Abstract

Environmental management certification is a common means for companies to conduct environmental management activities. By constructing a comprehensive certification-innovation-performance research framework, this paper analyzes whether environmental management certification can generate innovation incentives and then promote the improvement of corporate economic performance and social responsibility performance. Taking seven-year panel data of companies listed on GEM as a sample, a dynamic effect test including lag periods is carried out. The results show that voluntary environmental management helps to improve economic performance and social responsibility performance, but the influence paths are different. Voluntary environmental management affects economic performance through the mediator variable of green innovation and has a more obvious impact on long-term performance. However, for the performance of social responsibility, the direct effect of voluntary environmental management is significant, and green innovation does not play a mediating role. Regarding voluntary policy, this paper provides new support for the applicability of the Porter hypothesis. The conclusion of this paper has some implications for understanding the impact of voluntary environmental management on enterprise performance and can provide some theoretical support for promoting voluntary environmental management.

Similar content being viewed by others

Explore related subjects

Discover the latest articles, news and stories from top researchers in related subjects.Avoid common mistakes on your manuscript.

1 Introduction

With worldwide attention given to sustainable development, environmental management certification has become a popular tool for enterprise environmental management. In 1996, the International Organization for Standardization issued the first version of the ISO 14001 environmental management system certification, which was revised in 2004 and 2015. According to the ISO survey report, by the end of 2019, a total of 312,580 enterprises had been certified worldwide, and the number of certified enterprises in China reached 134,926 in 2019. China is the country that has the most enterprises with an ISO 14001 environmental management system certification in the world. The purpose of ISO 14001 environmental management system certification is not only to prove that an organization has built an internal environmental management system and reached the international level in environmental management but also to cultivate awareness of the environmental protection activities of enterprises. Through the implementation of the Plan-Do-Check-Act (PDCA) cycle, enterprises’ environmental management systems can be continuously improved, and win-win results of economic and environmental benefits can be achieved.

However, academic research has been quite divided on whether environmental management certification can achieve the expected effects in practical applications (Russo, 2009; Bromiley & Rau, 2016; Hernandez-Vivanco et al., 2019; Treacy, 2019). There are theoretically different opinions on whether voluntary environmental management can improve the economic performance of enterprises. According to the traditional point of view, enterprises must pay a price to carry out environmental management. Environmental investment is an additional cost for enterprises, and an increase in costs means a decline in economic benefits, which weakens the profitability of enterprises, especially the short-term profitability (Brammer et al., 2006; Jaggi & Freedman, 1992; Walley & Whitehead, 1994). The revised theory holds the opposite view. The environmental management of enterprises can help to improve the efficiency of the enterprises, enhance the competitiveness of the enterprises, and stimulate the innovation ability of the enterprises; at the same time, it can also help to establish a good brand image for the enterprises and enhance their reputation in the eyes of consumers (Al-Tuwaijri et al., 2004; Esty & Porter, 1998; Perrini et al., 2011; Porter & Linde, 1995). As a typical representative of the revised theory, Porter's theory proposes that government environmental regulation can help enterprises strengthen their environmental management and enhance their competitiveness through innovative paths, thereby enhancing their economic and environmental benefits. Orsato’s (2009) research shows that the environmental performance improvement brought about by enterprise voluntary environmental management does not have a direct impact on economic performance. Compared with studying whether voluntary environmental management can bring about economic performance improvement, studying when it can bring about economic performance improvement is more important. In addition, in the research on the relationship between environmental management and environmental performance, some variables, such as cultural differences, play a significant moderating role (Vincenzo et al., 2017).

At present, “innovation, coordination, green, open, and sharing” has become the five development concepts recognized by the public in China. The State Council issued the “Opinions of the State Council on Strengthening the Construction of a Quality Certification System and Promoting Comprehensive Quality Management” on January 26, 2018, in which Article 10 mentions the need to create a voluntary certification system. Against the background of this system, it is of practical significance to study the existing environmental management certification system in China and to clarify whether voluntary environmental management can achieve the double dividends effect of innovation incentives and performance improvement. Our research is carried out in accordance with Porter's theory and resource-based theory. According to the basic logic of certification-innovation-performance, we analyze whether environmental management certification can generate innovation incentives for enterprises and influence corporate social responsibility performance and economic performance through the mediating effect of those innovation incentives. Since it is difficult to reflect the long-term impact mechanism and effect in most of the survey data, we collect the data of GEM-listed companies through the CSMAR database and conduct a dynamic impact effect test.

The results show that enterprise voluntary environmental management helps to improve the enterprise’s economic performance and social responsibility performance. Different from voluntary environmental management, which can have a direct impact on social responsibility performance, voluntary environmental management affects the economic performance of enterprises through the mediator variable of green innovation, and the impact on long-term performance is more obvious. This paper makes certain contributions in the following respects. First, a comprehensive framework involving environmental management certification, green innovation, social responsibility performance, and economic performance is constructed as a supplement to Porter's theory. Porter's theory has been widely considered by academia since it was put forward, but the relevant studies mainly focus on the effect of the government's command-and-control policy and economic policy (Brouhle et al., 2013; Chen et al., 2018; Hamamoto, 2006; Lanoie et al., 2008; Testa et al., 2011). In terms of policy classification, voluntary environmental policy is an important part of environmental regulatory policy. Enterprise voluntary environmental management can be understood as the response of enterprises to voluntary environmental policy. The construction of the comprehensive framework in this paper can be understood as explaining Porter's theory from the perspective of voluntary environmental policies. Second, most of the research data of existing studies come from survey data (Boiral & Henri, 2012; Borsatto & Amui, 2019). Considering the limitations of research time and region, research conclusions are often applicable to a specific region or industry. Moreover, survey data are mostly cross-sectional data, which makes it difficult to conduct dynamic analyses. We collected 7 years of data in the database to provide support for dynamic analyses and long-term effect testing. Last, although China is currently the country that has the highest number of enterprises that have obtained the environmental management certification, there are few theoretical studies on the effects of environmental management certification in China compared with the popularity of environmental management certification in practical application. Existing research conclusions are quite different. Providing Chinese evidence on this controversial topic is expected to play a certain enlightening role. The rest of the paper is arranged as follows: the second part reviews the literature and proposes research hypotheses, the third part explains the study design, the fourth part analyzes the empirical results, and the fifth part concludes and discusses the research.

