Abstract

In this paper the survivor technique is employed to study American manufacturing establishments in four-digit SIC industries. A major finding is that “down-sizing” during the late 1980s is more than anecdotal. Survivor estimates of economies of scale using the 1987 and 1992 Censuses of Manufactures clearly illustrate a general movement toward smaller scales. Moving beyond prior survivor studies, the sources of changes in scale are investigated. However, increases in either number of establishments or value added had a statistically significant effect on the occurrence of a change in scale, respectively decreasing or increasing the likelihood of change. The HHI of the industry also had a significant positive effect on the likelihood of a significant change in scale of output.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

The period from the 1970s through the early 1990s saw the United States economy buffeted by the forces of increased foreign competition and technological revolution. During this period, manufacturing’s role in the American economy continued its secular decline from 32.8 per cent of GDP in 1982 to 25.9% in 1992, while service activities of various descriptions continued their growth to 72.2% of GDP in 1992.

At the same time, U.S. manufacturing was confronted with a huge increase in import competition, with imported manufactures rising 187% between 1982 and 1992. Comparatively speaking, United States manufacturing exports lagged, rising by only 146% (World Bank 2004). Pressured by lower wage competition and a strong American dollar throughout the 1980s, American firms scrambled to restructure and relocate their manufacturing capabilities. This raises an interesting question: Did the scale of output in American manufacturing change during this period?

In this paper the survivor method for determination of the efficient scale of output for industry is applied to data from the 1987 and 1992 Censuses of Manufactures to resolve this question. The method, first proposed in its modern form by Stigler (1958), is conceptually quite simple. In a competitive environment, firms face a selective pressure to adopt a scale of output that is economically efficient. Establishments whose scale of production activities falls outside of the most efficient range are more likely to be unprofitable.Footnote 1 Thus inefficiently sized establishments will either exit the industry or adapt to efficiently sized operations. In either case, efficiently sized establishments will constitute an increasing share of the industry.

The technique was implemented for large segments of the United States economy during the 1960s by Sands (1961), Saving (1961), Weiss (1964) and Shepherd (1967), using data from the 1940s and 1950s. More recent applications of the technique have been limited to analysing specific industries, such as trucking (Giordano 1997), or other countries’ manufacturing: Germany (Hofmann 1986), Italy (Cardani 1979), and South Africa (Reekie 1984). Giordano (2003) provides a summary of both the strengths and the criticisms of the technique and further results.

This paper considers survivorship trends in the U.S. economy between 1987 and 1992. It extends the classic literature of the 1960s by: (1) examining a much larger segment of manufacturing; (2) employing statistical tests of changes in establishment distributions of manufacturing output, rather than the impressionistic evaluation of the prior literature; and (3) offering some statistical tests to determine which features of the changing environment of business are most responsible for the observed changes in the establishment distribution of economic activity among different sized manufacturing facilities.

The balance of the paper consists of four sections: In the next section, the methodology of survivorship, the nature of the data, and the techniques employed are explained. The succeeding section derives and reports the survivor estimates of optimal scale of establishments for the industries that are covered. The survivorship experience of some of specific industries is discussed. The following section applies statistical techniques to explain the trends in the optimal scale of industries that are estimated in this study. A brief conclusion rounds out the paper.

2 Methodological Considerations

In this section the methodological basis for the survivor technique is described. The data that are required to conduct survivorship analysis are outlined. Subsequently the sources of this data are identified. Following this, the techniques for conducting survivorship analysis are detailed. Finally, the statistical techniques for determining whether or not there has been a significant change in the distribution of production among different establishment size classifications are discussed.

The core idea of the survivor technique is the pervasive nature of competition. An establishment—whether it is a firm that operates in a single location or it is part of a multi-unit producer—is challenged competitively on many levels. In particular, every establishment must cover the opportunity costs of the resources that are consumed with revenues that are generated from the sale of its output. The long-run survival of an establishment depends upon its producing output at the lowest cost.

