Abstract

Italian health care expenditure (HCE) has been basically explained with two main groups of theories. (1) Those explaining the peculiarity of the HCE growth as depending on demand and supply factors, such as aging population, number of practising physicians per capita, mix of public and private hospitals, number of hospital beds,… (2) Those explaining the growth of total public expenditure as a common feature among industrialized countries, with a huge empirical literature emphasising the role of GDP and/or other structural/institutional variables as the main determinants of HCE across countries. In order to reassess previous findings, we exploit recent results on panel cointegration analysis and test the regional Italian data on HCE and GDP, also taking into account cross-section correlation. The results show that HCE and GDP are cointegrated. The long- and short-term dynamics of HCE are estimated. Our results, providing an empirical support for the existence of Wagner’s law, have important policy implications in terms of fiscal sustainability: as income rises, people will choose relatively more HCE. Given the level of the public debt in Italy, any further increases would imply that future government spending may be mainly directed toward debt servicing, likely at the expense of public expenditure on basic infrastructure.

Similar content being viewed by others

Explore related subjects

Discover the latest articles, news and stories from top researchers in related subjects.Avoid common mistakes on your manuscript.

1 Introduction

We exploit recent results on panel cointegration analysis to empirically study the determinants of (per-capita) health care expenditure (HCE) in the Italian regions in both the long and short term. We show that the long-term behaviour of HCE is mainly explained by GDP, whereas political and institutional variables shape the regions’ HCE dynamics in the short term.

The relationship between HCE and GDP has been the subject of a large portion of literature in health economics. Many early contributions employed cross sectional data to obtain estimates of this relationship, amongst others Gerdtham–Jönsson (2000), Gerdtham–Lothgren (2000), for OECD countries; Giannoni–Hitiris (2002), for the Italian case. Without exception, it has been found that most of the observed variations in HCE can be (also) explained by variation in GDP. Culyer (1988) noticed that these models are probably mis-specified, because they do not consider the public budget mechanism used to finance health care.Footnote 1 In explaining the evolution of health care, issues relating to budgetary processes and institutions, including the current decentralisation process in Europe (in countries such as France, Spain, Belgium) should, however, be accompanied by a careful analysis of what the data are actually saying.

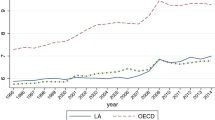

With this purpose, we first consider the behaviour of the HCE and GDP (per capita), both at constant 2005 pricesFootnote 2 and transformed into logarithms, in the 20 Italian regions, from 1982 to 2009. The visual inspection (Fig. 1) shows an impressively similar behaviour of HCE and GDP which, like many other economic variables, exhibit strong comovements across Italian regions. Moreover, the Granger causality test on the considered variables rejects the hypothesis that GDP does not Granger cause HCE (see “Appendix 1”). This seems to support the view that GDP is actually driving HCE. Apparently, after the health care reform of 1978, Italy established a health care system based on the economic development of the country with a continuous upward trend observed in public HCE.

Behaviour of per capita HCE and GDP in the Italian regions (1982–2009)

In contexts like these, resorting to panel data offers a number of advantages for the analysis. In this respect, a number of articles studying the behaviour of HCE in OECD countries support the view of a positive association between HCE and GDP.Footnote 3 Here on the basis of a newly built panel data set consisting of all the 20 Italian regions and covering the period 1982–2009, we verify the hypothesis of cointegration between HCE and GDP.Footnote 4 We show the existence of a long-run equilibrium relationship between HCE and GDP.

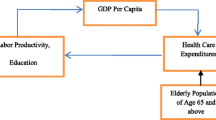

In addition, we model the short-term behaviour of HCE. In this respect, we postulate the presence of short-term factors that might affect the HCE annual dynamics. In particular, we investigate whether those variables that have been traditionally credited to influence the HCE can find room in a short-term relationship. In modelling the short term, we refer to those theories explaining the peculiarity of the growth of the HCE as depending on demand and supply factors as well as on economic, political and institutional features of industrialised countries. On the one side, we refer to the body of empirical literature examining the traditional determinants of HCE, namely: per-capita GDP, proportion of population over 65 and under 5, migration rate, public finance share of health care spending, urbanization, unemployment rate, activity rate and number of practising physicians per capita (see, for example, Newhouse 1977; Leu 1986; Gerdtham et al. 1992; Hitiris–Posnett 1992; Gerdtham et al. 1998; Barros 1998; Di Matteo–Di Matteo 1998; Crivelli et al. 2006). On the other side, we refer to the recent debate in a political economy approach relating public expenditure growth to the role played by political and institutional elements as determinants (principal or secondary) of public expenditure (see Persson–Tabellini 1999, 2000, 2001, 2005; Milesi-Ferretti et al. 2002). These elements are the ones more frequently studied in the most recent (empirical and theoretical) literature, with different approaches to the context of the HCE. For example, Crivelli et al.(2006) apply the determinants approach to the Swiss cantons considering among the independent variables the cantonal index for direct democracy discussed by Trechsel–Serdult (1999) and Frey–Stutzer (2000); whereas Vatter–Ruefli (2003) present a comparative study of Swiss cantons investigating the role of specific political factors on HCE. In this paper we want to explore whether any role has been played by the factors mentioned above on choices relating to the health care system in Italy, at least in the short term.

Our finding seems to support those theories that consider public HCE growth inevitable, as it is determined by changes in the economic and social structure. On the one side, the so called “Wagner’s law”Footnote 5 seems to be confirmed in that economic and social progress implies an increase of government expenditures (here for health) proportional to the national product.Footnote 6 We refer to the literature originated by Wagner hypothesis—for example, the works by Peacock–Wiseman (1961), Timm (1961), Gupta (1967), Pryor (1969), Musgrave (1969), Alt (1980), Mann (1980) and Henrekson (1993), see the discussion below—and also to the health care literature, for example Newhouse (1992), explaining the raise in health spending with the relevance of technological progress, and the adoption of new, more expensive medical treatments. On the other side, our empirical results also confirm the view (Hall–Jones 2004) that health care is a superior good because as individuals get richer they choose to spend a larger proportion of their income on health care, with policy-makers merely adjusting public health spending to individual preferences, likely for electoral reasons.

The main implication of our finding is in term of fiscal sustainability. Indeed, the public debt in Italy stands at about 133 % of GDP (est. 2013), and any further increases of current expenditures would imply that future government spending may be mainly directed toward debt servicing.

In Sect. 2 we briefly describe the Italian health care system. In Sect. 3 we assess the model and depict the data. Section 4 reports the empirical results. Conclusions follow in Sect. 5.