2 Literature review and research hypotheses

Due to the existence of externalities, the government's environmental regulation policy has played a leading role in the environmental governance of enterprises for a long time (Jin et al., 2019). At present, there is no unified definition of voluntary environmental management in academia. Most of the existing studies equate it with external environmental management certification (such as ISO 14001 and EMAS) or voluntary agreements (such as the 33/50 project in the United States, the ClimateWise plan in the UK, the long-term energy efficiency agreement (LTA) in the Netherlands, and the industrial energy conservation activity CIPEC in Canada). As an internationally recognized environmental management certification system, the effect of ISO 14001 on environmental performance has been confirmed in some documents (Botta & Comoglio, 2007; Ferrón-Vílchez, 2016; Graafland, 2018). However, there is still considerable controversy about its impact on economic performance (He & Shen, 2019; Heras-Saizarbitoria et al., 2013). The effect of environmental management certification on environmental performance and economic performance is still under exploration. Innovation is the essential requirement of economic development. Therefore, according to the logic of Porter's theory, environmental management certification can stimulate corporate green innovation and then affect corporate social responsibility performance and economic performance, which is the basic idea of this paper. The existing research related to this paper mainly involves the following aspects:

2.1 Enterprise voluntary environmental management

As a tool of enterprise voluntary environmental management, environmental management certification is embedded in the environmental management work of enterprises and becomes an important part of the enterprise environmental management system. At present, the research on environmental management certification mainly focuses on the motivation analysis of enterprises carrying out environmental management certification and the effect test of environmental management certification. Regarding the motivation for environmental management certification, Massoud et al. (2010) propose that the actions of enterprises pursuing voluntary environmental management certification demonstrates their preventive motivation for environmental governance and their confidence in promoting sustainable development. However, more studies have shown that although environmental management certification is a voluntary environmental management behavior adopted by companies, the main reason why companies obtain environmental management certification is external stakeholder pressure, including regulatory pressure from the government and nonregulatory pressure from consumers, communities and environmental protection organizations (Massoud et al., 2010; Nishitani, 2010;Liao Z. et al., 2018).

The most direct benefit of ISO 14001 certification is that it contributes to the reduction of pollutant emissions and the improvement of environmental performance (Nishitani et al., 2012). At the same time, because ISO certification implements the principle of continuous improvement, it may reduce risk, bring unique competitive advantages to enterprises and enhance economic benefits (Ferron-Vilchez & Darnall, 2014; Anne et al., 2015; Hojnik & Ruzzier, 2017). In addition, in the international market, the ISO environmental management system certification can be regarded as a signal that the enterprise sends to the outside world, which helps the enterprise establish a good image(Christmann & Taylor, 2006; Montiel et al., 2012). However, in recent years, there have been constant doubts about ISO certification. The lack of third-party verification, the uncertainty about the improvement in environmental performance, and the mere formality have all become criticisms of ISO certification (Boiral & Gendron, 2011; Lannelongue et al., 2014). If an enterprise obtains the certification only for appearances and only meets the minimum requirements of the certification without actually implementing the certification requirements into the enterprise's daily production and operation, the certification cannot provide substantial help to improve the enterprise's environmental performance. The research of Yin and Schmeidler, (2009) finds that some enterprises only complete some procedural work to obtain ISO certification, and the ISO certification does not play a substantial role in improving their environmental performance. Considering that environmental performance is an important part of social responsibility performance and that social responsibility performance is a comprehensive evaluation of corporate social responsibility, we focus on measuring corporate performance from two aspects in this paper: economic performance and social responsibility performance. Based on the above analysis, we propose the first research hypothesis:

Hypothesis 1a

Environmental management certification can improve business economic performance.

Hypothesis 1b

Environmental management certification can improve corporate social responsibility performance.

2.2 Green innovation

For green innovation, similar concepts include ecological innovation, green technology innovation, environmental innovation, sustainable innovation, etc. Their common ground is that they emphasize the environmental benefits of innovation. Considering the similarity of their contents, this research does not make strict distinctions between these concepts but uses the concept of green innovation uniformly. Chen (2008) believes that green innovation is product and process innovation using energy-saving, pollution prevention, waste-recycling and environmental management technologies. These innovations can effectively promote green growth and meet environmental protection requirements. Apak and Atay (2015) believe that green innovation is a necessary step for enterprises to enhance their international competitiveness in the global market. From the perspective of input and output, the classification of green innovation can be divided into green innovation input (such as green innovation R&D expenditure) and green innovation output (such as the number of green patents). From the perspective of the nature of innovation, it can be divided into green process innovation and green product innovation (Li et al., 2017; Wagner & Llerena, 2011). Abu et al. (2019) adds consideration of green market innovation in his research. Demirel and Kesidou (2011) distinguish three types of ecological innovation: terminal treatment technology, integrated clean production technology and environmental R&D investment. Their research finds that environmental R&D investment can bring about the greatest degree of environmental and technological impact, and the driving factors for these three kinds of innovations are quite different.

