Abstract

While a growing body of literature has examined the link between green activities and firm innovation, little attention has been paid to the underlying mechanisms through which green activities take effect. This paper leverages the context of ISO 14001 certification among Chinese listed firms to investigate how the certification of environmental management system (EMS) to ISO 14001 shapes corporate technological innovation. Drawing from the resource-based view and the resource management perspective, we argue that EMS certification to ISO 14001 facilitates corporate technological innovation through the mediating effects of firms’ internal resource management practices, namely resource utilization, resource accumulation, and resource allocation. A difference-in-differences research design, together with the propensity score matching approach and the instrumental variable technique, provides corroborating evidence for our predictions. The current research not only makes substantial contributions to the literature, but also provides important ethical implications for both policymakers and firm managers.

Similar content being viewed by others

Explore related subjects

Discover the latest articles, news and stories from top researchers in related subjects.Avoid common mistakes on your manuscript.

Introduction

China has a dire need of a new paradigm that shifts away from the model of high input, high resource consumption, and high pollution, to sustainable growth to ease the conflict between economic & social development and the environmental damage it has caused in the past three decades.

– BBC, February 28, 2011

Along with the rapid industrialization, China has long been plagued by major environmental problems. Recently, the successive waves of thick smog in northern China have aroused worldwide concerns. For instance, the Guardian newspaper reports that 150,000 travelers headed abroad in last December in a bid to outrun the smog (The Guardian 2016). And CNN covers that acrid air incurred at least one million deaths a year in China and contributed to a third of all fatalities in major cities, on par with smoking (CNN 2017). China Daily in the USA has criticized that the local government in China was reluctant to impose sweeping change, for fear of increase in production costs and possible loss of jobs (China Daily USA 2016). Given the severity of pollution in today’s China, green activities, like ISO 14001 certification, seem an urgent need for Chinese firms to meet both the regulatory requirements and social expectations.

With the quick expansion of EMS certification all over the world, like ISO 14001 standard, many economists and management scholars have investigated its impact on firm performance (for a review, see Castka and Corbett 2015). Among the large body of literature, a growing number of studies in recent years have focused on the linkage between green management and firm innovation, given the importance of innovation to firms’ long-term competitiveness (Porter and van der Linde 1995) and a country’s economic growth (Aghion et al. 2013; Solow 1957). Nevertheless, extant studies do not seem to reach a unanimous conclusion. Some of the literature claims positive effects on firm innovation (see, for instance, Chang and Sam 2015; Chen and Chang 2013; Shu et al. 2016), whereas some other studies report mixed or even negative findings (see, for instance, Carrión-Flores et al. 2013; Wagner 2008, 2007; Brunnermeier and Cohen 2003). Such inconsistent findings in the literature are largely due to the paucity of theoretical frameworks, different research settings, and different measurements of firm innovation. Moreover, while few exceptions exist (see, for instance, Shu et al. 2016), most of the extant studies have not explored the underlying mechanisms through which green management takes effect. Therefore, new and rigorous research is still needed to provide broader-based empirical facts about how green management, like ISO 14001 certification, affects corporate technological innovation performance.

Given that R&D and innovation activities are resource-consuming and investment-intensive (Holmstrom 1989) and that firm’s resources are limited in supply at a certain time point (Barney 1991; Penrose 1959), internal resource management hereby affects firm’s innovation performance. On the other hand, prior studies have revealed that green management, like ISO 14001 certification, influences firm’s resource management practice (see, for instance, de Jong et al. 2014; Djupdal and Westhead 2015). Therefore, based on the resource-based view and the resource management perspective, the current research aims to investigate how ISO 14001 certification affects corporate technological innovation through the mediating effects of internal resource management practices. We argue that ISO 14001 certification improves the focal firm’s efficiency of resource utilization, facilitates its accumulation of R&D-related resources and capabilities, and encourages its allocation of resources for long-term goals, thus enhancing its innovation performance.

To empirically test our predictions, we leverage ISO 14001 certification among Chinese firms as the research context, because China has become the largest country for ISO 14001 certification, with 114,303 certificates issued as of 2015 (ISO 2015). Our sample includes 770 Chinese listed firms with 7670 firm-year observations. The observing time window is from 2005 to 2014. To capture corporate technological innovation, we utilize the patent data obtained from China’s State Intellectual Property Office (SIPO) and develop a computer program to match them with Chinese listed firms, as well as their subsidiaries. Using a difference-in-differences (DID) research design, we find corroborating evidence for our hypotheses. As robustness tests, we deploy various empirical techniques, which provide additional support to our arguments.

The current research seeks to make the following contributions. First, while extant studies have offered some valuable insights into the relationship between green activities and firm innovation, the current research contributes to the literature by providing a plausible theoretical framework based on the perspective of resource management. Second, the current research probes into the underlying mechanisms of how EMS certification takes effect, which largely remain unexplored in prior research, and thus, it complements the literature. Third, the current research also extends the theoretical perspective of resource management by providing empirical applications. Last but not the least, the current research makes significant empirical contributions as well. Unlike extant studies which mainly relied on cross-sectional survey data, the current research leverages panel data of a large sample and consolidates a variety of empirical techniques that deal with the endogeneity problems, thus effectively overcoming the empirical limitations in prior research.

Apart from the above-mentioned theoretical and empirical contributions, the current research also aims to come up with important ethical implications for both policymakers and firm managers. Distinct from much of the existing business ethics literature that recommends the government to play a more coercive role and formulate command-and-control policies, like deploying more stringent regulations to pressure organizations to take more green management initiatives (see, for instance, Li et al. 2016; Shu et al. 2016), the current research suggests policymakers play a more supportive role and take some market-oriented approaches, such as subsidies, tax deduction, and preferential policies, to motivate firms to voluntarily carry out green activities. Our findings may also deepen managers’ understanding of how green management synergizes innovation activities, which ultimately enhances corporate competitiveness. Accordingly, firm managers are advised to take a more strategic tack on EMS certification. We will talk about the ethical implications in more detail later in Discussion and Conclusion section.

Literature Review

The widespread and rapid expansion of EMS certification has garnered a substantial amount of interest from both economists and management scholars. Extant studies have primarily focused on the antecedents and outcomes of firms’ EMS certification (e.g., Ambec and Lanoie 2008; Baek 2015; Bansal and Hunter 2003; He et al. 2015, 2016; Iatridis and Kesidou 2016; for a review, see Castka and Corbett 2015). In recent years, a growing number of scholars in different fields, such as economics, management, and environmental science, have shifted their research focus to the impact of green activities on firm innovation. A majority of these studies reveal a positive relationship. Typically, Shu et al. (2016) find that green management facilitates corporate product innovation through the mediating effects of institutional benefits and that such positive effects are larger for radical product innovation than for incremental product innovation. Jakobsen and Clausen (2016) deploy the survey data of Norwegian firms and find that the adoption of environmental objectives has positive effects on firms’ innovation process. In addition, Rennings et al. (2006) use a survey of German firms and report that the implementation of EMS facilitates environmental product and process innovation.

