Abstract

Recent research has shown a huge impact of non-renewable energy (NRE) production on environmental health. In this context, this work analyzes the effects of GDP growth and long- and short-term consumption of renewable and non-renewable energy (RE and NRE, respectively) on carbon emission in BRICS and OECD economies. The quantile autoregressive distributed lag (QARDL) model was employed on the panel data from 1980 to 2016. Findings suggest a negative GDP-carbon emission correlation and a positive NRE-carbon emission correlation in the considered economies. Furthermore, carbon emission decreases with increase in gross capital formation, whereas trade openness does not have any significant effect on carbon emission. It has been determined that the application of the error correction method (ECM) has less effect on energy consumption as compared to the past levels and changes in energy consumption. In the long-term, a positive correlation of carbon emission and energy consumption is observed, whereas limited short-term effects of energy consumption on carbon emission are observed. Therefore, an RE-based energy production approach is recommended in the selected region for the future projects.

Similar content being viewed by others

Explore related subjects

Discover the latest articles, news and stories from top researchers in related subjects.Avoid common mistakes on your manuscript.

Introduction

Developing nations primarily rely on industrialization to meet economic targets and to improve the living standard of their citizens. In advanced and developing nations, to adopt modern production techniques, and to make industrial production more attractive and effective, the utilization of non-renewable resources as a source energy has increased. This has a substantial influence on per capita GDP and improves the quality of life by increasing the provision of goods. However, the efforts to increase per capita GDP through increasing the production, economies are compromising on the quality of the natural environment; as a result, environmental challenges are increasing in emerging nations (Kim 2013; Sobhee 2004, and Zambrano-Monserrate et al. 2018). However, better quality or healthy environment is an equally important factor to promote the living standard of individuals (Sun et al. 2020c; Sun et al. 2020d; Sun et al. 2019b, and Sun et al. 2020a). Thus far, it seems that clean and healthy environment is only a demand of modern societies and essential for their well-being. Thus, the notion of economic development in developing economies is suspected to intensify the emissions of greenhouse gases as it shows the greater reliance on the usage of non-renewable energy resources (NER) to achieve development targets (Anser et al. 2020; Mohsin et al. 2019c; Mohsin et al. 2020a; Iram et al. 2019, and Baloch et al. 2020).

Thus, the existing development pattern in developing nations is highly based on the utilization of non-renewable resources with the least importance of environmental quality. The reason for high consumption of non-renewable resources of energy is economical and cost-effective, in terms of goods production. Thus, the utilization of NER may cause a greenhouse effect on the environment of developing Asian economies. Meanwhile, the utilization of renewable energy resources RER seems environment-friendly in developed and developing economies (Chow 2015). The advancement of the industrial sector, extension in the size of trade, and improvement in the production of goods largely depends on energy, therefore it can be argued that the achievement of development goals in advanced and emerging economies is not possible without adequate energy supply. Thus, energy is a basic input to produce goods at a large scale; therefore, the significance of energy utilization to produce goods is studied by number of studies (Omri 2013). Zheng and Walsh (2019) stated that China ranked amongst the largest energy-consuming economies.

Although there is an extensive research for the assessment of CO2 emissions and their effects, there still exist some limitations to address. For instance, CO2 emissions are mostly modeled through linear models (Kazmi et al. 2019). This approach is however not a realistic representation of this non-linear dynamic process, due to some important time-series variables. Another limitation is the existence of specific variables within cross-sectional data, which can not be modeled through linear appraoch in case of heterogeneity (Hsiao 2005). Next, it is not possible to evaluate the threshold value through conventional models when the change in the independent variables lies at different spatial and temporal locations.

This work aims to fill the aforementioned literature gap and presents a more accurate assessment. This research used quantile asymmetries for the short- and long-run associations between globalization in various types and energy usage using Quantile Autoregressive Distributed Lag (QARDL) framework proposed by Cho et al. (2015). By employing the QARDL methods, this research assesses the reliability of the long-run association over the quantile and offers a more adjustable econometric model to assess the links being taken into account (Le et al. 2019). The benefit of using potential imbalance in the reaction of energy usage to addition/reduction in assessing results while the QARDL framework is more useful than linear frameworks, as it permits for geographical imbalance. At the same time, the QARDL framework takes into account the long-run association between energy usage and carbon discharge qualities of cointegration characteristics. Hence, panel data between 1980 and 2016 is assessed by using the ARDL framework. Hence, the final objective of this research is to offer strong findings that can be established as useful for decision-makers and specialists to enhance the advantages of the OECD and BRICS program by presenting carbon regulation regulations for the emerging countries.

The rest of the paper is organized as follows: “Literature review” presents the essential literature review; “Methodology” discusses the data and methodology used; “Results and discussion” presents the obtained results and discussion; and “Conclusion and policy implication” is a brief conclusion and policy implication from the study.

Literature review

Rapid growth of globalization in the 1990s had a huge impact on the socio-economic and political aspects of life. Continuous economic progress enables a country to develop through capital flow avenues, international trade, and foreign direct investments (FDIs) (Gasser 2020). According to Dreher (Trotta 2020), countries with higher globalization have the better framework for a long-term economic growth. His findings susggest that globalization is a key factor in a country’s economic growth. However, recent change in policy structure and globalization have not only been significant in determining the relationship between globalization and economic progress but it has also changed the globalization-to-energy consumption relationship (Iqbal et al. 2020). Particularly, it is important to determine the importance of globalization in the energy demand progression for countries like India (Sun et al. 2020b; Mohsin et al. 2018b; Mohsin et al. 2019a; Maulidia et al. 2019).

