Abstract

This paper examines the association between conservatism and the value relevance of accounting information over the 1975 through 2004 period. We measure conservatism using approaches developed in Penman and Zhang, The Accounting Review 77:237–264, (2002) and Beaver and Ryan, Journal of Accounting Research 38:127–148, (2000) and value relevance using (1) adjusted R 2 from regressions of price on earnings and book values, (2) adjusted R 2 from regressions of returns on earnings and changes in earnings, and (3) returns earned by perfect foresight of earnings and book values. We find no evidence that firms with increasing conservatism exhibit greater declines in value relevance. Rather, we observe most significant declines in value relevance for firms where conservatism has not increased. When we adjust financial statements for the effects of conservatism, we find that the value relevance of adjusted numbers is generally lower and trends in value relevance unaffected. Based on these results, it is implausible that increasing conservatism drives the decline in value relevance.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

This paper examines the association between the trends in accounting conservatism and the value relevance of accounting earnings and book values over time. Prior literature has found that the value relevance of accounting information has declined in recent years (Lev and Zarowin 1999; Francis and Schipper 1999; Core et al. 2003). It has often been claimed that increasing accounting conservatism is responsible for the decline in value relevance (Elliott and Jacobsen 1991; Jenkins 1994; Sever and Boisclaire 1990).

This claim reflects accounting’s failure to recognize growing expenditures on items such as R&D and advertising on balance sheets. Nakamura (2003) documents significant growth in R&D and advertising in the last few decades. Some practitioners consequently argue that the growing omission of the intangible assets created by R&D and advertising hamper the relevance of financial statements because, “Accounting is no longer counting what counts” (Stewart 2002).

In contrast, accountants have stressed the role of conservatism in accounting for the purposes of valuation and contracting since Bliss (1924). Sterling (1967) and Watts (2003) argue that conservatism provides more reliable information for both contracting and valuation by imposing a high threshold of reliability and verifiability. This suggests that increasing conservatism should enhance rather than reduce value relevance. Furthermore, Penman (2009) argues that, while conservative accounting does not recognize speculative intangible assets on the balance sheet, the stream of income from these assets does flow through the income statement.

Prior literature distinguishes between unconditional conservatism which reflects the predetermined application of conservative accounting policies, and conditional conservatism which is event-driven (Beaver and Ryan 2005). Examples of unconditional conservatism include the expensing of R&D and advertising, leading to economic assets being omitted from balance sheets. Prior research has identified these omissions as the primary drivers of the decline in value relevance (Lev and Zarowin 1999; Elliott and Jacobsen 1991). Hence, we examine measures of unconditional accounting conservatism (henceforth, conservatism) rather than conditional conservatism discussed in Basu (1997). We ask the following research question: is the decline in the value relevance of accounting associated with increasing conservatism?

Prior research examining the relationship between conservatism and value relevance has yielded mixed results. While Lev and Zarowin (1999) find a greater decline in value relevance for firms with increasing R&D, Francis and Schipper (1999) do not find a greater decline in value relevance in high-technology industries relative to other industries. It is difficult to draw conclusions about the relationship between conservatism and value relevance based on these seemingly conflicting results for two reasons. First, neither paper measures conservatism comprehensively, focusing either on a particular business activity (R&D) or particular industries (high-technology) more likely to be affected by conservatism. Second, while Francis and Schipper (1999) condition on the level of conservatism, Lev and Zarowin (1999) focus on growth in conservatism.

This paper addresses these limitations by measuring conservatism comprehensively and conditioning on both the level of and growth in conservatism. We use two metrics to measure conservatism. The first, BR-CONS, based on Beaver and Ryan (2000), measures the downward bias in book value after removing the effects of delayed recognition of past economic shocks. The second, C-SCORE, developed in Penman and Zhang (2002), measures the downward bias in book value from the expensing of R&D and advertising and the use of LIFO for inventory. We group firms annually on the levels of and growth in conservatism and study trends in value relevance across groups.

We measure value relevance using three approaches. First, we use the adjusted R 2 from regressions of price on contemporaneous earnings and book value as a measure of price value relevance. Second, we use the adjusted R 2 from regressions of returns on contemporaneous earnings and change in earnings as a measure of returns value relevance. Third, we use a market-adjusted measure of returns that could be earned from perfect foresight of earnings and book value.

Overall, we find no evidence that declining value relevance is associated with increasing conservatism. In price value relevance regressions using BR-CONS, the decline in value relevance is more pronounced for the groups with steady conservatism than for the groups with increasing conservatism. Trends are similar across the groups using C-SCORE. The decline in returns value relevance is more pronounced for groups with steady conservatism than for those with increasing conservatism, using either BR-CONS or C-SCORE. Trends in perfect foresight returns are similar for firms with increasing and steady conservatism. Finally, when income statements and balance sheets are adjusted for the effects of conservatism, the value relevance is generally lower and trends in value relevance are unaffected.