A few other studies, however, find mixed or even negative effects of green activities on firm innovation. For instance, Wagner (2007, 2008) examines the impact of EMS implementation on different types of innovation and reveals that EMS implementation positively affects environmental and process innovation, rather than general and product innovation. Carrión-Flores et al. (2013) find that voluntary participation in pollution reduction activities may lead to an increase in environmental patents in the short run but a decrease in the long run. Accordingly, the following Table 1 provides a comprehensive review of the related literature in the past two decades.

Based on the literature review, most of the extant studies lack the theoretical framework, the absence of which weakens their arguments and leads to arbitrary results. Besides, while few exceptions exist (see, for instance, Chen and Chang 2013; Shu et al. 2016), extant studies have not paid enough attention to the underlying mechanisms through which green activities can take effect. With regard to their empirical analyses, extant studies have mainly relied on survey data. Such a cross-sectional data structure often incurs endogeneity problems and thus constrains the extent to which consistent conclusions can be drawn. Moreover, extant studies have primarily used survey items or established scales to capture firm innovation subjectively, which may result in common method bias. Instead, objective indicators like patents are of limited use in this literature, although they have been widely used in other technology and innovation research (Cohen et al. 2000; Griliches 1990; Trajtenberg 1990). In addition, most of the extant studies on the linkage between green activities and firm innovation are conducted in the context of developed economies. Nevertheless, due to the difference in institutional infrastructure, conclusions in prior research cannot be simply applied to emerging economies. Taken together, new and rigorous research, which aims to explore the latent channels and overcomes endogeneity bias, will contribute to the literature both theoretically and empirically.

Theory and Hypothesis

Founded on the idea that firm is a bundle of resources and resources determine firm performance (Penrose 1959), the resource-based view (RBV) suggests that firms’ sustainable competitive advantages are derived from valuable, rare, non-imitable and non-substitutable resources (Barney 1991; Wernerfelt 1984). Although the connection between resources and firms’ competitive advantages has been widely recognized, the RBV has long been criticized for its inability to uncover the process of resource management within firms, which undermines its explanatory power (Priem and Butler 2001). To make up for this deficiency, Sirmon et al. (2007) integrate the resource management perspective into the traditional RBV arguments and depict the comprehensive process through which firms effectively manage their resources to create and maintain competitive advantages.

Extant studies have examined how green activities reshape firms’ resources and capabilities, which in turn affect firm performance (see, for instance, de Jong et al. 2014; Djupdal and Westhead 2015). Following the literature, we ground our arguments on the RBV and the resource management perspective in the current research, given that innovation is characterized by resource-consuming and investment-intensiveness (Holmstrom 1989). In what follows, we investigate how green efforts via EMS certification affect corporate technological innovation through the mediating role of resource management process, including resource utilization, resource accumulation, and resource allocation.

Mediating Role of Resource Utilization

EMS certification improves firms’ efficiency of resource utilization (Darnall and Edwards 2006). In this regard, with specific requirements and documented standard, EMS certification drives firms to set environmental goals and to standardize environmental protection process during their daily operations. Such standardized process not only enables firms to better comply with environmental regulations, but also helps them to more efficiently handle environmental-related problems (de Jong et al. 2014; Porter and van der Linde 1995). Moreover, EMS certification requires firms to carry out cleaner production, which significantly lowers down firms’ pollution amounts and discharge capacity. Given that pollution is generally associated with an incomplete utilization of resources, the reduction in pollution incurred by EMS certification indicates the improved efficiency of resource utilization.

On the other side, the improved efficiency of resource utilization in turn facilitates corporate technological innovation. Specifically, the optimized process of resource utilization enables firms to refine the operational process, update the manufacturing technology, and adopt new materials, thus leading to product or process renewal (Park 2014; Porter and van der Linde 1995). Besides, the improvement of efficiency in resource utilization also saves resources, like capital and human resources, and managerial cognitive resources, for firms’ innovation activities. Given that firms’ resources are limited in supply at a certain time point and that innovation needs a significant amount of resource investments, the saved resources can be invested in R&D activities, thus promoting corporate technological innovation.

Based on the arguments above, we propose that:

Hypothesis 1

The certification of EMS with ISO 14001 facilitates corporate technological innovation through the mediating effect of resource utilization.

Mediating Role of Resource Accumulation

In addition, the effect of EMS certification on corporate technological innovation can be also channeled by the accumulation of R&D-related resources. Based on the RBV, resources are heterogeneously distributed and imperfectly mobile across firms. Such idiosyncratic and immobile resources contribute to firms’ competitive advantages (Barney 1991). Internal development and accumulation of resources increase causal ambiguity and thus enhance isolation mechanisms for firms that hold heterogeneous resources to sustain advantages. Hereby, we propose that the accumulation of resources, especially those related to R&D activities, mediates the positive relationship between EMS certification and corporate technological innovation.

On the one hand, EMS certification with ISO 14001 enables firms to accumulate R&D-related resources and build technological capabilities. To be specific, ISO 14001 standard follows the procedure of Plan-Do-Check-Act (PDCA), which is designed as an iterative process starting from the establishment of environmental objectives, then the implementation and the monitoring of process, and finally the actions for continuous improvement (ISO 2015). Following the PDCA model, firms with ISO 14001 certification can learn through the trail–feedback–evaluation process and develop tacit knowledge to better identify technological opportunities (Russo 2009). Besides, ISO 14001 certification requires firms to make continuous improvements to existing technologies and redesign the production or service delivery process. In such a scenario, firm managers have the incentives to increase investment in technology upgrading activities, thus accumulating R&D-related resources and technological capabilities.

On the other hand, the accumulation of R&D-related resources and technological capabilities in turn enhances corporate technological innovation. Specifically, based on the RBV, resources and capabilities contribute to firms’ competitive advantages. Accordingly, with the internal accumulation of R&D-related resources and technological know-how, firms become more capable of capturing the opportunities induced by the changing environment (Sirmon et al. 2007). Besides, the accumulation of R&D-related resources and technological capabilities facilitates firms to adopt cleaner production, resulting in more product or process innovation (Carrión-Flores and Innes 2010). In addition, the accumulation of R&D-related resources and technological capabilities enhances firms’ overall R&D capability, thus improving corporate technological innovation substantially (Jakobsen and Clausen 2016).

Taken together, we come up with the following hypothesis:

Hypothesis 2

The certification of EMS with ISO 14001 facilitates corporate technological innovation through the mediating effect of resource accumulation.

Mediating Role of Resource Allocation

Besides the two above-mentioned mediations, we propose the third underlying mechanism of the temporal orientation in resource allocation. Resource allocation is a core strategy for firms to manage innovation activities and predicts firm innovation performance (Klingebiel and Rammer 2014). Focusing on “time,” a common element of resource allocation decisions (Reilly et al. 2016), we argue that the long-term orientated allocation of resources mediates the positive relationship between EMS certification and corporate technological innovation.

First, EMS certification with ISO 14001 may lead to a long-term oriented resource allocation strategy. To be specific, ISO 14001 certification assists with firms’ overall management throughout the planning, organizing, implementing and monitoring process and is closely related to resource allocation decisions. In particular, ISO 14001 standard requires certified firms to incorporate values of sustainable development into their culture and routines (ISO 2015). Top managers are required to be actively involved in the goal-setting process for long-term development, whereas employees are encouraged to behave in conformity with firms’ long-term oriented routines (Aravind 2012). Following such routines, firm managers may invest heavily in employee training for both the concept and skills of sustainability, such as pollution prevention, energy saving, and resource recycling, and employees may extensively participate in such trainings and regard sustainability as a basic criterion when dealing with all kinds of issues. In sum, the certification of EMS with ISO 14001 helps to develop a company-wide long-term orientation in corporate culture, which directs managerial attention and firm resources to support long-term oriented activities.

