Abstract

In this study, the effect of a fiscal reform of government level implemented in China on enterprise pollution emissions is estimated, using data from the Chinese polluting enterprise database. The results provide strong evidence that fiscal decentralization decreases environmental quality as measured by a comprehensive indicator composed of wastewater, waste gas, and waste solids. Compared to non-province-managing-counties in province-managing counties, corporate pollution has increased by 3.4%, especially in companies owned by cities and counties and in companies that belong to low-pollution industries and are facing financial constraints. This shows that, although the PMC reform enhanced the provision of environmental public goods by local governments, it also strengthened the race to the bottom caused by interjurisdictional competition. Therefore, the total effect of the PMC reform on pollution is positive. This suggests that relying solely on fiscal decentralization cannot effectively improve environmental quality. Higher-level governments should design a more effective incentive mechanism to decrease enterprise emissions.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

China has experienced rapid economic growth since 1994, which has resulted in increasingly serious environmental pollution. Many studies attributed this to fiscal decentralization arguing that such decentralization introduces interjurisdictional competition, which ultimately causes local governments to engage in a race to the bottom (Liang & Yang, 2019; Taguchi & Murofushi, 2010; Zhang et al., 2018). In this study, using the fiscal reform of government level implemented in China in the early 2000s, known as Province-Managing-County (PMC), strong evidence is provided that fiscal decentralization increases pollution by enterprises. This represents a good chance for exploring the causal effect of decentralization with the aim to shift a larger share of fiscal powers from cities to counties and improve the efficiency of the provision of public goods (Liu & Alm, 2016; Ma & Mao, 2018).

Fiscal decentralization is the mainstream in most countries. Following Oates (1972), it is generally assumed that local governments are benevolent in their provision of local public goods. However, certain industrial products, the production of which reduces environmental quality (e.g., by causing sulfur dioxide emissions, water pollution, and industrial wastewater discharge), remain debated and understudied. According to data obtained via "voting with feet," as emphasized by Tibout (1956) and Oates (1972), interjurisdictional competition helps to enhance environmental quality, because it leads localities to participate in a race to the top, rather than a race to the bottom (Konisky, 2007; List & Gerking, 2000; Sigman, 2014). Khan et al. (2021) showed that fiscal decentralization could indirectly improve environmental quality through both institutions and human capital. Xu and Li (2022) tested the relationship between different types of fiscal decentralization and environmental pollution. Other scholars argued that fiscal decentralization may harm the environment because of the associated free-riding caused by negative externalities proposed by the pollution-heaven hypothesis (Dean et al., 2009; Farzanegan & Mennel, 2012). Especially in the context of Chinese fiscal decentralization, local officials are appointed and removed by upper-level officials, rather than through elections by taxpayers (Blanchard & Shleifer, 2001; Li & Zhou, 2005). As China’s political system is dominated by promotion tournaments, lower-level local officials may prioritize economic growth represented by per capita Gross Domestic Product (GDP) at the expense of the environment (He, 2015). According to data from the World Bank (2016), the social welfare loss caused by air pollution in China has reached 10.9% of the GDP. Previous studies also suggested that local governments, especially those mainly relying on heavy industries, are inclined to relax environmental regulations or standards to promote the local economy, even colluding with them by applying a pollution first and governance later approach (Shi & Shen, 2013; Wang et al., 2003; Zhang et al., 2018). According to the Bulletin of the State of China’s Environment in 2015, among a total of 338 cities, 265 cities (accounting for 78.4%) exceeded environmental air quality standards, and of 448 cities, 22.5% are subject to acid rain (District, county).

However, one important challenge-related studies face is the endogeneity of fiscal decentralization, and studies usually construct decentralization indicators such as revenue and expenditure decentralization based on provincial data (He, 2015). Therefore, endogeneity is inevitably generated, and clearly identifying the causal relationship becomes key to solving such problems. The PMC reform, which has changed the long-standing five-layer political system into four layers since the 2000s (from central-province-prefecture-county-town to central-province-county-town) provides a valuable opportunity to accurately identify the causal effects. Far more spending responsibilities and tax autonomy were shifted to counties, which are directly under provincial management instead of under city management (Liu & Alm, 2016). Based on this reform, existing literature often provides further empirical evidence on the reforms of developing countries from a fiscal decentralization perspective (Chen & Lu, 2014; Ma & Mao, 2018). For example, while Ma and Mao (2018) showed that the effect of PMC on economic growth is significantly positive, in contrast, Li et al. (2016) found that PMC does not increase the economic growth performance of counties, but rather, it reduces the social welfare level. Chen and Lu (2014) argued that the reform has a certain distortionary effect on counties’ fiscal expenditure. However, little evidence has been found that enables an analysis of its impact on local environmental pollution, especially based on the firm level.

