Abstract

In this paper, the approximate solution u(x, t) of the temporal fractional Black–Scholes model involving the time derivative in the Caputo sense with initial and boundary conditions has been studied. This equation has the main part in defining the European option in the financial activities. Time discretization is performed by linear interpolation with a temporally \(\tau ^{2-\alpha }\) order accuracy, and the Chebyshev collocation is based on the orthogonal polynomials used for spatial discretization. Additionally, the convergence and stability analysis of the specified methods are considered. Finally, the numerical solutions of some examples were obtained and compared with their analytical solutions that demonstrate the high accuracy and feasibility of the proposed approach.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

An option is a contract that gives its owner the due to buy or sell a defined value of a special asset at a fixed value, called the exercise value, before or on a given date, known as the maturity date. An option can be applied before maturity at any moment, called the American option, or on the maturity, called the European option. Moreover, the option that offers the right to buy defines the call option, and the option that gets the right to sell defines the put option. The pricing of an option is very important in financial derivatives to mitigate losses incurred. Therefore, we must introduce the manner to investigate the price of this option.

First of all, in 1973, three mathematicians named Black and Scholes (1973) and Merton (1973) presented a scheme to estimate the price of option named the Black-Scholes model (BSM). The merchants of an option generally buy and sell the right of an option. Because of the accuracy in options trading and the success of the strategy in anticipating options prices, it eventually adds to large growth. This financial theory was introduced by applying fractional calculus of the stochastic system’s fractal assembly. This was done by replacing the fractional Brownian movement compared to its classic type. Many phenomena in nature such as the dynamical model (Kumar et al., 2020d), the epidemic of measles (Kumar et al., 2020e), transport phenomena (Tuan et al., 2020; Kumar et al., 2020b, 2020c), tumor cells (Kumar et al., 2020b), and population model (Kumar et al., 2020a) can be modeled with the help of these fractional calculations. The only problem with this type of equation is its analytical solution. So to solve the problem of the non-locality of fractional calculus, you have to use numerical solution. In recent years, many numerical methods have been proposed to solve fractional equations (Ren & Liu, 2019; Ren, 2022; AlAhmad et al., 2021; Alia et al. 2021). Below we will summarize an important part of this work. Compact finite difference design to discrete time variable with third Chebyshev polynomials to gain full discrete in Safdari et al. (2020a), hybrid Laplace transform-finite difference method in Salama et al. (2021), the fourth kind of shifted Chebyshev that presented by Safdari et al. (2020b), an extended cubic B-spline approximation in Akram et al. (2021), Hermite wavelet by kumar in Kumar et al. (2021), spectral method based on Legendre polynomials in 2019 by singh in Singh et al. (2019a), the Fibonacci collocation method to solve two-dimensional fractional-order reaction advection sub-diffusion model by Dwivedi and Singh (2021). Moreover, numerous methods in the spectral method and homotopy perturbation method are also presented in papers (Verma et al., 2019; Singh et al., 2019b; Gao et al., 2020).

Now, this type of field, because fractional calculus is a strong instrument to illustrate the inherited and retention characteristics in mathematics, has been used with the help of modeling in financial equations and can be used in detail to model the type of European or American options (Björk & Hult, 2005; Meerschaert & Sikorskii, 2011). In this regard, many authors have developed modeling for the option, which can be referred to in the following sample. The pricing of the European call option (Wyss 2000), specific state of the bi-fractional BSM (Liang et al., 2010), describing the value of European-style derivatives (Cartea, 2013), and implementing spectral methods to develop BSM (Leonenko et al., 2013).

