Abstract

Relative to common equities and fixed-income securities, preferred securities have received scant attention from the academic and professional communities. Here, we utilize bivariate dynamic conditional correlation (DCC) and conventional mean-variance optimization models to construct asset portfolios of stocks, bonds, and REITs (real estate investment trusts), including publicly traded equity REIT securities (EREITs), mortgage REITs (MREITs), and REIT preferred stocks (PSREITs). Our analysis of weekly data from January 2000 through December 2019 reveals strong evidence that PSREIT securities have meaningful diversification benefits. During periods of economic expansion, the results indicate that increasing the portfolio inclusion of PSREIT securities, owing to their equity-like characteristics, increases the Sharpe reward-to-variability ratios of portfolios from 0.237 to 0.296. Time-varying correlations and optimal weights in our models exhibit dependence on the state of the economy. Highlighting the benefits of including PSREIT securities within a traditional mixed-asset portfolio, we also acknowledge liquidity constraints and other microstructure considerations that may limit market participation by individual investors and managers of small portfolios.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

The investment literature that is focused on common stocks and fixed-income securities is enormous. Its contents are broad, deep, and rich. Meanwhile, there has been scant academic examination of preferred stocks despite their dissociation from common stocks and their substantial value, reportedly exceeding $500 billion in value as of 2019. For example, in an analysis of mutual funds, Sharpe (1992) examines twelve asset classes, including U.S. Treasury securities, corporate bonds, large-cap common equities, small-cap common equities, and international securities, but preferred stocks are neither included nor mentioned. Even 20 years later, Damodaran (2012) devotes only three pages to preferred stocks in an encyclopedic 992-page book on investment valuation. Moreover, in a subsequent otherwise comprehensive analysis of income-producing portfolios, Blanchett and Ratner (2015) do not include any analysis of preferred stocks.

Treatment of preferred stocks in the literature commenced in the 1970s with the work of Bildersee (1973), who looks at stock returns and risk characteristics by producing estimates based on a standard one-factor model. That seminal work examines the behavior of 72 large-cap company preferred stocks from 1956 to 1966, showing that low-beta preferred stocks behave like bonds while high-beta preferred stocks behave like common stocks. In the 1980s, Emanuel (1983) presents the construction of a theoretical model of preferred stocks that is anchored on the assumption that preferred stock dividends are omitted if a firm's value falls below a critical level. Examining 554 liquid, non-convertible preferred stocks from 1972 through 1980, Stickel (1991) finds that the ex-dividend trading of preferred stocks yields abnormal returns with significant trading volumes. Based on data from 1933 to 1991, Chen (1996) documents a January effect for all grades of preferred stocks and a summer effect for low-grade preferred stocks. Likewise, tracking preferred stock returns from 1935 to 1987, Vetter and Wingender (1996) also find a January effect.

Little substantive research examining preferred stocks exists beyond the aforementioned somewhat-dated studies. Reasons for the lack of survey data and of investor sentiment questioning preferred stock attributes range from thin trading and illiquidity to subordinated bond rate interest-rate sensitivity and limited capital appreciation. Crabbe (1996), for example, asserts that preferred stocks trade more like a bonds than stocks because of their subordinated capital structure and credit risk spreads. However, preferred stocks carry a higher default risk than bonds, which raises doubts about their suitability within a balanced portfolio of stocks and investment-grade fixed-income securities. Li et al. (2010) extend Crabbe's assertions, stating that a preferred stock offers bond-like returns without the capital appreciation potential of a common stock. Swedroe (2016) points to several asymmetric risks of preferred stocks that investors overlook relative to fixed-income securities, suggesting that preferred stock investors incur a higher portfolio risk than they realize. Additionally, while 97% of all preferred security issuers, a majority of whom are banks, carry investment-grade bond ratings, about 30% of all preferred securities are rated Ba/B.B. or lower. These subdued views notwithstanding, emerging evidence indicates that preferred stocks, including those representing shares in Real Estate Investment Trust (REITs), may have portfolio enhancement attributes. Based on an analysis of data from 1992 through 2012, Boudry et al. (2020) show that investment in preferred stock REIT (PSREIT) securities can mitigate risk for highly risk-averse investors who are facing short-sale constraints and cannot borrow at the risk-free rate. Loviscek's (2017) analysis of data from 2000 through 2014 yields similar results, showing that a preferred stock fund allocation can reduce risk while preserving returns in an efficient mean-variance portfolio of mutual funds. Tracking the ten largest exchange-traded funds over periods starting between 2009 and 2013 and ending in October of 2016, Beck et al. (2017) obtain a significant and positive Jensen's alpha value for preferred stock exchange-traded funds. Furthermore, in the current historically-low interest rate environment, it is common to find PSREITs offering yields over 8% and thus after-tax returns of over 5%, which is much higher than currently available on Treasury securities and investment-grade corporate debt. This favorable after-tax yield provides income-focused portfolio managers and income-seeking investors with opportunities to meet their respective objectives.

