Abstract

Natural gas is a worldwide commodity traded among regions. Regulated or unregulated natural gas markets are in a new process phase leading to a critical change in the market structure and organization while demand grows. Moreover, international trade of high gas volumes and complexity of transportation alternatives create new difficulties in market modeling and price forecasting. Hence, there is a need to define and analyze the future of recently developing gas markets. Turkey has an important geopolitical position with short distances to the regions of the largest natural gas reserves. While largely dependent on the gas import from Russia, Iran and Azerbaijan through pipelines, it is also very close to high demanding countries. That is why Turkey may have the opportunity to play an important role in pricing gas between international market players and becoming a market maker. This paper aims to underline the importance of hub pricing through structuring a virtual gas trade hub in Turkey.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Being a substitute to oil and oil-products, natural gas has a very important and strategic role in the energy agenda of the countries. As Stern and Rogers have pointed out, northern and central European countries have begun to increase the use of natural gas—especially in domestic consumption—which has more advantages than coal and petroleum products since 1950s [30]. As a result of development of European economics after 1970s, industrial and household natural gas consumption for heating rather than coal and oil, and electricity generation from combined cycle gas turbine power plants have widely expanded throughout the countries, hence, natural gas industry has highly accelerated. With these developments, the European countries concurrently have given importance to the investment of pipelines and LNG facilities in order to facilitate the transportation of natural gas and to ensure supply security [30].

The recent developments especially in natural gas and shale gas reserves have huge impacts on global natural gas trade dynamics. On the other hand, global natural gas supply chain network has technical limits for transportation; hence those developments are not sufficient in terms of integration of natural gas into the global market, contrary to the fact that the oil market has been successful in this regard [15]. In the regions where natural gas reserves are available, different types of global natural gas markets have developed due to the effects of demand level and market dynamics. In recent years, approximately 70% of the natural gas flow in the world has been transported to the markets around the producer countries, while 20% has been delivered to the international area through pipelines, and 10% has been shipped to consumers as LNG. The development of international natural gas markets is mainly based on the natural gas potential, the discovered reserves, demand and supplier structures, and working of the entire system in harmony [21].

It is a well-known fact that there are many discussions about the future of pricing mechanisms. The most critical one is whether pricing mechanisms generally shaped by oil-indexed contracts will try to reinforce their priorities in the world and strengthen their positions in the global gas-trading network, or these pricing methodologies will be replaced by other methods. It is also important how the prices in the natural gas trading hubs will continue against oil indexed prices in the world. The question of how the obligations of importers will be shaped under the presence of new mechanisms due to the current trade structure will also need. As the uncertainty of natural gas pricing systems increases and global wealth in the future loses clarity, the question of “how transportation safety and investments will be shaped” is yet to be answered. Moreover, how the gas power plants (that play an important role in the electricity markets) will be affected by these pricing mechanisms is to be answered.

In the middle of all these developments, Turkey is known to have a strong geographical position in the new hydrocarbon age. As the national and international reports claim, Turkey has no significant fossil fuel reserves. However, it is encircled by Russia, Azerbaijan, Iran, Turkmenistan, Iraq, Qatar and other Middle East countries. In the West, Europe’s increasing demand for natural gas and desire to secure supply allow the expansion of the market area where these reserves will be offered. Therefore, Turkey is an important country in order to ensure energy security and to create supply sources through various routes for Europe. Natural gas rich countries may choose Turkey in constructing new pipelines due to its critical geographical position. However, Turkey’s natural gas network structure, low storage capacity, low transmission capacity and regional problems do not still allow to realize its full potential. Turkey will have a great opportunity to have a saying in international gas trade operations and investment cooperation in a geopolitically sensitive environment if Turkey can increase the development of new natural gas market structure to support its goal of becoming a natural gas hub [19]. This paper analyzes the dynamics of Turkish gas market and discusses the opportunity for constructing a natural gas Hub in Turkey.

The paper is organized as follows. The players in natural gas trade, market structures and the mechanisms of the formation of gas prices were overviewed; and the characteristics of the natural gas hubs were detailed in section two. Section three covers the dynamics of the Turkish natural gas market and the potential gas import projects that are on the agenda. Finally, section four concludes by discussing the results.

2 Overview of natural gas markets

It is clearly known that 1 day we will run out of the natural resources. According to Hubert’s approach, developing technology and increasing of the usage of other alternative fuels, especially renewable energy sources, shift the curve, which can be seen in Fig. 1, to the right and delay the reaching of maximum production levels of oil and natural gas [10].

Trend of hydrocarbon market and production [10]

2.1 Natural gas producers and exporters

Amongst the natural gas rich countries, especially Turkey’s two neighbors have very important resources [34]. On the other hand, there is no single European country in the top 10 list in terms of its reserve potential (see Fig. 2). This means that the EU may need to transfer the concentrated gas reserves from Asia, the Middle East and Russia to the West, and set gas pricing in a hub.

(adapted from TPAO [34]

Countries with the most natural gas reserves

2.2 Natural gas consumers and importers

Europe’s consumption pattern in the last 4 years has generally increased in the same quarter of each year, as can be seen in Fig. 3. In order to ensure the supply of these quantities, huge import volumes are needed because the production values of the region are not sufficient to meet the demand [11].

EU countries gas consumption, net imports and production values [11]

According to Prognos, demand pattern of the European Union for natural gas imports is not very sharp, but it is expected to be in an upward trend by 2050, as shown in Fig. 4 (in billion Sm3). This increase is an important need for the sustainability of gas markets so that both household and industrial consumption and the operation of power plants will be lasted [27].

