Abstract

The purpose of this study is to examine the impact of green tax incentives such as investment tax credit and taxable income deductions related to the environmental sustainability and climate change which are becoming more popular in developing countries, whereas introducing green tax incentives related to the environment and climate change helps and meets the sustainability objectives of growth and development. For this purpose, we selected the top 100 listed companies on the Swedish stock market (SSM), Nasdaq Stockholm (SN), in order to better understand the real facts and figures of green tax environment. This study uses a longitudinal research design because sample observations vary across firms and over a short time and conducts probit and logistic regression to identify the beneficiaries of the tax incentives. The findings show that different firm-level characteristics significantly impact the probability of being an ITC beneficiary.

Similar content being viewed by others

Explore related subjects

Discover the latest articles, news and stories from top researchers in related subjects.Avoid common mistakes on your manuscript.

Introduction

Green tax incentives such as investment tax credit and taxable income deductions related to the environment and climate change are the frequently used tax incentives. Many countries worldwide are taking serious steps to counter the mounting challenges due to changing climatic conditions (Mao and Wang 2016). To meet the sustainability goals, Sweden has set a goal to lower greenhouse gas emissions by 55% in 2030 as compared to 1990 (Dahlberg and Wiklund 2018). In this regard, it is imperative to reflect on the green tax incentives provided by the Swedish government in terms of the investment tax credit. Investigating the beneficiaries of the Swedish government’s tax incentives related to the environment is significant in many instances.

However, Nordic countries were the first to introduce carbon taxes in the early 1990s. Sweden’s carbon tax was introduced in 1991 to mitigate the changing climatic conditions worldwide and within the country. This specific green tax policy was aimed at reducing greenhouse emissions cost-effectively and promoting the environment by developing and deploying clean technologies (Jagers and Hammar 2009). Pricing carbon emissions is the manifestation of the green tax increase. Sweden’s government derived the carbon tax model from the polluter pays principle, which says that the external cost of pollution must not be borne by society but by those who are causing it (Yikun et al. 2021). The carbon tax policy in Sweden has proved more successful in achieving its stated objectives, such as a decline in energy consumption, a rise in the efficiency of energy usage, and greater availability and use of more and more renewable energy alternatives (Yaqoob et al 2022a, b). In 2017, Nasdaq Stockholm introduced sustainable bonds and became the first stock exchange to launch a market for sustainable bonds, making it mandatory for companies to include sustainability efforts in their annual reports (Erhart 2018).

To investigate the effects of different environmental restrictions on the performance of green technologies and geographical disparities, a dynamic panel regression model was created. The findings demonstrate that the efficiency variable of green innovation is increasing in 30 provinces, although the disparities across provinces are significant. The efficiency of green inventions is not linearly related to environmental regulations (Saleem et al. 2022).

We did not find any comprehensive study on this topic, which particularly focus on green tax incentives and its impact on environment protection. The primary objective of this study is to evaluate and investigate the beneficiaries of green tax policy in Sweden by relying on tax-payer level observations. This study addresses the following research question: who are the beneficiaries of green tax incentives toward the environment protection in Sweden? To identify significant firm-level characteristics in taking advantage of green tax policy, in this study, we evaluate the implications of the carbon tax policies for Sweden and contribute to the literature in two aspects. This study evaluates the implications of the carbon tax policy for a developed country. It is important because Sweden introduced a carbon tax policy almost 30 years ago, and it is crucial to evaluate the implications of green tax incentives.

Literature review

It is noted that tax policy is more prevalent than direct regulation, because tax policy allows consumers and firms to continue with their basic goals, such as utility and profit maximization. Thus, tax policy is more efficient than direct regulation (Tresch 2022). The question of why firms respond to tax incentives has been answered by Hall and Jorgenson (1967). According to them, the user investment cost depends on many factors, including capital income tax. Therefore, tax incentives that cause a reduction in the user cost of investment will encourage firms to become the beneficiary of tax incentives. Regarding the efficiency of tax incentives, it is known that domestic public welfare can be increased more sustainably through investment tax credit than by cutting taxes on corporate income. Because of the endowment effect,Footnote 1 firms are more reluctant to accept the tax cut on corporate income than the tax credit on investments oriented to protect the environment. However, investment firms are far behind in capturing the benefit of an investment tax credit on the environment. It is found that increased demand for investment goods causes a price hike, and the suppliers of capital get a larger share of benefits than investing firms (Goolsbee 1998).