The survivor technique is a comparative-statics technique: observing the adaptation of firms to changing technological opportunities and market conditions. Within an industry, establishment size classes that are observed to grow relative to other sizes are judged to be efficient, while shrinking size classes are inefficient.

Thus in order to construct survivor estimates of efficient scales requires periodic observations of the shares of the various establishment size classes within an industry. For this paper, U.S. Census of Manufactures data from 1987 to 1992 are employed. Although this period is short, it permits the use of uniform industry definitions throughout. Both of these Censuses used the 1987 definitions of industries in the Standard Industrial Classification (SIC) to place establishments within industries.

Data are reported in various formats by the U.S. Census Bureau. In this paper, the focus is on the four-digit SIC individual industry reports and specifically on Table 5 within these reports. Table 5 in these reports includes data on—among other things—the distribution of industry value added, the number of industry production employees, and the value of shipments across different employment size classes for establishments. The size classes (“buckets”) for individual establishments range from 1–4 to 2500 or more employees.

Not all potential size classes are reported in Table 5. There are two reasons for this. First, some industries only produce on a very small scale, so that reporting at the largest scales would be gratuitous. The other reason is that Census confidentiality policies prohibit publication of data that might permit the identification of individual respondents. When there are three or fewer establishments reporting in a size class, results from that class are suppressed. Where a size class is suppressed to insure confidentiality, data for that class are consolidated with the next smaller class. Thus some—but not all—of the relevant scale information is lost.

There is an additional complication that must be considered: All of the industries that are considered in this study were defined consistently in both 1987 and 1992. A broader spectrum of industries was considered for the sample than was true of prior broad studies. In fact, the sample that is used for this study includes almost all of the manufacturing industries that reported using the SIC at a four-digit level of disaggregation. Unlike prior survivorship studies, this paper does not limit itself to homogeneous product industries. As explained below, the use of value added overcomes a major difficulty with applying the survivor method to industries where outputs are differentiated.

There were three categories of exceptions: (1) Tobacco products (SIC 21XX) were excluded because all four-digit SIC industries within this two-digit (21) category were uninformative due to confidentiality restrictions. (2) Some other industries could not be analysed because of similar confidentially problems. (3) The other industries that were excluded were those that ended with the digit 9 and thus that represented “catch-all” categories rather than coherent industries.

Value added is measured as a firm’s value of shipments less the cost of an establishment’s purchased inputs. Thus value added reflects the compensation of labor and capital (both fixed and working) in the manufacturing process plus any economic rents the establishment may earn. The ability to command rents from any source (barriers to entry, location, product differentiation, quality, etc.) has a clear bearing on the ability of an establishment to survive. Establishments where rents are negative—those that do not cover the full costs of labor, capital, and purchased inputs—are unlikely to survive.Footnote 2

Most manufacturing industries will have output of differing levels of quality. It may be that particular scales of output are suitable for producing output of high quality while other scales are suited to production of lower quality outputs. Differences in quality can lead to differences in value added, since high-quality goods will command a premium price relative to lower-quality goods and the higher quality may arise because of greater labor and capital inputs within the establishment (rather than just higher-quality purchased components). Thus measuring shares of industry output in terms of the value added at a specific scale of output avoids difficulties with measuring qualitative differences among outputs.Footnote 3 The rents (and costs) that are associated with providing higher-quality products are absorbed into value added.

Production employment was chosen as a metric because labor is usually the single most important input in manufacturing production. In addition, previously reported survivor studies have measured firm size by labor headcounts.

Value of shipments is also included as a metric. The costs of purchased inputs—which is the difference between the value of shipments and value added—may vary systematically across establishment size classes. If this is true, it may represent a significant advantage for establishments in their struggle to survive. Value of shipments and value added are naturally highly correlated. However, where there is a divergence in their performance this may reflect a reorganization of production along the lines that were suggested by Coase (1937) and Williamson’s (2005) transaction cost analysis: Firms choose to purchase inputs that were previously manufactured internally or vice versa.