The present study examines a widely overlooked type of income-producing security, namely the PSREIT security, and tests their portfolio-enhancement efficacy. To the best of the authors' knowledge, this work is the first study to construct time-varying optimal weights of PSREITs in risky portfolios incorporating S&P 500 index (SP500) and Bloomberg Barclays Aggregate Bond Index (BOND) securities, as well as equity REIT (EREIT) and mortgage REIT (MREIT) securities. Our study utilizes both dynamic conditional volatilities from univariate generalized autoregressive conditional heteroskedasticity (GARCH) models and rolling mean-variance optimization models to examine time-varying correlations and optimal allocations. In this study, we document PSREIT contributions to constructed portfolios in a non-recession economy.

We provide an overview of the data in Section II, and then examine short-term correlations and cointegration of the data in Section III. In Section IV, we introduce two alternative techniques for calculating optimal weights and time-varying correlations. In Section V, we examine the macroeconomic determinants of observed correlations and optimal weights. Liquidity constraints and other microstructure considerations are discussed in Section VI, and the study conclusions are presented in Section VII.

Descriptive Statistics

Weekly time-series data from January 2000 through December 12, 2019 were collated from the following five portfolio groups: (1) PSREIT securities from the Wells Fargo hybrid and preferred securities REIT index); (2) EREIT securities from the FTSE (Financial Times Stock Exchange) all-equity REIT index; (3) MREIT securities from the FTSE Mortgage REIT index; (4) SP500 securities; and BOND securities.

Statistics summarizing the weekly, continuously compounded returns obtained for the PSREIT, EREIT, MREIT, SP500, and BOND securities are summarized in Table 1. Note that significant mean weekly return rates are obtained for all five investment entities, ranging from 0.095 (BOND securities) to 0.201 (EREIT securities). Return variances for these outcomes, which provide a deeper perspective on the returns, range from 0.245 (BOND securities) to 10.22 (EREIT securities). The greatest reward/risk ratio by far, at 0.192, is obtained for BOND securities, while the lowest reward/risk ratio is obtained for SP500 securities, at 0.047. The distributions of returns in all cases are negatively skewed, and each series displays positive kurtosis (leptokurtic) (Table 1). The Jarque-Bera statistic for each dataset rejects a null hypothesis of normality at the 1% significance level. These results support the possibility that PSREITs may have portfolio enhancement attributes.

Short-Term Correlations and Cointegration Analysis

We proceed with an investigation of the short- and long-term relationships of PSREITs with other securities for which the diversification benefits are associated with low correlations and non-cointegrating relationships between the different assets within the portfolio. First, we construct 100-week rolling window correlations between PSREIT performance and the performance of each of the other analyzed securities to examine time-varying short-term associations. The first and last subsamples for the 100-week rolling window are 2000:02:26–2002:01:19 and 2018:01:27–2019:12:21. The time-varying nature of the short-term relationship between the PSREIT securities and each of the other four analyzed securities are presented in Fig. 1. Notably, PSREIT correlations with the other assets from the rolling estimations were weak, especially in the case of BOND securities (Table 2).

