Abstract

In this paper, we propose a partial internal model to determine the solvency capital requirement (SCR) for static and dynamic hybrid products. We present qualitative and quantitative results from several simulation studies for new business portfolios as well as for existing portfolios based on actual and fictitious historical financial market data. Our findings show that hybrid products are mainly exposed to interest rate, equity and lapse risks. Furthermore, we show that the SCR for dynamic hybrid products strongly depends on past financial market fluctuations.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Innovative life insurance products have been gaining in popularity during the last decade and now represent a majority of new business in Germany. Footnote 1 Among innovative life insurance products, static and dynamic hybrid products attract much attention, as they have the potential of higher returns than traditional insurance products while offering a high degree of security to the policyholders. However, and despite the importance of these products to the future of the life insurance industry, most discussions about the Solvency II framework focus on traditional insurance products. The results of the last quantitative impact studies QIS4 and QIS5 indicate that insurance companies do not calculate the solvency capital requirement (SCR) for innovative life insurance products as systematically as for traditional products. Footnote 2 Furthermore, the current standard formula for SCR calculations for traditional German insurance products Footnote 3 appears to be inaccurate for hybrid products because of its entirely deterministic approach. Alternatively, insurers may use internal models for SCR calculations for these products such as the model presented by Bauer et al. [1] and [2]. The downside of internal models is their considerable need for computational resources as a consequence of their complexity (i.e. due to nested simulations). In our paper, we present a partial internal model for the calculation of the SCR for hybrid products. The model is constructed such that it allows for both, using the basic principles of the standard formula as well as incorporating stochastic calculations. The model is based on the standard formula as outlined in the Solvency II directive [30], the technical specifications of the latest Quantitative Impact Study (QIS5, CEIOPS [5]) and the consultation papers (CEIOPS [3]).

Hybrid products have not been of academic interest so far. Literature is restricted to product descriptions as done by Zwiesler [31], Deichl [14], Fix and Käfer (15) or Hammers [18]. The valuation of the rebalancing options of dynamic hybrid products has been discussed by Menzel [23], Siebert [28] and Reuß and Ruß [25]. An analysis of the risks of static and dynamic hybrid insurance products and the development of a framework that enables insurers to assess the SCR for these products is still due.

This paper is organized as follows. In Sect. 2 we present two relevant product types: static hybrids and 3-pot dynamic hybrids with single premiums. The partial internal model is described in Sect. 3 and is based on the model in Kochanski [20, 21], where it was used in the context of simple German unit-linked insurance with guaranteed death benefits. In Sect. 4 we present and interpret qualitative and quantitative results from several simulation studies. Section 5 concludes.

2 Hybrid products

Traditional German life insurance products Footnote 4 include an annual interest rate guarantee. Other features are a strict regulation of the asset investments of the insurer and guaranteed surrender values. Furthermore, German policyholders are very familiar with these traditional products. Therefore, a high degree of security and acceptance is associated with these products. Unfortunately, this comes at the cost of high charges and low investment returns during phases of booming markets. Especially, the rallies of stock markets during the last two decades enhanced the demand for unit-linked insurance products with little guarantees. The major disadvantage of pure unit-linked insurance products were exposed in the course of financial crises. Policyholders experienced high losses and therefore lost confidence in these products. Hybrid products were designed to combine the best of both: strong guarantees and high returns. In the following, we describe the typical properties of a hybrid insurance policy.

Accumulation period The insurer collects a single premium P at time t = 0 and invests the premium according to the investing strategy of the corresponding product type for T years Footnote 5. This period is called the accumulation period. Depending on the product type, the insurer will invest in the premium reserve stock (PRS t ), an equity fund (EF t ) or a guarantee fund (GF t ). The account value of the policy at time t is defined as AV t = PRS t + EF t + GF t . During the accumulation period the insurer also agrees to pay a death benefit (DB t ) in case of death and a surrender benefit (SB t ) in case of surrender. The death benefit at time t has a guaranteed minimum: \(\hbox{DB}_t = \max{\left(\hbox{P}; \hbox{AV}_t \right)}.\) The surrender benefit equals the account value net of the surrender fee (C s):SB t = AV t − C s t with \(C^s_t=\alpha_s \cdot \left(\hbox{P}-t \cdot \frac{\hbox{P}}{12 \cdot T}\right).\) In order to cover administrative expenses, the insurer deducts acquisition charges \((C^a_0=\hbox{P}\cdot \alpha_a)\) and fixed unit charges (\(C^u_0=\hbox{P} \cdot \frac{\alpha_u}{2}\) at t = 0 and \(C^u_t=\frac{\hbox{P}}{12\cdot T} \cdot \frac{\alpha_u}{2}\) every other month).Footnote 6

Pension period At the end of the accumulation period, the policyholder can choose between a lump sum payment, which equals the current account value but is at least the initial single premium, and an annuity. For simplification, we assume that all policyholders choose the lump sum payment.