Liu et al. (2022a, b, c, d, e, f) analyze the effect of the implementation of China’s environmental tax in 2018 on firms’ environmental investments. The findings of this study indicate a significant increase in firms’ environmental investments after the implementation of the tax. However, Shabbir et al. (2020) examined the relationship between CSR activities and firm performance through non-linear and disaggregate approach. Moreover, Shabbir and Wisdom (2020) investigated the causal association between CSR and firm performance from manufacturing sector. The results of both studies indicate a positive and significant impact on firm performance. Arslan et al. (2021) described the mediating role of green creativity and the moderating role of green mindfulness in the relationship among clean environment, clean production, and sustainable growth. They took primary data set from top seven fertilizer companies list in Pakistan. The results indicate that green creativity and green mindfulness have a positive effect on clean environment. Cao et al. (2022a, b) explain the relationship among financial development, energy consumption, and sustainable environmental-economic growth through sustainable environmental agenda in the era of globalization, whereas Ge et al. (2022) examine the causal effect of foreign private investment on clean industrial environment through CO2 emissions, energy consumption, trade openness, and sustainable economic growth.

Liu et al. (2022a, b, c, d, e, f) investigate whether the impact of green environmental innovation really matters for carbon-free economy through green technological innovation, green international trade, and green power generation. The findings of their study show positive and significant effect green environmental innovation on carbon-free economy. Sadiq et al. (2022) explain the dynamic role of globalization toward energy consumption, economic growth, and carbon dioxide emissions through sustainable environmental agenda. Liu et al. (2022a, b, c, d, e, f) investigate the impact of China’s new Environmental Protection Law on the green innovation behavior of listed companies in high-polluting industries. Khurshid et al. (2022) examined the role of environmental policy, energy consumption, environmental taxes, urbanization, and economic growth on the environment.

Wang et al.’s (2022a, b) environmental adequacy is a requirement for happiness since it affects people’s health and quality of life. Data from 30 Chinese provinces and autonomous territories’ 2019 green taxes are combined with information from the 2019 China Social Survey (CSS).

The basis for the system’s design is a complex and dynamic interaction between economic development, pollution emissions, resource consumption, and environmental taxation, where the functions of environmental taxes are represented by linear parameters. The behavior of the system is complicated, as evidenced by theoretical study. The spectrum of the Lyapunov exponents and the distribution diagram is used to infer the existence of chaos, which is subsequently supported by the discovery of a chaotic attractor. A major contributing factor to green development is the environmental tax.

Data and methodology

Data description

There are two sources of data collection such as primary and secondary sources of data. Primary data contain first-hand information from the respondents, whereas secondary data is not first-hand information but rather has already been collected by different private and public organizations. One way to differentiate primary versus secondary data is to identify whether any statistical methods have been applied to the data or not (Hox and Boeije 2005). For example, companies’ annual reports will be considered secondary sources of data. In this study, we also use annual reports of 100 top-listed companies in NASDAQ Stockholm. Therefore, our data source is secondary. This study uses short panel data because the cross-sectional elements are greater than the periods. Specifically, we are using secondary data from 2016 to 2020 for 100 companies.

Econometric specification

Ordinary least square assumes normal distribution to estimate parameters. However, the distribution is no more normal, characterized by 0 mean and 1 standard deviation. Instead, dichotomous dependent variables assume Bernoulli distribution to estimate parameters. In other words, using OLS will likely produce inefficient parameters, especially when the experiment is drawn from the Bernoulli distribution. A random variable is said to have a Bernoulli distribution if it assumes only two values: 0 with probability 1 − p and 1 with probability p, where 0 ≤ p ≤ 1. Random variables of this category can be generated from a population whose outcomes can assume two values, i.e., yes or no. The binomial distribution is the generalization of the Bernoulli distribution, where the former draws outcomes from repetition.

Binary response models such as logit and probit assume mutually exclusive binary outcomes and focus on the occurrence of one outcome with the probability p. It implies that binary response models do not focus on the alternative outcome that occurs with a probability of 1 − p.

