Abstract

The management and exploitation of renewable energy sources is now recognised as central to sustainable development. Environmental concerns, recurring oil crises and market weaknesses, combined with the availability of power from natural resources and resulting possibilities for job creation and energy independence, have all pushed developed and developing countries towards new energy strategies that include RES. This paper analyses the profitability of potential investments in small, medium and large RE electrical power facilities, applying a Net Present Value (NPV) methodology. The proposed financial analysis permits strategic selection of an energy portfolio from among available sources and plant sizes. The paper then discusses potential constraints, and where possible applies the NPV methodology for estimating the necessary changes in decision-making. It defines the role of government incentive schemes in the financial results and evaluates the impact of variation in critical variables (subsidies, sale price of electricity, investment cost, operating cost and equivalent operating hours) on the estimation of NPV. Finally, the paper analyses the environmental impact of all the energy sources examined, examines the links with the financial results and proposes socio-economic policy considerations based on the entirety of the research results. While the methodology is applied to the Italian case, it could be modified to serve in other nations by adapting the input parameters to reflect the different regulatory and market contexts.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

Renewable energy is derived from natural sources that are replenished at a higher rate than they are consumed. Planning for the use of renewable energy currently attracts significant attention within the academic, managerial and policy-making communities (Manzano-Agugliaro et al. 2013). The questions involved are multidisciplinary and complex, and management must be timely and strategic. The renewable sources that have shown the greatest increase in recent years are biomass (Panepinto et al. 2014), wind (Fokaides et al. 2014) and solar (Ranjan and Kaushik 2014). The diversification of electricity generation portfolios is recognized as capable of influencing wholesale prices (Banal-Estañol and Micola 2009). For fossil fuel power plants, carbon capture and storage technologies offer the potential for significant reductions in carbon dioxide emissions (Reza et al. 2013). According to the White Paper for a Community Strategy and the Action Plan, Renewable Energy Sources, the goal of the European Union is to use RES to reduce dependence on imports and increase supply security. Other positive effects are the amelioration of climatic problems and job creation. According to the Renewable Energy Policy Network for the 21st Century (REN 21) 2013 Global Status Report:

-

Global investment in RE reached 244 G$ in 2012, down 12 % from the previous year’s record;

-

Global renewable power capacity worldwide exceeded 1,470 GW in 2012, up about 8.5 % from 2011;

-

Global demand for renewable energy was equal to 19 % of global final energy consumption in 2011;

-

About 5.7 million people worldwide work either directly or indirectly in RE industries: 30 % of these are in China, 22 % in the European Union; 42 % are employed in bioenergy and 24 % in photovoltaic industries.

The global electricity supply industry has been identified as a major source of greenhouse gas (GHG) emissions. Most nations are investing in RE technology to meet emission targets and increase the share of power from RES, but the sector is not yet self-sustaining (Verma and Kumar 2013). One cause is that while the RE sector is potentially appealing, private investment remains insufficient. An analysis by Masini and Menichetti (2013) has revealed that to the private investor, the technical adequacy of the opportunity plays a much more important role than the perceived effectiveness of existing policies. In fact the EU capability to coordinate the member countries’ renewable energy policies is low, while such coordination is necessary to be competitive on the energy market (Krozer 2013). For improved competitiveness, a useful strategy is the application of “green” supply-chain management principles (Cucchiella and D’Adamo 2013). Distributed generation is also emerging as a successful means to meet the increasing demand for electricity (Planas et al. 2013). Under this strategy, micro-grids and virtual power plants (clusters of linked small plants) facilitate the cost-efficient integration of distributed energy resources into the existing power system (Strbac et al. 2008). In these systems, the various small plants are interconnected and managed by an intelligent network known as the smart grid. The smart grid reduces the extent of intermittent RES power fed into the main grid, achieving better stability, and also reduces the total demand of electricity from the main grid, thus gradually reducing the need for further investments in the national distribution system (Barnham et al. 2013).

Concerning the residential sector, studies have defined some of the determinants of consumer willingness to adopt renewable energies in the residential sector: middle-aged and highly educated people are more willing to adopt RES for their homes, and a tax deduction is seen as more attractive than an energy subsidy (Chen et al. 2011). Several requirements are necessary in order to achieve increased use of RES in the residential sector: (i) construction or adaptation of houses and condominiums that generate electricity using RE technologies; (ii) development of appropriate storage systems with appropriate technologies and sizes; and (iii) development of RE plants that remain self-sufficient over a useful lifespan (Cucchiella et al. 2013b).

The development of RES and the objectives of environmental protection requires the achievement of sustainability in the development of RES power plants and systems (Cucchiella et al. 2012). Investments in RES must be financially profitable (Bader et al. 2005). For the investor, the definition of performance and risk is crucial in identifying the optimal energy portfolio (Cucchiella et al. 2012). The aim of the current paper is to support the decision-maker by illustrating an analytical methodology for examining such potential performance and risks. The context is the Italian national energy system, with its relative incentive and sales systems. An essential part of the methodology used is discounted cash flow analysis, using the indicator of Net Present Value (NPV) (Vanhoucke et al. 2001). The specific objectives of the paper are as follows:

-

1.

To define a methodology for the assessment the financial profitability of investment in different RE-source electrical plants, given a series of potential plant dimensions

-

2.

To compare the profitability of investment in different potential RE sources for a given plant size

-

3.

To compare all the facilities examined (all combinations of sources and plant size)

-

4.

To discuss and identify changes in decision-making due to the presence of constraints

-

5.

To identify the incidence of incentives on the financial results achieved

-

6.

To analyse the environmental impact of all the RE sources examined

-

7.

To identify some socio-economic policy considerations arising from the analyses.

While the methodology is applied to the Italian case, it could be modified to serve in other nations by adapting the input parameters to reflect the different regulatory and market contexts.

Methodology

The next section of the paper provides a brief review of the Italian energy system, which is the context for the study.

The actual methodology of the paper then involves several steps. “Mathematical model and input parameters for the Italian context” section continues with the detailed presentation of the mathematical model and the relative environmental and economic data for the different types of RE generation facilities, with these data in some cases being specific to the Italian context. We consider four RE sources: (i) solar, particularly photovoltaic generation, which is the most widespread technology in Italy; (ii) wind, specifically on-shore generation; (iii) bioenergy, where biomass is the most common source, having higher electrical production than bio-liquids and biogas; and (iv) hydro, which represents the most mature technology. Geothermal energy is used in only one region (Tuscany) and thus is not considered. The input data for the NPV model are developed in function of a series of plant sizes for each of the four sources: 10, 100 kW, 1, 5, 10 and 100 MW. The consideration of this range of sizes permits analysis of economies of scale and the impact of several incentive schemes.

