Abstract

Exchange-traded commodities (ETCs) open the commodity markets to both private and institutional investors. This paper is the first to examine the pricing efficiency and potential determinants of price deviations of this new class of derivatives based on daily data of 237 ETCs traded on the German market from 2006 to 2012. Given the unique size of the sample, we employ the premium/discount analysis, quadratic and linear pricing methods, as well as regression models. We find that the ETCs incur, on average, price deviations in their daily trading and are more likely to trade at a premium from their net asset values than at a discount. In addition, we examine the influence of certain factors such as management fees, commodity sectors, issuers, spread, assets under management, investment strategies, replication and collateralization methods on quadratic and linear price deviations.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Exchange-traded commodities (ETCs) have evolved into a significant financial instrument within the commodity asset class. They were first introduced by Investor Resources Limited under its founder Graham Tuckwell in 2003 and listed on the Australian Securities Exchange. Marking a cornerstone for the development of commodity investing, they are designed to provide both institutional and private investors with exposure to a range of investment possibilities, from well-known commodities, such as gold, silver, or platinum, over exotic ones, such as lean hogs (e.g. Brooks 2008), to commodity futures or commodity indices. ETCs are open-ended passive derivative instruments that are listed on an exchange and traded like shares. This article is the first to explore the pricing efficiency of ETCs and to examine potential determinants of price deviations for the case of the German market which is the most important one for ETCs in Europe.

ETCs undoubtedly belong to the group of exchange-traded products (ETPs), which also include exchange-traded notes (ETNs) and exchange-traded funds (ETFs). ETCs, that sometimes are also called commodity ETFs, all share the following features: First, they are open-ended investments that are listed and continuously traded like shares on a stock exchange. Second, they are passive investments that track the performance of a given benchmark. Third, they use either a physical or synthetic replication method. Despite these common characteristics and the grouping as “exchange-traded” to increase the popularity of ETCs and ETNs in light of the success of ETFs, a clear distinction has to be made due to many structural and regulatory differences. ETCs are debt securities that enable investors to gain exposure to commodity markets without the requirement of physical delivery or futures trading. According to Lang (2009), they are undated and normally secured zero-coupon notes from a legal point of view. ETNs are also debt securities based on the performance of references outside the commodity sector, such as currencies or volatilities; however they are, unlike ETCs, generally non-collateralized and therefore bear the default risk of the issuer. By contrast, ETFs are collective investment funds, based on the performance of literally all held assets and are subject to strict regulatory requirements of the UCITS,Footnote 1 which do not permit the replication of single commodities or less diversified indices.

For investors, ETCs are a means of gaining exposure to commodity returns. Therefore, the classification of ETCs with regard to investable resources may be based on the common classification of commodities. Even though commodities share unique investment characteristics separating them as a distinct asset class, there is a notable lack of homogeneity among the different types of commodities. In accordance with Engelke and Yuen (2008) and Fabozzi et al. (2008), commodities can traditionally be summarized as hard or soft commodities depending on their degree of availability and perishability and further be categorized into five commodity sectors (agriculture, livestock, precious metals, industrial metals, and energy).

The first two sectors, agriculture and livestock, are among the soft commodities, which can be characterized as renewable, perishable, non-limited in quantitiy and typically grown products for consumption. In terms of ETCs, the agricultural sector comprises diverse sub segments such as corn, wheat, cotton, coffee, soybeans, soybean oil, cocoa, and sugar, whereas the livestock sector mainly bifurcates into live cattle and lean hogs.

The latter three sectors, precious metals, industrial metals and energy, can be considered as hard commodities which are non-renewable, non-perishable, limited in quantity, and typically extracted by a mining process or obtained from a non-agricultural source. Examples of investable precious metals are mainly gold, palladium, platin, rhodium, and silver. Moreover, industrial metals can be split into aluminium, lead, copper, nickel, zinc, and tin while the energy sector provides gasoline, fuel oil, crude oil, natural gas, and electricity as subsegments.

It is not only the limited attention of the academic literature to date, but also the positive outlook for the market of passive investment and the commodity sector in general (Fabozzi et al. 2008) which provide a motivation for our comprehensive analysis of ETCs. By identifying the reasons for the expected ongoing popularity of ETCs and other ETPs with regard to the investment horizon, Bienkowski (2007) mentions the easy access to the commodity markets previously reserved for sophisticated investors, the high liquidity, flexibility, transparency and appealing cost structure as major drivers.

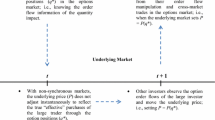

A key consideration in the investigation of ETCs is the creation/redemption mechanism and the unique trading mechanism that ETCs have in common with ETFs and ETNs, which require a distinction between primary and secondary markets. In the primary market, ETC shares can be created and redeemed on an on-demand basis by the so-called authorized participants (APs). The issuer of an ETC is a special purpose vehicle (SPV) in the legal form of a limited liability company or a limited partnership created for the sole purpose of issuing ETCs and liable under the law of its incorporated country. APs are large financial institutions, brokers, or approved market makers that are contractually entitled to solely serve this role and directly operate with the SPV. For the creation of ETC units, the APs transfer securities or cash at the issuer’s deposit in exchange for a block of a given number of ETC shares, often called “creation unit”, which they split for a secondary market sale. The subscription price per unit is determined by the intrinsic value, the net asset value (NAV), which is calculated on a daily basis depending on the official price of the underlying asset. The process operates in reverse if ETC shares are redeemed. Due to this on-demand creation/redemption mechanism, ETCs can be defined as open-end investments.

The secondary market mainly takes place on stock exchangesFootnote 2 where the APs purchase and sell the ETC shares. Investors can trade and settle them at a price determined by the best bid and best ask within a defined spread during trading hours while market makers provide liquidity all day.

The existence of the creation/redemption process ensures that the price of the ETC shares is close to the NAV of the primary market (see Borsa Italiana 2009). Otherwise, Gastineau (2001) suggests the APs could exploit arbitrage opportunities. When ETC prices are lower than their respective NAVs, the APs will acquire the underlying securities and redeem ETC shares and vice versa.Footnote 3

However, as in reality market imperfections exist, the factual pricing efficiency of theses derivative instruments is an important issue for investors and researchers. In our analysis we determine whether there are deviations between the prices of ETCs and their respective NAVs and consider 237 ETCs traded in Germany, which is the largest market for such ETCs in the euro zone.

Compared to previous studies on ETPs, this is one of the largest samples to analyze. Thus, we contribute to the literature not only by introducing a new asset class, but also by providing a data set of unique size and regional focus to further extend existing research of exchange-traded products. Despite its short market history of about six years and the occurrence of the financial crisis, we can identify a tremendous growth in the ETC assets under management (AUM) by more than a factor 10 from EUR 164 million up to EUR 23096 million as well as in the number of products increasing by eight times from 31 to 276 products from November 2006 to June 2012.Footnote 4 With regard to the European ETC AUM by the end of 2011, we find a market share of nearly 70% of the German market with AUM of EUR 19951 million. In terms of turnover as of 2012, the German stock exchange “Deutsche Börse AG” is also the market leader with a turnover of EUR 7598 million for ETCs in the Euro area (Lan et al. 2013), followed by the “Börse Stuttgart AG”.

Given these facts, we concentrate on the German market for the investigation of the ETCs from the perspective of a euro investor. We employ a number of various approaches: the premium/discount analysis (PD analysis), quadratic and linear pricing efficiency measures, and regression analysis. We first investigate the existence of price deviations based on daily figures of the ETCs under consideration and subsequently analyze potential influencing factors of these deviations. We find, on average, for all different price measures significant pricing deviations from theoretical fair values in the daily trading of ETCs. Aiming to detect influencing factors of the pricing mismatch, we run several multiple ordinary least squares (OLS) regressions which could explain the potential arbitrage opportunities of investors.

The remainder of the paper is organized as follows. We commence with a discussion of related literature, and then describe the data and methodology we use in our empirical analysis. The next section introduces the variables and hypotheses developed as part of the regression analysis. Subsequently, we present and discuss our empirical results. Finally, a conclusion completes the paper.

2 Related literature

Since a number of studies is relevant for our analysis, we next discuss a selection of publications in the fields passive management, commodities in general, and ETPs.