Second, a long-term oriented allocation of resources in turn facilitates corporate technologic innovation. As Holmstrom (1989) points out, innovation activities are unpredictable, idiosyncratic and of long-term payoffs. Long-term resource commitment and company-wide support are needed to deliver innovation outcomes. With a long-term oriented resource allocation strategy, firms’ investment becomes more favorable to activities that benefit the future, such as innovation. In addition to the financial support, a long-term orientation in organizational culture provides a fertile environment for employees to develop creative solutions to daily operations and gives firms an impetus to establish an internal climate of never-ending innovativeness. With higher tolerances for early failures and greater rewards for long-term success, both the managers and employees are supposed to be actively engaged in promoting innovation activities (Manso 2011).

Taken together, we predict that:

Hypothesis 3

The certification of EMS with ISO 14001 facilitates corporate technological innovation through the mediating effect of resource allocation.

Based on the above arguments, the following Fig. 1 presents the theoretical framework of the current research.

Theoretical framework

Research Design and Methods

Research Setting

ISO 14001 standard is a worldwide certifiable environmental management system. It provides organizations with guidance to protect the environment and respond to the changing environment in balance with socioeconomic needs (ISO 2015). By certifying with ISO 14001 standard, organizations can develop environmental strategy that enables them to achieve the intended environmental outcomes. Since its release in 1996, ISO 14001 standard has been adopted by a growing number of organizations around the world. A total of 319,324 certificates were issued world-widely in 2015, with an annual growth of 8% (ISO 2015).

The current research leverages ISO 14001 certification among Chinese listed firms as the research context, because China has become the largest country for ISO 14001 certification as of 2015 (ISO 2015). Research findings and conclusions about ISO 14001 certification in China thus have great generality in other contexts. Although ISO 14001 certification occurs at the facility level (Aravind and Christmann 2011; King et al. 2005), the current research is conducted at the firm level, because such facility-level certification of ISO 14001 standard inevitably incurs company-wide influences.

Since the Chinese listed firms certify with ISO 14001 standard for reasons other than innovation, such proactive environmental strategy can be considered plausibly exogenous for their technological innovation outcome. This is attractive for our purpose by enabling us to use a difference-in-differences (DID) design to identify the causal effect of ISO 14001 certification on corporate technological innovation performance, using the uncertified firms and yet-to-certify firms as a control group. Such a DID research design has some key advantages. First, it rules out omitted trends that are correlated with ISO 14001 certification and technological innovation performance in both certified firms (the treatment group) and uncertified/yet-to-certify firms (the control group). Second, it also controls for constant unobserved differences between the treatment and the control groups. Third, the Chinese listed firms certify with ISO 14001 standard at different times. Therefore, compared with studies with a single “shock” that is applied to all sample firms at a single point of time, our research has stronger identification because the identified causal effect is less likely to be contaminated by a coinciding event that could have driven a similar outcome. Last but not the least, as the control group includes not only uncertified firms but also those firms that have not certified the ISO 14001 standard up to the time of treatment, it enables us to more precisely estimate the treatment effect, because yet-to-certify firms are a good approximation of the counterfactual of how already-certified firms would have performed if they had not certified with the ISO 14001 standard.

Sample and Data

To implement this study, we constructed a unique database by matching Chinese patents obtained from China’s State Intellectual Property Office (SIPO) to Chinese listed firms and their subsidiaries, in a similar way to Hall et al.’s (2001) pioneering work of matching USPTO patents to listed firms in Compustat.Footnote 1 In brief, we first retrieved firm and subsidiary information from the WIND Info database (www.wind.com.cn) that collects and codes such data based on listed firms’ annual reports. In the next step, we followed the NBER patent data project (Bessen 2009) and developed a computer program, which is based on the Levenshtein edit distance (Levenshtein 1966), to match patents in the SIPO database, which contains over several million published patent applications, to Chinese listed firms and their subsidiaries. In the final step, we conducted three independent sets of manual check to make sure those computers outputted name pairs were truly matched.

For the purpose of the DID design in the current research, we limited the sample to the period from 2005, when Chinese listed firms began to publicize their Corporate Social Responsibility (CSR) report, to 2014, when the truncation problem of patent filings could be minimized.Footnote 2 The sample firms are all listed firms on the main boards of the Shanghai and Shenzhen Stock Exchanges in China and have filed at least ONE single patent in both pre- and post-certification periods.Footnote 3 Besides, we excluded firms in finance and insurance industries, because they were heavily regulated by the government. The final sample contained 770 listed firms with 7670 firm-year observations.

Variables and Measures

Dependent Variable

We deploy patent data to capture corporate technological innovation performance, which have been widely used in other technology and innovation research (Cohen et al. 2000; Griliches 1990; Trajtenberg 1990). Using patents as the proxy of technological innovation performance has some obvious virtues. Compared with self-reported survey data, patent data are objective and publicly available. Besides, they are useful for large samples and are readily replicable for follow-up research (Arora et al. 2014). In addition, patent data mainly indicate innovations that are significant enough to be patentable and thus focus on a narrower set of more radical innovations, while exclude incremental innovations which only represent very minor inventive steps (Wagner 2007).

Following prior research (see, for instance, Carrión-Flores et al. 2013; Chang and Sam 2015; Wagner 2007), we create the variable Total patent flow as the dependent variable in the main analyses, which counts the number of patent filings by the focal firm in a certain year. In robustness test, we break down Total patent flow into different types of patents.

Independent Variable

To identify the effect of ISO 14001 certification, we create a dummy variable ISO 14001 certification, which equals 1 in years after the focal firm certified with the ISO 14001 standard, and 0 otherwise.Footnote 4 We obtain the information of Chinese listed firms’ ISO 14001 certification in their annual CSR reports, which disclose information like whether or not to certify with ISO 14001 standard, the year of certification, subsequent improvements, and so on. And the annual CSR reports of Chinese listed firms are available in the CSMAR database.