EU’s gas import demand projection (Prognos [27]

The net import value is obtained by subtracting the amount of exported gas from the total imports of EU member countries. As shown in Fig. 3, the net import value is above the total production value of the Union. It is also clear that Russia and Norway are the main suppliers [11] (Fig. 5).

Countries importing gas to EU countries [11]

Imported Russian gas, which is available to European Union member states, enters the region through three main routes:

-

1.

With the activation of the brotherhood gas pipeline through Ukraine in 1967, 100 billion Sm3 gas is transported to Slovakia. Here, the route of the pipeline is divided into two: one line goes to the Czech Republic and the other to Austria. Moreover, the gas from this second pipeline is also sent to Italy, Hungary, Slovenia and Croatia, as a result, the transportation is carried out through the Balkan route [14].

-

2.

Gas is supplied to Germany via the Yamal pipeline through Belarus. The construction of this line, which has a total length of over 2000 km, started in 1994. It currently has 14 compressors and a capacity of approximately 33 billion Sm3 gas per year [14].

-

3.

Another gas supply to Europe is the Nord Stream pipeline, which is approximately 1224 km long, with a capacity of 55 billion Sm3 carrying under the Baltic Sea. Russia sees the UK, the Netherlands, France, Germany, Denmark and other Northern European countries as a market for itself with this line, which reaches the Greifswald region near Germany’s coast [14] (Figure 6).

Fig. 6

Routes from Russia to Europe [11]

With the conflict in Russian–Ukrainian natural gas prices in 2009, import diversity has emerged as an increasingly important element in the agenda of European policy makers. The problems in Ukraine’s gas supply which started in 2014, together with the The Crimean crisis after the Western sanctions imposed on Russian companies have brought back the problems of European gas supply security and import diversification. This accounted for about 15% of the total gas imports of the EU in the same year. The fact that the problem of Russia’s Crimean peninsula co-existed with an already existing Russian–Ukrainian gas price dispute has increased the fear of the European Union’s access to natural gas import sources [4].

2.3 Price formation in liberalized natural gas markets and market structure

In addition to the physical difficulties for natural gas, the pricing mechanisms, which are the economic backbone of trade, generally include prices determined by the market regulators, indexed prices for other fuels, or prices in the free markets. Since natural gas does not initially have its own pricing system unlike petroleum, the main structure of commercial natural gas contracts in each of the competitive market areas has developed independently from each other. Therefore, systematic pricing capabilities of the already existing mechanisms have decreased in terms of having the same structure and the interaction with each other. To determine the natural gas prices, gas contracts are indexed to oil and oil products. This initially was very popular in Europe and then became widespread in Asia. Unlike this system, the systematic approach of natural gas hub pricing has had an active role in the US Commodity Markets [23]. Figure 7 shows the development of the trading structures and market sizes of natural gas trading operations. It is argued that each region follows the same steps with oil, even if it is not at the same speed [1].

(adapted from Accenture [1]

Development dynamics of natural gas markets

2.3.1 Price formation

Pricing mechanisms that allow the formation of prices based on supply and demand are one of the main elements of a market liberalization path. In order to ensure the functioning of the system, regulatory agents/companies may take various fees from market players, but even when doing so, it is necessary to avoid all kinds of activities and regulations that prevent the formation of a free price [17].

Different pricing mechanisms are used during the realization of natural gas trading activities. The most commonly known methods are detailed below [20].

-

1.

Oil price escalation (OPE) With this method, the pricing system is based on a special formulation that includes the prices of other commodities such as gas oil and crude oil which are substitutes for natural gas. Some approaches include electricity prices and coal prices during formulation.

-

2.

Gas-on-gas competition (GOG) The price is determined by the intersection of supply and demand for gas for different periods of time such as daily, monthly and yearly. This type of price formation today occurs in virtual natural gas hubs such as TTF and NBP, or physical natural gas hubs such as ZEE and Henry Hub. In the markets dominated by this pricing system, the level of development of futures markets is also very important.

-

3.

Bilateral monopoly (BIM) Bilateral agreements between a major buyer and a major seller determine the price. Such agreements are mostly signed either through state-owned companies or through direct intergovernmental dialogue. In this method, commercial activities are generally carried out at a fixed price on an annual basis.

-

4.

Netback from final product (NET) The price to be paid to the natural gas supplier is defined as a function based on the price of the final product produced by the customers who will use the gas as input in production operations. This can occur when natural gas is used in chemical plants as methanol or ammonia and the input is the main variable cost for the production of the targeted product.

-

5.

Regulation—cost of service (RCS) The price is determined or approved by an official public company or related ministry, but the price level must have a level of return that is acceptable to the investment, including an acceptable rate of return for investment and the payback of the relevant investment.

-

6.

Regulation—social and political (RSP) The price is determined without relying on any systematic, possibly by a ministry, to meet rising costs, or by taking into account political and social balances as a source of income for the government.

-

7.

Regulation—below cost (BC) With this approach, the price is applied to citizens, usually under the average cost of transportation and production of natural gas as a state subsidy.

-

8.

No price (NP) The extracted and produced natural gas can be offered free of charge to citizens and industrialists to be used as an input for fertilizer and chemical plants or for processing in refinery processes.

In 2016, around 1000 billion Sm3 natural gas was imported via LNG and pipelines [20]. Figure 8 shows which of the pricing mechanisms mentioned in this section are carried out between 2005 and 2016 in global natural gas trade. The existence of oil-indexed contracts in the world still continues to dominate the 49% of the import market.