Green innovation has dual externalities, namely environmental externalities and innovation externalities (Rennings, 2004). This also leads to the fact that green innovation has the attributes of public goods more than ordinary innovation, and it is more likely to lead to free-riding behavior in the market, which makes it difficult for enterprises to have sufficient internal motivations for green innovation. Different from ordinary innovation, which comes from the mission of corporate practice, green innovation faces greater uncertainty. Pure technology promotion and market pull are not enough to form a complete corporate green innovation power mechanism. Green innovation is regarded as a passive choice made by enterprises under pressure from stakeholders and systems (Hojnik & Ruzzier, 2016). In addition to policy pressures, market demand, the desire of companies for expected returns, corporate management concepts, and technological development are also important sources of motivation for companies to carry out green innovation (Horbach, 2016; Wang & Yang, 2021).

The research of Costa-Campi et al. (2017) shows that subsidies have the strongest innovation incentive effect among the environmental fiscal and taxation policies of pollution taxes, energy taxes, and subsidies. They also recommend a combination of policy tools. Liao et al. (2018) collect the annual reports of 120 listed companies in China's A-share energy industry. Using the content analysis method and grounded theory, they find that environmental regulation policies and fiscal and taxation policies are the main driving factors of enterprise environmental innovation. Market competition and consumer demand are also important factors affecting corporate environmental innovation, while self-interested motives (such as cost savings, resource acquisition, and risk aversion) and green value concepts are important adjustment factors. Li et al. (2013) find that when considering the two control variables of industry scale and innovative human resource investment, strict environmental regulation policies can effectively promote the implementation of green technology innovation in pollution-intensive industries. However, without considering these two control variables, strict environmental regulation policies have a negative effect. This phenomenon confirms the condition for the establishment of the Porter hypothesis. The research of Cai and Li (2018) also shows that the most significant factor affecting corporate ecological innovation is competitive pressure, followed by market policy tools, technological capabilities, consumer green demand and organizational environmental capabilities. Market-based policy tools are effective for ecological innovation, while control-command policy tools are ineffective. Kesidou and Demirel (2012) provide empirical insights on the drivers of eco-innovations. Their research shows that the stringency of environmental regulations affects eco-innovations of the less innovative firms differently from those of the more innovative firms. For the analysis of the influencing factors of green innovation, most of the existing studies focus on factors such as environmental regulation policies, market competition, and consumer demand. Several studies have shown that green innovation can have a significant impact on a firm's environmental performance and competitive advantage (Cai & Li, 2018; Küçükoğlu & Pınar, 2015). Green innovation may bring about the improvement of environmental performance, and environmental performance is an important part of social responsibility performance. However, the impact of voluntary environmental management on green innovation within enterprises is relatively rare. We refer to the view of Porter's theory that appropriate environmental regulations can stimulate enterprise innovation by considering enterprise voluntary environmental management as the enterprise implementation of voluntary environmental policies, and we propose hypothesis 2 accordingly.

Hypothesis 2

Environmental management certification can promote the green innovation of enterprises.

2.3 Comprehensive research on environmental management certification, green innovation, and corporate performance

At present, the number of enterprises that have passed environmental management certifications in China has ranked first in the world. However, research on environmental management certification in China is still very limited and in the stage of research and exploration. It is relatively rare that comprehensive research can connect the relationship among voluntary environmental management, green innovation and enterprise performance at the same time. Particularly for the relationship between internal factors, there is still no clear research path or research conclusion. Some studies have discussed the relationship between them. The research by Li et al. (2017) shows that institutional pressure will significantly affect green product innovation and green process innovation. Corporate profitability has a significant impact on green product innovation but has no significant impact on green process innovation. In addition, in the effect of institutional pressure on green innovation, corporate profitability plays a significant regulatory role. The environmental protection effect of green innovation has been confirmed in some empirical studies. However, the influence of green innovation on the economic performance of enterprises is controversial in existing research. Some studies show that green innovation can enhance a company’s competitive advantage (Chan et al., 2012).

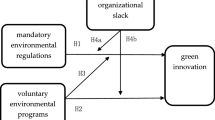

Drawing on the theoretical lenses of Porter’s theory and resource-based theory, this article puts forward the idea of “inner double dividends” and develops a conceptual framework illustrates the relationships of voluntary environmental management, green innovation and corporate performance (Fig. 1). Firstly, the environmental management certification process for an enterprise can be understood as voluntary environmental management behavior induced by voluntary environmental policy. In the research related to Porter’s theory, environmental regulation is mostly defined as external environmental protection laws and regulations. As for the specific types of environmental regulatory policies, the OECD divides environmental regulatory policies into three categories: command-and-control, market incentive, and voluntary policies. With the strengthening of enterprise environmental awareness, enterprise voluntary environmental management certification has become a useful supplement to command-and-control policies. Secondly, the Porter hypothesis means that environmental regulations can promote the innovative activities of enterprises, and the resulting competitive advantages may enable enterprises to obtain economic benefits. From a macroeconomic perspective, it is possible to achieve a win-win effect between “environmental protection” and “economic growth.” Similar to the dual effectiveness of environmental tax in improving environment and increasing tax revenues, enterprise voluntary environmental management is also expected to achieve the inner double dividends of promoting environmental innovation and enhancing performance. Finally, according to the resource-based theory, an enterprise is an aggregation of various resources, and the unique heterogeneous resources are the key factors to competitive advantages. Environmental management is a strategic resource, which is valuable, scarce, difficult to imitate and difficult to substitute. Therefore, it can be assumed that environmental management will help enterprises gain competitive advantages. Corporates that take the initiative to carry out voluntary environmental management will take the lead in developing environmentally friendly green products in the face of environmental regulations, and gain competitive advantages in the competition, so as to expand market share and improve corporate benefits. Therefore, when faced with environmental policies, enterprises can take the initiative to carry out voluntary environmental management, reduce pollutant emissions through green innovation, and rationally improve resource utilization efficiency, so as to realize the improvement of economic and environmental performance.