This paper provides strong evidence that the PMC reform has had a significant and positive effect on enterprise pollution, measured by a comprehensive indicator composed of waste water, waste gas, and waste solids generated by industrial enterprises. This result supports the conclusion that Chinese fiscal decentralization induces local officials to engage in a race to the bottom, rather than a race to the top (Shi & Shen, 2013; Wang et al., 2003; Zhang et al., 2018). Compared with non-PMC counties, corporate pollution in PMC counties has increased by 3.4% since the gradual PMC reform, especially in companies owned by cities and counties and companies of low-pollution industries that are facing financial constraints. Moreover, enterprises with stronger waste water and waste gas treatment capacities are more willing to discharge sewage. The mechanism shows that, although the PMC reform enhances the provision of environmental public goods by local governments, it strengthens interjurisdictional competition, which decreases environmental quality.

One concern is that the criteria of the reform are determined by provinces and are therefore not strictly random. To test the reliability of the results, a parallel trend test is conducted using the event study method. No significant differences were found between the control and the treatment group before the PMC reform. Furthermore, placebo tests were conducted for various pollutants to check whether the effect is subject to random interference by other policies. A series of robustness checks are also conducted such as multiplying all control variables with the polynomial of time to obtain a more sensitive regression. The results show that the basic conclusion is reliable.

This study contributes to the existing literature regarding fiscal decentralization and local environmental pollution by exploring the relationship between PMC reform and firms’ pollution emissions. First, the relationship between fiscal decentralization and environmental pollution is theoretically unclear and depends on the net effect between the race to the top and the race to the bottom of local governments. This relationship needs to be confirmed empirically, and available empirical findings mainly focused on developed countries. This study provides additional evidence originating from China, which is one of the largest developing countries. Second, this study fills the gap in the literature by conducting a quasi-experiment, using the combination of Chinese pollution industrial enterprise data and county-level data. Previous studies usually concentrated on province-level pollution, which is a rough sum of enterprise data but cannot represent the polluting behavior of companies (Shi & Shen, 2013). To overcome the endogeneity of fiscal decentralization, a Differences-in-Differences (DID) model was employed to identify the causal effect.

The remainder of this paper is organized as follows: Sect. 2 provides a brief overview of the PMC fiscal reform in China and introduces the theoretical hypotheses. Section 3 presents the identification strategy and data. Section 4 presents the main results and robustness tests. Section 5 discusses the dynamic and heterogeneous effects of the reform and the potential mechanism. Section 6 provides the conclusion.

2 Background and theoretical hypotheses

2.1 Background

China’s hierarchical system of administration has been highly centralized since 1949. It consists of the five layers of central, province, prefecture, county, and town, listed from the highest to the lowest level. In this system, governments at lower levels are wholly subordinated to those at higher levels. The central government directly ordinates the provincial levels, and the provincial governments can determine the promotion of prefectural officials, i.e., central-managing-province, province-managing-prefecture, prefecture-managing-county, and county-managing-town. Correspondingly, higher-level governments strictly control fiscal revenues and expenditures of lower-level governments. To obtain finance for urban construction and development, prefectural governments are inclined to shift the responsibilities of expenditure to the county government, while withholding revenue resources, especially tax revenues allocated to counties. This mismatch between revenues and expenditure responsibilities causes the supply of county public goods and services to be insufficient, which leads to a long-time lag in the development of counties (Huang et al., 2017; Wang et al., 2012).

To resolve this dilemma, China has undertaken the PMC reform since 2003, implementing the four-layers political system of central-province-county-township which replaces the five-layers hierarchical system of central-province-city-town-township. That is, in the four-layers hierarchical system, the counties’ fiscal revenues will be directly controlled by provincial governments instead of cities. This avoids the situation that fiscal funds (such as fiscal revenues, intergovernmental transfer payments, and fiscal budgets and final accounts) may be withheld by cities. Through the PMC reform, China has established a fiscal system with a simplified fiscal hierarchy at the core. Therefore, previous literature refers to this reform as the flattening government hierarchy reform (Li et al., 2016).

According to the Ministry of Finance (MOF) of the People’s Republic of China, in almost all provinces except for ethnic autonomous regions, the PMC reform was implemented by the end of 2012. Furthermore, the MOF stipulated that provinces and counties shall be directly connected in five aspects: income and expenditure division, transfer payments, fiscal budgets, final accounts, fund exchanges, and fiscal settlements. In fact, to solve the fiscal difficulties of counties, Zhejiang delegated fiscal and economic management powers to counties as early as the 1990s, and Hainan implemented the PMC in its year of establishment 1988. Since the 2000s, Fujian began to implement the PMC reform in 2003, which was then expanded to pilot projects in Anhui, Hubei, Henan, and Guangdong in 2004, and further extended to Hebei, Jilin, and Jiangxi in 2005. The peak of the reform was in 2007 and 2009. By the end of 2012, 1099 counties in 24 provinces (approximately 56% of all counties) had implemented this reform (Huang et al., 2017).

The PMC reform has expanded the fiscal authority of county governments and enhanced the counties’ power to claim local taxes and their fiscal autonomy. Transfer payments from higher-level governments were also coming from provincial fiscal accounts directly, which were cities before the reform. This not only helps counties to get rid of the fiscal funnel, rights funnel, and efficiency funnel formed by the interception and misappropriation of fiscal funds, but also helps to resolve the mismatching problem of fiscal revenue rights and expenditure responsibilities of counties (Chen & Lu, 2014; Jia et al., 2020).