Profit participation The insurer uses prudent assumptions for mortality and expenses and the actuarial interest rate for the calculation of the premiums. Since the best estimates for mortality and expenses are assumed to be less adverse and the earned interest on the PRS is assumed to be higher than the actuarial interest rate, the insurer is likely to generate profits. In Germany, the policyholder participates in three profit categories. The participation rate on profits generated by the interest on the PRS is denoted by π i , the participation rate generated from mortality assumptions is denoted by π m and π o denotes the participation rate on profits generated from expenses and other sources. The insurer is not allowed to pass losses in a profit category to the policyholder or charge them against profits in other profit categories. During the accumulation period, surpluses are reinvested into the account. See Table 3 (Appendix A) for all product parameter values. In the following, we describe the different investing strategies of the two hybrid products.

Static hybrid products Static hybrid products were the first hybrid products introduced in Germany.Footnote 7 The insurer divides the insurance benefits into a guaranteed and a non-guaranteed part. We assume a guaranteed account value of the initial single premium at time T and guaranteed death benefits of the initial single premium during the accumulation period. The insurer invests just enough of the account deposits in the PRS to meet the guarantees at any point of time . The rest of the account deposit is invested into an equity fund. The investments are made at the beginning of the accumulation period and there is no rebalancing. Therefore, in the worst case (Fig. 1), the policyholder will retrieve at least the initial single premium at time T. Let G t denote the account value that is needed to meet the guaranteed insurance benefits at time t and i denote the actuarial interest rate, then the investment strategy of a static hybrid insurance product can be expressed as follows:

Static hybrid product—worst case scenario

Dynamic hybrid products The downside of static hybrid products is that the portion of the account deposit invested in the PRS is very high. The worst case scenario suggests that the equity fund could lose all its value at any time and also in any time span. It is clear that the worst case assumptions that underlie the investment strategy of static hybrids are far too strict. Not surprisingly, the extension of the concept of hybrid productsFootnote 8 is based on a more realistic approach concerning the worst case scenario. It is reasonable to define a maximum loss of the equity fund for a short and foreseeable time span. We use a month as the time span and denote the assumed maximum loss of the equity fund during a month as λ. Now, the insurer is able to invest a much higher portion of the account deposits into the equity fund. The insurer invests just enough in the PRS that all guarantees can be fulfilled after a maximum loss of the equity fund. In this unlikely case (Fig. 2), the insurer would sell all shares of the equity fund immediately and fully invest in the PRS. Although the maximum loss is usually highFootnote 9 there is still some risk that the equity fund might lose even more value than assumed. In order to eliminate that risk, the insurer invests in a guarantee fund, equivalent to the equity fund with a hedge, that actually can lose λ at most during a month. The other implication of this strategy is that the insurer is forced to review the asset allocation regarding whether the guarantees are still met or not, and rebalance if needed. In situations where the account deposit is entirely invested in the guarantee fund and where it exceeds the needed account value even after a maximum loss, there is some portion of the account deposit that is hedged unnecessarily. In this case, the investment strategy of a 3-pot dynamic hybrid insurance allows for additional investments in an equity fund:

3-pot dynamic hybrid product—worst case scenario

3 Partial internal model

The main objective of insurance supervision and regulation is to provide adequate policyholder protection. For that purpose, qualitative and quantitative requirements, such as the solvency capital, transparency and accountability, are addressed in the Solvency II framework by a three pillar approach. Pillar I focuses on the calculation of the SCR. The Solvency II framework allows insurers to choose among three methods in order to determine the SCR: the standard formula, an internal model or a partial internal modelFootnote 10. National organizations, such as the GDV, developed own and more detailed interpretations of the standard formula (GDV [16]). Insurers that use the GDV standard formula are not required to perform stochastic calculations but the model is restricted to certain product types and does not include hybrid products. On the other hand, a full internal model requires the modeling of the insurance company as a whole. This task requires the determination of all correlations and of stochastic models for all risk factors. It is doubtful that small and mid-sized insurers are able to implement such models, therefore, we believe that a partial internal model is most suitable for small and mid-sized insurers that want to assess the SCR for hybrid products.

Set-up of the model In the standard formula risks are categorized in modules such as the market module or the life underwriting module, and decomposed in submodules such as equity risk or mortality risk.Footnote 11 The submodules contain stress scenarios that are calibrated to a significance level of 99.5%. Since the stress scenarios and the correlation matrices of the modules are provided with the standard formula, the insurer is left with the task of calculating the SCR on the submodule level. In some cases, e.g. in case of the operational risk, the SCR is calculated using a factor formula. For most submodules, the standard formula applies the \(\Updelta\)-NAV (net asset value) approach that defines the SCR as the difference of the NAV of the best estimate economic balance sheet and the NAV of a stressed economic balance sheet. The economic balance sheets contain the market values of the assets and the liabilities of the insurance undertaking. The GDV standard formula [16] is based on a deterministic cashflow model and uses closed form approximation formulas that are calibrated on traditional German insurance products for the valuation of the economic balance sheet items. As opposed to the GDV standard formula, our partial internal model uses stochastic simulations for the valuation of the economic balance sheet items.