2 The Italian National Health Care System

The Italian National Health Care System (NHS), founded in 1978, is a universal health care system that provides comprehensive health insurance coverage and uniform health benefits to the whole population, subject to user charges for certain services. The system, now organized according to three-level government structure (national, regional, and municipal), was originally highly centralized. An increased degree of decentralization for hospital care had already begun in 1972 when the administrative functions for hospital care assistance were transferred to regions with an ordinary bylaw. The state was left with residual competences, mainly related to fund rising. In 1978 an extended regionalization (and a strengthened role of municipalities) of the expenditures responsibilities became a key feature of the whole Italian health care system characterised as follows. Primary care in Italy is provided mostly by general practitioners who refer patients to specialist care and hospitals on a regional basis. They are independent self-employed practitioners paid on a capitation basis.Footnote 7 Ambulatory treatments, diagnostic and laboratory tests, specialist care, drugs, medical appliances and glasses are co-paid by patients at a price called ticket, determined according to income, age, health conditions and other individual characteristics. It is also possible for the regional government to outsource the delivery of medical health services. As a result, part of health care services is currently provided by accredited private units, with patients free to choose between public or private providers.Footnote 8

As mentioned, since 1978, the amount of funds financing the NHS has been fixed by the central government which determines the resources available for HCEs on a regional basis. The separation of revenue raising responsibilities of the central government and expenditure responsibilities of the regional governments, resulted in continuous increases of the Italian public HCEs, with Regions regularly running budget deficits determining large regional debts, subsequently repaid by the central government. This has led to periodic attempts of reforming the NHS financing mechanisms, with the main source of financing remaining public. In this respect three periods seem relevant. The first period 1978–1992 is characterised by the full financing of HCE by means of the National Health Fund, NHF, originating from general tax revenues with constrained destination to health care financing. In the second period, from 1993 to 1997, a mixed mechanism of financing was introduced, with the NHF having an apparent complementary role to the revenues deriving from health care social contributions levying on dependent labour income.Footnote 9 In the third period, from 1998 on, health care social contributions were substituted by a regional tax on production activities, by a regional surtax on personal income, by revenue sharing of the VAT revenue and excise duty on petrol. Apparently, regions have to rely on regional taxes for funding both health care and other regionally funded activities.Footnote 10 Nevertheless, the devised measures have not been sufficient to contrast the massive debt overhang originated by the health care system, with the consequence of increasingly serious problems of fiscal sustainability for the state (see Fedeli 2008). In this respect, it should be noted that regional differences in public finances also suggested the use of specific policies to solve specific situations of crisis: since 2007 for those regions under risk of financial default due to indebtedness originated by the health care system a policy of Repayment Plans (Piani di Rientro) begun with the following features.Footnote 11 The Plan is setup and agreed upon amongst the Region presenting structural health deficit, the Ministry of Health, and the Ministry of Economic and Finance. The plan outlines objectives and strategies to recover the financial equilibrium (recovery plan) and to remove the structural determinants of disequilibrium by means of targeted actions against the structural determinants of health deficits (turnaround plan) still keeping a given quality of assistance levels.Footnote 12 As we shall see below none of these policy action has had any effect in shaping the HCE.

3 The Model and the Data

The empirical analysis of long-run relationships among integrated variables with both a cross sectional dimension, N, and a time-series dimension, T, by means of panel cointegration techniques has been developed in two broad directions. On the one side, the approach mainly explored by Pedroni (1999, 2004) is based on the methodology of Engle and Granger (1987) whereby the residuals of a static least squares regression are subject to a unit root test. On this basis, however, some studies have failed to reject the no-cointegration null hypothesis even in cases where cointegration is strongly suggested by theory.Footnote 13 On the other side, Westerlund (2005, 2007) has recently developed new panel cointegration tests based on structural rather than residual dynamics (see below). The asymptotic results reveal that such tests have limiting normal distributions, and that they are consistent. Westerlund (2007) reports simulation evidence suggesting that the new tests maintain good size accuracy, and that they are more powerful than the residual based tests by Pedroni (2004). On this basis, we shall analyze the influence of per capita Italian regional GDP on per capita Italian regional HCE.

Notice here that the existence of a positive association between income and health care has been often established for OECD countries,Footnote 14 whereas some controversy remains on the direction of causality. Does the relation stem from health affecting individual working opportunities—and hence income—or from income providing a protective effect on health? A broad overview of the existing literature suggests that both directions of causality are indeed at work (see Smith 1999) and this is also the results suggested by the Granger causality test reported in “Appendix 1”. For this reason, we have also tested for cointegration the inverse relation of HCE on GDP again using the Westerlund tests above mentioned. In this case, however, cointegration is not supported by the Italian data (see “Appendix 2”). Thus, we concentrate on the impact of income on health expenditures only.

The basic model we postulate between HCE and GDP is the following:

where i = 1, …, 20 identifies the regions; t = 1982, …, 2009 identifies the years. Both HCE_PCit and GDP_PCit are per capita measures of, respectively, the regional HCEs and the regional GDP, both at constant 2005 prices and taken in logarithms. The time trend, t, to be tested, has been included. The interpretation of such a trend, if significant, would be that it captures the impact of technological change. \(\mu_{i}\) is the region specific effect, ɛ it represents the regression error.

The setting of Eq. (1), can be modified if accounting for cross-section dependence in the data. This can be generated by unobserved factors affecting all regions, but to a different degree. The model can be described as follows:

where f and g are unobserved factors (most likely, common shocks) affecting directly or indirectly [i.e. impacting on ln (GDP_PC) it ] the ln (HCE_PC) it . \(\, \varphi_{{i^{{^{{}} }} }}\) and \(\, ^{{^{{}} }} \psi_{i}^{{}}\) are the region specific factor loads which cause a heterogeneous response to common shocks.

If the variables in Eq. (1) [and (2)] are I(1) and cointegrated, the error term is I(0) process for all i. The principal feature of cointegrated variables is their responsiveness to any deviation from the long-run equilibrium. This implies an error correction model, in which the short-term dynamics of the variables in the system are influenced by the deviation from the equilibrium. As for the short-term, we postulate the dynamic panel specification as follows:

Φ i is the error-correction speed of adjustment parameter, which is expected to be significantly negative if the variables exhibit a return to the long-run equilibrium, whereas if it is zero there would be no evidence for a long-run relationship.

\(\theta {\text{s }}\) are the long-run coefficients, which give the long-run relationship between the variables as from Eq. (1) [and (2)]. With the inclusion of \(\theta_{0i} \,\) a nonzero mean of the cointegrating relationship is allowed.

