Abstract

The famous “Faustmann” equation, which allows for identifying the most profitable tree species on a given unstocked piece of land, assumes constant timber prices. In reality, timber prices may fluctuate dramatically. Several authors have proven for monocultures that waiting for an acceptable timber price (reservation price) before harvesting (flexible harvest policy) increases the net present value of forest management. The first part of this paper investigates how efficient a flexible harvest strategy may be applied in mixed forests and whether the optimal species mixture is changed under such harvest policy. Mixtures of the conifer Norway spruce [Picea abies (L.) Karst] and the broadleaf European beech (Fagus sylvatica L.) were investigated. In order to evaluate mixed forests, the risks and the correlation of risks between tree species as well as the attitude towards risk of the decision-maker (risk-aversion is assumed) were considered according to the classical theory of optimal portfolio selection. In the second part we took up a recent critique on modern financial theory by Mandelbrot. Whether or not the assumption of normally distributed financial flows, which are supposed to occur under risk, would be appropriate to evaluate the risk of forest management was investigated. Market and hazard risks as well as their correlation were integrated in the evaluation of mixed forests by means of Monte-Carlo simulations (MCS). The risk of the timber price fluctuation was combined with the natural hazard risk, caused mainly by insects, snow and wind. Applying the μ-σ-rule, the mean net present value (NPV) from 1,000 simulations and their standard deviation were used for the optimisation. Given a low-return, risk-free interest rate to assess potential species mixtures of the Norway spruce and European beech, optimal proportions of European beech increased according to the theory of optimum portfolio selection with growing risk aversion from 0 (ignorance of risk) to 60% (great risk-aversion). In relation to a fixed harvest policy, the net present value of both, Norway spruce and European beech, could be increased significantly. Since the hazard risks of European beech were substantially lower compared with the Norway spruce (relation of susceptibility 1:4) beech benefited more from the flexible harvest policy. A comparison of simulated frequency distributions of the NPV with the expected density functions under the assumption of a normal distribution revealed significant differences. Only in the case of European beech was the general shape of the simulated frequency distribution similar to a normal distribution (bell-shaped curve). However, the density of NPV close to the mean was much greater than expected under the assumption of a normal distribution. Consequently, the frequency of a negative NPV for a European beech forest was greatly overestimated when applying the normal distribution. Though the shape of the simulated frequency distribution was rather different from a normal distribution for Norway spruce the simulated part of negative NPV was quite well approximated by the normal distribution. Therefore the simulated and expected frequencies of negative NPV were similar in case of Norway spruce; only a slight underestimation was seen in the assumption of a normal distribution. It can be concluded that actually simulated frequencies of negative NPV seem to be better measures for risk than computed probabilities of negative NPV, which assume normal distribution. As the risk for European beech was greatly overestimated by the conventional assumption of a normal distribution, the optimal proportions of European beech were surely rather underestimated according to the theory of portfolio. MCS on optimum mixtures derived by the classical portfolio theory seems necessary to test the robustness of such mixtures.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

In Germany, it is a major concern of forest policy and management to convert single-species coniferous forests into broad-leaved or mixed forests (Baumgarten and von Teuffel 2005). However, little is known on the economics of mixed forests. Some German forest scientists rather expect poor profitability while excluding risk, risk correlation and the opportunity of flexible timber harvesting from their analyses (Möhring 2004; Spellmann 2005). In contrast, the economic attractiveness of mixed forests was proven by, for example, Lohmander (1993) and Valkonen and Valsta (2001). Also Knoke et al. (2005) demonstrated that mixed forests could be an economically attractive option for risk-averse decision-makers. The authors, however, employed a fixed harvest policy, that is, harvesting was simulated at fixed points regardless of the timber price.

But a fixed harvest policy is not necessarily a useful option. In several studies it was shown that a flexible harvest policy is well suited to increase the profitability of monocultures. Brazee and Mendelsohn (1988), for example, applied dynamic programming to determine reservation prices. The reservation price would indicate that the current revenue would be equal to the expected net present valueFootnote 1 (NPV) of revenues from delayed harvests. Harvesting only if the actual price exceeded the reservation price increased the profitability significantly. Haight (1990) developed optimal feedback thinning policies with volatile prices that significantly increased NPV. Teeter and Caulfield (1991) obtained methodologically valuable results. They derived recommendations for thinning decisions based on a stochastic price model, which contained a first-order Markov process. While often a normal distribution of timber prices is assumed (e.g. Brazee and Mendelsohn 1988; Knoke et al. 2001), Reed and Haight (1996) used a log-normal diffusion process incorporating changes in stumpage price. They obtained extremely long right-hand tailed distributions of NPV. In addition to the aspect of volatile future stumpage prices, Gong (1998) incorporated risk preferences into calculations. However, up till now the aspect of timber price volatility and a flexible harvest policy has rarely been applied to mixed forests.

A flexible harvest policy may change the relation of profitability between different tree species. Moreover, waiting for an acceptable timber price bears the risk that it could not occur in a reasonable time. Hence, while it is possible to increase the NPV, if one applies flexible harvest policies, the dispersion of the expected NPV could also increase. Conventionally, an increased dispersion is synonymous to increased risk. Because of possible changes in profitability and risk, we assume that the optimum composition of species is sensitive to the flexible harvest policy. Considering the background this paper tries to test in a first part the following hypothesis.