2.2 Theoretical hypotheses

The key to supporting the green development of industrial enterprises is to reduce their pollutant emissions. As an important attempt to reform China's fiscal system, it remains to be explored whether the radical PMC fiscal reform provides counties with more financial autonomy and motivates enterprises to reduce pollutant emissions and improve their environmental management efficiency.

Clearly, the PMC reform affects the pollutant emissions of enterprises through two main channels. First, the PMC reform prevents the retention of fiscal resources by municipalities. This may promote counties to optimize the supply of environmental public goods and increase environmental management efforts, thus promoting both energy conservation and emission reduction by enterprises. Second, most provinces have stipulated the reform goal of promoting the economic development of their counties. Certain provinces have also put forward specific requirements for the economic growth level of pilot counties. For example, Liaoning Province imposed the clear requirement that the economic growth rate of PMC-counties must exceed the average level of the province, and Fujian Province also imposed the requirement that PMC-counties must double their GDP by 2008. While equipping provincial counties with certain financial and administrative powers, these measures may strengthen the counties’ development strategy of competing for growth. On the one hand, these measures strengthen intervention in local enterprises' investment, while on the other hand, enterprises' pollution behavior is ignored and condoned. Overall, a "pollution first and treatment later, and treatment while polluting" approach is often pursued, which is not conducive to reducing pollution caused by enterprises. Therefore, theoretically, the net effect of the reform at the government level on the emission reduction of enterprises depends on whether the financial effect is greater or smaller than the second effect.

At the same time, the impact of fiscal incentives on emission reduction may vary depending on the nature of enterprise ownership. Soft budget constraints and corporate autonomy problems associated with stated-owned enterprises may not provide the required incentive to improve energy efficiency and reduce pollution in actual operation. Coupled with their ability to obtain energy resources at prices cheaper than market prices (which are unavailable to private enterprises), the reliance on technological progress to improve energy technologies lacks incentive mechanisms, especially for county-owned enterprises (COEs) (Chen & Chen, 2019). Moreover, because of the public characteristics of stated-owned enterprises, the heads of central or province-owned enterprises (CPEs) may have stronger political resources than county government officials. The difference in administrative levels prevents county governments from exerting substantial influence on the business decisions of CPEs. Instead, they may significantly influence the business decisions of COEs under their jurisdiction, thus affecting the energy conservation and emission reduction behaviors of these COEs.

In summary, this paper considers the following two hypotheses:

Hypothesis 1

Whether reform at the governmental level will reduce enterprise pollution depends on the net effect of its financial effect and the effect of the race to the bottom.

Hypothesis 2

The impact of reform at the governmental level will be more significant for CPEs, especially for COEs.

3 Empirical strategy and data

3.1 Identification strategy

In this subsection, the identification strategy is presented. Based on the previous theoretical analysis and provincial differences in the timing of PMC reform, a gradual DID model is constructed to identify the net effect of the PMC reform on industrial pollution. The model is set as follows:

where \(\ln \left( {{\text{pollution}}_{ijt} } \right)\) is the measure of the pollution emissions of the ith firm in the jth county, and the tth year, represented by pollution indicator, air pollution, water pollution, and waste solids. \({\text{PMC}}_{jt}\) is a dummy variable which equals 1 if the county implemented the PMC reform in year t and subsequent years, and otherwise 0. \(Controls\) are control variables from enterprise and county levels. \(\lambda_{i}\) is the individual effect, \(\eta_{t}\) is the year fixed effect, and \(\varepsilon_{ijt}\) is the error term. In the baseline regression, county fixed effect is also added to control certain effects that do not change with the year. Errors are clustered at the city-industry level to enable the correlation of the error term across city and industry.\({\text{PMC}}_{jt}\) is the core explanatory variable this study focuses on, which reflects the net effect of the PMC reform on industrial pollution. If \(\beta\) is significantly positive, fiscal decentralization increases industrial pollution.

3.2 Variables

3.2.1 Dependent variables

Since 1973, China has formulated the three industrial wastes discharge standard, and detailed regulations on the standard discharge volume of waste water, waste gas, and solid waste. The reason why these three pollutants were used is that these are the main environmental pollutants that are dangerous or harmful to human health (Greenstone & Hanna, 2014; He, 2015; Sigman, 2014). Wastewater, waste gas, and solid waste per unit output value are used to represent the dependent variable. For convenience, a comprehensive indicator was also constructed to represent the enterprise overall pollution based on a simple averaging method in the baseline regression. All indicators are deflated at the province level.

3.2.2 PMC

As the PMC reform is gradually implemented in different regions, this paper assigns a value of 1 to the year when the county implemented the reform (and to all following years). The number of counties that implemented the reform is 672, accounting for 46.34%. This is roughly consistent with Ma and Mao (2018) and Jia et al. (2020), where the number of counties that has not implemented the reform was 778, accounting for 53.66%.

