Abstract

Energy efficiency accounting systems (EEAS) have been widely used to track progress in economy-wide energy efficiency. In the literature, there is general agreement on the approach for handling energy consumption in end-use sectors. However, this is not the case for the energy sector which captures losses arising from energy transformation, transmission and distribution. The energy sector constitutes between 25 and 40% of total primary consumption in most countries. How it is handled in an EEAS greatly affects quantification of progress in economy-wide energy efficiency and its accompanying policy implications. This study systematically compares the various approaches used to incorporate energy losses from the power sector in an EEAS and discusses interpretation and implications of the results in the context of different energy systems. A new approach, which quantifies the contribution of changes in the share of renewable energy and separates transmission and distribution losses in the power sector, is recommended and illustrated through a case study of Canada. The approach can also accommodate energy systems with electricity trade. Extensions from an EEAS to an energy-related emissions accounting system (EMAS) are also presented in light of the increasing interest in emissions accounting and climate mitigation.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

Energy efficiency is one of the key solutions to the energy trilemma. It allows for the simultaneous improvement of energy security, economic competitiveness and environmental sustainability. To this end, national and international agencies have sought to implement policies to encourage greater energy efficiency. The tracking of progress in energy efficiency improvements has become one aspect of the policymaking process that provides information on historical trends and facilitates policy evaluation.

There are several ways to track progress in energy efficiency at the economy-wide level. The simplest is to use the ratio of primary energy consumption to gross domestic product (GDP). This performance indicator has been widely applied nationally and internationally. For example, it is tracked by IEA (2017c) and used as a target by the Asia-Pacific Economic Cooperation (2011) and is often tabulated in national statistical yearbooks. The ratio is commonly used as a proxy for energy efficiency, but for such an application, it is overly general as it includes factors which are not directly linked to energy efficiency. Sectoral energy intensities, which are ratios of the energy consumed in an energy-consuming sector such as industry or passenger transport to the service provided, can also be used. Different services can be considered for different energy-consuming sectors or sub-sectors to provide the best results for specific applications, but aggregation to form an economy-wide indicator in a systematic manner is often difficult.

More sophisticated approaches such as the development of an energy efficiency accounting system (EEAS) system have been proposed. The EEAS is a consistent bottom-up framework that allows analysts to study energy efficiency at the sector level and aggregate the results at the economy-wide level. The design of an EEAS is often linked to index decomposition analysis (IDA) in the energy literature.Footnote 1 IDA provides the underlying framework from which a composite energy efficiency indicator may be constructed based on disaggregated sectoral energy and activity data (Ang et al. 2010). This composite energy efficiency indicator is seen as a better representation of economy-wide energy efficiency as effects unrelated to energy efficiency are not amalgamated in the indicator (Ang 2006; Ang and Goh 2018). Using this technique, energy savings from energy efficiency improvements can also be estimated.

Over the years, an increasing number of national and international agencies have developed EEAS on the basis of IDA. Examples include Australia (Petchey 2010), Canada (Office of Energy Efficiency 2016), New Zealand (Lermit and Jollands 2001), the USA (Belzer et al. 2017) and the European Union (European Commission 2017). Such studies which reveal economy-wide and sectoral energy efficiency trends allow governments to understand the impact of energy efficiency policies and underlying trends in energy consumption. Studies on national accounting systems have also been reported in academic journals for a number of countries (Bashmakov and Myshak 2014; Colinet and Román 2016; Kerimray et al. 2017; Torrie et al. 2018).

The design considerations of an EEAS have been looked into in studies such as Ang et al. (2010) and Goh and Ang (2018). In the literature, there is general agreement on the IDA approach for quantifying the energy efficiency improvements of energy end-use sectors. However, there is a lack of consensus on the approach that should be applied for the energy sector, i.e. energy transformation, and transmission and distribution (T&D).Footnote 2 For this sector, different approaches have been used or it is simply ignored. The energy sector contributes to about a third of total global primary energy consumption and in most countries the share varies between 25 and 40% (IEA 2017d). Changes in the energy losses and efficiency of the sector can therefore have a significant impact on total primary energy consumption and economy-wide energy efficiency. Furthermore, the rapid adoption of renewables and increase in cross-border electricity trade lead to further complications in treatment and decomposition analysis of the energy sector.

This study seeks to analyse the different approaches and examine the methodological issues surrounding the inclusion of the energy sector in an EEAS. This is an area that has not been adequately addressed in the literature. In the next section, the conventional EEAS framework and IDA methodology are presented. A systematic analysis of the various approaches that have been used to incorporate the energy sector in an EEAS is then presented. The pros and cons of each approach are analysed and issues concerning the inclusion of renewables are also considered. Based on the findings, a new approach is proposed and a case study using Canada’s data is presented to illustrate how a comprehensive EEAS can be developed. Finally, in light of the growing interest in climate mitigation, the extension of the EEAS to an energy-related emissions accounting system (EMAS) and the related methodological issues are discussed. The same case study of Canada is used to construct an EMAS to decompose the changes in economy-wide energy-related CO2 emissions.

Tracking energy efficiency trends using EEAS

In simple terms, an EEAS is an accounting system for the tracking of energy efficiency trends at the sectoral and economy-wide levels. In most EEAS, an analytical framework based on IDA is used to decompose a change in energy consumption into effects associated with various driving factors (Ang et al. 2010; Goh and Ang 2018). This is conducted at the sectoral level and the results obtained are aggregated to give the economy-wide level performance. In an EEAS that covers the total primary energy consumption (TPEC) in a country, TPEC can be divided into six sectors, i.e. five end-use sectors (industry, services, freight transport, passenger transport and residential) and the energy sector. The energy consumption in sector i, Ei, is expressed in terms of an IDA identity. In the decomposition analysis, the following three-factor identity is the most basic form:

where Qi is the activity which drives energy consumption of sector i and Eij, Qij, \( {S}_{ij}=\frac{Q_{ij}}{Q_i} \) and \( {I}_{ij}=\frac{E_{ij}}{Q_{ij}} \) are respectively the energy consumption, activity, activity share and energy intensity of sub-sector j in sector i.Footnote 3

Assume that the energy consumption in sector i in year 0 and year T are respectively \( {E}_i^0 \) and \( {E}_i^T \), and the change in total energy consumption between the 2 years is \( {\Delta E}_{\mathrm{tot},i}={E}_i^T-{E}_i^0 \). Based on Eq. (1), this change can be decomposed into an activity effect, a structure effect and an intensity effect:

With the decomposition conducted for all sectors, the measure at the economy-wide level is obtained by summing the individual changes at the sectoral level, e.g. ∆Etot = ∑i∆Ei, tot and ∆Eint = ∑i∆Ei, int are respectively the change in primary energy consumption and the energy intensity effect at the economy-wide level. The energy intensity effects ∆Eint, i and ∆Eint are often used as a proxy to estimate improvements in energy efficiency at the respective level. A negative intensity effect represents energy savings from energy efficiency improvements.