H1: Employing flexible timber harvesting policies does not affect the optimum species composition according to the theory of portfolio selection

Recently, Mandelbrot and Hudson (2005) voiced fundamental critique on the so-called “modern financial theory,” which can also be applied to the theory of optimal portfolio selection. Mandelbrot argues that the standard assumption of a normal distribution of financial flows under risk, which is well described by its mean and standard deviation, is not the normal case. Hence, the second part of this paper investigates whether the simulated distributions of the NPV of different species and mixtures follow a normal distribution. Using the simulation technique it was analysed, whether the risk is adequately described by the standard deviation. The second part is consequently focussed on the following hypothesis.

H2: The assumption of normally distributed financial flows is appropriate to quantify the risk of forest management in pure and mixed forests

This study extends an existing approach on evaluating mixed forests, where harvests were carried out regardless of the actual simulated timber price (see Knoke et al. 2005), and builds upon data of the latter investigation. However, two completely new aspects relevant for the optimisation of species mixtures are considered. Consecutively, the silvicultural treatments are described briefly (section on “Silvicultural treatments”) as it is not the objective of this paper to investigate the effect of different silvicultural treatments on riskFootnote 2. After demonstrating how natural hazard risks were incorporated in the study, the timber price models are explained (section on “Modelling risks”). In the next section, the generation of the data via Monte-Carlo simulations (MCS) is presented. The approach of computing the combined risk of both species and the evaluation of the risks of mixed forests is demonstrated in the subsequent section.

While in the section on “Probability of a negative NPV,” the description of how and under which assumptions the probability of a negative NPV was simulated is explained, the section on “Results” contains the tests, which are divided into the effect of a flexible harvest policy and the test of the appropriateness of the normality assumption. In conclusion, the results are then discussed and summarised in the final section.

Material and methods

Silvicultural treatments

Possible mixtures of Norway spruce [Picea abies (L.) Karst] and European beech (Fagus sylvatica L.) were investigated. For both species rotations common in German forest management were applied (101 to 110 years for Norway spruce and 121 to 130 years for European beechFootnote 3). Knoke et al. (2005) have already described the approach and the growth simulations for each species. Hence, in this paper their description will be rather brief. All simulations were carried out for hypothetical pure stands of each species with an area of 1 ha. While simulating the mixture of the two species, it was assumed that the part of each species in a mixed stand would grow identically to a pure stand of that species. Hence, we adopted the position that neutral growth interactions occur if both species are mixed. For instance, Pretzsch (2005) has observed this for European beech and Norway spruce on several sites. Rather conservative silvicultural treatments were simulated. In spruce, thinning from below was applied, concluding with a clear cut at the end of the rotation. For beech the random selection treatment according to Knoke (2002) was used, which also ends with a clear cut. Silvicultural operations were scheduled once in a 10-year period. Both these treatments for Norway spruce and for European beech are obviously not modern treatments. However, the stands, which can be analysed at present have more or less developed under such treatments. As it is not known how silvicultural treatments will change in the future, it seems appropriate to assume historical treatments. The investigation of the effect of modern silvicultural treatments on risks and species mixtures is so abundant that it would fill another paper.

The data on simulated harvests were obtained from Knoke et al. (2005), who utilised the results of growth simulations from two other studies (Knoke 2002; Felbermeier, not published).

Modelling risks

Several risks were considered by means of MCS, of which the technical details are described later. Hazard risksFootnote 4 were adopted from the literature (e.g. Möhring 1986; Dieter 2001; Kouba 2002). We mainly concentrated on the survival probability curves published by Dieter (2001). These were derived from historical data on damages by insects, snow and wind throws. However, the curves were unable to predict realistic proportions of timber, which was harvested because of damages by natural hazards. Consequently, the curves were adjusted in order to reflect realistic proportions of damaged timber. Table 1 summarises the scheduled timber harvests for several age classes and the respective expected amounts of timber harvested due to natural damages. The curves applied to predict survival probabilities are depicted in Fig. 1.

Survival probabilities for European beech and Norway spruce [according to Dieter (2001) with alterations described in the text]

The data in Table 1 describes how much timber damaged by natural hazards is expected for stands of different age classes. The sum of all harvests due to natural hazards makes up 43% of the totally scheduled harvests for Norway spruce and only 11% for European beech. The proportion of harvests due to hazard damages within the area of the Bavarian forest service forms 43% of the total harvest between the years 1990 and 2001 (Bavarian Forest Service 2001). This proportion, which mainly arose from damaged coniferous timber, fits well to the simulated proportion for Norway spruce. Moreover, the simulated relation of the sensitivity for natural hazards was around 4:1 between Norway spruce and European beech. This relation also seems realistic; even von Lüpke and Spellmann (1999) reported susceptibility for storm damage of 4.6:1 when Norway spruce and European beech were compared in Bavaria. Further details of the calculation of hazard rates from the survival probabilities were described in Knoke et al. (2005).