\({\text{X}}_{\text{it }} \,\) is a vector of explanatory stationary variables entering the dynamic specification and \(\delta {\text{s }}\) are the corresponding coefficients. In this respect, we test the variables that are traditionally credited to influence the HCE. In particular, we take into consideration the traditional structural, socio-economic and demographic characteristics by evaluating, in turn, the significance of: aging population (i.e. the proportion of people over 65 in each region) that has been often identified as the major culprit of the raise in public health care spending (see Bethencourt–Galasso 2008); the regional net migration rate; labour market indicators such as unemployment rate and activity rate; the number of public hospital beds; the density of hospital doctors and general practitioners; the number of public and private hospitals. Footnote 15 Following Culyer (1988) three variables—CGP(82–92), CGP(93–97), CGP(98–09)—capturing homogeneous periods of central government budget policies for health-care public finances are considered; they refer to the central government fiscal reforms, respectively, of the periods 1982–1992, 1993–1997, 1998–2009.Footnote 16 We also consider the specific policies known as “repayments plans” addressed to those regions under the risk of financial default in the period considered—i.e. Abruzzo, Calabria, Campania, Latium, Liguria, Molise. Finally, following the political economy approach—in particular, Weingast et al. (1981), Tornell–Velasco (1992), Chari–Cole (1995), Persson–Tabellini (1999, 2000, 2001, 2005) and Milesi-Ferretti et al. (2002), but also Roubini–Sachs (1988, 1989), Lijphart (1984, 1994), Santagata (1995), Grofman (2001), Grilli et al. (1991)—we test a set of political and institutional variables, defined as follows: (1) the type of electoral system under which the regional government was elected is considered by means of the variable electoral_law, which takes on a value of 0 under the proportional system and a value of 1 under the plurality system. The regional electoral system changed from proportional to mixed plurality in 1994. (2) In 1999, the direct election of the president of the region, who becomes formally and substantially responsible for regional administration, was introduced for all Italian regions with ordinary bylaw (in 2001 for regions with extraordinary bylaw). The rationale of this institutional reform was to give direct administrative responsibility to the regional presidents as a measure aimed at curbing both deficits and expenditures. We capture the change in the electoral law related to the election of the president of the region by means of the variable president_election which takes on value 1 since the year when direct election was introduced. (3) The test has also been carried out considering the “political colours” of regional ruling coalitions over the period. In this respect, a variable depicting the centre-left ruling party coalitions over time has been considered. (4) Political and local elections are captured by the variable election, which takes on value 1 for the years of political and local elections and 0 otherwise. As for the impact of this variable on HCE, the theory says that under the proportional system the “universal” type of expenditure such as HCE should be higher than under the plurality system, which, in principle, favours those kind of expenditures addressed toward specific objectives (likely in favours of the electoral district or of specific interest groups supporting the political campaign of the elected representatives), see Persson and Tabellini (1999, 2000, 2001). In the same vein, Milesi-Ferretti et al. (2002) support the view that the more proportional the electoral system the wider variety of interests shall be accomplished, the more the electoral system stick to the single-member constituency the more the public expenditures shall accomplish local interests. By analogous reasoning, we should expect that after the introduction of the direct election of the president of the region, who becomes formally and substantially responsible for regional administration whose main duty is related to health care, the president himself is in the position to curb HCE, which is the main cause of regional deficits. As for the political colour of the regional ruling coalitions, at least for the Italian experience, we might expect left-wing ruling party coalition pay more attention to the health care system. Finally, in line with those theories of the electoral cycle, we would expect an increase of HCE in the proximity of both political and local election years (for the Italian case see Santagata 1995).

The dataset is a yearly panel data for all the 20 Italian regions for the period 1982–2009. The statistics of the considered variables are summarized in Table 1. Our source of data for structural health-care, economic and demographic characteristics is the Italian National Statistical Office (ISTAT), while the source of political and institutional variables is the Italian Ministry of Internal Affairs.

4 Empirical Results

We test for cointegration the model depicted in Sect. 3. We, first, assume cross-section independence in the data. As a robustness check, we, then, test for the presence of cross-section dependence. In both cases, we analyse the long- and short-term relations. The results obtained in either case provide evidence in favour of our specification. We report only the results which are significant for our analysis; full results are available from authors upon request.

4.1 Absence of Cross-Section Dependency

The first step is to test whether the variables are nonstationary or not. Dealing with longitudinal data, we refer to the test by Im et al. (2003), which is based on the assumption of no cross-sectional dependence. The results, reported in Table 2, indicate that, as for ln_HCE_PC, we reject the null hypothesis at the 1 % level of significance for a number of lags going from 1 to 6, whereas for ln_GDP_PC, once a linear time trend has been accommodated, we end up with a rejection of the null hypothesis at the 1 % level of significance for a number of lags going from 1 to 6 (in Table 2 we have marked in italicised values the statistics that accept the null hypothesis).Footnote 17

The second step is to test whether HCE_PC and GDP_PC are cointegrated. As already mentioned, we refer to Westerlund (2005, 2007) and Persyn–Westerlund (2008). Their idea is to test the null hypothesis of no cointegration by inferring whether the error-correction term in a conditional panel error-correction model is equal to zero. The four tests are all normally distributed and are general enough to accommodate unit-specific short-run dynamics, unit-specific trend and slope parameters, and cross-sectional dependence. Two tests are designed to test the alternative hypothesis that the panel is cointegrated as a whole, while the other two test the alternative that at least one unit is cointegrated. The calculated values of the error correction statistics are presented along with asymptotic p values in Table 3. When using the asymptotic p values, for both the cases in which the deterministic chosen is constant only and constant and trend, all four tests lead to a clear rejection of the null hypothesis at 1 % level, which we take as strong evidence in favour of cointegration between ln_HCE_PC and ln_GDP_PC.

As for the estimation of the cointegrating vector and the short-term dynamics, the recent literature has suggested several approaches. Table 4 reports the estimation results in three cases, i.e. (1) In Dynamic Fixed Effects Regression model (DFE), we restrict the coefficients of the cointegrating vector to be equal across all panels; moreover, DFE further restrict the speed of adjustment coefficient and the short-term coefficient to be equal.Footnote 18 (2) The mean group estimates (MG) are the unweighted mean of the N individual regression coefficients. They are calculated, as proposed by Pesaran–Smith (1995), with intercepts, slopes, coefficients and error variances allowed to be different across groups. Here they are reported as a two equation models. The full model estimates are available from authors on request. (3) The pooled mean group estimation (PMG) proposed by Pesaran et al. (1997, 1999) allows for heterogeneous short-term dynamics and common long-run effects of GDP. The long-run effects and the averaged short-run parameter estimates are reported in Table 4, the full estimates of a N + 1 multiple equation model are available from authors on request.

In either case the output is divided into two equations: the first, labelled EC, shows the long-run equation; the second, labelled SR, shows the short-term dynamics of the ln_HCE_PC. The SR equation, in either case, has been obtained by testing separately groups of variables mentioned before (i.e. the traditional determinants, budget policy variables, political and institutional variables). In either case the variables which turn out to be significant are always the same, as reported in the specifications of the model in Table 4.

First, notice that, as for the long-run equation, in all cases, the estimated coefficient for ln_GDP_PC is significantly positive. Moreover, the time trend is never significant in the long term equation. This is quite interesting because the time trend has been commonly interpreted as the impact of technological progress on health spending. In this respect, the health care literature has emphasized the relevance of technological progress, and the adoption of new, more expensive medical treatments to explain the raise in health spending (see Newhouse 1992). Apparently, these new technologies are not so massively used in Italy.