Since decomposition is performed at the sector level, the activity of each sector can be defined individually. For instance, physical activity such as passenger-kilometres travelled can be used for passenger transportation while monetary activity such as value-added can be used for the industry sector. Physical activity indicators are generally preferred as the corresponding intensities are seen as better measures of energy efficiency. (See IEA (2014) for details on the physical activity indicators and Goh and Ang (2018) for the commonly used activity indicators for each sector.) Depending on the activity selected for each sector, the structure effect can have different meanings. For example, if value-added is the activity, the structure effect represents the impact of changes in economic structure on energy consumption. On the other hand, for the transport sector, if passenger-kilometre or tonne-kilometre is used, the structure effect represents the impact of transport modal shifts. For the residential sector, floor area is a common activity indicator and the corresponding structure effect represents the impact of shifts in the total dwelling area by type of dwelling.

Different IDA methods can be applied to compute the individual effects as shown on the right-hand side of Eq. (2). Based on the equation, decomposition is conducted additively where an arithmetic change in energy consumption is decomposed. In this study, one of the most popular IDA methods, the additive LMDI-I method, is used. The detailed formulae are shown in the Appendix. Decomposition can also be conducted using the multiplicative approach based on a ratio change in energy consumption. The results are then given in indexes from which sectoral and economy-wide energy intensity indexes may be constructed to show energy efficiency trends (Ang et al. 2010; Ang 2015).Footnote 4 If time series data is available, one can choose between chaining and non-chaining decomposition analyses. In chaining analysis, decomposition is conducted based on data from consecutive years over a certain time period and the annual results are chained together. In non-chaining analysis, decomposition is conducted based only on the data for the first year and the final year of the time period without making use of the data for the intervening years. Non-chaining analysis is adopted in this study for simplicity. Further details about the tracking of economy-wide energy efficiency trends using EEAS and the LMDI approach can be found in Goh and Ang (2018).

Overview of existing approaches

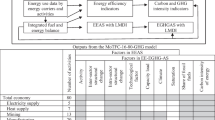

Changes in final energy consumption of the five end-use sectors are generally decomposed via Eqs. (1) and (2). Empirical results of various studies using such an approach have been widely reported, e.g. Bashmakov and Myshak (2014), Office of Energy Efficiency (2016) and Petchey (2010). In contrast, for the energy sector, in addition to the approach as defined by the two equations, there are several other ways to account for energy losses and to perform a decomposition analysis. From the literature, the differences among the various approaches can be discussed in terms of the IDA identity used and the treatment of renewables, nuclear energy and T&D losses. They are presented in the sections that follow. In this study, for simplicity, the energy sector is taken as the electricity sector as losses from electricity generation, transmission and distribution are the main sources of losses for this sector. Losses from heat generation and other energy transformations where there is a single output (e.g. heat or gas)Footnote 5 can be handled in the same way as that for the electricity sector by considering each output as a separate sector and applying the same identity for the electricity sector to each type of output.

IDA identity

As an extension of Eq. (1), a list of IDA identities that can be used in an EEAS are summarised in Table 1. Some countries/studies focus only on end-use energy efficiency and the EEAS comprises five sectors, e.g. Australia (Petchey 2010), New Zealand (Lermit and Jollands 2001) and Canada (Office of Energy Efficiency 2016). The identity shown in Eq. (1), which is named Identity A in Table 1, is applied to the five end-use sectors individually. This approach is reasonable if the study’s focus is on final energy consumption (TFEC). However, it is inadequate if the focus is on TPEC since the aggregate energy intensity effect, ∆Eint, obtained is not representative of changes in economy-wide energy efficiency.

To account for energy losses from electricity generation, transmission and distribution, the energy sector can be included as the sixth sector and the decomposition can be similarly performed via Identity A. The resulting EEAS is the conventional approach described in the “Tracking energy efficiency trends using EEAS” section. The EEAS of Russia in Bashmakov and Myshak (2014), Canada in Office of Energy Efficiency (2006)Footnote 6 and European Union Member states in Reuter et al. (2017)Footnote 7 are based on this approach. In this approach, the activity of the energy sector, Qij, is the electricity produced by each energy source j measured in kilowatt hour. \( \frac{Q_{ij}}{Q_i} \) is the share of energy source j in the total electricity output and the corresponding structure effect measures the contribution of changes in the energy mix to the total change in energy losses. The ratio \( \frac{E_{ij}}{Q_{ij}} \) is the loss intensity which is a measure of the ratio of energy losses from transformation and distribution to the electricity output from energy source j. The corresponding loss intensity effect is added to the sum of the intensity effects of end-use sectors to obtain the economy-wide energy savings from energy efficiency improvements.Footnote 8

If one wishes to decompose changes in the TPEC and yet retain only the five end-use sectors, a logical approach is to transform Identity A into Identity B shown in Table 1. In Identity B, energy losses from the energy sector are distributed proportionally to end-use sectors based on the electricity consumed by each sector. The three-factor decomposition remains largely the same. The only difference is that the energy consumed by each end-use sub-sector (Eij) in Identity A is replaced by the source energy (\( {E}_{ij}^s \)), which is the sum of the final energy consumed and the losses from the energy sector, in Identity B.Footnote 9 The corresponding intensity will be \( \frac{E_{ij}^s}{Q_{ij}} \). The intensity effect is influenced by a combination of changes in end-use energy intensity and changes in the energy losses of the energy sector. This amalgamation of factors prevents analysts from quantifying changes in end-use energy efficiency separately. Fuel switching and changes in generation efficiency can influence losses from the energy sector and result in changes in the intensity of an end-use sector even though there may be no changes to the end-use energy efficiency of that sector.