Mediating Variables

Based on our theoretical framework of resource management, we propose that Resource utilization efficiency, Resource accumulation, and Resource allocation for the long-term orientation mediate the effect of ISO 14001 certification on corporate technological innovation performance. To measure Resource utilization efficiency, we deploy the information of pollution cost of the focal firm in a given year, because pollution generally reflects an incomplete utilization of resources (Porter and van der Linde 1995). According to the 369th Decree of China’s State Council, which came into force on July 1, 2003, firms that discharge pollutants to the environment, including waste water, gas emission, solid waste, and noise, should pay the pollution discharge fees based on their amount of pollutants. Therefore, a certain firm’s pollution level can be measured by its pollution discharge fees. For instance, firms with heavier pollution are supposed to pay a larger amount of fees. Such pollution discharge fees are recorded as a cost item in the financial statement of Chinese listed firms. Thus, we calculate the variable Resource utilization efficiency as 1 minus the ratio of pollution cost to total sales of the focal firm in a given year, which can be formally denoted as:

Next, given that firms’ investments in technology upgrading activities can be considered as innovation-related resource accumulation or capability building (Helfat 1997), we hereby measure the variable Resource accumulation accordingly. To be specific, we refer to the annual reports and CSR reports of sample firms and conduct content analysis to code their investments relating to technological improvement, including “technology upgrading,” “technical transformation,” “new technology,” and “new process.” Then, we aggregate the amount of expenditures on these activities and calculate its ratio to total sales of the focal firm in a given year, which can be formally denoted as:

Then, with regard to Resource allocation for the long-term orientation, we refer to the CSR reports of sample firms as well, because they disclose detailed information of firms’ activities on sustainability. Specifically, we code activities involving “future development,” “learning,” “employee training,” “energy saving,” “recycling,” and “sustainability.” Then, we calculate the frequency of such activities for the focal firm in a given year and thus generate a count variable.Footnote 5

Control Variables

For all analyses, we control for Firm size, which is measured as the logarithm of the number of employees of the focal firm in a given year. We also control for the focal firm’s ownership type by a dummy variable, SOE, which equals 1 if the focal firm is majority-owned or ultimately controlled by the Chinese government (at the central or local level), and 0 otherwise. Information about sample firms’ ownership type is available in the CSMAR database. Besides, we control for the focal firm’s financial conditions, which have been found to affect corporate innovation activities (Hall 2002). Specifically, Debt ratio is measured as the ratio of total debts to total assets for the firm in a given year; Retained earnings is the logarithm of the firm’s retained profits in a given year; ROA is the ratio of the firm’s net profits to its total assets in a given year. Moreover, we control for corporate governance indicators, because prior studies have revealed that corporate governance usually influences firm innovation (for a review, see Ahuja et al. 2008). Following extant studies, we create two variables to measure corporate governance, namely Ownership concentration and Managerial shareholding ratio. The former is calculated the Herfindahl–Hirschman index (HHI) of the TEN largest shareholders, while the latter is captured by the percentage of equity owned by the top manager. Then, we control for R&D intensity, which is measured as the ratio of R&D expenditure to total sales of the focal firm in a given year. In addition, we control for the industry-level characteristics of innovation activities, because some industries are more involved in innovation and patenting activities than other industries. Accordingly, we create two variables, namely Ratio of firms with R&D department in the focal industry and Ratio of new product sales to total sales in the focal industry. The former variable reflects the input intensity of innovation activities in the focal industry, whereas the latter variable indicates the output intensity of innovation activities in the focal industry. Information of the two variables is available in China Statistical Yearbook on Science and Technology. Last but not the least, we include a full set of firm and year dummies to control for any fixed, unobserved firm heterogeneity, as well as macroeconomic factors that may affect firms’ innovation.

Statistical Approach

Because of the count nature of the dependent variables, we use the negative binomial regression model to analyze our data. A likelihood-ratio test of the over-dispersion parameter also confirms that negative binomial regressions provide a good fit. Since we predict that ISO 14001 certification enhances corporate technological innovation performance through improved efficiency of resource utilization (Hypothesis 1), resource accumulation (Hypothesis 2), and resource allocation for the long-term orientation (Hypothesis 3), we adopt a well-established approach for mediation test developed by Baron and Kenny (1986). The causal steps of Baron and Kenny’s approach can be specified in the following equations:

where Yit is a dependent variable, Mit stands for a mediating variable, β0 is the intercept, β1 identifies the effect of ISO 14001 certification, Xit is a vector of controls for firm i in year t, Fi is a set of firm fixed effects, λt is a set of year fixed effects, and εit is the error term. It is noteworthy that different firms certified with ISO 14001 standard at different times and that firms’ ownership might change over time. That means both ISO 14001 certificationit and SOEit are time variant; therefore, they can be included in the model with the presence of firm and year fixed effects. We estimate the unconditional fixed-effects negative binomial model by including dummy variables to represent firm fixed effects (Allison and Waterman 2002). Because firm fixed effects have already captured fixed industry differences (e.g., technological opportunity and patent effectiveness), industry dummies cannot be included.Footnote 6 In separate analyses, we also estimate Poisson and OLS models and the results were qualitatively similar and are available upon request.

Validating the Parallel Trend Assumption for the DID Design

For difference-in-differences estimations to be valid, the parallel trend assumption must hold, which means that the average outcome for the treatment group (i.e., ISO 14001 certified firms) and control group (i.e., uncertified firms and yet-to-certify firms) would have followed parallel paths over time in the absence of the treatment (i.e., ISO 14001 certification). Accordingly, we plot and inspect the temporal trends of the dependent variables for the treatment and control groups in both the pre- and post-certification periods. As shown in the five graphs in Fig. 2, the average numbers of applications for different types of patents between the two groups generally exhibit a parallel trend up to the year of ISO 14001 certification and then begin to diverge after that. In addition, the graphs show that there is no Ashenfelter’s dip in the pre-certification period (Ashenfelter 1978), meaning that if the regression results are significant, they are NOT caused by a pre-certification drop in the dependent variables of the treatment group, thus further strengthening our confidence in the DID design.

Technological innovation performance for the certified versus uncertified firms around ISO 14001 certification. aTotal patent flow, bInvention patent flow, cUtility model flow, dDesign patent flow, eNon-invention patent flow

Results

Table 2 presents the descriptive statistics and correlations for all the variables. To address the potential multicollinearity problem, we examine the variance inflation factor (VIF) values for the variables. The average VIF turns out to be 1.32, far below the recommended threshold (VIF ≤ 10.00).

DID Regressions

We first examine Hypothesis 1, which predicts that EMS certification with ISO 14001 enhances corporate technological innovation performance through the mediation of improved efficiency of resource utilization. The results are reported in Table 3. Model 1 regresses Total patent flow on ISO 14001 certification; the estimated coefficient is positive and statistically significant at the p < 0.01 level, indicating that ISO 14001 certified firms significantly increase their patent applications compared with uncertified firms and yet-to-certify firms. Model 2 regresses the mediator Resource utilization efficiency on ISO 14001 certification. The estimated coefficient on ISO 14001 certification is positively significant at the p < 0.01 level, suggesting that ISO 14001 certification improves firms’ efficiency of resource utilization in the post-certification period and thus saves more resources for innovation activities. Then, Model 5 regresses Total patent flow on both ISO 14001 certification and Resource utilization efficiency. The positively significant coefficient on Resource utilization efficiency (p < 0.01) indicates that improved efficiency of resource utilization enhances corporate technological innovation performance. Moreover, after adding the mediator Resource utilization efficiency, the estimated coefficient on ISO 14001 certification becomes smaller and insignificant compared with Model 1, thus supporting our prediction in Hypothesis 1.

