Abstract

In many R&D-intensive consumer product categories, firms deliver value to consumers through the quality enhancements provided by new and improved versions of existing products. Therefore, important marketing decisions relate to a firm’s strategy for developing quality enhancements and releasing new versions. This paper explores this type of product development using a dynamic duopoly model that endogenizes each firm’s decisions over how much to invest in R&D and when to release new versions. Specifically, I explore how two key industry fundamentals—the degree of horizontal differentiation and the cost of releasing a new version—affect firms’ product development strategies and, accordingly, the evolution of industry structure. I find that varying the degree of horizontal differentiation gives rise to three distinctly different types of competitive dynamics: preemption races when the degree of horizontal differentiation is low; phases of accommodation when it is moderate; and asymmetric R&D wars when it is high. Furthermore, I find that an increase in the cost of releasing a new version can induce firms to compete more aggressively for the lead and, in doing so, release new versions more frequently despite the higher cost.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

In many R&D-intensive consumer product categories, firms invest heavily in R&D in order to develop improvements for their existing products. They bring these improvements to market by periodically releasing new versions of their products that incorporate them. This is true of consumer electronics (e.g., smart phones, tablet computers, and video game consoles), software (e.g., office software suites and web browsers), and R&D-intensive consumer-packaged goods (CPG) categories, among others.

Consider the diapers category. Since the 1970s, Procter & Gamble (Pampers, Luvs) and Kimberly-Clark (Huggies) have intensely waged the so-called diaper war by investing heavily in R&D to develop improvements in comfort, absorbency, and containment, and bringing these improvements to market via version releases (Elzinga & Mills 1996; Parry & Jones 2001; Dyer et al. 2004). Both P&G and Kimberly-Clark have developed and incorporated reusable tabs, elastic leg bands, gel technology, and breathable material, among other improvements. This competition to innovate continues even today, as P&G and Kimberly-Clark continue to invest heavily in R&D to improve fit, absorbency, durability, and odor protection (Alfonsi et al. 2010). Other R&D-intensive CPG categories—such as toothpasteFootnote 1—have exhibited similar competitive dynamics.

In such categories, firms deliver value to consumers through the quality enhancements (or new “features”) provided by new versions. Therefore, important marketing decisions relate to a firm’s strategy for the development of product improvements and the timing of version releases. While they enhance demand, version releases are costly. Hence a firm may choose to accumulate new innovations over time and release a new version that incorporates them only periodically. Such categories are often concentrated because the high costs associated with both the R&D process and advertising serve as barriers to entry (Sutton 1991). Therefore, it is important to account for the strategic interaction that inevitably characterizes firms’ R&D investment and version release strategies. However, despite the prevalence of R&D-intensive consumer product categories, the academic literature has thus far given little attention to oligopolistic competition characterized by this type of product development.

In this paper, I seek to better understand how firms decide how much to invest in R&D to develop product improvements and when to release new versions of their products that incorporate them. Moreover, I explore how two industry fundamentals—the degree of horizontal differentiation and the cost of releasing a new version—affect firms’ R&D investment and version release strategies and, accordingly, the evolution of industry structure. I focus on these two industry fundamentals because they play key roles in determining a firm’s ability to profit from product development. The degree of horizontal differentiation determines the extent to which firms can translate successful product development into increased share, higher prices, and accordingly higher profits. The cost of releasing a new version determines the extent to which the cost of bringing product improvements to market erodes the increased profits that these product improvements can generate.

I model product development within the context of the Ericson & Pakes (1995) framework for numerically analyzing dynamic models of oligopolistic competition—in particular, dynamic stochastic games. (See Doraszelski & Pakes (2007) for a detailed review.) My model differs from earlier quality ladder oligopoly models (e.g., Pakes & McGuire 1994; Borkovsky et al. 2012) by allowing each firm to accumulate R&D successes (or “stockpile R&D”) over time and then decide exactly when to release a new version into which it attempts to incorporate them. Firms also engage in static price competition, where the degree of vertical product differentiation is determined by the firms’ (endogenous) product qualities, and the degree of horizontal differentiation is exogenous. Finally, the model restricts attention to the business stealing effect and in doing so abstracts from the market expansion effect in order to focus on how firms use R&D to improve competitive positioning. While the model could be used to study any of the product categories described above, because the model of price competition is static and therefore does not explicitly incorporate product durability, it perhaps best applies to R&D-intensive CPG categories.Footnote 2

The Ericson & Pakes (1995) framework is well-suited for studying the type of product development described above. First, the framework can easily accommodate a model in which firms make numerous successive releases, whereas the analytic theory literature on product launches tends to focus on new product introductions and therefore restricts attention to a single release decision per product.Footnote 3 , Footnote 4 Second, to study this type of product development, one must keep track of each firm’s product quality and R&D stock—the stock of product improvements that it has developed since its last version release. This demands a model with a multi-dimensional state space. However, dynamic stochastic games with multi-dimensional state spaces tend to be analytically intractable.Footnote 5 , Footnote 6 The Ericson & Pakes (1995) framework is well-suited for this problem because it allows for numerical analysis of models with multi-dimensional state spaces. Third, there are a few papers that explicitly consider repeated releases of the same product, but they either do so in a monopoly context (Ramachandran & Krishnan 2008) or they exogenize the behavior of rival firms (Morgan et al. 2001; Aizcorbe 2005). By numerically analyzing a model in the Ericson & Pakes (1995) framework, I am able to study such product development in an oligopolistic context. The equilibrium behaviors that I uncover (described in the next paragraph) are inherently oligopolistic and therefore could not possibly arise in a single-agent model. In summary, by numerically analyzing a model in the Ericson & Pakes (1995) framework, I am able to study an important type of product development that is not accessible through more familiar analytic research methods.

I find that varying the degree of horizontal differentiation gives rise to three distinctly different types of competitive dynamics. First, when the degree of horizontal differentiation is low, firms engage in preemption races; when neither firm has too large a lead, firms compete aggressively for the lead by investing heavily in R&D and releasing new versions frequently, and one firm eventually comes to dominate the market. Second, when the degree of horizontal differentiation is moderate, firms enter phases of accommodation during which they compete less aggressively. Accommodation is possible only because the leader induces the follower to sharply reduce its R&D investment by threatening to release a new version—which would incorporate its superior R&D stock—if the follower does not comply. Accommodation slows the leader’s march to market dominance. Third, when the degree of horizontal differentiation is high, firms engage in asymmetric R&D wars; i.e., they engage in aggressive competition once one firm achieves a sufficiently large lead. The understanding that aggressive competition would erupt were one firm to gain a large lead induces both firms to avoid striving for a large lead, hence neither firm comes to dominate the market. Finally, I establish that phases of accommodation and asymmetric R&D wars are unique to the setting I study in the sense that they arise only if firms can stockpile R&D and decide exactly when to release new versions.

The results summarized above emphasize the strategic nature of R&D stockpiling; in each of the three scenarios, a firm builds an R&D stock not only because it can ultimately enhance profits, but also because it can be used to influence rival behavior. (See Section 6.1 for details.)

I also explore the effect of the cost of releasing a new version (hereafter, the “release cost”) on firms’ product development strategies. Because an increase in the release cost erodes the profits that can be earned from future versions, one might expect it to induce firms to slow the pace of product development. However, I find that the opposite can occur; i.e., an increase in the release cost can induce firms to release new versions more frequently despite the higher cost. This perhaps counterintuitive result arises because as the release cost increases, it becomes more costly for a product market follower to catch up to the leader. This weakens the follower’s incentive to innovate and, as a result, the follower is less likely to ever catch up to the leader. So, a higher release cost makes the position of a product market leader more secure, which induces firms to compete more aggressively for the lead.

