Abstract

We adopt a Cointegrated Vector-Autoregressive (CVAR) model to analyze the long-run behavior and short-run dynamics of stock markets across five developed and three emerging economies. Our main aim is to check whether liquidity conditions play an important role for stock market developments. As an innovation, liquidity conditions enter the analysis from three angles: in the form of a broad monetary aggregate, the interbank overnight rate and net capital flows which represent the share of global liquidity that arrives in the respective country. A second objective is to understand whether central banks are able to influence the stock market.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Starting with the `Great Moderation’ in the mid-1980s, five phenomena have influenced and characterized economic conditions and financial markets, especially in developed markets: First, low and constant inflation rates; second, strong and persistent money growth and the unprecedented access companies, financial investment firms and ordinary people have to borrowing and foreign exchange; third, a massive increase in world trade, financial globalization and international capital flows; fourth, large asset price swings and an increased number of financial crises and finally, reduced output volatility.

Many economic observers point to globalization and the resulting pricing-to-market of companies to explain concurrent low inflation rates. They hypothesize that, contrary to conventional theory, abundant liquidity in the system has not led to goods price increases. Instead it is the antecedent to excessive asset price rises and increased volatility, such as in housing, commodities and stocks (Rogoff 2006, p. 2).

Price increases in real goods and services usually lead to reduced demand and substitution. This is not true in the case of asset prices. For example, rising share prices are regarded as a sign of confidence and breed optimism. Thus, ordinary people invest more money when prices go up and less when prices go down.

Abundant liquidity can exacerbate this pattern (Borio et al. 1994, p. 67). It is easier and cheaper for people, hedge funds and companies to borrow under conditions of ample liquidity. If portions of these additional funds are invested, prices are pushed up further and optimism spreads (Allen and Gale 2000, p. 239). Crowd behavior, for example in the form of herding, and rational speculation are signs of this process and lead to market exaggerations (Pepper 1994, pp. 24–28, Rajan 2005, p. 3). After all, even if prices departed from justified long-run levels it is still lucrative to bet on rising prices if the stocks can be sold at a higher level before a potential bubble bursts. Thus, irrationally high levels on the stock market may result from rational speculation and people’s perception that they are smarter than others and able to get out before the market turns (Campbell et al. 1997, p. 258). This runs contrary to the idea that in a market in which information is processed efficiently the actual value of stocks corresponds to the fundamental value. However, as Keynes (1936, p. 156) already pointed out in 1936, stock market levels do not necessarily reflect fundamental values. Instead, they reflect average expectations of what other market participants expect the market to do (on average). The Keynesian investor buys when prices rise and sells when they fall, that is, adopts positive feedback investment strategies (English 2001, p. 121). This further exacerbates stock price inefficiencies.

Additionally, confidence and optimism are also boosted because owners of assets feel richer if house or share prices increase. This results in increased spending on goods and assets (Kuttner and Mosser 2002, p. 16). The former helps companies increase profits and, thus, also leads to increases in share prices and the valuation of bonds (Borio et al. 1994, pp. 22–23). As a result, the number of defaults decreases and lenders want to lend more to participate in the upswing, thereby, further perpetuating it. In addition to healthier balance sheets, due to less defaults, banks are also directly influenced by rising asset prices. Adrian and Shin (2007, pp. 2-4) point out that banks, which very much like hedge funds or private equity funds actively target their leverage ratio, react to rising or falling asset prices. Asset price increases lead to stronger balance sheets and a higher net worth for banks. Higher net worth means lower leverage as leverage is inversely related to total assets. To keep the leverage ratio constant and at target level, banks engage in additional borrowing and invest the proceeds into more assets. As a result, leverage is procyclical, amplifying the already existent spiral between asset prices and money. The additional borrowing might show up in broad monetary aggregates. This additional `monetary’ liquidity also improves `market’ liquidity.Footnote 1 Market liquidity, in turn, increases rational speculation further as there always seems to be a ready buyer. Easier financing also enables executives to launch share buyback schemes, which at the same time increases stock prices and market liquidity.

The same self-reinforcing mechanism applies once markets have turned sour. When prices decline, previous overconfidence turns into crippling uncertainty and lenders demand that borrowers hold more collateral. At the same time, falling asset prices decrease the amount of collateral, forcing borrowers to sell assets. This drives prices down further. In addition, forced selling leads to inefficient asset liquidation, which is associated with additional costs (Allen and Gale 2002, p. 35). If banks have to write off loans in a market downturn their equity capital ratio might drop under a critical level of capital requirements set by the authorities. This leaves banks with two options (Belke and Polleit 2009, p. 37): dispose of risky assets and/or issue new equity. Whereas the latter is difficult in times of market distress and painful for existing share holders, the former lowers asset valuations and with it increases banks’ capital losses further (Allen and Gale 2000, p. 253). This downward spiral is aggravated further because investors’ concern rises and funding costs increase.

In conclusion, rising asset prices, abundant credit and liquidity conditions, optimism, confidence and rational speculation all feed into each other and amplify the normal behavior of stock markets. By this token, the same mechanisms apply in a downturn. This reasoning indicates a long-run relationship between liquidity/‘excess liquidity’ and stock market levels with a potential inclusion of economic activity or other macro variables. Four testable hypotheses can be derived from the above discussion:

-

H1 - Market agents’ behavior (herding, rational speculation, contagious confidence and optimism) leads to strong persistence in stock market developments, i.e., shocks to the stock market have positive long-run effects on future developments;

-

H2 - Long-run equilibria exist between stock prices and liquidity conditions;

-

H3 - Liquidity conditions influence stock prices positively in the long run;

-

H4 - Liquidity conditions influence stock prices positively in the short run.

Liquidity conditions can be described via the quantity of money, either the total level or the amount in excess of demand and via the price of money, i.e., the short-term interest rate.

The high level of integration of the international financial markets points to the importance of cross-country capital flows for domestic developments. Strong economic activity and rising stock markets attract foreign investments, which, in turn, enforce market trends. In addition, if a stock market boom is built on foreign money, the withdrawal of external financing often leads to a reversal of the direction of the market. In addition, inflation and markets seem to be strongly driven not only by national circumstances, but also by global trends and sentiment. The substantial growth of international capital flows and the cross-border holdings of financial assets and liabilities are indicative of this (Lane and Milesi-Ferretti 2006, pp. 12–14, 33–34). This has led to the growing influence of foreign portfolio decisions on domestic stock markets. International capital flows also influence the above mentioned liquidity conditions. This suggests the inclusion of the following testable hypotheses:

-

H5 - International capital flows have a positive long-run impact on the stock market behavior of individual countries;

-

H6 - International capital flows have a positive short-run impact on the stock market behavior of individual countries.

The above described mechanisms have led to ever larger swings in asset prices, with a potentially harmful effect on the real economy, as exemplified by the global financial crisis that started in July 2007 and more generally analyzed by Reinhart and Rogoff (2009, pp. 4-10) and Helbling and Terrones (2003, pp. 69-70). But, even before this severe financial crisis, economists began asking whether or not central banks should include asset prices in monetary policy setting or target them directly. The issue is still under discussion. Moreover, the ability to target asset prices in a manner which influences stock prices is unclear. Notwithstanding this lack of knowledge of central bank abilities, equity prices play a major role in various theories of the monetary transmission mechanism. This leads to the following questions which have to be answered empirically:

-

Q1 - Are central banks able to influence stock prices in the long run?