Furthermore, we conduct the extended Sobel test (Sobel 1982) using the bootstrapping mediation approach (Zhao et al. 2010), to test whether the mediating effect of Resource utilization efficiency is statistically significant. The extended Sobel test model is specified as:

where a and sa are the coefficient and standard error from the bootstrapping for the impact of ISO 14001 certification on Resource utilization efficiency, while b and sb are the coefficient and standard error from the bootstrapping for the impact of Resource utilization efficiency on total patent flow when ISO 14001 certification is also included in the model. The result of Sobel test for the mediation of Resource utilization efficiency is statistically significant at the p < 0.05 level (Zvalue = 2.415, a = 0.026, sa = 0.006, b = 0.916, sb = 0.315), which provides additional support for the mediating role of Resource utilization efficiency. Following Preacher and Kelley (2011), we also calculate the ratio of mediating effect to total effect.Footnote 7 As can be seen in the bottom of Model 5, the mediation of Resource utilization efficiency takes up to 32.3% in the total effect.

We continue to examine Hypothesis 2 and Hypothesis 3 in similar approaches. Due to limited space, we do not repeat the results step by step. Overall, Models 1, 3 and 6 in Table 3 offer strong support to Hypothesis 2. The Sobel test provides additional support for the mediating role of Resource accumulation, which takes up to 36.0% in the total effect. Models 1, 4 and 7 in Table 3 provide corroborating evidence for Hypothesis 3, and the Sobel test suggests that Resource allocation, as a mediator, takes 30.3% in the total effect.

Robustness Check

Mediation Test with the Simultaneous Equations Approach

Although the above results of Baron and Kenny’s approach have shown that each mediator is individually significant in separate tests, it is unclear whether the three mediators are still significant when they are put together in one model. Besides, recent developments in the research methods literature also have pointed out some other limitations in Baron and Kenny’s approach. For instance, some scholars have argued that a significant total effect of X on Y is not necessary for mediation to occur, because mediating variables may produce “indirect effects” that cancel out each other (Shrout and Bolger 2002; Preacher and Hayes 2008). Moreover, separate tests in Baron and Kenny’s approach may suffer from omitted variable problems, leading to biased coefficient estimates (Judd and Kenny 1981; Preacher and Hayes 2008). As well, separate tests assume that the two error terms in Eqs. (2) and (3) are uncorrelated with each other. However, if the two error terms are correlated due to unobserved variables that affect both M and Y, coefficient estimates in Eq. (3) will be biased and inconsistent (Shaver 2005).

A recent approach recommended by Preacher and Hayes (2008), and increasingly adopted by management scholars (e.g., Agarwal et al. 2016), addresses the above limitations by estimating Eqs. (2) and (3) simultaneously as a system and allowing their error terms to be freely correlated.Footnote 8 This simultaneous equations approach also easily incorporates multiple mediators. To implement the simultaneous equations approach, we specify a set of seemingly unrelated regressions (SUR) that contains four equations in one single test: the first three equations regress the mediators on ISO 14001 certification and all the control variables, respectively, and the fourth one regresses the dependent variable on ISO 14001 certification, the three mediators, and all the control variables.Footnote 9 The error terms of the four equations are allowed to be correlated. Table 4 reports the SUR results. The dependent variable Total patent flow here is transformed to the natural logarithm of one plus its respective count, because the SUR framework is applicable to linear regressions. As can be seen in Model 4, the positive and significant coefficients on the three mediators provide additional support for our mediation arguments.

In Table 5, we compute and report the “indirect effect” of each mediating channel. As it shows, the indirect effects via each mediator and the joint indirect effect are all positive and significant.

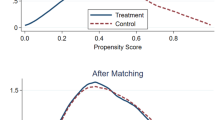

Propensity Score Matching Approach

Next, to strengthen the ‘equal trend’ assumption between the treatment group and the control group and to alleviate the concern that the difference in corporate technological innovation performance in the post-certification period is incurred by some observed factors other than ISO 14001 certification per se, we deploy the propensity score matching (PSM) approach to select firms that were more similar at the time of treatment for comparison. Such a matching approach allows us to include a number of covariate controls to adjust for potential differences in trends over time.

When applying the PSM procedure, we first estimate a Probit model using all 770 sample firms to calculate the propensity scores, which measure the extent of matching between the certified and uncertified firms in multiple dimensions. Specifically, propensity scores are calculated as p(X) = Pr[D = 1|X] = E[D|X], where X is the multidimensional vector of characteristics and D is the probability of receiving the treatment (i.e., ISO 14001 certification). With regard to the vector X, we include several dimensions that might affect firms’ propensity to certify with the ISO 14001 standard, namely Firm size, Ownership type, Debt ratio, Retained earnings, ROA, Corporate governance, R&D expenditure, Industry-level characteristics of innovation activities, as well as a full set of year and firm dummies. The Probit model is specified as:

With calculated propensity scores, we then use the nearest-neighbor matching method to search, both backwards and forwards, for the closest control samples (Corbett et al. 2005). It turns out that 246 ISO 14001 certified firms successfully find their matched uncertified counterparts. Then, we re-conduct the DID regressions with negative binomial model on the matched sample, which includes 492 firms. The results are reported in Table 6.Footnote 10 As can be seen, with the matched sample, the estimated coefficients on ISO 14001 certification are positive and statistically significant through Models 1–3, highly consistent with those in Table 6, thus providing additional support to our arguments.

Two-Stage Least Square Regressions

Although the combination of the DID research design and PSM approach helps to mitigate the endogeneity problem substantially, there might still be another potential endogeneity concern, due to the existence of unobserved time-variant factors that affect both firms’ ISO 14001 certifying behavior and their technological innovation outcomes. Therefore, we further deploy the instrumental variable technique, i.e., the two-stage least square regressions, to exclude the potential bias incurred by omitted time-variant factors. This method requires the selected instrumental variable to be uncorrelated with the dependent variable, but to have strong correlation with the independent variable. After an extensive search, we eventually find one variable that satisfies this prerequisite, both conceptually and empirically: The degree of air pollution in the focal city, the information of which is available in China Statistical Yearbook on Environment. Conceptually, greater degree of air pollution usually leads more firms to certify with ISO 14001 standard, but it seems to have nothing to do with firms’ technological innovation performance. Empirically, the correlation coefficient between the instrumental variable and the independent variable is 0.670 (p < 0.001), whereas the correlation between the instrumental variable and the dependent variable is 0.020 (p = 0.126).

Results of the 2SLS approach are presented in Table 7. Model 1 reports the first-stage result, which regresses ISO 14001 certification on the instrumental variable The degree of air pollution in the focal city, as well as all the control variables. The estimated coefficient on the instrumental variable is positive and statistically significant at the p < 0.05 level, confirming its relevance to the independent variable. Moreover, the Cragg–Donald Wald F statistic is 21.221, much larger than the critical value (F = 16.38) of Weak Identification Test suggested by Staiger et al. (1997), meaning that our instrumental variable is NOT weak. Models 2–6 report the second-stage results, which regress the dependent variables on the predicted value of the independent variable obtained from the first stage. Consistent with our earlier results, the estimated coefficients on the predicted ISO 14001 certification are all positive and statistically significant. Therefore, the instrumental variable technique suggests that our results are NOT biased by omitted variables.

Discussion and Conclusion

Based on the resource-based view, this study investigates the effect of ISO 14001 certification on corporate technological innovation. Leveraging ISO 14001 certification among Chinese listed firms as the research context, our findings show that the certification of ISO 14001 facilitates corporate technological innovation. Moreover, the results reveal that resource management practices, including resource utilization, resource accumulation and resource allocation, act as the underlying mechanisms through which ISO 14001 certification may take effect.