Comprehensive research framework

After Porter’s theory was put forward, a large number of empirical studies on the effects of environmental regulations on the creation of corporate competitive advantage and the improvement in corporate performance emerged. The overwhelming view is that environmental regulations will promote enterprise innovation (Borsatto & Amui, 2019; Demirel & Kesidou, 2011) and effective environmental policies will put pressure on enterprises to reduce emissions, create a shadow price of emissions, and help induce green technological innovation, which is a necessity for government intervention. The research of Borsatto and Amui (2019) shows that the effect of environmental regulation on green innovation may be positive or negative, and the relationship between them will be adjusted by factors such as the size of the enterprise, the degree of internationalization and other factors. Green innovation is regarded as one of the key factors that simultaneously improve a company's environmental, social and financial performance (Tang et al., 2021). Kraus et al. (2020) find that corporate social responsibility has no direct significant influence on environmental performance, but is positively correlated to environmental strategy and green innovation, which again improve environmental performance. With the awakening of enterprise environmental awareness, enterprise voluntary environmental management has become an important supplement to command-and-control environmental policies. The environmental management certification of enterprises can be understood as a voluntary environmental management behavior made by the enterprise under the guidance of a voluntary environmental policy. Facing continuous environmental problems and increasingly stringent policy pressures, the ability of enterprise voluntary environmental management to achieve the transition from green to gold is the key to maintaining an advantage in fierce competition. Based on the above analysis and the comprehensive research framework, we propose hypothesis 3.

Hypothesis 3

Green innovation plays an intermediary role in the relationship between voluntary environmental management and corporate performance.

3 Research design

3.1 Sample selection and data sources

This paper selects GEM-listed companies from 2012 to 2018 as the research sample. China's Growth Enterprises Market (GEM) was launched in October 2009. The establishment of the GEM aims to provide financing opportunities for small and medium-sized high-quality enterprises with strong innovation ability. Most of the research related to Chinese corporate innovation also revolves around GEM. In 2012, China Securities Regulatory Commission (CSRC) launched a new industry classification code. Since 2019, China has vigorously promoted the reform of the registration system, which has resulted in significant changes in the listing requirements for enterprises. Considering the consistency of policies, we set the time range of selected data as 2012–2018, and the seven-year time span also ensures that we can obtain a sufficient sample size for analysis. The reason for choosing GEM-listed companies is that the companies listed on GEM are basically independent innovation enterprises and other growth-oriented enterprises. These companies have high levels of investment in and requirements for innovation, and they can represent the leading innovative enterprises in China to a certain extent. The environmental management certification data of each company come from the information disclosed in the company's annual report and social responsibility report published by www.cninfo.com and are manually sorted. Based on the “Green List of International Patent Classification” proposed by the World Intellectual Property Organization (WIPO) in 2010, we identify green innovation data and count the number of green patents obtained by enterprises each year. This paper uses the number of green patents granted as the core indicator to measure the green innovation of enterprises. The financial data come from the CSMAR database, and the social responsibility data are the corporate social responsibility scores of Hexun from 2012 to 2018. Excluding samples with missing data, the numbers of GEM-listed companies collected from 2012 to 2018 were 342, 365, 405, 481, 584, 693 and 724. To control the influence of outliers, winsorize processing was performed on the continuous variables at 1 and 99%.

3.2 Variables and models

Combined with the comprehensive research framework proposed before, this paper selects enterprise performance as the explained variable, which is further divided into economic performance and social responsibility performance. The explanatory variable is enterprise voluntary environmental management, and the mediator variable is green innovation. In addition, referring to the existing relevant research (He & Shen, 2019; Inoue et al., 2013; Liang & Liu, 2017), this paper chooses enterprise size, number of employees, leverage ratio, company age, ownership nature and polluting industry as control variables. The names, symbols and specific definitions of the variables are shown in Table 1.

In accordance with the “Guidelines for Industry Classification of Listed Companies” revised by the China Securities Regulatory Commission in 2012 combined with the “Industry Classification Management Entry for Environmental Inspection of Listed Companies” (Huanbanhan, 2008, No. 373) published by the General Office of the Ministry of Environmental Protection in 2008 and the “Guidelines for Environmental Information Disclosure of Listed Companies” published in 2010, this paper classifies heavy pollution industries into eight categories: extractive industry; metal and nonmetal industry; petrochemical plastic industry; biopharmaceutical industry; water, electricity and gas industry; paper making and printing industry; textile, clothing and fur industry; and food and beverage industry.

Combined with the overall conceptual framework of the second part, an empirical measurement model is proposed. This article proposes that whether the mediating effect is established does not depend on whether the main effect is significant. Considering that the fixed-effects model is usually only applicable to the selected cross-sectional units, it is not suitable for units outside the sample. The data used in this paper are only data for some listed companies in some years. When analyzing the population with the sample results, it is more reasonable to regard the individual effect items reflecting individual differences as a random distribution across individual members. Using the random effects panel data model, we do not consider the individual time effect but only the individual cross-sectional effect to construct the following three test models.

The test of the mediating effect includes two parts: the direct effect test and the indirect effect test. For example, whether environmental management certification has a mediating effect on economic performance is used to test model formula (1) and (2). Figure 2 illustrates the test and analysis path of the mediating effect. When testing the significance of α1 × β2, this paper assumes that α1 × β2 obeys a normal distribution and manually calculates the z statistic and calculates the p value. The testing process for the mediating effect of the social responsibility performance of environmental management certification is the same, using model formula (1) and (3).

Test path of mediating effect

4 Analysis of empirical results

4.1 Descriptive statistics and related analysis

Table 2 shows the annual quantity statistics of the core variables in the sample data. Approximately 23.41% of the companies in China listed on GEM belong to polluting industries. Although the state has implemented mandatory environmental information disclosure requirements for companies in polluting industries, the number of companies listed on GEM that have obtained ISO 14001 environmental management system certification is still very limited, with only approximately 3.83% of companies doing voluntary environmental management and passing ISO 14001 certification. At the same time, although GEM-listed companies represent the leading level of innovation capability in China, the number of enterprises that obtain green innovation patents every year is not large. In terms of proportion, the average proportion from 2012 to 2018 was approximately 26.03% with a certain upward trend. Table 3 shows the descriptive statistics and correlation analysis of each variable.