In addition to generating the insights described above, my model and results could be very useful for future empirical work. Dynamic oligopoly models have played a central role in recent empirical work in marketing and industrial organization; see Aguirregabiria & Nevo (2013) and Bajari et al. (2013). It can however be very difficult to adapt a given dynamic oligopoly model to a specific empirical context without first having a deep understanding of the equilibrium behaviors that the model admits. This presents a challenge because one cannot realistically aspire to understand such a model without thoroughly exploring it, and this is especially true if the model includes multiple choice variables—in this case, R&D investment and version release decisions—which can interact in complex ways.

Consider the following two examples of empirical papers that are based on computational applied theory papers that preceded them: Qi (2013) adapts the Doraszelski & Markovich (2007) dynamic model of goodwill advertising to explore the impact of the 1971 U.S. cigarette advertising ban on industry structure, and is able to corroborate their findings. Borkovsky et al. (2017) exploit the in-depth understanding of the quality ladder model that Borkovsky et al. (2012) deliver in order to adapt it to study brand management and measure brand value in the stacked chips category. This paper could play a similar role in facilitating empirical work on R&D-intensive consumer product categories. In Section 7, I discuss several product categories to which the model could be applied, as well as the ways in which one might tailor the model to address the challenges that those product categories present.

The paper proceeds as follows. Sections 2 and 3 describe the model and my computational strategy. Sections 4–6 present the results. Section 7 explains how this paper helps us better understand product development in categories characterized by repeated releases; discusses limitations and possible extensions; and concludes.

2 The model

I model product development within the context of a dynamic quality ladder duopoly (Pakes & McGuire 1994; Borkovsky et al. 2012). In this section, I present the model (Section 2.1), discuss two model assumptions (Section 2.2), and describe the equilibrium conditions (Section 2.3).

2.1 Model setup

The model is cast in discrete time and has an infinite horizon. A firm engages in product development so as to move up a “quality ladder”. Specifically, in each period, a firm makes two product development decisions. First, it invests in R&D in order to develop product improvements, which it can accumulate over time. Second, it decides whether to release a new version of its product into which it attempts to incorporate the improvements developed since its last version release. Each firm sells a single product; hence, a new version of a product replaces the previous version. Finally, in each period, firms’ engage in static price competition, where the degree of vertical product differentiation is determined by the firms’ respective (endogenous) product qualities, and the degree of horizontal product differentiation is exogenous.

Firms and states

The state of firm i ∈{1,2} is \(\omega _{i}\equiv \left ({\omega _{i}^{m}},{\omega _{i}^{R}}\right )\), where \({\omega _{i}^{m}}\) is the quality of the good firm i sells in the product market, and \({\omega _{i}^{R}}\) is the number of R&D successes that firm i has achieved—henceforth referred to as its “R&D stock”—since it released the current version of its product. Let \({\omega _{i}^{m}}\in \Omega ^{m}\equiv \{0,1,...,L^{m}\}\) and \({\omega _{i}^{R}}\in \Omega ^{R}\equiv \{0,1,...,L^{R}\}\). I devise a model of product market competition (presented below) that allows me to reduce the dimensionality of the state space by restricting attention to the difference between firms’ respective product qualities, \(\omega ^{m}\equiv {\omega _{1}^{m}}-{\omega _{2}^{m}}\in {\Omega _{d}^{m}}\equiv \{-L^{m},-L^{m}+1,...,L^{m}-1,L^{m}\}\).Footnote 7 (I refer to ω m as the product market state.) It follows that the industry state is \(\boldsymbol {\omega }\equiv \left (\omega ^{m},{\omega _{1}^{R}},{\omega _{2}^{R}}\right )\in \Omega \equiv {\Omega _{d}^{m}}\times \Omega ^{R}\times \Omega ^{R}\). (I use boldface to distinguish between vectors/arrays and scalars.) Firm i is able to change its R&D stock over time through investment x i ≥ 0. Firm i is able to change the quality of the good it sells in the product market by releasing a new version. When firm i releases a new version, each unit of its R&D stock is incorporated into the new version with some exogenous probability. This resets firm i’s R&D stock, \({\omega _{i}^{R}},\) to zero.

In each period, firms first compete in the product market. Each firm then decides whether to release a new version of—or “update”—its product. Finally, firms make R&D investment decisions. Below I elaborate on the sequence of events in each period, describe the static model of product market competition, and then turn to investment and version release dynamics.

Timing

Each period is divided into two subperiods. Version release decisions occur in subperiod 1 and R&D investment decisions occur in subperiod 2. The sequence of events is as follows.

In subperiod 1:

-

1.

Firms observe the prevailing industry state ω. Each firm then learns how much it would cost to release a new version of its product, i.e., it draws a private release cost ϕ i ∈ Φ from a distribution G(⋅).Footnote 8

-

2.

Firms compete in the product market and earn profits.

-

3.

The firms simultaneously decide whether to release new versions.

-

4.

The outcome of the version release process is realized; i.e., if a firm has chosen to release a new version, the release occurs and the firm learns how much of its R&D stock has been successfully incorporated into the new version of its product. The industry state transitions from ω to ω ′, and firms observe the new industry state. If neither firm chooses to release a new version, then ω ′ = ω.

In subperiod 2:

-

5.

The firms simultaneously decide how much to invest in R&D.

-

6.

The outcomes of investments in R&D are realized. The industry state transitions from ω ′ to ω ″, and firms observe the new industry state.

Product market competition

In each period, firms engage in static price competition with products that are differentiated both vertically and horizontally. There is a continuum of consumers. Each consumer purchases exactly one unit of one product, i.e., there is no outside option. As a result, the dynamic model restricts attention to the business stealing effect and abstracts from the market expansion effect. (This assumption is discussed further in Section 2.2.)

The utility a consumer derives from purchasing from firm i is \(b{\omega _{i}^{m}}-p_{i}+\sigma \epsilon _{i}\), where p i is the price, 𝜖 i represents the consumer’s idiosyncratic preference for product i, and σ > 0. Assuming that the idiosyncratic preferences (𝜖 1,𝜖 2) are independently and identically distributed as standard type 1 extreme value, the demand for incumbent firm i’s product is

where the subscript − i refers to the rival firm, p = (p 1,p 2) is the vector of prices, and m > 0 is the size of the market (the measure of consumers).Footnote 9 Like Anderson et al. (1992), I interpret the parameter σ as the degree of horizontal differentiation between products; as σ increases, consumers’ tastes are more heterogeneous, so consumers are less responsive to differences in prices and (vertical) qualities.

The demand that a firm faces is not a function of the firms’ absolute product qualities, but only of the difference between them. Therefore, I can write each firm’s demand function as a function of ω m:

In doing so, I have reduced the dimensionality of the state space.

Incumbent firm i chooses the price p i of its product to maximize profits. Hence, its profits in product market state ω m are

where p −i (ω m) is the price charged by the rival and c ≥ 0 is the marginal cost of production. A Nash equilibrium of the product market game (for a given ω m) is characterized by the system of optimality conditions derived from the firms’ respective profit-maximization problems.Footnote 10 Because product market competition is static, it does not directly affect state-to-state transitions in the dynamic model; hence, for the purposes of the dynamic model, the equilibrium profit function π i (⋅) can be treated as if it is exogenous (see p. 1892 of Doraszelski & Pakes 2007).

State-to-state transitions

Here I present an abridged description of the state-to-state transitions; see the Appendix for details. In each period, the firms’ respective updating and R&D investment decisions determine the industry state that arises in the next period. As explained above, in subperiod 1, a firm is able to enhance the quality of its product by releasing a new version, which incorporates each unit of the firm’s R&D stock with some probability. (The uncertain nature of version releases is discussed further in Section 2.2.) Specifically, if firm i possesses \({\omega _{i}^{R}}\) units of R&D stock and it releases a new version, its product quality improves by \(\bar {\omega }_{i}^{R}\in \left \{0,1,...,{\omega _{i}^{R}}\right \} \) units with probability \(s(\bar {\omega }_{i}^{R}|{\omega _{i}^{R}})\). This resets firm i’s R&D stock, \({\omega _{i}^{R}},\) to zero.Footnote 11

Consider, for example, the industry state (0,4,4). If only firm 1 releases a new version and it successfully incorporates three units of its R&D stock, then the industry transitions to state (3,0,4). If only firm 2 releases a new version and it successfully incorporates two units of its R&D stock, then the industry transitions to state (-2,4,0). Finally, if both firms 1 and 2 release new versions and they successfully incorporate three and two units of R&D stock respectively, then the industry transitions to state (1,0,0).