These results are inconsistent with increasing conservatism driving declining value relevance. They might even suggest that increasing conservatism potentially mitigated declines in value relevance. This is potentially of interest to regulators, who have recently promulgated standards that reduce conservatism by introducing fair value estimates to the balance sheet.

The rest of the paper is organized as follows. We discuss our research question in Sect. 2 and our research design in Sect. 3. In Sect. 4, we provide evidence confirming prior findings that value relevance has declined and conservatism has increased over time. In Sect. 5, we present our results analyzing the relationship between conservatism and value relevance, using alternate definitions of conservatism and value relevance. We conclude in Sect. 6.

2 Research question

2.1 Definition of value relevance and conservatism

2.1.1 Value relevance

An accounting measure is said to be value relevant if it has a consistent association with equity market values (Barth et al. 2001). Typically, value relevance is measured as the adjusted R 2 of regressions with stock price as the dependent variable and book value and earnings as independent variables (Collins et al. 1997; Francis and Schipper 1999; Lev and Zarowin 1999). Alternatively, value relevance has also been measured as the adjusted R 2 of regressions with returns as the dependent variable and level of earnings and change in earnings as independent variables. Finally, value relevance has also been measured as the stock returns that could be earned from perfect foresight of accounting information (Francis and Schipper 1999).

These value relevance measures have been interpreted as the total market share, among all information impounded in stock price, attributable to accounting information. However, this interpretation is subject to certain caveats. First, these measures typically focus only on specific bottom-line accounting numbers and ignore financial statement line items. Second, there has been a considerable increase in footnote disclosure of assets and liabilities not recognized explicitly on the balance sheet (LIFO reserves, pension obligations, and liabilities) over the time period analyzed. Any increase in value relevance from these additional disclosures is omitted in these value relevance measures. Third, these measures may also reflect the value relevance of other more timely nonfinancial information that is correlated with accounting disclosures. Finally the information efficiency of price may have changed over time due to an increase in non-information based trading (Dontoh et al. 2004).

2.1.2 Conservatism

Conservatism is typically defined as the choice (by regulators, standard setters, or firms) of accounting treatments likely to understate net assets and cumulative income (Kieso et al. 2004; Revsine et al. 2005). Prior literature has measured conservatism as the downward bias in book values relative to market values (Beaver and Ryan 2000) or downward bias because of specific accounting practices (Penman and Zhang 2002).

2.2 Our research question: Is value relevance related to conservatism?

Many regulators, practitioners, and academics have long argued that a tradeoff often exists between relevance and reliability, with conservatism favoring reliability over relevance.Footnote 1 Holthausen and Watts (2001) state that the increase in conservatism shows that standard setters place “less emphasis on valuation.” Lev and Zarowin (1999) argue that declining value relevance is driven by the nonrecognition of increasingly important intangible assets such as R&D. Lev and Sougiannis (1996) show that adjusting financial statements by capitalizing R&D produces information that is relevant for investors. Similar adjustments are recommended by practitioners such as Stewart (2002). Finally, Blair and Wallman (2001) recommend mandatory disclosure of more information about intangibles to reduce information asymmetry.

In contrast, others argue that there need not be a tradeoff between value relevance and reliability, because conservatism constrains management incentives to bias earnings upwards. Sterling (1967) observes: “Faced with the universal tendency to overstate, the accountant conceived his role to be one of temperance… To combat overstatement, he proposed understatement.” Conservative accounting policies that favor more objective measures and less estimation can lead to more reliable accounting numbers. Watts (2003) argues that because conservatism limits the introduction of information that cannot be reliably measured, increased conservatism might be associated with increased relevance.

Research to date on the association between accounting conservatism and value relevance has yielded mixed results. While Francis and Schipper (1999) find that value relevance does not decrease more for high-technology than for low-technology industries, Lev and Zarowin (1999) show that value relevance declines most for firms with the largest increases in R&D. These results are difficult to compare directly, as Francis and Schipper (1999) examine the level of conservatism, while Lev and Zarowin (1999) examine the change in conservatism. Further, neither study measures conservatism comprehensively, focusing instead either on a particular type of business transaction (R&D) or particular industries (high-technology) that are more likely to be affected by conservatism. Hence, one cannot answer the question we set out to address: whether increasing conservatism is responsible for the decline in value relevance.

3 Research design

3.1 Measuring value relevance

3.1.1 Price value relevance

Our first measure of value relevance is the adjusted R 2 of the regression of stock price per share (PRICE) on earnings per share (EPS) and book value per share (BVPS).

PRICE is stock price three months after fiscal year end, and EPS and BVPS are earnings per share and book value per share, respectively.

We address two known econometric problems that affect the above regression. First, the incidence of losses has increased over time (Hayn 1995; Givoly and Hayn 2000; Klein and Marquardt 2006), which likely lowers the goodness of fit of value relevance regressions, as losses tend to be less informative than profits. To control for losses, Core et al. (2003) use separate intercepts and slopes for loss firms.

