Abstract

Two platforms compete for heterogeneous firms and consumers. Platforms are allowed to discriminate prices on the consumers’ side according to their past purchase behaviour. The findings of the paper depend on two dimensions: the relative cross-side externalities and the consumer discounting relative to platform discounting. Price competition is strengthened in the poaching phase compared to the case where a uniform price is charged in both sides, whereas the early price competition is relaxed if firms exhibit weaker externalities than consumers and if the latter discount sufficiently the future. The overall effect on inter-temporal profits of platforms is negative, but consumers might be harmed by BBPD when they discount sufficiently the future. Finally, depending on consumers’ discounting, total welfare may increase or decrease going from the uniform pricing to the discriminatory pricing.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Customer recognition often leads firms to charge old and new consumers with different prices. Taylor (2003) reports how this price discrimination based on past purchases, called behaviour-based price discrimination (BBPD), is very common in subscription markets. In these industries, the non-anonymity of subscriptions gives to firms information on the identity of current subscribers, so that there is scope for proposing low introductory prices to whom did not buy its product in the past.

Discounts take different forms such as low introductory prices, trial memberships and free installations. As mentioned in Caillaud and De Nijs (2014), a new subscriber for three months to the French newspaper “Le Monde”, pays 50 euros whereas a previous customer is charged 131.30 euros. Similar offers are the free trial memberships to software applications as well as online contents platforms such as Spotify and Amazon.Footnote 1 Moreover, first subscriptions to credit cardsFootnote 2 and TVs/internet services are often offered for free.

All these services have the common feature that subscribers are not the only customers, as business is also made on merchants (credit cards), advertisers (media) and content providers (online platforms). In economic jargon, these markets are run by two-sided platforms allowing the interaction between different groups of customers linked to each other by cross-group externalities. Think for example to credit cards. A cardholder’s utility is increasing in the number of shops where she can use it and merchants are in turn more willing to pay to hold a card reader as the number of consumers increases.

Because of the presence of the externalities, one of the distinctive features of these markets is the pricing rule, which is different from the one applying in a one-sided framework (i.e., market without externalities). Going back to the example of credit cards, the subscription fee charged to the cardholders affects not only the demand in this group, but also the willingness to pay of merchants to hold an electronic point of sale. This is the basic reason for the observation of a cross-group price discrimination, as the price charged to each group depends on the cross externalities, so that a group whose participation entails a large participation of the other group will be charged less. This is the so-called Divide and Conquer strategy, according to which the group having weaker externalities becomes a loss leader, as attracting it is necessary to make higher profits on the group with stronger externalities. According to this discussion, in many subscription markets two kinds of strategies are used by competing platforms: the mentioned cross-group price discrimination typical of a two-sided market and the within-group BBPD on subscribers’ side.Footnote 3

This paper provides a two-sided market analysis investigating the effects of within-group BBPD on prices, surplus distribution and welfare. The aim of the analysis is to tackle the following questions: (i) “ What is the impact of within-group BBPD in two-sided markets?” and (ii) “ What is the role of the relative discounting of subscribers in relation to the one of platforms?”. The paper demonstrates that within-group BBPD has a negative effect on platforms’ profits, does not affect the firms’ side, and benefits consumer only if they do not discount the future too much. On the one hand, platforms compete strongly to attract switchers and this always makes them worse-off when they can discriminate prices. On the other hand, when consumers are strongly interested in meeting firms, they become the profit-making group and BBPD results to be a further future alternative to attract consumers. As a consequence, early competition in consumers’ side is mitigated and, if consumers discount factor is sufficiently low, this may result in a lower consumer surplus in relation to uniform pricing. In terms of welfare, the loss of the platforms is compensated by the gain of consumers only when the latter give much weight on future utility, so that they really care about future possibilities of switching.

These findings result from a two-period model in which two platforms compete for subscribers and firms, located in a Hotelling line of length one. After a first round of subscription decisions, platforms are able to recognize first-period subscribers and are allowed to discriminate between old and new subscribers. This behaviour-based discrimination is allowed in the consumers’ side only. In the examples motivating the paper this type of discrimination is never used in the firms’ side. As a matter of fact, other types of price discrimination might be used by platforms on the firms’ side: in the media market, advertisers usually compete for a limited number of spaces through auctions, whereas per-click royalties are paid to content providers (majors/record labels/publishers) by online platforms. For the sake of simplicity, the model proposed here neglects these discriminating policies, by focusing on a uniform price on the firms’ side.

In terms of second-period prices, competition for consumers is strengthened compared to the case in which a uniform price is charged in both sides of the market, whereas firms are indifferent between the BBPD and the uniform-pricing regime. Indeed, both platforms invade rival turf putting pressure on subscription prices. As a result, they steal each other the same number of consumers, so that their total number is the same that would have been attracted under uniform pricing, with the consequence of an identical willingness to pay of firms.

Consumers are assumed to discount their future utility, with the usual parameter \(\delta \) representing the relative weight that a subscriber gives to second-period in relation to first-period utility. Differently, platforms are assumed not to discount the future. This allows to reinterpret the parameter \(\delta \) as the relative discounting between platforms in relation to consumers. The assumption of different discounting is common in several papers studying dynamic pricing, e.g. Villas-Boas (1999), Villas-Boas (2006), Chen and Zhang (2009), Zhang (2011), Carroni (2016), Rhee and Thomadsen (2017) and it is grounded on two arguments. On the one hand, as pointed out by Rhee and Thomadsen (2017), “research has shown that consumers generally discount future consumption utility at greater rates than are earned on capital (e.g., Andreoni and Sprenger 2012; Malkoc and Zauberman 2006)”, which is consistent with consumers discounting the future more than platforms. On the other hand, many papers in one-sided BBPDFootnote 4 show how consumers discounting has an impact on the first-period competition, as the anticipation of future discounted prices induces the indifferent first-period consumer to respond more weakly to first-period prices, so to mitigate early price competition. Therefore, considering different discounting allows to isolate this first period “elasticity effect” that BBPD brings about.