Let r be the risk-free interest rate, \(\sigma \) is the volatility and t is the time in the year. Then in this paper, we consider TFBSM with expressed features that u(x, t) be the value of an option, as below

and the boundary conditions as

where f(x, t) and \(r>0\) are the known term. Moreover, \({}_{0}D_{t} ^{\alpha }\) is the left Caputo fractional derivative that is described as

That’s why we take a numerical approach. Of course, many numerical methods have been used to solve this problem over the years such as Legendre multiwavelet and the Chebyshev collocation method for pricing the double barrier option in Sobhani and Milev (2018) and (Mesgarani et al., 2020), respectively. Furthermore, a \(\theta \) finite-difference structure and an implicit scheme in Zhang et al. (2014) and (Song & Wang, 2013), respectively are used to price the option, In addition, in papers (Bhowmik, 2014; Chen et al., 2015; Zhang et al., 2016), other methods have been used to approximate this type of equation.

In this article, we try to act according to the following sections. We will obtain the time-discrete by using the quadratic interpolation and full scheme by the collocation method based on the third Chebyshev polynomials and investigate the convergence analysis in Sect. 2. Moreover, we will investigate the new approach by providing two numerical examples and will demonstrate the accuracy and efficiency of the method.

2 The discretization of time and space variable

In this section, we introduce and obtain the semi-discrete design as below. Considering \(u^{k}=u(x,t_{k}), {\mathfrak {p}}=\frac{\Gamma (2-\alpha )}{2}\sigma ^{2}, {\mathfrak {q}}=\Gamma (2-\alpha )(r-\frac{1}{2}\sigma ^{2}), {\mathfrak {r}}=r\Gamma (2-\alpha ), F^{k}=\Gamma (2-\alpha )f(x,t_{k})\) and \({\overline{\mathcal{S}}}_{k,j}=-{\mathcal {S}}_{k,j}\) and applying the linear design for approximating \( _{0}{D}_{t}^{\alpha }u(x,t) \) in the paper (Kumar et al., 2017), we obtain this scheme. For \( 0<\alpha \le 1 \), we get the step size \(\tau =\frac{T}{M}\) and nodes of time is \(t_{k}=k\tau ,~ k=0, 1, \ldots , M\). Then we get

where C is a nonnegative constant, \({\mathcal {R}}^{k}\le C{\mathcal {O}}({ \tau } ^{2-\alpha })\) and

The variational scheme can be got by omitted \({\mathcal {R}}^{k}\) in Eq. (3), as

where \( U^{k},~~k=0,1,\ldots ,M\) in Eq. (3) is the approximate solution.

In the present discussion, we need to consider the convergence analysis of the method. As we will see later in the final section, according to the numerical results shown, this method is unconditionally stable and the convergence order of the method is \({\mathcal {O}}({ \tau ^{2-\alpha }})\). Suppose \({\mathcal {H}}^{n}\) is the functional space that is defined as follows

where the measurable function space in this relation is \( L^{2}(\Omega ) \) in \(\Omega \) that is square Lebesgue integrable. To prove the convergence and stability of the method, we need to convert Eq. (5) as follows. Let us assume that \( {\widehat{U}}^{j} \) is an approximate solution of Eq. (5). So by using the error function \(\varepsilon ^{k}={\widehat{U}}^{k}-U^{k}, ~k=0, 1, \ldots , M\), we get

Theorem 1

The generated design by Eq. (5) is unconditionally stable.

Proof

First of all, we know in Eq. (6) that \(\langle \frac{\partial \varepsilon ^{k}}{\partial x},\varepsilon ^{k}\rangle =0\) and also we have \(\langle \frac{\partial ^{2}\varepsilon ^{k}}{\partial x^{2}},\varepsilon ^{k}\rangle =-\langle \frac{\partial \varepsilon ^{k}}{\partial x},\frac{\partial \varepsilon ^{k}}{\partial x}\rangle \). As a result we get

Using the Cauchy–Schwarz inequality and \(1+{\mathfrak {r}}\tau ^{\alpha } \ge 1\), we get

Now, we apply the principle of mathematical induction on k as the numerator of induction. If \(k=1\), we get