Second, these regressions force coefficients on earnings and book values to be the same for firms in all industries. If inter-industry heterogeneity has increased over time, it would reduce value relevance, not because accounting numbers are less meaningful but because they are increasingly different across time and industry. To control for this, we allow for the intercepts and coefficients on earnings and book values to vary across industry, using Fama and French’s (1997) classification of SIC codes into 48 industry groupings.

We address these problems by expanding Eq. 1 to include separate slope and intercept coefficients for each industry and for profit and loss firms.Footnote 2

where PRICE, EPS, and BVPS are as defined earlier, INDj is a dummy variable for each of the 48 Fama–French industry groups, and LOSS is a dummy variable for firms with negative EPS. As a sensitivity test, we rerun the regressions without controls for losses and industry membership.

Figure 1a highlights the importance of controlling for losses and industry. On average, value relevance increases significantly (5.6%), with controls for losses and further increases when we allow for variation by industry (10.8%). Figure 1b graphs the incremental improvement in value relevance. While the improvement from controlling for losses shows a significant positive trend, the improvement from industry adjustment does not exhibit any noticeable trend.Footnote 3

a Impact of controlling for losses and industry. b Incremental impact of controlling for losses and industry

We measure PRICE 3 months after fiscal year-end, using the first quarter (Compustat Quarterly #14) financials for the following year, adjusting for splits. EPS is defined as income before extraordinary items (Compustat #18) divided by shares outstanding (Compustat #54). BVPS is common equity (Compustat #60) divided by shares outstanding (Compustat #54).

3.1.2 Returns value relevance

Our second measure of value relevance is the adjusted R 2 of a regression of annual stock returns (RET) on scaled earnings and changes in earnings, as in Easton and Harris (1991). We again allow for separate slope and intercept coefficients for loss firms and by industry with the following regression.

where RET denotes compounded monthly CRSP returns from the fourth month of the current fiscal year to the third month after fiscal year-end. E t is EPS scaled by beginning of period price. ∆E t is change in EPS scaled by beginning of period price. IND j and LOSS are as previously defined.

3.1.3 Perfect foresight measures of value relevance

Our third measure of value relevance is the percentage of returns that could be earned with perfect foresight of accounting information as in Francis and Schipper (1999). For each year, we estimate the following regression:

where RETM is the market-adjusted return for the 12-month period ending three months after fiscal year-end, (∆E) E is (change in) earnings before extraordinary items, and BV is book value of equity. All independent variables are scaled by lagged market value of equity. We estimate returns to a hedge portfolio long the top 40% and short the bottom 40% of the fitted values from this model. We scale the hedge returns by the hedge returns that could be earned by perfect foresight of returns.

3.2 Trends in value relevance

We regress each measure of value relevance, denoted VALREL j , on a time trend for each conservatism group j to examine whether value relevance has declined over time.

where YEAR denotes the year of the regression or return compounding. Our variable of interest is the coefficient β j , which we name TREND.

Brown et al. (1999) show that an increase in the coefficients of variation in either the dependent and independent variables of value relevance regressions leads to a mechanical increase in adjusted R 2 that obscures a real decline in value relevance (see Fig. 2). As they recommend, we add the coefficients of variation of PRICE and BVPS as additional independent variables in our trend regression for price value relevance regressions.Footnote 4

Scale effects across time

Our sample includes the period from 1998 to 2000, associated with the high-technology bubble, during which the value relevance of accounting information was markedly lower than other periods even after controlling for losses and industry (see Fig. 1). To ensure that our results are not driven by these anomalous years, we include a dummy to control for these years. Our modified trend regression for the price regression has the following specification:

where CVBVPS and CVPRICE are the coefficients of variation of BVPS and PRICE, respectively, and BUBBLE is a dummy variable that equals 1 for the years 1998, 1999, and 2000 and 0 otherwise.

For the other two approaches to measuring value relevance (returns value relevance, perfect foresight returns), we control only for the bubble years because scale effects should not exist. The resulting specification is:

The coefficient β j from these trend regressions, ADJTREND, is the adjusted trend in the corresponding metric of value relevance for group j.

3.3 Measuring unconditional conservatism

3.3.1 The Beaver and Ryan approach (BR-CONS)

Our first proxy for conservatism is based on Beaver and Ryan (2000), who distinguish the impact of biases and lags on the book-to-market ratio using this regression:

where BTM t,i is the book-to-market ratio for firm i at time t, R t-j,i is the annual raw return for firm i at time t − j, and α t and α i are time and firm fixed effects, respectively. The coefficients on the returns capture the lags because of delayed recognition due to historical cost accounting. The fixed effects represent bias. Beaver and Ryan (2000) show that the firm fixed effect is inversely related to conservative accounting such as accelerated depreciation and high levels of R&D.