In subperiod 2, the industry is initially in state ω ′. Firm i’s R&D stock for the subsequent period, \(\omega _{i}^{R^{\prime \prime }}\), is determined by the stochastic outcome of its investment decision:

where ν i ∈{0,1} is a random variable governed by firm i’s investment x i ≥ 0. If ν i = 1, the investment is successful and firm i’s R&D stock increases by one. The probability of success is \(\frac {\alpha x_{i}}{1+\alpha x_{i}}\), where α > 0 is a measure of the effectiveness of investment.

Equilibrium

I restrict attention to symmetric Markov perfect equilibria in pure strategies. Theorem 1 in Doraszelski & Satterthwaite (2010) establishes that such an equilibrium exists.

2.2 Model discussion

In this section, I discuss the assumption that there is no outside option, and the assumption that R&D stocks are mutually observable. I then motivate the uncertainty that characterizes the version release process.

No outside option

As explained above, by assuming that there is no outside option, I restrict attention to the business stealing effect and abstract from the market expansion effect. This same assumption is implicitly made in the related analytic theory literature that uses dynamic quality ladder models to study R&D competition.Footnote 12 While the papers in that literature make this assumption for the purpose of analytic tractability, I make it for the purpose of computational tractability.Footnote 13 Moreover, like the aforementioned papers, by restricting attention to the business stealing effect, I focus on how firms strategically use R&D to improve competitive positioning. Finally, assuming that there is no outside option may be a reasonable abstraction when considering essential CPG products such as diapers and toothpaste, which are discussed in Section 1, among others. It would be interesting to explore the effects of both business stealing and market expansion effects. However, because doing so would dramatically increase computational burden, I leave this for future work.

Mutually observable R&D stocks

I assume that each firm can observe its rival’s R&D stock. In some industries—e.g., software and biotechnology—it is common practice for firms to publicly announce intermediate R&D successes (Jansen 2010). Furthermore, a firm might be able to gather information on a rival’s undisclosed R&D activities through competitive intelligence (West 2001). That being said, in some industries, a firm might learn how successful a rival’s R&D has been only once the rival releases a new version. It would certainly be interesting to explore a model in which firms cannot observe each other’s R&D stocks, and therefore possess beliefs about them that evolve over time and take into consideration the information divulged by version releases. However, because this would significantly complicate the model, I leave this for future work.

Uncertainty in the version release process

Before a new version is released, there are several reasons why a firm faces uncertainty as to how successful it will be. First, a firm is often uncertain about how much consumers will value product improvements.Footnote 14 Second, there are various reasons why a new feature might fail from a technical standpoint—e.g., incompatibility with the base product or with other new features—even after rigorous testing. Mennen’s 1972 launch of a new version of its deodorant, which incorporated vitamin E, was plagued by both of these problems. First, despite an extensive advertising campaign, customers were not able to understand how vitamin E improved deodorant and therefore did not value the addition (Rivkin & Sutherland 2004). Second, many customers suffered allergic reactions and, as a result, the product had to be pulled from the market (Rietschel & Fowler 2008). (On a separate note, in Section 3, I explain how incorporating uncertainty into the version release process mitigates the effect of the edge of the state space.)

2.3 Model derivations

In this section, I derive the Bellman equation, discuss the optimality conditions (see the Appendix for a full derivation), and describe the system of equations that characterizes an equilibrium.

Bellman equation

To derive the Bellman equation, I first consider the investment decisions that firms make in subperiod 2 and then the updating decisions that they make in subperiod 1. I let V i (ω,ϕ i ) denote the expected net present value of all future cash flows to firm i in industry state ω in subperiod 1, immediately after it has drawn release cost ϕ i . Firm i’s value function is \(\boldsymbol {V}_{i} : \Omega \times \Phi \rightarrow \mathbb {R}\) and its policy functions \(\boldsymbol {x}_{i} : \Omega \rightarrow \mathbb {R}\) and \(\boldsymbol {r}_{i} : \Omega \rightarrow \mathbb {R}\) specify its R&D investment and its probability of updating in industry state ω. (I derive the latter by integrating out the release cost ϕ i .) As I explain further below, because I solve for a symmetric equilibrium, it suffices to solve for the optimality conditions for one firm; hence I hereafter restrict attention to firm 1.

Investment decision

At the beginning of subperiod 2, the industry is in state ω ′. The expected net present value of cash flows to firm 1 is

where β ∈ (0,1) is the discount factor. Firm 1 chooses investment x 1 ≥ 0 that maximizes the expected net present value of its future cash flows. In the Appendix, I derive the optimality condition for firm 1’s R&D investment, x 1(ω ′); see Appendix Eq. 3.

Version release decision

At the beginning of subperiod 1, the industry is in state ω. Let firm 1’s perceived probability that firm 2 releases a new version of its product be r 2(ω). (In equilibrium, r 2(ω) will be determined by firm 2’s equilibrium updating strategy.) Firm 1’s value function \(\boldsymbol {V}_{1} : \Omega \times \Phi \rightarrow \mathbb {R}\) is implicitly defined by the Bellman equation

where \({Y_{1}^{1}}(\boldsymbol {\omega })\) is the expected net present value of firm 1’s future cash flows in industry state ω if it decides to update and firm 2 does not; \({Y_{1}^{2}}(\boldsymbol {\omega })\) is defined analogously for the case in which firm 1 does not update and firm 2 does; and \(Y_{1}^{12}(\boldsymbol {\omega })\) is defined analogously for the case in which both firms update.

In the optimization problem on the right-hand side of Bellman Eq. 1, firm 1 releases a new version (χ = 1) only if the new version yields greater value than its existing product, net of the release cost ϕ 1. It follows that firm 1 plays a threshold updating strategy; i.e., if it draws a sufficiently low release cost ϕ 1, it releases a new version and otherwise it does not. I derive this updating threshold and then, by integrating over the release cost ϕ 1, I derive a closed-form expression for firm 1’s optimal probability of updating, r 1(ω); see Appendix Eq. 8.

Solving for an equilibrium

Because I solve for a symmetric Markov perfect equilibrium, the investment decision taken by firm 2 in state ω is identical to the investment decision taken by firm 1 in state \(\boldsymbol {\omega }^{[2]}\equiv (-\omega ^{m},{\omega _{2}^{R}},{\omega _{1}^{R}})\), i.e., x 2(ω) = x 1(ω [2]). A similar relationship holds for the probability of releasing a new version and the value function: r 2(ω) = r 1(ω [2]) and V 2(ω,ϕ 2) = V 1(ω [2],ϕ 2). It therefore suffices to determine the value and policy functions of firm 1. Solving for an equilibrium for a particular parameterization of the model amounts to finding a value function V 1(⋅) and policy functions x 1(⋅) and r 1(⋅) that satisfy the Bellman equation and the R&D investment and updating optimality conditions in Appendix Eqs. 3, 8 and 9 respectively for all industry states ω ∈ Ω.

3 Computation

In this section, I explain how incorporating uncertainty into the version release process mitigates the effect of the edge of the state space. I also present the baseline parameterization and discuss the algorithm that I use to compute equilibria.

Mitigating the effect of the edge of the state space

The incentives that a firm faces when its R&D stock reaches the maximal level (ω i R = L R) are different from those it faces elsewhere because it cannot further increase its R&D stock. This general issue—that the edge of the state space distorts incentives—arises commonly in models in the Ericson & Pakes (1995) framework. It is typically addressed by assuming that diminishing returns set in sufficiently quickly as a firm approaches the edge of the state space.Footnote 15 It follows that from a firm’s perspective, the states on the edge are not too dissimilar from the states near the edge, which mitigates the effect of the edge of the state space.