Theoretical Contributions

The current research makes important theoretical contributions to the literature. First, while a growing body of literature has investigated the relationship between green activities and firm innovation, most of them lack a theoretical framework. The current research, however, leverages the framework of resource management perspective and argues that ISO 14001 certification improves company-wide practices of resource management, which enable firms to better invest their resources in R&D and innovation activities. Therefore, the current research advances the understanding of the “environment–innovation” relationship, and also echoes to the classical notion in strategic management research that firms’ resources and capabilities bring about competitive advantages (Barney 1991).

Second, with few exceptions (see, for instance, Shu et al. 2016), extant studies on the relationship between EMS certification and firm innovation have largely left the latent channels unexplored as a black box. Instead of a simple replication study, the current research aims to extend the literature by probing into the underlying mechanisms through which EMS certification affects firm innovation. Toward this end, it focuses on the firms’ internal resource management and reveals that the certification of environmental management system with ISO 14001 standard enables firms to utilize resources more efficiently, to better accumulate R&D-related resources and capabilities, as well as to allocate resources for goals of longer terms, which in turn facilitates firms’ technological innovation. In this way, the current research contributes to the literature by uncovering plausible underlying mechanisms through which EMS certification takes effect.

Third, prior research on resource management has mainly relied on theoretical modeling, but lacked empirical verification (see, for instance, Sirmon and Hitt 2003; Sirmon et al. 2007), probably due to the difficulty in finding an ideal research setting. The current research leverages the context of ISO 14001 certification among Chinese firms and develops appropriate measures for the key constructs. Therefore, the current research complements the literature on resource management by providing empirical applications for the core argument that firms can create sustainable competitive advantages through the internal resource management (Sirmon and Hitt 2003).

Empirical Contributions

The current research also makes substantial empirical contributions to the literature. To be specific, prior studies on the link between green activities and firm innovation mainly relied on cross-sectional survey data (see, for instance, Chen and Chang 2013; Jakobsen and Clausen 2016; Shu et al. 2016), which usually incur endogeneity problems. Besides, they often used survey items to capture firm innovation, which might lead to common method bias and measurement errors. Instead, the current research deploys second-hand panel data of a large sample and consolidates a variety of empirical techniques, including the DID regression, PSM approach and the instrumental variable technique, thus systematically excluding the endogeneity issues. Moreover, it introduces the patent data, which are objective, publicly available and have been widely used in other technology and innovation research, into this strand of literature, thus addressing the common method bias and measurement errors.

Ethical Implications

The current research provides important ethical implications for policymakers. To be specific, with the growing conflict between human and nature in emerging economies, the traditional way of socioeconomic development, which is usually at the expense of the environment, is no longer sustainable. New patterns of development that harmonize economic growth and environmental protection are hereby in great need. On the other hand, emerging economies like China and India have put forward their national development strategy of becoming an innovation-oriented country. Therefore, the government in emerging economies is faced with considerable pressures to balance the multiple needs among socioeconomic development, environmental protection and technological innovation. A sustainable national system is thereupon needed to reconcile the multiple missions. ISO 14001 standard, as a certified environmental management system, not only reduces the monitoring cost for the government (He et al. 2016), but also minimizes the negative impact of production activities on the environment (Potoski and Prakash 2004). In addition, our results show that the certification of ISO 14001 standard facilitates the emergence of new technology and contributes to firm innovation. Accordingly, the government is suggested to incentivize more firms to certify with ISO 14001 standard by subsidizing the expenditures of certification and sequential maintenance, or providing preferential tax for the certified firms.

As well, the current research conveys important ethical implications for firm managers. Specifically, firms, especially those in emerging economies, are often constrained by limited resources and underdeveloped technology. Therefore, with the conventional wisdom of environmental protection, which believes that it comes at an additional cost imposed on firms and distracts limited resources away from value-enhancing activities like innovation, thus eroding firms’ competitive advantages (Ambec and Lanoie 2008), firm managers are hesitated whether they should allocate limited resources to green activities and ponder how they can benefit from EMS certification with ISO 14001 standard. Nevertheless, results in the current research have challenged this traditional paradigm and revealed that green management, such as ISO 14001 certification, can lead to a synergy between environmental protection and firm innovation. For instance, by certifying EMS with ISO 14001 standard, firms are able to cultivate their ability of using clean energy, recycling, and disposing waste to enhance the operation efficiency and thus reserve more resources to invest R&D and innovation activities. Besides, upon ISO 14001 certification, firms are motivated to upgrade their incumbent technologies, which strengthens their technical capabilities and accumulates R&D-related resources, thus facilitating innovation performance. Moreover, ISO 14001 certification shifts firms’ attention to sustainability and encourages firms to increase resource allocation for long-term activities, like innovation. Therefore, firm managers are suggested to actively certify EMS with ISO 14001 standard and integrate its required PDCA procedures into firms’ daily operations, so as to facilitate corporate innovation and competitive advantages.

Limitations and Future Directions

Notwithstanding the above contributions and implications, the current research has several limitations that encourage future investigations. First, in the current research, we are not able to accurately distinguish between symbolic and substantive ISO 14001 certification (Aravind and Christmann 2011; Boiral 2007), due to the unavailability of related information, which might bias our results. As a suboptimal remedy which is not presented in the manuscript but available upon request, we leverage firms’ exporting information to indirectly capture the quality of ISO 14001 implementation, because exporting firms, especially those with customers in developed countries, are found to comply better with ISO 14001 standard (Bansal and Hunter 2003; Christmann and Taylor 2001; King et al. 2005). Although the results with firms’ exporting intensity controlled hold consistent, future research is suggested to further address this issue with in-depth case studies and tell apart symbolic versus substantive certification more precisely. Second, the current research deploys patents as the proxy for innovation performance. Nevertheless, some types of innovation are not protected by patents, like process innovation and business model innovation. Future research needs to come up with alternative measures that reflect corporate innovation performance thoroughly. Third, the current research simply uses patent counts to capture firms’ innovation performance, regardless of the importance of each patent and whether the focal patent has been cited by subsequent innovation. Future research, therefore, is encouraged to weight patents by the citation information, which may be a better proxy for innovation performance.

Notes

This was part of a larger patent database construction project for all Chinese listed firms. An extended report on this project is available upon request.

According to China’s Patent Law, it takes 18 months from the patent filing date to its disclosure date. Therefore, by the time of the current research, patents that were filed in 2015 or 2016 might not be disclosed, which leads to a serious truncation problem.

Firms that have not filed any patents during the sample period are automatically dropped out in the regression process.

We aggregate the facility-level ISO 14001 certification up to the firm level, meaning that when (any) one of the focal listed firms’ facilities certified with the ISO 14001 standard, our independent variable takes the value of 1, and 0 otherwise.

As a robustness test, we also aggregate the amount of investments in such long-term oriented activities and calculate its ratio to total sales of the focal firm in a given year. The regression results are qualitatively consistent with those of the count variable and are available upon request.

As stated above in Variables and Measures section, relevant time-variant industry effects, i.e. industry-level characteristics of innovation/patenting activities, are controlled by two particular variables in the empirical models.

