETF ownership are associated with increases in the absolute firm returns. Column 2 of Table 3 reveals that controlling for ΔINST does not alter this observed relation. The average daily absolute return in our sample is 2.1%, indicating that a one percentage point increase in ETF ownership is associated with an increase of 2% in average daily absolute returns over the next year. Taken together, the results presented in Tables 2 and 3 provide strong evidence in support for H1 that an increase in ETF ownership is accompanied by an increase in trading costs for market participants.

4.3 Testing H2: ETF ownership and the deterioration of pricing efficiency

4.3.1 Synchronicity and FERC tests

Tables 4 and 5 present regression summary statistics from the estimation of Eqs. (4) and (5), which are designed to test our second hypothesis using two proxies for the extent to which stock returns reflect firm-specific information. Table 4 presents summary statistics from the estimation of two versions of Eq. (4), which models the relation between changes in ETF ownership and changes in annual stock return synchronicity. Column 1 reveals that the changes in synchronicity, ΔSYNCH, exhibit the expected relations with our control variables. Consistent with prior research (e.g., Li et al. 2014), ΔSYNCH is positively associated with increases in firm size (coef. = 0.595, t-stat. = 8.78) and negatively associated with changes in systematic risk, ΔBETA (coef. = −0.704, t-stat. = −14.85). Columns 1 and 2 reveal that changes in ETF ownership are significantly positively related to changes in stock return synchronicity (coef. = 0.090, t-stat. = 3.70 and 3.67). As is shown in column 2, controlling for changes in institutional ownership does not affect the positive association between ΔETF and ΔSYNCH. Our results indicate that a one percentage point increase in ETF ownership is associated with approximately a 9 percentage point increase in the average annual change in return synchronicity. This finding supports our hypothesis that increases in ETF ownership are associated with a deterioration of pricing efficiency for the underlying component securities.

Table 5 presents regression summary statistics from the estimations of Eqs. (5), (6), and (8), which are designed to examine the relation between ETF ownership and the extent to which current firm-level returns reflect future firm or macro-based and firm-specific earnings. In these estimations, measures of ETF ownership range from 0 to 1 (rather than from 0 to 100) to be more similar in ranges of magnitudes of the earnings and returns measures. Consistent with the literature, in both columns of Panel A, we observe a positive future earnings response coefficient, FERC (coef. = 0.015, t-stat. = 4.80 and 4.32). Consistent with H2, column 1 of panel A reveals that the interactions of current and future earnings with ETF ownership carry negative coefficients that are significantly different from 0 (coef. = −3.662, t -stat. = −2.60 and coef. = −0.212, t-stat. = −4.64). This suggests that, controlling for INST t-1 and a host of other variables prescribed by prior literature (LOSS t , ATGROWTH t , RET t+1 , LN(MVE) t-1 ), firms with higher levels of ETF ownership experience lower future earnings response coefficients. In other words, firm-level returns of firms with higher levels of ETF ownership incorporate less future earnings-related information. Column 2 of panel A presents summary statistics from the estimation of Eq. (6) in which the level of ETF ownership is split into lagged level of ETF ownership and most recent period change in ETF ownership. The results in column 2 further support H2 by showing that the coefficients on interactions of current and future earnings with changes in ETF ownership are also significantly negative (coef. = −3.636, t-stat. = −2.68 and coef. = −0.195, t-stat. = −2.07). This suggests that firms experiencing a one percentage point increase in ETF ownership also experience a 14% reduction in the average magnitude of their future earnings response coefficients.

Taken together, the results presented in Tables 4 and 5 indicate that an increase in ETF ownership is associated with increase in the co-movement of firm-level stock returns with market and related-industry stock returns and with a decline in the predictive power of current firm-level stock returns for future firm earnings. These two findings support our second hypothesis that stock prices of firms with high ETF ownership are impounding less firm-specific information.

4.3.2 Alternative earnings response tests

In a contemporaneous study, Glosten et al. (2016) explore the impact of ETF trading activity on the response of returns to contemporaneous earnings news. Using same-quarter changes in ETF ownership as a proxy for ETF trading activity, they demonstrate that ETF trading is associated with a stronger association of returns to contemporaneous earnings. They further document that the effect is concentrated in the association of returns to the systematic (or macro-based) component of earnings news. Their conclusion is that ETF trading improves a stock’s informational efficiency.