Many authors are concerned with a general discussion about active and passive management approaches. Major studies by Jensen (1967), Lehmann and Modest (1987), Malkiel (1995), Gruber (1996), and Rompotis (2011a) are not able to find an outperformance of active investment solutions when compared to market indices, passively managed mutual funds or exchange-traded products. With a particular focus on commodities, Mankiewicz (2009) undertakes a comparative analysis between the active and passive management of commodity indices with regard to pension funds and discusses the suitability of passive financial instruments such as ETCs as alternative sources of return in a theoretical framework. Plante and Roberge (2007) describe the benefits of passive commodity investing relative to active approaches and find that theoretical sources of returns such as return on collateral and excess return of the GSCI index between 1970 and 2006 can be realized as actual returns.

Another fast-growing class of literature has shown substantial interest in commodities since the beginning of an increasing investor demand due to financial and sovereign crises and inflation fears. Fabozzi et al. (2008) as well as Anson et al. (2011) identify investment characteristics of commodities differentiating them from traditional asset classes like stock or bonds. Gorton and Rouwenhorst (2006) examine both a negative correlation between commodity futures and other asset classes like shares and bonds due to different behavioral patterns in the business cycle as well as a positive correlation with expected and unexpected inflation and changes in expected inflation. Several authors investigate the diversification benefits of commodities in a traditional portfolio consisting of stocks and bonds using different methods with different findings (e.g. Bodie 1983; Anson 1999; Stoll and Whaley 2010; Belousova and Dorfleitner 2012).

The literature has begun to cover the topic of exchange-traded products as financial innovations. Laying the foundations for further research approaches, Gastineau (2001) is the first to analyze ETPs in his study about the characteristics, mechanics and benefits of ETFs. Other follow-up studies provide an overview of ETFs (e.g. Deville 2008; Gastineau 2010) and ETNs (e.g. Wright et al. 2010) in great detail.

Since before the advent of ETPs, there has been another class of investment instruments that provide exposure to indices or other difficult-to-trade underlyings or with exotic features like principal protection or discounts. Structured products, like market-index certificates of deposits, discount certificates and reverse convertibles, which are issued by financial institutions, are derivative products, that are made up from more basic assets and derivatives. The literature concerned with the pricing of such products looks at deviations from the fair price, which is given by the capital required to set up a static hedge in exchange-traded derivatives. Chen and Kensinger (1990) were the first to note the severe mispricing, which could be traced back to the profit maximizing behavior of issuers that make rational use of their quasi monopoly (Wilkens et al. 2003; Grünbichler and Wohlwend 2005; Muck 2006). Another driver is hedging difficulty, which is for example higher for single stock underlyings compared to index underlyings, that have more liquid derivatives markets (Stoimenov and Wilkens 2005). Wallmeier and Diethelm (2009) also provided evidence for behavioral effects, like the irrational preference for overpriced products as long as they offer high coupons.

From the investor’s perspective, structured products and ETCs serve a similar purpose, and pricing efficiency is an important topic in both classes. While the characteristics and drivers of the pricing anomalies are expected to be similar, the innovative, simpler and more transparent structures and mechanisms behind ETCs—devised in part to overcome the shortcomings of structured products—create the need for studies devoted to the peculiarities of ETCs.

However, we can only find incomprehensive studies that either focus on individual characteristics or are insufficient in terms of an in-depth review. Bienkowski (2010), for example, mainly presents a description of the development of commodity investments and addresses ETCs, especially oil ETCs and their various product strategies (long, short, forward, and leveraged positions) very briefly. In a further study with a sole focus on ETCs, Bienkowski (2007) depicts the backgrounds of the origins, the main advantages, and the general market development of ETCs based on assets under management and the number of existing products. In a similar introduction of ETCs, Brooks (2008) finds the predominance of precious metals ETCs in his global market analysis by sector and highlights the revolutionary role of ETCs in the opening of commodity markets to all investors. Despite the limited research on ETCs, many properties relating to ETPs, such as the creation/redemption process for the issuance and redemption of units (e.g. Gastineau 2001, 2010) are well explained in ETP literature. So far there is no study exploring the pricing efficiency of ETCs systematically.

The literature, then taking an empirical perspective on passive financial instruments, is often dedicated to various forms of price differences. Charupat and Miu (2011) distinguish between pricing efficiency and tracking errors in their study on leveraged ETFs. They describe pricing efficiency as the relationship between an ETF’s prices and its respective net asset values while tracking errors refer to the ability of an ETF to replicate the underlying benchmark’s return in the ETF’s NAV return. In the view of ETFs, authors (e.g. Jares and Lavin 2004; Engle and Sarkar 2006; Lin and Chou 2006; Aber et al. 2009; Charupat and Miu 2011; Kayali and Ozkan 2012) analyze the relative price differences between the price and its net asset value in the so-called PD analysis.

Other publications by Kostovetsky (2003), Gallagher and Segara (2006), Rompotis (2008), Shin and Soydemir (2010), and Tzvetkova (2005) use quadratic and linear deviation measures based on the concepts developed by Roll (1992) and Rudolf et al. (1999) in their determination of deviations. Especially the few studies related to ETNs are important for our analysis. Wright et al. (2010) find, in their investigation of 65 globally traded ETNs in the period from 2008 to 2010, significant price deviations between the prices and their respective NAVs. By contrast, Diavatopoulos et al. (2011) suggest that the prices of 93 ETNs are significantly higher than their indicative prices due to a less liquid creation/redemption process. Aroskar and Ogden (2012) employ five different measures to analyze both pricing efficiency and tracking errors in their sample of 25 ETNs divided into four categories in the period from 2008 to 2011; however, they find different results in their descriptive analysis of price deviations depending on the respective subcategory. Leung and Ward (2015) and Guo and Leung (2015) examine tracking errors of leveraged ETCs and demonstrate how a dynamic replication portfolio built from futures yields smaller tracking errors.

The literature about determinants of ETF tracking errors identifies several factors influencing the magnitude of errors. These are, among others, AUM, ETF trading volume (Buetow and Henderson 2012), management fee (Chu 2011), number of overlapping market hours as well as return differences between US and foreign markets (Johnson 2009), ETF age and standard deviations of returns (Rompotis 2011b). Physically replicating ETFs have smaller tracking errors than synthetically replicating ETFs (Fassas 2014). Schmidhammer et al. (2010) find that the tracking error of ETFs on the German stock index (DAX) is highly correlated with the price differences between DAX and DAX futures.

3 Data and methodology

3.1 Data

The data for our research covers 237 ETCs, with total assets under management exceeding EUR 21 billion as of June 2012, which are listed on the Frankfurt Stock Exchange on Xetra of Deutsche Börse AG or on regional stock exchanges, such as Stuttgart, and can be traded within trading hours of 9.00 a.m. to 5.30 p.m. on business days. The sample period of our daily data begins with the initial trading date of each ETC, the earliest with the start of the ETC trading in Germany on 03 November 2006, and ends on 25 July 2012. We constructed our dataset by comparing the 276 listed products of the German stock exchange to the product data available in Bloomberg, which only included prices and NAVs for 237 ETCs. The dataset analyzed differs from comparable studies of ETFs or ETNs in two ways. First, we focus on the German ETC market or, from a broader perspective, on the European market, which have not yet been investigated in academic literature. Second, by covering nearly all products available on the German market, the size of our dataset is significantly larger than that of comparable studies of other ETPs, which mostly include a range of between 5 and 100 investigation units (see Aber et al. 2009).

For the first part of our investigation, the ETC data consist of historical mid-prices as the average of bid and ask closing prices and of their net asset values (NAVs) as published by the issuers in euro currency for each ETC from its respective initiation date until 25 July 2012. The bid prices describe the highest prices a dealer will be prepared to pay whereas the ask prices are the lowest prices a dealer will be prepared to sell a security on a given day at. In accordance with Aroskar and Ogden (2012), we use mid-prices at closing of ETCs as they reflect more clearly the daily price movements of ETCs. Observations missing either bid price, ask price or NAV are removed from the respective ETC’s data set.

The NAVs are computed by subtracting the liabilities from the portfolio value of the securities and dividing that figure by the number of outstanding shares. These are calculated once a day for each ETC, providing another argument for using mid-prices of ETCs. In the subsequent analysis, our computations are based on both prices and log returnsFootnote 5 of mid-prices and NAVs.