I address this issue by introducing diminishing returns to R&D stock accumulation. Recall that when a firm releases a new version, it successfully incorporates each unit of its R&D stock with some probability; I assume that each additional unit of R&D stock is less likely to be successfully incorporated than the previous unit. Specifically, I assume that the nth unit of a firm’s R&D stock is successfully incorporated with probability ρ n, where ρ ∈ (0,1). It follows that when a firm attempts to incorporate a large R&D stock (say \({\omega _{i}^{R}}=10\)) into a new product, it is very unlikely to successfully incorporate all of its R&D stock units. See the Appendix for further detail.

Recall that a firm is uncertain as to how successful a new version of its product will be because (i) consumers may not value the improvements that are incorporated into the product, and (ii) the “improvements” may fail to be successfully incorporated for technical reasons. Therefore, the decreasing returns described above can be interpreted in two ways. First, the greater the number of new features that a firm incorporates into a new version, the less likely a consumer is to value each additional feature. This reflects the notion that consumers have limited attention for product attributes (Dahremoller & Fels 2015). Second, the greater the number of features that a firm attempts to incorporate, the less likely it is to succeed in incorporating each additional feature. This reflects the notion that it is more difficult to successfully incorporate many new features into a new version than it is to successfully incorporate only a few.

Baseline parameterization

I provide a few comments on the baseline parameterization, which is presented in Table 1. First, as \(\tfrac {L^{m}}{L^{R}}=2,\) a firm would have to make at least two version releases (while its rival made no releases whatsoever) in order to move from a state at which firms are tied in the product market to a state at which it achieves the maximal product market lead of 20 units. Selecting a relatively large L m value ensures that the edges of the state space at which ω m = 20 and ω m = −20 do not adversely affect equilibrium behavior. This is because the leader/follower roles that arise in equilibrium are established long before either firm begins to approach a state in which it achieves the maximal product market lead.Footnote 16

Second, the release cost, ϕ i , includes all costs that a firm might incur as it strives to transform its current product and the innovations that it has achieved since launching it into a new commercially-viable product that is successfully brought to market. This will typically include the costs required to incorporate the new innovations into the core product as well as the costs of a product launch and related marketing activities. However, the release cost also accounts for many possible complications. First, incorporating the new innovations might require unanticipated changes to the material requirements and/or the production process. Second, the new product might necessitate modifications to the existing packaging. Third, the existing distribution channel might not be ideally suited to the new product. Fourth, an important retailer (e.g., Walmart) might not immediately agree to stock the new product, or it might request product modifications. Finally, it might be impossible to simultaneously satisfy the different product specifications of two important retailers (e.g., Walmart and Target). Because the release cost incorporates a wide variety of different costs that might be incurred in launching a new version, I assume that the release cost is highly uncertain—specifically, that it is drawn from a uniform distribution over the interval [G l ,G u ] = [0,80].Footnote 17

Third, the discount rate of β = 0.951 corresponds to a period length of four months, an interest rate of 5% on an annualized basis, and an expected industry lifespan of 10 years—that is, in each period, the industry dies with probability \(\tfrac {1}{10\times \frac {12}{4}}=\tfrac {1}{30}\).

Algorithm

I first solve for the Nash equilibrium of the product market game (for each product market state ω m) by numerically solving the system of optimality conditions corresponding to the firms’ respective profit-maximization problems. The equilibrium profit function π i (⋅) is then treated as an input to the (Pakes & McGuire 1994) algorithm, which is used to compute Markov perfect equilibria of the dynamic model. To explore the equilibrium correspondence, I nest the (Pakes & McGuire 1994) algorithm in a simple continuation method (Judd 1998); see the Appendix for details.

4 Results: product market competition

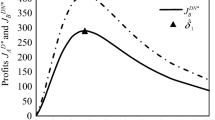

Before exploring the impact of changes in the the degree of horizontal differentiation on firms’ (dynamic) product development strategies, I explore the implications of such changes for firms’ (static) pricing strategies. In this section, I present the equilibria of the (static) product market game for low (σ = 0.1), moderate (σ = 2), and high (σ = 4) degrees of horizontal differentiation. Firm 1’s equilibrium price and profit functions are presented in Fig. 1, and its equilibrium market share functions are presented in the Appendix.Footnote 18

Equilibrium price p 1(ω m) (left panel), profit π 1(ω m) (middle panel), and the (discrete) rate of increase of profit π 1(ω m) − π 1(ω m − 1) (right panel) for σ = 0.1, 2, and 4

A low degree of horizontal differentiation

A low degree of horizontal differentiation (σ = 0.1) has several important implications. First, firms engage in aggressive price competition; hence, when they are tied in the product market—because neither firm has a quality advantage that it can leverage—they both earn very low profits. Second, a firm that gains even a small lead dominates the market in terms of share. Moreover, its profits increase relatively rapidly in the size of its lead because the larger its quality advantage, the higher the price it charges. Third, because a quality laggard sets very low prices and commands little market share, it earns extremely low profits that are highly unresponsive to the size of the leader’s lead.

A moderate degree of horizontal differentiation

When the degree of horizontal differentiation is moderate (σ = 2), as when it is low, a firm’s price and profits are strictly increasing in the size of its lead. However, due to the higher degree of horizontal differentiation, firms engage in less aggressive price competition, and a quality advantage does not translate into as large an increase in market share. This has several implications. First, the leader’s price and market share—and accordingly its profits—do not increase as rapidly as its lead grows. Second, a follower earns sizeable profits that increase substantially as it narrows the leader’s lead. So, unlike the σ = 0.1 scenario, a follower benefits from narrowing the leader’s lead even if it never overtakes the leader, or from slowing the rate at which the leader expands its lead. Third, following from the first two points, the benefits of leadership in the product market, while still significant, are not as great as when the degree of horizontal differentiation is low.

The first two points are summarized in the the right panel of Fig. 1, which presents the (discrete) rate at which a firm’s profits increase as its quality advantage grows (or its quality disadvantage declines). It emphasizes that an increase in the degree of horizontal differentiation makes the profit function flatter for the quality leader, but steeper for the follower; hence, it weakens the leader’s short-run incentives to invest in product development, but it strengthens those of the follower. The asymmetric impact of an increase in the degree of horizontal differentiation on the (short-run) investment incentives of the leader and follower has important implications, which are explored in Section 6.1.

A high degree of horizontal differentiation

A high degree of horizontal differentiation (σ = 4) induces firms to engage in even less aggressive price competition, and it only further softens the impact of a quality advantage on market share. Hence, it further reduces the benefits of leadership in the product market. Moreover, as the right panel of Fig. 1 emphasizes, the profit function becomes even flatter for the leader, and even steeper for the follower. Hence, the leader’s (short-run) incentives to invest in product development become even weaker, and the follower’s become even stronger.

5 A benchmark model with no version releases

Before turning to the results of the dynamic model presented in Section 2 (hereafter, the “full model”), I present results for a simplified version of the model (nested in the full model) in which firms cannot stockpile R&D and accordingly do not make version release decisions. Specifically, I assume that when a firm achieves an R&D success, it is immediately incorporated into its product with certainty and at no additional cost.Footnote 19 , Footnote 20 Benchmarking the model in Section 2 against this model will allow me to show exactly how the ability to stockpile R&D and decide on the timing of version releases impacts firms’ product development strategies.

In the benchmark model, because firms cannot stockpile R&D, the industry state is simply the product market state ω m. Because firms do not make version release decisions, each firm has only an R&D investment policy function. The model of product market competition is unchanged. In the Appendix, I restate the dynamic model while incorporating the simplifying assumptions described above.