Like other economies, energy utilization has also proved as a major input to improve GDP in China. Farhani (2013) also investigated the influence of energy usage on gross domestic product (GDP) across the Middle East and North Africa (MENA) economies. Their findings showed a bidirectional link amongst energy usage and GDP, in the long-run. Lin and Benjamin (2017) determined the link amongst GDP, foreign direct investment, and energy utilization by analyzing the data from MINT countries. Their results depicted bidirectional causality amongst GDP and energy consumption in Mexico, Indonesia, Nigeria, and Turkey. Furthermore, outcomes of the global panel analysis also revealed a bidirectional link amongst energy consumption and greenhouse gas emissions. Furthermore, it has been observed that GDP and energy utilization have a positive link in the top ten energy-consuming economies (Mohsin et al. 2019a; Shah et al. 2019, and Sun et al. 2019a).

Shahbaz et al. (2012) scrutinized the link of energy consumption with GDP by analyzing the data of top ten energy-consuming economies, i.e., China, France, Germany, India, Japan, South Korea, Brazil, Canada, Russia, and USA. Moreover, energy utilization is a primary input to promote GDP in the top ten energy-consuming economies. Ozcan and Ozturk (2019) scrutinized the link to energy utilization and GDP in China. Their results showed that in China, GDP primarily depend on energy usage. Liu and Hao (2018) found the link to energy usage and GDP by analyzing the panel data from one belt one road economies. Their results depicted that there exists a bidirectional link amongst GDP and energy utilization in developing Asian economies, in the long run. For instance, Tang and Abosedra (2014) scrutinized the link between GDP and energy usage by analyzing the data of twenty-four MENA economies. They indicated that energy has a paramount impact in stimulating GDP (Mohsin et al. 2020b; Mohsin et al. 2019b, and Mohsin et al. 2019c).

A study conducted by Sghari and Hammami (2016) depicted the positive influence of GDP and energy usage on greenhouse gas emission by analyzing the panel data from fifty-eight economies. Furthermore, the works of Lin and Benjamin (2017), Farhani (2013), and Omri (2013) have reported that GDP and energy usage are the main contributors to greenhouse gas emission. Moreover, Raza et al. (2019) scrutinized the role of energy usage on greenhouse gas emissions in the USA. According to their findings, energy utilization and gross regional products are primary sources of greenhouse gas emissions and threats to environmental sustainability. Thus, environmental quality in USA is deteriorated by excessive usage of NER. The study of Hanif (2017) has analyzed the data of fifteen emerging Asian economies to examine the influence of GDP and NER utilization on greenhouse gas emissions. The study indicated that usage of NER and GDP has escalated the carbon dioxide emission (Mohsin et al. 2018a; Mohsin et al. 2019c; He et al. 2020; Alemzero et al. 2020; Chandio et al. 2020, and Asbahi et al. 2019).

The research discovered contrary findings as the panel assessments backs a static process of per capita CO2 discharge for all the states of the sample whereas the sole assessments proposed a mean reversion for just 10 states. Despite the aforementioned discussion, previous literature study the averaged effects of energy consumption on the emission of CO2 and neglect its vartiation across different conditional distribution quantiles. Furthermore, linear models have been used to study the link between energy consumption and CO2 emission in most cases, which does not represent the complex relationship precisely (Sun et al. 2020b).

Methodology

Energy demand rises with a country’s economic growth avenues. This is the true especially in case of economies with ample resources of energy, which helps them grow faster. The feedback of economic improvement to affirmative advancement in non-renewable energy usage may vary from feedback to negative development, with the accompanying ramifications of environmental quality (Lee 2016). In essence, Kaya identity was the major contributor in the development of IPAT model. The Kaya identity provides a simple equation of relationship that clearly links energy consumption to energy related CO2 emissions, which can be used to decompose CO2 emission, as a product of individual factors. The IPAT model has the following assumptions.

-

1.

The country is engaged to reduce its emissions up to certain amount within a set deadline under international agreement.

-

2.

The obligation emission reduction cost is directly associated to the quantity of national emissions (I). This cost corresponds to the overall amount of money, which is being invested to reduce national emissions.

-

3.

The country or state gets financial aid or foreign direct investment from an international organization, which is related to its carbon emissions.

If country or state did not meet its obligation regarding emission reduction, it would pay penalty in the form of “fine” as compared to the difference between its actual emissions and its set target at the deadline date. Hence, in the current research, to investigate the impact of NRE, RE, and GDP improvement on CO2 emission, an analytical model is devised by pursuing the research of Shahbaz and Sinha (2019). Hence, a practical way of the suggested framework considering the EKC hypothesis can be stated as below:

Econometric framework in Eq. 1 can be defined through adding an error term and may be expressed by means of:

In Eq. (2), “λ1” and “λ2” shows the slope of GDP growth rate and GDP2. In this case, Xsn denotes the group of predicted an indicator of energy and economic which can impact the CO2 emission in emerging economies of the OECD and BRICS (Firpo et al. 2017). So, “s” is the slope of a further “n” variable. After computing renewable energy consumption (REE), carbon-based energy (FFE) consumption, capital (GCF), and trade openness (TRD), the following stage is the constitution of the linear equation for scientific investigation. The long-run panel ARDL model is presented below:

In this case, λ0 symbolizes an intercept term, λn represents the set of an independent variables coefficients, and “ui” represents the error term. While subscript “t” and “i” are employed for a time frequency and cross section respectively. Prior to predicting Eq. (3), the bounds’ method has been implemented to determine cointegration. The bounds’ assessment for null hypothesis was suggested by Kim (2013) to verify the cointegration relationship, which can be stated as below: the null hypothesis of bounds’ assessment, that is, cointegration does not exist, is expressed as below:

H0: λ1 = 0; λ2 = 0; λ3 = 0; λ4 = 0; λ5 = 0; λ6 = 0 (4).

After evaluating the cointegration between variables using boundary evaluation and implementing panel ARDL for long-term forecasting, the next step is to establish short-term and long-term relationships between variables and establish an error accuracy framework. For this aim, the short-term changes and error accuracy changes added in Eq. (3) can be stated as below:

In this case, “d” is the first difference operator and Φ1, Φ2, Φ3, Φ4, Φ5, Φ6, and Φ7 depict the slope of variables for short-term findings, whereas γ1, γ2, γ3, γ4, γ5, γ6, and γ7 depict the variable’s slope in the long-term (Chen and Hsiang 2019). When long-term and short-term associations are devised, there is a requirement to build an error accuracy model toward measurement of the pace of convergence to attain an equilibrium condition. Hence, to assess the speed of alterations, the below equation will be predicted.