Producing survivor estimates is a far less tedious task today than it was in the 1960s since most of the calculations can be done using a simple spreadsheet program. The value added, production employment, or value of shipments for each employment size class are divided by overall employment (or value added or value of shipments) for that industry to determine the percentage of the industry that each size class represents.

Earlier studies of survivorship were limited to impressionistic evaluation of how the scale of output had changed in an industry. However, this is not enough to establish definitively that the observed changes in industry structure are the results of selective survival of firms that operate plants in the most efficient size classes. A certain amount of variation among size classes is the result of random fluctuations in employment or output in response to the business cycle, international trade trends, or industry-specific events.

Rao (1973, pp. 399–402) demonstrates that it is possible to test whether two empirical distributions were generated by the same underlying process. The appropriate test statistic is distributed as Chi squared with degrees of freedom equal to the number of categories into which the data are apportioned minus one.

We test whether the distribution of value added, value of shipments, and production employment among establishment size classes in 1992 differs from the distribution observed in 1987. Under the null hypothesis, the representation ratio for each class ought to equal one. A Chi squared test can be performed upon the distribution of representation ratios to confirm whether the differences in distribution among size classes were greater than could be attributed to chance. Each ratio is squared and summed across all k categories. This statistic is distributed as Chi squared with k − 1 degrees of freedom.

Table 1 illustrates the procedure for the SIC industry 2068, SALTED AND ROASTED NUTS AND SEEDS. Part A shows the reported values for Production Employees, Value Added, and Value of Shipments for 1987 and 1992. The first column illustrates the size classes that are employed by the Census: starting with 1–4 employees and culminating with more than 2500 employees. Adjacent to each reported value is the percentage share that the size class represents of the industry total.

Representation ratios are formed by dividing the 1992 percentage share of each size class by the same size class’ share in 1987. These representation ratios are shown in Part B of the example. Obviously, where the representation ratio is greater than one, that size class of establishment has grown relative to the industry as a whole. In the 1987 Census, the two largest size classes are represented by establishments but not reported for confidentiality reasons. In 1992, only the largest class remains unreported. This data problem is resolved by combining the values that are reported in one Census but not the other with data from the next smaller size class. This is the same solution that the Census Bureau employs to prevent confidentiality breaches.

Three different representation ratios for each plant size class were calculated. For instance, representation of the 5–9 employee size class grew relative to the industry for value added and value of shipments. However, manufacturing employment was unreported in both years so that a representation ratio was not calculated. The calculated representation ratios for other size classes for all three measures are shown below the ratio illustrated here. The Chi squared test statistic is calculated by squaring each representation ratio and summing them.

The final rows in Table 2 part B first illustrate the calculated Chi squared. Next, appear the number of observations for this statistic. Finally, the last two rows present the critical values for the 90 and 95% levels of significance. These results suggest that there was a significant change in the scale of operation between the Census years measured by Value Added and Value of Shipments. This result occurs despite the fact that the median scale of output—establishment size class 250–499—is unchanged by all three measures.

3 Survivorships Results

In this section, the results of the survivor analysis are examined. This occurs along two tracks: The first is an examination of the aggregate results of industries that experienced statistically significant changes in the distribution of production among establishment size classes. Industries whose changes are statistically significant are examined to determine if there was a clear change in the direction of change of scale.

Using the procedures outlined above, we calculated the empirical Chi squared statistics for each industry distribution. The empirical Chi squared for value added and value of shipments are highly correlated (R2 = 0.866.) The correlation between calculated Chi squared for either of these and the statistic for the distribution of production employees is much lower (R2 = 0.313 and 0.331, respectively.)