In Fig. 2, I present equilibria for low (σ = 0.1), moderate (σ = 2), and high (σ = 4) degrees of horizontal differentiation. (I found only one equilibrium for each parameterization.) Firm 1’s R&D investment policy function is presented in the left panels.Footnote 21 To explore the evolution of industry structure over time, I use the firms’ equilibrium policy functions to compute the transient distribution over industry states in period t starting from state ω m = 0 in period 0. In the right panels of Fig. 2, I present the transient distributions for t = 30, which is the industry’s expected lifespan, and t = 100, which represents the long run.

Model with no version releases. Equilibria for σ = 0.1 (top row), σ = 2 (middle row), and σ = 4 (bottom row). R&D investment policy function x 1(ω m) (left panels) and transient distributions μ t m(ω m) for t = 30 and t = 100 (right panels)

The upper-left panel of Fig. 2 shows that when the degree of horizontal differentiation is low (σ = 0.1), firms engage in R&D preemption races; i.e., when neither firm has a large lead, each firm invests heavily in R&D in an attempt to become the market leader. Once one firm gains a lead of three units, it induces its rival to “give up”—i.e., to cease investing altogether; thereafter, because the rival no longer poses a threat to the leader’s leadership status, the leader reduces its R&D investment. The upper-right panel of Fig. 2 shows that this behavior gives rise to an asymmetric industry structure in the short and long run.

Preemption races are driven by the benefits of leadership in the product market. As explained in Section 4, because the degree of horizontal product differentiation is very low, a firm that gains only a small lead dominates the product market. It follows that each firm faces very strong incentive to become and remain the quality leader. Hence, when firms are tied in the product market, each firm invests heavily in R&D in an attempt to become the quality leader.

Moreover, in the middle panel of Fig. 1, one can see that the profit function is extremely flat for the follower (ω 1 < 0) and is quite steep for the leader (ω 1 > 0); hence, in the short run the follower can increase its profit negligibly by reducing the size of the leader’s lead, but the leader can increase its profit significantly by expanding its lead. It follows that a leader faces much stronger (short-run) incentive to invest in R&D than a follower. In a preemption race, each firm tries to exploit these incentives. That is, a firm invests heavily in R&D in hopes of gaining a lead over its rival because that lead would strengthen its own incentive to innovate and weaken its rival’s incentive to innovate. Accordingly, when one firm does gain a lead, it invests even more heavily and its rival invests less heavily, making it likely that the lead will only grow. This continues until the lead is large enough to induce the follower to give up, explaining why an asymmetric industry structure arises.

The middle-left panel of Fig. 2 shows that at a moderate level of horizontal differentiation (σ = 2), the preemption race is much milder, for several reasons. First, because the benefits of leadership are lower (as explained in Section 4), firms do not compete as aggressively for the lead. Second, because the higher degree of horizontal differentiation strengthens the follower’s (short-run) investment incentives and weakens those of the leader (as explained in Section 4), a lead is not as beneficial in terms of its differential impact on the investment incentives of leader and follower. Finally, for this same reason, the leader needs to achieve a much larger lead to induce the follower to give up, and this too weakens firms’ incentives to engage in preemption. As shown in the middle-right panel, it follows that the industry structure is more symmetric in both the short and long run.

The bottom panels of Fig. 2 shows that at a high level of horizontal differentiation (σ = 4), due to an amplification of the effects described above, firms engage in no preemption whatsoever, and this leads to a more symmetric industry structure in both the short and long run.

6 Results: the dynamic model of product development

In this section, I present results for the dynamic model of product development described in Section 2. Specifically, I explore the effects of two key industry fundamentals—the degree of horizontal product differentiation and the cost of releasing a new version—on product development strategies and, accordingly, the evolution of industry structure.

6.1 Horizontal differentiation

In this section, I show that low, moderate, and high degrees of horizontal differentiation give rise to three distinctly different approaches to product development.Footnote 22 Furthermore, by comparing the results to those of the benchmark model, I show that two of these approaches—for moderate and high degrees of horizontal differentiation—arise only if firms can stockpile R&D and decide exactly when to release new versions.

6.1.1 A low degree of horizontal differentiation

I first present the equilibrium for the baseline parameterization, at which the degree of horizontal differentiation is low (σ = 0.1). The equilibrium investment and probability of updating functions are mappings from the three-dimensional state space Ω to \( \mathbb {R}\); therefore, these functions are four-dimensional. I present equilibria by graphing three-dimensional cross-sections of these functions. Specifically, holding firm 1’s product market lead ω m fixed, I graph x 1(ω m,⋅,⋅), r 1(ω m,⋅,⋅), x 2(ω m,⋅,⋅) and r 2(ω m,⋅,⋅). Throughout the paper, I present cross-sections that best illustrate the equilibrium behaviors that arise. (All cross-sections of all equilibria presented and summarized below are available upon request.)

The ω m = 0 cross-sections of the equilibrium investment and probability of updating functions for both firms are presented in Fig. 3. From these figures, one can see how firms behave when they are tied in the product market. In particular, these figures present each firm’s investment choice and probability of updating for any possible pair of R&D stock levels \(({\omega _{1}^{R}},{\omega _{2}^{R}}\)). Firm 1’s equilibrium investment and probability of updating functions are in the top row of the figure; those of firm 2 are in the bottom row.Footnote 23

Preemption (σ = 0.1). ω m = 0 cross-sections of policy functions for R&D investment x i (ω) and release probability r i (ω) for firm 1 (top panels) and firm 2 (bottom panels)

Preemption races

Figure 3 shows that when firms are tied in the product market and neither firm has a large R&D stock lead, firms engage in a preemption race in which they invest heavily in R&D and release new versions with high probability. (Hence, I refer to this equilibrium as the preemptive equilibrium.) This behavior is reflected in the pronounced ridges—which I call preemptive ridges—that lie just off the diagonals of the cross-sections of all four policy functions. Figure 3 also shows that a firm can induce its rival to “give up”—i.e., to cease investing altogether and to release new versions with very low probability—by gaining a sufficiently large R&D stock advantage.Footnote 24 Hence, the preemption race can end even if neither firm has released a new version and, accordingly, firms are still tied in the product market. Once a rival has given up, it ceases to pose a significant threat to the leader, and the leader responds by significantly reducing its R&D investment and probability of updating. Before explaining why this behavior arises—and, specifically, how it relates to the preemption race of the benchmark model presented in Section 5—I present another cross-section of this equilibrium and then discuss the evolution of industry structure over time.

Figure 4 presents the ω m = 3 cross-sections of the equilibrium policy functions. From these figures, one can see how firms behave when firm 1 has a lead of three in the product market. These cross-sections are qualitatively similar to the ω m = 0 cross-sections. However, the preemption race does not occur when firms have similar R&D stocks—as in Fig. 3—but rather when firm 2’s R&D stock lead is large enough to threaten firm 1’s lead in the product market. In the heat of a preemption race, if both firms simultaneously release new versions, firm 2 is likely to catch up to firm 1 in the product market.

Preemption (σ = 0.1). ω m = 3 cross-sections of policy functions for R&D investment x i (ω) and release probability r i (ω) for firm 1 (top panels) and firm 2 (bottom panels)

Cross-sections of the equilibrium for other ω m ∈ {−10,...,10} are qualitatively similar to the cross-sections presented above; a preemption race occurs when the product market follower has a large enough R&D stock lead such that the expected product market lead would be close to zero if both firms updated simultaneously. Once the product market leader achieves a lead of eleven or more units, the follower ceases to invest; hence, firms no longer engage in preemption races. The qualitative differences between different cross-sections of the equilibria presented later in the paper are similar in nature to those discussed above. Therefore, I hereafter present only the ω m = 0 cross-sections of equilibrium policy functions.

To explore the evolution of industry structure over time, I use the equilibrium policy functions to compute μ t (⋅), the transient distribution over states in period t starting from state (0,0,0) in period 0. I then compute the transient distribution over product market states

for \(\omega ^{m}\in {\Omega _{d}^{m}}\), and I use this to compute the size of the leader’s expected lead in period t

In the left panel of Fig. 6, I present the transient distributions over product market states for t = 30 and t = 100. The industry is quite asymmetric after 30 periods, and extremely asymmetric in the long run; the size of the leader’s expected lead after 30 (100) periods is 15.94 (20.00).Footnote 25

Why do firms engage in preemption races?