The different estimation methods provide estimated coefficients not always so close to each other. As explained above, their main difference concerns assumptions on coefficients, with the DFE—at one extreme—imposing more restrictions, and the MG estimation representing the most flexible specification and allowing even slope coefficients to vary across countries. Comparing DFE, MG and PMG estimations, it turns out that the long-run GDP elasticity from DFE is about 0.94, the one from MG is about 0.92, and that from PMG is 1.596. The PMG constrains the long-run elasticities to be equal across regions, and this pooling across region gives efficient and consistent estimates when the restrictions are true. If the hypothesis of slope homogeneity is not true, i.e. the true model is heterogeneous, the PMG estimates are inconsistent, whereas the MG are consistent in either case.Footnote 19 Second, notice that in the short-run equation of all the estimated models, D1.ln_GDP_PC (GDP rate of growth) is significant and positive whereas D2.ln_GDP_PC (the variation of the rate of growth) is significant and negative. These results support the view that an increase of GDP increases HCE in both the long and the short-term (in the SR at a decreasing rate). Moreover, this seems to confirm the “Wagner law” also in the short term.

In the short-term, the effect of the estimated cointegrating vector (i.e. the ec term) is significant and negative, as expected, in all the three cases. The coefficients of the dynamics and the speed of adjustment terms are very similar in size, implying a slightly different short-term dynamics. Moreover, ln_HCE_PC is shown to be affected by the variable election, which captures both political and local elections. The variable president_election, which considers the introduction in the system of the direct election of the president of the region, is significant with positive value. The political colour of the regional ruling coalition is not significant and the same is true for those variables capturing the electoral system and the central government policies addressed both to all region and to specific regions by means of “repayment plans”.

Interesting enough is the result that the variable aging population is not significant in the short term. Analyzing the political support to social security and medicare, Bohn (1999) forecasts a further increase in spending driven by the change in the age profile of the electors. This, however, does not seem to be that case in Italy.

In Table 5, we test the difference in these models with the Hausman test (see Baum et al. 2003).

The calculated Hausman statistic for MG versus PMG is 9.48. Being distributed as χ2(2), it leads to conclude that, under the null hypothesis, MG is preferred. The DFE model is subject to a simultaneous equation bias from the endogeneity between the error term and the lagged dependent variable (see Baltagi et al. 2000). In order to measure the extent of this endogeneity we again perform the Hausman test of DFE versus MG. The results indicate that the simultaneous equation bias is minimal for these data and therefore the DFE is preferred over MG. We further perform the Hausman test of PMG versus DFE. The calculated Hausman statistic is 0.06, indicating that the DFE is also preferred over PMG.

The first insight we gather from the above tables is that the Hausman test has provided some evidence in favor of the DFE estimation strategy. In addition, the usage of three different estimators provides indications on the specification of the cointegrating vector. The results are robust in that the sign of the long-term variables coefficients are always confirmed, only their size is, in one case, affected by the estimation method. Before adding further comments on the estimated coefficients, in the next section we perform a robusteness check of our approach considering the issue of cross section dependence.

4.2 Presence of Cross-Section Dependency

The presence of cross-section dependency within the framework of our dataset is highly likely. In this context, this correlation can be the result of local spillover effects between regions.Footnote 20 We investigate this issue by implementing the most commonly used CD-test for cross section dependency (Pesaran 2003, 2004). In Table 6, the CD-tests reject the null hypothesis of cross-section independency. We therefore proceed by repeating the sequence of tests described in previous section—i.e. testing for unit root and for the presence of cointegration, and finally estimating cointegrating relationships—but allowing for cross section dependence.

We first run the t test for unit roots in heterogenous panels with cross-section dependence, proposed by Pesaran (2003).Footnote 21 We investigated results for a number of lags spanning from 1 to 6. The vast majority of the statistics, reported in Table 7, confirmed the nonstationarity. Only those statistics which have been highlighted in italicised values provide a different outcome.

The results obtained require a further test to confirm that the variables are still cointegrated. Following Westerlund (2005, 2007) and Persyn and Westerlund (2008), we assume their same data generating process for their error correction test, and test for cross sectional independence in its residuals by means of the Breusch–Pagan statistic. In this respect, notice that this test requires T > N, which is our case. However, as our time series are rather short, given that some periods are lost in the calculation of differenced variables and lags, we test for independence of the first 12 cross-sectional units and assume the same short-run dynamics for all series. As for the relation between ln_H_PC, and ln_GDP_PC, the Breusch–Pagan LM test of independence gives χ2(55) = 155.662 (Pr = 0.0000). As this result strongly indicates the presence of common factors affecting the cross sectional units, we bootstrapped robust critical values for the test statistics related to the Westerlund ECM panel cointegration tests, keeping the short-term dynamics fixed. Table 8 shows that, when taking into account cross-sectional dependency, the tests still reject the null hypothesis of no cointegration.

On these bases, we evaluate if the presence of cross section correlation changes at all the results when estimating the cointegration vector. The long-run coefficients estimated by means of the augmented mean group estimator (AMG), developed in Eberhardt–Teal (2010) (see also Bond–Eberhardt 2009), are reported in Table 9. The results of the AMG estimator provide evidence in favour of our specification in the absence of cross section correlation. Again, the time trend, which is often interpreted as capturing technological changes, does not turn out to be significant, whereas the ln_GDP_PC is still significant and correctly signed. Interestingly, its size is smaller than that resulting from all three models in Table 4, although we again find that the elasticity is greater than zero. The magnitudes of income elasticity equal to 0.18 imply that a 1 % increase in per capita income leads to an increase in the share of government spending for health of about 0.18 %. This result still supports Wagner’s law.Footnote 22 In this respect, also the view that health care is a superior good as suggested by Hall–Jones (2004) seems to be confirmed: as individuals get richer they choose to spend a larger proportion of their income on health care. Likely for electoral reasons (see below), policy-makers adjust public health spending to individual preferences.

We can now move on to achieve an error correction representation as we did in the case of absence of cross section correlation. We now impose the long-term specification, K, estimated in Table 9 with the AMG estimator.Footnote 23 Table 10 reports the MG results after averaging the short-term parameter estimates.Footnote 24 This is of some help for a comparison with the results of Table 4. (The full estimates are available from authors on request).

The results are markedly aligned with those presented in previous section (Table 4). Again, the effect of the estimated cointegrating vector (the ec term) is significant and negative, as expected. The coefficients of the dynamics and the speed of adjustment terms are very similar in size to the DFE specification. Still, this result supports the view that an increase of GDP increases HCE in both the long and the short term and seems to confirm those theories according to which public HCE growth is determined by changes of the economic and social structure. As before, in the short term the variable election is significant, confirming that during electoral years there is an increase of HCE. The variable president_election, which considers the introduction in the system of the direct election of the president of the region, takes on positive value, whereas the political colour of the regional ruling coalition is again not significant. This confirms that the role of the president of the region has really changed, acquiring greater power with respect to that of political parties. The variables capturing central government budget policies addressed both to all regions and to specific regions by means of Repayment Plans are never significant, confirming that the impact of policies aiming at controlling health care costs were not even effective in the short-term just like the changes in the electoral system.

5 Summary of results and conclusions

Hall and Jones (2004) argue that health care is a superior good, because, as individuals get richer, they choose to spend a larger proportion of their income on health care. In the Italian public health care system, this might mean that policy-makers are merely adjusting public health spending to the electorate’s wishes. Our empirical results confirm these findings.