4.2 The mediating effect test of economic performance

4.2.1 Current mediating effect test

According to models (1) and (2), the random effects panel data model is used to estimate the variable coefficients. When estimating in Eq. (1), considering that the number of green patents is count data, panel Poisson regression or panel negative binomial regression is used to estimate the coefficient. The test of whether there is “overdispersion” in the data found that the sample variance of the mediator variable GI is more than 17 times its average value. The variance is significantly larger than the mean value, indicating that the data are overdispersed. Negative binomial regression is used to estimate the data. The estimation results are shown in Table 4.

The results in Table 4 show that the mediating effect is significant but the direct effect is not significant, which indicates that the voluntary environmental management of enterprises can positively affect the economic performance of enterprises through the intermediary of green innovation, but voluntary environmental management cannot directly affect the economic performance of enterprises.

4.2.2 Mediating effect test with lag period

Considering that there may be a lag effect in the process of environmental management certification promoting green innovation and the process of green innovation transforming into economic benefits, the mediating effect test with lag period is considered. For the mediator variable green innovation and the dependent variable enterprise performance, three periods of lagging are considered for dynamic testing (Fig. 3).

Frame diagram of the mediating effect considering the lag period

The dynamic testing results are shown in Table 5. For the convenience of displaying only the value of the coefficient estimator and the z-statistic are given, the p value is no longer listed.

The results in Table 5 show that there are three paths with significant mediating effects: ISOt → GIt → ROEt+1, ISOt → GIt → ROEt+2, and ISOt → GIt → ROEt+3. The common feature of these three paths is that the variables of green innovation are all current values, indicating that green innovation has a lag effect on the increase in economic benefits. Current environmental management certification can affect the future economic performance of enterprises through the intermediary role of current green innovation, and the impact on economic performance will be strengthened with the passage of time. In addition, from the estimation of α1, it can be seen that current environmental management does not have a lag effect on green innovation. Therefore, the path in which current environmental management affects later green innovation and brings about economic effects is not tenable. The coefficients of the direct effects are not significant, and the voluntary environmental management certification does not have a direct impact on the economic benefits of enterprises.

It can be seen that the direct effect of environmental management certification on financial performance is not obvious, but green innovation can be used as a mediator variable to improve the long-term financial performance of enterprises. For enterprises that have passed the environmental management certification, the standardization and deepening of environmental management will prompt enterprises to attach importance to green innovation, and the competitive advantages brought by green innovation will further improve financial performance in the later stage.

4.3 The mediating effect test of social responsibility performance

4.3.1 Current mediating effect test

Combining formula (1) and formula (3) can complete the mediating effect test on social responsibility performance. The test results are shown in Table 6.

The results in Table 6 show that environmental management certification has a significant direct impact on social responsibility performance, but the mediating effect of green innovation is not significant.

4.3.2 Mediating effect test with lag period

Similar to economic performance, the mediating effect of environmental management certification on social responsibility performance may also lag. Therefore, the mediating effects of lagging phases 1, 2, and 3 were further tested, and the results are shown in Table 7. Table 7 shows that the mediating effect of green innovation is not significant in other cases except for ISOt → GIt → CSRt+1, which is one stage behind when considering the lag factor. This result is basically consistent with the results of the current value analysis. Considering the lag factors, the direct effect of environmental management certification on social responsibility performance is still significant, which means that whether to carry out environmental management certification will directly affect social responsibility performance, and there is no need to rely on the intermediary bridge of green innovation.

Environmental management certification has a direct impact on social responsibility performance without resorting to the mediator variable of green innovation. Environmental management certification is an environmental management activity of an enterprise, and its direct effect is reflected in the improvement of environmental performance in the form of reduction of pollutant discharge, reduction of energy consumption, and improvement of environmental ranking. Environmental performance is an important part of social responsibility performance, which means that the implementation of environmental management certification will promote the improvement of social responsibility performance.

4.4 Robustness test

4.4.1 Propensity score matching estimation

In order to solve the endogenous problem, propensity score matching (PSM) is used to estimate whether the implementation of voluntary environmental management has a significant impact on enterprise green innovation, economic performance and social responsibility performance. Taking whether the environmental management certification ISO is obtained as the treatment variable, taking the three variables of corporate green patent acquisition GI, return on equities ROE and Hexun social responsibility score CSR and their lag values as the explained variables, the propensity score is estimated by logit regression. The samples are matched to estimate the treatment effect ATT (as shown in Table 8). The results show that the treatment effect of the variable ISO on GI is only significant in the current period model, and there is no significant treatment effect on economic performance, while the treatment effect on CSR is significant, both in the current period model and lag period model. The PSM results are consistent with the estimation results of the previous panel data models.

4.4.2 Replace the explained variables

To further test the robustness of the model, the explained variables are replaced with ROA, which represents economic performance, and EGS, which represents corporate social responsibility performance, respectively. The estimation results of the current period and the lag periods are shown in Table 9. The results show that the direct effect of the variable ISO on corporate economic performance is not significant, and the indirect effects are significant in four paths. All of paths are indirectly through the effect of ISO on the current period GI, which in turn affects the current and lagged ROA and brings about the improvement of corporate economic performance. This estimation results are basically consistent with the previous estimation results. The results also indicate that the indirect effect of the variable ISO on ESG is not significant, while the direct effect is highly significant. The results are also consistent with the previous estimation results.