As our analysis requires a firm-year measure of conservatism, we run the Beaver and Ryan (2000) model for each year, using a panel of the current and five lagged years. Hence, for the regressions for 1990, we use data from 1986 to 1990. We use the market-to-book ratio as our dependent variable to yield a measure positively associated with conservatism.Footnote 5 Our model is:

The dependent variable, MTB, is measured at fiscal year-end as the ratio of the book value of common equity (#60) to market value of equity (#199*#25). We relax the requirement that 6 years of lagged returns are needed. We used actual returns for the first two lags. For the remaining lags, missing returns are set to zero.Footnote 6 The sum of the time effect (α t ) and firm-specific fixed effect (α i ) is our measure of conservatism, labeled BR-CONS.

3.3.2 The Penman and Zhang approach (C-SCORE)

Penman and Zhang (2002) measure conservatism as C-SCORE, the sum of capitalized R&D, capitalized advertising expense, and the LIFO reserve scaled by net operating assets. We capitalize and amortize R&D (Compustat #46) over 5 years and advertising expense (Compustat #45) over 2 years, using sum-of-years-digits amortization. We set R&D and advertising to zero when data are missing. We use total assets (Compustat #6) as our deflator, as the information to calculate net operating assets is either unavailable or net operating assets is negative for nearly 20% of firms.

3.4 Partitioning on the levels of and growth in conservatism

We partition our sample along both the level of conservatism and growth in conservatism. Partitioning on the level of conservatism allows us to ask whether firms with more conservative accounting experienced a greater decline in value relevance than firms with less conservative accounting, similar to Francis and Schipper (1999). It also serves as an additional control for heterogeneity in addition to industry membership. Firms with similar conservatism are likely to have similar amounts of assets omitted from their balance sheets and similar differences between reported earnings and what earnings would have been with unbiased accounting.

Partitioning on growth in conservatism allows us to study the impact of increasing conservatism on value relevance, similar to Lev and Zarowin (1999). If a firm has no growth in activities subject to conservative accounting, any bias in book value due to conservatism can be undone as a scale factor adjustment. There should also be no bias in income, as expensing new cash outlays will exactly offset amortizing previously capitalized expenses. Growth in activities subject to conservative accounting increases the downward bias in book values and creates a downward bias in income.Footnote 7 Further, uncertainty about the extent of growth or the implications of growth can have a detrimental impact on value relevance. Lev and Zarowin (1999) state that “It is not change per se that distorts financial reporting, rather it is the increased uncertainty associated with change.”Footnote 8

We partition the sample each year into two equal size groups based on level of conservatism and independently into two equal size groups based on growth in conservatism. We measure growth in conservatism by estimating firm-specific trends in the level of conservatism.Footnote 9 We label the groups based on trends as steady and increasing because the average trend for the low group is insignificantly different from zero, while the trend for the high group is significantly positive. Our tests are run on the four groups formed by the intersection of these two dimensions (low and steady, low and increasing, high and steady, and high and increasing). If increasing conservatism is responsible for the decline in value relevance, then such a decline should be most prominent in the groups with increasing conservatism.

4 Data and preliminary evidence

4.1 Data

Our sample consists of firms in the Compustat Annual Industrial dataset in the 30-year period from 1975 through 2004 for which data on security prices, splits, and share information are available in the CRSP monthly return file. The time period covers the period (1977 through 1996) analyzed by Lev and Zarowin (1999) and the more recent years analyzed by Core et al. (2003). Consistent with prior literature, we delete firms with negative book values and include all industries.Footnote 10

To estimate firm-specific trends in conservatism, we require that conservatism measures be available for at least two lagged years. This reduces our sample size from the population of firms on Compustat. Our sample consists of 100,984 observations over 30 years (average 3,366 observations per year) ranging from a low of 1,792 observations in 1975 to a high of 4,710 observations in 1999. As in prior research, we winsorize earnings per share and book value per share at the 0.5% level by year and delete influential observations with studentized residuals of absolute magnitude greater than 4.Footnote 11

4.2 Descriptive statistics

Table 1 presents descriptive statistics for subsamples based on levels of and growth in conservatism. Panel A presents statistics for groups based on BR-CONS. Firms with high and increasing conservatism are the largest in terms of market value of equity, book value of equity, revenues, and total assets. The high conservatism groups have higher mean revenue growth than the low conservatism groups, but within the groups increasingly conservative firms appear to be growing slightly more slowly. High conservatism firms have lower profitability (NI/assets) than low conservatism firms, consistent with conservatism lowering earnings. High conservatism firms also have lower leverage, presumably related to lower levels of tangible assets. Firms with higher BR-CONS also have higher C-SCORE.