The results show that at the 95% level of confidence there were 107 industries where one of the measures of the distribution across size classes changed. In 85 of those industries the distribution of value added significantly changed. Seventy-five industries had significant changes in value of shipments, while 60 had significant changes in distribution of production employees across size classes.Footnote 4

There were 38 industries where all of the metrics indicated a significant change in the distribution of activity across size classes. An additional 37 industries were signaled as significantly changed by two metrics. In particular, in 28 both value added and value of shipments indicated scale changes.Footnote 5 (Table 3).

The values of important characteristics of the overall sample and the industries which experienced significant changes are reported in Table 4. In Table 4, the relative size of five important industry measures (number of establishments, production employees, value added, value of shipments and value added per employee) are compared across the full sample and sub-samples.

In the 1987–1992 time period the manufacturing sector as a whole experienced a very low rate of growth of the number of establishments across all industries, less than 0.8% per year. There was growth of both value added and shipments (appropriately deflated by PPI-Manufacturing from the FRED database of the Federal Reserve Bank of St. Louis) of approximately 1.0% annually. Labor productivity (measured as the rate of increase in value added per worker) increased at a higher rate of around 2%, while production employment fell by about 0.8% annually.

In contrast, the industries where a significant change occurred in the distribution of value added or value of shipments across establishment size classes had negative growth in value added and value of shipments. The relative numbers of manufacturing establishments changed at more than triple the rate of overall manufacturing, while the decline in production workers was at least twice as fast as manufacturing as a whole. The lower growth of value added and value of shipments, when linked to the increases in the number of establishments, suggests that competition in these industries strengthened. However, the average HHI measured for the industries that experienced significant change was substantially higher initially than for industries that did not experience such change; and overall manufacturing industries experienced increases in HHI over the period, while the industries with significant changes saw decreases in HHI, except in manufacturing employment.

To investigate this further, two different definitions of changes of scale were employed. If an industry is determined to have experienced a statistically significant change in the establishment distribution of output as measured by any of the measures that were discussed above, the direction of scale change was evaluated. This was done by determining whether the establishment size class that produced the median output changed between the 1987 observation and 1992 value. Where the median industry output is produced by a smaller establishment size class, the optimal scale of output is held to have decreased, and vice versa.

If the establishment scale that produced the median output is unchanged, the share of output of the largest size classes was examined for changes. Where the percentage of industry output that was produced by the largest establishment classes declined by 5% or more, a decreased scale of operation is inferred. When the largest size classes increased the share of output that they produced by more than 5%, the scale of output is held to have increased.

The results of this analysis are summarized in Table 5. Under the more restrictive definition of scale change (change in median scale), 20 industries are shown to have decreased the establishment size class that produced the median output. In contrast, only four industries experienced a larger scale of production that produced the industry median output. When a less stringent definition of a change of scale based upon the behavior of the largest size classes was applied, roughly twice as many industries showed decreases as opposed to increases in scale. However, the modal case for all three distributions was of no discernible change in scale, despite the indication from the Chi squared statistic that the distribution of at least one of the three had experienced a statistically significant change.

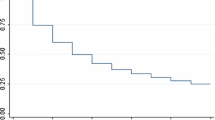

The Figs. 1, 2, 3, 4 and 5 present some examples of the various establishment size distributions in industries where a statistically significant change in the distribution of employment was indicated by the Chi square test. In Fig. 1, for Industry 2451 Mobile Homes the median establishment size was unchanged at 100–249 employees. In Fig. 2, for Industry 3264 Porcelain Electrical Supplies the median establishment size was reduced from 250–499 to 100–249 employees. In Fig. 3, for Industry 3484 Small Arms the median establishment size was unchanged but largest size class’ share was reduced from 71 to 55%. In Fig. 4, for Industry 3624 Carbon and Graphite the median establishment size was reduced from 250–499 to 100–249 employees. In Fig. 5, for Industry 3873 Watches and Clocks the median establishment size was unchanged at 250–499 employees. These results parallel the results that were reported in Table 4 that show a mixture of identifiable changes in median scale, ambiguous changes, and no visible changes despite the Chi squared results.