Identity C in Table 1 overcomes the problem arising from the use of Identity B through the inclusion of a delivered energy mix effect and a source-to-site ratio (SSR) effect in the IDA identity. It is used in the study of the USA in Belzer et al. (2017). The delivered energy mix, Hijk, measures the share of electricity in the delivered energy mix. Subscript k is set to 1 when there is direct fuel consumption and to 2 when electricity is used. SSRijk is the ratio of the energy input into electricity production to the final electricity delivered to the end user. As the SSR of electricity is only dependent on the energy sector, it is the same for all end-use sectors in a single year. It is influenced by factors such as power generation efficiency, electricity mix and T&D losses. Since the energy sector is considered under the SSR effect, the economy-wide energy savings derived based on Identity C comprise of the intensity effects of end-use sectors and do not include the intensity effect of the energy sector.Footnote 10

For the purposes of tracking progress in energy efficiency, Identities A and C are preferred as end-use energy efficiency is clearly quantified. Trends in each end-use sector can be analysed and the impact of policies targeting each end-use sector can be evaluated. With regards to the inclusion of the energy sector, the choice between Identity A and Identity C depends on the study objective. Identity A provides more details on the energy sector while Identity C provides more details on end-use energy consumption. In Identity A, energy losses from the energy sector are decomposed into three factors corresponding to changes in electricity demand, electricity mix and loss intensity. On the other hand, Identity C quantifies the switching of end-uses to electricity, a factor that cannot be quantified by Identity A. However, a drawback of Identity C is that changes in the energy sector are quantified by only one factor, i.e. the SSR effect. Additionally, as the identity requires the redistribution of energy losses to end-use sectors, electricity trade cannot be considered within the EEAS. Identity C is also more complex, with more factors, an extra level of disaggregation and the need to redistribute energy losses to each end-use sub-sector. In contrast, the data required for Identity A is largely consistent with the structure of a national energy balance and can be easily obtained. In summary, unless the switching of end-uses to electricity is of interest, Identity A is recommended for the development of a complete EEAS which includes the energy sector.

Treatment of renewables, nuclear energy and T&D losses

The growth in the use of renewable energy sources has made the energy sector more complex and diverse in recent years. The ways renewables and nuclear energy are treated can greatly affect the estimated economy-wide intensity effect. Historically, most electricity generation systems depend primarily on fossil fuels. As renewable energy and nuclear power entered the electricity mix later than fossil fuels, their primary energy equivalent values in an energy balance have often been computed based on the average efficiencies of fossil fuels. This method, known as the partial substitution method (IEA 2018), gives the amount of fuel input displaced by a shift to non-fossil-based energy sources in an energy balance. It is used by BP (2017) to estimate the primary energy equivalent of renewables and nuclear energy and the USA to compute the primary energy equivalent of renewables (Belzer 2014).Footnote 11

The high share of renewables in some countries, however, has reduced the relevance of the partial substitution method which sees fossil fuels as the incumbent. Instead, some organisations have adopted the physical energy content method (IEA 2018; Natural Resources Canada 2016b). In this method, the physical energy content of the energy source is its primary energy equivalent. For example, as electricity is the primary energy form of most renewablesFootnote 12, their efficiency is assumed to be 100%. On the other hand, the primary energy form for nuclear energy is heat. The subsequent transformation of heat to electricity results in energy losses. Belzer (2014) uses the actual thermal conversion factors for nuclear plants. IEA (2018) and the European Union (Eurostat 2018) assume an efficiency of 33% while Canada (Natural Resources Canada 2016b) assumes an efficiency of 31.1% for nuclear plants.

In many cases, the assumptions that have been used for energy balances have been applied to an EEAS. This is logical given that the energy consumption data of the EEAS is usually obtained from national energy balances. However, these assumptions can distort the decomposition results across IDA identities. The distortion is particularly pronounced for Identity A as more factors in the energy sector are studied and differences in the assumptions on efficiency have an impact on the aggregate economy-wide intensity effect.Footnote 13 A summary of the distortions and corresponding decomposition formulae for Identity A based on additive LMDI-I is shown in Table 2. In Identity A, the energy losses from the energy sector are defined as losses from electricity generation and T&D lossesFootnote 14, which are redistributed to each energy source based on the proportion of electricity output from that energy source. This means that the T&D loss fraction, defined as TT and T0 for the target year T and reference year 0Footnote 15, is multiplied by the electricity output of a particular energy source (i.e. Qij, T and Qij, 0) and added to the transformation losses. When the average thermal efficiency of fossil plants are used to represent the efficiency of renewables and nuclear energy as shown in case 1, the structure and intensity effects are misrepresented. In particular, the intensity effect for non-fossil-based energy sources does not have any relation to the efficiency of renewables or nuclear energy. Instead, it is primarily influenced by the changes in the average thermal efficiency of fossil plants which are defined as ηT and η0 in the target year T and reference year 0 in Table 2.

The physical energy content method is more appropriate as renewables and nuclear energy are not arbitrarily assigned a hypothetical efficiency based on their fossil fuel counterparts. In cases 2a and 2b, constant efficiencies of 33% for nuclear energy and 100% for renewables are used. For nuclear energy, 33% represents the average thermal efficiency of nuclear plants (IEA 2018). The IDA formulae in Table 2 show that in both cases, the intensity effect is determined by changes in the T&D loss fraction. This result is difficult to explain as policies targeting renewables or nuclear energy do not have any leverage over the T&D loss fraction but changes in the fraction represent the entire loss intensity of non-fossil-based energy sources. Furthermore, the weights assigned to each energy source are also influenced by the T&D loss fraction. For renewables, the energy losses, which determine the weights, are equivalent to the T&D losses. To tackle these problems, T&D losses can be considered separately and independently of the decomposition for the energy sector as shown in the IDA formulae in cases 3a and 3b in Table 2. The results are reasonable for nuclear energy—the structure effect measures the contribution of changes in the share of nuclear energy in the electricity mix while the intensity effect is zero. However, no weights can be assigned to renewables as there are no energy losses associated with electricity generation.Footnote 16 This means that changes in the share of renewables in the electricity mix cannot be quantified. Changes in the share of renewables will become more important as countries around the world increase the use of renewables to meet climate change and energy security concerns. Hence, the quantification of their contribution in an EEAS is important and should be studied in more detail.

An improved EEAS

From the foregoing, there are a number of problems in the development of a comprehensive national EEAS and the main issue relates to how to handle the energy sector. It has been recommended that the energy sector is taken as the sixth sector but with that the basic three-factor identity is unable to adequately account for renewables and T&D losses. A new approach is therefore needed and it is presented in this section.

Recommended approach

In the recommended approach, the identity for the end-use sectors remains the same as in Eq. (1) and a new identity is proposed for the energy sector to address the issues raised in the “Treatment of renewables, nuclear energy and T&D losses” section. An additional factor, \( {P}_i=\frac{Q_i}{G_i} \) , which measures the share of non-renewable electricity in the electricity mix, is included in Identity A for the energy sector to give Identity A1 below:

where Gi is the total electricity output, Qi is the total electricity output from fossil fuels and nuclear energy and Qij and Eij are the electricity output and energy losses from electricity production from fossil fuel or nuclear energy j respectively.Footnote 17 The energy losses for non-fossil energy sources are computed based on the physical energy content method. The change in energy consumption of the energy sector from year 0 to year T is given by

The first four factors on the right-hand side of the equation are the effects corresponding to the four factors in Identity A1 and their sum is the total change in energy losses from electricity production. The new effect ∆Eshr, i is the non-renewable share effect. It corresponds to the additional factor Pi. The change in T&D losses, ∆ET & D = ET & DT − ET & D0, is not decomposed. Instead, it is added to the total change in energy losses from electricity production to give the total change in energy losses from the energy sector, ∆Etot, i .