The incentives that give rise to the preemption races observed in Figs. 3 and 4 bear some similarity to those that underpin the preemption race of the benchmark model. Both the full model and the benchmark model include the same static model of product market competition; therefore in both, when the degree of horizontal differentiation is low (σ = 0.1), firms compete aggressively for the lead because the benefits of leadership in the product market are high and a firm can dominate it by gaining only a small lead.

That being said, there are some features of the preemption races in Figs. 3 and 4 that are not explained by the benchmark model. First, the left panels of Fig. 3 show that even if the firms remain tied in the product market, a firm can influence its rival’s incentive to innovate by building an R&D stock advantage—inducing its rival to invest less in R&D and, if it falls sufficiently far behind, even to cease investing altogether. This means that a firm can achieve the leadership position in the industry without releasing even a single new version. This raises the question of why the rival would reduce its R&D investment and even give up altogether if it has not fallen behind in the product market. The reason is that firms’ R&D investment incentives are shaped not only by the current product market state, but also by their expectations over future product market states. Firms understand that—given the equilibrium updating probabilities—a firm with an R&D stock advantage is likely to soon become the product market leader.Footnote 26 Accordingly, a firm that finds itself at an R&D stock disadvantage anticipates that it will soon become the product market laggard and—because the profit function for the product market laggard is so flat—it faces extremely weak R&D investment incentives.

The above discussion emphasizes the strategic nature of preemption and, specifically, the strategic advantage that stems from having an R&D stock advantage. However, this raises an important question: In a preemption race, firms not only invest heavily in R&D, but also release new versions with high probability. It follows that a version release must also confer a strategic advantage.Footnote 27 However, while a version release can certainly enhance (static) profits, if it simply entails transferring R&D successes from a firm’s R&D stock into its product, why does it also generate a strategic advantage? In other words, why would it impact firms’ incentives to innovate?

Consider the industry state (0,1,1)—in which firms are tied in the product market and in terms of R&D stock. Suppose that firm 1 releases a new version and successfully incorporates its unit of R&D stock, bringing about a transition to industry state (1,0,1). While firm 1 now has a one unit lead in the product market, it is one unit behind in the R&D stock race. So, it might seem as if the firms are still effectively tied, which suggests that the version release should have no strategic impact whatsoever. However, the version release does indeed have a strategic impact, and it stems directly from the fact that the version release process is uncertain. In industry state (1,0,1), firm 2 finds itself at a disadvantage because to catch up to firm 1 in the product market it would have to release a new version and successfully incorporate its unit of R&D stock; however, there is no guarantee that the latter will occur. This disadvantage weakens firm 2’s incentive to innovate. In the Appendix, I show that if the uncertainty in the version release process is “turned off”, then firms engage in much less aggressive preemption in terms of version releases.Footnote 28

The discussion above emphasizes that firms engage in preemption in terms of both R&D investment and version releases because each can confer a strategic advantage. While R&D preemption arises in multistage patent racesFootnote 29 and in quality ladder models (Borkovsky et al. 2012), this paper shows that firms also preempt in terms of version releases and helps us understand why. (More importantly, none of the earlier models admit the behaviors that are described in Sections 6.1.2 and 6.1.3.)

6.1.2 A moderate degree of horizontal differentiation

I now explore the effect of a moderate degree of horizontal product differentiation (σ = 2). Recall that in the benchmark model, firms’ product development strategies when the degree of horizontal differentiation is moderate are qualitatively similar to those that arise when it is low; the only difference is that when it is moderate, firms engage in a milder preemption race. Here I show that the full model gives rise to a qualitatively different result, which arises because of the interaction between firms’ R&D investment strategies and their version release strategies.

Figure 5 presents the ω m = 0 cross-sections of the equilibrium policy functions. Before turning to the trenches that appear prominently in all four panels, I will describe other aspects of the policy functions. First, because an increase in the degree of horizontal differentiation reduces the benefits of leadership in the product market, it follows that—as in the benchmark model—firms do not compete as aggressively for the lead. Hence, while firms still engage in preemption races, they are characterized by lower R&D investments and updating probabilities than in the preemptive equilibrium. Second, as in the preemptive equilibrium, a leader tends to invest more in R&D and update with higher probability than a follower. This is because a leader’s short-run investment incentives are stronger than those of the follower, and because, as before, the follower determines that it would be too costly to invest in catching up. However, even though the follower accepts its role as the laggard, it does not give up altogether because, as explained in Section 4, it benefits from slowing the rate at which the leader increases its lead.

Accommodation (σ = 2). ω m = 0 cross-sections of policy functions for R&D investment x i (ω) and release probability r i (ω) for firm 1 (top panels) and firm 2 (bottom panels)

Phases of accommodation

In Fig. 5, in the cross-sections of firm 1’s policy functions in the upper panels and firm 2’s investment policy function in the lower-left panel, there are two trenches: one is at \({\omega _{2}^{R}}=1\) for \({\omega _{1}^{R}}\geq 3;\) the other is at \({\omega _{2}^{R}}=4\) for \({\omega _{1}^{R}}\geq 8\).Footnote 30 I refer to these as accommodative trenches; when the industry enters such a trench, it begins a phase of accommodation. (I hereafter refer to this equilibrium as the accommodative equilibrium.Footnote 31)

Consider the accommodative trench along \({\omega _{2}^{R}}=1\) for \({\omega _{1}^{R}}\geq 3\). This trench arises only once firm 1 has achieved a lead large enough to establish itself as the industry leader; once the industry reaches state ω = (0,3,1), it is extremely unlikely that firm 2 will succeed in overtaking firm 1 in the product market.Footnote 32 In this trench, firms accommodate each other as follows. Firm 1 invests less in R&D and releases a new version with lower probability. Hence, it slows its march toward industry dominance by both slowing the rate at which it stockpiles R&D and exercising greater patience in making its updating decisions. Firm 2 invests very little in R&D; therefore, it is unlikely to achieve an R&D success and accordingly its R&D stock is likely to remain \({\omega _{2}^{R}}=1\).Footnote 33 As a result, firm 2 ceases to threaten firm 1’s dominance.

Both firms benefit from this accommodation. Because firm 2 ceases to pose a threat to firm 1’s leadership, firm 1 can spend less on R&D and save on the cost of releasing a new version by patiently waiting for a low release cost. Firm 2 benefits because, having accepted its position as the eventual product market laggard, it is able to slow its rival’s march toward industry dominance; thus it earns higher transient profits as it recedes in the product market more slowly.

I next explain how accommodation is enforced. In particular, I explain how a leader induces a follower to sharply reduce its investment. In doing so, I highlight the strategic role of R&D stockpiling—specifically, the leader’s ability to influence the follower’s incentive to innovate by threatening to release a new version, which would incorporate its R&D stock. Consider firm 1’s policy functions in the upper panels of Fig. 5 and in particular the accommodative trench at \({\omega _{2}^{R}}=1\). To induce firm 2 to depress its investment in this trench, firm 1 sets sufficiently high R&D investment levels and updating probabilities for the neighboring states along \({\omega _{2}^{R}}=2\). It follows that were firm 2 to achieve an investment success, it would be punished by firm 1, which would dramatically increase its R&D investment and updating probability. Firm 2 would both become a product market laggard sooner rather than later and recede in the product market more quickly, and its profits would decrease accordingly. The results of the benchmark model in Section 5 show that accommodation does not arise in an otherwise identical model without R&D stockpiling and endogenous version releases; this demonstrates that the ability to use an R&D stockpile as a threat is essential for sustaining accommodation.