Distribution of pricing mechanisms used in imports in the world between 2005 and 2016 (IGU [20]

There are significant risks related to cash flow management and exchange rate for pricing mels using natural gas contracts integrated into the change in oil prices. For example, although there are some specific definitions and different variables in each European oil-indexed natural gas contract, the general natural gas price calculation formula in order to express the structure of the contracts is shown in Eq. 1. [24].

Pn represents the natural gas price and P0 represents the first accepted price at the time of signing the natural gas contract. Since pricing is performed according to other product groups, W in the numerator of the equation shows the weight ratio given to those products; and F in the numerator shows the market prices of those products at the time of the gas imports. The F in the denominator reflects the market prices of the products at the time the contract is signed. Such formulation may also include fuel oil or gas oil as a parameter. The change in prices of the parameters used in the formulation is effective in the price of the gas being traded. Even if the average price of these two types of petroleum products is designed in EUR/ton, the real market price of gas for such contracts is taken into account in USD/ton. As a result, the EUR-USD exchange rate risk has a significant impact on pricing [33].

2.4 The hub concept in natural gas markets

In the IEA report, Dengel explained the most fundamental feature of the markets in terms of the formation of natural gas prices as follows: “It has the feature of being a place where both the current market players and the newcomers who want to be included in the same transaction are able to access under the same conditions, and the trading volume is high and there is a single price. Thus, this situation will be able to provide remarkable and reliable price formations in the spot and futures and options market which are not subject to any external influence.” [18]. In line with this philosophy, there is a need for a trade platform where gas supply can be provided to meet gas demand. This structure is defined as a natural gas hub.

A spot market where gas is traded for a limited period of time, and a futures market where natural gas delivery can be carried after a few years are alternative trade operation channels in a hub. The centers that enable these commercial activities are divided into two categories as virtual hub and physical hub depending on the physical gathering of gas supply at a point [17].

The way applied actively in Europe is the increase of virtual trade hubs. Among the European natural gas markets shown in Fig. 9, the Belgian-Zeebrugge Hub and the Austrian Central European Gas Center are the only physical hubs. Such hubs offer a structure where the purchase and sale of a significant amount of physical natural gas is achieved through storage and pipeline systems. On the other hand, the European virtual trading hub model combines all delivery points in an entry-exit zone. The network operator of the region provides transportation services between entry and exit points and balancing services. At the same time, European gas markets have developed from long-term contracts to short-term contracts, to flexible spot market structures and to the active use of futures products [19].

European natural gas markets

The development of these markets in the name of being able to carry the characteristics of the Trade Hub in the last 4 years has been evaluated by EFET (European Federation of Energy Traders). In the study, the natural gas markets of the leading countries in Europe were divided into two categories: Developed and developing natural gas hubs. Within the scoring system, EFET considers the country with the most advanced natural gas market as 20 points. It has tried to show how far the countries with the trade hub have developed the market depths and how far the countries without the hub have been able to reach that point [12] (Fig. 10).

Evaluation of European natural gas markets in terms of being a trade hub (EFET [12]

In the natural gas markets, the main factors that have an impact on the global markets are effective on the direct supply and demand side and shape the future of the natural gas market. Several factors and definitions on both the demand and supply side are listed below. In general, the essential elements that may affect the supply of natural gas include extraordinary developments, new pipelines, floating technologies, new LNG capacities and government policies at national level. On the demand side, the most important factors are the economic growth of countries and government policies. Figure 11 shows the relationship between some factors that have an active role in natural gas markets [21].

(Adapted from [21]

The relationship between some factors in natural gas markets

-

1.

Storage The successful management of sudden demand fluctuations and seasonal changings is also directly related to the use of storage facilities in addition to natural gas production. As an expected consequence of this, the capacities of these facilities have an effect on the prices of natural gas since the amount of gas that will be in the storages is related to the amount of supply to be offered to the market [22]. Storage, especially in the case of lack of local natural gas production and sufficient imports, is a necessity to meet the sudden and seasonal increases in demand. In particular, during the declines in demand, storage facilities increase their occupancy rates with imported and local production gas quantities. The capacities of the storage facilities also support the efficient operation of the network in addition to meet the sudden demands [7].

-

2.

Transmission infrastructure Disruptions caused by planned maintenance, heavy weather conditions or problems in operating systems can lead to short-term negative effects in natural gas supply [22]. Moreover, since natural gas has a lower energy density and different chemical properties, its transportation cannot be easily carried out like oil. There is a need for a specially planned pipeline network to supply and deliver the gas to the end user [2]. The effects of technological progress on the gas supply and the increase in demand have also had an important impact on the management of the network [3].

-

3.

Climate and weather condition Prices are severely affected if there is no supply of gas that can respond to the demand increases that occur in the event of severe and unexpected sudden weather events. Especially, when the network is running at full capacity, additional demand will not be met. Under such conditions, prices may increase to very high levels to reduce natural gas demand. Another condition that has an effect on prices is the temperatures in the cooling season. Because the gas power plants for electricity generation use natural gas as fuel to meet the electricity demands caused by the intensive operation of the air conditioners. This situation may lead to a decrease in the amount of gas in the storages. Under the circumstances these decreases cannot be compensated, gas prices may show an upward trend in the course of winter demand [22]. In addition, harsh climatic conditions can also affect production activities. For example, a significant portion of total gas production in the United States is provided by offshore production, and severe hurricanes in 1997 and 2011 led to 8% reduction in the production. These cuts in the supply side caused the fluctuations in prices [2].

-

4.