Regarding Lemma 5 of the paper (Safdari et al., 2020b), we can write \(-1< \mathcal {{S}}_{k,j}<0 \Longrightarrow 0<{\overline{\mathcal {S}}}_{k,j}<1,~~ j=0, 1,, 2, \ldots , k-1\). So it results

Assume the mathematical induction is true for all \(k=1, 2, \ldots , M-1\). Now we prove it for \(k=M\). One obtains

Being used again with Lemma 5 of the paper (Safdari et al., 2020b) is \(-2<\mathcal {{S}}_{M,0} + \sum \limits _{j=1}^{M-1}\mathcal {{S}}_{M,j}<1\), we have

This means that the method is stable. \(\square \)

Theorem 2

The order of convergence of the semi-discrete method (5) is \({\mathcal {O}}({ \tau ^{2-\alpha }})\).

Proof

From Eqs. (3) and (5), we define \( \xi ^k=u^k-U^k, ~~k=1, 2, \ldots , M\) and subtract Eq. (3) from Eq. (5) leading to

Without loss of generality and using the method of proving the previous theorem, we get

It is quite evident that

Because \( \frac{1}{1+{\mathfrak {r}}\tau ^{\alpha }} \le 1 \) and \(\Vert \xi ^{0}\Vert =0\). So we conclude that the convergence order is \({\mathcal {O}}({ \tau ^{2-\alpha }})\) in the case of smooth solutions in time direction. \(\square \)

Now, to get the discretization of space in Eq. (5), we use the shifted Chebyshev polynomials of the third kind (SCPTK) \({\mathcal {V}}_{i}(x), ~i=0,1,\ldots \) as

In space variable with domain [0, 1], we can apply the first \(N+1\)-terms of SCPTK as the following expansion of \( u(x,t_{j})\).

where the unknown coefficients is \(\epsilon _{i}(_{j})\) that are defined as following.

Now, to approximate the space derivative of the first and second order, \(\frac{\partial ^{l}u^{M}}{\partial x^{l}}, l=1,2\), in Eq. (5), we use features of the basis SCPTK and Eq. (9) as

where coefficients \(N_{i, k, l}^{\xi }\) is defined as

To get the linear system, we need to take the roots of SCPTK as collocation points i.e. \(\lbrace x_{s}\rbrace _{s=1}^{N+1-\xi }\) and substitute Eq. (11) in Eq. (5), we have

where the unknown coefficients in this system are \(\upsilon _{i}^{j}=\upsilon _{i}(t_{j})\) that must be obtained. To determine the uncharted coefficients \(\upsilon _{i}^{i}, i=0, 1, 2, \ldots \), we need two extra conditions such as the boundary conditions to turn the above relation into a linear system with \(N+1\) equations and \(N+1\) unknowns. Heed that by replacing Eq. (9) in Eq. (2), we get the boundary conditions as

Moreover, we obtain the initial condition \(\upsilon _{i}^{0} \) with combining \(u(x, 0)=\phi (x)\) and Eq. (10).

3 Numerical Results

The current form of value barrier choice driven by a time-fractional BSM structure, which is one the most interesting ideas in the financial sector, has now been applied inside this part. Furthermore, using the numerical technique of TFBSM, the efficiency of the system of the proposed methodology is demonstrated. We denote the order as \( {\mathcal {C}}_{{\mathcal {O}}} \) that is calculated as follows.

in which \(E_{i+1}\) and \(E_{i}\) are errors In accordance with mesh sizes 2M and M. The theoretical study is supported by the estimated findings.