In “NPV analysis: financial profitability of investments in RES” section of the paper, we calculate the NPV of all the potential RE facilities (four sources and six plant sizes), to define the financial profitability of investment in the various forms and sizes of RES. For each potential plant size, we identify the RES that generates the best financial outcome. We examine the decision-making implications of these results in some detail.

In “Effects of real-world constraints on managerial decision-making” section some we identify potential constraints on managerial decision-making: (i) the availability of the RE source; (ii) the possibility of obtaining the initial investment amount; (iii) the need to provide sufficient energy to meet a specific demand; (iv) the changing cost of the plants in function of market conditions; (v) changes in subsidies arising from incentive scheme; and (vi) local conditions specific to the nature of the individual RE sources. The paper discusses the influence of these constraints on decision-making, and where relevant it applies the NPV model to calculate their effects.

The development of RE is strongly characterized by incentive policies. Thus in “The role of incentives” section we examine the impact of subsidies on the financial results and evaluate the role of several incentive schemes. In “Sensitivity analyses” section we use sensitivity analysis to determine how changing values for the independent variables (costs, revenues and operating hours) impact on NPV for the various RE sources and their plant sizes.

Section “Environmental impact analysis and policy considerations” analyses the environmental benefits resulting from the utilization of RE plants, and finally proposes several socio-economic policy considerations regarding the entire sector of renewable energy. “Conclusions and future directions” section notes the paper’s conclusions in terms of decision-making at the investor and policy levels and suggests some further research directions.

The mix of energy sources in Italy

The Italian energy sector is strongly dependent on imported crude oil and gas, thus exposing national energy security to vulnerability. Over the past decade, the use of oil has decreased significantly (down 11 %), with replacement by natural gas (+3.5 %) and renewable sources (+6 %). The Italian state has promoted development of RE sources as a strategy to increase generating capacity and decrease electricity imports. Hydro power provides the most relevant contribution, while wind and bioenergy have shown strong growth over the years. Solar was almost completely neglected, until 2006 but has shown a remarkable growth trend over the more recent 2010–2012 period (Table 1).

The expectation of the EU is that in Italy, RE should achieve a 17 % share of national electricity production by 2020: equal to 28.4 Mtoe (Million tons of oil equivalent) compared to an expected energy demand of 167 Mtoe. The latest estimates by the Italian Ministry of Economic Development show a decrease in energy consumption in 2012 (178 Mtoe) compared to 2011 (184 Mtoe) and an yearly increase (1.8 %) of energy produced by renewable sources, achieving a national share of 15.1 %. Italy is thus on track towards the EU targets.

Given this context in the subsequent sub-sections, we begin the analysis of the investments process for the four RE sources considered. We consider the first year of potential project start-up as 2011. Each renewable system requires different time for its installation: 1 year for photovoltaic and wind, 1.5 years for biomass and hydro (Munoz et al. 2009). As a consequence, photovoltaic and wind systems will operate in the first semester of 2012, while biomass and hydro will start to operate at the end of the same year. According to the EU planning guidelines, the project lifetime is 20 years, and opportunity cost is 5 %. We assume 100 % funding of the initial investment based on a 15 year loan with a three-monthly rate, estimated with the simple capitalization method. The spread is equal 1.75 % and the 3 month Euribor is 1.14 %. The following sub-sections show the methodology used, and the input data needed in order to establish the future cash flows.

Mathematical model and input parameters for the Italian context

Mathematical model

It is standard practice to use NPV for the financial evaluation of long-term plant investments, measured in terms of the difference between incomes and costs. For a detailed description of the model applied to energy plants see Cucchiella et al. (2012).

For all energy plants, costs are linked to size. Moreover, for all renewable energy sources, with varying plant sizes, there are also variations in government financial support systems (in Italy, specifically Feed-in Tariff—FiT and Premium Feed-in Tariff—FiP). Equations [1] and [2] define the NPV, respectively, from a photovoltaic (PV) renewable resource and from biomass, hydro or wind (Bi, Hy and Wi) sources. In this case, it is not possible to use a single equation, since PV investments can benefit from FiT financial support, while the other renewable sources benefit from FiP support (quantified, respectively, at formulas [3] and [4]). The subsequent equations [5], [6] and [7] quantify the input parameters for government financial support for energy produced from RES plants (E f—see equations [8] and [9]). The different subsidies change in function of two variables: equivalent hours of operation (h eq) and installed capacity facility (C in).

The second potential source of income for investment in RE sources is revenue from the sales of electricity (SP el) injected into the national grid. SP el is related to several variables, with all the cases described by equations [10], [11] and [12].

Costs are defined under equations [13] and [14]. Since the projects are not definitive, it is necessary to gather benchmarks on project costs for renewable sources. This includes information on capital expenditure (capex—see equation [17]) and operating expenditure (opex—see equation [18]). In the case of external financing, additional costs must be accounted for rates on capital (L CS—see equation [15]) and interest (L IS—see equation [16]). For this, we assume a 15 year loan with three-monthly rate.

NPV, as described above, is the indicator of financial profitability. The economic model is described in the following formulae:

Revenue estimations

The potential revenues from RE plants are from two sources:

-

Feed-in Tariff (FiT) incentives and

-

Sales of energy.

The revenues vary with installed plant size and production levels, as summarised in Table 2

In Italy, a specific tariff (“Premium” Feed-in Tariff) is paid only for electricity generated by ground-mounted photovoltaic plants (PV). The tariff applies for a period of 20 years and we assume that the rate remains fixed. For investment in other RE sources (excluding PV), government support is given by an “all-inclusive” Feed-in Tariff, but this support is only available for plants with a nominal power of less than 1 MW, with the exception of on-shore wind, where the tariff is available for plants of up to 200 kW. This tariff is granted for a period of 15 years based on the amount of electricity fed into the grid, and we assume that the rate remains fixed. In addition, RES plants receive a number of “Green Certificates” equal to the product of their potential net electricity generation and a multiplication factor differentiated by RE source: a factor of 1 for wind and hydroelectric plants and 1.8 for “short-chain” biomass. This support is granted for 15 years, and the reference price is 74.72 €/MWh. The data on these tariffs, as indicated in our tables, are derived from data sets presented in government institution Web sites, particularly the site of GSE (Gestore dei Servizi Energetici), the state-owned company that promotes and supports renewable energy in Italy.