For the second part of our empirical analysis, we extended our database by collecting additional information from stock exchanges, issuers’ publications and Bloomberg. For each ETC, we gathered data on the following categories: Management fees, bid-ask-spreads, assets under management, age, issuers, commodity sectors, single versus broad-based ETCs, investment strategies, replication methods, and collateralization. Tables 1 and 2 provide a summary of our database for the categorical and the metric variables, respectively.

3.2 Methodology

In accordance with Tzvetkova (2005), due to the unique features of ETCs—and ETPs in general—their assessment as suitable investment vehicles to gain exposure to the underlying has two aspects. The first is usually measured by the tracking error (TE), which indicates how well the ETP’s assets replicate the underlying benchmark (see e.g. Frino and Gallagher 2002; Engle and Sarkar 2006). The TE is predominantly determined by the way the ETC is set up and the execution skill of the management.

The second aspect is pricing efficiency. It measures how efficient the secondary market prices the ETC. Shares of an ETC can be bought (or created) on the primary market in exchange for its NAV per share and are basically—through the redemption mechanism or at termination or maturity—claims to the NAV per share. Consequently an ETC’s fair value, and thus the comparison price for pricing efficiency is given by its NAV.

While both aspects are important, this study is concerned with the second aspect, which especially for ETCs deserves special attention. The reason for this is found in the way most ETCs are structured. For physically replicated ETCs—all of which are ETCs on precious metals or chopper—shares are created or redeemed in exchange for the physical underlying and thus ETCs do not engage in trading for tracking purposes (ETFS Metal Securities Ltd. 2016). As a consequence the NAV will always equal the underlying’s spot price after fees, which is exactly the benchmark for these types of ETCs.

Then there are synthetically replicated ETCs that track their benchmark with the help of derivatives. For many of these ETCs (e.g. the largest synthetic ETC in our sample, the ETFS Agriculture, cf. ETFS Commodity Securities Limited 2016) the issuer enters into a swap agreement guaranteeing that on creation and redemption of ETC shares swap positions with predetermined conditions are automatically opened and closed. As in the case of physical replication, there is no actual tracking activity required. Therefore, the NAV equals the accumulated cash flows from the swap position, which is contractually specified to equal the benchmark.

Summing up, as the tracking error between the NAV and the underlying can be regarded as a minor issue for ETCs, we identify pricing efficiency as the primary concern for investors looking to participate in the commodity markets via ETCs.

Premium/discount analysis The objective of our study is to determine the daily pricing efficiency of ETCs before we identify potential factors influencing the pricing of ETCs in the German market. Therefore, we first apply specific quantification concepts that are able to measure potential differences between the price (yield) performance of ETCs and their respective benchmarks.

Consistent with past research on ETFs (e.g. Elton et al. 2002; Jares and Lavin 2004; Charupat and Miu 2011; Aber et al. 2009) and ETNs (e.g. Diavatopoulos et al. 2011; Aroskar and Ogden 2012), we measure the daily price deviations using PD analysis. In accordance with Aber et al. (2009), the relative price deviations are calculated for each ETC as follows:

where \(\pi _{t}\) is the ETC’s price deviation on day t, \(P_{t}\) is the midprice on day t, and \(\mathrm {NAV}_{t}\) is the official net asset value on the same day t. When this deviation is positive (negative), the ETC is traded at a premium (discount). In case of \(\pi _{t}=0\), the pricing is perfect and, thus, the creation/redemption process does not allow arbitrage opportunities. The PD analysis serves well as a first indicator of the pricing deviation but due to its limited interpretation further methods must be implemented for a more thorough analysis.

Quadratic and linear pricing efficiency analysis The quadratic and linear pricing measures focus on return-based deviations as opposed to absolute deviations of the PD analysis (e.g. Roll 1992). We will analyze the pricing efficiency of the ETCs by means of different discrepancy measurement called the pricing efficiency (PE) methods. In general, the methods aim to reflect the extent to which a security’s price deviates from its target value over a certain period of time (e.g. Frino and Gallagher 2002) and may be regarded as a form of quality measurement of a security. They are not only commonly used for a posteriori analysis of pricing and tracking errors, but also for tracking error minimization (see e.g. Rudolf et al. 1999; Gharakhani et al. 2014 in the context of index tracking). Therefore, we choose these measures over different methods, like regression approaches (e.g. Shin and Soydemir 2010).Footnote 6

The quadratic pricing masures have been heavily discussed in the academic literature and been implemented in the expression of various statistical forms (e.g. Roll 1992; Ammann and Tobler 2000). Consistently with Ammann and Tobler (2000) we implement the pricing error volatility as the square root of the non-central second moment of the deviations in the framwork of quadratic pricing methods. As a first pricing measure, we define the pricing error volatility \(\text {PE}_{\text {VOL}}\) as:

where \(R_{P,t}\) denotes the log return of the ETC’s midprice in period t, \(R_{B,t}\) the log return of the NAV as benchmark B in period t, and T the sample size.

This quadratic error definition is the most common quadratic pricing error in the academic literature due to its advantageous statistical properties. The \(\text {PE}_{\text {VOL}}\) reflects both random positive or negative deviations and a constant under- or outperformance of the underlying index. However, Rudolf et al. (1999) criticize the fact that Eq. (2) is difficult to interpret from an investor’s perspective and does not reflect investment objectives in an adequate way. Therefore, they suggest four linear error definitions as being more appropriate alternatives for the purpose of exemplifying an investor’s risk attitude. The proposed alternative definitions are based on absolute deviations between the security’s price and its target value instead of squared deviations. In addition, these pricing errors provide both consistency with expected utility maximization and explicit solutions. Considering all these benefits, we apply the following four linear pricing models in our empirical analysis. The \(\text {PE}_{\text {MAD}}\) captures the mean absolute deviations of the ETC’s mid-price and its NAV by calculating the average of the absolute deviations between the mid-price returns and the NAV returns as follows:

where \(R_{P,t}\) is the log return of the ETC’s mid-price in period t, \(R_{B,t}\) the log return of the NAV as benchmark B in period t, and T the sample size.

The \(\text {PE}_{\text {MAX}}\), as our second linear pricing error, method focuses on the maximum deviation between the return differences and can be expressed as:

The measure \(\text {PE}_{\text {MAX}}\) characterizes a worst-case-scenario in which greater deviations are to be expected compared to the two other PE concepts. Obviously, \(\text {PE}_{\text {MAD}}\) and the \(\text {PE}_{\text {MAX}}\) are symmetrical pricing error methods as neither distinguish between positive and negative deviations by only calculating absolute values. However, investors may also be interested in assessing the downside risk, i.e. the risk of mid-price returns being below the NAV returns. Consequently, we use two asymmetrical linear models as analogs to \(\text {PE}_{\text {MAD}}\) and \(\text {PE}_{\text {MAX}}\), but with a restriction to negative deviations. For a proper notation, we define the set of all instants of time at which the return deviation is negative, i.e. \({{\mathcal {N}}}:= \{t|R_{P,t}<R_{B,n}\}\) with cardinal number \(N:=|{{\mathcal {N}}}|\)

The \(\text {PE}_{\text {MADD}}\) is the mean absolute downside deviation, i.e. deviations where the mid-price returns are less than the NAV returns, by the following formula:

Analogously, \(\text {PE}_{\text {MAXD}}\) is defined by:

We will use the two abbreviations MeMs, short for mean-based measures (\(\text {PE}_{\text {VOL}}\), \(\text {PE}_{\text {MAD}}\) and \(\text {PE}_{\text {MADD}}\)) and MaMs, short for maximum-based measures (\(\text {PE}_{\text {MAX}}\) and \(\text {PE}_{\text {MAXD}}\)).

4 Regression variables and hypotheses

Unlike other studies, we do not confine ourselves to measuring the different pricing error measures for all of the examined ETCs and listing the results in a table. In aiming to identify determining factors influencing the pricing efficiency, we go one step further. To this end, we regress all five pricing error measures of every one of the 237 ETCs—each calculated over the whole available time series—on several explanatory variables. These are operational ETC characteristics and general market factors comprising management fees, bid-ask-spreads, market share of assets under management, age, issuers, commodity sectors, single versus broad-based ETCs, investment strategies, replication methods, and collateralization forms. All of them could have an influence on pricing efficiency. Therefore, we formulate nine hypotheses (numerated H1 through H9), proposing expectable relationships of the explanatory variables on the pricing error measures. As many of the variables are categorial (with, say, c categories), we use the standard approach of setting up \(c-1\) dummy variables for each category with one value being the reference category.