This approach has several advantages. First, only the electricity output of renewable sources is required for the decomposition. The energy input values are not required and there is no assumption on the efficiency of renewable sources. Hence, there is no distortion of the structure or intensity effects. Second, changes in the share of renewable energy are quantified by the non-renewable share effect associated with changes in Pi and are not left out of the decomposition. A positive share effect represents a decrease in the share of renewables while a negative effect represents an increase. This effect will be useful for the evaluation of the impact of renewables on changes in energy losses. Third, energy losses from the production of electricity for export can be accounted for in this identity and the impact of changes in the share of electricity trade can be quantified if necessary. Fourth, the identity distinguishes between electricity generation efficiency and T&D losses. The loss intensity only captures generation efficiency changes of fossil fuel and nuclear plants. T&D losses are considered separately and are not decomposed. A separate decomposition can be performed to understand the factors influencing T&D losses if necessary.Footnote 18 This approach ensures that the loss intensity is more well-defined and avoids the problem of having to assign the T&D losses to different energy sources by the share of electricity produced. The coverage of the energy sector remains the same and still comprises of losses due to electricity production, transmission and distribution.

Case study

A case study based on changes in Canada’s economy-wide primary energy consumption between 1990 and 2013 is presented. Identity A is applied to end-use sectors while Identity A1 is applied to the energy sector. Between 1990 and 2013, Canada’s TPEC increased by 2246 PJ, from 8452 to 10,698 PJ. This change in TPEC is decomposed at the sectoral level to reveal the factors influencing it. The data used is shown in Appendix Table 5.Footnote 19

From the results obtained using the additive LMDI-I method, the effects for each sector are summed to obtain the aggregate economy-wide effects shown in Fig. 1. The energy sector contributes to the two additional factors shown in Fig. 1—the non-renewable share effect and change in T&D losses. As expected, the key driver of the increase in TPEC was the activity effect. The aggregate intensity effect, which measures the economy-wide energy savings from energy efficiency improvements, was the key factor that reduced energy consumption. Without these energy savings, the TPEC in 2013 would have been 11,660 PJ. The remaining factors had relatively smaller impacts on the total change in energy consumption.

Economy-wide aggregate decomposition results from EEAS for changes in Canada’s total primary energy consumption between 1990 and 2013

The sectoral decomposition results shown in Fig. 2 reveal more details on the contribution of each sector to the total change in TPEC. The activity effect was consistently positive across all sectors. In particular, the activity effect for the industry sector was the largest contributor to the total increase in energy consumption. This was partially offset by a shift away from energy-intensive industries such as the pulp and paper, petroleum refining and chemicals industries, represented by the negative structure effect.Footnote 20 The second largest contributor was the activity effect of the residential sector. This was offset by large reductions from the intensity effect. This means that while the total floor area occupied by residential units increased substantially, the energy consumption per floor area decreased. Improvements to the efficiency of household appliances, better insulation and energy conservation are some of the changes that may have led to a reduction in energy intensity. For the passenger and freight transport sectors, although there was a reduction in energy intensity, these energy savings were largely offset by the worsening activity and structure effects. In particular, for the freight transport sector, there was a shift towards the use of trucks for the transportation of goods. Trucks have a higher energy consumption per tonne-kilometre in comparison to other modes of freight transport.

Sectoral decomposition results from EEAS for changes in Canada’s total primary energy consumption between 1990 and 2013

For the energy sector, the activity effect, which is primarily driven by electricity demand, was the main factor contributing to the increase in energy losses. An increase in the share of renewables in the electricity mix and an improvement in power generation efficiency offset some of the increase in energy losses. The decomposition results for the energy sector will differ if Identity A is used for the energy sector (conventional EEAS) instead of Identity A1 (recommended EEAS).Footnote 21 As an illustrative comparison, the physical energy content method is used together with Identity A based on the formulae shown in Case 2 of Table 2. The differences between the results given by the two approaches are shown in Table 3. A larger activity effect is obtained via Identity A as larger weights are used across all energy sources due to the inclusion of T&D losses in the weights for each energy source. T&D losses are not included in Identity A1. Instead, they are computed separately by taking the difference in the T&D losses between the 2 years of interest. The impact of changes in T&D losses are redistributed across the activity, structure and intensity effects in Identity A.

For the structure effect of the energy sector, it is more reasonable to compare the structure effect from Identity A (− 90.6 PJ) with the sum of the structure and share effects from Identity A1 (− 91.3 PJ). The small difference is entirely due to changes in T&D losses.Footnote 22 Differences at the energy source level are more significant and a comparison is shown in Fig. 3. The increase in the share of hydropower and other renewables is viewed as a beneficial development when Identity A1 is used, which is represented by the negative non-renewable share effect of − 73 PJ. However, in Identity A, this shift towards the use of more renewables is not captured. It is represented by a small positive structure effect attributed to renewables due to the small weights assigned to renewables.Footnote 23 Arguably, between the two, Identity A1 gives a better representation of the impact of changes in the share of renewables.Footnote 24 This is especially so for countries with large shares of renewables such as Canada where renewables make up more than 60% of the electricity mix. The small structure effect attributed to renewables when Identity A is used cannot be meaningfully interpreted in countries with large shares of renewable energy as a significant portion of the energy sector is not adequately explained or represented. Identity A1 is more refined as the contribution of renewables is explicitly defined through the non-renewable share effect of − 73 PJ. The negative structure effect for the energy sector of − 18 PJ indicates that less energy-intensive fuels such as natural gas replaced more energy-intensive energy sources. When Identity A is used, there is no differentiation between the impact of renewables and shifts among less efficient energy sources. In a sense, the share effect is reallocated to fossil fuels and nuclear energy.

Comparison of structure effect from EEAS by energy source derived based on Identity A1 and Identity A for Canada between 1990 and 2013

Finally, the intensity effect obtained via Identity A is larger in magnitude than that from Identity A1 as changes in the T&D loss fraction influence the intensity effect obtained via Identity A. The T&D loss fraction decreased between 1990 and 2013 although total T&D losses increased due to a higher electricity output. The decrease in T&D loss fraction resulted in a greater reduction in loss intensity when Identity A is used.

In summary, the decomposition results from the recommended EEAS are more refined as there is clearly differentiation among the factors of interest. Problems arising from distortions to the structure and intensity effects of renewable and nuclear energy are not encountered. The approach can be applied more generally to different energy systems, unlike the conventional EEAS which is more suitable for fossil-based energy systems.