The modelling of hazard risks was then carried out on the basis of a binomial distribution (function RANBIN of the SAS statistic program) with the possible outcomes of ‘1’ (damage) and ‘0’ (no damage). The frequency of ‘1’ depended on the regarding hazard risk. Vice-versa, the frequency of ‘0’ was proportional to the transition probability of the forest stands being the survival probability during growth from the current age to an older age. If an ‘1’ occurred, only 50% of the expected net revenue flow without damage was used in the calculation.

Also timber price fluctuation is a source of risk (e.g. Brazee and Mendelsohn 1988; Haight 1990). The timber price for Norway spruce was modelled by means of a first-order autoregressive model. Using historical data on timber prices from the Bavarian Forest Service, the following regression curve emerged (Eq. 1):

Here P t (S) denotes the timber price of Norway spruce and P t−1(S) the timber price from the previous year. The stochastic term s p contains the dispersion not explained by the model. It resulted in ± €7.91 per cubic metre. The expected mean timber price of this model was €83.1 per cubic metre achieving an r 2 of 0.57. Standard errors of parameters are given in parentheses.

In order to consider a possible timber price correlation between Norway spruce and European beech, a regression was carried out with the Norway spruce timber price as the independent and the European beech price as the dependent. The following regression curve resulted (Eq. 2, see Knoke et al. 2005):

In Eq. (2), P t (B) is the timber price of European beech and s p the stochastic term (±€8.89 per cubic metre). The expected mean timber price of this model was €90.07 per cubic metre achieving an r 2 of 0.38. The slope of the regression curve 2 indicates a slight negative correlation of the timber prices of both species.

For the estimation of the parameters of the two regression curves data from 1980 onwards were utilised. Applying data up to 1979 led to a positive correlation between timber prices of Norway spruce and European beech. The influence of the different timber price models (market models) has already been explored in the previous paper (Knoke et al. 2005).

Generation of data by means of MCS

MCS is often used to analyse the effects of stochastic processes (Yool 1999; Runzheimer 1999; Waller et al. 2003). This technique uses random numbers to incorporate the dispersion of expected values in a model. MCS is especially helpful if multiple sources of dispersion interact in affecting outcomes. Hence, the method is ideally suited to realistically simulate options in forest management that are usually exposed to multiple sources of risk.

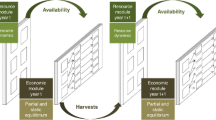

Basically, two steps were carried out: First, possible outcomes of harvest yields and net revenue flows had to be simulated for every year of the regarding simulation cycle. However, only one silvicultural operation was scheduled per 10-year period. Hence, in a second step, only one relevant observation was selected for every period out of the data that were generated previously. The first step is schematically summarised with Fig. 2, the second is depicted in Fig. 4.

Flow chart for generation of simulation data

After defining the planting expenses and initial timber price, it was simulated for each species whether or not a hazard damage occurs. This again was based on random numbers drawn from a binomial distribution (function RANBIN of the SAS statistic program). The net revenue flow (NRF) was estimated by age-dependent functions. The development of the stand values (net revenue when harvesting the stand and selling the timber at a specific stand age) without the impact of risks is shown in Fig. 3.

Development of the stand value for European beech and Norway spruce

In case a hazard was simulated, the NRF was reduced by 50% (this value was empirically derived by Dieter 1997), the stand age was set to zero and an artificial regeneration of the stand was simulated. Subsequently, a stochastic timber price was estimated with the autoregressive curve (Eq. 1) for Norway spruce and by means of an ordinary least square regression curve (Eq. 2) for European beech. Thereby, the latter curve depended on the Norway spruce timber price. Normally distributed stochastic deviations (mean of zero, standard deviation being the root mean square error of the regarding regression curve) were considered in both models. The actual NRF was estimated by multiplying the deterministically estimated value with a quotient. This was calculated by dividing the stochastic timber price by the expected timber price. Eventually, the adjusted stochastic NRF was discounted. The assumed discount rate was 2%. Within a single 10-year period the number of “period years” was enlarged by one with each re-iteration, after 10 years this number was set to zero repeating the loop over again. The simulation for one management cycle was stopped if the age was greater than the production time T (100 years) and the stochastic timber price exceeded the reservation price or if the age was beyond T+10. Furthermore, the simulation cycle was stopped if the number of periods was greater than the maximum number of periods to project. Two different time horizons were analysed. The baseline simulations were carried out for 101–110 years (ten periods); additionally, simulations over 501–510 years were conducted (50 periods). Assuming also long simulation cycles of over 500 years allowed for comparing different rotation periods.Footnote 5 After one simulation cycle had ended, the next one was started until 1,000 repetitions were attained.

In a second step, the relevant data (one observation per 10-year period) had to be selected (Fig. 4) out of the data generated with Program 1. The main reason for selecting one observation was the simulated hazard damage. Moreover, an observation was selected if the simulated timber price exceeded the expected threshold (reservation price) for the first time. If neither a hazard was simulated nor a timber price was greater than the reservation price during the 10 years of a period, the last observation was selected regardless of the timber price. This means that one silvicultural operation had to be carried out in every period. Based on the selected observations, NPV for every simulation cycle (one up to 1,000) were computed. Through 1,000 repetitions, the average NPV and its dispersion could be computed. In addition, the coefficient of correlation between the NPV of both species resulted.