-

Q2 - Are central banks able to influence stock prices in the short run?

The objective of this contribution is to empirically analyze hypotheses H1 - H6 and answer questions Q1 - Q2 on a national level. The empirical analyses focus on five developed economies and three emerging markets, namely the United States (US), the euro area, Japan, the United Kingdom (UK), Australia, South Korea, Thailand and Brazil. The goal of the country comparisons is to distinguish features that may influence the above described relationships. We focus on the previous before the financial crises to assure that our results are not affected by unconventional monetary policy after the onset of the financial crisis.Footnote 2

Since cointegration between non-stationary data series represents the statistical expression of the economic notion of a long-run economic relation, the above outlined issues are analyzed applying the parametric approach of the cointegrated vector autoregressive (CVAR) model. The classification of the data generating process into stationary and non-stationary parts enables the distinction between long-run equilibria and short-run dynamic adjustment. In addition, common trends that push the variables and determine the long-run impact of shocks to the variables can be identified.

There exists a wide array of angles in approaching the topic of money and stock prices. Over the last 60 years, many authors have tried to corroborate empirically that there is a relationship between money and stock prices (Sprinkel 1964; Hamburger and Kochin 1972; Chen et al. 1986; Friedman 1988). Most studies focus solely on the US market. Obviously, an exhaustive overview is impossible, simply because the amount of literature is too vast. While empirical methods have changed over the course of the years, the main result has remained the same: overall evidence is mixed. Some authors find a significant and causal relationship between money and stock prices (Marshall 1992; Dhakal et al. 1993; Lastrapes 1998). Others can not reject empirically that the relationship does not exist at all (Lee 1992). And a third group is able to show that causality runs from stocks to money (Hashemzadeh and Taylor 1988; Gouteron and Szpiro 2005).

For the most part, publications that focus on national stock markets and domestic macro variables apply cointegration analysis.Footnote 3 Unfortunately, the interpretation of the results remains questionable since important information on the behavior of the variables in the system is either ignored or not provided. For example, many analyses do not restrict the cointegration space, which enables empirical testing of the cointegration relations and provides information on the significance of the coefficients. In addition, the analysis of the short-run adjustment structure is widely ignored. This, however, is essential to determine whether or not the stock market actually reacts to the variables in the system.

The main conclusion that can be drawn from this discussion is that scholars still argue over whether or not a relationship exists, and if it does exist, how important it is and in which direction causality runs. Room for improvement exists via a full and correct analysis of liquidity conditions and stock market behavior in a cointegrated VAR framework, which includes long-run equilibria as well as short-run dynamics and the long-run impact of shocks to the variables.

2 Data

The concept of liquidity can be interpreted in many different ways and liquidity measures differ widely. However, there is no `best’ liquidity measure that fulfills all purposes. Instead, the important point is to choose a measure that is in line with the objectives of the study.

Monetary aggregates can be used to analyze the portfolio-balance effect and, together with inflation, whether higher inflation has a negative relationship with the stock market can be tested. One theory that describes the linkage between changes in the quantity of money and the stock market is the portfolio-balance effect, which represents the Monetarist view. It shows that increased money supply leads to a portfolio rebalancing towards other assets, such as stocks (Meltzer 1995, p. 52; Brunner 1961, pp. 52–53). This asset reallocation results in upward pressure on stock prices, which, in turn, enables a new equilibrium level between money holdings and other assets in investors’ portfolios (Sprinkel 1964, pp. 11–12). Higher money supply may also have a negative effect on stock prices, which results from increases in expected inflation. Inflation uncertainty rises with the absolute level of inflation and can have adverse consequences on the stock market (Ball and Cecchetti 1990, p. 215; Taylor 1981, pp. 59–71; Okun 1971, pp. 493–497).

The main distinctions of monetary aggregates are between narrow and broad money and between the overall level of liquidity and measures of excess liquidity. Broad instead of narrow money is chosen to avoid the influence of portfolio allocations of money holdings in the private sector on the monetary aggregate. In addition, the instruments included in broad money reflect the readily available liquidity position, which can be used for stock market investments. If a stable cointegration relationship exists between money and its demand determinants, the residuals describe the monetary overhang (excess liquidity), which then is a stationary variable (Belke and Polleit 2009, p. 686). In this case, the impact of excess liquidity on stock markets can be analyzed.

In addition to the quantity of money available, liquidity can also be measured via the price of money, which is the short-term interest rate.Footnote 4 Interest rate movements affect stock market prices mainly in three ways: one is via the relative attractiveness of the investment alternatives bonds and stocks (Mishkin 2001, p. 2). The other two can be rationalized via the standard present-value evaluation principle. First, a decreasing interest rate reduces the discount factor with which future dividend payments are transferred to the present value (Sellin 2001, p. 492; Baks and Kramer 1999, p. 5). Second, lower interest rates might exert a positive effect on aggregate output, which, in turn, increases economic prospects and dividends and, thus, also increases the present value of equity investments (Adalid and Detken 2007, p. 12; Tobin 1991, p. 14). On the basis of the present value formula, a discount rate and a measure of the income from stocks should be included. GDP might be used as a proxy for the latter, indicating changes in dividends. The long-term interest rate can proxy the yield on alternative assets. In addition, the short-term interest rate can be associated with a proxy for the interest paid on money (ECB 1999, p. 30). Moreover, and more importantly, it can be used to analyze the abilities of central banks, since the short-term interest rate is the preferred monetary policy operational target of central banks around the globe (King 2003, p. 85).

Last, it needs to be discussed whether it is preferable to focus on global or national money developments. To account for the fact that capital is increasingly mobile and can be readily deployed internationally, capital flows are included in the analysis. The capital flow proxy applied by us measures the flows that affect the money stock and, hence, liquidity conditions in the respective country. Capital flows are included instead of global liquidity because of the focus on country-level analyses and aggregation issues connected with global liquidity. Capital flows in this contribution are derived according to the `Monetary Presentation of the Euro Area Balance of Payments’(see, ECB 2003, p. 15). However, we feel legitimized to argue that net flows of the Balance of Payments (BoP) are less helpful because of the double-entry system of the BoP. All financial transactions enter the financial account twice, once on the credit side and once on the debit side. This means that, by definition, financial transactions alone always have a net balance of zero. Consequently, the `financial and capital account’ balance mirrors the `current account’ balance. Accordingly, net flows in the BoP only depend on the net amount of goods and services traded and the net income and net current transfers. While it is true that this is the amount of money flowing into or out of the country, it is not a complete measure of transactions that actually affect the money stock. If foreigners buy stocks and bonds of domestic companies from residents, this also increases the domestic money stock. In addition, the amount of financial transactions financial transactions is sometimes larger than that of real transactions. However, these `financial’ effects are not included in the net BoP and, thus, the net balance is an inferior liquidity measure with regard to overall liquidity conditions in a country and the analysis of stock price movements.

The `Monetary Presentation of the Euro Area Balance of Payments’ has been developed to highlight the effects of international transactions on monetary developments. The underlying idea is the fact that money and banking statistics (i.e., the consolidated balance sheet of the domestic banking system) and BoP data are derived from a coherent methodological framework. As a result, the change in the net external position of the domestic banking sector can be presented as the mirror image of the external transactions of the banking system in the BoP, which, in turn, is the same (with the opposite sign) as the external transactions of non-bank residents in the BoP. The derivation of the capital flows time series, as used here, closely follows IMF (2008, pp. 335-336), BeDuc et al. (2008, pp. 12-16) and Bank of England (2006, pp. 13-18).