For the deterministic parts of the partial internal model such as mortality, expenses or lapses, we use a set of best estimate parameters (see Sect. 4). The stochastic financial market model consists of stochastic models for the risky assets and interest rates. We also need management rules that determine managerial actions which are sensitive to different scenarios and the product model as described in Sect. 2. The product model contains all relevant parameters of the insurance policies and all relevant information about the insurers portfolio. With most of the cash flows being stochastic now, Monte Carlo simulations are used to obtain a best estimate economic balance sheet and to determine the value of the insurance portfolio, more precisely the present value of future profits (denoted by PVFP), which, in our model, is equivalent to the NAV. In order to obtain the SCR, we use the stress scenarios as defined in the standard formula. They affect either the best estimate assumptions or the parameters of the stochastic financial market model. Again, we perform Monte Carlo simulations in order to obtain stressed economic balance sheets and to determine the value of the insurance portfolio, now under the assumption that a stress occurs. Applying this procedure to every stress scenario of every relevant risk module and using the \(\Updelta\)-NAV approach, the outcomes can be aggregated to the resulting SCR the same way as in the standard formula (see Fig. 3).

Partial internal model

Management rules The partial internal model includes management rules for the asset management and profit sharing. The management controls the rebalancing of the account assets as specified in Sect. 2. The management also controls the asset composition of the PRS, more precisely, the equity exposure level and the bond investment strategies. The limit of the equity exposure level e m is set to 35% by the German regulator but most insurers calculate with significantly lower limits. We define e a as the targeted equity exposure level, the minimum level is naturally at 0%. Now let S t denote the equity price at time t, then the equity exposure level E t is described by E 0 = e a and

for t > 0. The bond investment strategy addresses the managerial actions in case the insurer needs to buy bonds or sell them. We assume that the insurer will buy zero coupon bonds with a maturity of 5 years and sell bonds of all maturities according to their proportion of the portfolio. We already outlined the profit participation system in Sect. 2 but it is worth noticing that the profit participation rule for the investment profits leaves all losses to the insurer and most of the profits to the policyholder. Therefore, insurers aim to smooth those profits. We implemented two mechanisms that have a smoothing effect on profits. Firstly, profits are aggregated throughout the year and paid out at the end of the year. The aggregation allows to offset possible losses in 1 month by profits in another. Secondly, investment profits and losses are generated through changes of the book value of the PRS which is less volatile than the market value. Doing so, the calculation of investment profits also takes into account that hidden reserves are amortized while selling assets of the PRS. Furthermore, a friction of hidden reserves of the equity of the PRS is amortized monthly. This is done by simply selling and rebuying 2% of the equity every month and does only affect the book value of the equity. A comparable approach to model the calculation of investment profits has been carried out by Graf et al. [17].

Financial market The stochastic financial market model contains stochastic models for the short rate and for the stock market. From these models, we can derive forward rates, bond prices, stock prices and the values of the equity and guarantee fund. The Cox–Ingersoll–Ross model is used to model the short rate (see [19, 27]). Let θ denote the constant long run short rate, κ the constant mean reversion speed, σ r the volatility of the short rates and W r t a standard Brownian motion, then the stochastic differential equation that describes the short rate r t is given by

The discount rate D t is then defined as

The Cox–Ingersoll–Ross model also provides an analytical formula for the bond price of a zero coupon bond at time t and maturity T:

The implementation of the model is achieved using a discretization schemeFootnote 12. Let S t denote the value of one share of the risky asset. We assume that S t evolves according to a geometric Brownian motion. Then, the dynamics of S t under the risk-neutral measure are described by the following stochastic differential equation:

We assume constant volatility σ and a Brownian motion W t that is uncorrelated to W r t . The equity fund is holding shares of the risky asset and charging a constant annual rate of management fees denoted by ν. Let \(S^{\hbox{EF}}_t\) denote the value of one share of the equity fund, then

describes the equity fund dynamics. The equity fund is modeled as a continuous dividend paying share.Footnote 13 The analytical solution of the stochastic differential equation can be written as

The guarantee fund is modeled similarly to the equity fund with the difference that the fund management also hedges the guarantee of a maximum loss of λ% per month by investing in put options.Footnote 14 The fund management adds the hedging costs to the constant rate of management fees ν. In order to determine the price of the put option, we use the extended Black-Scholes formula for option pricing (see [19]). For simplicity, we assume a constant short rate of 0%, where the put option price \(P_t^{\hbox{CP}}\left(K,t+\frac{1}{12}\right)\) with the strike price K = x S t , with \(x \in \left(0,1\right]\) and maturity \(t+\frac{1}{12},\) has a maximum. Additionally we assume a volatility σCP that is higher than the volatility σ of the actual model. These assumptions lead to a price of the put option that only depends on the current price of the equity share and can be interpreted as a prudent estimate:

Now, the price of a share of the guarantee fund can be expressed as follows:

Kickbacks are paid by the equity fund and guarantee fund management to the insurer and are financed by the management fees.Footnote 15 The amount of monthly kickback payments is denoted by

In our model the insurer is assumed to use a constant actuarial interest rate i, which is also the guaranteed interest on the PRS. The parameter settings can be obtained from Table 6 (Appendix B).