In Eq. (7), the error accuracy term ecmt − 1 is included to investigate the merging from short-term to long-term predictions. In this instance, “∅” portrays the slope of ECM, which depicts the pace of alterations from short adjustment from short-run to long-run direction. To assess the cointegration association between energy usage and CO2 discharge for fifteen developing Asian countries over quantiles, we used the presently suggested QARDL framework devised through McNown et al. (2018), as we presented earlier QARDL assessment guarantees assessment of quintile long-run equilibrium influence of energy usage on ecological disarray.

Smallest σ − field generated by {Gt, GDPt, Kt, ECt − 1, Gt − 1, GDPt − 1, Kt − 1, …}, and p, q1, q2, and q3 are lag orders, ecological disorder examined through carbon dioxide

Ecological disarray is examined through carbon dioxide. It can be presented that energy usage cointegrated CO2 discharge, such that εt(τ) = ECt − QECt(τ/Ft − 1) and QECt(τ/Ft − 1) is the τth quintile of ECt dependent on the data set Ft − 1 outlined above. To investigate the QARDL, we rewrite Eq. (12) as,

where

whereas

To avoid multicollinearity, the QARDL model is shown as,

Employing the framework in Eq. (16), there prevails a chance of contemporaneous correlation between νt and ΔGt, ΔGDPt, and ΔKt. The estimation of νt on ΔGt, ΔGDPt, and ΔKt with the form νt = γGΔGt + γGDPΔGDPt + γKΔKt + εt. The ultimate innovation εt is, hence, not associated with ΔGt, ΔGDPt, and ΔKt. QARDL-ECM model is outlined as,

The initial difference (Chiang and Sasaki 2019) assessment by employing the vector autoregressive (VAR) framework offers a partial result for cointegrated variables. Hence, one extra variable is added in the vector autoregressive (VAR) system, such as error correction term (ECM) to discover the long-term association between the variables. Much reliance on NER resources for better growth has boosted the environmental pollution hazard. The rapid increase in environmental degradation has reduced the level of environmental sustainability in emerging economies. According to previous studies, increased level of energy usage although has improved GDP yet a main source of greenhouse gas emissions in the emerging as well as advanced economies (Zhang et al. 2019). The study conducted by Zhang et al. (2019) investigated the impact of energy utilization on greenhouse gas emissions in China. The results showed the presence of bidirectional causality from the growth of the agriculture sector to greenhouse gas emission in China. Ito (2017) found the impact of RER usage on greenhouse gas emissions and investigated the panel data of forty-two emerging economies. The results indicated that renewable energy utilization plays a significant role in reduced carbon dioxide emission in emerging economies. The descriptive statiscts values are presented in the Table 1.

Results and discussion

Table 1 shows the essential statistical measures established on the basis of independent and dependent variables. During the second step of statistical examination, multicollinearity is observed by investigating the intensity of pairwise correlation. Hence, Table 2 shows the results of the correlation matrix. The findings portray that the coefficient of correlation"r2" is adequately lower compared to the critical value (i. e., r2 ≤ 0.8), which portrays that the suggested model does not have multicollinearity. The findings depict that there is not a strong correlation of carbon dioxide emissions (CO2) with energy consumption (REE), carbon-based energy usage (FFE), GDP growth (GDP), squared of GDP (GDP2), trade openness (TRD), and capital formation (GCF).

These results show that considerable volumes of energy usage enhance the environmental performance index for the OECD countries. Hence, the findings from unit root tests shows that this study’s variables possess a blended cointegration sequence. Hence, to predict the effect of RE, NRE, GDP, and GDP2 at CO2 emissions in the countries of OECD, and BRICS regions, an ARDL method is used to predict findings (Table 3).

The support of exports in CO2 discharge 1.7090%. A 0.4472% of carbon discharge is caused due to modern disturbances resulting in foreign direct investment. A significant part of carbon discharge, that is, 94.5437%, is justified by its modern impacts due to carbon discharge. The results highlight that the usage of renewable energy resources (RER) has a negative influence on greenhouse gas emissions in emerging Asian economies. The coefficient of RER usage is − 0.19 which is significant at 1% and indicating that a percent upsurge in the share of RER usage has the potential to reduce greenhouse gas emissions about 0.19% in the selected Asian economies. When HTR is applied, the results show that 1% increase in the share of RER consumption in total energy usage has the potential to control greenhouse gas emissions about 0.13% if all other factor considered constant. Thus, the results are in lined with Sinha and Shahbaz (2018) and Mazur et al. (2015); they also highlighted the negative influence of energy usage on greenhouse gas emissions in different regions of the world. By itself, technological advancement is responsible for i.e. 54.3583% due to its own contemporary impacts.

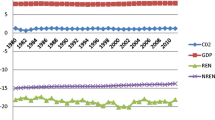

In 2015, the energy use of the BRICS Clubs (Fig. 1) reached 2.1 billion tons of oil equivalent (toe), accounting for about 35% of the total global energy production. In that year, the BRIC countries emitted more than 15.5 billion tons of carbon dioxide, accounting for 43% of the world’s total emissions. The results also show that the population growth rate in developing Asian economies is also promoting greenhouse gas emissions. According to the results of RE and HTR, 1% increase in population growth rate leads to increase in greenhouse gas emissions about 0.93 and 0.73% respectively. The results are validating the finding of Usenata (2018) and Waluyo and Terawaki (2016); they also found an increasing relationship between population growth and environmental degradation in developing economies. The empirical results of this study are emphasizing the implementation of environmental management policies and improvement in the share of RER is necessary to control greenhouse gas emissions in emerging Asian economies. Interestingly, we found inverted U–shaped ECKC, which is of strong statistical significance. We find that the highest point or turning point of environmental crime relative to GDP per capita is using the blocking boot method; we restored the 90% confidence interval for the vertices (Fig. 2).