Long term contracts In particular, prices for natural gas imported to Central and Eastern Europe are generated by long-term contracts based on the terms of take or pay, which are usually linked to oil prices. In order to block potential arbitrage earnings by importers, contracts held during import operations usually include a clause which means that gas prices are limited for only the importing market. This is called “destination-clause” [29].

-

5.

Import structure Pipelines, LNG terminals, capability of infrastructure, content of contracts, and pricing mechanisms of imported gas are main parameters that have an effect on the definition of import structure. For example, globally speaking approximately 80% of LNG imports are long-term contracts, with destination-clause and mostly oil-indexed prices, while only about 20% are traded on the spot gas market [6].

-

6.

Natural gas production While natural gas production is relatively unchanged throughout the year, problems on short-term supply shortages may have temporary effects on production. Examples of such situations are the absence of a qualified workforce at the production sites for a certain period of time. Another obstacle is the lack of necessary equipment. As a result of the unusual cost of production equipment such as drilling rigs, any temporary failure of the equipment may cause operations to be stopped until a new equipment installation is made. A third obstacle is due to regulatory issues. Even if new drilling sites are explored, permits to be obtained within the framework of the regulations and extension of the license rights will affect the gas production time [16]. Both the production efficiency and the investments to be made to ensure supply security are very important due to the above-mentioned obstacles. Also, the gas price levels are very critical in order to cover the search and production costs [13]. Some critical weather events may also have an impact on natural gas production. For example, hurricanes on the US Gulf Coast reduced approximately 4% of US natural gas production from 2005 to 2006 [7].

-

7.

Export volume If there is an obligation to export natural gas especially because of gas trade contract terms (as Turkey’s export 0.75 billion Sm3/year Azerbaijani gas to Greece), this situation may affect the gas prices in the spot market. Due to the destination-clause restriction of the structure of contracts based on long-term oil, the re-export of imported gas is prevented. With the active business of spot markets and the lifting of such restrictions, more integrated gas trading will be possible. These and similar situations will also affect gas prices due to the expansion of export opportunities and the increase in the number of end users.

-

8.

Global matters After 9/11, there were serious speculations on gas prices in the United States. Moreover, the crisis between Russia and Ukraine in 2006 was also influential on the fluctuations in NBP prices. In October 2008, the UK started to increase its LNG import due to both the global financial crisis and the decline in global natural gas demand. During this period, some important LNG procurement facilities have concurrently started to operate in Yemen, Nigeria and Qatar. Hence, the UK has had alternative options supplying significant quantities of LNG and as a result, NBP prices have declined [2].

-

9.

Futures markets In the US natural gas market, the price of this commodity is heavily influenced by the factors associated with demand or supply. Along with this, the variability and trend of Henry Hub prices are generally shaped in connection with the speculative activities in the financial markets for natural gas [2]. Henry Hub natural gas futures provide significant protection to market participants in order to manage the risk against the fluctuations in natural gas prices [31]. Thanks to derivative markets, both transaction volumes increase and market depth is formed.

-

10.

International natural gas markets Unlike the petroleum market, natural gas markets are regional, and different market dynamics in each geographical region can affect commercial activities. Therefore, pricing mechanisms may vary between markets. For example, although the UK and the US have a fully liberal market, most European countries are doing business with contracts based on long-term oil products. In addition, Asian LNG contracts are based on the price formation of oil, which is imported into Japan in the long term, known as JCC. Even though they have different geographic dynamics, possible interactions may be sometimes between those markets. For example, since the US LNG imports increased between 2006 and 2008, Henry Hub prices have started to be linked to the global liquefied natural gas market [2].

-

11.

Effect of substitution products Natural gas demand may increase due to rising prices in the fuel markets, which may be used as a replacement product on the gas supply side. For example, due to drought in the US, the production rate of hydroelectric power plants in the late 1990s has been partially reduced, and the reduction in supply has led to a 40% decline in HEPP production from 1997 to 2001. In the same period, the production of natural gas-fired power plants increased by 33% and the demand for electricity was met to a considerable extent due to the fact that such power plants could respond much more flexibly than the others [22]. In some cases, consumers who need a large amount of fuel, such as paper mills and iron-steel plants, may have a flexible structure by choosing the appropriate fuel between coal, natural gas and oil, depending on the cost of each fuel. When the cost of other fuels decreases, the decrease in the demand for natural gas can create lower prices for this input. On the other hand, when the cost of these fuels increases more than the natural gas cost, demand to natural gas can increase the prices [7].

-

12.

Official costs and fixed costs Taxation has a significant impact on natural gas prices in EU countries, which indirectly affects the growth of industrial production, electricity consumption, heating, cooling and the total cost of living in the European Region. Taxes are also accepted as one of the determining factors in the formation of natural gas prices in a spot market. Collected taxes can be added as a cost on acquisition costs, exploration costs, development costs and operating costs. In addition, VAT can be added to the final price of the natural gas controlled by the government [35]. There are also fees related to the storage and re-transmission of the gas to the network, as well as the penalty fees associated with unbalance in the system during the natural gas trade.

-

13.

Market depth The companies in the market must manage their portfolios in a strong manner. If there is an increase in the share of the companies performing inefficient operations in the total trade, this will cause the prices to rise upwards. For this reason, it is very important to have players with different characteristics in the markets, to provide transparent price formation and to include different instruments during pricing.

-

14.

Electricity prices The increase in electricity prices will encourage investors to produce more and increase their income in line with the nature of the market. At this point, the high electricity production opportunity of combined cycle power plants using natural gas as fuel increases the widespread use of this type of power plant to gain more income in the liberalized electricity markets [32]. As a natural consequence of this, the need for gas consumption will increase due to these plants.