Flow chart for selection of relevant data

To form a basis to start from, all simulation cycles were carried out assuming a fixed harvest schedule at first, that is, a harvest policy without a reservation price. Here, the silvicultural operations were carried out regardless of the timber price in the first year of the period. Subsequently, different reservation prices were tested. The reservation price was used here as a threshold. When the simulated timber price exceeded the reservation price for the first time in a 10-year period, a harvest operation was simulated (presuming that no harvest due to damage occurred). In an initial step, 90% of the mean historical timber price was tested as a reservation price, followed by 95% of the mean historical timber price. Thereafter, the reservation price was gradually enlarged in 5% increments up to 115% of the mean historical timber price. Hence, the optimum reservation price was not derived analytically, but iteratively. For the computation of the optimum species mixture, the reservation price was utilised which maximised the NPV of forest management.

Combining risks of tree species and evaluation of risks

The following section contains some fundamental assumptions of the theory of portfolio selection (see, e.g. Elton and Gruber 1995). First, it is assumed that the NPV of a mixed forest, where two tree species are combined, can be calculated on the basis of Eq. (3).

- a 1,a 2 :

-

Proportion of each tree species (a 1+a 2=1)

- npv 1, npv 2 :

-

NPV of Norway spruce or European beech, respectively (computed as the sum of all discounted NRF)

Conventionally, the standard deviation of an expected value is used to quantify financial risk (Pflaumer 1992). Therefore, it is important to be able to compute the standard deviation of NPV for mixed forests. It is obtained through Eq. (4) (see, e.g. Markowitz 1952).

- SNPV :

-

Standard deviation of the NPV of a mixed forest with a certain species composition

- \( s_{{npv_{1} }} {\text{, }}s_{{npv_{2} }} \) :

-

Standard deviation of NPVs – npv 1 or npv 2 – of the individual tree species

- k npv1,npv2 :

-

Correlation coefficient between the net present values of tree species 1 and 2

Risk-aversion is an attitude often observed among humans (Bamberg and Coenenberg 1992; Elton and Gruber 1995; Spremann 1996; Valkonen and Valsta 2001). Financial risk obviously diminishes the economic utility of financial investments. The existence of numerous insurances in real life proves this attitude. Assuming risk-aversion means that a decision-maker prefers a secure NPV rather than one, which is subject to dispersion. This means a lower NPV may be equivalent to a higher one if the first is subject to a small dispersion (low risk) while the second is subject to a great dispersion (high risk). Hence, low risk might compensate for low NPV, whereas only a considerably high NPV can compensate great risk. In order to include this effect in our study, a simple preference function (Eq. 5) was used. The equation estimates the certainty equivalent of risk-averse decision-making under the assumption of the classical negative exponential utility curve.

- CE:

-

Certainty equivalent

- E(NPV):

-

Expected NPV

- S 2NPV :

-

Variance of financial returns

- α :

-

Constant depending on the decision-maker’s attitude towards risk

The expected mean NPV and the standard deviation are combined in Eq. 5 as a μ-σ-rule. This shows that a decision-maker values an investment not only by means of its expected average NPV but also on the basis of its uncertainty, which is expressed by the expected variance of the NPV. Thus, expected utility is defined in terms of mean and variance. As Eq. (5) shows, the expected NPV is reduced proportionally to the variance of the NPV. The function is an approximation for the certainty equivalent of a risk-averse decision-maker, valid for a small α (Gerber and Pafumi 1998, p. 77). The constant α in Eq. 5 quantifies the degree of risk-aversion of the decision-maker. It may be estimated by the quotient “a/initial investment” (Spremann 1996, p. 502). In investment analysis ‘a’-values around 1 are considered normal. We carried out calculations for ‘a’-values between 0.5 (almost no risk-aversion) and 2.5 (very risk-averse). The maximum initial investment for a forest plantation of €3,000 per ha was used to estimate α-values depending on the degree of risk aversion (expressed by ‘a’).

For every ‘a’, the mixture of Norway spruce and European beech was computed that maximised the certainty equivalent according to Eq. (5).

Probability of a negative NPV

What is important to an investor is with which probability the returns of an investment will be less than the investment. This information is provided by the frequency of a negative NPV during the simulations, which can be interpreted as the probability of a negative NPV.

However, to obtain realistic information the overhead costs had to be considered in this analysis. Hence, a constant yearly payout of €50 per ha was assumed as overhead costs. The analysis was exemplarily carried out for time horizons between 101 and 110 years. First, the sum of the discounted yearly overhead costs was formed. Then, the simulated NPV were diminished by the sum of the discounted overhead costs.

To test the appropriateness of the normality assumption (i.e. the distribution of NPV follows the Gaussian distribution) when quantifying risk the frequency of negative NPV was also calculated on the basis of a normal distribution. The frequency of negative NPV under the normality assumption was compared with the actually simulated frequency of negative NPV.