As a result of the above discussion, the data vector consists of the following variables:

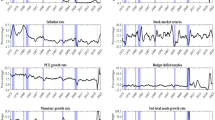

where mr is the log of real broad money, sr is the log of real stock market levels (total market including dividends) and yr is the log of real GDP. Real variables are transformed from nominal variables using the consumer price index, p, and, hence, Δp is the inflation rate.Footnote 5 Short and long-term interest rates are represented by the overnight interbank rate, or, and the 10-year government bond yield, b10.Footnote 6 All interest rates have been converted to quarterly rates and divided by 100 to achieve comparability with the inflation rate (logarithmic quarterly changes, Juselius and Toro 2005, p. 515). Capital flows, cf., are calculated in percent as a share of the total money stock M3. All time series are obtained either from Datastream or the IMF International Financial Statistics (IFS) database.

Table 1 provides information on data characteristics of the individual country analyses. The data used for the quarterly analyses covers the last 25 years with the exception of Thailand and Brazil.Footnote 7 Our motivation for starting the sample period in 1983 was to ensure a constant parameter regime. Therefore, the volatile and high-inflation periods of the 1970s and the beginning of the 1980s are excluded. In addition, the starting point was chosen such as to follow the Fed’s decision to abandon targeting the money supply in favor of setting a target for the Fed funds rate.

3 Econometric approach - the cointegrated VAR framework

Many empirical analyses, which are based on macroeconomic variables, use the VAR model as a starting point. The variables used are usually assumed to be stationary or allowed to be non-stationary, even though stationarity is a necessary and sufficient condition for valid statistical inference (Johansen 1995, p. 11).Footnote 8

To allow for non-stationarity in the data and to be able to determine long-run equilibria as well as the above mentioned adjustment forces a CVAR model with Gaussian errors is applied (Hoover et al. 2008). The idea is to formulate a well-specified statistical model and then apply the principle of maximum likelihood to estimate the parameters. This parametric approach allows for a formal check of the model specification and for testing of economic hypotheses.

For a detailed presentation and discussion of the econometric methodology of the CVAR model see Juselius (2006) and Johansen (1995). As a starting point, consider the p-dimensional VAR(k) model,

Where xt is a (p × 1) vector of endogenous variables and єt is an error term, which is assumed to be independently and identically distributed (i.i.d.) multivariate normal with constant variance: єt~i. i. d. Np(0, Ω), where Ω is a (p × p) covariance matrix. (π1, …, πk) is a (p × p) matrix of unrestricted parameters, Dt is a vector of general deterministic terms, such as a constant, a linear term, seasonal dummies and intervention dummies and Ф is the corresponding vector of unrestricted parameters.Footnote 9

The error-correction version of the VAR (k) model is used to account for non-stationarity in the data and to facilitate the economic interpretation. The vector equilibrium-correction model reformulates the VAR model in terms of differences, lagged differences and levels of the process. It is obtained from a reparametrization of (2):

where \( \uppi =\sum \limits_{\mathrm{i}=1}^{\mathrm{k}-1}{\uppi}_{\mathrm{i}}-{\mathrm{I}}_{\mathrm{p}} \)and \( {\Gamma}_{\mathrm{i}}=-{\sum}_{\mathrm{j}=\mathrm{i}+1}^{\mathrm{k}}{\uppi}_{\mathrm{j}} \).

The properties of xt can be investigated by solving the characteristic polynomial associated with eq. (3):

with determinant ∣π(z)∣. If π(z) has a unit root, z = 1, i.e., ∣π(1)∣ = 0, then -∣π(1)∣ = π is of reduced rank r < p, and π can be decomposed into π = αβ′ where and are (p x r) of rank r. The presence of a unit root in the VAR model corresponds to non-stationary stochastic behavior, which can be accounted for by a reduced rank restriction of the long-run levels matrix π = αβ′. By substituting π = αβ′ into (3) an expression for the CVAR model, which is the reduced form error-correction model, is obtained:

where the parameters (α, β, Γt, ..., Γk − 1, Ф, Ω) vary freely.

The main advantage of modeling non-stationary data is being able to focus on two economic aspects. On the one hand are the stable economic relations between the variables and the related adjustment dynamics. On the other are the cumulated disturbances, referred to as common trends, which lead to the non-stationary behavior in the data (Johansen 1995, p. 34). The latter are analyzed via the moving-average (MA) representation and can be used to determine the long-run impact of shocks to the levels of the variables.Footnote 10 For an I(1) process the number of unit roots equals p-r, which is the same as the number of common stochastic trends. The common stochastic trends describe the long-run movements of the series. They are combinations of the cumulated residuals of each variable. Put in a different way, cointegrated variables share the same stochastic trend. As such they can not drift too far apart. As a result, cointegration and common trends are two sides of the same coin.Footnote 11

Using the CVAR model means `letting the data speak’. Thus, a theoretic model is not directly estimated in the empirical model. However, some macro relations that are often assumed to explain the economy are helpful in statistically testing for stationary relationships in the data. The ideas from theoretical economic models can be expressed as statistical concepts. In this case `economical’ long-run steady-state relations can be interpreted as cointegrating relations in the statistical model. Table 2 summarizes relationships between our variables, which are based on standard economic theory (see, for example Blanchard (2009)). In each case, linear combinations of the variables represent stationary long-run relations. In addition, a time index is added.

We translate the relations in Table 2 into testable hypotheses within the CVAR framework. We test them individually in each specific country analysis to improve the identification procedure of an economically and statistically identified long-run structure. Since sub-elements of the relations might be stationary, they also have to be tested to arrive at a complete picture. The respective hypotheses run as follows:

where H is the design matrix, ϕ contains the restricted parameters and φ is a vector of parameters which are freely estimated. Thus, the hypotheses test restrictions on a single vector but leave the other vectors unrestricted (Johansen and Juselius 1992, pp. 233–236).

4 Results

4.1 Overview of empirical analysis

The empirical analysis is structured as follows. We organized it primarily by country, in each case assessing long-run equilibria, short-run dynamic adjustments and long-run impact. To keep our pre-sentation managable in length the results of the individual country analyses are not reported in detail except those for the US as a benchmark. Instead, the focus is on cross-country comparisons. The structure of each country analysis is the same. They all begin with a presentation of the data and model specifications that guarantee a statistically well-specified model. To achieve this, the variables of the system are defined and deterministic terms and the lag length is specified and tested.Footnote 12 Once a well-specified model is obtained, the cointegration rank is determined.Footnote 13 Table 3 provides information on the included deterministic components, lag length and cointegration rank.

Afterwards, the focus is on the identification of the long-run structure. This starts with a first inspection of the unrestricted -matrix and some preliminary hypotheses testing before turning to the final identified long-run structure. Preliminary tests include a couple of tests for β′ and α. Automated tests β′ include the possibility to exclude variables from the long-run relations and stationarity of individual variables. The α-matrix is formally analyzed for weak exogeneity and unit vectors. Afterwards, we conduct single cointegration tests in order to test for potential long-run equilibria, as outlined in Table 2. Table 3 shows the results on stationarity and weak exogeneity.