-

15.

Electricity demand The state of electricity demand causes the issue of supply security to be on the agenda naturally. In this context, the presence of gas plants will be subject to evaluations due to the characteristics of being a base-load plant and the use of on-site production facilities such as cogeneration systems will be considered as alternative supply sources for electricity generation.

-

16.

Economic development One of the main driving forces in the natural gas markets is economic activities at both national and international levels. When the economy develops, the demand from the industrial and commercial markets causes an increase in the demand for natural gas. In this case, industrial players, which are generally the biggest consumers of natural gas that is used as a process input or as a facility fuel for many products such as fertilizers, play an important role. In addition, methanol plants and oil refineries are also important natural gas consumers, so the increase in demand for refined products may lead to increased use of natural gas. The per capita GDP increase may also lead to an increase in household demand [22]. In Oklahoma, during the global financial crisis of 2008, natural gas storage facilities have had full capacity due to low demand and this situation has become one of the main factors affecting the price variability of natural gas for that period [2]. From the perspective of economic structure, during the natural gas trade, exchange rates are very effective at the price levels and the trade volumes to be formed. For example, the exchange rate of the US dollar may cause a decrease or increase in the price of natural gas in local markets. As a result of this effect, the US dollar is known as a commodity currency [31].

-

17.

Technological developments In all the latest technological developments in the liquefied natural gas value chain, some analyses show that the floating LNG (FLNG), a vessel capable of processing and liquefying natural gas on board, is a technology that can have influence in the sector completely. Moreover, this technology may have an important role in transportation against conventional liquefaction operations performed on land. This potential alternative will give the advantage of less construction time, more controlled use of environment and the ability to put the inaccessible resources into economies as a part of trade. On the other hand, high operating and maintenance costs, extreme weather conditions that may affect production.

-

18.

Geographical conditions This factor includes some important issues such as, appropriate storage areas, complexity of transmission routes, and availability of ports.

With all these factors, there is not a single factor that has a dominant role in pricing formation in the natural gas markets. Hence, uncertainties in future strategies are fundamentally decisive for all natural gas forecast analyses and significantly affect international business activities [21]. All these factors are grouped in Fig. 12 by creating 5 main factor classes according to their characteristics.

Factors on natural gas prices

3 Natural gas markets in Turkey

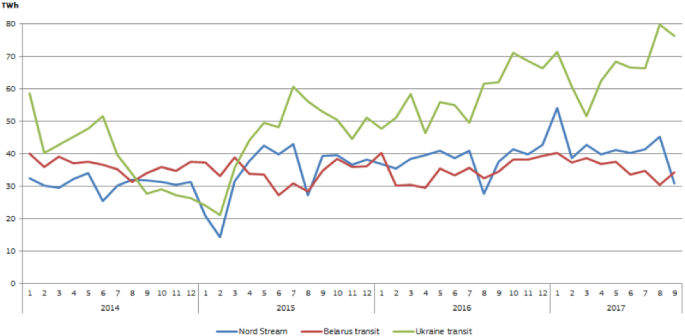

Since its share in electricity generation is 37.2% in 2017 [8], natural gas plants are at an important point in Turkey’s electricity supply security. Turkey was able to produce only 0.7% of its 54 billion Sm3 gas consumption in the same year [9]. In other words, since 2005, Turkey almost entirely depends on imports, especially due to the increased natural gas demand in residential, industrial and private combined cycle gas turbines. Moreover, the rate of dependency to foreign countries is around 76% in terms of all energy sources [25]. In Fig. 13, the monthly natural gas sector reports of the EMRA have been compiled for gas import amount of Turkey.

Natural gas imports and supply amount between 2012 and 2017 (EMRA 2012–2017)

As supply safety concerns are on the agenda, new regulations about the development of natural gas hub in the free market and cost-based pricing system have been made since 2009. Hence, the fact that the Natural Gas Market Law was published in 2001 was an important step towards the goal [19].

3.1 Players and trading system in natural gas market

As of the end of 2017, Turkey has 4 International active pipelines with a total technical capacity of 52.9 billion Sm3 per year, which can import natural gas from Azerbaijan, Iran and Russia [28]. Through these lines, gas supplies are provided with long-term contracts indexed to oil and petroleum products. LNG trade is also carried out from Nigeria and Algeria with the same pricing mechanism. In addition, imports from the spot market are also carried out to meet demand. Gas supply with such contracts is provided by BOTAŞ, the institution responsible for meeting the country’s gas demand, and by 7 private companies holding import licenses. Additionally, gas supply in the spot market is provided by the participation of 43 licensed companies [9].

In Rzayeva’s report, gas supply agreements of BOTAŞ and other potential suppliers that Turkey can import are shown in Table 1 [28].

Approximately 50% of the natural gas production in Turkey is mainly carried out by the public Petroleum Company Turkey Petroleum Corporation (TPAO) in the Black Sea coastal regions. The rest is provided by Corporate Resources B.V., Thrace Basin Natural Gas Corporation, and 7 other companies [9]. Besides the existing production levels, potential shale gas reserves of Turkey are shown in Fig. 14 [26].

Regions with potential shale gas reserves in Turkey [26]

In liberalized natural gas markets, all natural gas market operations must be separated. Therefore, a legal actor involved in wholesale natural gas trade transactions should not take part in distribution or transmission activities. Transmission companies should not perform any other activities and distribution companies cannot also perform other activities, but they may take action in retail sales. For all these activities, all natural gas market participants require a license according to the Natural Gas Market Law [19].