Example 3.1

Consider the following problem with the homogeneous boundary conditions

that \(u(x, t)=(t+1)^{2}x^{2}(1-x)\) is the exact solution and the known parameters are \(\sigma =0.25, p=\frac{1}{2}{\sigma }^{2}, q=r-p, r=0.05, \alpha =0.7\) and

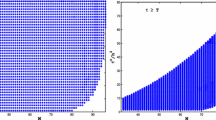

We demonstrate the error and order of this example in Table 1 at \(T=1\) with \(N=7\) that is seen the convergence order is \({\mathcal {O}}(\tau ^{2-\alpha })\) and it’s also related to the TOC (temporal order of convergence). Furthermore, as the number M increases, the error diminishes. one can deduce from the thorough findings in Table 2 that the results are remarkably similar to those of De Staelen and Hendy (2017) and Golbabai et al. (2019). Furthermore, reasonably precise findings are provided with a very small space size. When \(T=1\), we draw the absolute error and approximate solution in Fig. 1 and can deduce from this figure that the numerical method has a close accuracy.

The error (left-side) and approximate solution (right-side)) for Example 3.1 at \(T=1\)

Example 3.2

Take the TFBSM with nonhomogeneous boundary conditions as a second instance as follows.

where \(u(x, t)=(t+1)^{2}(x^{3}+x^{2}+1)\) is the exact solution and f(x, t) is got by using this solution. Moreover, the known values are \( p=1, q=r-p, r=0.5\) and \(\alpha =0.7\)

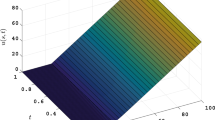

This question’s conclusions have also been reported in Tables 3, 4 and Fig. 2. Table 3 includes the new approach with compact finite difference manner (De Staelen & Hendy, 2017) and radial basis functions based on finite-difference construction (Golbabai et al., 2019) to produce successful results for the methodology. Furthermore, the order is demonstrated in Table 4 with \(N=5\) at \(T=1\) that this is supported the theoretical predictions. The numerical finding and absolute error that as seen as the approximation solution is approaching the exact solution are displayed in Fig. 2.

The absolute error (left-side) and approximate solution (right-side) for Example 3.2 at \(T=1\) and \(N=5\)

4 Conclusion

Rather than the construction of the integer-order derivative, the model’s fractional-order derivative’s “worldview" contributes to extremely exact and numerical approaches. For this reason, we considered the time-fractional Black-Scholes equation in this paper and presented a numerical scheme to solve that. Because for \(0 < \alpha \le 1\) the fractional derivative of Caputo and Riemann-Liouville coincide, then It is already replaced in the TFBSM. To discretize in a time sense, the authors used a linear interpolation with the accuracy order of \({\mathcal {O}}({\tau }^{2-\alpha })\). Then by using the Chebyshev collocation manner based on the third kind, we explained how to obtain a fully discrete numerical method. Moreover, the unconditional stability and the order of the temporal discrete are also stated. Two numerical examples with exact solutions are chosen to prove the resolution and convergence order of the numerical model, and the numerical result has shown the reliability of the new plan.

Data Availibility Statement

Data sharing is not applicable to this article as no datasets were generated or analyzed during the current study.

References

Akram, T., Abbas, M., & Ali, A. (2021). A numerical study on time fractional Fisher equation using an extended cubic B-spline approximation. J. Math. Comput. Sci., 22(1), 85–96.

AlAhmad, R., AlAhmad, Q., & Abdelhadi, A. (2021). Solution of fractional autonomous ordinary differential equations. Journal of Mathematics and Computer Science, 27(1), 59–64.

Alia, A., Abbasb, M., & Akramc, T. (2021). New group iterative schemes for solving the two-dimensional anomalous fractional sub-diffusion equation.

Bhowmik, S. K. (2014). Fast and efficient numerical methods for an extended Black–Scholes model. Computers & Mathematics with Applications, 67(3), 636–654.

Björk, T., & Hult, H. (2005). A note on wick products and the fractional Black–Scholes model. Finance and Stochastics, 9(2), 197–209.

Black, F., & Scholes, M. (1973). The pricing of options and corporate liabilities. Journal of Political Economy, 81(3), 637–654.

Cartea, Á. (2013). Derivatives pricing with marked point processes using tick-by-tick data. Quantitative Finance, 13(1), 111–123.