Panel B of Table 1 presents statistics for groups based on C-SCORE. Results are similar to Panel A with two notable differences for high C-SCORE firms. Among these firms, those with increasing C-SCORE are smaller and have slightly higher revenue growth, indicating that smaller firms have greater growth in R&D and advertising, which are subject to conservative accounting. Also among high C-SCORE firms, firms with increasing C-SCORE also have higher levels of C-SCORE. This contrasts with the finding among high BR-CONS firms where mean BR-CONS is higher for steadily conservative than for increasingly conservative firms.

Table 2 indicates there is a consistently strong positive correlation between BR-CONS and C-SCORE that strengthens with time. We view this as a corroboration that these metrics both pick up aspects of conservatism.Footnote 12

4.3 Trends in conservatism and value relevance

We first examine the trends in conservatism and value relevance to establish prima facie evidence of a possible relationship between increasing conservatism and the declining value relevance of accounting.

4.3.1 Has conservatism increased?

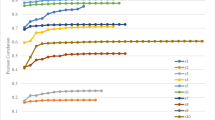

Figure 3 and the last two columns of Table 2 present trends in BR-CONS and C-SCORE. The mean level of BR-CONS increases from −0.034 to 0.505 over the sample period 1975 through 2004, with a significantly positive trend. The mean level of C-SCORE nearly doubles, from 5.5% in 1975 to 10.5% in 2004, consistent with a dramatic increase in R&D and advertising intensity. Hence, conservatism has increase significantly over time using either metric.

The increase in conservatism across time

The increase in conservatism is driven by two factors. First, there has been significant growth in activities subject to conservative accounting such as R&D and advertising (Nakamura 2003). Within our sample, the average R&D/sales rose from in 1.5% 1975 to 8.2% in 2004. Similarly, advertising/sales rose from 1.7% in 1975 to 2.6% in 2004. Second, financial reporting standards have become increasingly conservative with earlier recognition of expenses and losses or deferral of revenues and gains.Footnote 13

4.3.2 Has value relevance declined?

Table 3 presents our attempt to replicate results from prior research that indicate that the value relevance of accounting has declined. For the regressions for PRICE, value relevance has declined over time. The mean adjusted R 2 of the regression in the early period (1975 through 1989) is 79.3%, in the later period (1990 through 2004) 75.3%.Footnote 14 The adjusted trend is significantly negative (ADJTREND = −0.41%). The return regressions show stronger evidence of a decline in value relevance. The mean adjusted R 2 for the return regressions declines significantly from 30.9 to 24.8% from the early period to the later period, and the adjusted trend is significantly negative (ADJTREND = −0.29%). Finally, the market-adjusted perfect foresight returns decline from an average of 41.3% in the early period to 37.1% in the later period, but the adjusted trend in the perfect foresight returns is insignificant (ADJTREND = −0.09%).

Our findings corroborate prior research that shows that conservatism has increased over time and that value relevance from regressions for price and returns has declined. These two phenomena might coexist but be unrelated or the increase in conservatism may have tempered the decline in value relevance. In the following section, we test whether the decline in value relevance is associated with increasing conservatism.

5 Results

5.1 Price value relevance

We first analyze trends in price value relevance. The results are presented in Table 4. Panel A presents the results for groups based on BR-CONS. The first set of columns presents results for firms with a low level of conservatism. For firms with low and steady conservatism, average value relevance declines significantly from 84.9% in the early period to 81.3% in the later period. For firms with low and increasing conservatism, average value relevance increases from 84.9% in the early period to 86.8% in the later period. The difference in the changes over time (1.9% for increasing vs. −3.5% for steady) is significant. Similar patterns are observed with the trends in value relevance, with firms with low and steady BR-CONS experiencing significantly negative trends in value relevance (ADJTREND = −0.20%) and firms with low and increasing BR-CONS experiencing no significant decline (ADJTREND = −0.12%).

The next set of columns presents results for firms with high conservatism. Again, the decline in value relevance is observed in firms with steady conservatism as opposed to firms with increasing conservatism. For the steady conservatism group, mean value relevance drops significantly from 83.5% in the early period to 75.8% in the later period, a decline of −7.7% (t-stat = −2.70). For the increasing conservatism group, value relevance also declines, from 82.0% in the early period to 77.9% in the later period, but the decline is insignificant (t-stat = −1.30). Significant negative trends in value relevance are observed for firms with steady conservatism (ADJTREND = −0.23%) but not for firms with increasing conservatism (ADJTREND = −0.08%).Footnote 15 If the decline in value relevance was driven by increasing conservatism, we should have observed a greater value relevance decline in firms with increasing conservatism. Instead, we observe significant declines in value relevance only in firms with steady conservatism. Hence, increasing conservatism could not have driven the decline in value relevance.