There are a large number of private importers and wholesale companies; however, their market shares are very little against the public company BOTAŞ. The company imports almost 80% of all natural gas consumed in Turkey and also carries out its transportation, transmission, trade and wholesale activities as well as investing in a new natural gas storage facility. Moreover, the company is the owner and operator of two LNG facilities. Share of import operations of BOTAŞ has always been continued by the government strategies in line with a policy supplying natural gas to Turkey for a national interest [19].

Operations at the LNG terminal are regulated by a natural gas storage license. The law also aims to regulate third-party access to storage facilities and LNG. On the other hand, due to the lack of competition in this market segment, tariffs are determined by EMRA. Furthermore, the third party agreement to the regulated LNG and storage facilities has not been fully implemented [19]. According to the assessment in 2015, Turkey’s storage capacity is behind most European countries, as shown in Fig. 15 [26]. In order to build natural gas storage facilities, underground facilities with appropriate physical structure are needed. Therefore, Turkey continues its investment efforts to increase the percentage of natural gas storage per total consumption to higher levels.

Percentage of natural gas storage in Europe according to total consumption in 2015 [26]

In 2005, BOTAŞ started contract negotiations with Gazprom to transfer its rights to private companies. The negotiations were resulted in the transfer of 4 billion Sm3 natural gas per year to private importers, which will be terminated in 2022 within the framework of the natural gas sales and purchase agreement. BOTAŞ has transferred its rights to Bosphorus Gaz, Enerco Energy, Shell Energy and Eurasian Gas for the gas coming from the West Line in 2009.

In addition, Gazprom and BOTAŞ concluded the natural gas sales and purchase contract for the delivery of 6 billion Sm3 natural gas annually through the West Line from Russia at the end of 2011. Hence, this situation allowed the transfer of 6 billion Sm3 natural gas per year to private sector companies. In 2013, four private gas companies—Kibar Energy, Akfel Energy, Bosphorus Gas, Batı Hattı—started to import this amount through the Western Line from Russia. Currently, in addition to BOTAŞ, 7 private companies are bringing 10 billion Sm3 natural gas annually to Turkey via the western pipeline.

3.2 BOTAŞ and price formation

State-owned BOTAŞ was established in 1974 as a TPAO (Turkish Petroleum Corporation) subsidiary to manage Iraqi crude oil transportation through the pipelines between Kirkuk and Yumurtalik. The main responsible party of the natural gas market was also BOTAŞ. In 1987, duties and responsibilities of BOTAŞ were expanded. Today, the duties and responsibilities of BOTAŞ include the following areas: Transportation of natural gas through pipelines, construction and maintenance of natural gas pipelines, import and export of natural gas, natural gas trade, gas distribution, storage, exploration-drilling and natural gas production activities [5]. The prices of gas imported through oil indexed long-term contracts may be very sensitive due to the fluctuations in exchange rates between Turkish lira and US dollar. For the price of gas offered to the domestic market, BOTAŞ had implemented the cost-based pricing system in which monthly gas prices must be updated according to import prices, USD/TL parity and other variables until 2008, but then BOTAŞ started to determine the wholesale prices in a subsidized way for distribution companies, eligible consumers and gas-powered power plants [5].

In addition to focusing on daily oil prices, other parameters affecting gas prices should be considered in order to better understand the structure of imported gas prices. Although the details of import contracts are not disclosed to the public, it is generally known that gas import contracts have a formula such as the approach in Eq. (1) to evaluate the gas price of 3 months. The formula takes the average of 6-month oil price as the main parameter 1 month before the start of the 3-month delivery. The domestic prices are published every year in January, April, July and October.

3.3 Privatization and natural gas hub requirement

Energy need plays an important role in today’s commercial relations. There are very critical strategic advantages for Turkey provided by its geopolitical position. Considering the demand projection of Europe, which appears to be the closest market to Turkey, it is very important to transport gas from supply resources to these regions. Considering Europe’s need for Russia, and looking at Fig. 6, it is clear that Europe may need important measures on supply security.

Ukrainian line is the largest line supplied from Russia for Europe. It is very significant that Russia can securely transmit the gas on this line to Europe in terms of both the country’s income guarantee and the supply security of the importing countries. For these reasons, especially in order to avoid the shadow of Russia’s problems with Ukraine, Turkish-Russian cooperation, which has been increasing rapidly in recent years, has created an alternative route on the road to Europe for Russia. The cancellation of the South Stream project by Russia and the launch of the Turkish Stream project in 2014 were one of the main turning points for Turkey to become an important player in the global gas market [4]. In addition, in terms of Turkey’s interest, the exclusion of transit countries on the transmission route increases supply security by making direct gas flow possible between Turkey and Russia [28]. This development also supports Ankara’s strategy to increase its political weight with the help of its geopolitical position. Moreover, Europe’s dependence on Russia encourages it to find an alternative. In order to increase resource diversification in the region, the TANAP (Trans Anatolian Natural Gas Line) and its continuation TAP (Trans Adriatic Pipeline) have recently started to have a significant place in the strategic sense [26].