As an example, the structural representation of the cointegration space of the US analysis is depicted in Table 4 which contains the estimated eigenvectors β and the weights α. The restrictions on the identified long-run structure are accepted with a p-value of 0.35. This shows that the imposed restrictions describe the data well. The structure can be considered formally and empirically identified because all -coefficients are strongly significant (Juselius and MacDonald 2004, p. 18). The rank conditions are accepted for the full cointegration space. This means that the four cointegration relations are linearly independent and, as such, cannot be replaced by each other. The graphs of the cointegrating relations look stationary and our plots of the empirical realisations of forward and backward recursive tests of parameter constancy show that parameter constancy for αi and βi (i = 1, …, 4) is given (not reported here).

The first cointegrating relation, listed in Table 4 describes liquidity, wealth and balance sheet effects on aggregate demand for goods:

with real activity being positively related to real money and the stock market. The α -coefficients show that output is significantly adjusting to this relation and that it takes approximately five quarters to reestablish equilibrium after innovations in real money or the stock market.Footnote 14 In addition, deviations from the long-run steady state between real output, real money and the stock market exert positive pressure on inflation and the short-term interest rate. The positive reaction of the inflation rate can be interpreted in the framework of the short-run Phillips curve, where inflation increases with excess aggregate demand for goods (Juselius 2001, p. 344).

The second long-run relation in in Table 4 describes a relationship between `excess liquidity’ (in its weak form) and inflation:

where inflation is driven by money growth exceeding increases in transactions. It has to be stressed that this is a very simple representation of excess liquidity. The inflation rate strongly reacts to this relationship and the α-coefficient of 1 indicates that inflation corrects disequilibria over the course of one quarter. In addition, the analysis of the α-coefficients shows that both interest rates are positively influenced by deviations from this equilibrium. This is a sign that the Fed reacts to increases in the inflation rate and the bond rate reacts to higher expected inflation.

The third β -vector describes a homogeneous relationship (i.e., the coefficients sum to zero) between the short and the long-term interest rate as well as inflation:

Both interest rates show dynamic adjustment behavior towards this relationship. This indicates that it can be interpreted either as a bond rate relation or a fed funds rate relation. Economically, it is more reasonable to regard it as a bond rate relation because it shows that the bond rate is positively related to the fed funds rate (term structure hypothesis) and inflation (expected inflation effect). The bond rate takes approximately four quarters to restore the long-run equilibrium.

In addition, using the homogeneity property of relation 9, it can be restated to reflect cointegration between the yield spread and the long-term real interest rate:

This, in turn, shows that the interest rate spread and the real interest rate form a stable long-run relationship. Cointegration between both interest rates and the inflation rate suggests that a single nominal trend drives all three processes (Cassola and Morana 2002, p. 22).

The last cointegrating relation consists of the capital flows variable, which is found to be stationary on its own:

The α -coefficient shows that capital flows error correc with high significance and take less than two quarters to reverse towards equilibrium. Additional analysis of the last column in the α -matrix shows that capital inflows increase inflation and reduce long-term interest rates. This is in line with previous findings in the literature that inflationary spillover effects exist between countries and that large capital inflows suppress long-term yields in the US.

Once an overidentified long-run structure is tested and fixed, we analyze short-run dynamics in the framework of a structural error-correction model.Footnote 15 Significant short-run effects are tested for by applying the full information maximum likelihood estimator in simultaneous equation modeling. To be able to understand short-run adjustments of the variables, we identify and test an economically valid short-run structure. Since the long-run structure is fixed, the equations of the system variables in first differences can include the stationary equilibrium errors of the cointegration relations.

Finally, in the last part of our analysis we focus on the common trends and the permanent impact of shocks to the variables.Footnote 16 The C-matrix provides the key to understanding the long-run implications of the model. It contains information on the overall effects of the stochastic driving forces in the system. Central banks can only influence the stock market in the long run if a shock to a monetary instrument has a significant impact on the stock market.

The residual ϵi, t is interpreted as an estimate of the unanticipated shock to variable xi. Taking the US analysis as an example, the estimated long-run impact of these cumulated shocks is reported in Table 5. Since C has reduced rank, only p - r = 3 linear combinations of the p = 7 innovations, t, have permanent effects. The C-matrix can be read column or row-wise. The columns show the long-run impact of a shock to a variable on each of the variables in the system and the rows show which of the shocks have a long-run impact on the particular variable.

The C-matrix displayed in Table 5 confirms the exogeneity of real money and real stock market levels. Both variables are only influenced by themselves in the long run. This indicates the procyclical behavior of the money stock due to credit expansion in good economic times and credit constraints during economic downturns. For the stock market, this confirms the herding and trend-following behavior of economic agents. The C-matrix also shows that for the period under investigation, the Fed was unable to influence stock market developments in the long run, which confirms findings of Durham (2003, p. 2).

Aside from that, the C-matrix shows that shocks to both, real money and the stock market, have positive long-run effects on the level of economic activity. The positive reaction of real output to shocks to the stock market confirms previous findings. Based on a multivariate VAR-analysis Lee (1992, p. 1602) finds that shocks to stock returns help to explain a substantial fraction of the variance in real output for postwar monthly data.Footnote 17

In addition, shocks to real money translate into higher inflation. This means that the Fed’s decision to disregard broad monetary developments and to stop reporting M3 must be seen as a mistake. Another interesting finding is the non-existent long-term impact of the fed funds rate on inflation, which indicates that the Fed was unable to control inflation over the past 25 years. This result is confirmed by cointegration analyses conducted earlier by Christensen and Nielsen (2003) and Johansen and Juselius (2001).

4.2 Empirical findings of main hypotheses - cross-country comparisons

This section provides an aggregated overview of the results of the main hypotheses. Table 6 shows the results of our empirical tests of the hypotheses with respect to the main objectives of this contribution across the eight regions of the analysis.

A more sophisticated picture of the above findings can be obtained by investigating the respective hypotheses in more detail. Table 7 provides a more comprehensive overview of the effects of the included macro variables on the stock market in the long and short run. The former is constructed such as to cover all aspects of our empirical analysis, including long-run effects and equilibria (columns a to e) as well as short-run dynamics (columns f to j).

Columns a and b show which cumulated shocks to the variables have a significant positive or negative long-run impact on stock markets, respectively. Columns c to e provide information derived from the long-run cointegration relations, which can be interpreted as economic equilibria between the variables. Columns c and d show to which of the variables the stock market is related in the long run and to which it dynamically adjusts in the short run. These entries are based on the cointegration relations depicted in column f. Column e, on the other hand, shows cointegration relations in which the stock market variable is present but the stock market does not react to disequilibria.Footnote 18

As usual, the analysis of the short-run dynamics is divided into adjustment to the equilibrium errors of the cointegration relations and significant effects of lagged variables. More precisely, on the one hand, column f documents the cointegration relations, to which the stock market shows error-correction behavior. Columns g and h, on the other hand, demonstrate to which disequilibrium errors the stock market reacts without being part of the cointegration relation. Finally, the entries in columns i and j list the positive and negative significant effects of lagged values of the variables in first differences. We derive these effects by applying the full information maximum likelihood estimator in simultaneous equation modeling. Dissecting the findings in Table 6 with the help of Table 7 adds insight to the main conclusions of our research exercise.