Revenues from the sale of electricity injected into the grid are calculated based on the minimum price guaranteed by the Italian Authority for Electricity and Gas for 2012. This income occurs only after the closure of the incentive period for plants that access the all-inclusive feed-in tariff, while in other cases for the full duration of the useful life of the plants. We assume the energy price inflation rate at 2.40 %.

Cost estimations

Costs can be summarized as:

-

Capital expenditure (capex);

-

Operating expenditure (opex); and

-

Taxes.

The costs vary with plant size, as summarised in Table 3:

Costs are linked to the system size. A full analysis of the entire range of potential system sizes is unfeasible; however, it has been hypothesized that capital costs remain constant within some size classes (Cucchiella et al. 2012; Department of Energy and Climate Change 2011), therefore we take the approach of considering such size classes in the cost calculations. In the photovoltaic and wind sectors, there is a 31 % reduction in cost for 50 kW–5 MW plants, and a 59 % reduction for <50 kW plants. We consider these two classes for these RE sources, and two other size ranges for photovoltaic and wind plants: for PV, 5–10 MW and >10 MW; for wind, 5–50 MW and >50 MW. In the biomass, there is a reduction of cost equal to 13 % for >50 MW plants compared to 5–50 MW ones. Smaller sized biomass plants (50 kW–5 MW and <50 kW) can be configured as Combined Heat and Power (CHP), therefore we also consider these classes. For hydro resource, we consider only three size classes: > 5 MW plants achieve cost reductions of 40 and 48 % compared to 1–5 MW and <1 MW ones.

Based on the available literature, we also hypothesise that operating costs remain constant within some size classes. While photovoltaic plants have the lowest values, biomass plants have costs much higher than other RE sources. We assume the inflation rate at 2 %. FiT incentives are considered lost funds and thus are not subject to direct taxation. The sale of energy, being instead classified as other income, is subject to taxes (average 33 %).

Technical parameters

The profitability of RES plants also depends on their production of electricity, which is in turn determined by three parameters:

-

Equivalent operating hours: a measure of the efficiency of the plant, given by the ratio between gross production and gross efficient power. The values, we identify are derived from those identified by the GSE (Gestore dei Servizi Energetici- Italian Electrical Services Authority): 1,650 h/y for photovoltaic resource, 1,900 h/y for wind power resource, 2,900 h/y for hydro resource and 3,550 h/y for biomass;

-

The size of the plants, which we have chosen as 10, 100 kW, 1, 5, 10 and 100 MW. These values are identified by two aspects: size classes characterized by different unitary cost and power range divided by different unitary incentive;

-

Annual decrease in system efficiency caused by deterioration of the RES plants. Based on published research, we assume a value of 0.70 % (Cucchiella and D’Adamo 2012b).

Considering all the combinations of the four RE sources (solar, wind, hydro and photovoltaic) and the six plant sizes (10, 100 kW, 1, 5, 10 and 100 MW), we obtain 24 possible investment cases.

Environmental considerations

In the national context, environmental pollution, premature mortality, lost workdays and overall healthcare costs could all be reduced by the substitution of fossil fuels with RE sources (Machol and Rizk 2013). GHG covers six categories of gases (CO2, CH4, N2O, HFC, PFC and SF6) and is measured in terms of CO2 equivalents (CO2eq), a metric used to compare the emissions from the various greenhouse gases based upon their global warming potential. The ranges of values of GHG/kWh for RE technologies are much lower than for fossil fuel sources. The International Panel on Climate Change provides figures for GHG emissions from electricity generation technologies based on the aggregated results of Lifecycle analysis (LCA), as published in the literature (Edenhofer et al. 2012). In Table 4 a further detailed analysis of GHG in the PV life cycle is presented, the analysis is based on the type of solar cells and the location where the system is installed (published in Cucchiella and D’Adamo 2012a).

The issues of water and land use have not yet been well analysed for the RE sector, but they are becoming increasingly significant (Arent et al. 2014). For a correct sustainability assessment model, it is necessary to consider the impact of RE development on these resources, in terms of both direct water and land usage and any transformations caused by direct and indirect releases of pollutants (Vinodh et al. 2014). Dai (2011) has examined the range of water-related impacts on future electricity production (Dai 2011). For wind and solar energy, the use of water is not essential; however, biomass and geothermal plants require water for cooling. In addition, hydro facilities have a direct impact on the river ecosystems both upstream and downstream of the dam. Overall for the RE sector, the largest use of land is associated with biomass crops. Energy-producing crops are grown in an intensive manner, with application of pesticides and fertilizers (Singh et al. 2011). Hand et al. (2012) have defined land use factors for renewable technologies as follows: for biopower, 25,800 GJ/km2; for hydropower 1,000 MW/km2; on-shore wind 5 MW/km2; utility-scale PV 50 MW/km2; distributed rooftop PV 0 MW/km2; and Geothermal 500 MW/km2.

NPV analysis: financial profitability of investments in RES

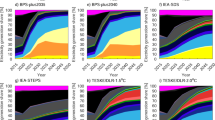

The choice of the most appropriate indicator for assessing the profitability of a potential investment depends on the aims of the project. If the decision-maker is a private operator, the goal is the maximization of profit and the methodology used is a financial analysis. In the case of a public decision-maker, the aim is the maximization of social welfare, and the appropriate methodology is economic analysis. The transition from a financial to an economic analysis requires transformation of market prices into accounting prices that avoid market imperfections, as well as the valuation of externalities, particularly the social cost of carbon (Cucchiella et al. 2013a). For financial evaluation of investments in renewable energy, the most widely used methodology is NPV (Golusin et al. 2012). Under this type of analysis, the investment project is defined as acceptable if the present value of all the cash inflows from the project is equal to or greater than the present value of all cash outflows. Given the assumptions and input data presented in the previous section, we calculate the NPV estimates as seen in Fig. 1. The analysis of the values demonstrates that all 24 case studies are profitable. It is not possible to define any one of the renewable resource as consistently more advantageous, since the result depends on the plant size considered, with different sources resulting in the highest NPV at different plant sizes: hydro at 10 kW plant size, wind at 100 kW, photovoltaic for 5 MW plants and biomass for 1, 10 and 100 MW plants.