Extensions to an emissions accounting system

There is a close relationship between CO2 emissions and energy consumption.Footnote 25 Notably, the combustion of fuels for energy generates CO2 emissions and this issue has gained international attention in light of concerns regarding climate change. Energy-related CO2 emissions are a key source of greenhouse gas emissions, contributing to about 60% of total global greenhouse gas emissions in 2014 (IEA 2017a). The need to rein in CO2 emissions worldwide has prompted researchers and analysts to seek to gain a better understanding of CO2 emission trends. IDA is a method that can be used to understand the drivers of CO2 emissions and a CO2 emissions accounting system (EMAS) is a logical extension of the EEAS. An EMAS can be particularly helpful in facilitating the analysis of both energy efficiency improvements as well as emission reductions. Notably, energy efficiency is just one of the many ways to reduce CO2 emissions. Fuel switching and increasing the share of non-fossil-based energy sources are other measures that can be implemented.

Studies which apply decomposition to economy-wide CO2 emissions of various countries and regions have grown rapidly in recent years (Ang 2015). Many IDA studies have been conducted on economy-wide CO2 emission trends (de Freitas and Kaneko 2011; Liu et al. 2012; Wang et al. 2005). Countries such as Switzerland (Federal Statistical Office 2015) and Australia (Vivid Economics 2013) have also utilised IDA to study their respective economy-wide CO2 emissions. Most of these studies decompose CO2 emissions directly and a formal study looking at the extension of the EEAS to an EMAS, including the linkages between the two, has not been reported. We examine the two systems in detail to reveal the similarities and differences between them. Design considerations and methodological issues relating to the development of an EMAS are discussed to facilitate a smooth extension of a national EEAS to a national EMAS.

EMAS framework

It may appear that an EEAS can be extended to an EMAS by simply replacing energy consumption in each sector with their equivalent CO2 emissions. The extension is not as straightforward and two issues need to be considered. The first is the number of factors in the decomposition identity. If only three factors are used, the last factor will be the CO2 emissions intensity, i.e. the CO2 emissions for each unit of activity. Besides changes in energy intensity, the emission intensity is also influenced by changes in the energy mix and CO2 emissions per unit of energy used. As a result, for the same amount of energy consumed, the CO2 emissions can be very different.Footnote 26

To account for these additional factors, the three-factor identity can be expanded into a five-factor identity, where the CO2 emissions for end-use sector i are given by:

where Cijk is the CO2 emissions arising from energy source k, \( {M}_{ij k}=\frac{E_{ij k}}{E_{ij}} \) is the share of energy source k in the total final energy consumption of sub-sector j and \( {U}_{ijk}=\frac{C_{ijk}}{E_{ijk}} \) is the emission intensity of energy source k in sub-sector j. The other factors are the same as those in the EEAS. The arithmetic change in CO2 emissions in each end-use sector i can then be decomposed into five factors—the activity effect, structure effect, intensity effect, mix effect and emission intensity effect:

The extension leads to an additional level of disaggregation by energy source k and more data is required to construct an EMAS as compared to an EEAS.Footnote 27 The detailed formulae for each effect based on LMDI-I is shown in the Appendix.

The second issue is how the energy sector can be suitably incorporated. Unlike the case of energy which experiences losses during transformation, transmission and distribution and is thereafter used by end-use sectors, CO2 emissions are only emitted during the stage of electricity generation. If these emissions are allocated to the energy sector, i.e. having an energy sector as the sixth sector as in the EEAS, the emissions from electricity consumption in end-use sectors will be zero. Since the weights for the decomposition effects are in terms of CO2 emissions in an EMAS, end-use energy efficiency from the use of electricity cannot be quantified as no weights are allocated to activities that consume electricity. This would be a problem as some sectors such as the services and residential sectors depend almost entirely on electricity in some countries.Footnote 28 Given the importance of quantifying end-use energy efficiency, it is therefore recommended that CO2 emissions from the energy sector are allocated to end-use sectors. This means that only end-use sectors are considered in an EMAS. Electricity is given an emission factor based on the emission intensity of electricity generation which is the CO2 emissions per kilowatt hour of electricity consumed by end-use sectors.

The approach described above has been adopted in some economy-wide CO2 emission studies. (See for example O’ Mahony et al. (2012), Sheinbaum et al. (2011) and Xu et al. (2014).) In this formulation, end-use energy efficiency from the use of electricity can be quantified. At the same time, changes in emissions from the energy sector are reflected in the emission intensity effect, which is similar to the SSR effect in an EEAS based on Identity C. If one wishes to gain a better understanding of the factors influencing the emissions from the energy sector such as changes in generation efficiency and fuel mix, a two-step decomposition is recommended. After Eq. (5) is used to decompose economy-wide CO2 emissions, the emission intensity of electricity, Uelec, which is the same for every sub-sector, can be decomposed in a second step. Footnote 29 This step is necessary as the CO2 emissions from electricity generation should not be allocated more than once. The framework will provide a complete decomposition analysis of the energy system and its related CO2 emissions.

EEAS and EMAS for Canada

To extend the EEAS for Canada in the “Case study” section to an EMAS, the first step is to focus on the three effects of end-use sectors in an EEAS. As shown in the formulae for each effect in the Appendix, the activity, structure and intensity effects of both accounting systems only differ in the weights assigned at the sub-sector level. The weights based on energy consumption in the EEAS are replaced by weights based on CO2 emissions. Note that the weights for the EMAS are computed by energy source k before they are summed to obtain the sub-sector level weights. Next, the mix and emission intensity effects can be computed based on energy data that has been disaggregated by fuel type shown in Appendix Table 5.Footnote 30 The mix effect measures the changes in the energy mix at the sub-sector level while the emission intensity effect measures changes in the emissions per unit of energy consumed. Both factors have to be computed by energy source.

Energy-related CO2 emissions in Canada increased by 110.7 million tonnes of CO2 (MTCO2) between 1990 and 2013, from 431.7 MTCO2 to 542.4 MTCO2. The aggregate economy-wide results for the EMAS are shown in Fig. 4. The activity effect was the dominant driver and the intensity effect offset some of the increase in CO2 emissions. The mix and emission intensity effects also offset some of the increases in CO2 emissions due to the activity effect. The negative mix effect captures the shift in end-use energy mix to cleaner sources such as electricity and natural gas while the negative emission intensity effect shows that the electricity sector became less carbon-intensive.

Economy-wide aggregate decomposition results from EMAS for changes in total CO2 emissions from Canada between 1990 and 2013

The emission intensity effect quantifies changes in the energy sector in the EMAS, unlike in the recommended EEAS where the energy sector is treated separately and different factors that influence the energy sector are quantified. There are other differences between the two accounting systems. From the aggregate decomposition results for the EEAS in Fig. 1 and EMAS in Fig. 4, one will notice that the structure effect is negative for the EEAS but is almost insignificant for the EMAS. The sectoral results reveal the sources of this difference. The sectoral results for the EMAS are shown in Fig. 5 and the numerical results are presented in Table 4 and these are compared with the sectoral EEAS results in Fig. 2.