Panel B of Table 4 repeats the analysis using groups based on trends in C-SCORE. For low conservatism groups, average value relevance remains steady between the early and later periods for both the steady and increasing conservatism subgroups. A significantly negative trend is observed only for the group with steady conservatism (ADJTREND = −0.19%) and not for the group with increasing conservatism (ADJTREND = 0.08%).Footnote 16 Both the steady and increasing conservatism subgroups in the high conservatism groups exhibit similar patterns. For the high and steady conservatism subgroup, average value relevance declines significantly from 82.0% in the early period to 72.9% in the later period. For the high and increasing conservatism subgroup, the decline in average value relevance is less pronounced (82–76.7%) but still significant. The trends in value relevance are similar and insignificant for both subgroups.

To conclude, there is no evidence that increasing conservatism drives the decline in price value relevance. In fact, using BR-CONS, significant declines in value relevance are observed only for firms with steady conservatism.

5.2 Returns value relevance

We next analyze the trends in returns value relevance. Panel A of Table 5 presents results based on levels of and trends in BR-CONS. The first set of columns presents results for firms with a low level of conservatism. While for firms with low and steady conservatism, average value relevance declines significantly from 37.3% in the 1975 through 1989 period to 33.4% in the 1990 through 2004 period, for firms with low and increasing conservatism, average value relevance increases significantly from 36.8% in the early period to 42.3% in the later period, and the difference in the changes over time (5.5% for increasing vs. −3.8% for steady) is significant. Similar patterns are observed for trends in value relevance. While firms with low and steady BR-CONS experience negative trends in value relevance (ADJTREND = −0.18%), firms with low and increasing BR-CONS see a significantly positive trend (ADJTREND = 0.30%). The difference in the adjusted trend (0.30% for increasing vs. −0.19% for steady) is significant.

The next set of columns presents results for firms with high conservatism. The decline in value relevance is stronger for firms with steady conservatism than for those with increasing conservatism. Mean value relevance declines, for firms with steady conservatism, significantly from 35.8% in the early period to 22.4% in the later period, a drop of −13.4% (t-stat = −4.76), and for firms with increasing conservatism, less significantly from 38.4% in the early period to 29.5% in the later period (t-stat = −2.52). The difference in the changes over time (−8.9% for increasing vs. −13.4% for steady) is, however, insignificant. Similarly, more significant declines are observed in the trends of value relevance for firms with steady (ADJTREND = −0.67%) than for firms with increasing conservatism (ADJTREND = −0.36%), but the differences in trends are insignificant.Footnote 17

Panel B of Table 5 repeats the analysis for groups based on C-SCORE. Average value relevance declines significantly from 42.1% in the early period to 37.2% in the later period for firms with low and steady conservatism, while it increases slightly from 40.0% in the early period to 41.1% in the later period for firms with low and increasing conservatism. The trends, however, are insignificant for both subgroups. Among the high conservatism groups, we see for the first time evidence of increasing conservatism being associated with a steeper drop in value relevance. The value relevance for the high and steady conservatism group declines insignificantly, from 32.7% in the early period to 26.4% in the later period. The corresponding decline for the high and increasing conservatism group, from 31.8% to 20.2%, albeit more pronounced, is driven by the 2 years that correspond to the bubble period (1998 and 1999). The trends between the two subgroups are almost identical (ADJTREND = −0.60% for the steady group vs. −0.54% for the increasing group), suggesting that although returns value relevance has declined, the decline is virtually identical for firms with increasing and firms with steady conservatism. Hence, it is implausible to attribute declines in returns value relevance to increasing conservatism.

5.3 Perfect foresight returns

We finally analyze trends in the market-adjusted returns earned by perfect foresight of earnings and book values using the methodology described in the research design section (Sect. 3.1.3). Results are presented in Table 6.

Panel A of Table 6 presents the results for groups based on BR-CONS. The first set of columns shows the results for firms with a low level of conservatism. For firms with low and steady conservatism, average market-adjusted perfect foresight returns decline significantly from 47.7% in the early period to 41.0% in the later period. For firms with low and increasing conservatism, the decline in perfect foresight returns (from 41.8 to 39.2%) is insignificant. Similar patterns are observed with the adjusted trends in perfect foresight returns. Firms with low and steady BR-CONS experienced a significant negative trend in perfect foresight returns (ADJTREND = −0.36%), while firms with low and increasing BR-CONS showed no significant decline (ADJTREND = −0.15%). Hence, among firms with low conservatism, the decline in perfect foresight returns is observed not in firms with increasing conservatism but rather in those with steady conservatism.

The next set of columns presents the results for firms with high conservatism. Here, too, we observe the decline in perfect foresight returns not in the increasing conservatism group, but in the steady conservatism group. Average market-adjusted perfect foresight returns drops, for firms with steady conservatism, significantly from 40.5% in the early period to 32.6% in the later period, a decline of −7.9% (t-stat = −2.17), and for firms with increasing conservatism, from 38.4% in the early period to 34.5% in the later period, the latter decline being insignificant (t-stat = −1.01). The adjusted trends are however insignificant for both the steady subgroup (ADJTREND = −0.25%) as well as the increasing conservatism subgroup (ADJTREND = 0.02%).