Given the difference in their conclusions and ours, we take several steps to reconcile the findings. The first key difference between their setting and ours is rooted in the time lag between measurement of changes in ETF ownership, returns, and firm earnings. Because they focus on understanding the impact of contemporaneous ETF trading, they measure changes in ETF ownership and returns over the exact same quarter. In contrast, we are interested in understanding the long-run implications of increases in ETF ownership on pricing efficiency, so we measure levels and changes of ETF ownership prior to the start of the returns measurement window. To verify that this shift in ETF measurement window is a key driver of the differences between our results and theirs, we estimate Eq. (8) while measuring changes in ETF ownership and earnings contemporaneously with returns, as they do.

Column 1 of Table 5, panel B, presents the results of this estimation. The results show that the coefficients on the variables of interest (the interaction of ΔETF with contemporaneous aggregate and firm-specific earnings) are positive, consistent with the findings reported by Glosten et al. To ensure that the effect they documented does not subsume those reported in our FERC analyses, we also estimate Eq. (8) including both the Glosten et al. measurement of ΔETF and our original measurement of ΔETF. The summary statistics from this estimation are presented in column 2 of Table 5, panel B. This test shows that all our prior findings on a reduction in FERCs with increased ETF ownership continue to hold, after controlling for the Glosten et al. variables. Specifically, all eight of the interaction terms between ETF ownership and future earnings measures have negative coefficients. In particular, the coefficient of lagged changes in ETF ownership with future firm-specific earnings is significantly negative (coef. = −0.172, t-stat. = −3.26), as is the interaction of the lagged level of ETF ownership with future firm-specific earnings (coef. = −0.136, t-stat. = −2.02). These results support our hypothesis that increases in ETF ownership lead to slower incorporation of firm-specific earnings information into stock prices.

The analyses presented in panel B of Table 5 demonstrate the importance of lagging the changes in ETF ownership variable, which is a key difference between our study and Glosten et al.’s. However, there are other research design differences that might have contributed to the differences in results (such as annual versus quarterly data, the measurement window for future earnings, the choice of control variables, and their use of seasonally adjusted earnings). To address these differences more completely, we re-estimate the main results from Glosten et al.’s Eq. (3) following their research design and sample construction.

The summary statistics from this estimation are presented in column I of Table 6. Their main variable of interest is the interaction of the contemporaneous quarterly change in ETF ownership (δETF t ) with current period seasonally adjusted earnings (SEARN t ). For firm i in quarter t, SEARN it , seasonally adjusted earnings news, is defined as the difference between quarter t and quarter t-4 earnings before extraordinary items, scaled by stock price at the beginning of quarter t. Consistent with the results reported by Glosten et al., our estimate of the coefficient on the interaction δETF t × SEARN it is positive and significantly different from zero (coef =0.438, t-stat. = 2.458).

Having successfully replicated the results reported by Glosten et al., we further explore how research design modifications affect the gap between their results and ours. The estimates in columns II through VII of Table 6 are from re-estimations of their Eq. (3) with modifications to the measurement windows of δETF and SEARN. Specifically, in column II, we hold all other aspects of the research design constant (and consistent with Glosten et al.) but allow for the measurement of δETF to take place prior to the return measurement window, rather than in the same quarter as the stock returns. In other words, we shift from δETF t to δETF t-1 . Making this shift causes the magnitude of the coefficient on the interaction of δETF t-1 with SEARN to decline (coef. = 0.386 versus 0.438) and also causes the statistical significance to fall (t-stat. = 1.729 versus 2.458).

The next modification we examine is the effect of measuring annual changes in ETF ownership rather than quarterly. We accomplish this by summing quarterly changes over the prior four quarters. We use this four-quarter sum of ETF ownership changes (δETF SUM t-1 to t-4 ), instead of the contemporaneous ETF ownership change, in the estimation results presented in column III of Table 6. The results in column III reveal that measuring ETF changes annually notably changes the inferences of the test, as the interaction of δETF SUM t-1 to t-4 with SEARN is positive (coef = .101) but not significantly different from zero (t-stat. = 0.767).