Net Present Value (k€) per RE source and plant capacity

An important observation is that biomass plants are those that most often have the highest profitability, despite their greater capital and operating costs. This result derives from a mix of factors in our model, including: (i) the optimistic choice to consider that biomass plants operate on a “short-chain” feed and supply system; (ii) the high value of equivalent operating hours for biomass; and (iii) the structure of the Italian FiT scheme, in which biofuel plants receive the highest unit tariff value for 1 MW facilities, while for plants >1 MW the only incentive scheme that offers a higher unit value is the “Premium” feed-in tariff (available only for PV).

However, instead of the more optimistic assumption of a short-chain system, the model also permits consideration of long-chain biomass. In this case, the multiplicative factor for Green Certificates is 1.30, and there is a substantial decrease of NPV for 5, 10 and 100 MW biomass plants: these now achieve NPV values of 3,348, 15,048 and 203,401 k€. Given these considerations, the public decision-maker is in fact encouraging investment in biomass plants when the proposed power output is equal to 1, 10 and 100 MW. In these cases, biomass is favored by the fact that the value of incentives is 80 % higher than for wind and hydro plants, while the guaranteed minimum prices for sales of for energy from biomass are also almost always higher than for wind and hydro energy.

For photovoltaic plants, the Premium feed-in tariff is a very profitable incentive scheme; however; the reduced value of equivalent operating hours still determines a less profitable performance. Only in the case of plants of 5 MW dimension does photovoltaic have the highest NPV because for hydro and biomass resources, to difference to 1 MW ones, the minor convenient Green Certificates are applied. It is also important to highlight that in the case of biomass and hydro, the profit produced from a 1 MW plant is greater than the values obtained for certain larger plants, specifically of 5 MW size.

Wind facilities achieve excellent financial results in the 50–200 kW plant range due to economies of scale, which serve to reduce capital costs 58 % (see Table 3), and from an all-inclusive tariff that is greater than for other resources (recognized for wind plants with a capacity of up to 200 kw). However, when plant size reaches >1 MW, this situation no longer holds true. Although hydro and wind have the same unit value of subsidies and sale price of energy in the larger plants, hydro now achieves higher NPV: hydro plants consistently benefit from greater equivalent operating hours than wind plants, and at larger plant size, the lower capital costs of wind are no longer sufficient to balance out this advantage.

Finally, we compare all 24 investments by dividing the NPV of the plant by its relative size (Table 5). An important and useful observation is that the gain in NPV per unit of plant capacity is greatest in those plants that benefit from the all-inclusive feed-in tariff, and in biomass plants in general. In particular, the highest of all NPV values are achieved by 100 kW wind and biomass plants (respectively, 3.87 and 3.63 €/W), while the lowest values are observed for 5 MW hydro (0.51 €/W) and 100 MW wind (0.52 €/W).

Effects of real-world constraints on managerial decision-making

The previous section assesses the financial profitability of RE plants without taking into account the types of constraints that influence individual projects in the real world (for a consideration of the potential constraints see Ascough et al. 2008). To continue our analysis, we thus discuss a series of limiting factors, including indications of where the decision-maker can draw support by applying the NPV methodology.

-

a.

Availability of the energy sources

This is obviously the first consideration in real-world decision-making, since only those resources that are actually available in the local context can be considered for potential investment. In the current paper, we analyse only four RE sources, which is already a limitation. In the absence of one of these four sources, investors might be forced to opt for an available RES that is less profitable.

-

b.

The initial amount available for investment

A private decision-maker invests when two simultaneous conditions occur: first a need to expand the firm, and second the availability of the necessary financial capital. In the energy sector, the need to expand occurs when a specific energy demand develops (this case is analysed in the following c. bullet point), while the availability of capital depends in part on the nature of the investment (strategic or speculative). However, regardless of the strategic/speculative issue, if capital is restricted then the available options will change. If the available capital is for example, 350,000 € and the project envisioned is a 100 kW plant, it will not be possible to invest in the more expensive sources of hydro and biomass: in applying NPV analysis only the more economical choices of wind and solar can be considered.

-

c.

The quantity of energy required to meet a specific demand

When the energy produced is required for the investor’s own consumption, the need defines the size of the plant. For example, the annual need is 200 MWh, 100 kW wind and solar facilities will be insufficient, and the decision-maker’s analysis can consider only the choices of biofuel and hydro. On the other hand, if the decision-maker intends to sell the energy then the constraint of a specific need does not occur. It should also be noted that photovoltaic and wind sources are intermittent and in some cases the specific demand would then require a storage system, which could present a still further constraint.

-

d.

The changing cost of plants in function of market conditions

As indicated in the existing literature, the capacities of investment installed power, economies of scale and economies from ongoing learning all affect the costs of RE sources, and these vary over time (Cucchiella et al. 2012; Department of Energy and Climate Change 2011). The model can respond to these changes. For example, an increase or decrease of 20 % of capital expenditure due to changing economies of scale for 10 kW photovoltaic would determine that NPV for such a plant would become, respectively, 9 or 22 k€. Variations in the required capital expenditures would also reflect directly on the issue of initial capital constraints, discussed above.

-

e.

Changes in subsidies from incentive schemes

The role of incentive schemes is primary in RES investment. The unit value of tariffs is set by state authorities and is distinguished by RE source and size. The actions of policy makers in setting the incentives may impact in such a way as to favour one or another plant size of a particular source. As an example of the effects of changing incentives, a decrease or increase of 20 % in the subsidies for a 10 kW photovoltaic would determine that NPV becomes, respectively, 8 or 22 k€. In the next section, we provide a detailed analysis of the issues of subsidies, in which we see that the choices of different subsidies for RE sources, and plant sizes have a series of implications for both the investor and policy maker.

-

f.

Constraints due to the nature of the specific RE sources used

These constraints depend on local factors and the technical characteristics of the RE source. For example, in an earlier work (Cucchiella and D’Adamo 2012a), it emerged that the photovoltaic sector shows a greater return on investment in the regions of southern Italy than in northern regions, due to differences in annual irradiation. In modelling this example, if equivalent operating hours are increased or decreased by 400 h due less irradiation, the NPV becomes, respectively, 27 or 3 k€.

In a decision-making context the optimum choice is one that is simultaneously effective and efficient. The application of decision-making models with increasing levels of input data (more precise consideration of constraints) tends to achieve more reliable predictive results; however; this strategy can also lead to concurrent increases in planning costs. On the other hand, the use of simpler models is less costly but may omit information useful to improving the prediction. Thus in evaluating the individual cases that contribute to planning an optimal energy portfolio, it is necessary proceed by identifying only those constraints that require more thorough analysis (Cucchiella et al. 2012; Kontogianni et al. 2013).