Economic balance sheet In order to calculate the SCR, we need to calculate a stochastic economic balance sheet (see Fig. 4) for the best estimate and every stress scenario. While the values of the assets are determined by their current market values (mark to market), the value of the liabilities result from stochastic simulations under the risk-neutral measure (mark to model). The PVFP, the insurance benefits and the management fees equal the average of the corresponding sum of the discounted cash flows. The PVFP includes all positive and negative cash flows to the insurer. The insurance benefits include death benefits, annuity benefits, surrender benefits (net of lapse fees), and lump-sum payments. The balance sheet item “management fees” (MF) includes all fees that are deducted by the equity and the guarantee fund management net of kickbacks. The balance sheet item “insurance benefits” can be broken down into benefits that result from profit participation (FDBFootnote 16) and the value of options and guarantees (O&G) and other insurance benefits (OIB). The value of the O&G is defined as

where PVFPCE denotes the PVFP under the certainty equivalent scenario.Footnote 17 Note, that we use a MCEV type approach to determine the value of O&GFootnote 18 which differs from the approximation formulas as defined in the GDV standard formula.

Economic balance sheet

Partial internal models require an interpretation of the standard formula stress scenarios. Since our model is based on a stochastic financial market model, we define the equity stress, the interest rate stress, the illiquidity premium stress and the default stress scenario as follows: The equity stress is performed immediately and as a whole at the level of the standard formula in the first month. The interest rate stresses and the illiquidity premium stress affect the parameters of the interest rate model and the resulting bond prices.Footnote 19 In case of a default of the management of the guarantee fund, the insurer is obligated to close the gap. In this case, we did not adjust the future profit participation for simplicity. In order to assure the validity of our model, we tested our stochastic financial market model with the martingale test and our economic balance sheets with the leakage test.

In spite of the elaborate design, the partial internal model has some shortcomings. The complex of nature of the German PRS and the associated management rules increases the model uncertainty. Since the results based on the partial internal model strongly depend on the underlying assumptions regarding the PRS, another set of assumptions can have a significant impact. Therefore, in the process of implementing a (partial) internal model it is a major task to identify and recognize managerial actions. Furthermore, our partial internal model does not sufficiently address the risk of illiquid assets. The concept of dynamic hybrid products is based on a rebalancing algorithm, that stipulates major asset sales during or directly after a market distress. The correspondent market risk stress scenarios might underestimate the actual risks, given a sufficiently large market share of those products.

4 Numerical results

In this section, we present and analyze results from several simulation studies. First, we specify the analysis assumptions in Sect. 4.1. In Sect. 4.2, we examine the SCR for the year 2010 of a portfolio of new business started in 2010 in order to acquire unbiased information about the risk structure of hybrid insurance products. In Sect. 4.3 we analyze the SCR for the year 2010 of fictitious sample portfolios that are in force for 2 and 7 years (started in 2008 and 2003) with real historical data. This analysis allows us to compare both products with respect to extreme market conditions. Finally, in Sect. 4.4 we perform a sensitivity analysis for a fictitious set of historical financial market data as well as for crucial model parameters. Throughout our analyses, we focus on the key indicators PVFP, SCR and SCR ratioFootnote 20 and on the economic balance sheet items FDB and O&G. More data is available upon request.

4.1 Historical data and parameter assumptions

Unless otherwise noted, we assume homogeneous portfolios of 5,000 policies and all policyholders to be male and 30 years old at the beginning of the policy. German mortality tables DAV [12] determine prudent and best estimate mortality during the accumulation period . Deaths are assumed to be uniformly distributed over the year. Lapses are assumed to be only dependent on the policy year, the corresponding annual lapse rates can be found in Table 5 (Appendix A). The fixed unit expenses \(C^{e}_{t}\) are assumed to increase at an annual cost inflation rate τ (\(C^e_0=\hbox{P} \cdot \frac{\alpha_e}{2}\) at t = 0 and \(C^e_t=\frac{\hbox {P}}{12\cdot T} \cdot \frac{\alpha_e}{2} \cdot \left(1 + \tau \right)^{\frac{t}{12}}\) every other month). Parameter assumptions can be found in Table 4 in Appendix A. We use historical financial market data to generate existing portfolios. For this purpose, we obtained a series of short term interest rates from the Bundesbank-DatabaseFootnote 21 and Bloomberg data for 5-year German interest ratesFootnote 22 as well as the DAX index. Since the DAX index represents the historical development of the risky asset, we obtain historical data of the equity fund and the guarantee fund by applying the stochastic financial market model as outlined in Sect. 3. Figure 5 shows the historical financial market data. The results in Sects. 4.2 and 4.3 are based on 100,000 Monte Carlo simulation paths. The number of Monte Carlo simulation paths in 4.4 is reduced to 1,000 due to the extensive computational requirements of the sensitivity analysis.

Historical financial market data

4.2 Numerical results for new business

The results of the simulation study of a portfolio of new business are presented in columns “SP 0” of Table 1. A modular representation of the composition of the respective SCR is shownFootnote 23 in Fig. 6. The accumulation period of 35 years implicates a rich compound interest rate effect, therefore both products can invest strongly in risky assets. Almost half of the account of the static hybrid is invested in the equity fund, the other half is invested in the PRS. The 3-pot dynamic hybrid account deposit is divided in two thirds of the guarantee fund and one third of the equity fund.