Rolling window correlations. The first 100-week rolling window subsample is from February 26, 2000 to January 19, 2002, and the last subsample is from January 27, 2018 to December 21, 2019. The average correlations (dashed lines) of the PSREIT with the EREIT, MREIT, SP500, and BOND are 0.46707, 0.46579, 0.35646, and 0.26331, respectively

Time-varying and low short-term correlations could overestimate diversification benefits if PSREIT securities share a long-term common trend with other assets in the investor’s portfolio. To explore this possibility, we conduct bivariate cointegration tests between the PSREIT index and the EREIT, MREIT, SP500, and BOND indices. First, we probe the stationarity and long-term cointegration relationships of these indices with the Dickey-Fuller and Phillips-Peron unit root tests, followed by Johansen Trace analysis (Table 2). Each series has a one-unit root at the 1% significance level that a first difference will remove. Thus, we can proceed under the assumption that each series is integrated at an order of 1 [i.e., I(1)] and that a cointegration analysis is necessary to evaluate the long-term benefits of including PSREIT securities in our portfolios Table 3.

Given these results, we search for a single common integrating factor between the PSREIT securities and those from other markets. We perform a rolling window Johansen's cointegration trace test to determine whether they are cointegrated and look for evolution in long-run relationships over time from the first to the last rolling window subsample. The lag in the vector autoregression model is three, and the model is specified with a constant term restricted to the cointegrated space.

As shown in Fig. 2, the rolling estimation results confirm that PREIT securities are cointegrated with the other markets with only 32% of the sample periods extending. Precisely, the percent rejection of the null hypothesis of no cointegration of the PREIT with the EREIT, MREIT, SP500, and BOND is 35%, 33%, 31%, and 27%, respectively. Thus, the absence of a long-run relationship of PREIT securities with the other investments supports the notion that there could be diversification benefits from incorporating PSREIT securities into market portfolios in the short term and in the long term. Furthermore, our correlation and cointegration analyses suggest that potential gains might be realized from diversification in the case of the PSREIT and BOND indices.

Rolling Johansen trace test for cointegration between PSREITs and the other assets in the portfolio over 100-week subsamples. The first 100-week rolling window subsample is from February 26, 2000 to January 19, 2002, and the last subsample is from January 27, 2018 to December 21, 2019

Portfolio Diversification and Optimal Weights

Mean-variance Optimization

Markowitz (1952) introduced conventional mean-variance optimization, which generates an optimal portfolio offering the highest expected premium per unit of risk. In our analysis, we calculate the optimal weights for a portfolio that includes PREIT, EREIT, MREIT, SP500, and BOND securities by considering the following optimization problem:

subject to

where

and xi is the optimal weight assigned to security i, and N is the number of securities.

Traditionally, a portfolio's risk is measured by the time-invariant standard deviation (SD), which is constant during investment holding period. However, unstable correlations have been documented between assets, suggesting that having different asset allocations across subperiods could increase returns while reducing risk. To evaluate the improvement of asset allocation when including PSREIT securities and recognizing time-varying correlations, we calculate the Sharpe ratio for 100-week rolling window subsamples, starting with the first subsample of February 26, 2000 to January 19, 2002 through the last subsample of January 27, 2018 to December 21, 2019. The optimal portfolio weights assigned to the PSREIT, EREIT, MREIT, SP500, and BOND investments from the rolling 100-week periods for three models are reported in Table 4 and illustrated in Figs. 3, 4, 5 and 6.

Rolling 100-week optimal weight for PSREIT in Model I. The first 100-week rolling window subsample is from February 26, 2000 to January 19, 2002, and the last subsample is from January 27, 2018 to December 21, 2019

Rolling 100-week optimal weights of the EREIT, MREIT, SP500, and BOND in Models I and II. The first 100-week rolling window subsample is from February 26, 2000 to January 19, 2002, and the last subsample is from January 27, 2018 to December 21, 2019

Rolling 100-week average returns and Sharpe ratios for Model I and Model II. The first 100-week rolling window subsample is from February 26, 2000 to January 19, 2002, and the last subsample is from January 27, 2018 to December 21, 2019

Rolling returns, Sharpe ratios, and optimal weights for Model III from rolling 100-week periods. The first 100-week rolling window subsample is from February 26, 2000 to January 19, 2002, and the last subsample is from January 27, 2018 to December 21, 2019