Suppose that the outcome variable Y assumes one of the two values:

In this stage, we must differentiate the observed binary outcome Y and the unobserved continuous Y*, which is often termed as a latent variable. For instance, the probability density function for the observed binary outcome Y is given by

with E (Y) = P and Var (Y) = P(1 − P).

The basic model of the single-index form is given by

where f (Yi/Xi) = PiY (1 − Pi)1−Yi

To satisfy the necessary condition of 0 ≤ p ≤ 1, f (Yi/Xi) must be a cumulative distributive function.

Assume that the latent variable Y* satisfies the single index model,

Although we cannot observe Y*, we can observe

Thus, we can transform expression 1 into expression 3.

Applying some mathematical operations on expression 2 and expression 3, we can have

Variables of the study

Table 1 explains the variables in details.

Research hypothesis

-

H1: The probability of being a beneficiary under the green tax incentive scheme is the same for domestic and foreign firms.

-

H2: The probability of being a beneficiary under the green tax incentive scheme is the same for older and younger firms.

-

H3: The probability of being a beneficiary under the green tax incentive scheme is the same for small and big firms.

-

H4: Firms with higher levels of new investment and fixed capital are more likely to benefit from the tax incentives than firms with lower levels of new and fixed capital.

-

H5: Firms with higher levels of profitability are more likely to benefit from the tax incentives than firms with low-profitability.

Results and discussion

Descriptive statistics

The average dependent variable for the current data set is 0.537 with a standard deviation of 0.498. It implies that 53% of the observations in the dependent variables contain a value of 1 while 47% of observations contain a value of 0. Alternatively, 53% of the top-listed companies secure an ESG score greater than 60 for the period 2016–2020. However, 47% of the top-listed companies secure an ESG score of less than 60. Our first explanatory variable is also a dummy indicating whether a company is a domestic or foreign firm and assumes value 1 for a foreign company. Its average value is 0.467 which implies that 46% of the top-listed companies are foreign-based while 54% are domestic companies. Age of company is our second explanatory variable which measures how long a company is operating. The mean age of the top-listed companies is 82 which implies the average age of the selected companies. For instance, the maximum age of a company in this data set is 147 and the minimum age is 7 as mentioned in below Table 2.

Our third explanatory variable is size which measures total number of employees. The mean of size is 17,731 which is the average number of employees for the selected companies for the period 2016–2020. However, its standard deviation is quite large indicating a higher gap between the minimum and maximum values. It can be said that the distribution of the size variable is lacking the normality assumption.

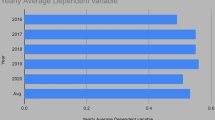

In the Fig. 1 as bar chart, we present the yearly average of our dependent variable. In 2016, the average dependent variable was 0.49 and in 2020, it is 0.51. It shows the early evolution of sustainable practices of the selected companies. For instance, only 49% of the selected companies were engaged in sustainable activities in 2016 but the percentage increased to 56% in 2019. The average dependent variable shows that 53% of the companies secured ESG scores above 60. To sum it up, 4% of companies have incorporated and prioritized sustainable activities in their daily operations.

Bar chart: yearly average dependent variable

Multicollinearity

The most crucial econometric issue in multiple linear regressions is to account for the degree of correlation among the explanatory variables. If one or more explanatory variables are correlated with another explanatory variable, we can have the issue of multicollinearity in the model.

In Table 3, we present the correlation matrix of the selected variables. Pearson correlation coefficient can take a value between 0 and 1, and we can categorize three different levels of correlation coefficients. For instance, a correlation coefficient between 0.1 and 0.30 indicates a weak degree of correlation. A correlation coefficient between 0.30 and 0.60 would imply a moderate correlation between the variables. And finally, a correlation coefficient above 0.60 indicates a strong correlation between variables (Chok 2010).

Probit regression results

The basic argument is that different firm-level characteristics play a significant role in determining the probability of being a beneficiary in a green tax incentive scheme. We hypothesize this idea and investigate the impact of different firm-level characteristics on the probability of being a beneficiary in a green tax incentive scheme. The results of hypothesis testing are presented in Table 4.