Energy consumption (million tone oil equilent)

GDP in billion US dollar

CD statistics shows − 1.1398 having p value 0.1792 while off diagonal average value is 0.5911. The findings depict the p value to be more than 5%, hence, accepting the null hypothesis. The findings also show that there does not exist any cross section dependency in the model. Hence, the findings predicted with the support of ARDL model are decisive and potent. Being major CO2 emitters, the BRICS nations (Fig. 3 and Fig. 4) were urged by developed countries during climate change arbitrations during the last decade.

CO2 emission (Mtoe)

Decoupling of the EEE categories from the economic activity GDP and CO2 emission

Table 4’s findings depict that RE and REE consumption possesses a coefficient value of − 0.06, being significant at 10%, showing 1% inclusion in RE consumption has decreased the 0.06% of CO2 emission amongst the emerging economies of the OECD and BRICS, if we knowledge all other aspects as constant. A critical contribution of 47.1969% toward foreign direct investment is through economic development. Carbon discharge contributes a 12.1999% chunk of foreign direct investment. Contemporary advancements resulting in technological innovations justify foreign direct investment by 7.7460% (Tsaurai and Ngcobo 2020).

A 1% enhancement in the consumption of NRE enhances CO2 emissions by 0.07% (Fig. 5) in emerging economies of the OECD and BRICS, if all other aspects are considered constant. This positive association between NRE consumption and CO2 emission has already been verified by (Salim et al. 2019).

Primary energy sector contributing in activity, structure, and intensity

In addition, the linear long-run cointegration specifications between energy usage, carbon discharge, and economic advancement are discovered to be inconsequential amongst the two most globalized areas. Financing has a compelling relationship with energy usage in the long-term amongst the OECD countries, where it is discovered to not impact energy usage in the long-term amongst BRICS countries (Table 5). Although these result is similar to most empirical evidence on EKC (Dinda 2004; Sinha and Shahbaz 2018), there may be different reasons. However, the study of Zafar et al. (2019) quantified the influence of RER on GDP in emerging economies. The results of the study depicted a bidirectional association amongst GDP and RER in the short run. A further study conducted by Sarkodie and Adams (2018) compared the impact of RER and NER to stimulate GDP. They showed that the role of NER to promote GDP is more evident as compared to the RER. Meanwhile, previous studies showed a crucial role of NER in GDP; however, there is also a strong association of NER with environmental hazards in the emerging economies. Therefore, further supplementary explanations will indicate that the commercial sectors of these provinces may shift illegal environmental activities from richer provinces to poorer (underdeveloped) provinces for opportunistic and strategic behavior. The results of our other socio-economic variable unemployment rates illustrate the positive impact on the outcome variables (as expected), but only in the normal case, and clustered by annual standard error. This finding confirms to some extent the fact that the unemployment rate reflects the indirect measure of the opportunity cost of crime, which has a complementary effect and induces the economic entity to commit more crimes. These results can be justified through the fact that these economies attained different phases of green and clean strategies because they are inviting ventures in fossil fuel storage. During 2000–2016, these economies tried to increase efficiency of energy by investing or inviting investor for the innovation in this field especially for those industries which were highly energy intensive but this not happened to the required level due to multiple (political, social, and economical) factors and thus CO2 intensity in these economies kept growing with the passage of time. In current time, these economies are conscious to achieve green environment as per international standard till 2050.

The findings in Table 6 and Table 7 show the OLS results. When we adjusted the coefficients to control the bias due to the expected correlation between the time-invariant error term and independent variables, then results highlight that once percent improvement in environment management policies leads to reduce greenhouse gas emission about 0.35%. This indicates that the improvement in policy design and strict compliance of environment policies could play vital role to control the emissions of greenhouse gases (Grosse 2018). The general assumption is that the cross sections should be serially independent. Therefore, to check the cross-sectional independence, the Pesaran (CD) test is performed and results yielded that the test statics 0.883 with absolute value of diagonal elements is 0.634. It is important to mention that the proposed model has a time-invariant error term and that could be correlated with other exogenous variables. In that case, the result of coefficients of random effect could be biased to some degree. The findings endorsed the outcomes of Shahbaz et al. (2017) and Hammoudeh et al. (2013). Thus, the results suggested that in emerging economies NRE resources such as oil, gas, and coal are primarily consumed at macro and micro levels to fulfill energy needs. Therefore, it is expected that increase in pace of industrialization in the developing economies could lead to increase in usage of NER; as a result, the level of greenhouse gas emissions in developing Asian economies might be increased further.

One of the precise conducts to reduce carbon emissions is with storage and capture and it is considered as a considerable approach for assemble CO2 emission diminution aim. Consequently, region adopted environmentally friendly policy since 2001, to conserve and defend the environment of the country and natural resources which will not affect the economic other growth process of the country. The positive significant impact of energy consumption on economic growth recommend that energy consumption is vital for continuous economic growth, but the fast speed of CO2 emissions necessitate the adoption of alternative energy sources and advances to enlargement of environment protection in the environment. Energy intensive enterprises should be responsible to mitigation throughout the supply chain of energy enterprises. Meticulous ecological principles should strictly apply.

Figure 6 shows sector-wise percentage changes in energy consumption. In the turning point, βK is portrayed in the middle quartile pair which has 10% and 90% respectively. Positive βK values have been discovered in case of both countries, hence verifying the analysis of efficiency. Financing offers loans to household organizations, hence supporting the purchase of “big” products. Due to this, the usage of energy is enhanced. If we look at short-term dynamic investigation, findings portray that the present energy usage variations are positive and significant, impacted by the previous extent of the two countries. In the short-run of globalization, present and previous variations would not impact the present variations in energy usage. It is found that the present and previous variations in globalization would not significantly affect. Variations in present energy usage in both fields in most globalized nations. While negligible, the effect of globalization’s short-run implications on energy usage is negative.