In columns IV through VII, we maintain use of the four-quarter sum of quarterly ETF ownership changes (δETF SUM t-1 to t-4 ) as an annual measure of changes in ETF ownership. The variation in columns IV through VII arises from shifting forward the measurement of SEARN. In column IV (V, VI), SEARN is defined as the quarterly earnings for quarter t + 1 (t + 2, t + 3), relative to the returns measurement window. In each iteration of the estimation, the coefficient on the interaction of δETF SUM t-1 to t-4 with SEARN grows increasingly negative. For example, Column VI shows that when examining three-quarter-ahead earnings, the interaction of δETF SUM t-1 to t-4 with SEARN t+3 bears a significantly negative coefficient (coef. = −0.568, t-stat. = −1.809). This negative interaction effect is consistent with our second hypothesis.

In column VII, we sum the quarterly earnings for quarters t through t + 3 to approximate an annual version of future earnings (SEARN SUM t to t+3 ). Column VII of Table 6 presents estimations where the combined modifications to the measurement of ETF ownership changes and earnings bring the overall specification close to our main FERC test, Eq. (5). Specifically, we use SEARN SUM t to t+3 as an approximation of future annual earnings and δETF SUM t-1 to t-4 as an approximation of annual change in ETF ownership prior to the returns measurement window. The results in column VII further support our second hypothesis; the coefficient on the interaction of δETF SUM t-1 to t-4 with SEARN SUM t to t+3 is −0.198 (t-stat. = −1.848). This indicates that, with larger increases in ETF ownership over the past year, current returns capture less information about firm earnings over the next year.

4.3.3 Analyst coverage tests

Table 7 presents regression summary statistics from the estimation of Eq. (9), which is designed to examine the effect of changes in ETF ownership on analyst coverage. The signs on the control variables are largely consistent with those reported in the literature. For example, Column 1 shows that changes in analyst coverage, ΔANALYST, are higher among firms with larger increases in research and development expenses (coef. = 1.965, t-stat. = 2.79) and firms with larger increases in intangible assets (coef. = 1.386, t-stat. = 3.77). In columns I and II, the coefficients on ΔETF are positive but not significantly different from zero (coef. = 0.042 and 0.017, t-stat. = 1.24 and 0.46). These results suggest that increases in ETF ownership in over year t-1 have no significant effect on analyst coverage. However, the coefficient on ΔINST presented in column II is positive and highly significant (coef. = 0.013, t-stat. = 9.06), suggesting that an increase in institutional ownership over year t-1 does tend to increase analyst coverage in year t.

To explore the possibility that ETF ownership might have a more long-run effect on analyst coverage, we include lagged level of ETF ownership as an additional explanatory variable in the estimation of results presented in columns III and IV. The results show that the level of ETF ownership from year t-2 exhibits a strong negative relation with changes in analyst coverage in year t. For example, column IV shows that higher ETF ownership is associated with lower analyst coverage (coef. = −0.025, t-stat. = −3.25), after controlling for both the level and the change in lagged institutional ownership.

In sum, over shorter windows, we find no reliable evidence that links changes in ETF ownership to changes in the number of analysts covering a firm. Over longer horizons, our results do suggest that increased ETF ownership is associated with lower analyst coverage. However, we hasten to point out that, as the time gap between the measurement of ETF ownership and analyst coverage increases, so does the likelihood that some other confounding factor is at work. Thus we think that our results on the consequences of ETF ownership on analyst coverage should be interpreted cautiously. At best, our findings are consistent with the idea that analysts slowly respond to changes in the information environment associated with changes in ETF ownership.

5 Conclusion

We use changes in ETF ownership to examine the economic linkages between the market for firm-specific information, the market for individual securities, and the role of uninformed traders. The market for ETFs has grown dramatically in the past decade, and ETFs now constitute close to 30% of the daily value traded in US exchanges. By focusing on the natural growth of exchange traded funds over the past decade, we study how changes in the composition of a firm’s investor base impacts its share pricing efficiency.

Theoretical work offers two predictions on the possible impacts of ETF ownership. First, a number of studies in the market microstructure literature suggest that trading associated with the ETF-arbitrage mechanism can improve intraday price discovery for the underlying stocks (Hasbrouck 2003; Yu 2005; Chen and Strother 2008; Fang and Sang 2012; Ivanov et al. 2013). This line of inquiry suggests that increased ETF ownership can lead to improved pricing efficiency in the underlying securities, particularly in the short run.