In the present work, the inter-temporal effect introduced by consumers’ perception of future switching opportunities is enriched by the interaction between the Divide and Conquer in the early and the BBPD in the late price competition. In particular, if subscribers exhibit stronger externalities than firms, the optimal Divide and Conquer will entail a cross-subsidization from the consumers’ to the firms’ side, with consumers becoming the profit-making group. As BBPD offers the platforms a new opportunity to enlarge their market lately, this reduces early competition in the subscribers’ side so to fully exploit the positive impact of late poaching on early competition. This unambiguously reduces consumer surplus in the first period and may reduce it overall if consumers discount sufficiently future utility. Differently, if platforms “divide” on the subscribers’ side to “conquer” the firms’ side, offering a very low price to the former and making profits on the latter, BBPD may increase first-period competition. In particular, unless consumers discount the future very little, so that the demand is not too “inelastic”, within-group BBPD makes platforms more aggressive in the early competition, so that future switching becomes a threat of loosing consumers (the key group to make profits on the other side) rather than a future opportunity of attracting new ones. In this case, BBPD benefits consumers, as they enjoy lower prices in both periods when they put no weight on future utility or, if they do it, the surplus improvement in the switching phase associated to BBPD prevails over the detriment given by higher first-period prices.

Related literature This paper is naturally linked to the two-sided market literature, initially formalized by Rochet and Tirole (2003), Armstrong (2006) and Caillaud and Jullien (2003). The main result around which this literature is built on is the cross-group price discrimination, which follows the concept of Divide and Conquer firstly proposed by Caillaud and Jullien (2003). In order to develop a business, a platform offers a low (often below-cost) price to one side of the market and thus restores its losses by charging a relatively high price to the other side. As in Rochet and Tirole (2003) and Armstrong (2006), the present paper proposes a Hotelling model, to capture the idea that customers exhibit heterogeneous preferences over rival platforms, which are then expressed by locations on the Hotelling line. An alternative way to model two-sided markets is the one proposed by Gabszewicz and Wauthy (2014) and Roger (2017), among others, which interpret two-sided market as vertically differentiated with consumers heterogeneous in terms of the strength of the externalities rather in terms of locations. Moreover, the present model focuses on the simplest case in which platforms charge only a fee independent of the number of interactions with the other sideFootnote 5 and customers can join at most one platform.Footnote 6

On the other side, the paper is strongly related with BBPD literature. In particular, the model builts on Fudenberg and Tirole (2000), who provide a Hotelling model played twice, allowing firms to know whether a customer in the second period is new or old. In different setups, the literature of BBPD mainly agrees on the fact that customer’s recognition harms firms compared to a situation in which the targeted pricing is not possible. Even if a firm alone prefers to obtain the information and so use it to benefit from a surplus extraction, if both get it, then a market stealing effect tends to prevail.Footnote 7

In recent years, first investigations of within-group price discrimination have been presented, both from an empirical and a theoretical viewpoint. Gil and Riera-Crichton (2011) and Angelucci et al. (2013) provide empirical analysis respectively on Spanish TV and French newspaper industries. The first paper is mainly focused on the relationship between competition and price discrimination, while the second one studies how advertisement revenues affect price discrimination on the readers’ side. Both competition and advertisement revenues are found to have a negative impact on the likelihood of medias to use price discrimination. From a theoretical point of view, two papers are close to the present one. Carroni (2017) provides an industry-specific model of BBPD that suits the case of media markets taking into account the negative externality that advertisers create on consumers (nuisance). In that case, within-group BBPD intensifies competition in the firms’ side, as some firms single-home: this may reduce consumers’ surplus and total welfare. Liu and Serfes (2013) allow platforms to engage in perfect within-group price discrimination. Their main finding is that discrimination might be a tool to neutralize cross-group externalities with a positive effect on prices and platforms’ profits. The main difference with the present paper is that they analyze the case of perfect price discrimination rather than discrimination based on past purchase behaviour, in which also an inter-temporal trade-off plays an important role in platforms’ decisions.

The remainder of the paper is organized as follows. Next section introduces the model, which is analyzed in Sect. 3. Section 4 provides a welfare analysis and, finally, Sect. 5 concludes.

2 The model

Two competing platforms \(j=A,B\) aim to sell a service to two different groups of customers, subscribers and firms.Footnote 8 Both subscribers and firms are assumed to be uniformly distributed along a unit segment. In turn, platforms’ locations are kept fixed at the end-points of this segment, i.e., platform A’s location is \(l^{A}=0\), while platform B is located at \(l^{B}=1\).

A side-i agent enjoys some utility u from joining a platform, faces a transportation cost normalized to 1 per unit of distance coveredFootnote 9 and receives a benefit measured by the parameter \(\alpha _{i}\in (0,1)\) for each side-i agent joining the same platform. According to these assumptions, the utility of a side-i agent located at x who joins platform j will be:

and \(n_{i'}^{j}\) is the total number of the other side’s agents joining platform j. Platforms set prices in order to maximize profits, facing a unitary cost normalized to 0 to put “on board” each side of the market. Platforms and firms do not discount the future (discount factor normalized to 1), whereas consumers give value \(\delta \in [0,1]\) to future utilities.Footnote 10 The platforms’ profits are simply given by the sum of the products between the price charged to each group and the number of joiners belonging to the same group. Thus, the profit of platform j when charging prices \(p_{i}^{j}\) to each side i is indicated in equation by the following:

Three main assumptions are used throughout the paper. First, the utility u is big enough so that every agent prefers to join at least one platform instead of joining none (Full Market Coverage). Moreover, each agent joins at most one platform (Single-Homing) and profit functions are concave in prices in each time period. In particular, as demonstrated in “Appendix A.3”, we need:

Assumption 1

Externalities are not too strong with respect to the unitary transportation cost: (i) \(1>\max \{\alpha _S,\alpha _F\}\) and (ii) \(3>(2 \alpha _F+\alpha _S) (\alpha _F+2 \alpha _S)\).

As shown in Armstrong and Wright (2007), single-homing is the case when condition (i) is verified, meaning that agents are interested in reaching the other side, but not so much to decide to join both platforms and bear price and transportation cost twice. Moreover, condition (ii) in Assumption 1 is required in order to get rid of senseless situations in which the first-period market share increases in own (and decreases in rival’s) prices, which would also undermine concavity in overall profits.

3 Analysis

This section provides an analysis of the model. We first analyze the benchmark case of uniform pricing, and then we allow for consumer’s recognition and BBPD. The results in the two benchmarks will be then compared in the next section to understand the net effect of BBPD.