3.2.3 Other variables

To further reduce problems of heteroscedasticity and endogeneity, this study also considers the following variables at the enterprise and county level. Following Chen and Chen (2019), corporate control variables are capital intensity, asset profitability, number of employees, size, age, and number of sewage facilities. Among these, capital intensity is expressed as the proportion of net fixed assets of the company to total assets. The higher the capital intensity, the higher the replacement cost of adopting energy-saving facilities. It can be predicted that capital intensity will have a significant positive effect on pollution. The number of employees is calculated with the natural logarithm of the company’s annual average number of employees plus 1, reflecting the level of human capital of the company, and implying the innovative capability that could improve clean production technology (Ang, 2009). It has been predicted that a higher number of employees will lower the pollution of an enterprise. The company’s scale is represented by using the natural logarithm of the total enterprise assets. Compared with small enterprises, usually, only large-scale enterprises have sufficient cash flow and can afford to reduce pollutants to avoid the polluting cost. The age of an enterprise is expressed by using the natural logarithm of the current year minus its year of establishment. The number of corporate sewage facilities is represented by using the natural logarithm of the number of waste water and abandoned treatment facilities, indicating the environmental protection capacity of enterprises. County-level variables are mainly the real per capita GDP, population density, industry structure, real per capita government expenditure, public service, and financial development. A dummy environmental protection policy variable is also introduced, which equals 1 after 2006 and 0 before 2006. The reason is that China has used environmental protection as a binding indicator since the 11th Five-Year Plan, and both energy-saving and emission reduction measures have been emphasized during the subsequent 12th and 13th Five-Year Plan periods. This emphasis on protection inevitably affected local governments’ environmental protection behavior; therefore, it is predicted that strengthening policy constraints will reduce these three pollutant emissions.

3.3 Data

The data used in this paper are taken from Chinese industrial pollution enterprise's database from 2001 to 2009, which is published by the National Bureau of Statistics of China. This database details pollution information of industrial enterprises such as air pollution, water usage, water pollution, and total assets. At the county level, the utilized data originate from the corresponding year China Statistical Yearbook for the Regional Economy, and the GDP deflator is uniformly calculated using provincial GDP. Data processing is conducted according to Brandt et al. (2012), as follows: (1) Observations that are missing and less than or equal to 0 are excluded, such as total assets, fixed assets, main business sales income, fixed assets, total profit, and total industrial output value; (2) observations that are missing and less than or equal to 0 in the explained variable are excluded; (3) certain observations that are clearly not in compliance with accounting standards are excluded, such as data on companies whose total assets are less than their current assets, where total assets are less than fixed assets, or where total assets are less than profits; (4) finally, firms whose main business sales income is less than 5 million yuan, and whose average annual number of employees is less than 8 were also excluded.

Regarding the PMC variable, following Ma and Mao (2018): (1) Hong Kong, Macao, and Taiwan regions were excluded; (2) the four municipalities directly under the Central Government (Beijing, Shanghai, Tianjin, and Chongqing) were excluded because these municipalities themselves are two-level political systems, which do not belong to the scope of the policy reform; (3) the data of Hainan, Zhejiang, and Hubei’s three sub-prefecture-level cities (such as Tianmen, Xiantao, and Qianjiang) were excluded because Hainan has been in the PMC from the beginning of the establishment of the province since 1988, and Zhejiang has implemented the PMC reform since 1953; and (4) data from the three autonomous regions of Tibet, Xinjiang, and Inner Mongolia were excluded, for there are many ethnic minority populations in these autonomous regions, the fiscal systems of whom are not comparable to those of other provinces.

Finally, all variables are tailed off at the 1% and 99% quantiles to remove extreme values. After the above processes, about 65 thousand observations of 1450 counties were obtained. Table 1 shows the descriptive statistics of the main variables in this study.

4 Empirical results

4.1 Baseline results

In this section, the DID model shown in Formula 1 is adopted to evaluate the treatment effect of the PMC reform on firms’ pollution emissions. Table 2 presents the results. As shown in Table 2, only the variables at the enterprise level in the first column are controlled. The estimated coefficient of the PMC reform is significantly positive at the level of 1%, showing that compared with non-PMC counties, the pollution levels of counties that implemented PMC increased by 3.9%, meaning that fiscal decentralization has decreased environmental equality (Kong et al. 2022). The second column adds county-level control variables based on the first column, which is also significant at the 1% level. As mentioned above, although fiscal decentralization represented by the PMC reform increases local fiscal autonomy and improves the supply capacity of local public goods, it also stimulates prioritization by local governments of local GDP growth driven by investment. This even colludes with local polluting companies to promote local economic growth at the expense of environmental quality.