Ratio of mediating effect to total effect = a * b/(a * b + c′), where c′ is the estimated coefficient on the independent variable (i.e. ISO 14001 certification) from the bootstrapping of the third step.

Note that Eq. (1) is not estimated by the simultaneous equation approach. As explained above, the first step in the traditional Baron and Kenny’s approach is not necessary for mediation to occur.

The estimation steps of this approach can be found at http://www.ats.ucla.edu/stat/stata/faq/mulmediation.htm. See Agarwal et al. (2016) for a recent application in management.

Due to limited space, the results of the first-step probit regression are omitted here, but are available upon request.

Abbreviations

- CMV:

-

Common method variance

- CSR:

-

Corporate social responsibility

- DID:

-

Difference-in-differences

- EMS:

-

Environmental management system

- HHI:

-

Herfindahl–Hirschman index

- ISO:

-

International Standardization Organization

- PDCA:

-

Plan-Do-Check-Act

- PSM:

-

Propensity score matching

- RBV:

-

Resource-based view

- SIPO:

-

State Intellectual Property Office

- SOE:

-

State-owned enterprises

- VIF:

-

Variance inflation factor

- 2SLS:

-

Two-stage least square

References

Agarwal, R., Campbell, B. A., Franco, A. M., & Ganco, M. (2016). What do I take with me? The mediating effect of spin-out team size and tenure on the founder-firm performance relationship. Academy of Management Journal, 59(3), 1060–1087.

Aghion, P., Van Reenen, J., & Zingales, L. (2013). Innovation and institutional ownership. American Economic Review, 103(1), 277–304.

Ahuja, G., Lampert, C. M., & Tandon, V. (2008). Moving beyond Schumpeter management research on the determinants of technological innovation. Academy of Management Annals, 2(1), 1–98.

Allison, P. D., & Waterman, R. P. (2002). Fixed-effects negative binomial regression models. Sociological Methodology, 32(1), 247–265.

Ambec, S., & Lanoie, P. (2008). Does it pay to be green? A systematic overview. Academy of Management Executive, 22(4), 45–62.

Aravind, D. (2012). Learning and innovation in the context of process-focused management practices: The case of an environmental management system. Journal of Engineering and Technology Management, 29(3), 415–433.

Aravind, D., & Christmann, P. (2011). Decoupling of standard implementation from certification: Does quality of ISO 14001 implementation affect facilities’ environmental performance? Business Ethics Quarterly, 21(1), 73–102.

Arora, A., Belenzon, S., & Rios, L. A. (2014). Make, buy, organize: The interplay between research, external knowledge, and firm structure. Strategic Management Journal, 35(3), 317–337.

Ashenfelter, O. (1978). Estimating the effect of training programs on earnings. Review of Economics and Statistics, 60(1), 47–57.

Baek, K. (2015). The diffusion of voluntary environmental programs: The case of ISO 14001 in Korea, 1996–2011. Journal of Business Ethics. doi:10.1007/s10551-015-2846-3.

Bansal, P., & Hunter, T. (2003). Strategic explanations for the early adoption of ISO 14001. Journal of Business Ethics, 46(3), 289–299.

Barney, J. (1991). Firm resources and sustained competitive advantage. Journal of Management, 17(1), 99–120.

Baron, R. M., & Kenny, D. A. (1986). The moderator–mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. Journal of Personality and Social Psychology, 51(6), 1173–1182.

BBC News. (2011). China pollution ‘threatens growth’, February 28, 2011.

Bessen, J. (2009). NBER PDP project user documentation: Matching patent data to Compustat firms. http://www.nber.org/~jbessen/matchdoc.pdf.

Boiral, O. (2007). Corporate greening through ISO 14001: A rational myth? Organization Science, 18(1), 127–146.

Brunnermeier, S. B., & Cohen, M. A. (2003). Determinants of environmental innovation in US manufacturing industries. Journal of Environmental Economics & Management, 45(2), 278–293.

Carrión-Flores, C. E., & Innes, R. (2010). Environmental innovation and environmental performance. Journal of Environmental Economics & Management, 59(1), 27–42.

Carrión-Flores, C. E., Innes, R., & Sam, A. G. (2013). Do voluntary pollution reduction programs (VPRs) spur or deter environmental innovation? Evidence from 33/50. Journal of Environmental Economics & Management, 66(3), 444–459.

Castka, P., & Corbett, C. J. (2015). Management systems standards: Diffusion, impact and governance of ISO 9000, ISO 14000, and other management standards. Foundations & Trends in Technology Information & Operations Management, 7(3–4), 161–379.

Chang, C. H., & Sam, A. G. (2015). Corporate environmentalism and environmental innovation. Journal of Environmental Management, 153, 84–92.

Chen, Y. S., & Chang, C. H. (2013). The determinants of green product development performance: Green dynamic capabilities, green transformational leadership, and green creativity. Journal of Business Ethics, 116(1), 107–119.

China Daily USA. (2016). Lack of long-term pollution control behind heavy smog, December 20, 2016.

Christmann, P., & Taylor, G. (2001). Globalization and the environment: Determinants of firm self-regulation in China. Journal of International Business Studies, 32(3), 439–458.

Corbett, C. J., Montes-Sancho, M. J., & Kirsch, D. A. (2005). The financial impact of ISO 9000 certification in the United States: An empirical analysis. Management Science, 51(7), 1046–1059.

CNN. (2017). Beijing’s smog: A tale of two cities. January 15, 2017.

Cohen, W. M., Nelson, R. R., & Walsh, J. P. (2000). Protecting their intellectual assets: Appropriability conditions and why US manufacturing firms patent (or not) (No. w7552). National Bureau of Economic Research.

Darnall, N., & Edwards, D. (2006). Predicting the cost of environmental management system adoption: The role of capabilities, resources and ownership structure. Strategic Management Journal, 27(4), 301–320.

de Jong, P., Paulraj, A., & Blome, C. (2014). The financial impact of ISO 14001 certification: Top-line, bottom-line, or both? Journal of Business Ethics, 119(1), 131–149.

Djupdal, K., & Westhead, P. (2015). Environmental certification as a buffer against the liabilities of newness and smallness: Firm performance benefits. International Small Business Journal, 33(2), 148–168.

Griliches, Z. (1990). Patent statistics as economic indicators: A survey (No. w3301). National Bureau of Economic Research.

Hall, B. H. (2002). The financing of research and development. Oxford Review of Economic Policy, 18(1), 35–51.

Hall, B. H., Jaffe, A. B., & Trajtenberg, M. (2001). The NBER patent citation data file: Lessons, insights and methodological tools. NBER working paper no. 8498, National Bureau of Economic Research.

He, W., Liu, C., Lu, J., & Cao, J. (2015). Impacts of ISO 14001 adoption on firm performance: Evidence from China. China Economic Review, 32, 43–56.

He, W., Yang, W., & Choi, S. J. (2016). The interplay between private and public regulations: Evidence from ISO 14001 adoption among Chinese firms. Journal of Business Ethics. doi:10.1007/s10551-016-3280-x.

Helfat, C. E. (1997). Know-how and asset complementarity and dynamic capability accumulation: The case of R&D. Strategic Management Journal, 18(5), 339–360.