3.1 Uniform pricing

Without BBPD, there is no inter-temporal effect, as the problem solved by the platforms is the same across periods. Thus platform j solves:

where \({\bar{n}}^{j}_{i}=\frac{1}{2}+\frac{\alpha _{i}\left( p_{i^{\prime }}^{j'}-p_{i^{\prime }}^{j}\right) +t(p_{i}^{j'}-p_{i}^{j})}{t^{2}-\alpha _{i}\alpha _{i^{\prime }}}\text {, with } i\ne i^{\prime }\text { and } j\ne j'\), represents the market share of platform j in side i. This depends on the price difference between platforms on side i and on the price difference on the other side \(i^{\prime }\), which affects the location of the indifferent agent. Solving the system of FOCs gives:

with correspondent \(n_{F}^{j}=n_{F}^{j'}={\bar{n}}_{F}=1/2\) and \(n_{S}^{j}=n_{S}^{j'}={\bar{n}}_{S}=1/2\). Hence profits are common to both platforms and equal to:

In the two sides of the market, consumer’s aggregate surplus will be given by:

whereas firms’ aggregate surplus will be:

3.2 Consumer recognition

3.2.1 Second period

Let us assume that the two platforms have attracted some subscribers in the past, say all subscribers located below \(x_{S1}\) subscribed to platform A and all the remaining \(1-x_{S1}\) to platform B. Since each platform can observe its past subscribers, prices can be discriminated between old and new ones. Let us define \(p_{S2}^{jA}\) as the price set by platform j for an A’s inherited subscriber, while \(p_{S2}^{jB}\) is charged to B’s inherited clients. Firms are instead charged \(p_{F2}^A\) by firm A and \(p_{F2}^B\) by firm B. Let us first consider the optimal decisions of firms and subscribers when these prices are offered.

Subscribers In what follows, \(x_2^A\) represents the location of that A’s subscriber who is indifferent between switching to the rival or being loyal for given prices \(p^{AA}_{S2}\) and \(p_{S2}^{BA}\) offered to him. Following the same reasoning, \(x_2^B\) is the location of the indifferent agent in B’s turf. Simply equalizing utilities in both turfs, the two cutoffs will be:

Therefore, provided that \(x_{S1}\) is sufficiently close to 1 / 2,Footnote 11 the number of subscribers switching from platform A to platform B is given by \(n^{BA}_{S2}=x_{S1}-x_2^{A}\), while \(n^{AB}_{S2}=x_2^{B}-x_{S1}\) move towards the other direction. The remaining \(n^{AA}_{S2}=x_2^A\) and \(n^{BB}_{S2}=1-x_2^B\) are loyal respectively to platform A and platform B.

Firms Firms take their decision following the same reasoning as consumers. They observe prices offered by both platforms and form expectations about how many consumers will subscribe to each platform. Therefore, each firm correctly anticipates the switching behaviour of the other side and, by simple comparisons of utilities, the indifferent firm will be located at:

All firms located below this cutoff will join platform A (i.e., \(n^A_{F2}=x_{F2}\)) and all above will prefer platform B (\(n^B_{F2}=1-x_{F2}\)).

It is important to notice that the cutoffs in Eqs. (8) and (9) depend on the platforms’ first-period market shares on the subscribers’ side, but not on the ones on the firms’ side. This comes from the fact that, since at the beginning of the second period customers are free to join the platform giving them the higher utility, the past has in principle no impact on their choices.Footnote 12 However, BBPD creates a link between period one and period two in the subscribers’ side, because, for given prices, the size of the two segments of loyal and switching subscribers depends on the number of subscribers attracted in the first-period by each platform. Anticipating participation decisions on each side of the market, platform maximize profits setting prices. The equilibrium prices are summarized in the following lemma:

Lemma 1

Assume that \(n_{S1}^A=x_{S1}\) and \(n_{S1}^B=1-x_{S1}\) side S agents subscribed respectively to platform A and B in the past, then the equilibrium prices will be:

where \(\Lambda \equiv \frac{\left( 3 -2\alpha _{S}\left( 2\alpha _{S}+\alpha _{F}\right) \right) }{2\left( 9 -2\left( 2\alpha _{S}+\alpha _{F}\right) \left( \alpha _{S}+2\alpha _{F}\right) \right) }\in (0,\frac{1}{2})\) and \(\Omega \equiv \frac{(\alpha _{F}-\alpha _{S})}{4\left( 9 -2\left( 2\alpha _{S}+\alpha _{F}\right) \left( \alpha _{S}+2\alpha _{F}\right) \right) }\).

Proof

See “Appendix A.1”. \(\square \)

Therefore, the own inherited number of subscribers affects positively the price to loyal consumers and negatively the one to the switchers. Intuitively, the relation between prices and inherited subscriptions follows directly from the effective power that the size of the first-period market creates in each turf for the “attacking” (else turf) and the “defending” firm (own turf). Clearly, the attack in the rival turf turns out to be more costly as the size of the market already conquered becomes larger. In other words, the price offered by a platform to the switchers should be lower when many consumers subscribed in the past, since the non-conquered portion is very far away in the Hotelling line. Therefore, from the point of view of the defending firm, the higher the market share inherited from the past, the weaker the price competition in its own turf, as the rival becomes less aggressive. For this reason, the equilibrium price for loyalists is increasing in the inherited market share.

On the other hand, the extent to which the inherited number of subscribers affects the equilibrium price chosen in firms’ side ultimately depends on the relative strength of externalities between the two sides. If firms are more interested in meeting consumers than the other way around (i.e., \(\alpha _F>\alpha _S\)), then firms’ equilibrium price decreases with the number of inherited consumers. In this case, competition for consumers is very strong and switching is mainly due to offers in the subscribers’ side. Since firms expect switching movements towards the small-sized platform, they are willing to pay less as the number of inherited subscribers increases. Differently, if consumers are more interested than firms in the interaction, the latter are charged more as the inherited market increases. In this case, since competition for subscribers is less intense, switching is mainly driven by a decrease in the price offered to firms. This decrease will be smoother as the inherited number of consumers increases, given that the incentives to attract new subscriptions are lower (smaller potential market to conquer).

Given the prices in Lemma 1, the agent located at

is indifferent between switching to platform B and joining again platform A, whereas the one located at

is indifferent between joining again platform B and switching to platform A. It is important to notice that an increase in the inherited market of platform A turns out to make the two cutoffs move towards right, so that this platform is more likely to attract new subscribers and to keep loyal subscribers.