A phase of accommodation can come to an end in two ways. First, if the follower achieves an investment success, the industry transitions from the accommodative trench to an adjacent state that is outside of the trench. Second, if either firm elects to release a new version, the industry may transition to a different cross-section of the state space characterized by a different ω m value. In this other cross-section, the industry might immediately find itself in a different accommodative trench, or in a preemption race, or in neither; this all depends on the success of the version release and, accordingly, the magnitude of the leader’s product market lead after the release occurs.

The right panel of Fig. 6 presents the transient distributions over product market states. It shows that after 30 (100) periods, the industry structure is asymmetric; the size of the leader’s expected lead is 9.84 (19.98). Due to the albeit mild preemption races, and because the leader invests more in product development than the follower, one firm eventually gains as large a lead as is possible; however, it takes much longer under the accommodative equilibrium (90 periods) than under the preemptive equilibrium (60 periods), for several reasons. First, as explained above, the preemption races are milder. Second, the disparity between the leader’s and follower’s investments in product development is smaller. While these differences alone would slow the rate at which the firms diverge, the firms slow it even further by entering mutually beneficial phases of accommodation, allowing the leader to save on investment and upgrade costs and the follower to earn higher profits as it falls back more slowly than it otherwise would.

Transient distributions μ t m(ω m) for t = 30 and t = 100 for σ = 0.1 (left panel) and σ = 2 (right panel)

I conclude this section by explaining that the accommodation described above is very different from that which arises in two-stage “accommodation” games (see pp. 328-329 of Tirole1988), in which firms take some action in a first stage (e.g., restrict capacity) so as to soften price competition in a second stage. While the accommodation in such two-stage games is predicated only on irreversible investments made in the past, phases of accommodation depend critically on firms’ expectations for the future; specifically, firms’ accommodate one another because they both benefit from slowing the rate at which the industry evolves toward an asymmetric industry structure.

6.1.3 A high degree of horizontal differentiation

To explore the effect of a high degree of horizontal differentiation, I examine the three equilibria that I have found for the σ = 4 parameterization. Each row of Fig. 7 presents one equilibrium; the ω m = 0 cross-sections of the policy functions are presented in the left and middle columns, and the corresponding transient distributions for periods 30 and 100 are presented in the right column.Footnote 34 I briefly describe the equilibrium in the top row before moving on to a discussion of the asymmetric R&D wars that characterize the equilibria in the middle and bottom rows.

Three equilibria (σ = 4); one in each row. ω m = 0 cross-sections of policy functions for R&D investment x 1(ω) (left panels) and release probability r 1(ω) (middle panels). Transient distributions μ t m(ω m) for t = 30 and t = 100 (right panels)

The equilibrium in the top row is qualitatively similar to the accommodative equilibrium presented in Fig. 5. While the ω m = 0 cross-section includes only one accommodative trench (at \({\omega _{2}^{R}}=0\)), other cross-sections include additional accommodative trenches. Like the accommodative equilibrium presented above, this equilibrium ultimately yields an extremely asymmetric industry structure. The size of the leader’s expected lead after 30 (100) periods is 6.82 (19.76).

Asymmetric R&D wars

The equilibria presented in the middle and bottom rows of Fig. 7 are characterized by asymmetric R&D wars. I first describe these equilibria and then explain why asymmetric R&D wars arise.

Unlike the equilibria of the full model presented thus far, the equilibrium in the middle row of Fig. 7 admits no preemption whatsoever; i.e., on or near the diagonal—where neither firm has too large an R&D stock advantage—the R&D investment levels and updating probabilities of both firms are relatively low. Firms do however engage in asymmetric R&D wars; once one firm achieves a sufficiently large R&D stock advantage, both firms drastically increase their R&D investments. Hence, while firms do not engage in aggressive competition for the lead, they do engage in aggressive competition once one firm achieves a large lead. Because the follower invests more than the leader,Footnote 35 it tends to succeed in narrowing the leader’s lead and, as a result, a (nearly) symmetric industry structure arises; the size of the leader’s expected lead after 30 (100) periods is 1.36 (1.27). The aggressive R&D investment competition that occurs when one firm gains a sufficiently large lead both induces firms to avoid striving for a large lead and prevents a firm from sustaining such a lead if it is achieved.Footnote 36

The equilibrium in the bottom row of Fig. 7 is qualitatively similar to the one in the middle row, with one exception; firms engage in preemption by investing heavily in R&D when neither firm has too large a lead. The preemptive investment behavior gives rise to an industry structure that is more asymmetric than that of the equilibrium in the middle row; the size of the leader’s expected lead after 30 (100) periods is 3.55 (3.60). However, the industry structure is still relatively symmetric because, as in the equilibrium in the middle row, asymmetric R&D wars prevent either firm from gaining or sustaining a large lead.Footnote 37

Why do firms engage in asymmetric R&D wars?

I next explain why asymmetric R&D wars arise. In the preemptive equilibrium (Section 6.1.1) and the accommodative equilibrium (Section 6.1.2), a firm that falls behind accepts its role as the laggard, i.e., it invests in product development only in order to slow its decline in the product market. However, in an asymmetric R&D war, a laggard fights back by investing heavily in R&D in hopes of narrowing the leader’s lead (and this gives rise to aggressive competition because the leader responds by also investing heavily). As explained in Section 4, an increase in the degree of horizontal differentiation weakens the leader’s (short-run) incentives to invest in product development, and strengthens those of the follower. When σ = 4, the leader’s (short-run) incentives are sufficiently weak and the follower’s are sufficiently strong such that it is worthwhile for the follower to invest in catching up. However, R&D stockpiling and endogenous version releases also play a critical role. In fact, Section 5 shows that an otherwise identical model without R&D stockpiling and endogenous version releases does not admit asymmetric R&D wars.Footnote 38 This raises the question of why asymmetric R&D wars arise only when firms can stockpile R&D and decide when to release new versions.

In the full model, a firm that falls behind in the R&D stock race does not necessarily fall behind in the product market; rather, it falls behind in the product market only if its rival releases a new version. However, in the benchmark model, a firm that falls behind immediately becomes the product market laggard, and accordingly it necessarily finds itself on the flatter portion of the (static) profit function. It follows that falling behind (in the R&D stock race) in the full model does not weaken investment incentives as much as falling behind (in the product market) in the benchmark model. To put it more simply, in the full model, it is as if the R&D stock laggard strives to catch up to the leader before the leader releases a new version in order to avoid falling behind in the product market; in the benchmark model, the laggard has no such opportunity.

Finally, because the model admits qualitatively different equilibria at the σ = 4 parameterization (and more generally when the degree of horizontal differentiation is sufficiently high, see Fig. 10 in the Appendix), it follows that the nature of firms’ strategies and accordingly the industry structure that arises are determined not only by the parameterization, but also by the equilibrium itself.Footnote 39

6.2 Increasing the cost of releasing a new version

The cost of releasing a new version could increase for a wide variety of reasons, e.g., an increase in the complexity of incorporating product improvements into a new version, an increase in the cost of labor or capital that must be employed to launch a new version, or an increase in the marketing costs that must be incurred. I explore how an increase in the cost of releasing a new version affects firms’ product development strategies. Because the equilibria presented in Sections 6.1.1 and 6.1.2 are characterized by the two most prevalent behaviors that arise—preemption races and phases of accommodation—I use them as baselines. That is, I explore how these two behaviors change as the mean release cost increases. To this end, I use each equilibrium as a starting point for a simple continuation method in which I incrementally increase the mean release cost E[ϕ i ] = (G l + G u )/2 by increasing both G l and G u , while holding the width of the support, G u − G l , constant. In Fig. 8, I summarize each equilibrium computed using the size of the leader’s expected lead in period 30, L 30.