The portfolio compositions, Sharpe reward-variability ratios, and optimal component weights of Models I, II, and III are reported in Table 4, and the impact of adding PSREIT securities to portfolios is illustrated in Fig. 5. Notably, a higher Sharpe reward-variability ratio is obtained for Model I (PSREIT included) than for Model II (PSREIT not included), suggesting that inclusion of PSREIT securities (average weight, 39.26%) can play a substantive role in reducing portfolio risk over time. In addition to increasing the Sharpe reward-variability ratio by 25.11%, we find that PREIT inclusion at the expense of BOND inclusion (weight reduction, 27.32%) increases average weekly rolling-portfolio returns of the rolling portfolios by 4.96% (Table 4). These results demonstrate that PSREIT inclusion can be employed defensively and as a replacement for BOND investment. Analysis of Model III, which includes the PSREIT, EREIT, and MREIT indices, shows that the PSREIT index (Model III weight, 0.80) plays a dominant role (Table 4 and Fig. 6). Furthermore, as shown in Fig. 7, Model I (unrestricted frontier with PSREIT) offers higher returns than Model II (restricted frontier without PSREIT) for given levels of risk across the spectrum, providing additional evidence of the efficacy of PREIT security investment. These results provide additional support for the inclusion of PREIT securities in portfolios, particularly those targeting risk reduction.

Unrestricted efficient frontier (Model I) and restricted efficiency frontier (Model II). Model I and Model II data are shown with a solid line and a dotted line, respectively

In sum, the present analysis yields three main findings. First, the PSREIT and BOND indices constitute 80% of the optimal weights among the five presently analyzed portfolio group constituents. Second, the PSREIT portfolio outperforms both the EREIT and MREIT portfolios significantly in terms of a reward-risk basis. Third, during times of economic expansion, the PSREIT portfolio tends to replace the BOND portfolio's role in optimal allocations.

Dynamic Conditional Correlation (DCC)

Results based on correlational data without appropriate allowances for time-varying market volatility can be problematic. As demonstrated by Forbes and Rigobon (2002), correlations become seriously biased when time-varying volatility is not accounted for in portfolio efficiency estimations. The existence of such time-varying volatility is well-documented for real estate asset returns. In the context of this study, low time-varying volatility of PSREIT securities could have an artificial reducing influence on pairwise unconditional correlations with other assets. Thus, to estimate the time-varying correlations of REIT markets with both stock and bond markets, we employ a DCC-bivariate GARCH model (Engle, 2002). As described by Sadorsky (2012), for DCC estimation, we first fit each pair of returns (rit) to the vector autoregressive moving average (VARMA)-GARCH(1,1) model proposed by Ling and McAleer (2003). This specification for conditional variance (hit) allows for covariance and correlation spillovers as follows:

where Ωi, t − 1 is the information available at time t−1, and the coefficients αiiand βii, respectively, are measures of short- and long-term persistence in the conditional variance equations. Meanwhile, αij and βij (i ≠ j) are measures of short- and long-term volatility spillover across markets, and zt is the standardized residuals vector with a mean of zero and a variance of one.

Second, as described by Engle (2002), we allow the conditional matrix to be time-varying (Rt) as follows:

where Ht is the conditional covariance matrix, and Dt is the diagonal matrix with the square root of the estimated GARCH variance \(\Big({D}_t={\operatorname{diag}}\ \left\{\sqrt{h_{i,t}}\right\}\)). Equation 4 can be rewritten as:

As stated by Engle (2002):

where Qt is the covariance matrix that can be defined as:

In Eq. 8, θ1and θ2 are non-negative scalars (θ1+ θ2 < 1) that introduce a time-varying property into the correlation matrix. In simpler terms,

where \(\overline{\rho_{ij}}\) is a (2 × 2) matrix of correlations among the standardized residuals (zt) calculated from the bivariate VARMA-GARCH (1,1) model. Intuitively, with Engle's (2002) method, the values of qij are iterated over time, being updating as a function of deviations observed in lagged zizj and qij with respect to constant correlation. When θ1 = 0 and θ2 = 0, the DCC model is reduced to a constant conditional correlation model as follows:

Based on normality, the log-likelihood implied by Equations 1–7 is maximized to estimate Rt. Quasi-maximum likelihood properties of estimated coefficients are retained even in the absence of normality.