On the other hand, the noisy rational expectations (NRE) literature suggests a possible negative relation between ETF ownership and pricing efficiency. A number of models in this literature (Grossman and Stiglitz 1980; Hellwig 1980; Admati 1985; Diamond and Verrecchia 1981; Verrecchia 1982; Kyle 1985, 1989) predict that pricing efficiency will be a function of the information costs faced by agents seeking to profit from becoming informed about the asset. To the extent that a migration of uninformed investors away from underlying component securities increases their information costs, these models predict that increased ETF ownership will lead to a decline in pricing efficiency, particularly in the long run.

Our study examines, and provides support for, both predictions. We first demonstrate that an increase in ETF ownership is associated with an increase in firms’ trading costs. This is consistent with the idea of uninformed traders exiting the market of the underlying security in favor of the ETF. Next, we find that increases in ETF ownership are associated with increases in stock return synchronicity, decreases in future earnings response coefficients (FERCs), and decline in the number of analysts covering the firm. These findings are consistent with the idea that as uninformed traders exit the market for component securities and trading costs for these securities rise, their pricing efficiency declines.

Our main results link ETF ownership changes to subsequent changes in FERC. Consistent with the microstructure literature and Glosten et al. (2016), we find a positive contemporaneous relation between increases in ETF ownership and the market’s ability to incorporate same-quarter earnings (i.e., higher ERCs). More importantly, we go a step further and show that this positive relation holds only when all three variables (stock returns, ETF changes, and earnings) are measured in the same quarter. As the time lag between ETF changes and future earnings is increased, the relation turns negative. This negative relation becomes stronger as we increase the time lag between past ETF changes and current period returns. In other words, while same-quarter ETF trading seems to improve pricing efficiency, the more salient result over the longer run is that increases in ETF ownership undermine pricing efficiency for the underlying securities. These findings are largely consistent with predictions from the NRE literature.

We also provide some evidence on the differential impact of changes in ETF ownership on the incorporation of “macro-based” versus “firm-specific” components of earnings news. Glosten et al. find a positive relation between ETF changes and pricing efficiency and show the effect is primarily driven by better price integration of macro-based earnings. We replicate their main findings and demonstrate that, while ETF trading may improve pricing discovery for same-quarter macro-based earnings, over the longer term (beginning with the next quarter), increases in ETF ownership actually lead to lower FERCs, for both macro-based and firm-specific components of earnings news.

Our findings contribute to a growing literature on the economic consequences of basket or index-linked products. The rapid increase in index-linked products in recent years has attracted the attention of investors, regulators, and financial researchers. Adopting key insights from information economics, we present empirical evidence on how incentives in the market for information can affect pricing in the market for the underlying securities. Our results suggest that ETF ownership can lead to increased trading costs for market participants, with further consequences for the amount of firm-specific information that is incorporated into stock prices.

These findings highlight the link between information costs and market pricing efficiency. Lee and So (2015) argue that the study of market efficiency involves the analysis of a joint equilibrium in which supply must equal demand in the market for information about the underlying security as well as in the market for the security itself. In the same spirit, Pedersen (2015) argues that financial markets are “efficiently inefficient”—that is, markets are “inefficient enough that money managers can be compensated for their costs through the profits of their trading strategies, and efficient enough that the profits after costs do not encourage additional active investing.” Our study provides support for this view of market efficiency, and our main findings bring into sharp relief the close relationship between the market for stocks and the market for information about these stocks.

It is useful to remind ourselves of an important caveat imposed by our research design. While we have demonstrated an association between lagged changes in ETF ownership and changes in firms’ trading costs and pricing efficiency, this association alone does not imply causality. Both the changes in ETF ownership and the subsequent changes in other firm characteristics may be due to another, yet unidentified, latent variable. We cannot think of a good candidate, but our inability to do so does not preclude its existence. At a minimum, we have documented a set of empirical findings that are broadly consistent with an information-based explanation, which future researchers seeking an alternative explanation should address.

It is also important to interpret our findings in context. Our evidence suggests the growth of ETFs may have (unintended) long-run consequences for the pricing efficiency of the underlying securities. However, ETFs are clearly an important development in financial markets, which have brought many well-documented benefits to investors. We have not conducted a welfare analysis, and our findings should not be construed an indictment against these funds. Rather, we view these findings as yet another reminder that the informational efficiency of financial markets is not, after all, a free good.