Sector-wise percentage changes in energy consumption

Table 8 shows socio-economic indicator of BRICS region. In a similar manner, the global effect of BRICS can be predicted from the observation that these countries, when looked at cumulatively, employ 30% of the world’s land, depicting world’s 40% population, and are responsible for almost 50% of world’s GDP during the previous few decades. In spite of the unremarkable annual growth rate of 1.37% during 2017, after the previously GDP growth of − 3.5% during 2015 to 1.6% in 2016 (Zhang and Wang 2019), Brazil’s economy has portrayed an incredible recovery from three economic disturbances—the Eurozone crisis, commodity price dilemma, and financial decline. Russia has reclaimed the positive strength after GDP negative growth with − 7.8% during 2009 to a balanced GDP growth of 1.6% during 2017 (World Bank 2019) due to enhanced public purchasing power, improved trading climate, and balanced prices of energy; increased enhancements in growth of GDP in the forthcoming future continue to be arguable in light of the possible impact of deteriorating labor, building up currency, and balancing oil prices. However, every representative in the group possesses an abundant and unique share of resources, hence enhancing the total power and advancement possibilities of the entire group.

Figure 7 shows percentage change in energy consumption and the findings depict that the gross capital formation (GCF) has a significant and negative relationship with CO2 emissions. The GCF coefficient’s value is − 0.04 and significant at 1%, showing that a 1% enhancement in gross capital formation in emerging nations of OECD and BRICS has decreased the CO2 emission by 0.04%. Nevertheless, trade openness (TRD) possesses a negative sign, but statistically has an insignificant association with CO2 emissions. The long-term ARDL findings have depicted the significant relationship of gross capital formation, RE usage, and squared GDP growth to regulate the CO2 emissions in emerging countries of Silk Road Economic Belt. In addition, findings verify that, originally, the improvement in GDP growth enhances CO2 emissions, whereas after the turning point has been crossed, an enhancement in GDP (square term) reduces CO2 discharge.

Percentage changes in energy consumption

The impact of RE, NRE consumption and GDP growth on CO2 emissions is concluded in the short-term. The short-term findings depict that 91% of CO2 emissions in the present duration is linked with the CO2 discharge during the previous duration in the OECF and BRICS where OECD has driven the argument for a decrease in the greenhouse gas discharge globally, using international arbitration (The World Bank 2019). Being the early advocate of green improvement, OECD nations can be employed as an international benchmark for analysis. As an extension to fossil fuel energy (like natural gas, coal, and oil), renewable energy usage has improved. According to World Bank’s research, the moderate ratio of fossil fuel energy usage in OECD representatives is 80.7% during 2010, where the ratio is 94.4 in Australia, 84.2% in the USA, 79.6% in Germany, 49.8% in France, and 11.5% in Iceland, etc. Ultimately, the ECM model has been derived to discover the pace of improvement from the short-term to long-term predictions to obtain an equilibrium condition.

Findings represent the ecm(t − 1) are significant at 1%, while showing the negative symbol. In this case, negative symbol represents that the model converges having short- and long-run predictions with arithmetical consequence of ecm(t − 1) verifies the independent indicators combine to result in CO2 discharge in the area. More specifically, the findings depict that an 8% error would be adjusted yearly to achieve an equilibrium condition.

The results show pairwise dumitrescu hurlin panel causality tests. In addition, regression findings suggest that regression coefficient of R&D investment is significantly negative at a 1% level. R&D investment has a negative effect on carbon discharge. For every 1% improvement in R&D investment in total GDP, carbon discharge BRICS nations would be reduced by 0.8122%. In addition, regression coefficient of energy architecture is negative, denoting its negative effect on carbon discharge. If renewable energy usage is improved by 1%, carbon discharge will be reduced by 0.8122%. On the other hand, regression coefficient of industrial and urbanization structure is 0.7332 and 0.4067, showing a positive effect on carbon discharge. Each 1% enhancement in industrialization and urbanization will result in carbon discharge increasing by 0.7332% and 0.4067% respectively.

Table 9 shows the Westerlund error correction. The top five countries taking in discharge amongst BRICS economies were the USA (470 Mt), Italy (80 Mt), Germany (150 Mt), Japan (175 Mt), and UK (80 Mt). To decrease the discharge demonstrated in BRICS’ trade, the developed economies ought to be accountable for almost 66.66% of discharge demonstrated in businesses activities having the BRICS countries. Amongst BRICS countries, China being the biggest importer and exporter of emissions, it transmitted more than 1.4 Gt demonstrated carbon dioxide discharge to countries other than BRICS countries. In case of BRICS countries, the exported discharge is likely to be ruled by China, considering that China’s prominent trade collaborators, that is Japan (7%), USA (20%), and Germany (6%), likewise accounted amongst the higher 3 carbon dioxide importers amongst BRICS countries. Regarding the highest 3 carbon dioxide emitter for the BRICS countries, the USA (7%), Korea (7%), and Japan (5%) have too been prominent transaction collaborators with China. It is noteworthy that the findings in this research are in line with the recent evaluation performed by the OECD, along with other researches.

Conclusion and policy implication

The study employs the ARDL method to predict findings and has also implemented multiple statistical analysis to predict decisive and powerful findings. The associated amongst GDP growth, NRE and RE usage, and CO2 emissions for the OECD and BRICS countries have been examined by using data between 1980 to 2016. The long-term findings portray that the rise in GDP growth enhances CO2 emissions, hence verifying the EKC hypothesis amongst OECD and BRICS regions. In addition, the gross capital formation has also been seen valuable in decreasing the CO2 emissions in these countries, whereas it was discovered that NRE and GDP growth have been discovered as significant aspects of enhanced CO2 emission in the economies under consideration. The short-term findings have seen a rise in CO2 emission by NRE consumption while deteriorating in CO2 by use of RE. Hence, it can be derived that the OECD and BRICS regionsought to focus on RE resources to reduce the environmental dilemmas rising because of large CO2 emissions and various other greenhouse gases.