In particular, with a panel of all the 20 Italian regions (1982–2009), we investigated the long-run relationship between HCE and GDP. Moreover, we tested for the short-term behaviour of HCE, controlling for additional structural variables which have been credited to affect it, namely, the traditional determinants of health expenditure, and the political and institutional features likely affecting the public choices related to the Italian health-care system.

We found confirmatory evidence of a long-run equilibrium equation between ln_HCE_PC and ln_GDP_PC, with the estimated long-run real income elasticity greater than zero. The method of estimation provided consistent results concerning the impact of income on shares of government spending in health care with income elasticity of about 0.18. This implies that a 1 % increase in per capita income leads to a 0.18 % increase in the share of government expenditure for health care in the long term. Thus, per capita income increases more than the increase in the share of the government spending in health.

The presence of cointegration also implies that there exists short-term dynamics which will lead to equilibrium in the long run. In this respect, notice that the short term adjustment coefficient, as expected, is negative and statistically different from zero, thus suggesting that any deviation of per-capita public spending for health care from the value implied by the long-run equilibrium relationship with per-capita GDP brings about a correction in the opposite direction. Here, the error correction coefficient signals a relatively slow adjustment to the long-run equilibrium. Moreover, we found that the share of government spending in health is affected by per capita income also in the short term. Indeed, the significant—and >1—coefficient of the change of rate of growth of GDP in the short-run equation of all estimated models confirms the presence of some instantaneous impact of increasing GDP on the size of public expenditure for health care, although at a decreasing rate given that the variation of the change of rate of growth of GDP takes on negative sign. This result, together with the result found for the long term equation, further supports those theories according to which the growth in public expenditure for health is a natural consequence of economic growth both in the long and the short term.

In the short term, the variable related to the presence of elections is always significant with positive sign, confirming that during electoral years there is an increase of about 0.015 % of HCE. This result supports the existence of a type of electoral cycle involving health care with an increase of the related expenditure in the electoral year. Finally, the introduction in the system of the direct election of the president of the region positively affects the HCE. This result signals that the role of the president of the region has indeed changed, having gained greater power with respect to that of political parties. Unexpectedly enough, the increased responsibility of the president of the region does not curb the increase of HCE as the regional institutional reform of the end of the ‘90s hoped for. The impact of the reform is, in fact, about 0.07 % increase of public expenditure for health. On the other hand, those theories belonging to the so called political economy approach which points out that expenditure of “universal” type, such as HCE, are likely to be raised in those countries under the proportional electoral systems are not supported by the Italian data on health. As well as the presence of a political cycle is not supported by the Italian data because the variables related to the “political-colour” of the regional ruling coalitions are never significant.

The overall conclusion that emerges from the empirical analysis is that there exists a long- and a short-term relationship between GDP growth and growth of public expenditure for health in Italy. The estimates also support the view, already noted by Wagner, that there is a proportion between public expenditure and national income which may not be permanently overstepped (Alt 1980). This suggests an equilibrium relative size of government rather than an ever-growing government sector. Our result, other than providing an empirical support for the existence of Wagner’s law, whose meaning should be further explored in the Italian context also for different types of public expenditure, has important policy implications. For example, after the current global financial recession, the Italian government should be cautious about its present and future spending. Indeed, as income shall rise again, people will choose relatively more government expenditure. The growth of HCE—as well as the growth of social security transfers and unemployment compensation, major programs redistributing cash,…—is consistent with this finding. Nevertheless, extra public spending poses the issue of fiscal sustainability. Indeed, the public debt in Italy stands at about 133 % (est. 2013) of GDP, and any further increases would imply that future government spending may be mainly directed toward debt servicing, likely at the expense of public expenditure on basic infrastructure (particularly education and health facilities).

Finally, our results generally support the view that a substantial part of the growth of per-capita health care expenditure is a response to voter demand irrespective of the “political colour” of the regional governments’ ruling coalitions. Although we have not tested, and cannot exclude, other plausible explanations—including the much discussed role of pressure groups and bureaucrats—our findings assign a non-negligible role to voters’ choice. In this respect, notice that Rowley and Tollison (1994) compare Wagner’s law with the principle of comparative advantage: the law explains the complementarity between the growth of the industrial economy and the associated growth in demand for public services. In other words, social progress brings about an increase in state activity which in turn means more government expenditure (Henrekson 1993). Wagner himself (1883) stated that there is a persistent tendency both towards an ‘extensive’ and an ‘intensive’ increase in the functions of the state: new functions are continually undertaken and old ones are performed more efficiently and on an extended scale, which increases the spending of the government. Public expenditure is resorted to perform these activities. Wagner asserts that, among the reasons for the fact that increases in real income lead to more demand for basic infrastructure, there may well be the fact that the government provides these same facilities more efficiently than the private sector.Footnote 25 This assertion, however, is still to be proved, and evidence should be provided to support the claim by Peacock and Scott (2000) that when the comparative advantage of government declines, the share of public expenditure in total GDP also declines.

Notes

There are, of course, some exceptions. See Di Matteo–Di Matteo (1998) on Canadian Provinces, and Levaggi–Zanola (2003) and Bordignon–Turati (2009) on Italian Regions. In particular, Bordignon–Turati (2009) point out that HCE is generally the result of the behaviour of several layers of government, whose strategic interactions should be considered in the analysis. Their results are specific to the peculiar institutional framework of Italy in the 1990s.

The choice of the base year is a critical decision because of its importance for the considered series. The following aspects have been kept in mind when selecting 2005 as base year: The chosen base year is both a “normal” period and “stable” with respect to the economic activities, i.e., 2005 does not suffer from business cycle fluctuations. It was also felt that it would be desirable to choose a base year like 2005 that is not out of date or out of tune with the universe that it is designed to represent. Finally, 2005 is not distant in the past, this is important because the more recent the base year, the more representative it will be. For a discussion of this issue see, for example, Arulmozhi and Muthulakshmi (2009).

In the latter part of the nineteenth century, in spite of the limited role played by public expenditure in economic activity, Wagner (1883) observed that there exists a relationship between economic growth and public spending, later formulated as ‘Wagner’s Law of Increasing State Activities’.

Franco (1993) gathers the theories interpreting the public expenditure growth into two principal seams. The first includes conflicting-type explanations, according to which the growth of public expenditure depends both on the contrasts among the subjects that make up the society and on the institutions of the country. The second includes those theories of “structural” or “functional” type according to which the expenditure growth is determined by changes in the economic and social structure. In this respect, two relevant paradigms are the already mentioned “Wagner’s law” and the so-called “Tocqueville law”, according to which government expenditure growth with respect to GDP depends on the expansion of the electoral body and on the unequal distribution of income.

They are of two types: one type provides paediatric care to people aged under fourteen, the other type of care is for adults. Their number, role and pay are periodically determined by separate national contracts.

Obviously, individuals are also free to buy private health insurance and to receive treatment at non-contracted private hospitals or consult private outpatient specialists, at their own expense. As in other European countries, with increasing personal income levels, individuals often opt to supplement their public health insurance with the purchase of private insurance and/or private services.