Panel B of Table 6 repeats the analysis using groups based on trends in C-SCORE. Average perfect foresight returns change insignificantly between the early and later periods for both the steady conservatism and increasing conservatism subgroups of the low conservatism groups. However, the trend observed for the steady conservatism subgroup is insignificant (ADJTREND = −0.19%), while the trend for the increasing conservatism subgroup is significantly positive (ADJTREND = 0.34%) and significantly higher than the trend for the steady conservatism subgroup. Similar patterns are exhibited by the steady and increasing conservatism subgroups of the high conservatism groups. Average perfect foresight returns dropped, for the high and steady conservatism subgroup, significantly from 43.1% in the early period to 32.8% in the later period, and for the high and increasing conservatism subgroup, from 42.1 to 32.3%, a less pronounced but still significant decline. The trends in value relevance however indicate a marginally greater decline in perfect foresight returns for the increasing conservatism (ADJTREND = −0.50%, t-stat = −2.72) than for the steady conservatism (ADJTREND = −0.34%, t-stat = −1.48) subgroup, although the differences in the trends are insignificant.

Combining the results for the groups based on trends in BR-CONS and C-SCORE, we conclude that there is limited evidence that increasing conservatism is responsible for the decline in perfect foresight returns. In fact, for the BR-CONS measure, we find significant declines in perfect foresight returns only for the subgroup of firms with steady conservatism. The results, similar to those for the other two specifications, are slightly weaker using C-SCORE as the conservatism measure. However, we fail to find any evidence that the decline in value relevance is significantly more pronounced for the subgroup of firms with increasing conservatism.

5.4 Value relevance of adjusted numbers

The results thus far fail to show increasing conservatism to be associated with declining value relevance. However, our tests do not compare the effects of conservative and nonconservative accounting on the same firm. An alternate approach is to adjust the reported accounting numbers to undo conservatism and test whether the value relevance of adjusted accounting information displays similar declines in value relevance. If the decline in value relevance is due to accounting conservatism, we should observe an increase in value relevance post-adjustment. Further, the decline in value relevance should weaken after the adjustment is made, as firms are becoming increasingly conservative.

We adjust the balance sheet by adding back the tax-adjusted C-SCORE to shareholders’ equity. We adjust the income statement in two steps. First, we use the change in LIFO reserve to estimate the impact on cost of goods sold. Second, we capitalize and amortize R&D and advertising using the same amortization periods used to calculate C-SCORE (5 years for R&D, 2 years for advertising). The impact on net income is measured as the tax adjusted effect of changes in cost of goods sold and advertising and R&D expense.Footnote 18 We use the adjusted EPS and BVPS numbers for our value relevance regressions and to estimate perfect foresight returns. As a benchmark, we compare the value relevance using adjusted numbers with the value relevance of unadjusted numbers from Table 3. The results are presented in Table 7.

The first set of columns presents the results for price value relevance. Inconsistent with increasing conservatism lowering value relevance, value relevance declines in each year. Average value relevance declines in the early period from 79.3% with reported numbers to 74.1% with adjusted numbers (t-stat = −2.23). In the later period, average value relevance declines from 75.3% with reported numbers to 72.7% with adjusted numbers, but the decline is insignificant (t-stat = −0.84). The difference in the changes across time periods between reported and adjusted numbers is insignificant. Further, trends in price value relevance appear to be similar for reported (ADJTREND = −0.41%) and adjusted (ADJTREND = −0.36%) numbers.

In the next set of columns, which presents the results for returns value relevance, the adjustments improve value relevance in only four of the 30 years. Average value relevance declines marginally in both the early and later periods after adjustments. The decline in average value relevance between the early and later periods is similar for reported (30.8–24.7%) and adjusted (29.5–24.3%) numbers, and the declining trend persists post-adjustment.

The final set of columns presents the results for perfect foresight tests. Here, we find weak evidence that adjusting accounting numbers for conservatism improves perfect foresight returns. Average market-adjusted perfect foresight returns increase from 41.3 to 43.9% in the early period, and from 37.1 to 38.6% in the later period, but the increases are insignificant. However, we find a steeper decline in value relevance post-adjustment. ADJTREND increases from an insignificant −0.09% for reported numbers to a significant −0.25% for adjusted numbers, inconsistent with adjustment arresting the decline in value relevance.

Overall, the results in Table 7 fail to provide evidence that increasing conservatism drives declining value relevance. The value relevance of numbers adjusted for conservatism is generally lower. Further, the trends in value relevance are either similar or more negative post-adjustment.