4.2.1 Stock market persistence

One objective of this contribution, as hypothezised in the introduction, is to test whether or not confidence and optimism of market participants are important factors for the development of stock prices. Our empirical findings show that past stock market movements are much more important for stock market developments in the long run than in the short run. While the persistent long-run effect is statistically valid in every country contained in our empirical analyses, significant short-run effects can only be identified in the analysis of Thailand. This suggests that confidence and optimism of market participants are very persistent and translate into self-reinforcing and trend-following behavior.Footnote 19 This pattern also confirms that rational speculation can be reasonable even if markets diverge from fundamental values (Trichet 2005, p. 2). This result is in line with findings by Brunnermeier and Nagel (2004) on hedge fund behavior during the dot-com boom.

This empirical finding of long-run stock market movements coincides with the erratic short-run behavior of stock markets. This means that bearish developments in a bull market and bullish developments in a bear market are acceptable characteristics of the long-term persistence of stock markets. In addition, our empirical finding adds to the broad evidence of the stock market’s susceptibility to bubbles and crises and the often observed phenomenon that upturns and downturns last longer than widely expected.Footnote 20

4.2.2 Long-run equilibria between liquidity conditions and the stock market

According to our results, liquidity and real output developments appear to play a role for stock markets. The long-run equilibria between the stock market, liquidity and/or real output (depicted in columns e and f in Table 7) show that these variables are often subject to a common driving trend. One explanation for this could be the often cited `animal spirits’ which might represent a common driving trend that affects all three variables (Mishkin 2001, p. 16; Keynes 1936, pp. 161–162). The three aspects of the economy have inherent procylicality in common. This means that current developments of real money, the stock market and real output amplify the respective existing trend. Sprinkel (1964, p. vii) describes this pattern by saying that "[i]t is the basic thesis of this exposition that economic and stock price changes have a common `cause', changes in money, which directly influence the demand for assets such as common stock as well as the demand for goods and services". This contribution, however, maintains that the direction of causality is not so clear. It does show, though, that the variables are tied together. However, the combination of variables that react to reestablish the long-run equilibrium differs across countries. The results displayed in Table 7 show that the stock market does not react to these long-run equilibria in the four most developed economies in our sample. This shows that while the hypothesis of existent long-run equilibria can be accepted, it is, nevertheless, a quite unsatisfying finding and contrary to the stock market behavior that was expected from the outset.

Another objective of this contribution is to test whether or not abundant liquidity amplifies the upward and downward spirals of stock prices, which is represented by hypotheses H3 and H4 in Table 6. A closer look at Table 7 reveals that real money does not affect stock prices in the four most developed financial markets, namely, the US, the euro area, Japan and the UK. This is contrary to the widespread belief that "developments in monetary aggregates and credit play an important role in the development of asset price boom episodes" (Trichet 2005, p. 5).Footnote 21 Real money developments do, however, play a role for Australia, and for two of the three Emerging Markets included in our analysis, South Korea and Brazil.Footnote 22 As such, the results on the liquidity hypotheses are mixed.

Different country-specific reasons might help to explain why liquidity conditions affect the stock market in developed countries less than it does in developing economies. First, over the period under investigation, abundant liquidity might not have been predominantly channeled to the stock market but into real estate.Footnote 23 The real estate bubbles in the US, the UK and parts of Europe at the beginning of the 1990s and the first years of the new millennium exemplify this. This is further indicated by the analyses of Belke et al. (2008, pp. 416-420) and Giese and Tuxen (2007, pp. 22-24), who identify the positive impact of global liquidity on global real estate prices, but not on global stock markets. Even though their analyses are based on global liquidity, strong movements in housing prices might be the prime reason for the missing direct link between money and stocks in the US, the UK and the euro area.Footnote 24

Rising house prices, however, should in principle also serve as an argument for the Australian market for which the positive effect of real money on stocks could be corroborated by us. This apparent puzzle leads us to a second argument. Liquidity conditions facilitated a major bull market in global commodities.Footnote 25 This, in turn, had a positive impact on the Australian stock market, which is characterized by a high share of commodity-related stocks.Footnote 26 This property could explain the stronger role of real money for stock prices in Australia in comparison to the above mentioned developed countries.

Third, some specific macroeconomic circumstances can explain our results for Japan. The extended period of economic stagnation and difficulties in the banking sector after the burst of the stock market and real estate bubbles have distorted the relationship between money and stock prices. The BoJ’s policy of `quantitative easing’ has not led to goods or asset price inflation because the BoJ was unable to alter the economic agents’ expectations.Footnote 27 Deflationary expectations led people to save more and invest less in goods or stock markets. The positive short-term impact of inflation on the stock market is indicative of this (see column i in Table 7). While in other countries inflation has a negative impact on the stock market, this is not true for Japan according to our results. The reason for this might be found in the different perception of inflation. After the bust of the stock market and real estate bubbles, Japan’s main concern was deflation rather than inflation. Hence, inflation was perceived as an indication of improving economic conditions and, consequently, helped to spur stock market upturns.

Fourth, financial markets in the US, the euro area, Japan and the UK are so deep that additional money only plays a subordinate role for stock market developments as a whole. Consequently, liquidity conditions have a bigger impact on Emerging Countries’ less developed financial markets.

4.2.3 Capital flows and the stock market

A third objective is to understand how global liquidity conditions, proxied by capital flows, affect the stock market (hypotheses H5 and H6 in Table 6). Our focus is on net capital flows because they represent the share of global liquidity that actually flows into a given country. A closer inspection of the importance of capital flows delivers the following pattern. The time series for capital flows is found to be stationary every second of the countries under investigation, namely the US, the euro area, Japan and Australia. This has the direct consequence that capital flows and the stock market can not form a long-run relation because cointegration can not exist between stationary and non-stationary variables. Nevertheless, cumulated shocks to capital flows could have a permanent effect on the stock market. In addition, the stock market could react to lagged values of capital flows in the short run. This is not the case for any of the developed countries. This is in line with previous findings, as for instance Warnock and CacdacWarnock (2006, p. 1): "evidence of any meaningful impact of capital flows on large economies is scarce.".Footnote 28

Capital flows do play an important role in the long and short run for South Korea and Brazil. This confirms that external financing is more important for emerging economies than for established markets. Unlike financial markets in industrialized countries, financial markets in South Korea and Brazil are less deep but are still very open. As a result, international developments as well as investments from abroad play a more prominent role. As such, it appears reasonable for central banks in emerging economies to closely monitor international capital flows.

4.2.4 Ability of central banks to influence stock markets

The final aim of this contribution has been to test whether or not central banks are able to influence stock prices. The empirical findings corroborate the popular view that the ability to influence the stock market is limited.Footnote 29 Table 6 documents that only in Australia and in Thailand stock markets are negatively influenced by the central bank policy rate. One could argue that the money market rate does not completely reflect central banks’ actions. Instead, the target rate should be used.

However, both interest rates move closely together. In addition, the market-determined overnight rate has one main advantage, taking into account, that monetary policy is closely followed and anticipated by economic agents. Consequently, central bank communication can affect markets without altering the short-term target rate. Quite often changes in the market interest rate happen before the policy action. As a result, the important monetary impulse for the markets takes effect before the announcement. Consequently, the subsequent `actual monetary policy shock’ has no effect (Meltzer 1995, p. 50).