SCR—static and 3-pot dynamic hybrid (new business portfolio)

The annual guaranteed interest rate and the profit participation system (investment profits) of the PRS have huge impact on the O&G and the FDB of the static hybrid, while the dynamic hybrid includes enormous management fee payments. Overall, the PVFP of the dynamic hybrid product significantly exceeds the PVFP of the static hybrid. Both products are primarily exposed to market risks. Again, the annual guaranteed interest rate of the PRS has a heavy impact as it increases the market risk of static hybrid products. The relevant interest rate stress scenario is the down-scenario throughout all simulation studies in this paper. The only relevant underwriting risk is the massive lapse scenario. The portfolio of static hybrid products requires about 30% more SCR than the dynamic hybrid product portfolio, while having about 20% less PVFP and therefore a much lower SCR ratio of 1.14 compared to 2.07. In some market stress scenarios, the stressed value of the FDB for dynamic hybrid products exceeds the best estimate FDB. This effect is due to a high investment in the PRS during a market stress and the implied profit participation on investment returns. Unfortunately, this leads to a gross SCR lower than the net SCR. We prohibited this by setting the net SCR as a lower bound of the gross SCR. In the mortality and lapse submodules the gross SCR significantly differs from the net SCR. Both scenarios imply a massive reduction of business in force and therefore also a reduction of the FDB. This is mainly not an effect of the loss absorbing capacity of technical provisions. In our model, the SCR calculations of the operational risk module use expenses that have been experienced in the past as a reference. Therefore, in our model the operational risk is not present for new business.

4.3 Numerical results for sample portfolios

At first, we begin with a fictitious portfolio that is in force for 7 years with underlying historical data from 2003 to 2010 (Fig. 5). That period is characterized by relatively low interest rates, a stock market rally followed by a financial crisis with a beginning recovery. However, stock markets never fall below the starting value. Figure 7 shows the impact of the last financial crisis as the account value drops by a half for dynamic hybrid products. The account value of the static hybrid is affected less severely. Figure 7 also shows that no rebalancing is needed during this period.

Account composition—historical data (from 2003 to 2010)

The results of the simulation study are presented in columns “SP 7” of Table 1 while the modular representation of the composition of the respective SCR is shown in Fig. 8. The structure of the composition of the account assets remains similar to the new business portfolios, the portion of risky assets increased through all products. The dynamic hybrid outperformed the static hybrid comparing the account value. The PVFP, most of the liabilities and the SCR are similar compared to the new business portfolios.

SCR—static and 3-pot dynamic hybrid (7 years in force)

The value of the O&G decreased significantly for both products, the value of the management fees increased. While the structure of the SCR remained almost unchanged for the static hybrid, it changed for the dynamic hybrid. Market risks are less dominant since the probability of an investment in the PRS is lower while the SCR for lapse risk increased. The massive lapse of policyholders implies a loss of future profits that result from kickbacks. Overall, the SCR ratio of the static hybrid increased to 1.28 while the SCR ratio of the dynamic hybrid product increased to 2.25. Note that we used the assumption that all profits earned by the insurer are distributed to the shareholders immediately.

The second sample portfolio analysis is performed on market data from the last financial crisis (2008–2010). This period is characterized by a massive fall of stock markets followed by a beginning recovery. Interest rates are almost as low as the guaranteed annual interest rate of 2.25%. Figure 9 shows that both products deal with extreme decline of the account values. Here, the dynamic hybrid product takes the biggest toll since the account is composed only of risky assets at the beginning of the crisis. The dynamic hybrid has to be rebalanced shifting most of the account deposit to the PRS. Again, results can be obtained from Table 1, columns “SP 2”. The PVFP of the static hybrid drops by 24% compared to the new business portfolio and the O&G as well as insurance benefits and management fees decrease significantly. The decline of the account value implies a decline of policyholders benefits. The changes of the results of the static hybrid product are mostly due to the losses in the equity fund value. The results of the 3-pot dynamic hybrid product show an extreme drop of the PVFP by 59%. Because of the shift to the PRS the O&G increased by 277%. Insurance benefits decline similar to the static hybrid. The SCR of both products is almost equal now as a result of a strong increase of the dynamic hybrid SCR (23%). Both products have very low SCR ratios of about 0.95 and 0.70. Figure 10 shows that the composition of the SCR is similar in both products, with only the market risks (especially the interest rate risk) being relevant.

Account composition—historical data (from 2008 to 2010)

SCR—static and 3-pot dynamic hybrid (2 years in force)

4.4 Sensitivity analysis

The analyses in Sect. 4.3 indicate that the SCR of both, static and dynamic hybrid products, depends strongly on the development of the account values. In case of dynamic hybrid products, the SCR is also very sensitive to past rebalancing actions. These dependencies can be revealed by means of a sensitivity analysis. For this purpose, we determined the SCR of 7 and 2 years sample portfolios subject to different fictitious historical market data. The parameters used are specified in Table 2. All historic interest rates and the historic stock index rate of return are assumed to be constant. The historical monthly interest rate is set to half of the 5-year interest rate. The interest rates for all other maturities are obtained performing a linear interpolation between the 5-year interest rate and the monthly interest rate.