4.4.3 Replace the mediator variable

We further replace the original mediator variable green patent authorization GI with enterprise R&D investment, and test the robustness of the mediating effect. The results are shown in Table 10. The results show that the direct effect of ISO on ROE is significant at the 10% significance level in the lagged three-period model, and the direct effect of ISO on ROE is not significant in other cases; the indirect effects are significant in seven paths, of which four paths take the effect of ISO on GI in the current period as an intermediate path, and the other three paths take the ISO's effect on GIt+1 as an intermediate path. The results also show that after replacing the mediator variable as R&D, the direct effect of ISO on CSR performance is still significant, while only two paths of indirect effects are significant at the 5% significance level. Although the robustness test results are slightly different from the above estimation results, the conclusions of the above estimation results are basically supported.

5 Research conclusions and discussion

Against the background of vigorous advocation of scientific and technological innovation and green development in China, the environmental regulation of enterprises has become a hot topic in academia. The government’s implementation of environmental regulations is essentially a process of internalizing the external costs of the environment. From the perspective of enterprises, they will face an increase in explicit costs such as increased pollution treatment equipment. However, if an enterprise can change from passive to active and actively carry out environmental management, it is possible for the enterprise to enjoy the benefits of increased efficiency and innovation brought about by environmental management. During the accelerated formation of the ecological civilization system in China, enterprises' active environmental management is needed to avoid environmental penalties and also may bring new competitive advantages to enterprises. This paper takes companies listed on GEM as the research object, uses the mediating effect model to study the effect of environmental management certification, and answers the question of whether enterprises have an inherent motivation to engage in environmental management and whether an enterprise’s voluntary environmental management can promote the company's green innovation and performance improvement. The conclusions are as follows:

First, enterprises’ voluntary environmental management can promote the green innovation of the enterprises. As the leader of innovative enterprises in China, companies listed on GEM have large R&D investments and strong innovation capabilities. We use the number of green patents and amount of R&D investment as proxy variables for green innovation. The regression results show that one of the benefits of enterprise environmental management certification is to promote the enterprises’ green innovation.

Second, the voluntary environmental management of enterprises can promote the improvement of the economic performance of the enterprises, but this role needs to rely on the mediating effect of green innovation. Corporate environmental management certification indirectly affects the economic performance of the companies through green innovation and shows a relatively obvious long-term effect; that is, the degree of impact strengthens over time. This is mainly because green innovation can bring competitive advantages to enterprises, but this advantage serves the long-term sustainable development of enterprises. This also shows that environmental management certification is more conducive to the improvement of the long-term economic performance of enterprises.

Third, enterprises’ voluntary environmental management can promote the improvement of corporate social responsibility performance. Different from the impact of voluntary environmental management on economic performance, the effect of corporate voluntary environmental management on social responsibility performance is directly generated and does not need to rely on the intermediary bridge of green innovation.

The Porter hypothesis provides a useful blueprint for environmental regulation and enterprise voluntary environmental management. The results of this paper provide new empirical evidence for the Porter hypothesis. Our findings shed light on how and to what extent voluntary environmental management influences corporate performance. Although there have been a large number of research results on environmental management certification, most of the existing literature focuses on the effects of ISO certification implementation on pollutant emission reduction or economic performance improvement, and they are rarely discussed in the same framework. There is little analysis on the specific path of voluntary environmental management on enterprise performance. Therefore, this paper makes a new attempt in the construction of an integrated model, the examination of the mechanism and the analysis of dynamic effects. The research results also reveal that enterprises have a spontaneous motivation for voluntary environmental management and provide strong support for subsequent policies to promote enterprise voluntary environmental management. The findings of this paper have certain practical implications. Since environmental management certification has a positive effect on the improvement of corporate financial performance and social responsibility performance, the government can further promote the standardization and deepening of certification. Environmental certification is difficult to improve the financial performance of enterprises through green innovation in the short term, but the long-term effect is significant. Therefore, in the early stage of innovation, it is necessary for the government to provide certain support to enterprises, such as reducing the financial burden of enterprises in the form of tax exemptions and government subsidies, so as to promote the long-term sustainable development of enterprises. From the enterprise’s perspective, enterprises should further strengthen the awareness of environmental management and pay attention to green innovation investment. Entrepreneurs should have the entrepreneurial spirit of innovation-driven and shoulder the necessary social responsibility. For some mature green innovation achievements, they can be exported as soon as possible to obtain cash inflows in the form of technology transfer fees. However, among the sample enterprises, those that have passed environmental management certification do not account for the majority, and there is still a long way to go to improve the level of voluntary environmental management of enterprises.

There are some issues in this research that are worthy of further discussion. First of all, environmental management certification is only a form of voluntary environmental management. The environmental management system may be a formal system that conforms to the ISO 14001 standard or an informal system. In view of the differences in the internal and external environments faced by enterprises, it is difficult to have a standardized environmental management system that is “one size fits all.” When choosing an environmental management system, an enterprise will definitely and must consider its own characteristics. This article only takes ISO 14001 environmental management certification as an example to evaluate the effect of enterprises’ voluntary environmental management. Follow-up research can also be carried out in the context of various types of voluntary environmental management. Secondly, it is also meaningful for further research to divide green innovation into different types and stages, and to discuss its mediating effect between voluntary environmental management and corporate performance. Finally, this study only selects GEM-listed companies as the sample, the research sample is subject to certain restrictions, and further verification on a larger scale can be considered. A wider range of research is also expected to provide policy basis for encouraging enterprises' voluntary environmental management behavior.

Data Availability

The datasets used in the study are available from the corresponding author on reasonable request.

References

Abu Seman, N. A., Govindan, K., Mardani, A., Zakuan, N., Mat Saman, M. Z., Hooker, R. E., & Ozkul, S. (2019). The mediating effect of green innovation on the relationship between green supply chain management and environmental performance. Journal of Cleaner Production, 229(8), 115–127.