Chen, W., Xu, X., & Zhu, S.-P. (2015). A predictor-corrector approach for pricing American options under the finite moment log-stable model. Applied Numerical Mathematics, 97, 15–29.

De Staelen, R. H., & Hendy, A. S. (2017). Numerically pricing double barrier options in a time-fractional Black–Scholes model. Computers & Mathematics with Applications, 74(6), 1166–1175.

Dwivedi, K. D., & Singh, J. (2021). Numerical solution of two-dimensional fractional-order reaction advection sub-diffusion equation with finite-difference Fibonacci collocation method. Mathematics and Computers in Simulation, 181, 38–50.

Gao, W., Günerhan, H., & Baskonus, H. M. (2020). Analytical and approximate solutions of an epidemic system of HIV/AIDS transmission. Alexandria Engineering Journal, 59(5), 3197–3211.

Golbabai, A., Nikan, O., & Nikazad, T. (2019). Numerical analysis of time fractional Black-Scholes European option pricing model arising in financial market. Computational and Applied Mathematics, 38(4), 173.

Kumar, S., Ghosh, S., Kumar, R., & Jleli, M. (2021). A fractional model for population dynamics of two interacting species by using spectral and Hermite wavelets methods. Numerical Methods for Partial Differential Equations, 37(2), 1652–1672.

Kumar, S., Kumar, R., Agarwal, R. P., & Samet, B. (2020a). A study of fractional Lotka–Volterra population model using Haar wavelet and Adams–Bashforth–Moulton methods. Mathematical Methods in the Applied Sciences, 43(8), 5564–5578.

Kumar, S., Kumar, A., Samet, B., Gómez-Aguilar, J., & Osman, M. (2020b). A chaos study of tumor and effector cells in fractional tumor-immune model for cancer treatment. Chaos, Solitons & Fractals, 141, 110–321.

Kumar, S., Nisar, K. S., Kumar, R., Cattani, C., & Samet, B. (2020c). A new Rabotnov fractional-exponential function-based fractional derivative for diffusion equation under external force. Mathematical Methods in the Applied Sciences, 43(7), 4460–4471.

Kumar, K., Pandey, R. K., & Sharma, S. (2017). Comparative study of three numerical schemes for fractional integro-differential equations. Journal of Computational and Applied Mathematics, 315, 287–302.

Kumar, S., Kumar, A., Samet, B., & Dutta, H .(2020d). A study on fractional host-parasitoid population dynamical model to describe insect species. Numerical Methods for Partial Differential Equations

Kumar, S., Kumar, R., Osman, M., & Samet, B. (2020e). A wavelet based numerical scheme for fractional order SEIR epidemic of measles by using Genocchi polynomials. Numerical Methods for Partial Differential Equations.

Leonenko, N. N., Meerschaert, M. M., & Sikorskii, A. (2013). Fractional Pearson diffusions. Journal of Mathematical Analysis and Applications, 403(2), 532–546.

Liang, J.-R., Wang, J., Zhang, W.-J., Qiu, W.-Y., & Ren, F.-Y. (2010). The solution to a bifractional Black–Scholes–Merton differential equation. International Journal of Pure and Applied Mathematics, 58(1), 99–112.

Meerschaert, M. M., & Sikorskii, A. (2011). Stochastic models for fractional calculus (Vol. 43). Walter de Gruyter.

Merton, R. (1973). Theory of rational option pricing. The Bell Journal of Econometrics and Management Science, 4, 141–183.

Mesgarani, H., Beiranvand, A., & Aghdam, Y. E. (2020) The impact of the Chebyshev collocation method on solutions of the time-fractional Black–Scholes. Mathematical Sciences, pp. 1–7.

Ren, L., & Liu, L. (2019). A high-order compact difference method for time fractional Fokker–Planck equations with variable coefficients. Computational and Applied Mathematics, 38(3), 1–16.