Notes

We use the terms “pricing efficiency” and “informational efficiency” interchangeably. Both refer to the speed and efficiency with which price incorporates new information. Empirically, we use several proxies to measure informational efficiency, including “price synchronicity” (SYNCH), “future earnings response coefficients” (FERC), and the number of analysts covering a firm (ANALYST).

Several models predict noise investors will migrate to index-like instruments because their losses to informed traders are lower in these markets than in the market for individual securities (Rubinstein 1989; Subrahmanyam 1991; Gorton and Pennacchi 1993). Empirically, we have observed such a migration from actively managed assets to passively managed ETFs in recent years. As of June 2015, total ETF trading is close to 28% of the total daily value traded on US equity exchanges (Pisani 2015).

Note that the siphoning of liquidity from component securities can occur with other basket securities as well, such as open-end index funds. However, a key difference between ETFs and index-linked open-end funds is that ETF shares can be traded throughout the day, while transactions with open-end funds occur only at the end of the day and only at net asset value (NAV). Thus ETFs are a more attractive instrument for uninformed traders who trade for speculative reasons, while index funds are better suited to longer term buy-and-hold investors. In section 2, we explain in detail the implications of this difference for our tests.

We use annual holding periods to test our hypotheses because we expect the information-related effects of ETF ownership changes to be experienced gradually over time. Our inferences are the same if we use quarterly panels.

To improve our ability to identify the consequences of increased ETF ownership in a cleaner setting, we focus mainly on analyzing the associations of lagged changes in ETF ownership with firms’ trading costs and measures of pricing efficiency.

Compared to Hamm (2014), we use alternative measures of stock liquidity, include different control variables, examine annual versus quarterly observations, and use a more complete firm-level longitudinal data set. Our main findings with respect to the effect of ETF ownership on stock liquidity are consistent with those of Hamm (2014). It should be noted that Hamm (2014) does not examine the implications of ETF ownership on the informational efficiency of security prices.

Sullivan and Xiong (2012) note that, while passively managed funds represent only about one-third of all fund assets, their average annual growth rate since the early 1990s is 26%, double that of actively managed assets. Much of this increase has been in the form of ETFs. According to Madhavan and Sobczyk (2014), as of June 2014, there were 5217 global ETFs representing $2.63 trillion in total net assets.

Specifically, unlike ETFs, open-end funds do not provide a ready intraday market for deposits and redemptions with a continuous series of available transaction prices. Hence investors may not know with sufficient certainty the cash-out value of redemption before they must commit it.

Note that ETFs are most likely to be successful when the underlying securities are relatively less liquid or difficult to borrow (thus creating an equilibrium demand for the ETF shares, with its lower trading costs). For example, the highly popular small-cap ETF, IWM, is based on the Russell 2000 index. While the underlying securities are typically less liquid (they represent the 2000 stocks in the Russell Index that are below the largest 1000), IWM itself is over $26 billion in assets and trades at extremely low costs.

What happens if the cost of private information remains constant? In that case, pricing efficiency may not be affected by an exodus of uninformed traders. This result derives because the following two opposing forces are at work.

a. As uninformed traders exit the market the profits from trading with them as an informed trader becomes smaller.

b. As fewer informed traders purchase private signals, the value of being one of the remaining informed traders becomes larger.

The net effect is that fewer informed traders will individually make more money, with no net change in the economy-wide value of becoming informed (which remains equal to the information cost). Although the source of noise differs in the models of Verrecchia (1982) and the Grossman and Stiglitz (1980), the same result obtains in both. In both, pricing efficiency will be unaffected by an exodus of uninformed traders if information costs remain constant. We are grateful to the editor for pointing this out.

We test our hypotheses using annual panels because we expect the effect of increased ETF ownership to manifest itself gradually over time after an increase in ETF ownership. Figure 2 presents a sample construction timeline for the key empirical variables used in our tests. Most of our analyses are done using annual changes in ETF ownership, returns, and earnings (Panel A). However, in our replication and reconciliation of the Glosten et al. results, we used quarterly data (Panel B) to match their analyses.

Prior research on the relation between bid-ask spreads and institutional ownership is mixed. Glosten and Harris (1999) suggest that higher levels of concentrated institutional ownership will increase bid-ask spreads, while higher levels of dispersed institutional ownership might encourage competition that reduces bid-ask spreads.