4.1 Costs

The cost analysis of ETCs plays a vital role in the investment decision of investors. ETCs as passive financial instruments are a relatively simple and inexpensive means of participation in the commodity markets compared to other products. On the contrary, a physical acquisition of commodities, if at all feasible, involves substantial costs due to storage, transportation and insurance and commodity futures are associated with considerable margin and rollover costs. Due to their passive investment structure, ETCs limit management costs for complex analysis tasks as well as transaction and distribution costs. Depending on the particular structure of the ETC, different cost components are to be distinguished and the individual investor may incur both direct and indirect costs.

One type of direct primary cost applying to all ETC structures is the management fee which covers management and administrative services of the issuer. These costs are often incorrectly stated as total expense ratios (TER), a term summarizing all cost components of ETFs. Since the management fee is to be specified explicitly in the issuers’ publications and prospects and is applicable to all ETC products, it represents an appropriate basis for comparison. The management fee indicated as an annual percentage fee is deducted in equal parts from the ETC assets and varies according to different products and issuers. Besides these costs, physical ETCs may charge fees for storage and custody whereas derivative-based ETCs carry swap, collateral, index or licensing costs. However, these cost components are variable over time and, thus, often not clearly defined by the issuer. In addition to these primary costs, transaction feesFootnote 7 may be levied in the acquisition or selling process by brokers, custodian banks, or states. Some issuers charge varying ancillary fees for the creation and redemption of ETC units which are not applicable to investors in the secondary market and exchange markets. These fees increase if predefined threshold values of ETC units are not reached and are usually higher for the redemption than the creation of new shares.

Thus, the average annual management fees provide a proper basis for the cost analysis of ETCs as they are incurred for all products and are to be reported explicitly by the issuers. In our sample, management fees are rather low (with a median value below 5%, cf. Table 2), with a tendency of lower values for plain vanilla ETCs. Therefore, we can view management fees as a proxy for the exoticness of the respective ETC as they are positively correlated with the effort in product management.

Moreover, in their analyses of ETF tracking errors, Chu (2011) and Rompotis (2011b) find a negative influence of management fees on pricing efficiency. The perspective taken above leads us to the same conclusion. Our first hypothesis (H1) conjectures a negative influence of management fees on the pricing efficiency because with more complex products arbitrage opportunities are harder to exploit, which is essentially a basic transaction costs argument.

4.2 Spread

Despite their difficult determination, indirect or implicit costs in the form of bid-ask spreads are also important in the cost analysis. We calculate the average relative bid-ask-spreads as the mean of the differences between the daily closing ask and bid prices divided by the closing mid prices.

Amihud and Mendelson (1991) interpret the bid-ask spread as a measurement of liquidity or, to be more precise, as the cost of immediate execution. The spread calculated between the ask (offer) and bid (sell) prices are to be as tight as possible and significantly influence the asset return. The bid-ask-spreads represent transaction costs imposed by market makers, which may negatively affect pricing. Delcoure and Zhong (2007) emphasize that higher bid-ask spreads could harm the effectiveness of the creation/redemption process by making arbitrage activities less attractive. In contrast, Buetow and Henderson (2012) use another variable as proxy for second market liquidity, namely ETF trading volumes, and also find a negative effect on the magnitude of tracking errors.

Therefore, we hypothesize a positive effect of the relative spread on the magnitude of pricing errors (H2).

4.3 Market share of assets under management (AUM)

Based on quarterly AUM data of all 276 listed ETCs, also extracted from Bloomberg, we calculate the quarterly market share of each ETC, by dividing the ETC’s AUM by the sum of all ETCs’ AUM. This number is then averaged over all quarters of the considered time period. We choose market share as dependent variable in the sense of the relative AUM, to exclude the influence of the rapid overall growth of the ETCs market in terms of AUM, from 0 in 2006 to EUR 23.1 billion in the second quarter of 2012.

A higher market share is expected to indicate a more mature, possibly more liquid, and above all more lucrative market for a potential arbitrageur. This effect can be explained by the fixed costs of implementation and monitoring, which are independent of the size of the market. This economies of scale argument is also used by Buetow and Henderson (2012) and Chu (2011), who suggest that ETF fund size has a positive effect on pricing efficiency.

Thus, our third hypothesis can be stated as follows: the relative AUM market share has positive effect on pricing efficiency (H3).

4.4 Age

The age, measured as the time in years between the initial trading date of the relevant ETC and the end of the investigation period, is used as a proxy for the age of a product and its market maturity.

To explain the overpricing of structured products in the German market, Wilkens et al. (2003) propose a life cycle hypothesis, conjecturing “that issuers orient their pricing toward the expected volume of purchases and sales.”. It is indeed confirmed by numerous studies that overpricing is highest at initiation when the products are sold by the issuers and vanishes over the lifetime of the product, or even becomes negative, when the product is sold back to the issuer. ETFs are open ended, yet it is still expected that excess demand creates overpricing for younger products and we conjecture the variable to have a negative relationship with the mean based pricing errors (H4).

This reasoning cannot be applied to MaMs, which monotonically increase with the number of observations. Thus, we expect the opposite effect, in which age has a positive influence of the magnitude of the (maximal) pricing errors (H5).

4.5 Single-commodity versus broad-based ETCs

Through the usage of ETCs, investors gain exposure to one single commodity or to a basket of multiple commodities. Taking a position in single-commodity ETCs allows investors to invest in certain commodity markets without having to adhere to a certain level of diversification to meet regulatory requirements as is the case with ETFs. In addition, single-commodity ETCs are often used for short-term investment strategies and require a precise knowledge about the opportunities and risks associated with the respective commodity. By contrast, broad-based commodity ETCs offer the possibility of diversified investments in all commodity sectors, in combinations of commodity sectors, and in combinations of two or more or even all commodities of a sector through one single trade. These types of ETCs are more suitable for long term investment motives.

Single-commodity ETCs only replicate one underlying commodity whereas broad-based ETCs cover two or more commodities. Therefore, single-commodity ETCs may incur smaller replication costs compared to broad-commodity ETCs. In contrast, for structured products with equity underlyings, Stoimenov and Wilkens (2005) expect the opposite effect, as indices can have a more liquid derivatives market compared to single stocks. Even if the liquidity argument cannot be transferred to ETCs in general, there can be effects that make replication of broad underlyings less costly, namely lower volatility and lower average roll-yield effects due to diversification.

As it is possible for each of both effects to dominate the other, we conjecture an effect of the variable on the pricing efficiency (H6), but we do not have an ex-ante expectation on the direction.

4.6 Investment strategies

With regard to investment strategies, investors implement long, short, leveraged long, and leveraged short positions with or without currency hedging through the acquisition of ETCs. A long ETC, the simplest and most intuitive type of ETC, closely tracks the daily performance of its underlying. As with stocks, investors generate profits if the underlying’s prices rise and, vice versa, losses if prices fall. Forward long ETCs, whose underlying are composed of longer-maturity forwards, are counted among the long-investment products as well. Short ETCs as counterparts to long ETCs are aimed to reflect the daily performance change of the respective underlying times minus one and, thus, behave inversely to their target benchmarks. Consequently, an investor profits from falling prices and loses in case of increasing prices.

However, the losses are limited to the amount invested, constituting a major difference to the classical short sale transactions with theoretically uncapped losses.

Leveraged long and leveraged short ETCs are relatively new types of ETC investments and are more suited to risk-taking investors for the purpose of speculating or hedging. A leverage of two to four leads to an above-average participation in value changes of the underlying on a daily basis.

For longer holding periods than one day the realized return does not necessarily correspond with the indicated leverage over the same period. As with short ETCs, the potential losses are limited to the investment total which illustrates a significant advantage of ETCs.