The results of the partial internal model depend on many parameters. Among these, the market volatility, the actuarial interest rate and the length of the accumulation period are found to have a significant influence on the SCR of a new business portfolio. In case of the volatility analysis, the volatility of both, the interest rates and the stock market, evolve simultaneously and proportionally. In case of the accumulation period analysis, we also adjust the age of the policyholders in order to let the accumulation period end at the age of 65.

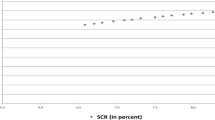

The results (SCR and SCR ratio) of the sensitivity analysis with respect to different market developments for 7 and 2 years in force static hybrid portfolios are illustrated in Figs. 11 and 12. These figures display that both, the SCR and the SCR ratio, are influenced by the equity return rates as well as by interest rates. Higher return rates lead to a higher SCR but also a higher SCR ratio since they have a stronger impact on the PVFP. High interest rates reduce the SCR and lead to higher SCR ratios. The buckle at the equity return rate of 0 and −1% is a consequence of the management rule for the equity exposure level of the PRS.

SCR and SCR ratio—static hybrid—sample portfolios (7 years in force)

The results (SCR and SCR ratio) of the outlined sensitivity analysis for dynamic hybrid portfolios are illustrated in Figs. 13 and 14. For most scenarios, decreasing equity return rates induce increasing SCRs and strongly decreasing SCR ratios while the interest rates have only negligible impact. Decreasing equity return rates come with an increasing probability of rebalancing into the PRS. This result demonstrates the pro-cyclical nature of dynamic hybrid products. For equity return rates less than −3% p.a. (for 7 years in force) and less than −15% p.a. (for 2 years in force), the portfolio starts to be rebalanced into the PRS. Since the rebalancing has a severe impact on the policy account’s assets, the nature of the SCR and SCR ratio of dynamic hybrids quickly resembles the one of static hybrids. Overall, the SCR of static hybrids exceeds the SCR of dynamic hybrids significantly in most of the analyzed scenarios while the SCR ratios are lower for most scenarios. The SCR ratio of static hybrid products exceeds the SCR ratios of dynamic hybrids only in extreme scenarios. Footnote 24 The results show that the SCR ratios of dynamic hybrid products are more volatile than those of static hybrids.

SCR and SCR ratio—static hybrid—sample portfolios (2 years in force)

SCR and SCR ratio—3-pot dynamic hybrid—sample portfolios (7 years in force)

SCR and SCR ratio—3-pot dynamic hybrid—sample portfolios (2 years in force)

Figures 15, 16 and 17 show the SCR and the SCR ratio for new business portfolios of static and dynamic hybrid products dependent on the volatilities of interest rates and equity, the guaranteed interest rate and the length of the accumulation period. Not surprisingly, high volatilities lead to a high SCR and a low SCR ratio. The difference of both products decreases with increasing volatilities. The new business portfolio of dynamic hybrid products induces a lower SCR and a higher SCR ratio than the static hybrid product portfolio in all cases.

SCR and SCR ratio—volatility analysis—new business portfolios

SCR and SCR ratio—actuarial interest rate analysis—new business portfolios

SCR and SCR ratio—accumulation period analysis—new business portfolios

The SCR of both products is also increasing with an increasing guaranteed interest rate, while the SCR ratios decrease. The difference between the static and the dynamic hybrid product decreases with a decreasing guaranteed interest rate. Again, the new business portfolio of dynamic hybrid products induces a lower SCR and a higher SCR ratio than the static hybrid product portfolio in most cases. For a guaranteed interest rate of 1% and below, the SCR and SCR ratio of a static hybrid portfolio is lower and higher respectively than the SCR and SCR ratio of a dynamic hybrid portfolio as a result of a low interest rate risk in these scenarios.

Finally, the accumulation period length has a major influence on the SCR and the SCR ratio of both products. The SCR of a static hybrid product portfolio is increasing with an increasing accumulation period length while the SCR of a dynamic hybrid product portfolio is decreasing. This results in a higher SCR for dynamic hybrids for an accumulation period of 21 years and less. The SCR ratios decrease both for an decreasing accumulation period length, while the difference between both ratios is decreasing, too. The SCR ratio of the dynamic hybrid product portfolio exceeds the SCR ratio of the static hybrid product portfolio for all analyzed scenarios.

5 Conclusions

In this paper, we present a partial internal model based on the Solvency II modular formula to assess the SCR for static and dynamic hybrid insurance products. The SCR is calculated using risk-neutral valuation methods similar to the MCEV approach. In the partial internal model, the economic balance sheets are derived using a stochastic financial market model. Therefore, we think that our model is superior to the GDV approach which is deterministic and not calibrated to innovative life insurance products.

The results of various simulation studies reveal that market and lapse risks dominate. Among market risks, the interest rate risk, more precisely, the downward shift of the interest rate term structure, is the most important risk. The only relevant underwriting risk is the lapse risk (a massive lapse scenario). This results are also in line with the general results from QIS4 and QIS5. Furthermore, the results reveal that the SCR ratio of dynamic hybrid products is highly volatile. The rebalancing of dynamic hybrid products has a pro-cyclical effect. After a stage of rising stock markets, the account of dynamic hybrid products is not investment in the PRS. The SCR, and in particular the interest rate risk, is low and the product has a more linear structure since the value of options and guarantees is also low. In this case, the SCR and its structure are comparable to pure unit-linked products. After a crisis on the stock markets, the accounts of dynamic hybrid products are rebalanced with high probability or already contain an investment in the PRS. The SCR, the interest rate risk and also the value of options and guarantees are very high. In contrast to dynamic hybrid products, static hybrid products are not rebalanced, the investment in the PRS does not change. Therefore the SCR of static hybrid products is almost always at a high level.