SIC 2451 Mobile homes—comparative shares 1987 and 1992

SIC 3264 Porcelain electrical supplies—comparative shares 1987 and 1992

SIC 3484 Small arms—comparative shares 1987 and 1992

SIC 3624 Carbon and graphite products—comparative shares 1987 and 1992

SIC 3873 Watches and clocks—comparative shares 1987 and 1992

4 Statistical Analysis of Sources of Scale Change

In this section of the paper, an attempt is made to determine why the significant changes in the distribution of output or production labor inputs among the establishment size classes that were reported previously occurred.

There are four possible sources of change that may alter the scale decision: changes in consumer preferences that favor the output of a particular size class of producer; changes in the relative price of capital and labor; changes in production technology; and changes in product prices. Three of these four possibilities are tested in the results that are reported below.

A logit analysis of the survivorship results reported was performed. The dependent variable was whether or not the industry in question had experienced a significant change in the distribution of value added (or value of shipments or production worker employment) among plants. (The absence of a change that was statistically significant at the 95% level = 0; Significant change = 1). The independent variables were the relative change in the number of establishments, the relative change in value added, and the relative change in value added per worker between 1987 and 1992. Additional control variables were the number of size classes in 1987, and the 1987 HHI for the industry.

Table 6 reports the mean and standard deviation of the variables that were employed.

These results illuminate the independent variables that determine which industries experienced significant change in the establishment scale of output. In order to detect the effects of changes in factor prices or technological change that is biased towards some particular factor, we consider value added. As noted earlier, value added is the sum of wages paid, return to physical and working capital, and any rents earned. Where changes in factor prices induce changed factor proportions, and thus changes in scale, this should be detectable by differential responses to changing the number of establishments. Where technological change provides opportunities for earning rents for some size classes, after the other elements of value added are independently accounted for, changed value added should result in changes in the distribution of output among plant sizes.

An a priori expectation is that the most significant changes in the distribution of output among establishments would to occur in those industries where the number of plants changed the most. According to the logic of survivorship, exits will be predominantly of plants that are inefficiently sized. By the same token, new entrant plants that are not saddled with the legacy of an inefficient scale or obsolete technology will choose to enter at the cost-minimizing scales. Thus a relatively larger number of establishments ought to result in a significant change in distribution, and the sign on this independent variable ought to be positive.

In the case of the relative change in the real value of shipments, the a priori expectation is that an increase in the real value of shipments—measured by a ratio greater than one between 1992 and 1987—indicates an expanding industry.Footnote 6 In such an industry the competitive pressures for scale changes will be reduced. Thus the expected parameter on this variable would be negative.

A positive relative change in real value added—measured by a ratio greater than one between 1992 and 1987—indicates that the combined rents, return to capital, and wages rose. Since capital and labor are already accounted for by other variables, increased value added indicates the possibility of earning rents from whatever source. Increasing rent extraction will reduce the need for changing the scale of operation. Thus this independent variable too should have a negative sign.

The initial number of size classes in each industry enters the equation as an explanatory variable with an ambiguous sign: It is possible that more opportunities for variation will lead to more variation in output among size classes. However, the number of size classes in an industry is dependent upon the scale of operation, and industries with significant economies of scale may be less likely to experience changes in the distribution of output.

The industry HHI measures the degree of concentration in the industry. At a higher initial level of concentration, firms ought to be able to extract rents more successfully without altering their production processes. However, the presence of such rents can attract the competitive entry of establishments into the industry. This is reflected in Table 4 above, where the initial HHI for industries that experienced significant change in scale is greater than is true for the all-industry average. The all industry average rose between 1987 and 1992. However, for industries where Value Added and Value of Shipments changed, the HHI was reduced. Thus, the expectation is that a higher initial value of HHI will increase the probability of significant changes in the establishment distributions considered; consequently, the parameter estimate is expected to be positive.