Al-Tuwaijri, S., Christensen, T., & Hughes, K. (2004). The relations among environmental disclosure, environmental performance, and economic performance: a simultaneous equations approach. Accounting, Organizations and Society, 29(5), 447–471.

Anne, O., Burskyte, V., & Stasiskiene, Z. (2015). The influence of the environmental management system on the environmental impact of seaport companies during an economic crisis: lithuanian case study. Environmental Science and Pollution Research, 22(2), 1072–1084.

Apak, S., & Atay, E. (2015). Global competitiveness in the eu through green innovation technologies and knowledge production. Procedia-Social and Behavioral Sciences, 181(5), 207–217.

Boiral, O., & Gendron, Y. (2011). Sustainable development and certification practices: lessons learned and prospects. Business Strategy and the Environment, 20(5), 331–347.

Boiral, O., & Henri, J. F. (2012). Modelling the impact of ISO 14001 on environmental performance: a comparative approach. Journal of Environmental Management, 99(5), 84–97.

Borsatto, J. M. L. S., & Amui, L. B. L. (2019). green innovation: unfolding the relation with environmental regulations and competitiveness. Resources, Conservation and Recycling, 149(10), 445–454.

Botta, S., & Comoglio, C. (2007). Environmental management systems in local authorities: the case study of the cesana torinese municipality, a turin 2006 olympic site. American Journal of Environmental Sciences, 3(3), 126–134.

Brammer, S., Brooks, C., & Pavelin, S. (2006). Corporate social performance and stock returns: UK evidence from disaggregate measures. Financial Management, 35(3), 97–116.

Bromiley, P., & Rau, D. (2016). Operations management and the resource-based view: another view. Journal of Operations Management, 41(1), 95–106.

Brouhle, K., Graham, B., & Harrington, D. R. (2013). Innovation under the climate wise program. Resource and Energy Economics, 35(2), 91–112.

Cai, W., & Li, G. (2018). The drivers of eco-innovation and its impact on performance: evidence from China. Journal of Cleaner Production, 176(3), 110–118.

Chan, H. K., Chiou, T. Y., & Lettice, F. (2012). Research framework for analysing the relationship between greening of suppliers and green innovation on firms’ performance. International Journal of Applied Logistics, 3(3), 22–36.

Chen, X., Yi, N., Zhang, L., & Li, D. (2018). Does institutional pressure foster corporate green innovation? evidence from china’s top 100 companies. Journal of Cleaner Production, 188(7), 304–311.

Chen, Y. S. (2008). The driver of green innovation and green image-green core competence. Journal of Business Ethics, 81(3), 531–543.

Christmann, P., & Taylor, G. (2006). Firm self-regulation through international certifiable standards: determinants of symbolic versus substantive implementation. Journal of International Business Studies, 37(6), 863–878.

Costa-Campi, M. T., García-Quevedo, J., & Martínez-Ros, E. (2017). What are the determinants of investment in environmental R&D? Energy Policy, 104(1), 455–465.

Dangelico, R. M., & Devashish, P. (2010). Mainstreaming green product innovation: why and how companies integrate environmental sustainability. Journal of Business Ethics, 95(3), 471–486.

Demirel, P., & Kesidou, E. (2011). Stimulating different types of eco-innovation in the UK: government policies and firm motivations. Ecological Economics, 70(8), 1546–1557.

Esty, D. C., & Porter, M. E. (1998). Industrial ecology and competitiveness: strategic implications for the firm. Journal of Industrial Ecology, 2(1), 35–43.

Ferrón-Vílchez, V. (2016). Does symbolism benefit environmental and business performance in the adoption of ISO 14001? Journal of Environmental Management, 183(3), 882–894.

Ferron-Vilchez, V., & Darnall, N. (2014). Two better than one: the link between management systems and business performance. Business Strategy & the Environment, 25(4), 221–240.

Graafland, J. J. (2018). Ecological impacts of the ISO 14001 certification of small and medium sized enterprises in Europe and the mediating role of networks. Journal of Cleaner Production, 174(2), 273–282.

Hamamoto, M. (2006). Environmental regulation and the productivity of Japanese manufacturing industries. Resource and Energy Economics, 28(4), 299–312.

He, W., & Shen, R. (2019). ISO 14001 certification and corporate technological innovation: evidence from Chinese firms. Journal of Business Ethics, 158(10), 97–117.

Heras-Saizarbitoria, I., Dogui, K., & Boiral, O. (2013). Shedding light on ISO 14001 certification audits. Journal of Cleaner Production, 51(1), 88–98.

Hernandez-Vivanco, A., Domingues, P., Sampaio, P., Bernardo, M., & Cruz-Cázares, C. (2019). Do multiple certifications leverage firm performance? a dynamic approach. International Journal of Production Economics, 218(12), 386–399.

Hojnik, J., & Ruzzier, M. (2016). What drives eco-Innovation? a review of an emerging literature. Environmental Innovation and Societal Transitions, 19(6), 31–41.

Hojnik, J., & Ruzzier, M. (2017). Does it pay to be eco? the mediating role of competitive benefits and the effect of ISO 14001. European Management Journal, 35(5), 581–594.

Horbach, J. (2016). Empirical determinants of eco-innovation in European countries using the community innovation survey. Environmental Innovation and Societal Transitions, 19(4), 1–14.

Inoue, E., Arimura, T. H., & Nakano, M. (2013). A new insight into environmental innovation: does the maturity of environmental management systems matter? Ecological Economics, 94(10), 156–163.

Jaggi, B., & Freedman, M. (1992). An Examination of the impact of pollution performance on economic and market performance: pulp and paper firms. Journal of Business Finance & Accounting, 19(5), 697–713.

Jin, G., Chen, K., Wang, P., Guo, B., Dong, Y., & Yang, J. (2019). Trade-offs in land-use competition and sustainable land development in the North China Plain. Technological Forecasting and Social Change, 141(4), 36–46.