Using the scientific findings of this research, it can be derived that the change from NRE to RE origin is unavoidable to curb CO2 emissions and enhance the advantages of the SREB initiative. Our findings imply that energy usage is significantly associated with carbon discharge during the long-term for the two highest globalized areas (OECD and BRICS). Nevertheless, the findings also depict that the short-term impact of energy demand on energy usage is limitless and continues to be significant for these greatly globalized areas. This finding is compelling, since it shows that a single policy plan would not be neither constant nor universal across various countries and time, when taking into account nations with spiked extent of energy usage.

The scientific findings also depict that there are particular difficulties for policymakers in their quest of bringing about suitable environmental changes. The long-term effects of energy usage on carbon discharge and economic growth can possibly offset the appeal of short-run changes. Our findings do, in fact, reinforce this assumption. Hence, we recommend that environmental transformation ought to go on over a longer duration to achieve the anticipated results in the long-term. Although stimulating renewable resources in the energy mix has clear policy implications, in terms of applicability, dependence on fossil (non-renewable) energy remains an obstacle. This shows that the increase in renewable energy consumption under high carbon emission levels will have a reasonable impact on environmental degradation.

In addition, it is possible to conduct this research with other regions (such as the BRICS, the G7 or the next 11 countries) by introducing new and advanced econometric methods.

To promote the more and efficient use of renewable energy, government of such countries should make invest in the production advanced technologies and for such purpose, the responsibility of developed countries has been increased many folds to assess developing countries in the provision or accessing for new renewable technologies early and at affordable price.

It is also being noted that most of the developing countries are energy importer so the model of advanced countries’ transformation toward renewable energy production due to huge energy bills can be case study for such developing economies.

Data availability

The data that support the findings of this study are openly available on request.

References

Alemzero DA, Sun H, Mohsin M, Iqbal N, Nadeem M, Vo XV (2020) Assessing energy security in Africa based on multi-dimensional approach of principal composite analysis. Environ Sci Pollut Res. https://doi.org/10.1007/s11356-020-10554-0

Anser MK, Mohsin M, Abbas Q, Chaudhry IS (2020) Assessing the integration of solar power projects: SWOT-based AHP–F-TOPSIS case study of Turkey. Environ Sci Pollut Res 27:31737–31749. https://doi.org/10.1007/s11356-020-09092-6

Asbahi AAMHA, Gang FZ, Iqbal W et al (2019) Novel approach of principal component analysis method to assess the national energy performance via Energy Trilemma Index. Energy Rep 5:704–713. https://doi.org/10.1016/j.egyr.2019.06.009

Baloch ZA, Tan Q, Iqbal N, Mohsin M, Abbas Q, Iqbal W, Chaudhry IS (2020) Trilemma assessment of energy intensity, efficiency, and environmental index: evidence from BRICS countries. Environ Sci Pollut Res 27:34337–34347. https://doi.org/10.1007/s11356-020-09578-3

Chandio AA, Jiang Y, Rehman A, Twumasi MA, Pathan AG, Mohsin M (2020) Determinants of demand for credit by smallholder farmers’: a farm level analysis based on survey in Sindh. Pakistan J Asian Bus Econ Stud ahead-of-print. https://doi.org/10.1108/jabes-01-2020-0004

Chen JE, Hsiang CW (2019) Causal random forests model using instrumental variable quantile regression. Econometrics 7. https://doi.org/10.3390/econometrics7040049

Chiang HD, Sasaki Y (2019) Causal inference by quantile regression kink designs. J Econom 210:405–433. https://doi.org/10.1016/j.jeconom.2019.02.005

Cho JS, Kim TH, Shin Y (2015) Quantile cointegration in the autoregressive distributed-lag modeling framework. J Econom 188:281–300. https://doi.org/10.1016/j.jeconom.2015.05.003

Chow GC (2015) Environmental Kuznets curve. Economic Analysis of Environmental Problems, In, pp 159–167

Dinda S (2004) Environmental Kuznets curve hypothesis: a survey. Ecol Econ 49:431–455. https://doi.org/10.1016/j.ecolecon.2004.02.011

Farhani S (2013) Renewable energy consumption, economic growth and CO2 emissions: evidence from selected MENA countries. Energy Econ Lett 1:24–41

Firpo S, Galvao AF, Song S (2017) Measurement errors in quantile regression models. J Econom 198:146–164. https://doi.org/10.1016/j.jeconom.2017.02.002

Gasser P (2020) A review on energy security indices to compare country performances. Energy Policy 139:111339. https://doi.org/10.1016/j.enpol.2020.111339

Grosse M (2018) How user-innovators pave the way for a sustainable energy future: a study among German energy enthusiasts. Sustain 10. https://doi.org/10.3390/su10124836

Hammoudeh S, Nandha M, Yuan Y (2013) Applied economics dynamics of CDS spread indexes of US financial sectors dynamics of CDS spread indexes of US financial sectors. Appl Econ 45:213–223. https://doi.org/10.1080/00036846.2011.597727

Hanif I (2017) Economics-energy-environment nexus in Latin America and the Caribbean. Energy 141:170–178. https://doi.org/10.1016/j.energy.2017.09.054

He W, Abbas Q, Alharthi M, Mohsin M, Hanif I, Vinh Vo X, Taghizadeh-Hesary F (2020) Integration of renewable hydrogen in light-duty vehicle: nexus between energy security and low carbon emission resources. Int J Hydrog Energy 45:27958–27968. https://doi.org/10.1016/j.ijhydene.2020.06.177

Hsiao C (2005) Why panel data? Singapore Econ Rev 50(02):143–154

Iqbal W, Fatima A, Yumei H, Abbas Q, Iram R (2020) Oil supply risk and affecting parameters associated with oil supplementation and disruption J Clean Prod 255:. https://doi.org/10.1016/j.jclepro.2020.120187

Iram R, Zhang J, Erdogan S, Abbas Q, Mohsin M (2019) Economics of energy and environmental efficiency: evidence from OECD countries. Environ Sci Pollut Res 27:3858–3870. https://doi.org/10.1007/s11356-019-07020-x