Finally, we utilize Kroner and Ng’s methodology (1998) to calculate the optimal portfolio weights (W) between assets i = {PREIT} and j = {EREIT, MREIT, SP500, and BOND} at time t as follows:

where hjj, t is the conditional variance of asset j at time t, hii, t is the conditional variance of PREIT at time t, and hij, t is the conditional covariance between PREIT and asset j at time t. These relationships are subject to the following conditions:

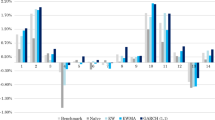

The results obtained with our DCC-GARCH model are reported in Table 5. Notably, the estimated θ1 and θ2 are statistically significant at the 1% level for all specifications, and their sum is very close to one in case of PSREIT/SP500, PSREIT/MREIT, and PSREIT/BOND but below one in case of PSREIT/EREIT. Thus, generally, our results confirm DCC persistence between PSREIT securities and the other investments. In addition, all conditional ARCH (αii) and GARCH (βii) coefficients are statistically significant at the 1% level, and the βii coefficients are larger than the αiicoefficients, demonstrating stronger persistence of the conditional correlations in the long term than in the short term (Table 5). Statistical significance of α12, α21, β12, and β21 at the 1% level signifies substantial short- and long-term volatility spillover across markets while statistical significance of five of eight coefficients (a12 and a21) at the 10% level signifies strong spillover across the mean equations (Table 5). Note that the optimal portfolio weights reported in Table 5 demonstrate highly dominant PSREIT weights in PSREIT & EREIT (98.9%), PSREIT & MREIT (96.8%), and PSREIT & SP500 (92.1%) portfolios, but a minor PSREIT weight in the PSREIT & BOND portfolio (34.1%).

Graphs showing the evolution of dynamic time-varying optimal weights of PSREIT securities when combined with EREIT, MREIT, SP500, and BOND securities are presented in Fig. 8. Note the increasing PREIT weight in the PREIT & BOND portfolio during expansionary economic periods. Overall, the optimal weights calculated from DCCs are consistent with the main findings that we obtained for rolling windows of mean-variance optimization in section IV.A.

Time-varying correlations and optimal weights from the dynamic conditional correlation (DCC) model. The first 100-week rolling window subsample is from February 26, 2000 to January 19, 2002, and the last subsample is from January 27, 2018 to December 21, 2019

Macroeconomic Determinants of Time-varying Correlations and Optimal Weights

Because understanding the forces that drive time-varying correlations between securities is crucial for asset allocation and risk management, we investigate the macroeconomic determinants of time-varying correlations between PSREIT securities and each of the other investment types based on the rolling window of mean-variance optimization data in section IV.A. In accordance with the work of Yang et al. (2012), we select the following four candidates for analysis: default spread (DEF), term spread (TERM), mortgage spread (MGTB), and Chicago Board Options Exchange SP500 volatility index (VIX).

We define DEF as the difference between Moody BAA and AAA bond yields. The magnitude of DEF increases in periods of economic deterioration, especially during recessions and other episodes of financial stress. DEF may widen or narrow depending on economic conditions. For example, Moody BAA bond yields and DEF attained their maximum values (9.54% and 3.5%, respectively) during the Great Recession of 2008–09.

We define TERM as the difference between the ten-year and three-month U.S. Treasury yields, based on data from the Treasury yield curve, a widely recognized economic health indicator. Generally, inverted yield curve, in which the three-month Treasury yield exceeds the ten-year yield, is considered to be a harbinger of an impending recession. However, the term premium can also be affected by a Federal Funds rate lift and large capital inflows.

We define MGTB as the difference between the thirty-year mortgage rate and the thirty-year Treasury bond yield. Yang et al. (2012) characterize MGTB as the best available macroeconomic proxy for the real estate sector. Like DEF, MGTB attained its maximum value (2.74%) during the real estate turbulence peak in December 2008.

Finally, VIX reflects the overall near-term market risk implied by the options market. Like DEF and MGTB, VIX peaked during the most recent financial crisis. A dummy variable, called NORMAL, is added to account for potential changes in correlations during recessions.