On the firms’ side, all firms located below

will join platform A, and all above will prefer the rival platform. Plugging prices and cutoffs into the profit function of platform j, its second-period profit will be:

3.2.2 First period

Taking into account the possibility of tomorrow’s switching, the utility of a subscriber located at x who joins platform j in the first period and \(j^{\prime }\) in the second one is \(U^{j^{\prime }j}(x) = u-p_{S1}^{j}+\alpha _{S} n_{F1}^{j}-|x-l^{j}| +\delta (u-p_{S2}^{j^{\prime }j}+\alpha _{S} n_{2F}^{j^{\prime }}-|x-l^{j^{\prime }}|\), with j possibly different from \(j^{\prime }\) in case of second-period switching. The indifferent subscriber who joins platform j will switch to platform \(j^{\prime }\ne j\) in the subsequent period. Therefore, plugging second-period prices and considering that \(n^{j}_{2F}=|x_{2F}-l^{j}|\), some rearrangements allow us to conclude that the indifferent subscriber locates at:

where \(\Gamma =\frac{9-2 (2 \alpha _{F}+\alpha _{S}) (\alpha _{F}+2 \alpha _{S})}{2 ((\delta +2) (2\alpha _F+\alpha _S) (\alpha _F+2\alpha _S)-3 (\delta +3))}>0\) under Assumption 1. Notice that under the assumption of full market coverage, it holds that the total numbers of customers joining respectively platform A and platform B will be \(n_{S1}^{A}=x_{S1}\) and \(n_{S1}^{B}=1-x_{S1}\). An important feature of the cutoff in Eq. (14) is that it is less sensible to price changes when BBPD is used and the magnitude of this effect depends on how much consumers value the future.

Lemma 2

For each platform \(j\in \{A,B\}\), it holds that:

Moreover, \(\left| \frac{\partial n _{S1}^{j}}{\partial p_{1}^i}\right| \) is decreasing in \(\delta \).

Compared to the non-discriminatory regime, the demand is less “elastic” because the indifferent consumer takes into account not only the direct impact of prices, but also the indirect effect on the prices offered by platforms in the switching stage. Moreover, the higher \(\delta \), the less responsive the indifferent consumer will be to first-period prices. When subscribers are fully myopic (\(\delta =0\)), \(\Gamma =1/2\), so that \(x_{S1}\) is the same of the uniform pricing case, whereas in the opposite extreme of \(\delta =1\), \(\Gamma \) becomes minimal, so that first-period demand for subscriptions is maximally “inelastic”.

On the other side of the market, the future does not play any role as long as firms are allowed to make their preferred choice in the subsequent period. Namely, differently from the indifferent subscriber who is sure to switch in the second period, the future utility of a firm located at x does not depend on the choices that this firm makes in the first period. Therefore, the location of the indifferent firm is simply found by comparing the static utilities and therefore given by:

Notice that the cutoff \(x_{F1}\) takes into account the inter-temporality in an indirect way. Indeed, \(n_{1S}^{A}\) and \(n_{1S}^{B}\) have an impact on the second period and they take into account the impact on future prices.

When the platforms maximize first-period profits, they take into account that current prices have an effect on future profits, as the market share of today determines the future switching. Indeed, having a high number of subscribers today reduces the chances both to steal customers from the rival and to retain old customers overcoming the poaching attempted by the rival. As demonstrated in the appendix, we will have the following equilibrium:

Proposition 3

The equilibrium is characterized by:

-

1.

first-period subscription fees equal to

$$\begin{aligned} p_{S1}^{*}=1-\alpha _{F}+\frac{9 \delta +\alpha _F^2 (1-6 \delta )-\alpha _F (3-\alpha _S (1-12 \delta ))+\alpha _S (3-2 \alpha _S) }{3 (9-2 (2 \alpha _F+\alpha _S) (\alpha _F+2 \alpha _S))}, \end{aligned}$$ -

2.

second-period prices for loyal and switching subscribers respectively equal to \(p_{S2}^{jj}=\frac{2}{3}-\alpha _{F}\) and \(p_{S2}^{jj^{\prime }}=\frac{1}{3}-\alpha _{F}\), with \(j^{\prime }\ne j\) and \(j^{\prime },j\in \{A,B\}\).

-

3.

firms’ prices equal to \(p_{F1}^{*}=p_{F2}^{*}=1-\alpha _{S}\),

-

4.

\(x_{S1}=x_{F1}=x_{F2}=1/2\) and \(x_{2}^{A}=1-x_{2}^{B}=1/3\).

Proof

See “Appendix A.2”. \(\square \)

Proposition 3 summarizes the main characteristics of the equilibrium prices and their effects on current market shares, competition, and future switching behaviour. Unsurprisingly, the market splits at locations 1/2 in both sides of the markets. After, 1/6 of subscribers switch platform in time 2 and 1/3 of them remain loyal,Footnote 13 whereas no switching occurs on the firms’ side. In equilibrium, the inter-temporal profits of each platform are:

In the two sides of the market, consumer’s aggregate surplus will be given by:

whereas firms aggregate surplus will be \({\overline{FS}}\) as in Eq. (7).

4 Welfare analysis

This section is devoted to the welfare analysis. Comparing the two benchmarks of uniform pricing and BBPD, the aim is to understand what are the effects of consumers recognition on surplus distribution and on total welfare, defined as the sum of consumer surplus, firms’ surplus and platforms’ profits. In order to perform the welfare analysis, it is useful to compare first prices in the two regimes.

Proposition 4

Allowing platforms to price subscribers according to their past purchase behaviour entails no effect on firms’ prices, whereas it always leads to lower-than-uniform second-period prices. If

-

(i)

either subscribers exhibit stronger externalities than firms (\(\alpha _{S}>\alpha _{F}\)),

-

(ii)

or they discount little the future \(\left( \delta > \frac{\left( \alpha _F-\alpha _S\right) \left( 3-\alpha _F-2 \alpha _S\right) }{9-3 \left( 2 \alpha _F+\alpha _S\right) \left( \alpha _F+2 \alpha _S\right) }\right) \),

then first-period prices are higher than uniform. If none of conditions (i) and (ii) is met, also first-period prices are lower in the discriminatory regime.

Proof

The results are found by comparing the prices in Proposition 3 with the prices in Eq. (4). \(\square \)

Two main effects are playing a role in the determination of optimal prices when platforms engage in within-group price discrimination.