Kazmi H, Mehmood F, Tao Z, Riaz Z, Driesen J (2019) Electricity load-shedding in Pakistan: unintended consequences, opportunities and policy recommendations. Energy Policy 128:411–417. https://doi.org/10.1016/j.enpol.2019.01.017

Khattak SI, Ahmad M, Khan ZU, Khan A (2020) Exploring the impact of innovation, renewable energy consumption, and income on CO2 emissions: new evidence from the BRICS economies. Environ Sci Pollut Res 27:13866–13881. https://doi.org/10.1007/s11356-020-07876-4

Kim KH (2013) Inference of the environmental Kuznets curve. Appl Econ Lett 20:119–122. https://doi.org/10.1080/13504851.2012.683163

Le TH, Chang Y, Taghizadeh-Hesary F, Yoshino N (2019) Energy insecurity in Asia: a multi-dimensional analysis. Econ Model 83:84–95. https://doi.org/10.1016/j.econmod.2019.09.036

Lee YY (2016) Interpretation and semiparametric efficiency in quantile regression under misspecification. Econometrics 4. https://doi.org/10.3390/econometrics4010002

Lin B, Benjamin NI (2017) Influencing factors on carbon emissions in China transport industry. A new evidence from quantile regression analysis J Clean Prod 150:175–187

Liu Y, Hao Y (2018) The dynamic links between CO2 emissions, energy consumption and economic development in the countries along “the Belt and Road.” Sci Total Environ 645:674–683. https://doi.org/10.1016/j.scitotenv.2018.07.062

Maulidia M, Dargusch P, Ashworth P, Ardiansyah F (2019) Rethinking renewable energy targets and electricity sector reform in Indonesia: a private sector perspective. Renew Sust Energ Rev 101:231–247

Mazur A, Phutkaradze Z, Phutkaradze J (2015) Economic growth and environmental quality in the European Union countries – is there evidence for the environmental Kuznets curve? Int J Manag Econ 45:108–126. https://doi.org/10.1515/ijme-2015-0018

McNown R, Sam CY, Goh SK (2018) Bootstrapping the autoregressive distributed lag test for cointegration. Appl Econ 50:1509–1521. https://doi.org/10.1080/00036846.2017.1366643

Mohsin M, Rasheed AK, Saidur R (2018a) Economic viability and production capacity of wind generated renewable hydrogen. Int J Hydrog Energy 43:2621–2630

Mohsin M, Zhou P, Iqbal N, Shah SAA (2018b) Assessing oil supply security of South Asia. Energy 155:438–447. https://doi.org/10.1016/j.energy.2018.04.116

Mohsin M, Abbas Q, Zhang J, Ikram M, Iqbal N (2019a) Integrated effect of energy consumption, economic development, and population growth on CO2 based environmental degradation: a case of transport sector. Environ Sci Pollut Res 26:32824–32835. https://doi.org/10.1007/s11356-019-06372-8

Mohsin M, Rasheed AK, Sun H, Zhang J, Iram R, Iqbal N, Abbas Q (2019b) Developing low carbon economies: an aggregated composite index based on carbon emissions. Sustain Energy Technol Assessments 35:365–374. https://doi.org/10.1016/j.seta.2019.08.003

Mohsin M, Zhang J, Saidur R, Sun H, Sait SM (2019c) Economic assessment and ranking of wind power potential using fuzzy-TOPSIS approach. Environ Sci Pollut Res 26:22494–22511. https://doi.org/10.1007/s11356-019-05564-6

Mohsin M, Nurunnabi M, Zhang J, Sun H, Iqbal N, Iram R, Abbas Q (2020a) The evaluation of efficiency and value addition of IFRS endorsement towards earnings timeliness disclosure. Int J Financ Econ. https://doi.org/10.1002/ijfe.1878

Mohsin M, Taghizadeh-Hesary F, Panthamit N, et al (2020b) Developing low carbon finance Index: Evidence From Developed and Developing Economies. Financ Res Lett. https://doi.org/10.1016/j.frl.2020.101520

Omri A (2013) CO2 emissions, energy consumption and economic growth nexus in MENA countries: evidence from simultaneous equations models. Energy Econ 40:657–664. https://doi.org/10.1016/j.eneco.2013.09.003

Ozcan B, Ozturk I (2019) Renewable energy consumption-economic growth nexus in emerging countries: a bootstrap panel causality test. Renew Sust Energ Rev 104:30–37. https://doi.org/10.1016/j.rser.2019.01.020

Raza SA, Shah N, Sharif A (2019) Time frequency relationship between energy consumption, economic growth and environmental degradation in the United States: evidence from transportation sector. Energy 706–720. https://doi.org/10.1016/j.energy.2019.01.077

Salim R, Rafiq S, Shafiei S, Yao Y (2019) Does urbanization increase pollutant emission and energy intensity? Evidence from some Asian developing economies. Appl Econ 51:4008–4024. https://doi.org/10.1080/00036846.2019.1588947

Sarkodie SA, Adams S (2018) Renewable energy, nuclear energy, and environmental pollution: accounting for political institutional quality in South Africa. Sci Total Environ 643:1590–1601. https://doi.org/10.1016/j.scitotenv.2018.06.320

Sghari MBA, Hammami S (2016) Energy, pollution, and economic development in Tunisia. Energy Rep 2:35–39. https://doi.org/10.1016/j.egyr.2016.01.001

Shah SAA, Zhou P, Walasai GD, Mohsin M (2019) Energy security and environmental sustainability index of south Asian countries: a composite index approach. Ecol Indic 106:105507. https://doi.org/10.1016/j.ecolind.2019.105507

Shahbaz M, Sinha A (2019) Environmental Kuznets curve for CO2 emissions: a literature survey. J Econ Stud 46:106–168

Shahbaz M, Lean HH, Shabbir MS (2012) Environmental Kuznets curve hypothesis in Pakistan: Cointegration and Granger causality. Renew Sust Energ Rev 16:2947–2953