As a conclusion, we think that our model is of interest for small and midsized insurers that have not enough capacities to design a full internal model. The results are important for product designers as well as risk managers. Our analysis can be extended in various ways, for example to other premium paying types and a dynamic pension period. The model is also useful to test more sophisticated and risk reducing management rules as well as smoothing mechanisms for the asset management of the PRS. As the issue of dynamic policyholder behavior is of concern, our model is also useful to analyze the impact of various dynamic lapse models and models for the lump sum option. Furthermore, we modeled the PRS without the presence of a portfolio of traditional insurance products. Often, only one PRS is used for all products. Finally, our model and the results of the simulation studies can be used to derive approximation formulas in order to avoid stochastic simulation techniques.

Notes

The German Insurance Association (GDV [16]) version of the standard formula.

We refer to participating life insurance products such as the “Kapitallebensversicherung” or the “Kapitalrentenversicherung”.

With \(t = 0,\ldots,T\) years and a monthly discretization such that \(t \in \bigg\lbrace 0,\frac{1}{12},\ldots,\frac{12T}{12}\bigg\rbrace. \)

See Table 3 (Appendix A) for parameter values of α s , α a and α u .

Volksfürsorge introduced Best Invest in 1999 (see [26]).

HDI-Gerling introduced Two Trust in 2006 (see [24]).

A maximum loss of 20% is usually assumed.

See Fig. 18 (Appendix C).

We use the Euler–Maruyama scheme with absorption, see Korn et al. [22].

Paying negative dividends, see Shreve [27].

A similar approach to model a guarantee fund has also been used by the DAV-Arbeitsgruppe “Bewertung von Garantien” [13].

Therefore, the rate of kickbacks γ (p.a.) is chosen to be smaller than the rate of investment fund management fees ν.

See CFO Forum [7] for a detailed definition of the certainty equivalent scenario.

See Appendix B for details on the calibration of the CIR-model.

Defined as \(\hbox{SCR ratio} = \frac{\hbox{PVFP}^{{\rm BE}}}{\hbox{SCR}}.\)

See SU0101 (2010).

For the interest rates, we used the GDBR5 index (synthetic German zero-coupon bonds).

The boxes show (top–middle–bottom): (sub)module–gross SCR–net SCR.

7 years in force: scenarios with constantly negative equity return rates. 2 years in force: scenarios with interest rates lower or equal to 2.25% p.a. and equity return rates lower than −20% p.a.

References

Bauer D, Bergmann D, Reuß A (2009) Solvency II and nested simulations: a least-squares Monte Carlo approach. http://www.uni-ulm.de/fileadmin/website_uni_ulm/mawi/forschung/PreprintServer/2009/200905_Solvency_Preprint-Server.pdf (preprint)

Bauer D, Bergmann D, Reuß A (2010) On the calculation of the solvency capital requirement based on nested simulations. http://www.willisresearchnetwork.com/Lists/Publications/Attachments/75/2010BauerBergmannReuss.pdf (preprint)

CEIOPS (2004–2010) Consultation papers. https://eiopa.europa.eu/consultations/consultation-papers/index.html

CEIOPS (2008) QIS4 Report. https://eiopa.europa.eu/consultations/qis/quantitative-impact-study-4/index.html

CEIOPS (2010) QIS5 technical specification. https://eiopa.europa.eu/consultations/qis/quantitative-impact-study-5/index.html

CEIOPS (2011) QIS5 Report. https://eiopa.europa.eu/consultations/qis/quantitative-impact-study-5/index.html

CFO Forum (2009a) Market consistent embedded value basis for conclusions. http://www.cfoforum.eu/downloads/CFO_Forum_MCEV_Basis_for_Conclusions.pdf

CFO Forum (2009b) Market consistent embedded value principles. http://www.cfoforum.eu/downloads/MCEV_Principles_and_Guidance_October_2009.pdf

Daalmann S, Bause C (2011) FLV-Update 2010. Towers Watson. http://www.towerswatson.com/germany/press/4495

Daalmann S, Märten G (2009) Fondsgebundene Versicherungsprodukte mit Garantien trotzen der Finanzmarktkrise. Towers Perrin. http://www.towersperrin.com/tp/showdctmdoc.jsp?country=deu&url=Master_Brand_2/DEU/Press_Releases/2009/20090511/2009_05_11.htm

Daalmann S, Märten G (2010) FLV-Update 2009. Towers Watson. http://www.towerswatson.com/germany/press/1812

DAV (2008) Herleitung der Sterbetafel DAV 2008 T für Lebensversicherungen mit Todesfallcharakter. http://www.aktuar.de/download/dav/veroeffentlichungen/2008-12-04-DAV-2008-T.pdf