The estimated coefficients reported in columns 3–6 are also significant and positive at least at the 5% level, and dependent variables are waste gas, waste solid, and waste solid per capita output, respectively. The results show that waste water, waste gas, and waste solid emissions from industrial enterprises in PMCs all increased significantly after the reform. Specifically, the estimated coefficient of waste gas per capita output is 0.016, which is significant at the 1% level. This implies that the reform increased waste emissions of firms by 1.6%, and waste solid and wastewater emissions increased by 5.2% and 4.2%, respectively. Compared with the sample mean, these effects are of economic significance. However, the association between fiscal decentralization and environmental pollution cannot be assumed to be causal. In the following subsection, robustness tests are employed to test reliance.

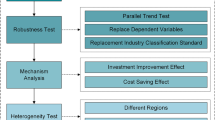

4.2 Robustness checks

In this subsection, the following measures are adopted to test robustness: First, following Storeygard (2016), all control variables are multiplied with the time trend to control enterprise and county-specific trends for possible selection bias. The result is reported in Column 1 of Table 3. Second, as shown by Gentzkow (2006) and Li et al. (2016), to control for potential pre-existing differences between control and treatment groups, the cubic polynomial of the time trend is added to make the time trend assumption more flexible. The result is shown in the second column of Table 3. Third, following Campante and Yanagizawa-Drott (2015), the interaction between the pretreatment characteristics and year dummies is added to baseline regressions to control for the time effects of the characteristics of outcome variables. The third column reports the result. Fourth, counties of province-level municipalities and sub-provincial cities usually have inherent political advantages in obtaining fiscal and financial resources from upper-level officials. In this aspect, they differ from other counties, and therefore, such counties will naturally receive more attention from their superiors. Therefore, these observations were excluded for the robustness test. The results are shown in Column 4 in Table 3. Fifth, pollution may vary in different industries. Therefore, the interaction terms of industry and time dummy variables are controlled in the benchmark regression to control the influence of unobservable factors that change across different industries over time. At the same time, standard errors are clustered at the city-industry level to control for differences in different city industries. Sixth, all variables were tailed at the 1% quantile in the baseline regression. In this subsection, all variables are retailed at the 5% quantile to further remove extreme values. The results are shown in the last column of Table 3.

After the above resetting of the benchmark regression, the re-estimated coefficients of PMC reported in Table 3 are all significant and positive at the 5% level at least, which further supports the above conclusion.

4.3 Mechanism

The above results represent the negative effects of decentralization on enterprise pollution emissions. In this subsection, potential channels are explored further. According to the documents of the PMC reform of provinces, the PMCs mainly aim to improve the level of local fiscal revenues and promote the development of the county. First, as shown in the above analysis, interjurisdictional competition is an important driving force of local economic growth. In the context of Chinese fiscal decentralization, interjurisdictional competition incentivizes local governments to compete for growth. To promote the local economy, governments will attract more capital, especially from industrial enterprises to flow into their jurisdiction. These enterprises are usually the main sources of industrial pollution. This means that interjurisdictional competition will induce local governments to engage in a race to the bottom regarding environmental quality. To test this, the outputs of all polluting enterprises of every county are summed and then divided by the county’s GDP to represent the interjurisdictional competition. Second, as emphasized by Tibout (1956) and Oates (1972), local governments hold more information advantages over the residents in the jurisdiction, which is conducive to improving the efficiency of the provision of local public goods and services. To enhance social welfare, local governments will implement stringent environmental regulations to limit pollutant emissions. As a result, the environmental regulation variable and its interaction with PMC are added to test the channel. Specifically, the logarithm of the treatment capacity of waste gas treatment facilities (standard m3/h) and the treatment capacity of wastewater treatment facilities (ton/day) are used to represent the regulation (regulation1 and regulation2, respectively).

As shown in Table 4, the estimates of interactions in Columns 1–2 are significant and negative at least at the 10% level. These results show that after the PMC reform, the regulations of counties implementing the PMC reform reduced the pollutant emissions of enterprises. The result in Column 3 shows that after the PMC reform, interjurisdictional competition increased pollution. In addition, all three channels are added into the baseline regression shown in Column 4. This implies that although the PMC reform enhances the local government’s provision of environmental public goods, this is offset by the negative effect imposed by interjurisdictional competition. The total effect is significantly positive, meaning that fiscal decentralization decreases environmental quality.

5 Parallel trends, dynamic effects, and heterogeneity

5.1 Parallel trends and dynamic effects

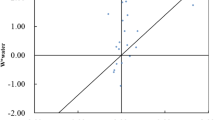

The above results show that fiscal decentralization has increased firms’ pollutants such as wastewater, waste gas, and waste solids; the conclusion is reliable. However, an important premise for DID is that there should be no significant difference between the treatment group and the control group. This implies that the model should satisfy the parallel trends hypothesis. To further examine pre-existing time trends, an event study is conducted to strictly test differences between before and after the implementation of the PMC reform, while at the same time identifying its dynamic effect. Specifically, the PMC dummy variables in the benchmark regression are replaced with new reform dummies generated before and after the reform, followed by re-estimation.