As shown in Table 6, correlations of the PSREIT with the EREIT, MREIT, and SP500 rise during periods characterized by low volatility, healthy economic conditions, and decreasing values of DEF, TERM, and MGTB. On the contrary, PSREIT-BOND correlations increase during periods characterized by poor economic conditions, high volatility, and increasing DEF values, TERM, and MGTB. These patterns of data highlight the debt and equity characteristics of PSREIT securities. The fact that they takes on the more positive attributes of debt and equity during expansionary macroeconomic periods suggests that they may represent a security type that is a positive portfolio contributor.

An investigation into the macroeconomic times-series determinants of the five optimal weights obtained in this study is in order. We supplement DEF, TERM, MGTB, and VIX with two determinants: (1) lagged changes in the ten-year Treasury yield; and (2) NORMAL, the dummy variable. The former is intended to capture the impact of capital gains (or losses) on weights. The latter, NORMAL, has a value of 1 during normal economic periods and a value of 0 otherwise. We define a normal economic period as one without recessions and without early recoveries, wherein a recovery has the same duration as the proceeding recession.

Several significant findings are reported in Table 7. First, optimal PSREIT weights increase by 0.326 during normal times, while BOND weights decrease by 0.286. Thus, optimal portfolios show high PSREIT weights with low BOND weights when the economy is normal. Second, BOND capital losses associated with higher ten-year yields contribute to an increasing allocation to PSREIT weights. Third, higher volatility, measured by the VIX, are associated with increased optimal MREIT and BOND weights together with decreased weights for other assets in the portfolio. Fourth, when DEF and MGTB increase during recessions and times of financial stress, PSREIT weights decrease and BOND weights increase in optimal portfolios.

Other Considerations

The present weight allocation for the PSREIT portfolio is set to 42% only to demonstrate that PSREIT securities can be a valuable addition to income-generation portfolios and that PSREIT securities represent an asset type investors should be made aware of, especially given the scant attention currently given to them. Indeed, the present results show that PSREIT reward-risk attributes favor PSREIT securities over bonds, especially during expansionary economic periods, when they may be the first choice of income-seeking investors. These results further indicate that PSREIT securities would be a worthy addition to income-generating portfolios and the classic 60-40 portfolio of stocks and bonds, especially during macroeconomic expansions and low-interest-rate periods.

As a caveat, because their trading volumes are light, PSREIT securities have illiquidity relative to stocks and investment-grade bonds. This illiquidity leads to relatively high yields (currently >8%) even during the current low-interest-rate period. As a result, however attractive the yields, large-scale institutional investors and managers of large portfolios can face difficulties entering and exiting the market. This illiquidity could reduce the pool to individuals and limit it to small-portfolio managers who can invest in PREIT securities. For managers of more considerable funds, it may lead to a smaller allocation than what would appear optimal. Notwithstanding, PSREIT securities are worthy candidates for significant, income-seeking funds for which liquidity is not a major issue, including investments of interval and tender offer funds.

We recognize that selections of other portfolios beyond the five examined here would produce different PSREIT weights. However, for the period under study, a 20-year span in which preferred stocks have been receiving increasingly greater attention, the results demonstrate that PSREIT securities deserve more attention from the investment community than they have thus far been receiving in published studies and investment advisory reports.

Conclusion

Investor sentiment in some circles is dubious of the efficacy of preferred stocks in investment portfolios, due to characteristics such as thin trading, illiquidity, and subordinated bond interest-rate sensitivity. However, the effectiveness of PSREIT securities as a component of portfolio allocations has rarely been reported. This dearth of research motivated this study in which we investigated whether PSREIT securities show portfolio enhancement attributes during the period of January 2000 through August 2019. Using five portfolios in which PSREIT securities are combined with EREIT, MREIT, SP500, and BOND securities, adjusting for non-stationarity of the data and variance in macroeconomic conditions, we found here that PSREIT securities have significant diversification benefits and their weight expands at the expense of the weight of bonds during recessions and early economic recovery periods. We also established that pairwise correlations of the performance of PSREIT securities with that of other securities increase during periods of low volatility, healthy economic conditions, and decreasing DEF and TERM values. These findings align with emerging literature reporting portfolio enhancement attributes of preferred stocks.