The 1992/1993 reform stated that Regions incurring budget deficits could rely on payroll contributions (previously collected by the central government) earmarked for health care. Regions were also allowed to raise contribution rates. These options, however, were never used. Therefore, the 1990s bail out of the regional health care deficits continued to affect NHS funding.

The 1997 fiscal reform aimed both at eliminating disparities in payroll tax contributions rates and at introducing fiscal decentralisation. Public financing of the NHS partially changed its components as follows: an income-type value added tax on productive activities was introduced with revenues going directly to regions; revenues from user charges and tariffs were paid directly from consumers to local health management units and hospital trusts; regional shares of general taxation collected centrally, and regional surcharges on personal income tax were introduced; an inter-regional equalization fund was created, redistributing extra-revenues from the most affluent to the poorest regions.

Within this context, in 1999, it was decided that, beginning in 2001, health care funding would become a regional responsibility. The definition of essential and uniform assistance levels (LEAs)—the essential benefit package covering all medical care considered necessary, appropriate and cost-effective—was introduced in the system: LEAs were expected to be defined contextually to their financing, namely the capitation rate of public spending granted to each citizen. Responsibilities for ensuring that the general objectives and fundamental principles of the system were maintained at the national level. Regional health authorities were responsible for ensuring the delivery of LEAs through a network of local health management units, including public and accredited private health care providers.

The Financial Law for 2005 first introduced specific forms of support to the Regions by part of Central government. The repayment plans were however introduced with the Financial Law for 2007. The type of support received is related to those activities of planning, management and evaluation of the regional health care in those regions who agreed with the repayment plan inclusive of deficit recovery plan. It involves the activities related both to technical support to the individual region by part of specific central government’s agents (Nuclei) and to monitoring of the (regional and inter-regional) impact of each action implemented by the region subject to the repayment plan.

Over the considered period the regions involved are the following: Abruzzo, Campania, Lazio, Liguria, Molise since 2007, Calabria since 2009 (source: http://www.salute.gov.it/portale/temi/p2_4.jsp?area=pianiRientro).

Most residual based cointegration tests require that the long-run parameters for the variables in their levels are equal to the short-run parameters for the variables in their differences. Banerjee et al. (1998) and Kremers et al. (1992) refer to this as a common-factor restriction and show that its failure can cause a significant loss of power for residual-based cointegration tests (Westerlund 2007).

Hansen–King (1996), with a panel of 20 OECD countries over the years 1960–1987, show that the unit root hypothesis for either HCE or GDP can rarely be rejected and their country specific tests rarely reject the hypothesis of no cointegration. Using a panel covering 24 OECD countries between 1960 and 1991, Blomqvist–Carter (1997) conclude that HCE and GDP appear to be nonstationary and cointegrated. Gerdtham–Lothgren (2000), using a panel of 21 OECD countries between 1960 and 1997, and Roberts (2000), with a panel of 10 OECD countries from 1960 to 1993, found evidence suggesting that HCE and GDP are nonstationary variables.

As observed by an anonymous referee, the technical variables used here affect only the hospital beds and general practitioner, whereas no activities (e.g. admissions), needs (e.g. chronic illness), technologies, variables of epidemiological situations and/or policies are considered. The reason is due to unavailability of such variables for all the period of analysis. For example, the variable “admissions” often proxied by the variable “discharges” is contained in the database Istat/Ministero della salute only for the years (1992–2012). The variable “chronic illness” is available, for specific pathologies from 1993 to 2013; moreover ISTAT (Health for all) collects under the chapters related to “disease prevention” and to “chronic disease”, a number of variables, most of which covering only the years 1994, 2000, 2005 and in few cases the period since 1992 on. The variable “technologies” would be proxied by specific instruments such as CAT (computerized axial tomography) or haemodialysis but, in these and other similar cases, data are available from 1997 to 2010. The variables depicting “epidemiological situation” are often proxied by the variables collected by ISTAT (Health for all) under the chapter “Causes of diseases and fatalities” and are available both for the period 1990–2003 and since 2006.

Given this picture, the empirical analysis of long-run relationships among integrated variables with both a cross sectional dimension, N, and a time-series dimension, T, by means of panel cointegration techniques proposed here would be greatly weakened by a reduction of the time dimension of about 8–10 years. Some tests explicitly require T > N, also considering that some periods are lost in the calculation of differenced variables and lags.

As mentioned in previous section, we can distinguish three main periods. 1982–1992: the full financing of HCE by means of the National Health Fund. 1993–1997: a mixed mechanism of financing, with the NHF having a complementary role to the revenues from health care social contributions levying on dependent labour income. 1998–2009: introduction of a regional tax on production activities, a regional surtax on personal income, revenue sharing of the VAT revenue and excise duty on petrol.

The number of lags selected by the Akaike criterion is 2.

The model is fitted allowing panel specific intercepts. The cluster on regions allows for intragroup correlation in the calculation of the standard errors.

The validity of the restrictions shall be tested via Hausman test (Table 5).

Details on the tests are in Pesaran (2007).

Wagner was not explicit in the formulation of his hypothesis. The earliest version of this law was given by Peacock–Wiseman (1961) and then by Pryor (1969) without taking into account the effect of increases in population. In this respect, Gupta (1967) suggested that Wagner’s law may be interpreted as the one wherein growth in real per capita government expenditure depends upon the growth in real GDP per capita. In all these models, Wagner’s law holds true in cases where the elasticity is greater than unity. On the other hand, Timm (1961) concludes that Wagner’s law should be interpreted in a relative sense, as predicting an increasing relative share of public expenditure as per capita real income grows (Henrekson 1993). In this vein, Musgrave (1969) and subsequently Mann (1980) explained the growth in public expenditure in the relative sense, thus supporting the view that Wagner’s law holds true in cases where the value of the elasticity is greater than zero (Henrekson 1993).

K corresponds to 4.957 + 0.183L.log_GDP_PC.

The MG estimator only allows us to impose the restriction in the long-run estimates in order to specify the short-term dynamics.

Wagner gave three main reasons of increasing government expenditure with economic growth. First, with economic growth industrialization and modernization would take place, which will diminish the role of public sector in favour of the private one. This continuous diminishing share of the public sector in economic activity leads to higher government expenditure aimed at regulating the private sector. Second, the rise in real income would lead to more demand for basic infrastructure, such as education and health care, supplied by the government more efficiently than by the private sector. Third, to remove monopolistic tendencies in a country and to enhance economic efficiency in sectors where lumpy investment is required, such as railways, governments should come forward and invest in that particular area, which will again increase government spending (Bird 1971).

Note that two-way causation is frequently the case. Granger causality does not imply that a variable is the effect or the result of the other. Granger causality measures precedence and information content but does not by itself indicate causality in the more common use of the term.

References

Alt, J. (1980). Democracy and public expenditure. St. Louis: Washington University.

Arulmozhi, G., & Muthulakshmi, S. (2009). Statistic for management (2nd ed.). New Delhi: Tata Mc Graw-Hill Education.