Knowing the identity of subscribers pushes firms to compete fiercely in the poaching phase in order to steal each other’s consumers and to “defend” their inherited market from rival’s attack. This poaching effect has a clear-cut negative impact on second-period prices charged to subscribers. Nevertheless, this may also entail a mitigation of early competition, because of two reasons. On the one hand, being aggressive in the first period would entail a relative disadvantage in terms of tomorrows’ conquest of new subscriptions. On the other hand, if consumers care about future utilities (\(\delta >0\)), the demand for subscription responds less to first-period prices, as reported in Lemma 2. This “poaching inter-temporal effect” is typical in any model of BBPD in a one-sided market. For instance, Colombo (2015) concludes: “It follows that the first-period benefit from shifting from firm i to firm j is lower when future is taken into account. Hence, the higher \(\delta \) is, the lower is the benefit from shifting after a first-period price decrease.”.

Moreover, any price cut on one side of the market involves a positive effect on other side’s participation (externality intra-temporal effect). This is captured by the terms \(-\alpha _i\) found in all prices, which are nothing more than the “rewards” that a side-\(i^{\prime }\) agent (with \(i^{\prime }\ne i\)) receives for the benefit that his presence creates to side i. For this reason, the group exhibiting the lower externality becomes a loss leader and is basically subsidized by the other group, on which platforms mostly make profits: this is the so-called “Divide and Conquer” strategy typical of two-sided markets. The first intuitive result coming from the externality effect is that the symmetry of the model brings to a situation in which firms are charged with the same price both under within-group uniform pricing and price discrimination. This depends on the fact that subscriptions are equally split between the two platforms, and thus firms’ willingness to pay is the same in both regimes. Switching determines a change in “who” joins each network, but platforms steal each other the same number of subscribers, keeping the aggregate market shares unchanged.

The interplay between externality and poaching effect determines the direction in the comparison between first-period prices across regimes. In the early competition, the main trade-off faced by the platforms is an inter-temporal one. Indeed, they can either compete fiercely in order to conquer a large market right away or make high margins postponing the attack to the rival’s territory. The balance between these two opposite forces ultimately depends on the relative strength of externalities and on how much consumers discount the future.

Two cases may arise. If subscribers exhibit stronger externalities than firms, i.e., \(\alpha _{S}>\alpha _{F}\), the optimal “Divide and Conquer” strategy in the early competition will be to charge firms with a very low price and then make profits on the subscribers. As BBPD offers the platforms a new opportunity to enlarge their market lately, they are tempted to reduce competition in the subscribers’ side so to fully exploit the positive impact of late poaching on early competition. This is true independently on how much consumers care about future utilities. Indeed, even though consumers did not care about the future (\(\delta =0\)), in such a way that their first-period purchase were not affected by the switching opportunities tomorrow at a lower price, platforms’ equilibrium strategy would be to maximize first-period markups on the consumers’ side and then to postpone price competition to the switching phase. Therefore, the externality and the stealing effect together drive towards a weakened competition on the subscribers’ side.

Differently, if \(\alpha _F>\alpha _S\) platforms “divide” on subscribers’ side and “conquer” firms’ side, offering a very low price to the former and making profits on the latter. In such a situation, the subscribers are the loss-leading segment, so that profits are mainly made on firms. Therefore, as in Colombo (2015), the size of the discount factor is crucial. If \(\delta \) is sufficiently high, the indifferent first-period consumer responds feebly to price, so that competition is weakened when BBPD is viable to platforms. Differently, if consumers do not care enough about the future, platforms compete for consumers more severely in the discriminatory than in the non-discriminatory regime. Since consumers are very important to platforms, future switching becomes a threat of losing consumers rather than a future opportunity of attracting new ones. This makes platforms very aggressive in the early competition on consumers’ side.

In terms of welfare distribution, the difference in prices stated in Proposition 4 affects the wellbeing of the platforms and of the firms in the expected way. On the one hand, it is confirmed the traditional result of BBPD in a one-sided market: the platforms suffer from a prisoner dilemma in which stealing the business of the rival in the second period finally exacerbates inter-temporal competition, thus reducing profits when prices can be discriminated. On the other hand, firms’ side is not interested by BBPD: switching determines a change in “who” joins each network, but platforms steal each other the same number of subscribers, keeping the aggregate subscriptions of each platform constant over time. Differently, the effects of BBPD on consumer surplus and social welfare depend on the discounting of subscribers, as stated in the following proposition.

Proposition 5

Let \({\tilde{\delta }}\equiv \min \left\{ \frac{6 (\alpha _S-\alpha _F) (3-\alpha _F-2 \alpha _S)}{39-(\alpha _F+2 \alpha _S) (3 \alpha _F+5 \alpha _S)},0\right\} \) and \({\hat{\delta }}\equiv \frac{9 (\alpha _S+4)-37 \alpha _F \alpha _S-\alpha _F (13 \alpha _F+9)-22 \alpha _S^2}{66-7 (\alpha _F+2 \alpha _S) (3 \alpha _F+2 \alpha _S)}\). Allowing platforms to price subscribers according to their past purchase behaviour:

-

(i)

reduces platforms’ profits and does not entail any effect to the firms’ side,

-

(ii)

increases subscriber surplus if they discount little the future (\(\delta >{\tilde{\delta }}\)),

-

(iii)

increases social welfare if subscribers discount little the future (\(\delta >{\hat{\delta }}\)).

Proof

For the first point, it is sufficient to notice that \(\Pi ^{*}<{\bar{\Pi }}\) under Assumption 1 and that the firms’ surplus is identical across regimes. Point (ii) comes from the comparison of \(CS^{*}\) and \({\overline{CS}}\) and point (ii) from the comparison of \(CS^{*}+2\Pi ^{*}+{\overline{FS}}\) and \({\overline{CS}} +2{\bar{\Pi }}+{\overline{FS}}\). \(\square \)

As Proposition 5 shows, the impact of BBPD on consumer surplus essentially depends on the subscribers’ discount factor. The size of \(\delta \) will determine the severity of first-period competition as well as the relative importance of each time period for consumers. On the one hand, the more consumers care about the future, the less responsive to early prices the indifferent subscriber would be, with the consequence of a mitigated first-period competition. On the other hand, the more they care about future utilities, the more they weigh the switching phase with respect to the first-period. It turns out that the second effect always dominates the first one: even if discounting less strongly the future would mitigate first-period competition would then result in higher subscription prices, the the switching stage becomes more important. Hence, a high \(\delta \) results in a benefit of BBPD to subscribers.