In the first column of Table 4, we enlisted the variables with their coefficients in the second column. For instance, the coefficient is negative for foreign-based companies indicating the fact that foreign-based firms are less likely to benefit from the green tax incentives. However, this coefficient is statistically insignificant at the standard 5% significance level. For instance, its associated probability value is almost 90%. Another way to look at the statistical significance of explanatory variables is to check whether the Z statistics is above 2 or not. In this case, it is far lower than the critical region of 2. Alternatively, the foreign dummy appears statistically insignificant in all three different specifications and is consistent with negative insignificant coefficient for foreign-based firms in Liu et al. (2022a, b, c, d, e, f), Mao and Wang (2016), and Muhammad et al (2022).

Our second explanatory variable in Table 4 is age. A positive coefficient for age would imply that older firms are more likely to benefit from the tax incentives than younger firms. However, the coefficient of age is negative and indicates that older firms are less likely to benefit from the green tax incentive scheme than younger firms (Li et al. 2022). Though this coefficient is statistically insignificant in Table 4 because the probability value is 11%, it appears statistically significant under robust standard error regression in Table 5. Therefore, we reject our second hypothesis that older and younger firms have the same impact on the probability of being beneficiaries under the tax incentive scheme and conclude that younger firms are more engaged in sustainable activities than older firms (Table 6).

Our second last hypothesis assumes that firms with higher levels of new investment and fixed capital are more likely to benefit from the tax incentives than firms with lower levels of new investment and fixed capital. In this regard, the coefficients for investment and capital are critical to be considered (Liu et al. 2022a, b, c, d, e, f). It appears that both coefficients are positive and statistically significant at 9 and 6% significance levels. For instance, in Table 5, we can see that the probability values of investment and capital are 0.09 and 0.07. The magnitude of the coefficient of capital is relatively higher and almost double than what it was in Mao and Wang (2016). However, the capital coefficient was significant at a 1% significance level.

It is imperative to conduct a goodness-of-fit test after presenting initial regression results. The null hypothesis of the goodness-of-fit test is such that there is no significant difference between the observed and the expected values. Rejection of this hypothesis would imply a significant difference between the observed and the expected values (Liu et al. 2022a, b, c, d, e, f). However, we are unable to reject the null hypothesis at a 5% significance level because the probability of chi2 is 74%. Therefore, it can be concluded that the model is well fitted as there is no significant difference between the observed and expected values in the Table 7.

In Table 8, we present our hypothesis testing. We make a conclusion about our hypothesis based on the coefficients and t-statistics values. A rule of thumb is to consider the sign and t-statistics that guides us either to reject or accept the null hypothesis. Because the coefficients in the table are actually the probabilities of being beneficiaries. For instance, Hypothesis 1 assumes the same probability of being a beneficiary between domestic and foreign firms. We can see that the coefficient is negative implying that the probability of being a beneficiary is greater for the domestic firm than for foreign firms. However, the coefficient is not statistically significant neither at 5% nor at a 10% significance level. As a result, we accept the null hypothesis and conclude that the probability of being a beneficiary is the same for both domestic and foreign firms. Regarding the second hypothesis that assumes the same probability of being beneficiary between older and younger firms, the coefficient is negative and indicates that older firms are less likely to benefit from the green tax incentive scheme than younger firms. Our study results are similar with studies such as Liu et al. (2022a, b, c, d, e, f), Anser et al. (2021), Bai et al. (2022), Cao et al. (2022a, 2020b), Chen et al. (2022), Dai et al. (2022), Jun et al. (2021), Mughal et al. (2022), Nawab et al. (2022), Muhammad et al. (2021), Yaqoob et al. (2022a, b), Wang et al. (2022a, b), Shabbir et al. (2021), Yu et al. (2021), Khan et al. (2021), Yang et al. (2022), and Jain et al. (2022).

Conclusion and recommendations

The purpose of this study was to investigate the impact of different firm-specific characteristics on the probability of being a beneficiary in the green tax incentive scheme introduced by the Swedish government. Green tax incentives are becoming popular to enhance the sustainability aspect of a firm’s production process. For instance, different green tax incentives in terms of investment tax credit and taxable income deductions are prevalent across the globe. In this regard, this study investigates and identifies the beneficiaries of the green tax incentive program introduced by the Swedish government.