An increase in the number of production employees in the industry could also be a marker for entry, while a decrease may signify exit. In fact, as exemplified in Table 4, the number of production employees fell for all industries on average between 1987 and 1992, and industries that experienced a significant change in their establishment distributions reduced production workers more than the overall average. This suggests that a major motivation for changes in establishment scale is the opportunity to economize on labor inputs. This leads to an expectation that the probability of changes should be negatively related to the number of production workers.

To capture the technological opportunities of individual industries, the ratio of the value added per worker in 1992 to the value added per worker in 1987 is included in the regression. Industries with improving productivity—measured by increase in value added per worker—offer more opportunities for profitable entry, which ought to increase competitive pressures on inefficient existing establishments and lead to more change in the establishment distribution of activity and a positive parameter value. Thus, the ratio (1992/1987) of value added per production worker also has an expected positive sign.

Firms with significant competition from imports will be likely to exit inefficient scales and reposition themselves to efficient scales, so parameters related to import share should be positive. Where a firm has significant opportunities to sell in export markets, this indicates firms have comparative advantage relative to foreign producers, so the parameter estimate for export share should be negative.

Three additional indices were considered as possibly explanatory for the likelihood of significant scale change: The first was the ratio of establishments (individual locations of production) to the number of firms. Multi-plant firms could be expected to more easily adapt to scale changes by concentrating production at their most efficient plants. Consequently, the parameter estimate of this variable should be positive.

Another potential explanatory variable is the extent of the market that an individual establishment serves and competes in. The variable Local assigned three-digit SIC codes the value of 1 where the product was shipped less than 250 miles on average, and zero otherwise; data were drawn from the U.S. Commodity Flow Survey for 1993. Establishments in localized markets may face lesser competitive pressures than do establishments in national industries, so parameter estimates may be negative.

Finally, a dummy variable, Consum, was employed to distinguish industries whose output was used for final consumption from the industries that are devoted to producer’s goods. The variable took a value of 1 where more than 50% of an industry’s total output was devoted to Final Use. The source of these data was the 1990 input–output tables (use table) that was produced by the U.S. Bureau of Economic Analysis. This data were reported by three-digit NAIC code. A concordance was used to apply the calculated values to the appropriate SIC code, usually at the two-digit level.

Table 6 displays the mean and standard deviation of all of these variables.

Table 7 shows the results of the logit estimates.Footnote 7 One equation is estimated for each of the distribution of value added, the distribution of value of shipments, and the distribution of production workers among size classes. In each, the dependent variable is zero for industries without significant change at the 95% significance level, and one otherwise. Adjacent to the columns are columns that report the marginal effects of the independent variables at their mean values. All three equations reported are highly significant statistically with Chi squared values of 141.44, 129.89 and 112.43, respectively.

When we turn to the individual explanatory variables, the relative change in the number of establishments is positive and statistically significant across all three equations. Indeed the estimated parameter values are not statistically distinguishable. This indicates that an increase in the number of establishments raises the likelihood of significant distributional changes in an industry. The calculated marginal effects of the variable are quite modest.

The relative change in the Value of Shipments parameter estimate had the expected negative and statistically significant value for distributions of activity that are measured in terms of value of shipments and production employment. However, the parameter in the value added distributions regression was not statistically significant. The marginal effects of this variable were more robust.

The number of employment size classes that are reported in an industry has a negative and statistically significant effect upon the likelihood of a significant change in distribution across all equations three equations. Once again, the calculated marginal effects are modest.

The industry’s 1987 HHI has a uniformly positive and statistically significant effect on the likelihood of distributional changes occurring. Apparently more concentrated industries are more likely to have changes in the distribution of production activities across size classes.

The relative change in valued added has a coefficient that is both significantly different from zero and negative in the regressions for the distributions of value added and the value of shipments. The relevant coefficient in the regression that involves the distribution of production employees—while negative—is not significant at conventional levels. The marginal effects of relative value added appear to be more robust than many of the other variables. This indicates that a decrease in an industry’s value added makes it more likely that the industry will experience significant changes in distribution across employment size classes. The change in value added appears to function as an indicator of increased competition in the industry.