Shahbaz M, Solarin SA, Hammoudeh S, Shahzad SJH (2017) Bounds testing approach to analyzing the environment Kuznets curve hypothesis with structural beaks: the role of biomass energy consumption in the United States. Energy Econ 68:548–565. https://doi.org/10.1016/j.eneco.2017.10.004

Sinha A, Shahbaz M (2018) Estimation of environmental Kuznets curve for CO2 emission: role of renewable energy generation in India. Renew Energy 119:703–711. https://doi.org/10.1016/j.renene.2017.12.058

Sobhee SK (2004) The environmental Kuznets curve (EKC): a logistic curve? Appl Econ Lett 11:449–452. https://doi.org/10.1080/1350485042000207216

Sun H, Ikram M, Mohsin M, Abbas Q (2019a) Energy security and environmental efficiency: evidence from OECD countries. Singapore Econ Rev:1943003. https://doi.org/10.1142/S0217590819430033

Sun HP, Tariq G, Haris M, Mohsin M (2019b) Evaluating the environmental effects of economic openness: evidence from SAARC countries. Environ Sci Pollut Res 26:24542–24551. https://doi.org/10.1007/s11356-019-05750-6

Sun H, Mohsin M, Alharthi M, Abbas Q (2020a) Measuring environmental sustainability performance of South Asia. J Clean Prod 251:119519. https://doi.org/10.1016/j.jclepro.2019.119519

Sun H, Pofoura AK, Adjei Mensah I, Li L, Mohsin M (2020b) The role of environmental entrepreneurship for sustainable development: evidence from 35 countries in sub-Saharan Africa. Sci Total Environ 741:140132. https://doi.org/10.1016/j.scitotenv.2020.140132

Sun L, Cao X, Alharthi M, Zhang J, Taghizadeh-Hesary F, Mohsin M (2020c) Carbon emission transfer strategies in supply chain with lag time of emission reduction technologies and low-carbon preference of consumers. J Clean Prod 264:121664. https://doi.org/10.1016/j.jclepro.2020.121664

Sun L, Qin L, Taghizadeh-Hesary F, Zhang J, Mohsin M, Chaudhry IS (2020d) Analyzing carbon emission transfer network structure among provinces in China: new evidence from social network analysis. Environ Sci Pollut Res 27:23281–23300. https://doi.org/10.1007/s11356-020-08911-0

Tang CF, Abosedra S (2014) The impacts of tourism, energy consumption and political instability on economic growth in the MENA countries. Energy Policy 68:458–464. https://doi.org/10.1016/j.enpol.2014.01.004

The World Bank (2019) Record high remittances sent globally in 2018. In: Foreign Aff

Trotta G (2020) Assessing energy efficiency improvements and related energy security and climate benefits in Finland: An ex post multi-sectoral decomposition analysis Energy Econ 86:. https://doi.org/10.1016/j.eneco.2019.104640

Tsaurai K, Ngcobo L (2020) Renewable energy consumption, education and economic growth in Brazil, Russia, India, China, South Africa. Int J Energy Econ Policy 10:26–34. https://doi.org/10.32479/ijeep.8497

Usenata N (2018) Environmental Kuznets curve (EKC): a review of theoretical and empirical literature. IDEAS Work Pap Ser from RePEc

Waluyo EA, Terawaki T (2016) Environmental kuznets curve for deforestation in Indonesia: an ARDL bounds testing approach. J Econ Coop Dev 37:87–108

World Bank (2019) Global Investment Competitiveness Report 2019–2020

Zafar MW, Mirza FM, Zaidi SAH, Hou F (2019) The nexus of renewable and nonrenewable energy consumption, trade openness, and CO2 emissions in the framework of EKC: evidence from emerging economies. Environ Sci Pollut Res Int 26:15162–15173. https://doi.org/10.1007/s11356-019-04912-w

Zambrano-Monserrate MA, Carvajal-Lara C, Urgiles-Sanchez R (2018) Is there an inverted U-shaped curve? Empirical analysis of the environmental Kuznets curve in Singapore*. Asia-Pacific J Account Econ 25:145–162. https://doi.org/10.1080/16081625.2016.1245625

Zhang YJ, Wang W (2019) Do renewable energy consumption and service industry development contribute to CO2 emissions reduction in BRICS countries? Environ Sci Pollut Res 26:31632–31643. https://doi.org/10.1007/s11356-019-06330-4

Zhang Y, Shen L, Shuai C, Tan Y, Ren Y, Wu Y (2019) Is the low-carbon economy efficient in terms of sustainable development? A global perspective. Sustain Dev 27:130–152. https://doi.org/10.1002/sd.1884

Zheng W, Walsh PP (2019) Economic growth, urbanization and energy consumption — a provincial level analysis of China. Energy Econ 80:153–162. https://doi.org/10.1016/j.eneco.2019.01.004

Author information

Authors and Affiliations

Contributions

Muhammad Atif Nawaz: conceptualization, data curation, methodology, writing—original draft. Muhammad Sajjad Hussain: data curation, visualization. Hafiz Waqas Kamran: visualization, supervision, editing. Syed Ehsanullah: review and editing. Rida Maheen: writing—review and editing and software. Faluk Shair: writing—review and editing.

Corresponding author

Ethics declarations

Conflict of interest

The authors declare that there is no conflict of interest.

Ethical approval and consent to participate

The authors declare that they have no known competing financial interests or personal relationships that seem to affect the work reported in this article. We declare that we have no human participants, human data, or human tissues.

Consent for publication

We do not have any individual person’s data in any form.

Additional information

Responsible Editor: Roula Inglesi-Lotz

Publisher’s note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

About this article

Cite this article

Nawaz, M.A., Hussain, M.S., Kamran, H.W. et al. Trilemma association of energy consumption, carbon emission, and economic growth of BRICS and OECD regions: quantile regression estimation. Environ Sci Pollut Res 28, 16014–16028 (2021). https://doi.org/10.1007/s11356-020-11823-8

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11356-020-11823-8