The findings of the study suggest that only two firm-specific variables secure negative coefficients, i.e., foreign dummy and age, while all the rest of the coefficients are indicating a positive and significant impact on the probability of being a beneficiary under the green tax incentive program. For instance, the coefficients are negative and significant for both foreign dummy and age variables. But the coefficients are positive and significant for size, investment, capital, asset return, and capacity. Based on the findings, it can be concluded that different firm-specific characteristics are critical in determining their probability of being beneficiaries in the green tax incentive program. Our findings also show that firms with higher amounts of new investment in fixed assets are more likely to benefit from the tax incentives. Finally, we found a statistically significant coefficient for firm capacity, an indicator of total inventory. Specifically, the higher the capacity of a firm, the more it is likely to be an ITC beneficiary.

Policy recommendations

Based on the study findings, we recommend the following policy recommendations:

-

Regarding our first hypothesis, we confirmed that foreign firms took less advantage of the green tax incentive scheme; therefore, it is imperative to redesign the green tax incentive programs in an attempt to attract foreign-based firms.

-

In addition, findings suggest that firms with greater capacity and capital accumulation took relatively greater advantage of the green tax system. Therefore, it is suggested that upcoming green tax packages must also include the concerns of smaller firms in terms of capacity and capital.

Data availability

The data is available on request from the corresponding author.

Notes

Mullainathan, S., & Thaler, R. H. (2000). Behavioral economics.

References

Anser MK, Usman M, Sharif M, Bashir S, Shabbir MS, Yahya Khan G, Lopez LB (2021) The dynamic impact of renewable energy sources on environmental economic growth: evidence from selected Asian economies. Environ Sci Pollut Res 1–13

Arslan Z, Kausar S, Kannaiah D, Shabbir MS, Khan GY, Zamir A (2021) The mediating role of green creativity and the moderating role of green mindfulness in the relationship among clean environment, clean production, and sustainable growth. Environ Sci Pollut Res 1–15

Bai D, Jain V, Tripathi M, Ali SA, Shabbir MS, Mohamed MA, Ramos-Meza CS (2022) Performance of biogas plant analysis and policy implications: evidence from the commercial sources. Energy Policy 169:113173

Cao X, Kannaiah D, Ye L, Khan J, Shabbir MS, Bilal K, Tabash MI (2022a) Does sustainable environmental agenda matter in the era of globalization? The relationship among financial development, energy consumption, and sustainable environmental-economic growth. Environ Sci Pollut Res 1–11

Cao Y, Tabasam AH, Ali SA, Ashiq A, Ramos-Meza CS, Jain V, Shabbir MS (2022b) The dynamic role of sustainable development goals to eradicate the multidimensional poverty: evidence from emerging economy. Economic Research-Ekonomska Istraživanja 1–12

Chen J, Su F, Jain V, Salman A, Tabash MI, Haddad AM, ... Shabbir MS (2022) Does renewable energy matter to achieve sustainable development goals? The impact of renewable energy strategies on sustainable economic growth. Front Energy Res 10: 829252

Chok NS (2010) Pearson’s versus Spearman’s and Kendall’s correlation coefficients for continuous data (Doctoral dissertation, University of Pittsburgh)

Dahlberg L, Wiklund F (2018) ESG investing in Nordic countries: an analysis of the shareholder view of creating value

Dai Z, Sadiq M, Kannaiah D, Khan N, Shabbir MS, Bilal K, Tabash MI (2022) Correction to: The dynamic impacts of financial investment on environmental-health and MDR-TB diseases and their influence on environmental sustainability at Chinese hospitals. Environ Sci Pollut Res 1–1

Erhart S (2018) Exchange-traded green bonds. J Environ Invest 1–41

Ge M, Kannaiah D, Li J, Khan N, Shabbir MS, Bilal K, Tabash MI (2022) Does foreign private investment affect the clean industrial environment? Nexus among foreign private investment, CO2 emissions, energy consumption, trade openness, and sustainable economic growth. Environ Sci Pollut Res 1–8