References

Beck, K. L., Chong, J., & Phillips, M. G. (2017). Risk-adjusted performance of the largest active ETFs. Journal of Wealth Management, 20(3), 52–63.

Bildersee, J. S. (1973). Some aspects of the performance of non-convertible preferred stocks. Journal of Finance, 28, 1187–1201.

Blanchett, D., & Ratner, H. (2015). Efficient income investing. Journal of Portfolio Management, 41(3), 117–125.

Boudry, W. I., deRoos, J. A., & Ukhov, A. D. (2020). Diversification benefits of reit preferred and common stock: new evidence from a utility-based framework. Real Estate Economics, 48(1), 240–293.

Chen, C. R. (1996). January seasonality in preferred stocks. Financial Review, 31(1), 197–207.

Crabbe, L. E. (1996). Estimating the credit-risk yield premium for preferred stock. Financial Analysts Journal, 52(5), 45–56.

Damodaran, A. (2012). Investment Valuation: Tools and techniques for determining the Value of any Asset, New York, NY: John Wiley & Sons. https://www.wiley.com/en-us/ Investment+Valuation%3A+Tools+and+Techniques+for+Determining+the+Value+of+Any+Asset%2C+3rd+Edition-p-9781118011522.

Emanuel, D. (1983). A theoretical model for valuing preferred stock. Journal of Finance, 38, 1133–1155.

Engle, R. (2002). Dynamic conditional correlation: A simple class of multivariate generalized autoregressive conditional heteroskedasticity models. Journal of Business & Economic Statistics, 20(3), 339–350.

Forbes, K. J., & Rigobon, R. (2002). No contagion, only interdependence: Measuring stock market comovements. Journal of Finance, 57(5), 2223–2261.

Johansen, S. (1991). Estimation and hypothesis testing of cointegration vectors in gaussian vector autoregressive models. Econometrica, 59(6), 1551–1580.

Kroner, K. F., & Sultan, J. (1993). Time dynamic varying distributions and dynamic hedging with foreign currency futures. Journal of Financial and Quantitative Analysis, 28(4), 535–551.

Li, G., McCann, L., & O’Neal, E. (2010). The risks of preferred stock portfolios. https://www.slcg.com/pdf/workingpapers/Preferred%20Stock%20Paper.pdf.

Ling, S., & McAleer, M. (2003). Asymptotic theory for a vector ARMA-GARCH model. Econometric Theory, 19(2), 280–310.

Loviscek, A. L. (2017). Should preferred stock funds be included in mutual fund portfolios? Journal of Wealth Management, 20(1), 83–96.

Markowitz, H. M. (1952). Portfolio selection. The Journal of Finance, 7, 77–91 https://www.jstor.org/stable/2975974?origin=crossref

Sadorsky, P. (2012). Correlations and volatility spillovers between oil prices and stock prices of clean energy and technology companies. Energy Economics, 34(1), 248–255.

Sharpe, W. F. (1992). Asset allocation: Management style and performance measurement. The Journal of Portfolio Management, 18(Winter), 7–19.

Stickel, S. (1991). The ex-dividend behavior of nonconvertible preferred stock returns and trading. Journal of Financial and Quantitative Analysis, 26(1), 45–61.

Swedroe, L. (2016). Are preferred stocks an alternative to safe bonds. Advisor Perspective. September, 26, 2016 https://www.advisorperspectives.com/articles/2016/09/26/are-preferred-stocks-an-alternative-to-safe-bonds

Vetter, D. E., & Wingender, J. R. (1996). The January effect in preferred stock investments. Quarterly Journal of Business and Economics, 35(1), 79–86 http://www.jstor.org/stable/40473175

Yang, J., Zhou, Y., & Leung, W. K. (2012). Asymmetric correlation and volatility dynamics among stock, bond, and securitized real estate markets. Journal of Real Estate Finance and Economics, 45(2), 491–521.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher’s Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

About this article

Cite this article

Anderson, R.I., Guirguis, H. & Loviscek, A.L. Do Preferred REITs Have Portfolio Enhancement Attributes? An Empirical Investigation. J Real Estate Finan Econ 67, 656–672 (2023). https://doi.org/10.1007/s11146-021-09873-x

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11146-021-09873-x