We propose that the investment strategies may also play a crucial role as determinants of the pricing error. Leung and Ward (2015) find that leveraged ETFs have significant tracking errors stemming from imperfect replication (they give an improved tracking performance by dynamic portfolios of futures). Moreover and Guo and Leung (2015) postulate the so called volatility decay, arising due to the convexity of the ideal leveraged underlying. Extending this argumentation, we expect the greater difficulty in performing leveraged and short strategies and the associated higher costs, to have a positive impact on the magnitude of the pricing errors (H7). In our regression models, the investment strategy Long serves as a reference category.

4.7 Replication methods

As passive financial instruments, ETCs use either a physical or synthetic approach to replicate the underlying benchmark accurately. Physical replication is achieved by buying the physical commodities or the securities of the relevant index. Physical ETCs often relate to spot prices of commodities or commodity baskets of precious metals, such as gold or silver, as they are relatively homogeneous, easy to standardize, and non-perishable. In comparison, the physical replication is less frequently applied in other commodity sectors as these investments are largely either unprofitable due to storage, transportation and insurance costs, or practically unimplementable. Ramaswamy (2011) emphasizes that the physical replication strategy can prove to be very costly especially in case of less liquid or broad-market underlyings with a daily change in their composition.

As a result, synthetic replication strategies are often employed to minimize costs and deviations from the underlying benchmark. In contrast to holding the underlying commodities directly, these derivative-based ETCs adopt both total return swaps and futures to gain exposure to their target commodities. The synthetic approach is usually effected by means of bilateral total return swap contracts in which generally the two parties exchange the total return of two designated financial instruments. At maturity, the ETC issuer transfers not only its assets in the form of cash or baskets of securities, which significantly deviate from the composition of the underlying benchmark to the swap counterparties but also the risk of deviations from the benchmark. The swap counterparties, which are often parent companies of the ETC issuer, in return transfer the respective total return of the ETC underlying for a given nominal exposure.Footnote 8 The daily offsetting of the swap transactions aims to mitigate the incurring exposure risk. Besides an issuer risk, the ETC investor bears a counterparty risk which describes the risk of insolvency of the swap counterparty.

An alternative synthetic replication method involves the use of futures contracts. Here, the ETC issuer acquires or sells futures contracts from a third party when units of ETCs are created or redeemed. This ETC structure can be found in the energy sector, in which the third parties are multinational oil companies with direct exposure to the relevant commodity and try to hedge their risk through the trading of futures.

The synthetic replication method is marketed by issuers as the superior replication method for tracking error minimization. Consequently, Fassas (2014) hypothesizes higher pricing efficiencies for synthetically replicated ETFs. However, he cannot confirm this statistically, possibly due to his small data set, which is less comprehensive than ours. Therefore, we expect a negative relation between the synthetic replication dummy and pricing efficiency (H8).

4.8 Collateralization

Due to their structure as debt notes, ETCs are subject to issuer credit risk. Issuers are special purpose vehicles (SPVs), corporations in the form of a limited liability company or a limited partnership, which are created for the sole purpose of issuing ETCs and are normally not rated by external rating agencies. Hence, ETCs are collateralized by physical holdings, securities pledging, or coverage by an independent third party to reduce the risk of an issuer’s insolvency whereas only few ETCs dispense with collateral. For comparison with other exchange-traded products, ETFs are structured as funds whose assets invested are not part of the liquidation assets in the event of an issuer’s bankruptcy. ETNs as debt notes are only backed by the credit-worthiness of their issuers which are mostly big financial institutions and hold more types of debt obligations.

One popular ETC structure comprises the collateralization through physical holdings, such as precious metals which are simple to be stored, standardized and associated as safe investments by investors. The posted collateral (e.g. gold, silver, or platinum) is equal to at least 100% of the value of the issued ETC units calculated on each business day. They are stored in a certificated vault of an eligible custodian and regularly audited in terms of available amounts or compliance with quality standards at the issuer’s discretion. Furthermore, an independent security trustee receives a primary security interest and is allowed to take control of the vault in the case of a credit event. The investors themselves only have a limited right of recourse and may incur losses in the event of insolvency.

The collateralization by securities is based on the pledging of stocks, cash, money market funds, or fixed-income securities with excellent credit ratings. These are transferred to a pledge account of a custodian and safeguarded by an independent trustee. In addition, the collateral is subject to a daily mark-to-market evaluation ensuring that their target value reflects the value of the issued ETC units plus a security surcharge of up to 10%. If the collateral value is less or certain collateral criteria are not met, the issuer will be requested to deposit additional funds. However, the pledging of securities is more risky for investors as the posted collateral may become worthless in extreme market conditions or not cover all liabilities due to changes in asset values.

A less common type of collateralization is the coverage by an independent third party with best credit ratings. The eligible collateral targeting at least 100% of the issued ETCs fulfills the same requirements as before with the sole exception of bearing the credit risk of the third party.

The explanatory variables collateralization by securities, physical collateralization as well as collateralization by third parties are included as dummies to explicate the pricing of ETCs whereby the lack of collateralization is regarded as reference category. On the one hand, positive coefficients of the three explanatory variables could be expected due to higher costs related to the collateralization of securities. On the other hand, a lack of collateralization could also lead to negative return deviations in case of worse credit situations. As both assumptions are reasonable, we take both scenarios into account and test the effect in the following analyses (H9).

4.9 Regression model

In order to test the different hypotheses simultaneously, we estimate a multiple linear regression model using ordinary least squares (OLS) for each of the five different dependent variables \(\text {PE}_{\text {VOL}}\), \(\text {PE}_{\text {MAD}}\), \(\text {PE}_{\text {MAX}}\), \(\text {PE}_{\text {MADD}}\), and \(\text {PE}_{\text {MAXD}}\).

Out data set comprises products from six different issuers, whose dummy variables are used as control variables. The issuer with the highest AUM value is used as reference category. Moreover, we also control for the commodity sector and set cross-sectional as reference category, i.e. those ETCs that track price changes across all commodity sectors.

The regression equation for each dependent variable \(Y \in \{\text {PE}_{\text {VOL}}, \text {PE}_{\text {MAD}}, \text {PE}_{\text {MADD}}, \text {PE}_{\text {MAX}}, \text {PE}_{\text {MAXD}} \}\) takes the following form:

for ETC number \(j\in \{1, \ldots , 237 \}\).

To test the significance of the regressors we use t-statistics adjusted for heteroskedasticity by White (1980).

5 Empirical analysis

In this section, we first present the results of the PD analysis as well as the quadratic and linear pricing analysis, from which we deduce the pricing efficiency of ETCs in the German market. In particular, the analysis of the quadratic and linear pricing measures plays a substantial role for the subsequent investigation of potential factors influencing the price deviations of ETCs and is therefore considered in more detail.

5.1 Premium/discount analysis

Table 3 reports upon the summary statistics for the PD analysis using daily figures of the data sample of 237 ETCs during the investigation period from 04 November 2006 to 25 July 2012. For each ETC, we calculate the mean of the price deviations between the mid-prices and the NAVs according to Eq. (1) as well as its standard deviations using the entire available corresponding times series. Then, we compute the fraction of days with premiums, i.e. positive deviations over the entire data history of each ETC.

The mean price deviation of the data sample is 0.09% implying that the ETCs on average trade at a premium. The maximum positive price deviation is 4.69% while the maximum negative price deviation is \({-0.41\%}\). On average, the standard deviation of all ETCs is 0.95% which ranges from 0.15 to 3.78%, implying relatively large and greatly fluctuating price deviations. These results are only in part consistent with those of the previous literature on ETPs. Charupat and Miu (2011) suggest the existence of large price deviations and price volatilities based on higher results in their analysis of eight ETFs. However, Kayali and Ozkan (2012) determines, in his analysis, an average price deviation of −0.8% whereas Elton et al. (2002) note a mean discount of −0.018%. We find that half of the ETCs traded at a premium over their NAVs for at least 53.7% of the time. This is consistent with the life cycle argumentation of Wilkens et al. (2003) (see also Sect. 4.4).

5.2 Quadratic and linear pricing efficiency measures

Next, we calculate the quadratic and linear pricing error measures introduced above. Table 4 displays the summary statistics for the whole sample of 237 ETCs measured over the whole investigation period. It provides the mean, the standard deviation, the minimum, and the maximum pricing error size.