Turkey will have the opportunity to trade more excess gas to Europe due to the expanding variety of resources and the ability to make hub pricing for natural gas passing through its territory with pipelines and LNG. For example, both TANAP and Turk Stream pipelines are transit pipelines, which will carry 16 and 31.5 billion Sm3/year gas from Azerbaijan and Russia respectively, and will provide gas to the foreign markets with 10 and 14.75 billion Sm3/year capacity [28]. Besides, Iraq and the Eastern Mediterranean region stand as two potential natural gas sources, but the fact that they both have political, geopolitical and economic difficulties puts them on hold in the short term. Iraq has always been seen as a strong option for new supply to Turkey. However, the biggest obstacle is the political turmoil and security issues of the region; so that, there will be no gas imports to Turkey through regional administration in the short and even medium term [28]. These major projects and such other strategic projects strengthen Turkey’s regional position and importance.

Turkey’s existing and potential suppliers, LNG terminals and storage facilities are shown in Fig. 16.

Natural gas supply network of Turkey

In the current system, the gas purchase price of all imports except LNG supplied from the spot market has been formulated by being indexed to oil and oil products through long-term contracts. Due to the low domestic production of Turkey, these contracts are vital in today’s conditions. Despite this situation, Turkey’s desire to be a regional gas hub that it has adopted and targeted may have the power to change this picture in addition to the existing contracts, new resources and the steps that the country will take in terms of infrastructure and storage capacity. Turkey’s geopolitical position is likely to secure to become a natural gas trade hub with the right to export the excess gas to be supplied. In this way, the price of the gas that will be created in its commercial hub according to supply and demand will also be strong in terms of purchase prices for international trade operations and Turkey will not have to enter into a variety of obligations under long-term contracts based on oil products.

With the natural gas potential in the Eastern Mediterranean, nearly 10 billion Sm3/year natural gas supply will be possible for Turkey. Although there are some financial issues related to this alternative source, from Turkey’s point of view, it will be fully compatible with the interest of the country for diversification of supply resources. Gas transportation from the Eastern Mediterranean to Europe through Greece and Italy would be more costly due to the longer distance. This makes the realization of this project unlikely for the time being. Hence, the most appropriate investment decision to transport the regional natural gas for the countries such as Israel and Egypt will be via Turkey [28]. The local investments that Turkey continues to make towards improvement for infrastructure, storage facilities and LNG capacity will also improve the usage area of the gas. As Turkey will have very diversified gas supply network, local and global market players will be easily able to meet in Turkish natural gas trade hub, so market clearing price for gas can be determined successfully in a transparent way. As a result, exporting gas back to neighboring European countries and the others may also place Turkey at the center of regional and geopolitical energy network of the Eastern Mediterranean [28].

Turkey tries to meet the country’s natural gas demand by making long-term purchases under contracts based on oil and petroleum products since the day it started to import gas. Gas production, which is very low in volume over time, and LNG, which is supplied from the spot market, are also targeted to contribute to the variety of supply. Fluctuations in oil prices also create price uncertainty for gas importing countries under these contracts and prevent the determination of the transparent value of the gas. With the expiry of Turkey’s long-term contracts in 2020s, BOTAŞ and other private import companies are expected to be in a position to negotiate better terms, including the pricing of the rich natural gas of the region surrounding Turkey, the conditions of take or pay, and other clauses [28]. In order to achieve the maximum benefit of this situation, Turkey must make serious investments in the expansion of gas infrastructure to be an important natural gas exporter in the coming years. Moreover, the greatest opportunity will be to become a new gas trade hub strategically and economically. In Fig. 16, when the supply structure of the desired gas trade hub is examined through the Turkish map, it is understood that Turkey will have a virtual gas trade hub (“virtual gas hub”) due to the gas inflows provided from various suppliers.

In this context, daily gas amount that can be supplied to Turkey in accordance with the existing agreements are shown in Table 2 in million cubic meters.

If the pricing of natural gas coming to Turkey continues based on long-term oil-indexed contracts, it will be difficult to develop an active and deep natural gas trade hub. In order to create a reliable price index for the commercial center strategy, spot natural gas is required to be in sufficient amount. In the case of a trade center, suppliers will be able to take advantage of prices in the free market instead of oil-indexed pricing in their long-term contracts. Hence, it is important to ensure energy supply security in order to establish a well-functioning pricing system. An energy trading market with the right price axis will contribute positively to the Turkey’s increasing trade volume and provide more opportunities for investments into medium-long-term energy projects.

4 Conclusion

In this study, the formation structures of natural gas prices were reviewed with the focus of hub formation. The paper analyzed the existing natural gas markets in the Globe, and presented information about pricing mechanisms. The insight about the increasing importance of gas markets and increasing natural gas prices are given. It has been emphasized that the classical pricing method of oil price based long term contracts are accompanied with the spot-markets and future markets. A new pricing method through the regional hub formation, seen mainly in Europe are presented with detailed descriptions.

Turkey is a globally accepted energy route since it has a very important geopolitical position in terms of energy resources and trading. Turkey has a growing demand of energy with fast developing economic structure. Despite the conflict of regional risks and richnesses of energy resources Turkey is giving a high effort for energy security in parallel with European energy security by using the natural gas. These three facts construct a great opportunity for Turkey to become an important hub, meeting point of natural gas supply and demand. The importance is shown by analyzing the existing Turkish Natural Gas Market through a variety of market players. Moreover, Turkey’s current gas imports and production resources were analyzed and new projects announced by the state target are examined. Within the scope of these projects, the contributions of FSRUs, gas storage facilities and pipeline projects (especially TANAP and Turk Stream projects) are detailed. The results of prescriptive and predictive analysis of constructing a Natural Gas hub in Turkey are shown. It is clearly observed that Turkey has to support the renewable resources with the natural gas imported but the contract and pricing have to be redefined. It is crystal clear that a reliable and active market cannot be formed by using the long term oil price based contracts. Just on the contrary, a new hub formation and allow the price construction through the market realities is a recommended policy.