where \(D_{jt}^{k}\) is a set of dummies newly generated five years before and after the PMC. The definitions of other variables are consistent with the baseline. Following Beck et al. (2010) and Ma and Mao (2018), the following rules are imposed: \(post_{i}\) is the reform year, if \(t - {\text{post}}_{i} = k\), \(D_{jt}^{k}\) equals 1, otherwise, it equals 0. When \(k \ge 5\) or \(k \le - 5\), it also equals 1. As a reference, the year before policy implementation is selected as the base year, and \(D_{jt}^{ - 1}\) is removed from the regression. Finally, the estimated coefficients and significance represented by \(\beta_{k}\) are observed, which reflect the difference before and after PMC implementation. As expected, if the results are reliable, \(\beta_{ - 5} , \beta_{ - 4} , \beta_{ - 3} , {\text{and}} \beta_{ - 2}\) should be of no significance. Moreover, \(\beta_{1} , \beta_{2} , \ldots , \beta_{5}\) reflect the dynamic effects.

The results reported in Table 5 and Fig. 1 show that the estimates before the PMC reform are all statistically non-significant, meaning that there are no significant differences between the control group and the treatment group. The firms in PMC and non-PMC counties meet the parallel trends test, which validates the employed DID identification strategy. Moreover, the coefficients of post-reform year dummies indicate that after the PMC reform, there was a significant increase in the firm’s pollutant emissions, and the positive effect persisted for at least 5 years after the PMC reform.

Parallel trends and dynamic effects

5.2 Placebo test

To eliminate interference of other policies and obtain more robust results, following La Ferrara et al. (2012) and Li et al. (2016), a placebo test was conducted by randomly assigning the adoption of the PMC reform to counties in the sample. Specifically, the same number of counties and random reform years were selected as control group. Then, re-regression was conducted. To increase the identification power of this placebo test, the above random process was repeated 1000 times. Given this random data generation process, if the obtained results are insignificant (i.e., are distributed around 0), and are normally distributed, this is a further indication that the basic conclusions of this study are robust and reliable.

Figure 2 reports the kernel density of the four estimated coefficients in the counterfactual analysis, the estimated values all obey the standard normal distribution, and the four means are all distributed around zero. However, the coefficients estimated in the baseline regression are almost larger than zero. This means that the PMC reform truly enhances firms’ pollutant emissions.

Placebo test results. The dotted line in the figure represents the estimated value of the corresponding coefficient in the baseline regression

5.3 Heterogeneity

5.3.1 Corporate ownership and industry nature

The basic conclusions show that the PMC reform has increased enterprises’ pollutant emissions. However, identifying which kind of firm the PMC impacted more significantly requires further analysis. Firstly, according to the main objectives of the PMC reform, this reform not only increased the fiscal autonomy of PMC counties, but also enhanced interjurisdictional competition, thus inducing a race to the bottom. In China, companies are under the control of different jurisdictions depending on where they are registered. The local government has the power to affect their business decision-making, but this may not affect companies with a higher administrative hierarchy such as CPEs. For example, certain polluting companies such as Sinopec and CNPC, which are relatively high-polluting central enterprises in China, can offer many jobs and taxes to the locality, and therefore gain a certain right to decide their pollutant emissions, even in collusion with the locality. Unfortunately, enterprises at a lower administrative hierarchy (such as COEs) will be more subject to local governments. Therefore, it is predicted that the PMC reform may increase the pollutant emissions of such enterprises and may be of no significance to enterprises that do not belong to them or those that have a firmer administrative hierarchy. Secondly, since 2006, China has gradually incorporated environmental governance into the political performance appraisal of local officials and central supervision of certain high-polluting industries has been implemented (Zhang et al., 2018). These high-polluting industries are mainly petroleum, coal, and other fuel processing industries, manufacturing industries of chemical raw materials, chemical products, non-metallic mineral products, ferrous metal smelting and rolling processing industry, non-ferrous metal smelting and rolling processing industry, electric power, thermal production, and supply industry. The focus on analysis was whether the implementation of the PMC reform aggravated the pollution levels of these enterprises or promoted their transition from low-pollution industries to high-pollution industries. According to the basic conclusion, it is predicted that the effect of the PMC reform on lower polluting enterprises will be more significant.

Therefore, the sample was divided into two sub-samples to investigate heterogeneity effects based on ownership and the level of industrial pollution. The results are shown in Table 6. As expected, implementing the PMC reform does not significantly affect central or province owned enterprises (CPE, Column 1), while significantly increasing the pollution emissions of COEs (Column 2), especially of state-owned enterprises at the county level (COE & SOE, Column 4). This means that to promote local economic growth, local governments will implement the strategic behavior of treatment after pollution or treatment while pollution. Local governments will rely on SOEs at the county level to promote economic growth at the expense of the environment. As reported in Columns 5–6, the effect of the PMC reform on high-pollution enterprises is not significant, while the estimated coefficient on low pollution enterprises is significant at the 5% level. This shows that the PMC reform enhanced the pollutant emissions of low polluting enterprises and also promoted low polluting enterprises to become high polluting enterprises.