For \(\text {PE}_{\text {VOL}}\), the mean of the pricing error of the sample is 1.29% with a standard deviation of 0.86%. Considering the range of the sample, we detect significant differences as the minimum within the sample is 0.21% and the maximum is 5.54%. The mean absolute deviation \(\text {PE}_{\text {MAD}}\) shows a lower mean pricing error of 0.90% with a standard deviation of 0.62%. In addition, the pricing deviations vary from a minimum of 0.17% and a maximum of 4.01%, indicating a tighter range within the sample. Considering \(\text {PE}_{\text {MAX}}\) as extreme value analysis, the sample average of all maximum deviations between the price and the NAV is 6.98% and a standard deviation of 4.40%, whereby the extreme values fluctuate between a minimum of 0.59% and a maximum of 23.90% in the sample.

A comparison of the preliminary results shows that the lowest values occur with \(\text {PE}_{\text {MAD}}\) followed by \(\text {PE}_{\text {VOL}}\) and \(\text {PE}_{\text {MAX}}\) as previously expected. The results for \(\text {PE}_{\text {MADD}}\), depicting restriction to negative price deviations reveals a great similarity to the findings of \(\text {PE}_{\text {MAD}}\). Only the maximum value of 4.74% is slightly higher. From this, we can infer that a multitude of ETCs are likely to trade at negative pricing deviations from their NAVs. This view is consistent with Tzvetkova (2005) and Kayali and Ozkan (2012) who also report similar results in their analysis of ETFs. When looking at \(\text {PE}_{\text {MAXD}}\), the daily pricing errors for the \(\text {PE}_{\text {MAXD}}\) are comparatively lower than those of the \(\text {PE}_{\text {MAX}}\). Furthermore, all results are statistically different from zero at the 1% level.

In summary, we state that the pricing of ETCs in the German market is far from being efficient according to the different PE measurement concepts.

Table 5 provides detailed results of the five pricing error measurement concepts in differentiation of various product characteristics, such as issuers, commodity sectors, single-commodity versus broad-commodity, investment strategies, replication methods and collateralization. We conduct an analysis of variance (ANOVA) by the F-test of Welch (1951) in order to test the differences between two or more means of the analyzed characteristics.

The results of \(\text {PE}_{\text {VOL}}\) are almost identical to \(\text {PE}_{\text {MAD}}\) and \(\text {PE}_{\text {MADD}}\) when scaled appropriately. To make the remaining differences between them visible, we include a version of the \(\text {PE}_{\text {MAD}}\) means scaled by \(x = \hbox {Mean}(\hbox {PE}_\mathrm{MAD}) /\hbox {Mean}(\hbox {PE}_\mathrm{VOL}) = 0.70\). Furthermore, due to the similarities among the measures, we focus on the differences between MeMs and MaMs—as introduced on Page 12.

In the issuer category we determine differences between the means of the six institutions issuing ETCs at the 0.1% level for all measures. Furthermore, all measures give consistent results, with Issuers 1 and 6 showing the highest errors throughout. The MaMs are higher and show smaller relative differences between the issuers—as is expected.

When differentiating between commodity sectors, all measures show almost identical order. The lowest pricing error is found for cross-sectional ETCs, the highest being energy for MeMs and agriculture for MaMs. The differences in the group means for the different sectors are again highly significantly different at the 0.1% level, with the exception of \(\text {PE}_{\text {MAX}}\) at 1% and \(\text {PE}_{\text {MAXD}}\) at 5%.

The differences between issuers and sectors underline the importance of including them as control variables in our regression model.

In view of single-commodity or broad-commodity ETCs, we note higher pricing errors for single-commodity ETCs than for broad-commodity ETCs under all five measures at the 0.1% significance level. This result provides further insights on our hypothesis H6 regarding the direction of the influence of the variable and is consistent with the fact that cross-sectional ETCs—which are by definition broad-commodity—also show the lowest errors.

Considering investment strategies, lower price deviations occur for short, long and with a certain gap for leveraged long followed by leveraged short. These results are consistent over all five measures and are further supported by the applied ANOVA, which indicates a systematic difference between the group mean values of the various investment strategies at the 0.1% level. This can be viewed as first supporting evidence in favor of H7, but only for the leveraged strategies.

Synthetic replication has lower pricing errors than physical replication for all pricing methods except for \(\text {PE}_{\text {MAXD}}\). While the results are in line with our hypothesis H8, the differences of the means are not statistically significant.

With regard to the type of collateralization, all measures induce a similar ranking, where no collateralization shows the smallest pricing errors. The ANOVA analysis indicates significant differences among the group means at the 0.1% level. This gives support to our hypothesis H9, that cost savings due to a lack of collateralization improves pricing efficiency.

Overall, these results show that all five measures give qualitatively similar answers that are consistent with our hypotheses, except in the case of single-commodity ETCs.

5.3 Regression analysis

The main findings of our analysis can be found in Table 6, which presents the results of the OLS regression models based on Eq. (7). It shows the determinants of the pricing efficiency of ETCs in the German market and is used in the following to assess the hypotheses of Sect. 4. The dependent variables of the five different regression models are the quadratic and linear pricing measures of the dataset, while the independent variables are the different product characteristics described above.Footnote 9 The significance of the independent variables is tested by t-statistics adjusted for heteroskedasticity by White (1980).

The overall explanatory power is satisfactory, with adjusted \(R^2\) in the range of 45–61%, and is the highest for \(\text {PE}_{\text {MAD}}\), \(\text {PE}_{\text {MADD}}\), closely followed by \(\text {PE}_{\text {VOL}}\) and then \(\text {PE}_{\text {MAXD}}\) and \(\text {PE}_{\text {MAX}}\). This order is to be expected for the outlier-driven MaMs. As in the previous section all measures show comparable results and Table 6 again includes a scaled version of \(\text {PE}_{\text {MAD}}\) for better comparison with \(\text {PE}_{\text {VOL}}\).

Corroborating the hypothesis H1, the management fee has a positive effect and is significant at the 1% level on MeMs and only at the 10% level for MaMs. In the case of \(\text {PE}_{\text {VOL}}\), a coefficient of 0.91 implies that a 1 bps change in management fees will lead to an almost equal change in the pricing error volatility. This is in accordance with the findings from Chu (2011) and Rompotis (2011b).

As was expected by H2 and also seen by Delcoure and Zhong (2007), the bid-ask spread shows a 0.1%-significant influence across all five dependent variables, with coefficients around 0.2 for MeMs and between 1.1 and 1.5 for MaMs.

The expected dependence on the AUM market share (H3) is also observed, in accordance with the results of Buetow and Henderson (2012) and Chu (2011). The coefficients are significant at the 1% level, expect for for \(\text {PE}_{\text {MAD}}\) and \(\text {PE}_{\text {MADD}}\), whose coefficients are closer to zero and do not follow the usual linear relationship with \(\text {PE}_{\text {VOL}}\). For MaMs the coefficients are below \(-17\), indicating a strong dampening effect of outliers for large ETCs. For example, the largest ETC’s market share of 23% explains the 4.3 p.p. increase in pricing efficiency measures by \(\text {PE}_{\text {MAX}}\) when compared to the smallest ETCs.

The positive coefficient of the variable age does not confirm our expectation (H4) and thus also deviates from the life cycle hypothesis and results of Wilkens et al. (2003). The positive coefficient indicates that newer products have a better pricing efficiency than older ones. This may be attributed to the fact that newer products have to cope with great market competition and, thus, try to perfectly replicate the NAVs in their pricing. It should, however, be noted that it is not significantly different from zero for \(\text {PE}_{\text {MAD}}\) and \(\text {PE}_{\text {MADD}}\) and only at a 5% level for \(\text {PE}_{\text {VOL}}\).

Our hypothesis H5 conjecturing a positive coefficient for the variable age for MaMs can be confirmed at the 0.1% significance level. The magnitude of the highest observed pricing error grows 0.86 p.p. per year on average. It should be noted, however, that this effect might be offset by growing AUM.

Hypothesis H6 can be confirmed. As in the previous section, single-commodity ETCs have higher pricing errors compared to broad-commodity ETCs—in analogy to the results of Stoimenov and Wilkens (2005). Except for \(\text {PE}_{\text {MAD}}\), this effect is significant at or below the 1% level.