This study will be continued by applying the predictive and prescriptive analytics of Turkey becoming a Global Natural Gas Hub. There is a need for further study on the dynamic pricing structures that will precise the future scenarios for using Natural Gas to respond the increasing power demand.

References

Accenture: Development of the Turkish natural gas exchange market. Petform (2013)

Alterman, S.: Natural gas price volatility in the UK and North America (Report No. 60). Oxford Institute for Energy Studies (OIES), Oxford (2012)

Avalos, R., Fitzgerald, T., Rucker, R.: Measuring the effects of natural gas pipeline constraints on regional pricing and market integration. Energy Econ. 60, 217–231 (2016). https://doi.org/10.1016/j.eneco.2016.09.017

Berk, I., Schulte, S.: Turkey’s role in natural gas—becoming a transit country? (Report No. 17/01). EWI, Cologne (2017)

Beyazgul, D.: Liberalisation of the Turkish natural gas market. Dissertation, Politechnico Di Milano, Dipartimento di Ingegneria Gestionale, Milano (2016)

Bourgeois, A.: Gas prices: models and trends [PowerPoint Presentation]. Bergen Energi (2011)

EIA: Natural gas factors affecting prices. https://www.eia.gov/energyexplained/index.cfm?page=natural_gas_factors_affecting_prices (2017). Accessed 21 Apr 2018

EMRA: Electricity power market sector report—December 2017 (2017a)

EMRA: Natural Gas Market Sector Report—December 2017 (2017b)

Energy Charter Secretariat: International pricing mechanisms for oil and gas. Energy Charter Secreteriat, Brussels (2007)

EU Commission: Quarterly report on natural gas markets (Report No. 10). EU Commission, Brussel (2017)

European Federation of Energy Traders: European gas hub study. https://efet.org/energy-markets/gas-market/european-gas-hub-study/ (2017). Accessed 29 Apr 2018

Foss, M.: The Outlook for US Gas Prices in 2020: Henry Hub at $3 or $10? (Report No. 58). OIES (2011)

Gazprom Export: Transportation. Gasprom. http://www.gazpromexport.ru/en/projects/transportation/ (2018). Accessed 21 Apr 2018

Geng, J., Ji, Q., Fan, Y.: A dynamic analysis on global natural gas trade network. Appl. Energy 132, 23–33 (2014)

Guerra, A., Shen, A., Zhao, T.: Determinants of natural gas spot prices. http://faculty.babson.edu/goldstein/Teaching/FIN3560Fall2012/2012%20group%20projects/Natural%20Gas/Group%20Project_FIN3560-01_Natural%20Gas.pdf (2012). Accessed 20 Apr 2018

IEA: Gas pricing and regulation—China’s Challenges and IEA Experience (2012)

IEA: Developing a natural gas trading hub in Asia (2013)

IEA: Energy Policies of IEA Countries—Turkey Review (2016)

IGU: Wholesale gas price survey—a global review of price formation mechanisms (2017)

Leidos: Global Natural Gas Markets Overview. EIA (2014)

Mastrangelo, E.: An analysis of price volatility in natural gas markets. EIA (2020)

Melling, A.: Natural gas pricing and its future—Europe as the bottleground. Carnegie Endowment for International Peace, Washington (2010)

Özdemir, V.: Natural gas market: spot market ot long-term contracts? (Report No. 13). EPPEN (2015)

Özden, A., Haçikoğlu, M.: Energy sector. A&T Bank Sector Report, Istanbul (2018)

Öztürk, A.: Natural gas sector report. Isbank, Istanbul (2017)

Prognos: Current status and perspectives of the European gas balance. https://www.prognos.com/en/publications/publications/690/show/6cc1f00f48b3cbfb40b3e384c9166b42/ (2017). Accessed 18 Apr 2018

Rzayeva, G.: Gas Supply Changes in Turkey (Rapor No. 24). OIES, Oxford (2018)

Slaba, M., Gapko, P., Klimesova, A.: Main drivers of natural gas prices in the Czech Republic after the market liberasation. Energy Policy 52, 199–212 (2013). https://doi.org/10.1016/j.enpol.2012.08.046

Stern, J., Rogers, H.: The dynamics of a liberalised European gas market (Report No. 94). OIES, Oxford (2014)

Swissquote: Natural Gas—Fact Sheet. https://en.swissquote.com/fx/files/swissquote.com.fx/SQB-FactSheet_NaturalGas-EN.pdf (2015). Accessed 04 Apr 2018

Şanlı, B.: Will renewable energy determine natural gas prices? Energy Panorama 5, 51–57 (2017)

Timera Energy: The Achilles heel of foreign exchange management. https://www.timera-energy.com/bleeding-value-from-residual-foreign-exchange-risk/ (2011). Accessed 21 Apr 2018

TPAO: Crued oil and natural gas sector report for 2016 (2017)

Yorucu, V., Bahramian, P.: Price modelling of natural gas for the EU-12 countries: evidence from panel cointegration. J. Nat. Gas Sci. Eng. 24, 464–472 (2015). https://doi.org/10.1016/j.jngse.2015.04.006

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

About this article

Cite this article

Nalbant, H., Kayalica, M.Ö., Kayakutlu, G. et al. An analysis of the natural gas pricing in natural gas hubs: an evaluation for Turkey. Energy Syst (2020). https://doi.org/10.1007/s12667-020-00395-8

Received:

Accepted:

Published:

DOI: https://doi.org/10.1007/s12667-020-00395-8