The role of incentives

Many nations have determined to favour a more “green” energy mix, and the development of renewable energy is now heavily influenced by incentive policies (Shen et al. 2010). The focus of the literature tends to be on government choice of the incentive schemes most appropriate for achievement of the intended objectives (Zhou et al. 2011) and on reviews of the different schemes and their results (Cansino et al. 2010). This objective of this section is to provide a detailed analysis that quantifies the weight of subsidies in the revenues from potential investment in the specific plant projects (Table 6).

In applying our model, we observe that in a scenario without subsidies all the RE sources considered would have a negative NPV, regardless of plant size. This implies that in a context without subsidies, no private decision-maker would invest in RES. Of the sources considered, biomass plants would in particular have the worst financial returns, due to higher expenditures.

Our analysis permits us to compare the effects of the Premium feed-in tariff (only for photovoltaic) to those of Green Certificates (for 1 MW wind, 5, 10 and 100 MW wind, hydro and biomass). The analysis reveals that the FiT subsidies represent a 59 to 65 % share in revenues from photovoltaic plants, while the weight of subsidies decreases to 17–20 % for wind and hydro facilities and to 13–14 % for biomass. Thus current Italian legislature encourages the development of photovoltaic source for these larger size classes: the unit value of the Premium feed-in tariff (PV only) is higher than for the other incentive schemes.

Considering the all-inclusive feed-in tariff (applicable to 10, 100 kW wind, hydro and biomass, 1 MW hydro and biomass), the model does not permit a direct comparison with the Premium feed-in tariff since these plants also achieve revenue from the sale of energy. For such a comparison, we must reduce the percentage obtained in Table 6 in function of the numerical relation between the sale of energy and the subsidies (derived from Table 3). Such an analysis demonstrates: (i) that the “revised value” of the all-inclusive feed-in tariff is greater for wind plants (67 %) than for solar ones; (ii) that biomass facilities have a revised value of all-inclusive tariff amounting to a 48 % share (constant for 10, 100 and 1 MW plants); (iii) 10 kW hydro plants gather the bulk of their revenues (86 %) from the sale of energy, while such sales revenues decrease to 55 and 44 % for larger 100 and 1 MW plants, in favour of increasing income from subsidies.

Finally, the results highlight that the percentage of subsidies compared to other revenues remains the same for photovoltaic and biomass plants regardless of the potential project size considered. The same happens for those hydro and wind facilities eligible for Green Certificates. The government’s decision to tailor incentive schemes relative to several classes of power has resulted in higher tariff unit values for plants of small and medium size. This choice is important, particularly given the current economic situation where the proper use of public funds is necessary. The tariff structure in effect favours investment in smaller plants by decision-makers such as families, condominium corporations, firms and local public administrations, with potentially lower capital resources, as opposed to offering further funds to speculative investors that may already have greater resources for larger projects.

Sensitivity analyses

In this section, a sensitivity analysis is presented to show how different values of the independent variables (costs and revenues) impact on the estimation of the financial indexes as shown in the base scenario of Fig. 1. Previous qualitative and quantitative analyses (Chatzimouratidis and Pilavachi 2009; Cucchiella and D’Adamo 2012a; Vikash and Atul 2010) have identified the critical variables in energy plant projects as being: FiT incentives, sales of energy, selling price of electricity, initial investment costs, operating costs and equivalent operating hours. We divide the sensitivity analysis in two sections: first for the economic variables, then the technical variables.

Variation of the economic variables

We develop two positive and two negative scenarios with respective increases/decreases in costs and revenues: of 10 % and by 20 %. The analysis demonstrates that in almost all RE and plant-size scenarios the profitability of the investment is verified.

As shown in Table 7, there are only five cases where the NPV has a negative value, all of which occur in cases of 5 MW plant sizes. More specifically, negative results are obtained for 5 MW biomass plants with a pessimistic 20 % variation of all the variables (FiT incentives, selling price, initial investment cost and operating cost). A negative NPV is also observed for a 5 MW hydro plant in the case of a 20 % increase in investment cost. The sensitivity analysis shows that the financial performance of biomass projects is in general higher compared with those of other types of RE plants. In this comparison of biomass and other sources, some important observations are as follows:

-

In all scenarios where there are optimistic variations of critical variables, biomass is the best solution for all plant sizes from 10 to 100 MW;

-

For a 100 kW plant, biomass is the best source in all scenarios where there are optimistic variations of variables, except for positive variation in the selling price.

-

For a 5 MW plant under the optimistic scenarios of all four variables, the higher NPV of biomass requires that the baseline choice (which favoured the solar energy source) must be changed to a biomass choice, under the hypotheses that costs are decreased of 20 % and revenues of the project are increased of the same 20 %;

-

For 10 kW plants the best NPV under the base scenario is achieved with hydro, but with a 20 % FiT incentive increase the best source becomes biomass;

-

For 1 MW plants the best NPV under the base scenario is achieved with biomass, but with a 20 % FiT incentive increase the best source becomes hydro;

The sensitivity analysis results, in keeping with previous studies (Cucchiella and D’Adamo 2012a), indicate that the impact of operating costs and selling price variables on NPV is marginal compared to that of investment costs and FiT incentives (except for 5 MW hydro projects). Thus, observing changing economies of scale and learning, government could define FiT subsidies in order to incentivize the development of one renewable resource rather than another, according to the objectives of its long-term energy policy (Zhang et al. 2011).

Variation of the technical variable

We now carry out the sensitivity analysis for the effect of equivalent operating hours. This variable depends primarily on specific local conditions and on the technical nature of the RE source. We hypothesise two positive and two negative scenarios, with respective increases/decreases of 200 and 400 h.

As shown in Table 8, the analysis verifies the profitability of investment in almost all the scenarios (96.9 %). The NPV values are negative in only three cases: 100 MW wind and 5 MW hydro and biomass, under the most pessimistic scenarios. This result is due to two effects: the incentive mechanism and the investment costs. In particular, when the investments are supported by Green Certificates and not by Feed-In Tariff it is possible to gain a lower profitability. This effect is not offset by the scale economy that can be recorded on investment costs.

With respect to the base scenario, the analysis reveals the following useful information:

-

For facilities between 10 and 100 MW in all the optimistic scenarios, the original best base choice for biomass, it is always confirmed;

-

For some cases of 10 kW facilities, wind achieves an NPV greater than the base choice of hydro;

-

For 1 MW facilities the financial returns for hydro are better than for the base choice of biomass;

-

For some cases of 5 MW facilities, wind and biomass would achieve a higher NPV than the base choice of photovoltaic; and

-

For 100 kW facilities, wind and hydro can sometimes achieve higher profitability than the base choice of wind resource.