Baltagi, B. H., Griffin, J. M., & Xiong, W. (2000). To pool or not to pool: Homogeneous versus heterogeneous estimators applied to cigarette demand. The Review of Economics and Statistics, 82, 117–126.

Banerjee, A., Dolado, J. J., & Mestre, R. (1998). Error-correction mechanism tests for cointegration in a single-equation framework. Journal of Time Series Analysis, 19, 267–283.

Barros, P. P. (1998). The black box of health care expenditure growth determinants. Health Economics, 7, 533–544.

Baum, C. F., Schaffer, M. E., & Stillman, S. (2003). Instrumental variables and GMM: Estimation and testing. Stata Journal, 3, 1–31.

Beraldo, S., Montolio, D., & Turati, G. (2009). Healthy, educated and wealthy: A primer on the impact of public and private welfare expenditures on economic growth. The Journal of Socio-Economics, 38, 946–956.

Bethencourt, C., & Galasso, V. (2008). Political complements in the welfare state: Health care and social security. Journal of Public Economics, 92, 609–632.

Bird, R. M. (1971). Wagner’s law of expanding state activity. Public Finance, 26(1), 1–26.

Blomqvist, A. G., & Carter, R. A. L. (1997). Is health care really luxury? Journal of Health Economics, 16, 207–229.

Bohn, H. (1999). Will social security and medicare remain viable as the U.S. population is aging? Carnegie-Rochester Series on Public Policy, 50(1), 1–53.

Bond, S., & Eberhardt, M. (2009). Cross-section dependence in nonstationary panel models: A novel estimator. Paper presented at the Nordic econometrics conference in Lund.

Bordignon, M., & Turati, G. (2009). Bailing out expectations and public health expenditure. Journal of Health Economics, 28, 305–321.

Chari, V. V., & Cole, H. (1995). A contribution to the theory of pork-barrel spending. FRB of Minneapolis discussion paper 156.

Crivelli, L., Filippini, M., & Mosca, I. (2006). Federalism and regional health care: An empirical analysis for the Swiss cantons. Health Economics, 15, 535–541.

Culyer, A. J. (1988). Health care expenditures in Canada: Myth and reality. Canadian tax papers, 82.

Di Matteo, L., & Di Matteo, R. (1998). Evidence on the determinants of Canadian provincial Government health expenditures: 1965–1991. Journal of Health Economics, 17, 211–228.

Eberhardt, M., & Teal, F. (2010). Productivity analysis in global manufacturing production. Economics series working papers 515, University of Oxford, Department of Economics.

Eberhardt, M., & Teal, F. (2011). Econometrics for grumblers: A new look at the literature on cross-country growth empirics. Journal of Economic Surveys, Wiley Blackwell, 25(1), 109–155.

Engle, R., & Granger, C. (1987). Cointegration and error correction: Representation, estimation and testing. Econometrica, 55, 251–276.

Fedeli, S. (2008). La situazione debitoria sanitaria reale delle regioni. La Formazione dei deficit e loro copertura. In Pedone, A. (Ed.), LA SANITA IN ITALIA (pp. 103–138). Milano: Ed. Il sole 24 ORE.

Franco, D. (1993). L’espansione della spesa pubblica in Italia (1960–1990). Bologna: Il Mulino.

Frey, B., & Stutzer, A. (2000). Happiness, economy and institutions. The Economic Journal, 110, 918–938.

Gerdtham, U.-G., & Jönsson, B. (2000). International comparisons of health expenditure: Theory, data and econometric analysis. In A. J. Culyer & J. P. Newhouse (Eds.), Handbook of health economics (Vol. 1, pp. 11–53). Amsterdam: Noth-Holland.

Gerdtham, U. G., Jönsson, B., MacFarlan, M., & Oxley, H. (1998). The determinants of health expenditure in the OECD countries. In P. Zweifel (Ed.), Health, the medical profession and regulation. Dordrecht: Kluwer Academic.

Gerdtham, U. G., & Lothgren, M. (2000). On stationarity and cointegration of international health expenditure and GDP. Journal of Health Economics, 19, 461–475.

Gerdtham, U. G., Sogaard, J., Andersson, F., & Jonsson, B. (1992). An econometric analysis of health care expenditure: A cross-section study of the OECD countries. Journal of Health Economics, 11, 63–84.

Giannoni, M., & Hitiris, T. (2002). The regional impact of health care expenditure: The case of Italy. Applied Economics, 34(14), 1829–1836.

Grilli, V., Masciandaro, D., & Tabellini, G. (1991). Political and monetary institutions and public finance policies in the industrial democracies. Economic Policy, 13, 341–392.

Grofman, B. (2001). Notes and comments. The comparative analysis of coalition formation and duration: Distinguishing between country and within-country effects. British Journal of Political Science, 19, 291–301.

Gupta, S. P. (1967). Public expenditure and economic growth: A time series analysis. Public Finance, 22(4), 423–461.

Hall, R. E., & Jones, C. I. (2004). The value of life and the rise in health spending. NBER working paper, vol. 10737.

Hansen, P., & King, A. (1996). The determinants of health care expenditures: A cointegration approach. Journal of Health Economics, 15, 127–137.

Henrekson, M. (1993). Wagner’s law: A spurious relationship? Public Finance, 48(2), 406–415.

Hitiris, T., & Posnett, J. (1992). The determinants and effects of health expenditure in developed countries. Journal of Health Economics, 11, 173–181.

Im, K. S., Peseran, M., & Shin, Y. (2003). Testing for unit roots in heterogeneous panels. Journal of Econometrics, 115, 53–74.

Kremers, J., Ericsson, N., & Dolado, J. (1992). The power of cointegration tests. Oxford Bulletin of Economics and Statistics, 54, 325–348.

Leu, R. E. (1986). The public-private mix and international health care costs. In A. J. Culyer & B. Jonsson (Eds.), Public and private health services. Oxford: Basil Blackwell.

Levaggi, R., & Zanola, R. (2003). Flypaper effect and sluggishness: Evidence from regional health expenditure in Italy. International Tax and Public Finance, 10, 535–547.

Lijphart, A. (1984). Democracies: Patterns of majoritarian and consensus government in twenty-one countries. New Haven: Yale University Press.

Lijphart, A. (1994). Electoral systems and party systems. Oxford, UK: Oxford University Press.

Mann, A. J. (1980). Wagner’s law: An econometric test for Mexico, 1925–76. National Tax Journal, 33(2), 189–201.

Milesi-Ferretti, G., Perotti, R., & Rostagno, M. (2002). Electoral systems and public spending. The Quarterly Journal of Economics, 117(2), 609–657.

Moscone, F., & Tosetti, E. (2009). A review and comparison of tests of cross section independence in panels. Journal of Economic Surveys, 27, 528–561.

Musgrave, R. A. (1969). Fiscal systems. New Haven, London: Yale University Press.

Newhouse, J. P. (1977). Medical care expenditure: A cross-national survey. Journal of Human Resources, 12, 115–125.