Results

Effect of the harvest policy

In Tables 2 and 3, the basic data achieved by the simulations is compared with the NRF without risk. For the sake of simplicity only data for rotations between 101 and 110 years are presented.

It is obvious that integrating natural hazard risks diminished the mean NRF especially in the case of Norway spruce dramatically. The NRF for harvesting the final crops decreased from €34,039 without hazard risks, to 17,622 under a fixed harvest, and to 19,917 per ha under a flexible harvest policy. The mean NPV decreased from €5,731 to 3,403 and 3,702 per ha, respectively. For European beech, the impact of natural hazard risks was by far less intense when compared with the Norway spruce. The NPV without hazard risks (€2,916 per ha) declined merely to €2,522 (fixed harvest policy) or 2,973 per ha (flexible harvest policy) when natural hazard risks were considered. Here, the loss by natural hazards could even be compensated by a flexible harvest policy.

The effect of a flexible harvest policy is obvious for both species. Harvesting only if the simulated price exceeded the reservation prices (presuming that no damage occurred), increased the discounted NRF for both species in most cases (Tables 2 and 3). Consequently, the NPV was increased, too. The maximum NPV was achieved when using 105% of the mean historical timber price as a reservation price (Table 4).

The NPV of Norway spruce increased by 9%, while the risk (standard deviation of NPV) increased by 5%. European beech benefited more from a flexible harvest policy than Norway spruce. Its NPV increased by 20%, while the risk increased only by 7%.

Considering 501–510 instead of 101–110 years, of course, increased the NPV (Table 5). The NPV of Norway spruce became about €1,300 per ha greater, while the NPV of European beech increased by about €900 per ha. Also here, the gain of a flexible harvest policy was greater for European beech (+ 34 %) than for Norway spruce (+ 19 %). The risk remained more or less constant even if a flexible harvest policy was applied.

Based on the NPV, the regarding standard deviations and the correlation coefficients of Tables 4 and 5, risk-return curves for both a fixed and a flexible harvest policy could be derived. For this purpose Eqs. (3) and (4) were used by varying the proportions of Norway spruce and European beech. Figure 5 depicts risk-return curves for time horizons of 101–110 years. Given a fixed harvest policy, European beech achieved only a NPV of €2,522 per ha (standard deviation ± €1,380), while €3,403 per ha (standard deviation ± €2,470) resulted for Norway spruce. Mixing Norway spruce into a European beech forest first diminished the risk, while it simultaneously increased NPV. A minimum of risk was achieved with 80% European beech and 20% Norway spruce. Starting from this point, any further admixture of Norway spruce increased NPV for the price of an increased risk. Somewhere between the minimum of risk and its maximum, the risk-averse decision-maker would find the optimum combination of Norway spruce and European beech according to the theory of portfolio selection (see later in this section).

Risk-return relation for several mixtures of European beech and Norway spruce (considered time horizons: 101–110 years)

For both tree species a flexible harvest policy increased NPV as well as the risk – with the latter only changing slightly. Thus, the risk-return curve shifts to the right. The risk minimum was still achieved when mixing 80% of European beech and 20% of Norway spruce. However, the slope of the curve between the risk minimum and maximum became steeper. This effect arises because the gain of NPV by a flexible harvest policy was €300 per ha for Norway spruce, but €500 per ha for European beech. Because of the steeper slope of the risk-return curve, admixing European beech in an existing Norway spruce forest would more effectively reduce risk than under a fixed harvest policy.

For times horizon of 501–510 years, the advantage of a flexible harvest policy of every rotation added up. Overall, the NPV of both tree species was increased to a greater extent than under the 101- to 110-year projection. In contrast to the 101- to 110-year time horizons, the risk-return curve between the risk minimum and maximum for 501–510 years became only slightly steeper. The effect is hardly visible. Nevertheless, it is present as the NPV of European beech benefited €1,000 per ha from a flexible harvest policy, while that of Norway spruce grew only by €800 per ha (Fig. 6).

Risk-return relation for several mixtures of European beech and Norway spruce (considered time horizons: 501–510 years)

For a varying degree of risk-aversion, Fig. 7 shows the proportions of European beech, which would maximise the certainty equivalent in a forest managed under a fixed or a flexible harvest policy respectively. It is evident that under a flexible harvest policy the optimum proportion of European beech is greater in comparison with a fixed harvest policy.

Optimum proportion of European beech and degree of risk-aversion (considered time horizons: 101–110 years)

The greatest difference occurred for a very small risk-aversion (a=0.5). Under this assumption the forest owner should hold about 30% of the European beech when employing a flexible harvest strategy. However, if a fixed harvest policy is practiced, only 10% of the European beech would be optimal. The impact of the harvest policy decreased with increasing risk-aversion. An extremely risk-avoiding person (a=2.5) would grow about 60% of European beech regardless of the harvest policy.

The effect of greater optimum proportions of European beech under a flexible harvest policy is still visible when considering 501–510 years (Fig. 8). However, the maximum difference between a fixed and a flexible harvest policy (i.e. at a=0.75) is merely a 5% points greater proportion of European beech.