Sectoral decomposition results from EMAS for changes in total CO2 emissions from Canada between 1990 and 2013

The first source of difference is the absence of the energy sector as a separate sector in the EMAS. The negative structure effect of the energy sector in the EEAS is not a factor in the EMAS. Second, the size of the effects for each end-use sector differs. In the EEAS, the structure effect for industry is much larger in magnitude in comparison to freight transport. However, this difference is not as prominent for the EMAS as the industry sector experiences a much smaller structure effect. This is because the weights used in computing the effects in the EEAS are based on the energy consumed while the weights used in the EMAS are based on the CO2 emissions arising from final energy consumption. The freight transport sector is mainly dependent on oil. In contrast, the industry sector consumes a mixture of electricity, coal, oil, natural gas and wood waste, which as a whole is less carbon-intensive compared to using only oil. As a result, the structure effect attributed to the industry sector is not as large in the EMAS in comparison to the EEAS. This explains the muted contribution of the structure effect in the EMAS results. The difference between energy consumption and CO2 emissions can also be observed from the difference in the total change. While the total change in final energy consumption for the industry sector was nearly twice that of the freight transport sector, the total change in CO2 emissions was only 20% more.

The sectoral results also highlight the importance of the mix and emission intensity effects. In the industry sector, shifts towards less carbon-intensive fuels and an improvement in the emission intensity of electricity helped to offset increases in CO2 emissions. If a three-factor identity was used instead, the energy intensity, mix and emission intensity effects would be combined into a single effect. The added advantage of the five-factor identity of the EMAS is the ability to quantify different climate mitigation measures as separate effects. Unlike energy consumption where policy measures mainly target energy efficiency improvements, a more diverse range of mitigation measures can be employed to reduce CO2 emissions. Switching of end-use energy consumption to less carbon-intensive sources and the decarbonisation of the electricity sector are additional measures that can be implemented to achieve emission reduction targets. They can be quantified separately by the mix and emission intensity effects respectively. These two measures, together with energy efficiency, form the three pillars of deep decarbonisation (Bataille et al. 2016). As concerns regarding climate change escalate, deep decarbonisation will become more important. In this regard, the EMAS will be beneficial in improving our understanding of the drivers of current CO2 trends and helping countries to track progress towards emission reduction targets at the national and sectoral levels. The effectiveness of existing policy measures can be evaluated and future targets can be determined.

Conclusion

A number of national EEAS have been developed by and for various countries. The aim is to quantify economy-wide energy savings from energy efficiency improvements and understand the factors influencing energy consumption in each sector. Over the years, accounting systems have become more sophisticated and there is general agreement on the framework to quantify end-use energy efficiency improvements. However, the peculiarity of the energy sector, where energy consumption is in fact the energy losses during transformation, transmission and distribution, has led to the development of several different approaches to accommodate the sector in an EEAS, each with its advantages and disadvantages. The recent rise in the adoption of renewable energy further complicates matters as countries with substantial shares of renewable energy are unable to accurately quantify and attribute changes in the loss intensity and the electricity mix using existing approaches. The failure to estimate and attribute the effects accurately can lead to confusion during results interpretation.

This study examines these issues in detail and recommends that energy losses from the energy sector be considered separately from final energy consumption of end-use sectors in an EEAS via a new approach. The new approach overcomes the problems faced by existing approaches by quantifying the contribution of changes in the share of renewable energy explicitly and separating T&D losses from losses due to energy transformation. It can also be extended in the future to account for energy losses due to electricity exports which may become more important as regional electricity grid integration becomes a reality in many geographical areas.

As motivations for improving energy efficiency and climate mitigation converge, national agencies and other organisations are likely to become interested in the possible extensions of the EEAS to an EMAS. This extension was also discussed in this paper and the linkages as well as differences between the two accounting systems were presented. Due to the differences between the two systems, for the EMAS, it is recommended that the CO2 emissions from the energy sector be allocated to the end-use sector that the energy is used in and the decomposition performed only for end-use sectors. A second-step decomposition can be performed to analyse the energy sector.

In the future, as new technologies are developed and climate mitigation measures evolve, further improvements to both accounting systems will be needed. Approaches that can capture economy-wide energy savings from the use of power generation technologies such as cogeneration or trigeneration power plants and combined water and power plants, as well as the energy penalty arising from low-carbon technologies such as carbon capture and storage, are areas for future research. These technologies influence efficiencies at the economy-wide level and require techniques that go beyond the analysis of individual sectors. Further studies on the inclusion of additional factors in each sector to account for unique features of each country as well as the merging of IDA with econometric analyses to examine the economic and political factors that influence changes in energy efficiency will shed more light on the factors that influence economy-wide energy efficiency. Another future area of research is the possible extension of emission accounting systems to scenario analysis to facilitate the comparison of different decarbonisation scenarios and the charting of national decarbonisation pathways.

Notes

IDA can also be used to analyse energy efficiency of primary or final energy separately (Landwehr and Jochem 1997), or examine specific sectors individually (Sorrell et al. 2009). These applications usually focus on more in-depth analyses of specific factors in comparison to the EEAS where the main aim is to develop an economy-wide composite energy efficiency indicator from sectoral trends.

The losses take the form of losses during the transformation of primary energy sources into secondary energy sources, the energy sector’s own use and losses in the transmission and distribution of secondary energy sources to final consumers.

The energy consumption of the five end-use sectors refers to final energy consumption while the energy consumption of the energy sector refers to the energy losses from transformation, transmission and distribution and the energy sector’s own use. Therefore, the sum of the final energy consumption of the five end-use sectors and the energy losses from the energy sector is theoretically equivalent to the TPEC.

In additive decomposition, the contribution of factors can be expressed directly in the units of the indicator (i.e. energy units for energy consumption) and the results can be interpreted more easily by policymakers. Multiplicative procedures have other merits and analysts may choose either procedure in their analysis. Further details about the commonly used IDA methods and the basis of making an appropriate choice can be found in Ang (2015).

The inclusion of generation systems where there are multiple outputs (e.g. combined heat and power plants) in an EEAS is complicated as the loss intensity may not reflect actual changes in efficiency accurately. How the changes in efficiency can be captured more accurately at the economy-wide level through an EEAS is an area that requires further research.

Canada’s EEAS for the period 1990 to 2004 incorporates the electricity generation sector but the intensity effect of the electricity sector is not included in the economy-wide energy intensity index.

Primary energy consumption of the electricity sector is decomposed instead of the energy losses during transformation in this study.