Ren, L. (2022). High order compact difference scheme for solving the time multi-term fractional sub-diffusion equations. In practice 28, 32.

Safdari, H., Aghdam, Y. E., & Gómez-Aguilar, J. (2020a). Shifted Chebyshev collocation of the fourth kind with convergence analysis for the space-time fractional advection-diffusion equation. Engineering with Computers, 38, 1–12.

Safdari, H., Mesgarani, H., Javidi, M., & Aghdam, Y. E. (2020b). Convergence analysis of the space fractional-order diffusion equation based on the compact finite difference scheme. Computational and Applied Mathematics, 39(2), 1–15.

Salama, F. M., Ali, N. H. M., & Abd Hamid, N. N. (2021). Fast \(o(n)\) hybrid Laplace transform-finite difference method in solving 2D time fractional diffusion equation. Journal of Mathematics and Computer Science, 23(1), 110–123.

Singh, H., Pandey, R. K., Singh, J., & Tripathi, M. (2019a). A reliable numerical algorithm for fractional advection-dispersion equation arising in contaminant transport through porous media. Physica A: Statistical Mechanics and its Applications, 527, 121077.

Singh, J., Kilicman, A., Kumar, D., & Swroop, R. (2019b) Numerical study for fractional model of nonlinear predator-prey biological population dynamic system.

Sobhani, A., & Milev, M. (2018). A numerical method for pricing discrete double barrier option by Legendre multiwavelet. Journal of Computational and Applied Mathematics, 328, 355–364.

Song, L., & Wang W. (2013). Solution of the fractional Black–Scholes option pricing model by finite difference method. In Abstract and Applied Analysis (Vol. 2013) Hindawi.

Tuan, N. H., Aghdam, Y. E., Jafari, H., & Mesgarani, H. (2020). A novel numerical manner for two-dimensional space fractional diffusion equation arising in transport phenomena. Numerical Methods For Partial Differential Equations.

Verma, V., Prakash, A., Kumar, D., & Singh, J. (2019). Numerical study of fractional model of multi-dimensional dispersive partial differential equation. Journal of Ocean Engineering and Science, 4(4), 338–351.

Wyss, W. (2000). The fractional Black–Scholes equation.

Zhang, H., Liu, F., Turner, I., & Yang, Q. (2016). Numerical solution of the time fractional Black–Scholes model governing European options. Computers & Mathematics with Applications, 71(9), 1772–1783.

Zhang, X., Sun, S., Wu, L., et al. (2014). θ-difference numerical method for solving time-fractional Black–Scholes equation. Highlights of Sciencepaper Online, China Science and Technology Papers, 7(13), 1287–1295.

Acknowledgements

The authors would like to express their sincere thanks to the referees for their careful review of this manuscript and their useful suggestions which led to an improved version. José Francisco Gómez Aguilar acknowledges the support provided by CONACyT: cátedras CONACyT para jóvenes investigadores 2014 and SNI-CONACyT.

Author information

Authors and Affiliations

Contributions

HM: Conceptualization, methodology, validation, formal analysis, investigation; MB: Conceptualization, methodology, validation; YEA: Conceptualization, methodology, validation, formal analysis, investigation; JFG-A: Conceptualization, methodology, validation, writing-review and editing. All authors have read and agreed to the published version of the manuscript.

Corresponding author

Ethics declarations

Conflict of interest

The authors declare no conflict of interest.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Springer Nature or its licensor holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Mesgarani, H., Bakhshandeh, M., Aghdam, Y.E. et al. The Convergence Analysis of the Numerical Calculation to Price the Time-Fractional Black–Scholes Model. Comput Econ 62, 1845–1856 (2023). https://doi.org/10.1007/s10614-022-10322-x

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10614-022-10322-x

Keywords

- Time-fractional Black–Scholes equation

- Chebyshev polynomials of the third kind

- Linear interpolation

- Collocation method

- Convergence analysis