The relative change in the number of production workers and value added per worker were both excluded from estimates because of collinearity. The other independent variables discussed previously never resulted in statistically significant results for any of the equations in which they appeared. They likewise were typically statistically insignificantly different from zero, which suggests that they did not possess much explanatory power. Alternative specifications also proved to have less explanatory power than the equations in Table 7.

As a robustness check, three additional logit regressions were run: One regression considered the SIC industries that were found significant by all three of distributional tests. The second regression evaluated the set of industries where the median establishment size decreased. The third regression used an indicator (= 1) if the largest scale’s share of industry output was reduced by more than 5%. These results are reported in Table 8.

In the first column of Table 8, the results apply where only industries with all three distributional measures are treated as 1 s and the remaining SIC industries are zero. Both the relative number of establishments and value of shipment have the same signs as in prior regressions and are statistically different from zero at 95% confidence levels. The marginal effects of these variables are an order of magnitude larger than in the prior logit regressions. Although both relative value added and the initial industry HHI retain their signs, neither is significant at conventional levels of significance.

The third and fifth columns of Table 8 report logit regressions where the dependent variable assumes a value of 1 for industries that are identified as experiencing significant scale decreases; all other industries are assigned a value of zero. In both regressions, the relative number of establishments and value added have significant coefficients at conventional levels of significance. The coefficients are positive and negative, respectively, which is consistent with prior results. The marginal effects of relative establishments is significantly larger than in the prior estimates. The marginal effects of relative value added are of the same order of magnitude as prior results.

For these estimates, in addition, the coefficient of the HHI is positive and statistically significant. The marginal effect of HHI is virtually identical to the marginal effects reported previously. However, in these estimates the relative value of shipments is not significantly different from zero.

Finally in column five, the variable All Three identifies the specific industries where the change in establishment distribution was validated by all three measures. This variable—as might be expected—is positive and statistically significant. It also has a large marginal effect on the probability of identifying an industry that experienced significant structural change.

However, the prior examination of the individual industry distributions and their changes produced a meagre yield. Only 36 of the 107 industries showed a change in the establishment size class that produced the median output.

5 Conclusion

This paper demonstrates that a surprisingly large percentage of manufacturing industries (107/367) experienced changes in the distribution of manufacturing across different establishment size classes between 1987 and 1992. More industries appear to have experienced a decreasing establishment scale of output (53/107) than an increasing scale of output (20/107).

In order to understand the forces that underlay the reorganization of production in these industries, logit and multinomial estimates were made. The estimates indicated that entry of new establishments was a significant influence in the reorganization of manufacturing among establishment size classes. This is unsurprising, since new establishments will presumably be constructed at the most efficient size.

The logit estimates also suggest that increased industry growth, which was reflected by increased real value of shipments, reduced the probability of reorganization of production—perhaps by reducing the incentives for efficient operation.

The estimates further suggest that initial industry concentration has a significant positive effect on the probability of structural change in an industry’s production activities. This may reflect the greater resources that large firms enjoy, which might permit them to invest in improving their productive technology.

Finally, the estimates suggest that rising value added may serve as an indicator of decreased competition within an industry. This decrease of competition makes it less urgent for firms to reorganize their production activities and change their scale of output.

Notes

In the modern economy where firms are significantly diversified in terms of both products and geographic distribution of production, the plant or “establishment” is the appropriate unit to examine for survivorship behavior. According to the Census’ definition, an establishment is a single physical location of production activities.

The vagaries of transfer pricing that is applied to shipments between the establishments that belong to the same company may dampen such consequences.

Giordano (2003) specifies output homogeneity as a requirement for survivor analysis. However, differentiation through location of production, among other things, is so pervasive that a truly homogeneous output is probably non-existent.

At the 90% significance level, approximately 30 additional industries were found to have experienced measurable changes in their distribution. This was true for all three distributions.