Leader’s expected lead at t = 30 vs. the mean release cost for σ = 2 (left panel) and σ = 0.1 (right panel)

I begin by exploring how the accommodative equilibrium presented in Section 6.1.2 changes as the mean release cost increases. In the left panel of Fig. 8, L 30 increases non-monotonically in the mean release cost. This non-monotonic relationship arises because increasing the release cost introduces two countervailing effects. The direct effect is intuitive; an increase in the release cost reduces the returns to innovation and accordingly weakens firms’ incentives to innovate. Therefore, firms invest less in R&D and release new versions less frequently. It follows that a market leader marches out toward industry dominance more slowly and accordingly the size of the leader’s expected lead in period 30 decreases. If this were the only effect at play, the size of the leader’s expected lead would be strictly decreasing in the mean release cost.

The strategic effect is perhaps less intuitive and arises strictly because of oligopolistic competition. As the release cost increases, it becomes more costly for a product market follower to catch up to the leader. This weakens the follower’s incentive to innovate. As a result, the higher the release cost, the less likely it is that the follower ever catches up to the leader. So, a higher release cost makes the position of a product market leader more secure. This induces firms to compete more aggressively for the lead by engaging in more aggressive preemption. That is, in the heat of a preemption race, a firm sometimes updates with higher probability—despite the higher cost—and invests more heavily in R&D. At the same time, phases of accommodation become less prevalent. For a sufficiently low mean release cost, the strategic effect dominates the direct effect. As a result, as the release cost increases, the industry converges to an asymmetric industry structure more quickly. The left panel of Fig. 8 shows that this occurs for E[ϕ i ] ≤ 66.5. However, for a sufficiently high release cost (E[ϕ i ] > 66.5), the direct effect dominates and accordingly the expected lead in period 30 declines as the release cost increases.Footnote 40

I next explore how the preemptive equilibrium presented in Section 6.1.1 changes as the mean release cost increases. The right panel of Fig. 8 shows that while the leader’s expected lead is non-monotonic in the release cost, the non-monotonicity is much milder than the one in the left panel. As the mean release cost increases, the direct effect quickly overwhelms the strategic effect and causes the size of the leader’s expected lead to decrease. This is because the preemptive equilibrium that serves as the starting point is already characterized by intense preemption and does not admit phases of accommodation. Therefore, the strategic effect—which intensifies preemption and lessens the extent of accommodation—has only limited impact before it is overwhelmed by the direct effect.

7 Discussion & conclusion

The purpose of this paper is to better understand product development that is characterized by repeated releases of new versions of existing products. To this end, this paper presents the first oligopolistic model of product development that endogenizes firms’ decisions over how much to invest in R&D to develop product enhancements and when to release new versions that incorporate them. I use the model to explore the role of two key industry fundamentals—the degree of horizontal product differentiation and the cost of releasing a new version—on firms’ product development strategies and accordingly the evolution of industry structure.

I find that varying the degree of horizontal differentiation gives rise to three distinctly different types of competitive dynamics: preemption races when the degree of horizontal differentiation is low; phases of accommodation when it is moderate; and asymmetric R&D wars when it is high. Furthermore, I show that phases of accommodation and asymmetric R&D wars arise only in a model that incorporates R&D stockpiling and (endogenous) version releases. My results also emphasize the strategic nature of R&D stockpiling, i.e., firms stockpile R&D not only because it can ultimately enhance profits, but also because it can be used to influence rival behavior.

I also explore the effect of the cost of releasing a new version on firms’ product development strategies. I find that an increase in the release cost can induce firms to compete more aggressively for the lead and, in doing so, release new versions more frequently despite the higher cost. This result yields a useful managerial insight. There are various reasons why an exogenous change in the cost of releasing new versions might occur. For example, in recent years, China has made efforts to develop a more high-tech economy and, as a result, some western firms have begun to build research labs there (Bradsher 2010; Hout & Ghemawat 2010). If firms anticipate that they will be able to outsource some of their R&D to China, this may ultimately reduce the cost of releasing a new version. One might be inclined to think that a decrease in the release cost would induce firms to release new versions more frequently and therefore intensify competition. However, the insights discussed in Section 6.2 explain why the exact opposite might occur; i.e., a decrease in the release cost could soften competition to innovate because it would make any product market lead less secure.

While the model presented in this paper perhaps best applies to R&D-intensive CPG categories, it could be augmented to study other types of categories. Consider the Internet browser industry. From 1995 to 2001, Microsoft and Netscape engaged in the first so-called browser war by both investing heavily to develop new features and releasing new versions of their respective browsers, which incorporated these features, on a frequent basis. Collectively, they released twelve versions in a span of only six years. By 2001, Microsoft’s Internet Explorer (IE) had won the browser war and come to dominate the market with a usage share of 90% (Markoff 2001). This brought an end to both the rapid innovation and the frequent version releases (Wildstrom 2003); Microsoft would not release another version of its browser for five years. In fact, in 2003, Microsoft announced that it would cease to release standalone versions of IE and that future enhancements would be bundled with operating system upgrades (Hansen 2003). However, in the face of increasing competition with the Mozilla Firefox browser—which included new features not offered by IE and had begun to encroach on IE’s usage share—Microsoft modified its strategy by releasing a new standalone version, IE7, in 2006. This version introduced several features that were already offered by Firefox and seemed to close the gap in perceived quality that had existed between IE and Firefox (Hoover 2006). Moreover, Microsoft announced its plan to release the next version of IE within 18 months (Hoover 2006), and ultimately released it after 29 months (Fried 2009). Therefore, in the face of the threat posed by Firefox, Microsoft began to release versions with greater frequency. While competition in this industry has been complicated by a host of other issues—such as the United States v. Microsoft antitrust case and the issues explored therein—strategically timed version releases that incorporate improvements developed through R&D have played a prominent role. Most notably, as explained above, Microsoft and Netscape engaged in a preemption race that was characterized by intense investment and frequent version releases until Microsoft came to dominate the browser market. This preemption race is similar in nature to those described in Section 6.1.1. However, while those preemption races can be attributed to a low degree of horizontal differentiation, the preemption race in the browser category likely arose because of the presence of indirect network effects.Footnote 41 Therefore, to apply this model to the browser category, it would be important to formally incorporate indirect network effects.Footnote 42

Another R&D-intensive CPG category that is characterized by periodic releases of new and improved versions is men’s razors with replacement blades. The market-leading brands, Gillette and Schick, have invested heavily in R&D to increase the number of blades, develop new ways of pivoting the blade head, increase lubrication, reduce friction, and improve razor grip (Richardson 2010; Chain Drug Review 2010). This category however also possesses two other important characteristics (Hartmann & Nair 2010): (i) razors are durable; and (ii) razors and blades are “tied”, i.e., a razor can only be used with compatible blades produced by the same manufacturer. Therefore, to model product development in this category, one would allow consumers to make forward-looking razor adoption and replacement decisions (Gordon 2009; Goettler & Gordon 2011). Furthermore, one would allow firms to make forward-looking product development and pricing decisions for both razors and blades, taking into consideration the implications of product complementarity for the demand of each product.Footnote 43

As with any theoretical work, this paper has limitations. First, as illustrated by the above examples, some R&D-intensive consumer product categories are complicated by other important characteristics such as indirect network effects, product durability, and the tied nature of products. If one is interested in studying one such category in particular, then it might be important to formally account for the relevant characteristic.

Second, in some categories—e.g., razors and blades—a manufacturer continues to sell the old version of a product even after the new version is released. I have abstracted from this because my objective is to study firms’ product development strategies; once a new version is released, even if a firm continues to sell the old version, it rarely invests in improving it. Moreover, while it would be theoretically straightforward to incorporate this into the above model, it would significantly increase the computational burden because it would add several dimensions to the state space (one for each old product that continues to be sold).

Third, the model in this paper does not include entry and exit. If one is interested in studying competition between a small number of national brands that dominate a market that has seen little if any entry or exit—like the U.S. diaper market (discussed in Section 1)—then one might abstract from entry and exit. Otherwise, one might incorporate entry and exit in order to explore how firms strive to prevent entry and induce exit via their product development strategies.Footnote 44 (Borkovsky et al. (2012) show that in the presence of entry and exit, firms investing in R&D to enhance product quality engage in both limit investment and predatory investment.)