When \(\delta \) is sufficiently low, BBPD can be detrimental to them. What sufficiently low means depends on the relative strength of subscribers’ and firms’ externality parameters \(\alpha _{S}\) and \(\alpha _{F}\). If \(\alpha _{S}<\alpha _{F}\), consumers are always better-off in the discriminating regime. This result is intuitive if one keeps in mind Proposition 4. Indeed, when subscribers have weaker externalities than firms and discount much future utility, subscription prices are lower-than-uniform in both periods, with the consequence of an increased surplus.

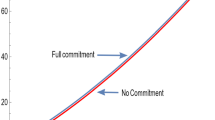

Effect of BBPD on CS and W

More generally, Fig. 1 shows that the space in which BBPD can be detrimental to consumers becomes wider as \(\alpha _{S}\) increases. This consumer-damaging space is represented by the regions below the blue curves, with \(\alpha _{S}\) low (left graph) and \(\alpha _{S}\) high (right graph). Again, this can be easily interpreted having in mind Proposition 4. When consumers exhibit strong externalities, they become the profit-making segment and BBPD gives a new opportunity to conquer demand. As a result, first-period competition is mitigated with respect to uniform pricing and this goes at the detriment of consumers when they do not put much weight on future utility.

5 Conclusion

The present paper provides a model of platform competition, in which the demand is composed by two sides, firms and consumers. Platforms are allowed to discriminate prices among consumers according to their past purchase behaviour. It contributes to the literature of two-sided markets by giving to the competing platforms the possibility to engage in within-group price discrimination as well as to the literature of behaviour-based price discrimination by considering a two-sidedness of the market. In particular, in a market with no cross-group externalities, the model proposed in this paper replicates the analysis of Fudenberg and Tirole (2000). Qualitatively, the paper shares with Fudenberg and Tirole (2000) similar results for what concerns the effects of BBPD on the discriminating rivals, but provides new effects for the consumers.

On the one hand, platforms face a strategic situation similar to a prisoner dilemma. Each one of them alone has the incentive to offer discounted prices for new subscriptions but, if both of them do it, the level of profits turns out to be lower than the one that would have been reached if they committed not to poach rival’s consumers. Going from the non-discriminatory to the discriminatory regime entails a loss in the consumers’ side, as platforms compete fiercely in order to poach each other’s clients. On top of that, the presence of cross-group externalities strengthens this loss when firms are more interested than subscribers in meeting the other side of the market. This is due to the fact that the latter group is pivotal to attract the former and BBPD makes platforms worried about the future attack of the competitor. Oppositely, when subscribers exhibit the strongest network externalities or put enough weight on future utility, early prices are higher in the discriminatory regime, as BBPD gives the platforms a further possibility to attract subscribers lately. Even in this second case, the negative effect of BBPD on poaching prices overcompensates the softening of early competition, making platforms worse-off. Moreover, the losses made on the subscribers’ side are not recouped on the firms’ side. Indeed, switching of subscribers determines a change in their identity, but their total number in each platform (what matters to firms) remains constant over time. This makes firms indifferent between BBPD and uniform pricing, so that the final price will be the same.

On the other hand, consumer surplus might be higher or lower under BBPD in relation to uniform subscription pricing, depending on the relative intensity of externalities and on the relative discounting of consumers in relation to the platforms. When consumers care less than firms to reach the other side of the market, then consumer surplus is higher under BBPD, regardless of the relative discounting. This is because either first-period competition is strengthened by BBPD or its mitigation is compensated by lower second-period prices. Differently, if consumers have stronger externalities and discount much future utility, the softened early competition drives the equilibrium towards higher first-period prices, reducing consumer surplus.

Hence, the platforms always lose when they discriminate, firms are indifferent and consumers might either gain or lose. The consequence on social welfare is thus straightforward. When consumers discount much the future, welfare would be higher if BBPD were banned, whereas it is higher if BBPD is allowed when the future is sufficiently important. The level of the discount factor needed for BBPD to be welfare-enhancing is higher than the one required to be consumer-surplus-enhancing. This means that when consumers discounting is intermediate, they gain from BBPD but not enough to compensate the loss made by the competing platforms.

The implications of the paper are in line with the idea that using a one-sided logic looking at two-sided markets may lead to incorrect policy evaluations.Footnote 14 In particular, the literature of one-sided BBPD agrees on an inter-temporal intensification of competition due to a market-stealing effect: prices are lower-than-uniform and this goes all at the benefit of consumers. The present paper demonstrates that, if the two-sidedness of the market is taken into account, the impact of BBPD on consumer surplus and total welfare might be positive or negative. This suggests that the implications of BBPD depend on the industry considered. In particular, the model can be tested empirically. Data on prices, on consumers’ and firms’ participation can be used to identify which group exhibits stronger externalities and to test consumers’ relative discounting. Then, the model would suggest to limit BBPD in markets where consumers discount strongly the future and are the profit-making group.

For instance, if one considers the case of media with readers/viewers on one side and advertisers on the other side of the market, the consumers are the loss-leading group and advertisers the profit-making group. Indeed, consumers are mostly disturbed by commercials and advertisers are there only to meet potential clients (i.e., they have stronger externalities). Hence, BBPD intensifies competition in both periods, increases consumer surplus and also social welfare provided that consumers care enough about future utility. Differently, online platforms make profits on subscribers while content providers are the loss-leading group. Indeed, the first pay positive subscription prices,Footnote 15 whereas the second ones receive a positive royalty. This suggests that consumers exhibit stronger externalities, so that, if they put little weight on future utility, consumer surplus and social welfare would be lowered by BBPD.

Notes

From Amazon website “Amazon Prime members in the U.S. can enjoy instant videos: unlimited, commercial-free, instant streaming of thousands of movies and TV shows through Amazon Instant Video at no additional cost. Members who own Kindle devices can also choose from thousands of books—including more than 100 current and former New York Times Bestsellers—to borrow and read for free, as frequently as a book a month with no due dates, from the Kindle Owners’ Lending Library. Eligible customers can try out a membership by starting a free trial”.

Taylor (2003) also mentions a 1998 Wall Street Journal’s article by Bailey and Kilman reported that “the \(60\%\) of all Visa and MasterCard solicitations include a “teaser” (low introductory rate) on balances transferred from a card issued by another bank”.

As for any type of price discrimination, some consumer-specific information is needed. On the one hand, to engage in cross-group price discrimination, platforms simply sort customers according to their externalities. On the other hand, within-group BBPD requires platforms to know the identity and the behaviour of customers.