Optimum proportion of European beech and degree of risk-aversion (considered time horizons: 501–510 years)

In conclusion, it can be said that a flexible harvest policy would increase the optimal proportion of European beech in mixed forests under the assumption that the NPV were normally distributed. Whether the assumption of a normal distribution is in fact appropriate when quantifying risk will be investigated in the next section.

The assumption of a normal distribution

The theory of optimal portfolio selection relies on the validity of the assumption that the financial flows and the indicators of economic performance (e.g. the NPV) are normally distributed. Under this assumption Eq. 4 can be applied and probabilities for negative NPV can be computed from the mean NPV and its standard deviation. In this section, we will test whether the normality assumption is reasonable for the analysed situations.

Figure 9 shows three examples of frequency distributions for simulated NPVFootnote 6 under the flexible harvest policy scenario. For Norway spruce a distribution with two maxima is seen. Thus, the shape of the simulated distribution differs rather from the expected under the assumption of normality (depicted as a solid line in Fig. 9). However, the part of the simulated distribution, which shows negative NPV (left part), is more or less well approximated by the expected normal distribution. Consequently, the simulated frequency of negative NPV (i.e. 30%) was quite similar to the frequency expected under the assumption of a normal distribution (i.e. 28%) (see Table 6). Merely a slight underestimation of this frequency arose when applying the normality assumption.

Simulated and expected frequencies of NPV under a flexible harvest policy

Though the general shape of the simulated distribution is quite similar to a normal distribution for European beech, major deviations are obvious especially where negative NPV occur (Fig. 9). The density of simulated values close to the mean is much greater than expected under the assumption of a normal distribution. However, few simulated NPV are extremely negative. This fact obviously led to an overestimation of the standard deviation. The expected normal distribution therefore becomes much broader than the simulated frequency distribution. The simulated frequency of negative NPV for European beech is only 17% while the same frequency under the normality assumption results in a frequency of 28% (Table 6). This analysis shows a great overestimation of risk for European beech when using the frequency of negative NPV as a risk measure and applying the assumption of normally distributed NPV.

In a mixed forest of 80% European beech and 20% Norway spruce the simulated frequency of negative NPV was only 16%, which was even slightly smaller than that in a pure European beech forest. Still, the overestimation of the frequency of negative NPV is great when applying a normal distribution. In the latter case, 23% of the NPV were expected to be negative.

As Table 6 shows only for a mixture of 50% European beech and 50% Norway spruce and under a fixed harvest policy, the simulated frequency of negative NPV agrees to the expected frequency. With growing proportion of European beech the bias of risk estimation increased when assuming normality.

In Fig. 10, the simulated frequencies of negative NPV are compared with the expected frequencies when assuming normality. It is quite clear that the expected probability of negative NPV under the assumption of normality is greatly biased. The minimum frequency of negative NPV would be found under this assumption with a mixture of 50% European beech and 50% Norway spruce. Actually, the minimum frequency of negative NPV (i.e. 15%) was simulated for a mixture of 90% European beech and 10% Norway spruce.

Comparison of several measures for risk

The demonstrated effect leads to an underestimation of the fraction of European beech when applying the theory of portfolio selection: According to our simulations, a mixture of 70% European beech and 30% Norway spruce would achieve an identical frequency of negative NPV when compared with a pure European beech forest. Focussing on the standard deviation used in optimisation according to the portfolio theory (μ-σ-rule) a mixture of 55% European beech and 45% Norway spruce would result in the same risk as a pure European beech forest (Fig. 10). Hence, the proportion of European beech in a mixed forest for an identical risk as in a pure European beech forest was underestimated by 15% points with the classical portfolio approach.

Discussion and conclusions

This paper focussed on two hypotheses. Regarding the first hypothesis, “Employing flexible timber harvesting policies does not affect the optimum species composition according to the theory of portfolio selection,” it was shown that a flexible harvest policy leads to increasing optimal proportions of European beech according to the theory of portfolio selection. Thus, the hypothesis H1 may be rejected.

It has become obvious that European beech benefits more from a flexible harvest policy. Since the natural hazard risk is much greater for Norway spruce, part of the gain in profitability is lost due to its frequent hazard damages. In contrast, European beech is much less susceptible to natural hazards. Thus, the advantage of flexible harvesting can almost be fully utilised when growing European beech. Logically, improved profitability makes it more attractive to have European beech in the portfolio, thus the proportion of European beech increases under a flexible harvesting policy.

These results, however, were based on the assumption of normally distributed NPV. The validity of this crucial assumption was tested with the second hypothesis, “The assumption of normally distributed financial flows is appropriate to quantify the risk of forest management in pure and mixed forests.” The results of this hypothesis showed that this assumption is appropriate neither for European beech nor for Norway spruce or mixtures. Particularly in the case of European beech, significant overestimation of risk results through the assumption of normally distributed NPV. The optimal proportions of European beech according to the theory of optimal portfolio selection are therefore too small. Hypothesis H2 must be rejected for this example.