Goolsbee A (1998) Investment tax incentives, prices, and the supply of capital goods. Q J Econ 113(1):121–148

Hall RE, Jorgenson DW (1967) Tax policy and investment behavior. Am Econ Rev 57(3):391–414

Hox JJ, Boeije HR (2005) Data collection, primary versus secondary

Jagers SC, Hammar H (2009) Environmental taxation for good and for bad: the efficiency and legitimacy of Sweden’s carbon tax. Environ Politics 18(2):218–237

Jain V, Ramos-Meza CS, Aslam E, Chawla C, Nawab T, Shabbir MS, Bansol A (2022) Do energy resources matter for growth level? The dynamic effects of different strategies of renewable energy, carbon emissions on sustainable economic growth. Clean Technol Environ Policy 1–7

Jun W, Mughal N, Zhao J, Shabbir MS, Niedbała G, Jain V, Anwar A (2021) Does globalization matter for environmental degradation? Nexus among energy consumption, economic growth, and carbon dioxide emission. Energy Policy 153:112230

Khan MB, Saleem H, Shabbir MS, Huobao X (2021) The effects of globalization, energy consumption and economic growth on carbon dioxide emissions in South Asian countries. Energy Environ 0958305X20986896

Khurshid A, Rauf A, Calin AC, Qayyum S, Mian AH, Fatima T (2022) Technological innovations for environmental protection: role of intellectual property rights in the carbon mitigation efforts. Evidence from western and southern Europe. Int J Environ Sci Technol 19(5):3919–3934

Li H, Jiang Y, Ashiq A, Salman A, Haseeb M, Shabbir MS (2022) The role of technological innovation, strategy, firms performance, and firms size and their aggregate impact on organizational structure. Manage Decis Econ

Liu C, Ni C, Sharma P, Jain V, Chawla C, Shabbir MS, Tabash MI (2022a) Does green environmental innovation really matter for carbon-free economy? Nexus among green technological innovation, green international trade, and green power generation. Environ Sci Pollut Res 1–9

Liu J, Jain V, Sharma P, Ali SA, Shabbir MS, Ramos-Meza CS (2022b) The role of sustainable development goals to eradicate the multidimensional energy poverty and improve social wellbeing’s. Energ Strat Rev 42:100885

Liu Y, Sharma P, Jain V, Shukla A, Shabbir MS, Tabash MI, Chawla C (2022c) The relationship among oil prices volatility, inflation rate, and sustainable economic growth: evidence from top oil importer and exporter countries. Resour Policy 77:102674

Liu Y, Cao D, Cao X, Jain V, Chawla C, Shabbir MS, Ramos-Meza CS (2022d) The effects of MDR-TB treatment regimens through socioeconomic and spatial characteristics on environmental-health outcomes: evidence from Chinese hospitals. Energy Environ. https://doi.org/10.1177/0958305X221079425

Liu G, Yang Z, Zhang F, Zhang N (2022e) Environmental tax reform and environmental investment: a quasi-natural experiment based on China’s environmental protection tax law. Energy Econ 109:106000

Liu L, Bashir T, Abdalla AA, Salman A, Ramos-meza CS, Jain V, Shabbir MS (2022f) Can money supply endogeneity influence bank stock returns? A case study of South Asian economies. Environ Dev Sustain 1–13

Mao J, Wang C (2016) Tax incentives and environmental protection: evidence from China’s taxpayer-level data. China Financ Econ Rev 4(1):1–30

Mughal N, Arif A, Jain V, Chupradit S, Shabbir MS, Ramos-Meza CS, Zhanbayev R (2022) The role of technological innovation in environmental pollution, energy consumption and sustainable economic growth: evidence from South Asian economies. Energ Strat Rev 39:100745

Muhammad I, Shabbir MS, Saleem S, Bilal K, Ulucak R (2021) Nexus between willingness to pay for renewable energy sources: evidence from Turkey. Environ Sci Pollut Res 28(3):2972–2986

Muhammad I, Ozcan R, Jain V, Sharma P, Shabbir MS (2022) Does environmental sustainability affect the renewable energy consumption? Nexus among trade openness, CO2 emissions, income inequality, renewable energy, and economic growth in OECD countries. Environ Sci Pollut Res 1–11