DAV-Arbeitsgruppe “Bewertung von Garantien” (2010) Bewertung von Fondsgebundenen Rentenversicherungen mit Garantiefonds und Variable Annuities

Deichl W (2008) Planbarkeit, Sicherheit und Rendite. VW 15:1265–1269

Fix W, Käfer I (2008) Dynamische Hybridprodukte—eine neue Produktfamilie mit viel Potential. VW 3:172–176

GDV (2010) Cashflow-Modell (QIS5_LV_Rst_Teil1-5) (unpublished)

Graf S, Kling A, Russ J (2011) Risk analysis and valuation of life insurance contracts: combining actuarial and financial approaches. Insur Math Econ 49(1):115–125

Hammers B (2009) Full Fair Value-Bilanzierung von Lebensversicherungsprodukten und mögliche Implikationen für die Produktgestaltung, vol 54. Versicherungswirtschaft

Hull JC (2008) Options, Futures, and Other Derivatives with Derivagem CD, 7th edn. Prentice Hall, Upper Saddle River

Kochanski M (2010a) Solvency capital requirement for German unit-linked insurance products. German Risk Insur Rev 6:33–70

Kochanski M (2010b) Solvenzkapital für FLV unter Berücksichtigung von dynamischem Storno. Zeitschrift für die gesamte Versicherungswissenschaft 99(5):689–710

Korn R, Korn E, Kroisandt G (2010) Monte Carlo methods and models in finance and insurance. CRC Press, Boca Raton

Menzel P (2008) Optionen in dynamischen Hybridprodukten. Der Aktuar 1:9–11

Ortmann M (2007) HDI-gerling two trust. Perfomance 6:28–34

Reuß A, Ruß J (2010) Vorteile innovativer Lebensversicherungsprodukte und ihre Risiken unter Solvency II. DAV-LEBENS-Gruppe, Herbsttagung, Köln. http://www.ifa-ulm.de/downloads/Innovative-Produkte-Solvency-II.pdf

Schmidt K (2010) Ruin am rollator. Das Investment 11:46–56

Shreve SE (2000) Stochastic calculus for finance 2. Springer, Berlin

Siebert A (2008) Aktuarielle Fragen zu dynamischen Hybridprodukten. Der Aktuar 2:79–81

SU0101 (2010) Zeitreihe SU0101: Geldmarktsätze am Frankfurter Bankplatz / Tagesgeld / Monatsdurchschnitt. http://www.bundesbank.de/statistik/statistik_zeitreihen.php?func=row&tr=SU0101&year=

The European Parliament (2009) Directive of the European Parliament and of the council on the pursuit of the business of insurance and reinsurance (Solvency II). http://register.consilium.europa.eu/pdf/en/09/st03/st03643-re06.en09.pdf

Zwiesler HJ (2007) Garantieprodukte. DAV-LEBENS-Gruppe, Herbsttagung, München. http://www.aktuar.de/download/dav/termine/HT07_LEBEN_Zwiesler.pdf

Author information

Authors and Affiliations

Corresponding author

Appendices

Appendix

A Parameter assumptions

Tables 3, 4 and 5 list the values of the parameters used in the model (provided by the Viadico AG).

B Stochastic financial market model parameter assumptions

Tables 6 and 7 list the values of the parameters used in the stochastic financial market model (provided by the Viadico AG). The interest rate term structure obtained from the CIR model should approximate the QIS5 Government interest rate term structures. Therefore, CIR-parameters have been set using the least squares optimization method.

C Modular structure and list of abbreviations

List of abbreviations | |

|---|---|

NAV | Net asset value |

MCEV | Market consistent embedded value |

PVFP | Present value of future profits |

FDB | (Value of) future discretionary benefits |

O&G | (Value of) options and guarantees |

OIB | Other Insurance Benefits |

MF | Management Fees |

PRS | Premium reserve stock |

EF | Equity fund |

GF | Guarantee fund |

BE | Best estimate |

CEIOPS | Committee of European Insurance and Occupational Pensions Supervisors |

EIOPA | European Insurance and Occupational Pensions Authority |

QIS | Quantitative Impact Study |

GDV | German Insurance Association |

(B)SCR | (Basic) Solvency capital requirement |

Adj | Adjustment for the risk absorbing effect of technical provisions and deferred taxes |

OP | SCR for operational risk |

SCRmkt | SCR for market risk |

SCRdef | SCR for default risk |

SCRlife | SCR for life underwriting risk |

SCRint | SCR for interest rate risk |

SCReq | SCR for equity risk |

SCRip | SCR for illiquidity premium risk |

SCRmort | SCR for mortality risk |

SCRlong | SCR for longevity risk |

SCRlapse | SCR for lapse risk |

SCRexp | SCR for expense risk |

SCRcat | SCR for catastrophe risk |

SCR—modular structure (obtained from CEIOPS [5])

Rights and permissions

About this article

Cite this article

Kochanski, M., Karnarski, B. Solvency capital requirement for hybrid products. Eur. Actuar. J. 1, 173–198 (2011). https://doi.org/10.1007/s13385-011-0040-2

Received:

Revised:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s13385-011-0040-2