Newhouse, J. P. (1992). Medical care costs: How much welfare loss? Journal of Economic Perspectives, 6(3), 3–21.

Peacock, A., & Scott, A. (2000). The curious attraction of Wagner’s law. Public Choice, 102, 1–17.

Peacock, A. T., & Wiseman, J. (1961). The growth of public expenditure in the United Kingdom. Cambridge: NBER and Princeton: Princeton University Press.

Pedroni, P. (1999). Critical values for cointegration tests in heterogeneous panels with multiple regressors. Oxford Bulletin of Economics and Statistics, 61, 653–670.

Pedroni, P. (2004). Panel cointegration: Asymptotic and finite sample properties of pooled time series tests with an application to the PPP hypothesis. Econometric Theory, 3, 579–625.

Persson, T., & Tabellini, G. (1999). The size and scope of government: Comparative politics with rational politicians. European Economic Review, 43, 699–735.

Persson, T., & Tabellini, G. (2000). Political economics. Cambridge: MIT Press.

Persson, T., & Tabellini, G. (2001). Political institutions and policy outcomes: What are the stylized facts? CEPR discussion paper, no. 2872.

Persson, T., & Tabellini, G. (2005). The economics effects of constitution. Cambridge: MIT Press.

Persyn, D., & Westerlund, J. (2008). Error-correction-based cointegration tests for panel data. The Stata Journal, 8, 232–241.

Pesaran, H. (2003). A simple panel unit root test in the presence of cross section dependence. Cambridge working papers in economics 0346, Faculty of Economics (DAE), University of Cambridge.

Pesaran, M. (2004). General diagnostic tests for cross section dependence in panels. Cambridge working papers in economics 435, and CESifo working paper series 1229.

Pesaran, M. (2007). A simple panel unit root test in the presence of cross-section dependence. Journal of Applied Econometrics, 22, 265–312.

Pesaran, M. H., Shin, Y., & Smith, R. P. (1997). Estimating long-run relationships in dynamic heterogeneous panels. DAE working papers amalgamated series 9721.

Pesaran, M. H., Shin, Y. C., & Smith, R. (1999). Pooled mean group estimation of dynamic heterogeneous panels. Journal of the American Statistical Association, 94, 621–634.

Pesaran, M. H., & Smith, R. (1995). Estimating long-run relationships from dynamic heterogeneous panels. Journal of Econometrics, 68, 79–113.

Pryor, F. L. (1969). Public expenditure in communist and capitalist nations. London: George Allen and Unwin Ltd.

Roberts, J. (2000). Spurious regression problems in the determinants of health care expenditure: A comment on Hitiris (1997). Applied Economics Letters, 7, 279–283.

Roubini, N., & Sachs, J. (1988). Government spending and budget deficits in the industrial countries. Economic Policy, 8, 100–132.

Roubini, N., & Sachs, J. (1989). Political and economic determination of budget deficits in the industrial democracies. European Economic Review, 33, 903–938.

Rowley, C. K., & Tollison, R. D. (1994). Peacock and Wiseman on the growth of public expenditure. Public Choice, 78, 125–128.

Santagata, W. (1995). Economia, elezioni, interessi. Bologna: Il Mulino.

Smith, J. (1999). Healthy bodies and thick wallets: The dual relation between health and economic status. Journal of Economic Perspectives, 13(2), 145–166.

Timm, H. (1961). Das Gesetz Des Wachsenden Staatsausgaben. Finanzarchiv, 19, 201–247.

Tornell, A., & Velasco, A. (1992). The tragedy of the commons. Journal of Political Economy, 100, 1208–1231.

Trechsel, A., & Serduult, U. (1999). Kaleidoskop Volksrechte. Die Istitutionen der direkten Demokratie in den schweizerischen Kantonen 1970–1996. Basilea: Helbing and Lichtenhahn.

Vatter, A., & Ruefli, C. (2003). Do political factors matter for health care expenditure? Swiss Cantons. Journal of Public Policy, 23(3), 325–347.

Wagner, A. (1883). Three extracts on public finance. In R. A. Musgrave & A. T. Peacock (Eds.), Classics in the theory of public finance. London: Macmillan.

Weingast, B., Shepsle, K., & Johansen, C. (1981). The political economy of benefits and costs: A neoclassical approach to distributive politics. Journal of Political Economy, 89, 642–664.

Westerlund, J. (2005). New simple tests for panel cointegration. Econometric Reviews, 24, 297–316.

Westerlund, J. (2007). Testing for error correction in panel data. Oxford Bulletin of Economics and Statistics, 69, 709–748.

Author information

Authors and Affiliations

Corresponding author

Appendices

Appendix 1

1.1 Granger Causality Test on the Considered Variables

The existence of a long run relationship between the government spending for health and GDP advocates that there must be Granger causality in at least one direction. In order, to identify the direction of temporal causality we apply Granger causality tests.

The Granger approach to the question of whether X causes Y is to see how much of the current value of the former can be explained by past values of the latter and then to see whether adding lagged values of X can improve the explanation. Y is said to be Granger-caused by X if X helps in the prediction of Y, or equivalently if the coefficients on the lagged X’s are statistically significant.Footnote 26 Here we report the F-statistics for the test of the null hypothesis that both ln_HCE_PCit does not Granger cause ln_GDP_PCit and ln_GDP_PCit does not Granger cause ln_HCE_PCit, where ln_GDP_PCit and ln_HCE_PCit are taken both in level and in difference.

The results are reported in Table 11, which shows that, for both variables taken both in level and in differences, we can reject the hypothesis that ln_HCE_PCit does not Granger cause ln_GDP_PCit and we do reject the hypothesis that ln_GDP_PCit does not Granger cause ln_HCE_PCit. Therefore, it appears that Granger causality runs two-ways from ln_HCE_PCit to ln_GDP_PCit.

Appendix 2

We test whether ln_GDP_PC and ln_HCE_PC are cointegrated. As already mentioned, we refer to Westerlund (2005, 2007) and Persyn and Westerlund (2008). Their idea is to test the null hypothesis of no cointegration by inferring whether the error-correction term in a conditional panel error-correction model is equal to zero. Recall that the four tests are all normally distributed and are general enough to accommodate unit-specific short-run dynamics, unit-specific trend and slope parameters, and cross-sectional dependence. Two tests are designed to test the alternative hypothesis that the panel is cointegrated as a whole, while the other two test the alternative that at least one unit is cointegrated. The calculated values of the error correction statistics are presented along with asymptotic p values in Table 12. When using the asymptotic p values, for both the cases in which the deterministic chosen is ‘constant and trend’ and ‘constant only’, all four tests clearly lead to accept the null hypothesis of no cointegration, which we take as strong evidence against cointegration between ln_GDP_PC and ln_HCE_PC.

Rights and permissions

About this article

Cite this article

Fedeli, S. The Impact of GDP on Health Care Expenditure: The Case of Italy (1982–2009). Soc Indic Res 122, 347–370 (2015). https://doi.org/10.1007/s11205-014-0703-x

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11205-014-0703-x