Nawab T, Raza S, Shabbir MS, Yahya Khan G, Bashir S (2022) Multidimensional poverty index across districts in Punjab, Pakistan: estimation and rationale to consolidate with SDGs. Environ Dev Sustain 1–25

Sadiq M, Kannaiah D, Yahya Khan G, Shabbir MS, Bilal K, Zamir A (2022) Does sustainable environmental agenda matter? The role of globalization toward energy consumption, economic growth, and carbon dioxide emissions in South Asian countries. Environ Dev Sustain 1–20

Saleem H, Khan MB, Shabbir MS, Khan GY, Usman M (2022) Nexus between non-renewable energy production, CO2 emissions, and healthcare spending in OECD economies. Environ Sci Pollut Res 1–12

Shabbir MS, Wisdom O (2020) The relationship between corporate social responsibility, environmental investments and financial performance: evidence from manufacturing companies. Environ Sci Pollut Res 1–12. https://doi.org/10.1007/s11356-020-10217-0

Shabbir MS, Aslam E, Irshad A, Bilal K, Aziz S, Abbasi BA, Zia S (2020) Nexus between corporate social responsibility and financial and non-financial sectors’ performance: a non-linear and disaggregated approach. Environ Sci Pollut Res 27(31):39164–39179

Shabbir MS, Bashir M, Abbasi HM, Yahya G, Abbasi BA (2021) Effect of domestic and foreign private investment on economic growth of Pakistan. TCR 13(4):437–449

Tresch RW (2022) Public finance: a normative theory. Academic Press

Wang J, Tang D, Boamah V (2022a) Environmental governance, green tax and happiness—an empirical study based on CSS (2019) data. Sustainability 14(14):8947

Wang G, Sadiq M, Bashir T, Jain V, Ali SA, Shabbir MS (2022b) The dynamic association between different strategies of renewable energy sources and sustainable economic growth under SDGs. Energ Strat Rev 42:100886

Yaqoob N, Ali SA, Kannaiah D, Khan N, Shabbir MS, Bilal K, Tabash MI (2022a) The effects of agriculture productivity, land intensification, on sustainable economic growth: a panel analysis from Bangladesh, India, and Pakistan economies. Environ Sci Pollut Res 1–9

Yaqoob N, Jain V, Atiq Z, Sharma P, Ramos-Meza CS, Shabbir MS, Tabash MI (2022b) The relationship between staple food crops consumption and its impact on total factor productivity: does green economy matter?. Environ Sci Pollut Res 1–10

Yikun Z, Gul A, Saleem S, Shabbir MS, Bilal K, Abbasi HM (2021) The relationship between renewable energy sources and sustainable economic growth: evidence from SAARC countries. Environ Sci Pollut Res 1–10

Yang X, Ramos-Meza CS, Shabbir MS, Ali SA, Jain V (2022) The impact of renewable energy consumption, trade openness, CO2 emissions, income inequality, on economic growth. Energ Strat Rev 44:101003

Yu S, Sial MS, Shabbir MS, Moiz M, Wan P, Cherian J (2021) Does higher population matter for labour market? Evidence from rapid migration in Canada. Economic Research-Ekonomska Istraživanja 34(1):2337–2353

Author information

Authors and Affiliations

Contributions

Mariuam Shafi: conceptualization and investigation; Carlos Meza: data creation and resources; Vipin Jain: methodology. Asma Salman: methodology and formal analysis; Mustafa Kamal: data analysis; Malik Shahzad: result and discussion section. Masood ur Rahman: abstract and conclusion sections and formation of paper as per journal requirements.

Corresponding author

Ethics declarations

Ethical approval and consent to participate

This study did not use any kind of human participants or human data, which require any kind of approval.

Consent for publication

Our study did not use any kind of individual data such as video and images.

Competing interests

The authors declare no conflict of interest.

Additional information

Responsible Editor: Nicholas Apergis

Publisher's note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Shafi, M., Ramos-Meza, C.S., Jain, V. et al. The dynamic relationship between green tax incentives and environmental protection. Environ Sci Pollut Res 30, 32184–32192 (2023). https://doi.org/10.1007/s11356-023-25482-y

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11356-023-25482-y