The literature distinguishes between subscription fee and usage fee. In the analysis of the media market of Ferrando et al. (2008) is pointed out how, while readers are charged with the price of the newspaper, advertiser are charged on per-reader basis.

In different setups, this is confirmed by Villas-Boas (1999), Esteves (2010), Chen (1997). The severity of this firm-damaging result is partially mitigated under weak time correlation between preferences of consumers (Chen and Pearcy 2010), strong demand elasticity (Esteves and Reggiani 2014), consumer arbitrage (Kosmopoulou et al. 2016) and firms’ asymmetries (Carroni 2016).

Hereafter, the paper uses indifferently the words subscribers, consumers, group S or side S. Similarly, firms are also called side or group F throughout the paper.

The assumption of a common transportation cost equal to 1 is made in order to keep notation as simple as possible, but the intuition behind the results provided in the paper remains the same even assuming arbitrary and side-dependent transportation costs.

As it will be discussed in detail in Sect. 3.2.2, the discount factor of firms is irrelevant as long as they are allowed to choose the preferred platform in each time period.

A similar assumption is made in the seminal paper by Fudenberg and Tirole (2000). It allows to consider only symmetric switching scenarios. See Gehrig et al. (2012) for an analysis of Fudenberg and Tirole (2000) second period with the past taken as given and Esteves (2014) and Carroni (2016) for an inter-temporal analysis of asymmetric equilibria.

This is true always in the uniform pricing regime discussed in the previous section.

The switchers towards platform A are located between 2/3 and 1/2, whereas 1/2–1/3 go towards platform B. The remaining agents closer to the extremes remain loyal.

See Wright (2004).

Actually, this depends on the business model adopted, which, depending on the market (see Carroni and Paolini (2017)) can be based on paying Premium subscription or mixed with Premium plus ad-based subscriptions, i.e., Freemium.

References

Andreoni J, Sprenger C (2012) Estimating time preferences from convex budgets. Am Econ Rev 102(7):3333–56

Angelucci C, Cage J, Nijs RD (2013) Price discrimination in a two-sided market: theory and evidence from the newspaper industry. Available at SSRN 2335743

Armstrong M (2006) Competition in two-sided markets. RAND J Econ 37(3):668–691

Armstrong M, Wright J (2007) Two-sided markets, competitive bottlenecks and exclusive contracts. Econ Theory 32(2):353–380

Caillaud B, Jullien B (2003) Chicken & egg: competition among intermediation service providers. RAND J Econ 34(2):309–28

Caillaud B, De Nijs R (2014) Strategic loyalty reward in dynamic price discrimination. Mark Sci 33(5):725–742

Carroni E (2016) Competitive customer poaching with asymmetric firms. Int J Ind Organ 48:173–206

Carroni E (2017) Poaching in media: harm to subscribers? J Econ Manag Strategy. https://doi.org/10.1111/jems.12238

Carroni E, Paolini D (2017) Content acquisition by streaming platforms: premium vs. freemium. CORE Discussion Papers 2017007, Université Catholique de Louvain, Center for Operations Research and Econometrics (CORE)

Chen Y (1997) Paying customers to switch. J Econ Manag Strategy 6(4):877–897

Chen Y, Zhang ZJ (2009) Dynamic targeted pricing with strategic consumers. Int J Ind Organ 27(1):43–50

Chen Y, Pearcy J (2010) Dynamic pricing: when to entice brand switching and when to reward consumer loyalty. RAND J Econ 41(4):674–685

Colombo S (2015) Should a firm engage in behaviour-based price discrimination when facing a price discriminating rival? A game-theory analysis. Inf Econ Policy 30:6–18

Esteves R-B (2010) Pricing with customer recognition. Int J Ind Organ 28(6):669–681

Esteves R-B (2014) Behavior-based price discrimination with retention offers. Inf Econ Policy 27:39–51

Esteves R-B, Reggiani C (2014) Elasticity of demand and behaviour-based price discrimination. Int J Ind Organ 32:46–56

Ferrando J, Gabszewicz JJ, Laussel D, Sonnac N (2008) Intermarket network externalities and competition: an application to the media industry. Int J Econ Theory 4(3):357–379

Fudenberg D, Tirole J (2000) Customer poaching and brand switching. RAND J Econ 31(4):634–657

Gabszewicz JJ, Wauthy XY (2014) Vertical product differentiation and two-sided markets. Econ Lett 123(1):58–61

Gehrig T, Shy O, Stenbacka R (2012) A welfare evaluation of history-based price discrimination. J Ind Compet Trade 12(4):373–393

Gil R, Riera-Crichton D (2011) Price discrimination and competition in two-sided markets: evidence from the Spanish local TV industry. IESE research papers D/894, IESE Business School

Kosmopoulou G, Liu Q, Shuai J (2016) Customer poaching and coupon trading. J Econ 118(3):219–238

Liu Q, Serfes K (2013) Price discrimination in two-sided markets. J Econ Manag Strategy 22(4):768–786

Malkoc SA, Zauberman G (2006) Deferring versus expediting consumption: the effect of outcome concreteness on sensitivity to time horizon. J Mark Res 43(4):618–627

Rhee K-E, Thomadsen R (2017) Behavior-based pricing in vertically differentiated industries. Manag Sci 63(8):2729–2740

Rochet J-C, Tirole J (2003) Platform competition in two-sided markets. J Eur Econ Assoc 1(4):990–1029

Roger G (2017) Two-sided competition with vertical differentiation. J Econ 120(3):193–217

Taylor CR (2003) Supplier surfing: competition and consumer behavior in subscription markets. RAND J Econ 34(2):223–46

Villas-Boas JM (1999) Dynamic competition with customer recognition. RAND J Econ 30(4):604–631

Villas-Boas JM (2006) Dynamic competition with experience goods. J Econ Manag Strategy 15(1):37–66

Wright J (2004) One-sided logic in two-sided markets. Rev Network Economics 3(1):1–21

Zhang J (2011) The perils of behavior-based personalization. Mark Sci 30(1):170–186

Acknowledgements

I am grateful to the editor Giacomo Corneo and two anonymous referees for helpful reviews on the paper. I also wish to thank Eric Toulemonde, Paul Belleflamme, Gani Aldashev, Jean Marie Baland, Marc Bourreau, Rosa Branca Esteves, Giulia Lai, Paolo Pin, Dimitri Paolini and Paola Rais for their helpful comments and suggestions. I am indebted to the participants to the Doctoral Workshop 2012 at UCLouvain, 2013 Ecore Summer School—Governance and Economic Behavior (Leuven), 3rd GAEL Conference—Product differentiation and innovation on related markets (Grenoble). I acknowledge the “Programma Master & Back—Regione Autonoma della Sardegna” for financial support.