Table 8 and 7 also identify the positive and negative scenarios that stimulate the maximum and minimum NPV for the various RE sources and plant sizes, as well as the variable that has the greatest impact on NPV:

-

For PV systems, the most significant NPV variations are due to variation of equivalent operating hours: for PV, NPV is more sensitive to operating hours than to any other potential variable;

-

For wind power facilities of 10 and 100 kW size, the most significant NPV variations are due to variation in the Feed-in tariff variable: for these smaller sizes, NPV is more sensitive to incentives than to any other potential variable;

-

Biomass facilities also have a strong sensitivity to the feed-in tariff variable. Especially for plants up to 1 MW, NPV variation is much more sensitive to FiT than to equivalent operating hours; and

-

As seen for biomass, hydro facilities up to 1 MW again have a strong sensitivity to FiT, while for the other dimensions there are varying results. For 5 MW plants the maximum and minimum, NPVs are observed with variation in investment costs, for 10 MW the extremes are observed with variation in FiT, for 100 MW plants with varying equivalent operating hours.

Finally, Table 9 provides a form of sensitivity comparison to the economic and technical variables. It presents the average NPV for the six potential facility sizes analysed under the most optimistic scenarios for each variable (20 % FIT incentive increase, 20 % investment cost decrease, 400 h equivalent operating hours increase). We observe that equivalent operating hours tends to have the most significant impacts on NPV.

Environmental impact analysis and policy considerations

The results of the previous sections have shown that investing in renewable energy is profitable, and have demonstrated a methodology for choosing among various options in developing an energy portfolio. In the final part of the paper, we analyse the environmental benefits resulting from the use of renewable energy plants and propose some socio-economic policy considerations.

Environmental impact analysis

The market for renewable energy technologies has continued to grow, showing substantial potential to contribute to sustainable development and also achieve significant environmental benefits. Renewable energy is typically environmentally friendly, especially with regard to air emissions. In this section, the emissions and pollutants released from renewable plants are compared to those produced from fossil fuels. In order to estimate the reduction of pollutant gases, we consider the Italian 2011 national energy mix regarding the portion composed exclusively of fossil fuels (46 % natural gas, 43 % oil and 11 % coal). Applying the averages values for GHG emissions per fuel source (Table 4), and excluding renewable energy and imports, the total of Italian emissions is equal to 771 g of CO2eq per unit of electricity generated (610*0.46 + 840*0.43 + 1182*0.11 = 771). Referring again to Table 4, we observe that average emissions from renewable sources are, respectively 22, 41.5, 48.5 and 189 gCO2eq/kWh for hydro, wind, solar and biomass. These emissions are low compared to those from fossil fuel plants. We can in fact calculate the savings: for example, a hydro plant allows a saving per energy unit of 771−22 = 749 gCO2eq/kWh. As seen in Table 10, the absolute levels of savings are related to the plant size and its operating hours. For example, a 10 kW wind plant, which generates 19,000 kWh annually, allows a saving estimated at 14 tCO2eq and a 10 kW biomass plant (which has an output of 35,500 kWh) a saving of 21 tCO2eq.

In Table 4, we have observed that biomass plants have an average level of emissions per unit of electricity that is higher than for other renewable sources. However, since the total annual GHG savings are linked to the number of operating hours (Table 8), biomass plants actually achieve total annual environmental performances that are “better” than from wind and solar power. Only hydro exceeds the performances of biomass plants: for these two sources the difference in operating hours is less marked, thus hydro achieves a greater reduction in emissions (Table 10).

We conduct a further sensitivity analysis to estimate the reductions of emissions under different scenarios. The reference values are the extremes (min and max) identified in Table 4 and Table 8, with respect to the lifecycle GHG emissions (Table 11) and the equivalent operating hours (Table 12).

The purpose of the analysis is not to determine, whether one renewable source is better than the others from an environmental perspective. In fact, it is not possible to identify such conclusions, since the various scenarios are not associated with probability values, and we cannot define which of them are most likely. However, the policy-maker could use such analyses to carry out dynamic assessments that further strengthen the results of the other modelling, particularly by quantifying the reaction of emission reductions to variations in plant energy production capacities and operating hours. The sensitivity analysis in regards to GHG emissions in fact highlights that under varying contexts, biomass can achieve very significant changes compared to the baseline scenario, while this does not happen with the other renewable sources examined.

Policy considerations

Our comparisons of financial and environmental performance allow a number of socio-economic policy considerations regarding the use of renewable energy sources:

-

The use of renewable energy protects the atmosphere and produces climatic improvements, but when considering public policy on incentives, it is necessary to conduct more precise analyses of the true environmental benefits. Biomass now provides the best performance in terms of financial returns, but it also tends to be the RE source that has the highest level of atmospheric emissions per unit of installed capacity.

-

For policies intended to promote the development of “distributed generation” systems, the attractiveness of small installations is crucial. Incentive structures should support choices to construct small installations, thus promoting private-citizen investment in self-sufficient energy. Incentives should also be designed to promote investment in larger systems and not only for end user, for example, on the part of businesses, industries and public administrations.

-

Incentive schemes should facilitate the development of “industrial-level” supply and distribution chains. The resulting competition between firms can push improvements in quality of service and stimulate more affordable prices. This approach can eventually enable RES industry to gain independence in the national energy market even in the absence of incentive structures, and in fact this scenario is now developing in many countries as the result of long-term policies.

-

National energy policies must be integrated with local ones. In this way each territory provides supports that are designed to maximize the social benefit for its community, and thus for the nation overall.

Conclusions and future directions

The paper has demonstrated that investments in renewable energy permit reliable and healthy long-term financial returns with low levels of risk, and in fact guarantees of future revenues are determined by subsidies. The trend for the future is that such subsidies will be reduced; however; the effects will be balanced by considerable reductions in expenditure costs, determined both by the level of installed power in each investment and by the increasing numbers of firms entering the sector, thus favouring competitiveness. In the current paper, we have relied on existing literature and market reports to define the values applied in our models; however, a further interesting approach would be to develop predictive models that define the probability of an outcome. In this way, it would be possible to provide detailed analyses of one or more alternative scenarios other those developed from the base observations.