It is often argued that the `surprise’ element of monetary policy might be the part of monetary policy that is relevant for financial markets (Kuttner 2001, pp. 533–535). The surprise could be a result of central bank communication or of unexpected interest rate changes. This reasoning is confirmed by findings of Bernanke and Kuttner (2005, p. 1253). They conclude that for the US only monetary policy surprises can explain part of stock market variability. The econometric method applied herein only includes monetary policy expectations in so far as they can be explained by the other macro variables in the system. The unexpected part is left in the residuals of the overnight rate. Consequently, the residual єi, t is interpreted as an estimate of the unanticipated shock to variable xi. The estimated long-run impact of these cumulated shocks is analyzed in the long-run impact matrix and is calculated from the estimates of the restricted VAR model. If the `surprise’ element of monetary policy were important for stock markets it would show up in the analysis herein.

The disappointing finding concerning central banks’ inability to influence stock markets actually has a clear bearing on the current policy debate over the question of how to deal with asset prices in monetary policy. On the one hand, it is crucial to understand central banks’ abilities to affect other macro variables. On the other hand, it is important to analyze, which variables affect monetary policy decisions.

5 Concluding remarks

This contribution applies the CVAR model to analyze the long-run behavior and short-run dynamics of stock markets across five developed and three emerging economies. The governing thought is that liquidity conditions play an important role for stock market developments. Liquidity conditions enter the analysis from three angles: in the form of a broad monetary aggregate, the interbank overnight rate and net capital flows, which represent the share of global liquidity that arrives in the respective country. A second objective is to understand whether central banks are able to influence the stock market.

The empirical findings demonstrate that the widely assumed impact of real money developments on stock prices in developed economies is very limited. Aside from Australia, no significant effects can be identified. A potential reason for the non-existent effect on stock prices could be that the abundant liquidity is being directed into real estate and commodities.

Our empirical analysis establishes, however, that real money, real output and the stock market form a stationary cointegration relation in most countries. This demonstrates that these variables are driven by a common trend. The forces behind this common trend must be analyzed further in future research. The starting hypothesis should be that the common trend is based on `animal spirits’ of market agents, which increase the inherent procyclicality of all three variables. This is further indicated by the self-reinforcing effects of stock price developments, which are present in the data across all countries because shocks to the stock market have a significant long-run impact on future stock prices. These self-reinforcing effects could be the result of behavioral effects, such as, among others, over-confidence, rational speculation or herding.

Our empirical results differ with respect to the Emerging Markets in our sample. Here, liquidity conditions play a significant role for stock market behavior. Both real money and capital flows have a significant positive short and long-run impact on stock prices in South Korea and Brazil. In addition, the short-term interest rate influences the stock market negatively in Thailand.

Seen on the whole, our results suggest that the ability of central banks to affect stock prices through changes in the policy rate is very limited. While being in line with previous findings, this result raises two follow-up questions, which have not yet been answered: first, if the policy rate has no significant effect on equity valuations, what does this imply for our current understanding of transmission mechanism theories that incorporate equity prices?Footnote 30 Second, which monetary policy instruments have a superior ability to affect stock prices in a desired way? It is especially crucial to solve this issue be-cause our empirical analysis shows that stock price developments have a significant effect on the real economy. Hence, we feel legitimized to argue that central bankers should pay more attention to asset price developments and consider alternative instruments to influence stock prices, such as changes in the minimum reserve requirement or active communication. While the difficulty of communicating asset price-based policy changes to the public has been recognized, the timing, right in the aftermath of the global financial crisis, could not be better. The chances for investors and the general public to understand the issue and, hence, the probability of gaining their support for a policy change might never be higher than now.

Notes

Brunnermeier and Pedersen (2007, pp. 35-37) find that market liquidity and funding liquidity are mutually reinforcing, which can lead to liquidity spirals. This also implies that central banks can influence market liquidity by affecting funding liquidity.

See Beckmann and Belke (2015) for a related analysis which includes the period of the financial crises. In contrary to our analysis, they also include sentiment indicators in their analysis.

The inclusion of not only a quantity measure but also of a price indicator of money, is in line with the reasoning of, for instance, the IMF, because an easing of liquidity conditions tends to show up in both an extending stock of money and lower interest rates (IMF 1999, pp. 118–121).

For our empirical analysis we have chosen the consumer price index instead of the GDP deflator for two main reasons. First, we want to capture monetary policy aspects. Thus, consumer price inflation is superior to the GDP deflator because central banks focus on consumer price developments. Second, within the scope of money demand analysis a cost-of-living index is preferable to the GDP deflator because it is a more important determinant of transaction balances (Muscatelli and Spinelli 2000, p. 722).

The data vectors for Thailand and Brazil do not include the long-term interest rate because a continuous bond market did not exist for most of the time period under investigation (Inoguchi 2007, p. 392). In addition, before the Asian financial crisis, the Thailand bond market was heavily regulated and had a very low trading volume due to the inefficient infrastructure of tax and information disclosure procedures. For a detailed presentation of the developments of the Thai bond market, see Ganjarerndee (2001, pp. 642-684). As a result, the long-term interest rate is inoperative for the purposes of the econometric analysis.

Throughout the whole contribution, ex-post revised data is used. This has the consequence that the effect of publications of real-time data can not be measured. However, the focus of the analysis is on the underlying fundamentals, not on announcement effects. Consequently, revised data is closer to the actual behavior of the economy. In addition, studies at the Deutsche Bundesbank by Döpke et al. (2006a, 2006b) show that predictions of stock returns and volatility based on real-time macro data do not differ much from hypothetical predictions, which are based on revised data.

See Johansen (2007, pp. 5-8) for a discussion of spurious correlations and the interpretation of correlation and regression in non-stationary economic time series. This view is confronted by Sims et al. (1990, pp. 136-137), who show that in a VAR analysis of non-stationary variables the ordinary least square estimates of the coefficients are consistent for a broad set of circumstances.

Seasonal dummies are included because throughout the whole contribution seasonally unadjusted data is applied where available. Seasonal adjustment procedures are problematic if the underlying time series is subject to structural shifts (Brüggemann and Lütkepohl 2006, p. 685).

The MA representation can be derived from (5) using Granger’s representation theorem (see Johansen 1995, Theorem 4.2, p. 49).

One discrepancy between the two, however, is the different behavior when the information set is increased. While the cointegration relations are not affected, the common trends are (Johansen 1995, p. 42).

Lag length is determined by the two information criteria ‘Schwartz’ (SC) and ‘Hannan-Quinn’ (H-Q) as well as the Lagrange multiplier (LM) test for autocorrelation. To ensure statistical validity of the model, multivariate and univariate tests on autocorrelation, normality and ARCH are conducted.

Since the distinction between stationary and non-stationary directions of the vector process is not always straight for-ward several formal and informal procedures are applied to determine the rank: trace test (formal LR test), modulus of the roots of the companion matrix, significance of the α-coefficients, graphical inspection of the recursively calculated trace test statistics and graphical inspection of the stationarity of the cointegration relations (Juselius 2006, p. 142).

The positive relation between the stock market and economic activity has been documented by several studies, for an overview see Mauro (2000, p. 3).

To save space, the structural error-correction model is not presented here.

See also Dhakal et al. (1993, p. 71) for similar findings.

To enhance readability of the table, the coefficients to the parameters of the cointegration relations are left out. The idea here is to gain understanding of significant relationships between the variables. The same table exists for all variables of the system to understand the drivers behind them. They are not reported here but are available on request.