Author information

Authors and Affiliations

Corresponding author

Appendix A

Appendix A

1.1 Proof of Lemma 1

Platform j expects to keep \(n^{jj}_{S2}=|x^j_2-l^j|\) of them. These agents are going to pay the fee that platform j charges to its loyalists, i.e., \(p^{jj}_{S2}\). On the other hand, \(|x^{j^{\prime }}_2-x_{S1}|\) are expected to switch from the rival platform \(j^{\prime }\) and these switchers are going to pay the price \(p^{jj^{\prime }}_{S2}\). Plugging these results into Eq. (9) and putting together with (8), the cutoffs depend on all prices as follows:

Anticipating the behaviour of both sides of the market, platform j solves the following maximization problem:

Using the first-order conditions of this problem and solving the system of best responses, the equilibrium prices are the the ones stated in Proposition 1. See “Appendix A.3” for the second-order conditions (concavity).

1.2 Proof of Proposition 3

Since firms and subscribers anticipate the other side’s participation, using Eqs. (14) and (15), we get:

and

Platform j sets respectively prices \(p^j_{S1},p^j_{F1}\) in order to maximize inter-temporal profits, i.e., solves:

where \(n_{S1}^{j}=|x_{S1}-l^{j}|\), \(n_{F1}^{j}=|x_{F1}-l^{j}|\) and \(\pi _{2}^{j}\) is as defined in Eq. (13). The first order-conditions of this problem give:

Looking at Eqs. (21) and (22), it is evident that \(\frac{\partial n_{F1}^{j}}{\partial p_{S1}^{j}}=2\alpha _{F}\Gamma \frac{\partial n_{F1}^{j}}{\partial p_{F1}^{j}}=\alpha _{F}\frac{\partial n_{S1}^{j}}{\partial p_{S1}^{j}}\), that \(\frac{\partial n_{S1}^{j}}{\partial p_{F1}^{j}}=\alpha _{S}\frac{\partial n_{S1}^{j}}{\partial p_{S1}^{j}}\) and that \(\frac{\partial n_{F1}^{j}}{\partial p_{F1}^{j}}=\frac{1}{2\Gamma }\frac{\partial n_{S1}^{j}}{\partial p_{S1}^{j}}\). Hence, the two FOCs can be rewritten as follows:

In a symmetric equilibrium, it holds that for \(j'\ne j\), we have \(p_{S1}^{j}=p_{S1}^{j^{\prime }}\) and \(p_{F1}^{j}=p_{F1}^{j^{\prime }}\), so that \(n_{F1}^{j}=n_{S1}^{j}=1/2\). Therefore, solving the system of the two equations above, we get the following equilibrium prices:

1.3 Concavity of the profit functions

In order for the first-order conditions to be sufficient for a maximum, it is needed that the profit functions of the two platforms are concave. This must be true in both time periods. In particular, for any given inherited history of the game, the profit function of platform i must be concave in \(p_{S2}^{jj}\), \(p_{S2}^{jj^{\prime }}\) and \(p_{F2}^{j}\). Then, when platform sets first-period prices, they anticipate the competition in the switching phase.

The second-period profit of platform j is given by \(\Pi _{2}^{j}=p_{S2}^{jj}|x_{2}^{j}-l^j |+p_{S2}^{jj^{\prime }}| x_{2}^{j^{\prime }}-x_{S1} |+p_{F2}^{j}|x_{F2}^{j}-l^j |\) where \( x_{2}^{j}\), \( x_{2}^{j^{\prime }}\) and \(x_{F2}\) are defined in Eqs. (18), (19) and (20). In order to verify concavity, the Hessian matrix is given by:

For the second-period profit to be concave we need the Hessian to be negative definite. Namely:

-

1.

\(Det|H|=\frac{(\alpha _F+\alpha _S)^2-2}{2 (1-2 \alpha _F \alpha _S)^2}<0\), which requires the condition \((\alpha _F+\alpha _{S})^{2}<2\).

-

2.

\(Det\begin{bmatrix} \frac{1-\alpha _F \alpha _S}{2 \alpha _F \alpha _S-1}&\frac{\alpha _F \alpha _S}{2 \alpha _F \alpha _S-1}\\ \frac{\alpha _F \alpha _S}{2 \alpha _F \alpha _S-1}&\frac{1-\alpha _F \alpha _S}{2 \alpha _F \alpha _S-1}= \end{bmatrix}=\frac{1}{1-2 \alpha _F \alpha _S}>0\), verified because the condition in point 1 implies \(\alpha _{S}\alpha _{F}<1/2\).

-

3.

\( \frac{1-\alpha _F \alpha _S}{2 \alpha _F \alpha _S-1}<0\), verified because the condition in point 1 implies \(\alpha _{S}\alpha _{F}<1/2\).

In the first period, the concavity of platform j profits will depend on both periods’ profits, i.e., on the direct effect of a price change on the first-period profit as well as on the indirect effect on the second-period profit. Differentiation of the left-hand-sides of Eqs. (23) and (24), gives:

In this case, with a \(2\times 2 \) Hessian matrix, we need \(\frac{2\partial n_{S1}^{j}}{\partial p_{S1}^{j}}<0\) and \(\frac{2\partial n_{S1}^{j}}{\partial p_{S1}^{j}}\times \frac{2\partial n_{F1}^{j}}{\partial p_{F1}^{j}}-\left( \frac{\partial n_{S1}^{j}}{\partial p^{j}_{F1}}+ \frac{\partial n_{F1}^{j}}{\partial p^{j}_{S1}}\right) >0\). By simply looking at the cutoffs in Eqs. (21) and (22), it is easy to verify that these conditions are verified for all discount factors only if \(3>(2 \alpha _F+\alpha _S) (\alpha _F+2 \alpha _S)\), which is a stricter condition than \((\alpha _F+\alpha _{S})^{2}<2\).

Rights and permissions

About this article

Cite this article

Carroni, E. Behaviour-based price discrimination with cross-group externalities. J Econ 125, 137–157 (2018). https://doi.org/10.1007/s00712-017-0591-z

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00712-017-0591-z