5.3.2 Business performance

How the effects vary according to the differences at the firm age, size, and probability was also explored. Generally, firms that are either young or small tend to be financially constrained (Zwick & Mahon, 2017), and firms with low profitability may not have enough cash to purchase environmental protection equipment, and may therefore take negative environmental action. Table 7 reports the heterogeneous effects. The results show that the effects of the PMC reform on corporate pollution are more significant for small firms and firms with low profitability, and the effects are stronger for young firms. So, it can be concluded that the emissions of such firms with much more financial constraints will be higher. The reason is that these firms, or the local governments, may be reluctant to purchase environmental equipment for the purpose of cultivating a tax base. Similarly, existing literature showed that firms that have little access to finance will have a low level of tax compliance (Fan & Liu, 2020).

6 Conclusions

Fiscal decentralization not only helps to enhance the efficiency of the provision of public goods such as environmental quality, it also induces a race to the bottom among local governments. Based on a fiscal reform implemented in China since the 2000s, this paper assesses the net effect of fiscal decentralization on environmental quality using the Chinese polluting enterprise database from 2001 to 2009. The results show that: First, compared with non-PMC counties, pollutant emissions of PMC counties increased by an average of 3.4%. This means that the PMC reform has significantly reduced the environmental quality, and this effect is continuous. Second, the effect of the PMC reform on pollution mainly manifests in promoting the transformation of low polluting enterprises to high polluting enterprises. Moreover, it also has a more significantly negative effect on state-owned enterprises, especially on those that are affiliated to county-ism, and firms facing financial constraints. Third, mechanism analysis shows that the PMC reform intensified interjurisdictional competition, and adopted the strategic behavior of treatment after pollution, i.e., inducing a race to the bottom. These conclusions remain reliable even after a series of robustness checks, parallel trends test, and placebo tests are conducted.

The results of this study showed that relying solely on fiscal decentralization cannot effectively improve environmental quality. If the competitive strategic behavior of local governments cannot be corrected in a timely manner, it will be difficult to improve the local environmental quality. Ultimately, this may even threaten the realization of China’s CO2 emission reduction goals. Since 2006, the Chinese government has been strengthening its legislative efforts regarding environmental quality issues. It has also included energy conservation and emission reduction targets as binding indicators in the political appraisal system of officials, in an attempt to change the distorted performance appraisal of local government officials who are promoted on the basis of GDP.

This paper argues that counties, as the first body responsible for local environmental governance and economic development, should continue to increase the accountability of government officials in their assessment. Higher-level governments should strengthen governance over environmental efforts of lower-level governments, which are primarily responsible for local environmental governance and economic development. The Chinese government should include environmental constraints and other indicators into performance assessments and should increase supervision from the National People's Congress and the public to effectively enhance governmental governance. At the same time, a more effective incentive mechanism should be designed that aims to improve the pollutant emissions of state-owned enterprises.

A major limitation of this study is that our data are not up to date. However, the findings are still valid. First, China is a developing country characterized by centralized political power and decentralized economic power. So in China, the relationship between the central and local governments is a hot issue for research, while the link of this relationship is fiscal decentralization. Second, since China proposed to achieve carbon peak by 2030 and carbon neutrality by 2060, it is very urgent and important to reduce corporate pollution from the government level. Therefore, the study is still meaningful for the improvement of current regional strategies. Future studies could recreate our study using current data to determine if anything has changed.

References

Ang, J. B. (2009). CO2 emissions, research and technology transfer in China. Ecological Economics, 68, 2658–2665.

Beck, T., Levine, R., & Levkov, A. (2010). Big bad banks? The winners and losers from bank deregulation in the United States. The Journal of Finance, 65, 1637–1667.

Blanchard, O., & Shleifer, A. (2001). Federalism with and without political centralization: China versus Russia. IMF Staff Papers, 48, 171–179.

Brandt, L., Van Biesebroeck, J., & Zhang, Y. (2012). Creative accounting or creative destruction? Firm-level productivity growth in Chinese manufacturing. Journal of Development Economics, 97, 339–351.

Campante, F., & Yanagizawa-Drott, D. (2015). Does religion affect economic growth and happiness? Evidence from Ramadan. The Quarterly Journal of Economics, 130, 615–658.

Chen, S. X., & Lu, S. F. (2014). Does decentralization increase the public services expenditures: A quasi-experiment of county administrated by province in China. China Economic Quarterly, 13, 1261–1282.

Chen, Z., & Chen, Q. Y. (2019). Energy efficiency of Chinese firms: Heterogeneity, influencing factors and policy implications. China Industrial Economics, 12, 78–95.

Dean, J. M., Lovely, M. E., & Wang, H. (2009). Are foreign investors attracted to weak environmental regulations? Evaluating the evidence from China. Journal of Development Economics, 90, 1–13.

Fan, Z., & Liu, Y. (2020). Tax compliance and investment incentives: Firm responses to accelerated depreciation in China. Journal of Economic Behavior & Organization, 176, 1–17.