For a theoretical model that describes the persistence of stock market bubbles, see Abreu and Brunnermeier (2003, pp. 178-197).

For example, Alan Greenspan’s warning of `irrational exuberance’ in 1996 came four years before the end of the dot-com bubble, with the Dow trading at 6.500 points and perhaps too early to be taken seriously by market participants (Ito 2003, p. 549).

One has to keep in mind, though, that the empirical findings herein are based on boom and non-boom conditions. The focus is on the total sample and the general relationship between money and stock prices instead of being restricted to boom and bust phases.

South Korea is regarded as a developing country even though it is by now considered developed. However, since the analysis focuses on the last 25 years, it is fair to say that over that time period it was in transition from a developing to a developed country.

Since housing prices are not included in the analysis, this is not tested herein.

Greiber and Setzer (2007, pp. 15-17) support this finding in their US analysis.

Approximately 200 of the 500 companies listed in the All Ordinaries Share Price Index conduct business in commodity related areas (Standard&Poor’s 2009).

In addition, a portion of the created liquidity has been invested abroad (carry trades).

This was one reason not to focus on the traditional measure of capital flows, which is the current account of the BoP, but to determine, which parts of capital flows affect monetary aggregates. Unfortunately, this has not delivered much additional insight for the behavior of developed economies’ stock markets.

This finding confirms previous analyses of the effectiveness of changes in the policy rate. For an overview of the policy rate and house prices, see Kohn (2008, p. 5) and the mentioned articles. One should note, though, that most articles focus on the fed funds rate and the US market. This contribution, however, confirms this result for other markets as well.

Many theories of the monetary transmission mechanism, such as the asset price channel, the balance sheet channel and the liquidity effects view, are based on the initial relationship between interest rates and asset prices (Mishkin 1995, pp. 5–9).

References

Abreu D, Brunnermeier MK (2003) Bubbles and crashes. Econometrica 71:173–204

Adalid, R., Detken, C., 2007. Liquidity shocks and asset price boom/bust cycles. ECB working paper series no. 732, February 2007

Adrian T, Shin HS (2007) Liquidity, monetary policy and financial cycles. Curr Issues Econ Financ 14

Allen F, Gale D (2000) Bubbles and crises. Econ J 110:236–255

Allen F, Gale D (2002) Liquidity, asset prices and systemic risk. CGFS Conference Vol. No. 2, Part 1, October 2002

Baks K, Kramer C (1999) Global liquidity and asset prices: Measurement, implications, and spillovers. IMF Working Paper No. 168

Ball L, Cecchetti SG (1990) Inflation and uncertainty at short and long horizons. Brookings Papers on Economic Activity No. 1:1990, p 215–254

Beckmann J, Belke A (2015) Money, stock prices and central banks - Cross-Country Comparisons of Cointegrated VAR Models. J Bank Financ, Elsevier, vol. 54(C), p. 254-265

BeDuc L, Mayerlen F, Sola P (2008) The monetary presentation of the euro area balance of payments. ECB Occasional Paper Series No. 96

Belke A, Polleit T (2009) Monetary economics in globalised financial markets. Springer-Verlag, Berlin

Belke A, Orth W, Setzer R (2008) Sowing the seeds for the subprime crisis: does global liquidity matter for housing and other asset prices? IEEP 5:403–424

Belke A, Bordon IG, Hendricks TW (2009) Global liquidity and commodity prices - A Cointegrated VAR Approach for OECD Countries. Ruhr Economic Papers No. 102

Bernanke BS, Kuttner KN (2005) What explains the stock market's reaction to federal reserve policy? J Financ 60:1221–1257

Blanchard O (2009) Macroeconomics. 5th edition ed. Prentice Hall International, London

Borio C, Kennedy N, Prowse S (1994) Exploring aggregate asset price fluctuations across countries: measurement, determinants and monetary policy implications. BIS Economic Papers No. 40

Browne F, Cronin D (2007) Commodity prices, money and inflation. ECB Working Paper Series No. 738

Brüggemann R, Lütkepohl H (2006) A small monetary system for the euro area based on german data. J Appl Econ 21:683–702

Brunner K (1961) Some major problems in monetary theory. Am Econ Rev 51:47–56

Brunnermeier M, Nagel S (2004) Hedge funds and the technology bubble. J Financ 59:2013–2040

Brunnermeier MK, Pedersen LH (2007) Market liquidity and funding liquidity. NBER Working Paper Series No. 12939

Campbell JY, Lo AW, MacKinlay AC (1997) The econometrics of financial markets. Princeton University Press, Princeton

Cassola N, Morana C (2002) Monetary policy and the stock market in the euro area. ECB Working Paper Series No. 119

Chen NF, Roll R, Ross SA (1986) Economic forces and the stock market. J Bus 59:383–403

Cheung YW, Ng LK (1998) International evidence on the stock market and aggregate economic activity. J Empir Financ 5:281–296

Christensen AM, Nielsen HB (2003) Has US monetary policy followed the Taylor rule?A cointegration analysis 1988–2002. Working Paper. http://www.edgepagenet/jamb2003/Jamboree-Copenhagen-Nielsen.pdf . Accessed 30 July 2013

Dennis JG, Hansen H, Johansen S, Juselius K (2005) CATS in RATS: Manual to cointegration analysis of time series. Evanston, Illinois. Estima

Dhakal D, Kandil M, Sharma SC (1993) Causality between the money supply and share prices: a VAR investigation. Q J Bus Econ 32:52–74

Doornik JA (2007) PcGive. volume version 12. Oxmetrics. http://www.doornik.com/

Döpke J, Hartmann D, Pierdzioch C (2006a) Forecasting stock market volatility with macroe-conomic variables in real time. Deutsche Bundesbank - Discussion Paper Series 2: Banking and Financial Studies No. 01/2006

Döpke J, Hartmann D, Pierdzioch C (2006b) Real-time macroeconomic data and ex ante pre-dictability of stock returns. Deutsche Bundesbank - Discussion Paper Series 1: Economic Studies No. 10/2006

Durham JB (2003) Does monetary policy affect stock prices and treasury yields? An error correction and simultaneous equation approach. Finance and Economics Discussion Series No. 10/2003

ECB (1999) Euro area monetary aggregates and their role in the eurosystem's monetary policy strategy. ECB Monthly Bulletin (February 1999): 29–45

ECB (2003) Monetary presentation of the euro area balance of payments. ECB Monthly Bulletin June 2003, Box 1, 15–16

English JR (2001) Applied equity analysis: stock valuation techniques for wall street professionals. McGraw-Hill Companies, Inc, New York

Friedman M (1988) Money and the stock market. J Polit Econ 96:221–245

Ganjarerndee S (2001) Thailand. In: Kim YH (ed) Government bond market development in Asia. Asian Development Bank, Mandaluyong, pp 642–684

Giese JV, Tuxen CK (2007) Global liquidity and asset prices in a cointegrated VAR. Preliminary Draft URL: http://www.edge-page.net/jamb2007/papers/GieseandTuxen06-07-2007.pdf. Accessed 30 July 2013

Gouteron S, Szpiro D (2005) Excès de liquidité monétaire et prix des actifs. Banque de France Working Paper No. 131, Septembre 2005

Greiber C, Setzer R (2007) Money and housing - evidence for the euro area and the US. Deutsche Bundesbank Discussion Paper, Series 1: Economic Studies No. 12/2007