The results of the regression analysis evidence the same effect as in Leung and Ward (2015), and thus confirm our hypothesis H7 concerning leveraged investment strategies. However, no significant effect can be found for short, which suggests that it is the leverage effect which causes price deviations.

Hypothesis H8 is supported only for MeMs and only at the 5% level. The \(\text {PE}_{\text {MADD}}\) measure has a coefficient closer to zero, while being more significant (at the 1% level). This indicates that when only negative deviations are considered, synthetic replication exhibits consistently higher pricing efficiency than physical replication. This result confirms the expected increase in explanatory power over the results of Fassas (2014), who did not find statistical evidence for the hypothesis, possibly due to a smaller sample size.

A negative coefficient for the variable collateralization by securities confirms hypothesis H9 at the 1% level. The pricing efficiency benefits through reduced risk seems to dominate the higher costs associated with collateralization by liquid securities with highest credit quality.

The control variables show significant effects on both groups of measures, except for the sector, which has no significant effects on the MaMs. As one example take Issuer 6, whose ETCs have on average more than one additional percentage point of pricing error volatility compared to ETCs from Issuer 1. Further research is needed to identify drivers of these effects which are not explained by our hypotheses.

Compared to the reference category of cross-sectional ETCs, which were the clear leader in the previous section, the other sectors now show both positive and negative coefficients. The higher pricing efficiency visible in Table 5 now seems to be explained by the broad-commodity variable, as conjectured above.

Summarizing the differences between MeMs and MaMs, the results show the expected age dependence of the MaMs, some effects are missing in the sector and the replication coefficients are quite significant for the MeMs.

The regression results corroborate seven of our nine hypothesis and only partly our hypothesis on the effect of investment strategy (H6). They can not confirm our hypothesis on the effect of age (H4).

5.4 Robustness test

In order to test the robustness of the regression results, we split up the observation period into two sub-periods before and after the 1 October 2010, respectively. Then, for each of the two sub-periods, we perform regression analyses for the five pricing efficiency measures, based on the subset of prices and NAV values from the respective date range. ETCs that have no valid data reported within a sub-period are excluded from that sub-sample’s regression.

The regression results for the first period are given in Table 7. It shows consistent results among the five measures and deviates from the full range regressions only moderately. To be more precise the following can be stated: Management fee shows no significant effect. The control variables issuer, and sector show differing significant effects, except for energy, which again has a significantly positive coefficient. The effect of synthetic replication is missing, instead there is a significantly positive coefficient for physical collateralization. Adjusted \(R^2\) is slightly smaller, e.g. at 0.52 compared to 0.57 for \(\text {PE}_{\text {VOL}}\). These differences can be explained by the fact that there are 64 ETCs missing that were present in the full regression, including all ETCs of issuer 6 and all leveraged short ETCs.

The second sub-period (cf. Table 8), which includes 231 ETCs, gives results that are much closer to the full range regressions. They differ only in the following item: The positive coefficient for age is now significant and AUM market share is no longer significant, except for \(\text {PE}_{\text {MAX}}\). The coefficient of issuer 5 is now also significantly different from zero and the effects concerning the investment strategy are now less significant. For this sub-period, the adjusted \(R^2\) is even higher, e.g. to 0.59 for \(\text {PE}_{\text {VOL}}\).

All other effects as well as the signs and magnitudes of the coefficients are reproduced in the sub-periods. Consequently, this test confirms the robustness of our main findings.

6 Summary and conclusion

This study investigates ETCs, a very successful recent financial innovation, from an empirical perspective. ETCs are an important exchange-traded product enabling all kinds of investors to participate in commodity markets and have experienced considerable growth in both popularity and assets under management since their inception. However, as the field is still under-researched, this is the first examination of ETCs and their pricing efficiency in the euro marketplace with a special focus on the German market, which is the biggest ETC market in terms of product availability, assets under management, and turnover.

Our empirical examination of the pricing efficiency of 237 ETCs listed in the German market utilizes different measures. This study is not only unique concerning its focus on the German, or more generally the euro market, but also in the size of our dataset which is by far the largest in the ETP literature so far and allows a representative analysis since the start of the German ETC trading. We concentrate on the daily pricing deviations between the mid-prices of ask and bid prices and the theoretical fair values in form of the net asset values calculated in euro.

The measures employed include the premium/discount analysis based on prices and the pricing errors based on returns and result in the following findings: First, the ETCs incur, on average, pricing deviations in their daily trading. They are also more likely to trade at a premium from their theoretical fair prices. These outcomes are also supported by the five symmetrical pricing error measures, which provide deeper insight in the magnitude of deviation by alternate interpretation models.

Second, we use the pricing error measures as dependent variables in our regression analysis to find potential contributors to the pricing errors of ETCs. The results imply that a set of several variables influences pricing efficiency and thereby confirm seven out of nine of our hypotheses, namely those on management fee, spread, AUM market share, single- versus broad-commodity, replication and collateralization. Mixed significance is found for investment strategy. No significant effects are found for our hypothesis on age.

Both the mean-based and the outlier driven maximum-based measures give comparable results. However, the observable and expected differences imply that the former is slightly better suited to assess the pricing efficiency of ETCs in the German market and slightly better explainable by economically relevant determinants.

ETCs as a passive, simple, and cost-effective financial innovation are likely to grow in investors’ interests. For example, they are likely to play an important role in private pension plans due to their advantageous characteristics. However, the prosperous outlook of ETC investing is limited by the potential systemic risks arising from extensive passive investing and its influence on the commodity markets, the stock markets, and the whole economy.

Hence, the ETC pricing problem is of considerable importance and interest to private and institutional investors and may be extended in a global analysis. Another potential extension of our study is to derive concrete trading opportunities to exploit the existing pricing deviations.

Notes

The acronym UCITS stands for “Undertakings for Collective Investment in Transferable Securities” directive and is the regulatory framework for an investment vehicle that can be marketed across the European Union.

Besides a stock market trading, over-the-counter (OTC) trading may also be possible.

Thus, the APs operate as an important link between the secondary and primary market from which retail investors are usually excluded. The settlement by an independent clearing and settlement organization takes place on a normal \(T+2\) or \(T+3\) basis. In summary, a clear distinction between the primary and the secondary market including its market participants is crucial for a correct understanding of the whole ETC structure.

The above given information are provided by the German stock exchange “Deutsche Börse AG”.

We use log returns instead of simple returns which are also widespread in the context of passive financial instruments in the academic literature and in practice, as the reliance on continuously compounded returns is more valid and suitable in the context of our further statistical computations.

In our framework, it would be necessary to aggregate \(\alpha \), \(\beta \) and standard errors into one deviation measure. Since there is no straight forward way to do this, we used the more proven concepts defined above.

Brokerage commissions, market fees, clearing and settlement costs as well as taxes and stamp duties are examples of direct or explicit trading costs (see D’Hondt and Giraud 2008).

See Ramaswamy (2011) for further information.

The independent variable ’Issuer 3’ was excluded from the model for it is identical to the variable ’no collateralization’.