When a monetary activity indicator such as gross value-added is chosen (Kerimray et al. 2017; Román and Colinet 2018; Shahiduzzaman and Alam 2013), the energy sector is often classified as one of the sub-sectors of the industry sector. A disadvantage of using monetary activity indicators for the energy sector is that the resultant intensity effect may not be a good reflection of changes in energy efficiency.

Assume that an electricity system requires an input of 2.4 million tonnes of oil equivalent (Mtoe) of energy to generate 1 Mtoe of electricity (i.e. the energy loss is 1.4 Mtoe). If a sub-sector consumes 1000 GWh of electricity, its source energy consumption will be 2400 GWh of electricity or 2.4 times the electricity consumed.

While the first three terms in Identity C are the same as those in Identity A, the corresponding sub-sectoral effects that are obtained based on the two identities are different due to the different weights assigned. Based on the additive LMD-I method, the weights assigned in Identity C are based on the source energy, \( {E}_{ij}^s \), while the weights assigned in Identity A are based on the final energy consumed, Eij. The impact of this difference depends on the scale of the energy losses from the energy sector and the share of electricity consumed in each end-use sub-sector.

Renewable energy and nuclear power plants have their own actual conversion efficiencies. For example, the conversion efficiency of a solar panel is a measure of the fraction of solar energy that can be converted to electricity. However, it does not have an impact on supply security as the energy source is renewable and no fuel needs to be imported or extracted.

The primary energy form of geothermal and solar thermal is heat.

If Identity C is selected, the energy sector is only accounted for under the SSR effect and no further breakdown is available. The impact of renewables, nuclear energy and T&D losses are all subsumed under the SSR effect and do not influence the aggregate economy-wide intensity effect.

Losses include the energy sector’s own consumption but this is not shown explicitly in the formulae in Table 2 as it is unlikely that this will result in significant differences across the different cases.

The loss fraction is computed as the ratio of the T&D losses in kilowatt hour to the electricity output in kilowatt hour (i.e. Qi).

This problem is unique to the energy sector. It does not occur when renewables such as wood and wood waste are consumed directly in end-use sectors as the energy is consumed directly and not transformed into electricity.

If geothermal energy or biomass is converted into electricity, it can be included as an additional energy source j.

For example, Bashmakov and Myshak (2014) decompose T&D losses by classifying them in a separate sector.

The data were collected from Energy Use Data Handbook (1990–2013) (Natural Resources Canada 2016b) and its accompanying comprehensive Energy Use Database (Natural Resources Canada 2016a). For simplicity, agriculture is included in the industry sector and street lighting is included in the services sector. Net exports of electricity from non-fossil based sources were obtained from the IEA world energy balance database (IEA 2017d). Electricity consumption by pipelines which constitutes less than 1% of total electricity consumption is excluded from end-use electricity consumption as there is no activity data.

Due to data limitations, the activity measure for the industry sector in this study is GDP output. Monetary activity indicators are not ideal as the resulting intensity effect may not be an accurate proxy for energy efficiency. Physical activity measures are preferred and will lead to more accurate estimations of the contribution of energy efficiency to changes in final energy consumption. For more reliable results, further refinements to the decomposition of the industry sector can be made with a more detailed data set. For example, Office of Energy Efficiency (2016) uses physical output as the activity measure and capacity utilisation is also included as a fourth factor in their report on Canada.

There are no differences in the results for the end-use sectors because Identity A is applied regardless of the identity used for the energy sector. This is an advantage of using Identity A or A1. Countries such as Australia, New Zealand and Canada that have developed EEAS for end-use sectors can simply include the energy sector as an additional sector using Identity A1.

If T&D losses are zero, the structure effect from Identity A will be equivalent to the sum of the structure and share effects from Identity A1. Therefore, Identity A can be seen as a less refined version of Identity A1.

The weights for renewables are based on the T&D losses which are a very small fraction of the generation losses from fossil fuels and nuclear energy.

When the conventional EEAS is used, the structure effect is mainly determined by energy intensive activities. This means that a shift to renewables is quantified by a large negative structure effect attributable to fossil fuels and nuclear energy while a shift away from renewables is quantified by a large positive structure effect which is also attributed to fossil fuels and nuclear energy.

In this study, CO2 emissions refer to energy-related CO2 emissions.

For example, a shift from coal to natural gas in industrial energy use can generally lower CO2 emissions. An increase in the fraction of renewables in the electricity mix can also reduce emissions from electric vehicles. These changes represent different climate mitigation measures and can be quantified by separate factors in the decomposition.

Since CO2 emissions data are usually estimated by multiplying energy consumption of each fuel type with their corresponding emission factors, the data used to derive the economy-wide CO2 emissions should be sufficient for the computation of the mix and emission intensity effects.

Of the 140 countries with available CO2 emissions data for the year 2015, the shares of CO2 emissions from electricity and heat generation in residential sector were more than 80% for 43 countries (IEA 2017b).

The emission intensity of electricity generation is of interest as emission reductions can be achieved more easily in this sector. IDA has been used by IEA (2017b) to decompose emissions from the electricity sector. (For more details on the identity that can be used to decompose CO2 emissions from electricity generation, see Xu and Ang (2013). For more details on two-step decomposition, see Xu and Ang (2014).)

Data by fuel types for some industry sub-sectors are not available. They are estimated based on the proportion of fuels in the sub-sector’s end-use energy mix for an earlier year or based on a rough estimate if no data is available. Constant emission factors measured in tonnes of CO2 per tonne of oil equivalent are used and they are 3.99 for coal, 3.08 for oil and 2.33 for natural gas.

References

Ang, B. W. (2006). Monitoring changes in economy-wide energy efficiency: from energy–GDP ratio to composite efficiency index. Energy Policy, 34, 574–582.

Ang, B. W. (2015). LMDI decomposition approach: a guide for implementation. Energy Policy, 86, 233–238.

Ang, B. W., & Goh, T. (2018). Bridging the gap between energy-to-GDP ratio and composite energy intensity index. Energy Policy, 119, 105–112.

Ang, B. W., Mu, A. R., & Zhou, P. (2010). Accounting frameworks for tracking energy efficiency trends. Energy Economics, 32(5), 1209–1219.

Asia-Pacific Economic Cooperation (2011). 2011 Leader’s declaration. Hawaii: 19th APEC Economic Leaders’ Meeting. Access at http://www.apec.org/Meeting-Papers/Leaders-Declarations/2011/2011_aelm. Accessed 7 February 2018

Bashmakov, I., & Myshak, A. (2014). Russian energy efficiency accounting system. Energy Efficiency, 7(5), 743–759.

Bataille, C., Waisman, H., Colombier, M., Segafredo, L., Williams, J. (2016). The deep decarbonisation pathways project (DDPP): insights and emerging issues. Climate Policy 16, S1–S6

Belzer, D. B. (2014). A Comprehensive system of energy intensity indicators for the U.S.: methods, data and key trends. Richland: Pacific Northwest National Laboratory.