Individual industry performance is illustrated in Table A1 in the appendix that is available from the author upon request.

Value Added, Value of Shipments, and Value Added per Production Worker were all deflated by the PPI-Manufacturing value for December 1987 and 1992.

At the editor’s suggestion, a multinomial logit was run with dependent variable values, 0 = no change, 1 = statistical change without obvious scale change, 2 = decreased scale through either reduced percentage share of largest size classes or median scale of output reduction, 3 = increased scale with either increased percentage share of largest size classes or median scale of output increased. The results are available from the author but do not significantly improve upon the results reported below.

References

Cardani, A. (1979). The survivor technique and the measurement of optimum size of plants in Italian manufacturing industries. Giornale Degli Economisti E Annali di Economia, 38(9–12), 927–942.

Coase, R. (1937). The nature of the firm. Economica, 4(16), 386–405.

Federal Reserve Bank of Saint Louis. (2017). FRED database series. Producer Price Index by Industry: Total Manufacturing Industries. https://fred.stlouisfed.org/series/PCUOMFGOMFG. Accessed 27 August 2017.

Feenstra, R. C. (1958–1994). Imports and exports by SIC 1958–1994. http://www.nber.org/pub/feenstra/. SIC58_94.ASC. Accessed 4 Sept 2017

Giordano, J. N. (1997). Returns to scale and market concentration among the largest survivors of deregulation in the US Trucking Industry. Applied Economics, 29(1), 101–110.

Giordano, J. N. (2003). Using the survivor technique to estimate returns to scale and optimum firm size. Topics in Economic Analysis & Policy, 3(1). https://doi.org/10.2202/1538-0653.1081

Hofmann, H. J. (1986). Minimum efficient plant size and the determinants of suboptimal capacity: An empirical analysis applying the survivor technique. Jahrbucher Fur Nationalokonomie Und Statistik, 201(2), 131–151.

Rao, C. R. (1973). Linear statistical inference and its application (2nd ed.). New York: Wiley.

Reekie, W. D. (1984). Minimum efficient scale in South-African industry: An application of the survivor technique. South African Journal of Economics, 52(3), 223–232.

Sands, S. S. (1961). Changes in scale of production in United States manufacturing industry, 1904–1947. The Review of Economics and Statistics, 43(4), 356–368.

Saving, T. R. (1961). Estimation of optimum size of plant by the survivor technique. The Quarterly Journal of Economics, 75, 569–607.

Shepherd, W. G. (1967). What does the survivor technique show about economies of scale. Southern Economic Journal, XXXIV, 113–122.

Stigler, G. (1958). Economies of scale. The Journal of Law and Economics, 1(3), 54–71. Reprinted in The Organization of Industry. 1968. Chicago: University of Chicago Press.

United States. Bureau of Economic Analysis. (1997) Benchmark input–output accounts for the U.S. economy, 1992 make, use, and supplementary tables. Survey of Current Business, November.

United States. Department of Commerce, Bureau of Census. (1987). Economic census: Census of manufacturers. Washington, DC: Government Printing Office.

United States. Department of Commerce, Bureau of Census. (1992). Economic census: Census of manufacturers. Washington, DC: Government Printing Office.

United States. Department of Commerce, Bureau of Census. (1993). Census of transportation: Commodity flow survey, table 5b shipments by three-digit commodity for the United States: 1993. Washington, DC: Government Printing Office.

Weiss, L. (1964). The survival technique and the extent of suboptimal capacity. Journal of Political Economy, 72, 246–261.

Williamson, O. E. (2005). The economics of governance. American Economic Review, 95(2), 1–18.

World Bank. (2004). http://www.worldbank.org/data/countrydata/aag/usa_aag.pdf. Accessed 4 Sept 2017

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Brown, J.H. Establishment Survivorship in U.S. Manufacturing, 1987–1992. Rev Ind Organ 53, 347–366 (2018). https://doi.org/10.1007/s11151-018-9613-4

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11151-018-9613-4