References

Aber JW, Li D, Can L (2009) Price volatility and tracking ability of ETFs. J Asset Manag 10(4):210–221

Amihud Y, Mendelson H (1991) Liquidity, asset prices and financial policy. Financ Anal J 47(6):56–66

Ammann M, Tobler J (2000) Measurement and decomposition of tracking error variance. Discussion paper no 2000-11

Anson MJ (1999) Maximizing utility with commodity futures diversification. J Portf Manag 25(4):86–94

Anson MJ, Fabozzi FJ, Jones FJ (2011) The handbook of traditional and alternative investment vehicles: investment characteristics and strategies. Wiley, Hoboken

Aroskar R, Ogden WA (2012) An analysis of exchange traded notes tracking errors with their underlying indexes and indicative values. Appl Financ Econ 22(24):2047–2062

Belousova J, Dorfleitner G (2012) On the diversification benefits of commodities from the perspective of euro investors. J Bank Finance 36(9):2455–2472

Bienkowski N (2007) Exchange traded commodities: led by gold, ETCs opened the world of commodities to investors. Alchem Lond Bullion Mark Assoc 48:6–8

Bienkowski N (2010) Oil futures, exchange-traded commodities and the oil futures curve. J Indexes 13(3):40–43

Bodie Z (1983) Commodity futures as a hedge against inflation. J Portf Manag 9(3):12–17

Borsa Italiana (2009) A new way of investing in commodities: ETC—exchange traded commodities. Borsa Italiana Publications

Brooks N (2008) Exchange traded commodities: commodity investing goes mainstream. Alchem Lond Bullion Mark Assoc 51:7–9

Buetow GW, Henderson BJ (2012) An empirical analysis of exchange-traded funds. J Portf Manag 38(4):112–127

Charupat N, Miu P (2011) The pricing and performance of leveraged exchange-traded funds. J Bank Finance 35(4):966–977

Chen AH, Kensinger JW (1990) An analysis of market-index certificates of deposit. J Financ Serv Res 4(2):93–110

Chu PKK (2011) Study on the tracking errors and their determinants: evidence from Hong Kong exchange traded funds. Appl Financ Econ 21(5):309–315

Delcoure N, Zhong M (2007) On the premiums of iShares. J Empir Finance 14(2):168–195

Deville L (2008) Exchange traded funds: history, trading, and research. In: Zopounidis C, Doumpos M, Pardalos P (eds) Handbook of financial engineering. Springer, New York, pp 67–98

D’Hondt C, Giraud JR (2008) Transaction cost analysis A-Z: a step towards best execution in the post-MiFID landscape. EDHEC Publications, Paris

Diavatopoulos D, Felton J, Wright C (2011) The indicative value-price puzzle in ETNs: liquidity constraints, information signaling, or an ineffective system for share creation? J Invest 20(3):25–39

Elton EJ, Gruber MJ, Comer G, Li K (2002) Spiders: where are the bugs? J Bus 75(3):453–472

Engelke L, Yuen JC (2008) Types of commodity investments. In: Fabozzi FJ, Füss R, Kaiser DG (eds) The handbook of commodity investing. Wiley, Hoboken, pp 549–569

Engle RF, Sarkar D (2006) Premiums-discounts and exchange traded funds. J Deriv 13(4):27–45

ETFS Commodity Securities Limited (2016) Prospectus for the issue of ETFS classic commodity securities. Jersey

ETFS Metal Securities Ltd (2016) Prospectus for the issue of ETFS metal securities. Jersey

Fabozzi FJ, Füss R, Kaiser DG (2008) A primer on commodity investing. In: Fabozzi FJ, Füss FR, Kaiser DG (eds) The handbook of commodity investing. Wiley, Hoboken, pp 3–37

Fassas AP (2014) Tracking ability of ETFs: physical versus synthetic replication. Index Invest 5(2):9–20

Frino A, Gallagher DR (2002) Is index performance achievable? An analysis of Australian equity index funds. Abacus 38(2):200–214

Gallagher DR, Segara R (2006) The performance and trading characteristics of exchange-traded funds. J Invest Strategy 1(2):49–60

Gastineau GL (2001) Exchange traded funds: an introduction. J Portf Manag 27(3):88–96

Gastineau GL (2010) The exchange-traded funds manual, 2nd edn. Wiley, Hoboken

Gharakhani M, Fazlelahi FZ, Sadjadi SJ (2014) A robust optimization approach for index tracking problem. J Comput Sci 10(12):2450–2463

Gorton G, Rouwenhorst KG (2006) Facts and fantasies about commodity futures. Financ Anal J 62(2):47–68

Gruber MJ (1996) Another puzzle: the growth in actively managed mutual funds. J Finance 51(3):783–810

Grünbichler A, Wohlwend H (2005) The valuation of structured products: empirical findings for the Swiss market. Financ Mark Portf Manag 19(4):361–380

Guo K, Leung T (2015) Understanding the tracking errors of commodity leveraged ETFs. In: Aïd R, Ludkovski M, Sircar R (eds) Commodities, energy and environmental finance. Springer, New York, pp 39–63

Jares TB, Lavin AM (2004) Japan and Hong Kong exchange-traded funds (ETFs): discounts, returns, and trading strategies. J Financ Serv Res 25(1):57–69

Jensen MC (1967) The performance of mutual funds in the period 1945–1964. J Finance 23(2):389–416

Johnson WF (2009) Tracking errors of exchange traded funds. J Asset Manag 10(4):253–262

Kayali MM, Ozkan N (2012) Does the market misprice real sector ETFs in Turkey? Int Res J Finance Econ 91:156–160

Kostovetsky L (2003) Index mutual funds and exchange-traded funds. J Portf Manag 29(4):80–92

Lan S, Mercado S, Levitt S (2013) 2012 ETF review & 2013 outlook: record inflows drive global ETP assets to near $2 trillion. Deutsche Bank Markets Research

Lang SE (2009) Exchange traded funds—Erfolgsgeschichte und Zukunftsaussichten. WiKu, Duisburg (i.a.)

Lehmann BN, Modest DM (1987) Mutual fund performance evaluation: a comparison of benchmarks and benchmark comparisons. J Finance 42(2):233–265

Leung T, Ward B (2015) The golden target: analyzing the tracking performance of leveraged gold ETFs. Stud Econ Finance 32(3):278–297

Lin A, Chou A (2006) The tracking error and premium/discount of Taiwan’s first exchange traded fund. Web J Chin Manag Rev 9(3):1–21

Malkiel BG (1995) Returns from investing in equity mutual funds 1971 to 1991. J Finance 50(2):549–572

Mankiewicz C (2009) Aktives vs. passives Management von Commodity/Investments—Sind passive Indexinvestments der geeignete Ansatz für Pensionskassen? e-J Pract Bus Res, Sonderausgabe Performance (01/2009), pp 1–26

Muck M (2006) Where should you buy your options? The pricing of exchange-traded certificates and OTC derivatives in Germany. J Deriv 14(1):82–96

Plante JF, Roberge M (2007) The passive approach to commodity investing. J Financ Plan 37(4):66–75

Ramaswamy S (2011) Market structures and systemic risks of exchange-traded funds. BIS working paper no 343, pp 1–17

Roll R (1992) A mean/variance analysis of tracking error. J Portf Manag 18(4):13–22

Rompotis GG (2008) Performance and trading characteristics of German passively managed ETFs. Int Res J Finance Econ 15:218–231

Rompotis GG (2011a) Active vs passive management: new evidence from exchange traded funds. Int Rev Appl Financ Issues Econ 3(1):169–186

Rompotis GG (2011b) Predictable patterns in ETFs’ return and tracking error. Stud Econ Finance 28(1):14–35

Rudolf M, Wolter HJ, Zimmermann H (1999) A linear model for tracking error minimization. J Bank Finance 23(1):85–103

Schmidhammer C, Lobe S, Röder K (2010) Intraday pricing of ETFs and certificates replicating the German DAX index. Rev Manag Sci 5(4):337–351

Shin S, Soydemir G (2010) Exchange-traded funds, persistence in tracking errors and information dissemination. J Multinatl Financ Manag 20(4/5):214–234

Stoimenov PA, Wilkens S (2005) Are structured products ‘fairly’ priced? An analysis of the German market for equity-linked instruments. J Bank Finance 29(12):2971–2993

Stoll HR, Whaley RE (2010) Commodity index investing and commodity futures prices. J Appl Finance 20(1):7–46

Tzvetkova R (2005) The implementation of exchange traded funds in the European market. Difo-Druck, Bamberg

Wallmeier M, Diethelm M (2009) Market pricing of exotic structured products: the case of multi-asset barrier reverse convertibles in switzerland. J Deriv 17(2):59–72

Welch BL (1951) On the comparison of several mean values: an alternative approach. Biometrika 38(3/4):330–336

White H (1980) A heteroskedasticity-consistent covariance matrix estimator and a direct test for heteroskedasticity. Econometrica 48(4):817–838

Wilkens S, Erner C, Röder K (2003) The pricing of structured products in Germany. J Deriv 11(1):55–69

Wright C, Diavatopoulos D, Felton J (2010) Exchange-traded notes: an introduction. J Invest 19(2):27–37

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Dorfleitner, G., Gerl, A. & Gerer, J. The pricing efficiency of exchange-traded commodities. Rev Manag Sci 12, 255–284 (2018). https://doi.org/10.1007/s11846-016-0221-0

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11846-016-0221-0