Farzanegan, M. R., & Mennel, T. (2012). Fiscal decentralization and pollution: Institutions matter. MAGKS Joint Discussion Paper Series in Economics.

Gentzkow, M. (2006). Television and voter turnout. The Quarterly Journal of Economics, 121, 931–972.

Greenstone, M., & Hanna, R. (2014). Environmental regulations, air and water pollution, and infant mortality in India. American Economic Review, 104, 3038–3072.

He, Q. (2015). Fiscal decentralization and environmental pollution: Evidence from Chinese panel data. China Economic Review, 36, 86–100.

Huang, B., Gao, M., Xu, C., & Zhu, Y. (2017). The impact of province-managing-county fiscal reform on primary education in China. China Economic Review, 45, 45–61.

Jia, J., Ding, S., & Liu, Y. (2020). Decentralization, incentives, and local tax enforcement. Journal of Urban Economics, 115, 103225.

Khan, Z., Ali, S., Dong, K., & Li, R. Y. M. (2021). How does fiscal decentralization affect CO2 emissions? The roles of institutions and human capital. Energy Economics, 94, 105060.

Kong, D., Zhang, W., & Kong, G. (2022). Does government decentralization shape firms’ pollution emissions? Evidence from a natural experiment in China. Emerging Markets Finance and Trade, 58, 3136–3151.

Konisky, D. M. (2007). Regulatory competition and environmental enforcement: Is there a race to the bottom? American Journal of Political Science, 51, 853–872.

La Ferrara, E., Chong, A., & Duryea, S. (2012). Soap operas and fertility: Evidence from Brazil. American Economic Journal: Applied Economics, 4, 1–31.

Li, H., & Zhou, L. A. (2005). Political turnover and economic performance: The incentive role of personnel control in China. Journal of Public Economics, 89, 1743–1762.

Li, P., Lu, Y., & Wang, J. (2016). Does flattening government improve economic performance? Evidence from China. Journal of Development Economics, 123, 18–37.

Liang, W., & Yang, M. (2019). Urbanization, economic growth and environmental pollution: Evidence from China. Sustainable Computing: Informatics and Systems, 21, 1–9.

List, J. A., & Gerking, S. (2000). Regulatory federalism and environmental protection in the United States. Journal of Regional Science, 40, 453–471.

Liu, Y., & Alm, J. (2016). “Province-managing-county” fiscal reform, land expansion, and urban growth in China. Journal of Housing Economics, 33, 82–100.

Ma, G., & Mao, J. (2018). Fiscal decentralisation and local economic growth: Evidence from a fiscal reform in China. Fiscal Studies, 39, 159–187.

Oates, W. E. (1972). Fiscal federalism. Harcourt Brace Jovanovich.

Shi, B., & Shen, K. R. (2013). The government intervention, the economic agglomeration and the energy efficiency. Management World, 10, 6–18.

Sigman, H. (2014). Decentralization and environmental quality: An international analysis of water pollution levels and variation. Land Economics, 90, 114–130.

Storeygard, A. (2016). Farther on down the road: Transport costs, trade and urban growth in sub-Saharan Africa. The Review of Economic Studies, 83, 1263–1295.

Taguchi, H., & Murofushi, H. (2010). Evidence on the interjurisdictional competition for polluted industries within China. Environment and Development Economics, 15, 363–378.

Tibout, C. M. (1956). A pure theory of local expenditures. Journal of Political Economy, 64, 416–424.

Wang, H., Mamingi, N., Laplante, B., & Dasgupta, S. (2003). Incomplete enforcement of pollution regulation: bargaining power of Chinese factories. Environmental and Resource Economics, 24, 245–262.

Wang, W., Zheng, X., & Zhao, Z. (2012). Fiscal reform and public education spending: a quasi-Natural experiment of fiscal decentralization in China. Publius: The Journal of Federalism, 42, 334–356.

World Bank (2016). Institute for health metrics and evaluation. The cost of air pollution: Strengthening the economic case for action.

Xu, H., & Li, X. (2022). Effect mechanism of Chinese-style decentralization on regional carbon emissions and policy improvement: evidence from China’s 12 urban agglomerations. Environment, Development and Sustainability, 25(1), 474–505.

Zhang, B., Chen, X., & Guo, H. (2018). Does central supervision enhance local environmental enforcement? quasi-experimental evidence from China. Journal of Public Economics, 164, 70–90.

Zwick, E., & Mahon, J. (2017). Tax policy and heterogeneous investment behavior. American Economic Review, 107, 217–248.

Funding

The research is supported by Natural Science Foundation of China General Projects (71973033), Natural Science Foundation of Guangdong Province of China (2019A1515011658), and Projects of University Scientific Research Characteristic Innovation Project of Guangdong Province (2021WTSCX032).

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Yu, J., Chen, S. & Li, L. Reform of government level and local environmental pollution: evidence from China. Environ Dev Sustain (2023). https://doi.org/10.1007/s10668-023-04032-z

Received:

Accepted:

Published:

DOI: https://doi.org/10.1007/s10668-023-04032-z