In order to achieve efficient and effective incentive schemes, the policy-maker must necessarily evaluate several factors: the levels of technology costs, the types of investors, environmental impacts and the benefits to the whole economic chain. Many variables are subject to change, and thus it is important to continuously monitor the financial performance of renewable sources, both in mature markets and in the case of those undergoing rapid growth. Sustainability will only sustainable if it is also profitable.

The results of the NPV analysis feed into the decision-making process. The paper highlights the relevance of properly sized facilities for the optimization of the investment. Depending on size, any one of the different sources analysed (biomass, hydro, photovoltaic and wind) could be the more profitable project, while the limits on size depends on the potential presence of constraints. Thus an investor must complete an accurate definition of the financial performance of the individual resources preparatory to defining their optimal energy portfolio. At the level of the local context, the geographic location and specific sites for the generating plants play a major role in their sustainability. With such context known, the investor can define the technical, environmental and economic variables with a high degree of precision.

The financial analysis has highlighted that the gain per unit of planned capacity is greatest in facilities that benefit from Italy’s “all-inclusive” Feed-in tariff and in biomass plants in general. In a base scenario closely resembling the current context, the plants with the greatest return per unit of capacity (between 3.3 and 3.9 €/W) are 100 kW wind, 10 kW hydro, 100 kW, 1 and 100 MW biomass, while all 5 MW plants and several wind plants present low values, in the range of 0.5–1.2 €/W.

The sustainability analysis highlights that the instances of positive financial and environmental assessments do not necessarily coincide. In fact biomass facilities not only achieve greater profitability, but also cause greater pollution per unit of energy than do other renewable sources (hydro, wind and photovoltaic produce average values of 22–49 gCO2eq/kWh, while biomass produces 189 gCO2eq/kWh). However, the total annual energy units produced by biomass and hydro facilities are greater than the totals from wind and solar plants of the same dimension, due to higher values of equivalent operating hours, and thus result in corresponding increases in total GHG savings, even with the use of “dirtier” biomass. (For the example of the smallest plant size, of 10 kW, biomass and hydro provide reductions of greenhouse gases of 21–22 tCO2eq, while wind and photovoltaic provide total annual reductions of only 12–14 tCO2eq, compared to fossil fuels.)

In conclusion, our analyses support the general argument that the renewable energy sector is indeed strategic for a sustainable future: renewable sources currently have valid financial, environmental and social roles and will continue to fill important roles under changing conditions.

Abbreviations

- AiFiT :

-

All-inclusive feed-in tariff for energy from Bi,Hy,Wi (€/kWh)

- Bi :

-

Biomass source

- Capex :

-

Total capital expenditure (€)

- capex U :

-

Net capital expenditure per kW (€/kW)

- C in :

-

Capacity of the installed facility (kW)

- dE f :

-

Annual decrease in plant efficiency (%)

- DT (PV) :

-

State duties on Net metered revenue from PV (€)

- DT (Bi,Hy,Wi) :

-

State duties on Net metered revenue from Bi,Hy,Wi (€)

- DT U :

-

Unit duty for Net metered kW (%)

- E f :

-

Embodied energy by RE facility (kWh)

- FiP CE :

-

Premium Feed-in Tariff per kW from PV (€)

- FiP PV :

-

Total Premium Feed-in Tariff for PV(€)

- FiT (Bi,Hy,Wi) :

-

Feed-in tariff for Bi, Hy, Wi (€)

- h eq :

-

Equivalent hours of operation (h)

- Hy :

-

Hydro source

- Inf :

-

Inflation rate (%)

- inf el :

-

Energy inflation rate (%)

- K :

-

Constant for Green Certificate

- L CS :

-

Loan capital share (%)

- L IS :

-

Loan interest share (%)

- N R :

-

Time for plant construction (years)

- opex :

-

Total operating expenditure (€)

- opex U :

-

Operating expenditure per kW (€/kW)

- p GC :

-

Price of Green Certificate (€/kWh)

- PV :

-

Photovoltaic source

- r :

-

Opportunity cost (%)

- SP el (Bi,Hy,Wi) :

-

Sales of electricity from Bi, Hy, Wi (€)

- SP el (PV) :

-

Sales of electricity from PV (€)

- SPu el :

-

Sale price per kWh of electrical energy (€/kWh)

- Wi :

-

Wind source

References

Arent D, Plessa J, Mai T, Wiser R, Hand M, Baldwin S, Heath G, Macknick J, Bazilian M, Schlosser A, Denholm P (2014) Implications of high renewable electricity penetration in the US for water use, greenhouse gas emissions, land-use, and materials supply. Applied Energy 123:368–377. doi:10.1016/j.apenergy.2013.12.022

Ascough JC, Maier HR, Ravalico JK, Strudley MW (2008) Future research challenges for incorporation of uncertainty in environmental and ecological decision-making. Ecol Model 219:383–399. doi:10.1016/j.ecolmodel.2008.07.015

Bader H-P, Scheidegger R, Real M (2005) Global renewable energies: a dynamic study of implementation time, greenhouse gas emissions and financial needs. Clean Technol Environ Policy 8:159–173. doi:10.1007/s10098-005-0015-6

Banal-Estañol A, Micola AR (2009) Composition of electricity generation portfolios pivotal dynamics, and market prices. Manage Sci 55:1813–1831. doi:10.1287/mnsc.1090.1067

Barnham K, Knorr K, Mazzer M (2013) Benefits of photovoltaic power in supplying national electricity demand. Energy Policy 54:385–390. doi:10.1016/j.enpol.2012.10.077

Cansino JM, Pablo-Romero MdP, Roman R, Yniguez R (2010) Tax incentives to promote green electricity: An overview of EU-27 countries. Energy Policy 38:6000–6008

Chatzimouratidis AI, Pilavachi PA (2009) Sensitivity analysis of technological, economic and sustainability evaluation of power plants using the analytic hierarchy process. Energy Policy 37:788–798. doi:10.1016/j.enpol.2008.11.021

Chen Y-T, Chang D-S, Chen C-Y, Chen C-C (2011) The policy impact on clean technology diffusion. Clean Technol Environ Policy 14:699–708. doi:10.1007/s10098-011-0435-4

Cucchiella F, D’Adamo I (2012a) Feasibility study of developing photovoltaic power projects in Italy: an integrated approach. Renew Sustain Energy Rev 16:1562–1576. doi:10.1016/j.rser.2011.11.020