Kesidou, E., & Demirel, P. (2012). On the drivers of eco-innovations: empirical evidence from the UK. Research Policy, 41(5), 862–870.

Kraus, S., Rehman, S. U., & Phillips, F. (2020). Corporate social responsibility and environmental performance: the mediating role of environmental strategy and green innovation. Technological Forecasting and Social Change, 160(11), 120262.

Küçükoğlu, M. T., & Pınar, R. (2015). Positive influences of green innovation on company performance. Social and Behavioral Sciences, 195(7), 1232–1237.

Lannelongue, G., Gonzalez-Benito, O., & Gonzalez-Benito, J. (2014). Environmental motivations: the pathway to complete environmental management. Journal of Business Ethics, 124, 135–147.

Lanoie, P., Patry, M., & Lajeunesse, R. (2008). Environmental regulation and productivity: new findings on the porter hypothesis. Journal of Productivity Analysis, 30(2), 121–128.

Li, D., Zheng, M., Cao, C., Chen, X., Ren, S., & Huang, M. (2017). The impact of legitimacy pressure and corporate profitability on green innovation: evidence from China Top 100. Journal of Cleaner Production, 141(1), 41–49.

Li, W., Bi, K., & Cao, X. (2013). The impact of environmental regulation tools on the green technology innovation of manufacturing enterprises——take paper and paper products companies as examples. System Engineering, 31(10), 112–122.

Liang, D., & Liu, T. (2017). Does environmental management capability of Chinese industrial firms improve the contribution of corporate environmental performance to economic performance? evidence from 2010 to 2015. Journal of Cleaner Production, 142(1), 2985–2998.

Liao, Z., Xu, C., Cheng, H., & Dong, J. (2018). What drives environmental innovation? a content analysis of listed companies in China. Journal of Cleaner Production, 198(10), 1567–1573.

Massoud, M. A., Fayad, R., El-Fadel, M., & Kamleh, R. (2010). Drivers, barriers and incentives to implementing environmental management systems in the food industry: a case of lebanon. Journal of Cleaner Production, 18(3), 200–209.

Melnyk, S. A., Sroufe, R. P., & Calantone, R. (2004). Assessing the impact of environmental management systems on corporate and environmental performance. Journal of Operations Management, 21(3), 329–351.

Montiel, I., Husted, B. W., & Christmann, P. (2012). Using private management standard certification to reduce information asymmetries in corrupt environments. Strategic Management Journal, 33(9), 1103–1113.

Nishitani, K. (2010). Demand for ISO 14001 adoption in the global supply chain: an empirical analysis focusing on environmentally conscious markets. Resource and Energy Economics, 32(3), 395–407.

Nishitani, K., Kaneko, S., Fujii, H., & komatsu, S,. (2012). Are firms’ voluntary environmental management activities beneficial for the environment and business? an empirical study focusing on Japanese manufacturing firms. Journal of Environmental Management, 105(8), 121–130.

Orsato, R. J. (2009). When Does It Pay to be Green? In Sustainability Strategies. London: Palgrave Macmillan.

Perrini, F., Russo, A., Tencati, A., & Vurro, C. (2011). Deconstructing the relationship between corporate social and financial performance. Journal of Business Ethics, 102(3), 59–76.

Porter, M. E., & Linde, C. (1995). Green and competitive. Harvard Business Review., 73(5), 120–134.

Rennings, K. (2004). Redefining innovation-eco-innovation research and the contribution from ecological economics. Ecological Economics, 32(2), 319–332.

Russo, M. V. (2009). Explaining the impact of ISO 14001 on emission performance: a dynamic capabilities perspective on process and learning. Business Strategy and the Environment, 18(5), 307–319.

Tang, M., Mihardjo, L. W., Haseeb, M., et al. (2021). The dynamics effect of green technology innovation on economic growth and CO2 emission in Singapore: new evidence from bootstrap ARDL approach. Environmental Science and Pollution Research, 28, 4184–4194.

Testa, F., Iraldo, F., & Frey, M. (2011). The effect of environmental regulation on firms’ competitive performance. Journal of Environmental Management, 92(9), 2136–2144.

Treacy, R., Humphreys, P., McIvor, R., & Lo, C. (2019). ISO 14001 certification and operating performance: a practice-based view. International Journal of Production Economics, 208(2), 319–328.

Vincenzo, V., Angeloantonio, R., & Clodia, V. (2017). Dealing with cultural differences in environmental management: exploring the CEP-CFP relationship. Ecological Economics, 134(4), 267–275.

Wagner, M., & Llerena, P. (2011). Eco-innovation through integration, regulation and cooperation: comparative insights from case studies in three manufacturing sectors. Industry and Innovation, 18(8), 747–764.

Walley, N., & Whitehead, B. (1994). The challenge is to figure out how fast and how far. Harvard Business Review, 72(4), 48.

Wang, Y., & Yang, Y. (2021). Analyzing the green innovation practices based on sustainability performance indicators: a chinese manufacturing industry case. Environmental Science and Pollution Research, 28, 1181–1203.

Yin, H., & Schmeidler, P. J. (2009). Why do standardized ISO 14001 environmental management systems lead to heterogeneous environmental outcomes? Business Strategy and the Environment, 18(7), 469–486.

Acknowledgements

Wang acknowledges the financial support from Shandong Social Science Planning Project [Grant number: 21CJJJ28]

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interests

The authors declare that they have no competing interests.

Ethics approval

Not applicable.

Consent to participate

Not applicable.

Consent for publication

Not applicable.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

About this article

Cite this article

Chen, X., Wang, N. From green to gold? A test of the innovation incentive and performance improvement effect of enterprise voluntary environmental management. Environ Dev Sustain 25, 8005–8029 (2023). https://doi.org/10.1007/s10668-022-02385-5

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10668-022-02385-5