The results were obtained while simulating the hazard risks explicitly. One could argue that it is sufficient to consider only the timber price fluctuations, since they already express the impact of natural hazards via low timber prices. Thus, the simulation of natural hazards could have been omitted. We did not pursue this idea because of several reasons: First, the timber prices were achieved all over Bavaria. Compensative effects might occur when computing average prices from several regions. Second, the forest service was normally forced in years of storm damage to sell only small amounts of timber to stabilise timber prices. Hence the prices achieved in such years could be biased. Third, focussing only on the timber price means ignoring effects of serious quality decreases (broken timber) and greatly increased harvesting costs incurred by natural hazards. Consequently, we assumed a reduction in the NRF by 50% after a natural hazard. According to Dieter (1997) this is a realistic relation. Considering the effect of hazard risk explicitly led to serious deviations of the simulated frequency of NPV from a normal distribution. Mandelbrot and Hudson (2005) have impressively proven that such deviation is not seldom. Simulation and optimisation of forest stand management means that the results of portfolio selection always have to be tested through MCS. The actually simulated frequency of negative NPV might be a more reliable indicator than the optimal mixture according to the theory of portfolio selection, which relies on the assumption of normally distributed financial flows. If the risk of a pure European beech forest is acceptable, we can recommend a mixture of 70% European beech and 30% Norway spruce. This mixture would significantly improve the profitability when compared with the pure European beech forest, while the risk would be the same.

This demonstrated analysis has rarely been applied in German forest science. In fact, Deegen et al. (1997) described the portfolio theory in the context of tree species choice in forestry, but did not apply this technique. Wippermann and Möhring (2001) and Weber (2002) were the first to apply the theory of portfolio selection to forestry in Germany. Penttinen and Lausti (2004) analysed the relevant English literature on portfolio applications to forestry. The majority of studies are applications of the Capital Asset Pricing Model developed by Sharpe in the year 1964 (e.g. Wagner and Rideout 1991, 1992; Zinkhan and Cubbage 2003). Applications of optimal portfolio selection with regard to the optimum species diversity were found rather seldom. However, Thomson (1991) computed a financially optimum mixture for a “moderately” risk-averse investor comprising of about 73% coniferous and 27% deciduous tree species.

All the cited references relied on the assumption of normality. As the present study shows, this assumption might lead to biased risk estimations. Consequently, we would strongly advise testing the robustness of optimal portfolios via MCS. The frequency of negative NPV seems to be a good measure to describe the risk of forest management in such simulations. The combination of several risks in MCS in order to investigate the effects of tree species diversity also seems a helpful aid for forest science decision-making. It allows for valuable insights and has proven that the economic concerns on the establishment of hardwoods offered by some German scientists can be overcompensated by beneficial effects of risk compensation. This is a crucial aspect, which should also be considered in future studies on tree species mixtures.

Notes

The NPV is formed by the sum of all appropriately discounted net revenue flows.

An earlier exemplary paper has already been written on this topic (see Knoke et al. 2001).

For European beech also rotation periods between 101 and 110 years were tested in order to provide identical investment periods.

Locally related survival probabilities for forest offices in Baden-Württemberg were published, for example, by Hanewinkel and Holcey (2005).

If two rotation periods of different lengths were compared (e.g. 100 and 120 years) considering only one rotation period would be a biased evaluation (see Knoke et al. 2005).

Here the NPV was reduced on average by €2,182 per ha, which was the sum of the discounted overhead costs.

References

Bamberg G, Coenenberg AG (1992) Betriebswirtschaftliche Entscheidungslehre. Vahlen, München

Baumgarten M, Teuffel K von (2005) Nachhaltige Waldwirtschaft in Deutschland. In: Teuffel K von, et al (eds) Waldumbau. Springer-Verlag, Berlin Heidelberg New York, pp 1–10

Bavarian State Forest Service (2001) Jahresbericht 2001. Bavarian State Ministry of Agriculture and Forests, Munich

Brazee R, Mendelsohn R (1988) Timber Harvesting with Fluctuating Prices. For Sci 34:359–372

Deegen P, Hung BC, Mixdorf U (1997) Ökonomische Modellierung der Baumartenwahl bei Unsicherheit der zukünftigen Temperaturentwicklung. Forstarchiv 68:194–205

Dieter M (1997) Berücksichtigung von Risiko bei forstbetrieblichen Entscheidungen. Schriften zur Forstökonomie Bd. 16. Frankfurt/Main: J.D. Sauerländer’s

Dieter M (2001) Land expectation values for spruce and beech calculated with Monte Carlo modelling techniques. For Policy Econ 2:157–166

Elton EJ, Gruber MJ (1995) Modern portfolio theory and investment analysis, 5th edn. Chichester, Wiley, New York

Gerber HU, Pafumi G (1998) Utility functions: from risk theory to finance. North Am Actuarial J 2:74–100

Gong P (1998) Risk preferences and adaptive harvest policies for even-aged stand management. For Sci 44:496–506

Haight RG (1990) Feedback thinning policies for uneven-aged stand management with stochastic prices. For Sci 36:1015–1031

Hanewinkel M, Holcey J (2005) Quantifizierung von Risiko durch altersstufenweise Ermittlung von Übergangswahrscheinlichkeiten mit Hilfe von digitalisierten Forstkarten. In: Teuffel K von, et al (eds) Waldumbau. Springer-Verlag, Berlin Heidelberg New York, pp 269–277