Hamburger MJ, Kochin LA (1972) Money and stock prices: the channels of influence. J Financ 27:231–249

Hashemzadeh N, Taylor P (1988) Stock prices, money supply, and interest rates: the question of causality. Appl Econ 20:1603–1611

Helbling T, Terrones M (2003) Real and financial effects of bursting asset price bubbles. IMF World Economic Outlook, April 2003, pp 61–94

Hoover KD, Johansen S, Juselius K (2008) Allowing the data to speak freely: the macroeconomet-rics of the cointegrated vector autoregression. Am Econ Rev: Pap Proc 98:251–255

Humpe A, Macmillan P (2009) Can macroeconomic variables explain long-term stock market movements? A comparison of the US and Japan. Appl Financ Econ 19:111–119

IMF (1999) Global liquidity. World Econ Outlook - Box 4(4):118–121

IMF (2008) Selected issues in balance of payments and international investment position analysis - alternative presentations of balance of payments data. Balance of Payments and International Investment Position Manual, Sixth Edition (BPM6) - December 2008, Pre-Publication Draft, pp 333–337

Inoguchi M (2007) Influence of ADB bond issues and US bonds on Asian government bonds. Asian Economic Journal 21:387–404

Ito T (2003) Looking forward on monetary and supervision policies to protect against bubbles. In: Hunter WC, Kaufman GG, Pomerleando M (eds) Asset Price Bubbles: The Implications for Monetary, Regulatory, and International Policies. Cambridge, pp 547–552

Johansen S (1995) Likelihood-based inference in cointegrated vector autoregressive models. Oxford University Press, Oxford

Johansen S (2007) Correlation, regression, and cointegration of nonstationary economic time series. Discussion Papers Department of Economics University of Copenhagen No. 07–25, November 2007

Johansen S, Juselius K (1992) Testing structural hypotheses in a multivariate cointegration analysis of the ppp and the uip for uk. J Econ 53:211–256

Johansen S, Juselius K (2001) Controlling inflation in a cointegrated vector autoregressive model with an application to US data. Working Paper ECO No. 2001/02, January 2001

Juselius K (2001) European integration and monetary transmission mechanisms: the case of italy. J Appl Econ 16:341–358

Juselius K (2006) The Cointegrated VAR model: methodology and applications, 2nd edn. Oxford University Press, Oxford

Juselius K, MacDonald R (2004) International parity relationships between Germany and the United States: A joint modelling approach. FRU Working Papers 2004/08, University of Copenhagen, Department of Economics, Finance Research Unit

Juselius K, Toro J (2005) Monetary transmission mechanisms in Spain: the effect of monetization, financial deregulation, and the EMS. J Int Money Financ 24:509–531

Keynes JM (1936) The general theory of employment, interest and money. Macmillan Cambridge University Press, London

King M (2003) No money, no inflation - the role of money in the economy. In: Mizen P (ed) Central banking, monetary theory and practice: essays in honour of Charles Goodhart - volume one, vol 1. Edward Elgar Publishing Limited, Cheltenham, pp 62–89

Kohn DL (2008) Monetary policy and asset prices revisited. In: Speech at the Cato Institute’s 26th Annual Monetary Policy Conference, Washington, D.C., November 19

Kuttner KN (2001) Monetary policy surprises and interest rates: evidence from the fed funds futures market. J Monet Econ 47:523–544

Kuttner KN, Mosser PC (2002) The monetary transmission mechanism: some answers and further questions. FRBNY Econ Policy Rev May 2002:15–26

Kwon CS, Shin TS (1999) Cointegration and causality between macroeconomic variables and stock market returns. Global Financ J 10:71–81

Lane PR, Milesi-Ferretti GM (2006) The external wealth of nations mark II: Revised and extended estimates of foreign assets and liabilities, 1970–2004. IMF Working Paper 06/69, March 2006

Lastrapes WD (1998) International evidence on equity prices, interest rates and money. J Int Money Financ 17:377–406

Lee BS (1992) Causal relations among stock returns, interest rates, real activity, and inflation. J Financ 47:1591–1603

Marshall DA (1992) Inflation and asset returns in a monetary economy. J Financ 47:1315–1342

Mauro P (2000) Stock returns and output growth in emerging and advanced economies. IMF Working Paper 00/89, May 2000

Maysami RC, Koh TS (2000) A vector error correction model of the Singapore stock market. Int Rev Econ Financ 9:79–96

Meltzer AH (1995) Monetary, credit and (other) transmission processes: a monetarist perspective. J Econ Perspect 9:49–72

Mishkin FS (1995) Symposium on the monetary transmission mechanism. J Econ Perspect 9:3–10

Mishkin FS (2001) The transmission mechanism and the role of asset prices in monetary policy. NBER Working Paper Series No. 8617, National Bureau of Economic Research, Inc, December 2001

Monetary and Financial Statistics Division (2006) Monetary and Financial Statistics. Handbooks,Centre for Central Banking Studies, Bank of England, number 25

Muscatelli VA, Spinelli F (2000) The long-run stability of the demand for money: Italy 1861-1996. J Monet Econ 45:717–739

Okun, A.M., 1971. The mirage of steady inflation. Brook Pap on Econ Act No 2:1971, pp. 485–498

Pepper G (1994) Money, credit and asset prices. St. Martin's Press, New York

Rajan RG (2005) Has financial development made the world riskier? NBER Working Paper Series No. 11728, November 2005

Ratanapakorn O, Sharma SC (2007) Dynamic analysis between the US stock returns and the macroeconomic variables. Appl Financ Econ 17:369–377

Reinhart CM, Rogoff KS (2009) The aftermath of financial crises. NBER Working Paper Series No. 14656

Rogoff K (2006) Impact of globalization on monetary policy. Paper prepared for the Symposium sponsored by the Federal Reserve Bank of Kansas City on "The New Economic Geography: Effects and Policy Implications," Jackson Hole, Wyoming, August 24–26, 2006

Sellin P (2001) Monetary policy and the stock market: theory and empirical evidence. J Econ Surv 15:491–541

Sims CA, Stock JH, Watson MW (1990) Inference in linear time series models with some unit roots. Econometrica 58:113–144

Sprinkel, B.W., 1964. Money and Stock Prices. Richard D. Irwin, Inc., New York

Standard & Poor’s (2009) Australia all ordinaries index by sector

Taylor JB (1981) On the relation between the variability of inflation and the average inflation rate. Elsevier - Carn-Roch Conf Ser Public Policy 15:57–85

Tobin J (1991) Money still counts. Wall Street J 73:A14

Trichet JC (2005) Asset price bubbles and monetary policy, Speech by Jean-Claude Trichet, Maslecture, The Monetary Authority of Singapore, 8 June 2005, Singapore. https://www.asx.com.au/products/capitalisation-indices.htm

Warnock FE, CacdacWarnock V (2006) International capital flows and U.S. interest rates. NBER Working Paper Series No. 12560, October 2006

Wong WK, Khan H, Du J (2006) Do money and interest rates matter for stock prices? An econometric study of singapore and USA. Singap Econ Rev 51:31–51

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Belke, A., Wiedmann, M. Dissecting long-run and short-run causalities between monetary policy and stock prices. Int Econ Econ Policy 15, 761–786 (2018). https://doi.org/10.1007/s10368-018-0413-y

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10368-018-0413-y