Holmstrom, B. (1989). Agency costs and innovation. Journal of Economic Behavior & Organization, 12(3), 305–327.

Iatridis, K., & Kesidou, E. (2016). What drives substantive versus symbolic implementation of ISO 14001 in a time of economic crisis? Insights from Greek manufacturing companies. Journal of Business Ethics. doi:10.1007/s10551-016-3019-8.

ISO. (2015). http://www.ISO.org/ISO/home/standards/management-standards/ISO14000.htm.

Jaffe, A. B., & Palmer, K. (1997). Environmental regulation and innovation: A panel data study. The Review of Economics and Statistics, 79(4), 610–619.

Jakobsen, S., & Clausen, T. H. (2016). Innovating for a greener future: The direct and indirect effects of firms’ environmental objectives on the innovation process. Journal of Cleaner Production, 128, 131–141.

Judd, C. M., & Kenny, D. A. (1981). Process analysis: Estimating mediation in treatment evaluations. Evaluation Review, 5(5), 602–619.

King, A. A., Lenox, M. J., & Terlaak, A. (2005). The strategic use of decentralized institutions: Exploring certification with the ISO 14001 management standard. Academy of Management Journal, 48(6), 1091–1106.

Klingebiel, R., & Rammer, C. (2014). Resource allocation strategy for innovation portfolio management. Strategic Management Journal, 35(2), 246–268.

Lanjouw, J. O., & Mody, A. (1996). Innovation and the international diffusion of environmentally responsive technology. Research Policy, 25(4), 549–571.

Levenshtein, V. I. (1966). Binary codes capable of correcting deletions, insertions, and reversal. Soviet Physics Doklady, 10(8), 707–710.

Li, D., Huang, M., Ren, S., Chen, X., & Ning, L. (2016). Environmental legitimacy, green innovation, and corporate carbon disclosure: Evidence from CDP China 100. Journal of Business Ethics. doi:10.1007/s10551-016-3187-6.

Llach, J., Castro, R. D., Bikfalvi, A., & Marimon, F. (2012). The relationship between environmental management systems and organizational innovations. Human Factors and Ergonomics in Manufacturing & Service Industries, 22(4), 307–316.

Manso, G. (2011). Motivating innovation. Journal of Finance, 66(5), 1823–1860.

Park, J. Y. (2014). The evolution of waste into a resource: Examining innovation in technologies reusing coal combustion by-products using patent data. Research Policy, 43(10), 1816–1826.

Penrose, E. T. (1959). The theory of the growth of the firm. New York: Wiley.

Porter, M. E., & van der Linde, C. (1995). Toward a new conception of the environment-competitiveness relationship. Journal of Economic Perspectives, 9(4), 97–118.

Potoski, M., & Prakash, A. (2004). Regulatory convergence in nongovernmental regimes? Cross-national adoption of ISO 14001 certifications. Journal of Politics, 66(3), 885–905.

Preacher, K. J., & Hayes, A. F. (2008). Asymptotic and resampling strategies for assessing and comparing indirect effects in multiple mediator models. Behavior Research Methods, 40(3), 879–891.

Preacher, K. J., & Kelley, K. (2011). Effect size measures for mediation models: Quantitative strategies for communicating indirect effects. Psychological Methods, 16(2), 93–115.

Priem, R. L., & Butler, J. E. (2001). Is the resource-based view a useful perspective for strategic management research? Academy of Management Review, 26, 22–40.

Reilly, G., Souder, D., & Ranucci, R. (2016). Time horizon of investments in the resource allocation process: Review and framework for next steps. Journal of Management, 42(5), 1169–1194.

Ramanathan, R., Black, A., Nath, P., & Muyldermans, L. (2010). Impact of environmental regulations on innovation and performance in the UK industrial sector. Management Decision, 48(10), 1493–1513.

Rennings, Klaus, Ziegler, Andreas, Ankele, K., et al. (2006). The influence of different characteristics of the EU environmental management and auditing scheme on technical environmental innovations and economic performance. Ecological Economics, 57(1), 45–59.

Russo, M. V. (2009). Explaining the impact of ISO 14001 on emission performance: A dynamic capabilities perspective on process and learning. Business Strategy and the Environment, 18(5), 307–319.

Shaver, J. M. (2005). Testing for mediating variables in management research: Concerns, implications, and alternative strategies. Journal of Management, 31(3), 330–353.

Shrout, P. E., & Bolger, N. (2002). Mediation in experimental and nonexperimental studies: New procedures and recommendations. Psychological Methods, 7, 422–445.

Shu, C., Zhou, K. Z., Xiao, Y., & Gao, S. (2016). How green management influences product innovation in china: The role of institutional benefits. Journal of Business Ethics, 133(3), 471–485.

Sirmon, D. G., & Hitt, M. A. (2003). Managing resources: Linking unique resources, management and wealth creation in family firms. Entrepreneurship Theory and Practice, 27(4), 339–358.

Sirmon, D. G., Hitt, M. A., & Ireland, R. D. (2007). Managing firm resources in dynamic environments to create value: Looking inside the black box. Academy of Management Review, 32(1), 273–292.

Sobel, M. E. (1982). Asymptotic confidence intervals for indirect effects in structural equation models. Sociological Methodology, 13, 290–312.

Solow, R. M. (1957). Technical change and the aggregate production function. The Review of Economics and Statistics, 39(3), 312–320.

Staiger, D., Stock, J. H., & Watson, M. W. (1997). The NAIRU, unemployment and monetary policy. The Journal of Economic Perspectives, 11(1), 33–49.

The Guardian. (2016). Smog refugees flee Chinese cities as ‘airpocalypse’ blights half a billion. December 21, 2016.

Trajtenberg, M. (1990). A penny for your quotes: Patent citations and the value of innovations. The Rand Journal of Economics, 21(1), 172–187.

Wagner, M. (2007). On the relationship between environmental management, environmental innovation and patenting: Evidence from German manufacturing firms. Research Policy, 36(10), 1587–1602.

Wagner, M. (2008). Empirical influence of environmental management on innovation: Evidence from Europe. Ecological Economics, 66(2), 392–402.

Wernerfelt, B. (1984). A resource-based view of the firm. Strategic Management Journal, 5(2), 171–180.

Zhao, X., Lynch, J. G., Jr., & Chen, Q. (2010). Reconsidering Baron and Kenny: Myths and truths about mediation analysis. Journal of Consumer Research, 37(2), 197–206.

Acknowledgements

We are grateful to Tony Tong (University of Colorado at Boulder), Jiangyong Lu (Peking University), and seminar participants at 2017 AOM and Peking University for helpful comments. This research was supported by the National Natural Science Foundation of China (Nos. 71702031, 71772038) and by the Foundation of Humanities and Social Sciences of the Ministry of Education in China (No. 17YJC630038).

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

Wenlong He has received research grants from the National Natural Science Foundation of China (Nos. 71702031, 71772038). Wenlong He and Rui Shen declare that they have no conflict of interest.

Rights and permissions

About this article

Cite this article

He, W., Shen, R. ISO 14001 Certification and Corporate Technological Innovation: Evidence from Chinese Firms. J Bus Ethics 158, 97–117 (2019). https://doi.org/10.1007/s10551-017-3712-2

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10551-017-3712-2