Knoke T (2002) Value of perfect information on red heartwood formation in beech (Fagus sylvatica L.). Silva Fennica 36:841–851

Knoke T, Moog M, Plusczyk N (2001) On the effect of volatile stumpage prices on the economic attractiveness of a silvicultural transformation strategy. ForPolicy Econ 2:229–240

Knoke T, Stimm B, Ammer C, Moog M (2005) Mixed forests reconsidered: a forest economics contribution to the discussion on natural diversity. For Ecol Manag 213:102–116

Kouba J (2002) Das Leben des Waldes und seine Lebensunsicherheit. Forstwissenschaftliches Centralblatt 121:211–228

Lohmander P (1993) Economic two stage multi species management in a stochastic environment: the value of selective thinning options and stochastic growth parameters. Syst Anal-Model-Simul 11:287–302

Lüpke B, Spellmann H (1999) Aspects of stability, growth and natural regeneration in mixed Norway spruce-European beech stands as a basis of silviculture decisions. In: Olsthoorn AFM et al. (eds). Management of mixed-species forests: silviculture and economics. Wageningen: IBN-DLO Scientific contributions, pp 245–267

Mandelbrot BB, Hudson RL (2005) Fraktale und Finanzen: Märkte zwischen Risiko, Rendite und Ruin. Piper, München

Markowitz H (1952) Portfolio selection. J Finance 7:77–91

Möhring B (1986) Dynamische Betriebsklassensimulation – Ein Hilfsmittel für die Waldschadensbewertung und Entscheidungsfindung im Forstbetrieb. Berichte des Forschungszentrums Waldökosysteme-Waldsterben der Universität Göttingen Band 20

Möhring B (2004) Betriebswirtschaftliche Analyse des Waldumbaus. Forst Holz 59:523–530

Penttinen M, Lausti A (2004) The competitiveness and return components of NIPF ownership in Finland. Finnish J Business Econ, Spl Edn 2/2004

Pflaumer P (1992) Investitionsrechnung. Oldenburg Verlag, München, Wien

Pretzsch H (2005) Diversity and productivity in forests: evidence from long-term experimental plots. In: Scherer-Lorenzen et al. (eds) Forest diversity and function: temperate and boreal systems. Ecological studies, vol 176. Springer-Verlag, Berlin Heidelberg New York, pp41–64

Reed WJ (1996) Predicting the present value distribution of a forest plantation investment. For Sci 42:378–387

Runzheimer B (1999) Operations research. Gabler, Wiesbaden

Sharpe WF (1964) Capital asset prices: a theory of market equilibrium under conditions of risk. J Finance 14:425–442

Spellmann H (2005) Produziert der Waldbau am Markt vorbei? Allg. Forstzeitschrift/Der Wald 60:454–459

Spremann K (1996) Wirtschaft, Investition und Finanzierung. 5., vollständig überarbeitete, ergänzte und aktualisierte Auflage. Oldenbourg: München und Wien

Teeter LD, Caulfield JP (1991) Stand density management under risk: effects of stochastic prices. Can J For Res 21:1373–1379

Thomson TA (1991) Efficient combinations of timber and financial market investments in single-period and multiperiod portfolios. For Sci 37:461–480

Valkonen S, Valsta L (2001) Productivity and economics of mixed two-storied spruce and birch stands in Southern Finland simulated with empirical models. For Ecol Manag 140:133–149

Wagner JE, Rideout DB (1991) Evaluating forest management investments: the capital asset pricing model and the income growth model. For Sci 37:1591–1604

Wagner JE, Rideout DB (1992) The stability of the capital asset pricing model’s parameters in analysing forest investments. Can J For Res 22:1639–1645

Waller LA, Smith D, Childs JE, Leslie AR (2003) Monte Carlo assessment of goodness-of-fit for ecological simulation models. Ecol Model 164:49–63

Weber M-W (2002) Portefeuille- und Optionspreis-Theorie und forstliche Entscheidungen. Schriften zur Forstökonomie Band 23. Sauerländer’s, Frankfurt a.M

Wippermann Ch, Möhring B (2001) Exemplarische Anwendung der Portefeuilletheorie zur Analyse eines forstlichen Investments. Forst Holz 56:267–272

Yool A (1999) Comments on the paper: on repeated parameter sampling in Monte Carlo simulations. Ecol Model 115:95–98

Zinkhan FC, Cubbage FW (2003) Financial analysis of timber investments. In: Sills EO, Abt KL (eds) Forests in a market economy. Forestry sciences, vol 72. Kluwer, Dordrecht, Boston, London, pp 77–95

Acknowledgements

The authors wish to thank Mrs. Edith Lubitz for the language editing of the manuscript and two anonymous reviewers for valuable suggestions.

Author information

Authors and Affiliations

Corresponding author

Additional information

Communicated by Hans Pretzsch

Rights and permissions

About this article

Cite this article

Knoke, T., Wurm, J. Mixed forests and a flexible harvest policy: a problem for conventional risk analysis?. Eur J Forest Res 125, 303–315 (2006). https://doi.org/10.1007/s10342-006-0119-5

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10342-006-0119-5