Cucchiella F, D’Adamo I (2012b) Estimation of the energetic and environmental impacts of a roof-mounted building-integrated photovoltaic systems. Renew Sustain Energy Rev 16:5245–5259. doi:10.1016/j.rser.2012.04.034

Cucchiella F, D’Adamo I (2013) Issue on supply chain of renewable energy. Energy Convers Manag 76:774–780. doi:10.1016/j.enconman.2013.07.081

Cucchiella F, D’Adamo I, Gastaldi M (2012) Modeling optimal investments with portfolio analysis in electricity markets energy education science and technology part A. Energy Sci Res 30:673–692

Cucchiella F, D’Adamo I, Gastaldi M (2013a) A multi-objective optimization strategy for energy plants in Italy. Sci Total Environ 443:955–964. doi:10.1016/j.scitotenv.2012.11.008

Cucchiella F, D’Adamo I, Lenny Koh SC (2013b) Environmental and economic analysis of building integrated photovoltaic systems in Italian regions. J Clean Prod doi:10.1016/j.jclepro.2013.10.043

Dai A (2011) Drought under global warming: a review. Wiley Interdiscip Rev: Clim Change 2:45–65

Department of Energy and Climate Change (2011) Review of the generation costs and deployment potential of renewable electricity technologies in the UK available at decc.gov.uk

Edenhofer O, Pichs Madruga R, Sokona Y (eds.) (2012) Renewable energy sources and climate change mitigation: Special report of the intergovernmental panel on climate change. Cambridge University Press,Cambridge

Fokaides P, Miltiadous I-C, Neophytou MA, Spyridou L-P (2014) Promotion of wind energy in isolated energy systems: the case of the Orites wind farm. Clean Technol Environ Policy 16:477–488. doi:10.1007/s10098-013-0642-2

Golusin M, Ostojic A, Latinovic S, Jandric M, Munitlak Ivanovic O (2012) Review of the economic viability of investing and exploiting biogas electricity plant—Case study Vizelj, Serbia. Renew Sustain Energy Reviews 16:1127–1134

Hand M, Baldwin S, DeMeo E, Reilly J, Mai T, Arent D, Porro G, Meshek M, Sandor D(eds.) (2012) Renewable Electricity Futures Study. Vol 4 NREL/TP-6A20-52409. National Renewable Energy Laboratory, Golden

Kontogianni A, Tourkolias C, Skourtos M (2013) Renewables portfolio, individual preferences and social values towards RES technologies. Energy Policy 55:467–476. doi:10.1016/j.enpol.2012.12.033

Krozer Y (2013) Cost and benefit of renewable energy in the European Union. Renew Energy 50:68–73. doi:10.1016/j.renene.2012.06.014

Machol B, Rizk S (2013) Economic value of US fossil fuel electricity health impacts. Environ Int 52:75–80. doi:10.1016/j.envint.2012.03.003

Manzano-Agugliaro F, Alcayde A, Montoya FG, Zapata-Sierra A, Gil C (2013) Scientific production of renewable energies worldwide: an overview. Renew Sustain Energy Rev 18:134–143. doi:10.1016/j.rser.2012.10.020

Masini A, Menichetti E (2013) Investment decisions in the renewable energy sector: an analysis of non-financial drivers. Technol Forecast Soc 80:510–524. doi:10.1016/j.techfore.2012.08.003

Munoz JI, de Sanchez la Nieta AA, Contreras J, Bernal-Agustın JL (2009) Optimal investment portfolio in renewable energy: The Spanish case. Energy Policy 37:5273–5284

Panepinto D, Viggiano F, Genon G (2014) The potential of biomass supply for energetic utilization in a small Italian region: basilicata. Clean Technol Environ Policy 16:833–845. doi:10.1007/s10098-013-0675-6

Planas E, Andreu J, Gil-de-Muro A, Kortabarria I, Martínez de Alegría I (2013) General aspects, hierarchical controls and droop methods in microgrids: a review renewable and sustainable. Energy Reviews 17:147–159. doi:10.1016/j.rser.2012.09.032

Ranjan KR, Kaushik SC (2014) Exergy analysis of the active solar distillation systems integrated with solar ponds. Clean Technol Environ Policy 16:791–805. doi:10.1007/s10098-013-0669-4

Reza B, Sadiq R, Hewage K (2013) Emergy-based life cycle assessment (Em-LCA) for sustainability appraisal of infrastructure systems: a case study on paved roads. Clean Technol Environ Policy 16:251–266. doi:10.1007/s10098-013-0615-5

Shen YC, Lin G, Li TR, Yuan KP, Benjamin JC (2010) An assessment of exploiting renewable energy sources with concerns of policy and technology. Energy Policy 38:4604–4616

Singh A, Nigam PS, Murphy JD (2011) Renewable fuels from algae: An answer to debatable land based fuels. Bioresource Technol 102:10–16. doi:10.1016/j.biortech.2010.06.032

Strbac G, Ramsay C, Pudjianto D (2008) Microgrids and virtual power plants: concepts to support the integration of distributed energy resources. Proceedings of the Institution of mechanical engineers Part A. J Power Energy 222:731–741. doi:10.1243/09576509jpe556

Vanhoucke M, Demeulemeester E, Herroelen W (2001) On maximizing the net present value of a project under renewable resource constraints. Manage Sci 47:1113–1121. doi:10.1287/mnsc.47.8.1113.10226

Verma YP, Kumar A (2013) Potential impacts of emission concerned policies on power system operation with renewable energy sources. Int J Electr Power Energy Syst 44:520–529. doi:10.1016/j.ijepes.2012.03.053

Vikash R, Atul R (2010) Optimization and sensitivity analysis of a PV/Wind/Diesel hybrid system for a rural community in the pacific. Appl Solar Energy 46:152–156

Vinodh S, Jayakrishna K, Kumar V, Dutta R (2014) Development of decision support system for sustainability evaluation: a case study. Clean Technol Environ Policy 16:163–174

Zhang H, Li L, Cao J, Zhao M, Wu Q (2011) Comparison of renewable energy policy evolution among the BRICs. Renew Sustain Energy Rev 15:4904–4909

Zhou Y, Wanga L, McCalley JD (2011) Designing effective and efficient incentive policies for renewable energy in generation expansion planning. Appl Energy 88:2201–2209

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Cucchiella, F., D’Adamo, I. & Gastaldi, M. Financial analysis for investment and policy decisions in the renewable energy sector. Clean Techn Environ Policy 17, 887–904 (2015). https://doi.org/10.1007/s10098-014-0839-z

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10098-014-0839-z