Belzer, D. B., Bender, S. R., & Cort, K. A. (2017). A comprehensive system of energy intensity indicators for the U.S.: methods, data and key trends (Rev 2). Richland: Pacific Northwest National Laboratory.

BP (2017). BP Statistical Review of World Energy. London

Colinet, C. M. J., & Román, C. R. (2016). LMDI decomposition analysis of energy consumption in Andalusia (Spain) during 2003–2012: the energy efficiency policy implications. Energy Efficiency, 9(3), 807–823.

de Freitas, L. C., & Kaneko, S. (2011). Decomposition of CO2 emissions change from energy consumption in Brazil: challenges and policy implications. Energy Policy, 39(3), 1495–1504.

European Commission (2017). 2017 assessment of the progress made by Member States towards the national energy efficiency targets for 2020 and towards the implementation of the Energy Efficiency Directive as required by Article 24(3) of the Energy Efficiency Directive 2012/27/EU, Report from the Commission to the European Parliament and the Council Brussels

Eurostat (2018). Calculation methodologies for the share of renewables in energy consumption. Accessed at https://ec.europa.eu/eurostat/statistics-explained/index.php/Calculation_methodologies_for_the_share_of_renewables_in_energy_consumption. Accessed 8 April 2019

Federal Statistical Office. (2015). Air emissions accounts: decomposition of Switzerland’s fossil CO 2emissions. Switzerland: Federal Statistical Office.

Goh, T., & Ang, B. W. (2018). Tracking economy-wide energy efficiency using LMDI: approach and practices. Energy Efficiency, 1–19.

IEA (2014). Energy efficiency indicators: essentials for policy making. International Energy Agency, Paris

IEA (2017a). Balance definitions. International Energy Agency, Paris

IEA (2017b). CO 2emissions from fuel combustion: overview. International Energy Agency. Paris

IEA. (2017c). IEA Key World Energy Statistics. Paris: International Energy Agency.

IEA. (2017d). World energy balances database. Paris: International Energy Agency.

IEA (2018). Statistics: frequently asked questions (FAQ). Accessed at https://www.iea.org/statistics/resources/questionnaires/faq/. Accessed 24 October 2018

Kerimray, A., Kolyagin, I., & Suleimenov, B. (2017). Analysis of the energy intensity of Kazakhstan: from data compilation to decomposition analysis. Energy Efficiency, 11(2), 315–335.

Landwehr, M., & Jochem, E. (1997). From primary to final energy consumption—analysing structural and efficiency changes on the energy supply side. Energy Policy, 25(7-9), 693–702.

Lermit, J., Jollands, N. (2001). Monitoring energy efficiency performance in New Zealand. Energy Efficiency and Conservation Authority. New Zealand

Liu, Z., Geng, Y., Lindner, S., & Guan, D. (2012). Uncovering China’s greenhouse gas emission from regional and sectoral perspectives. Energy, 45, 1059–1068.

Natural Resources Canada. (2016a). Comprehensive energy use database. Ottawa: Natural Resources Canada.

Natural Resources Canada. (2016b). Energy Use Data Handbook: 1990 to 2013. Ottawa: Natural Resources Canada.

O’ Mahony, T., Zhou, P., & Sweeney, J. (2012). The driving forces of change in energy-related CO2 emissions in Ireland: a multi-sectoral decomposition from 1990 to 2007. Energy Policy, 44, 256–267.

Office of Energy Efficiency. (2006). Energy efficiency trends in Canada 1990 to 2004. Ottawa: Natural Resources Canada.

Office of Energy Efficiency. (2016). Energy Efficiency Trends in Canada 1990 to 2013. Ottawa: Natural Resources Canada.

Petchey, R. (2010). End use energy intensity in the Australian economy. Canberra: Australian Bureau of Agricultural and Resource Economics - Bureau of Rural Sciences.

Reuter, M., Patel, M. K., & Eichhammer, W. (2017). Applying ex-post index decomposition analysis to primary energy consumption for evaluating progress towards European energy efficiency targets. Energy Efficiency, 10(6), 1381–1400.

Román, C. R., & Colinet, C. M. J. (2018). Is energy efficiency a driver or an inhibitor of energy consumption changes in Spain? Two decomposition approaches. Energy Policy, 115, 409–417.

Shahiduzzaman, M., & Alam, K. (2013). Changes in energy efficiency in Australia: A decomposition of aggregate energy intensity using logarithmic mean Divisia approach. Energy Policy, 56, 341–351.

Sheinbaum, C., Ruíz, B. J., & Ozawa, L. (2011). Energy consumption and related CO2 emissions in five Latin American countries: changes from 1990 to 2006 and perspectives. Energy, 36, 3629–3638.

Sorrell, S., Lehtonen, M., Stapleton, L., Pujol, J., & Champion, T. (2009). Decomposing road freight energy use in the United Kingdom. Energy Policy, 37, 3115–3129.

Torrie, R. D., Stone, C., & Layzell, D. B. (2018). Reconciling energy efficiency and energy intensity metrics: an integrated decomposition analysis. Energy Efficiency, 11(8), 1999–2016.

Vivid Economics (2013). Analysis of electricity consumption, electricity generation emissions intensity and economy-wide emissions. Report prepared for the Climate Change Authority, Australia.

Wang, C., Chen, J., & Zou, J. (2005). Decomposition of energy-related CO2 emission in China: 1957–2000. Energy, 30, 73–83.

Xu, X. Y., & Ang, B. W. (2013). Index decomposition analysis applied to CO2 emission studies. Ecological Economics, 93, 313–329.

Xu, X. Y., & Ang, B. W. (2014). Multilevel index decomposition analysis: approaches and application. Energy Economics, 44, 375–382.

Xu, J.-H., Fan, Y., & Yu, S.-M. (2014). Energy conservation and CO2 emission reduction in China’s 11th Five-Year Plan: a performance evaluation. Energy Economics, 46, 348–359.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors declare that they have no conflict of interest.

Additional information

Publisher’s note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix

Appendix

Based on the LMDI-I decomposition formulae for the additive LMDI-I method (Ang 2015), the three effects for Identity A in the EEAS are given as

where the logarithmic mean is given as \( L\left(x,y\right)=\frac{x-y}{\ln x-\ln y} \) for x ≠ y and L(x, y) = x for x = y.

Similarly, the five effects for the identity used in the EMAS are given as

Rights and permissions

About this article

Cite this article

Goh, T., Ang, B.W. Comprehensive economy-wide energy efficiency and emissions accounting systems for tracking national progress. Energy Efficiency 12, 1951–1971 (2019). https://doi.org/10.1007/s12053-019-09796-w

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s12053-019-09796-w