5.5 Sensitivity analysis

5.5.1 Alternate specifications for value relevance

In our regressions, we allow separate slope and intercept coefficients for profitable firms and loss making firms, consistent with the most recent literature. However, this is potentially not innocuous in the setting examined here, because accounting conservatism can increase the incidence of losses that in turn reduce value relevance. In other words, the controls for losses bias against finding a decline in value relevance among firms with high and increasing conservatism. As a sensitivity analysis, we repeat our analyses without allowing for separate slopes and intercepts for loss making firms. For brevity, the results are not tabulated but described below.

For the entire sample, the decline in price value relevance is more pronounced when we omit controls for losses (ADJTREND = −0.56%, compared to −0.41% in Table 3). We condition on the levels and growth in both BR-CONS and C-SCORE respectively as in Table 4 and find essentially similar results. Firms with low and steady BR-CONS experience significantly negative trends in value relevance (ADJTREND = −0.28%), while firms with low and increasing BR-CONS experiencing an insignificant decline (ADJTREND = −0.18%). Similarly, firms with high and steady BR-CONS experience significantly negative trends in value relevance (ADJTREND = −0.48%), while firms with high and increasing BR-CONS experience an insignificant decline (ADJTREND = −0.21%). For groups based on C-SCORE, firms with low and steady C-SCORE experience a significant negative trend in value relevance (ADJTREND = −0.34%), while firms with low and increasing BR-CONS experienced no significant decline (ADJTREND = 0.02%). For firms with high C-SCORE, the trends in price value relevance are now significantly negative. However, the trends are similar for both firms with steady C-SCORE (ADJTREND = −0.49%) and firms with increasing C-SCORE (ADJTREND = −0.47%). Hence, we do not find any evidence that increasing conservatism is associated with a steeper decline in value relevance.

We repeat the analysis without allowing for industry specific intercepts and slopes and find that, while the level of value relevance is lower, the patterns in the trends are unaffected. Lastly, we conduct similar analysis for the returns value relevance regressions and find that the patterns in the trends are essentially unaltered. Hence, our basic finding that increasing conservatism is not associated with a decline in value relevance is not driven by our decision to allow for controls for losses and industry membership.

5.5.2 Replication of Francis and Schipper (1999) and Lev and Zarowin (1999)

Our results are consistent with Francis and Schipper (1999), who find no statistically greater decline in value relevance among firms in high-technology industries, but inconsistent with Lev and Zarowin (1999), who find value relevance to decline in firms with increasing R&D intensity. As a sensitivity analysis, we replicate the tests of Francis and Schipper (1999) and Lev and Zarowin (1999) in the context of our paper. We continue to use our sample (1975 through 2004) and specification for the value relevance tests that includes controls for losses and allows for industry specific slopes and intercepts. Results are presented in Table 8.

Panel A of Table 8 presents the replication of Francis and Schipper (1999), who classify certain industries as high-technology based on “the extent to which accounting practices would generate unrecorded intangible assets.” Accordingly, we classify industries into high-technology and other based on industry average C-SCORE over the entire period. Industries with average C-SCORE greater than 6% are classified as high-technology. These include drugs and pharmaceuticals, computers, laboratory and medical equipment, and semiconductors.Footnote 19

For the price value relevance and returns value relevance tests, average change in value relevance between the early and later periods is almost identical for high-technology and other firms. The adjusted trends are also similar. Perfect foresight returns do decline significantly for high-technology firms, from 41.5% in the early period to 32.1% in the later period, but this is clearly driven by the bubble years (1998 through 2000) which had the largest impact on high-technology firms. Indeed, the adjusted trend is insignificantly negative for high-technology firms.

We next replicate the key analysis in Lev and Zarowin (1999), who partition their sample into four groups based on R&D intensity in early and later periods. We follow a similar approach using BRCONS and C-SCORE. We require firms to have at least three observations in the early (1975 through 1989) and later periods (1990 through 2004) to reduce survivorship bias. Firms are classified into low and high groups based on average level of conservatism compared to the sample mean. If increasing conservatism drives declining value relevance, we should see the greatest decline in firms that were less conservative in the early period and more conservative later.

Panel B of Table 8 presents the analysis for groups based on BR-CONS. The sub-sample of increasingly conservative firms experiences a slight decline in average price value relevance (86.4–83.1%), but the decline is insignificant and insignificantly different from the changes for other groups. For returns, this is the only group to experience an increase in value relevance (from 50.5 to 56.5%). Panel C of Table 8 presents the analysis for groups based on C-SCORE. As the results indicate, only the group with increasing conservatism shows an increase in average price value relevance (77.7–82.1%). Further, the decline in returns value relevance is smallest for firms with increasing conservatism (38.7–36.0%). In summary, the results are inconsistent with increasing conservatism driving a decline in value relevance.

How does one reconcile these results with Lev and Zarowin’s (1999) observed decline in value relevance? We offer three potential explanations. First, Lev and Zarowin (1999) focus exclusively on R&D, while we measure conservatism more comprehensively. Second, our analysis controls for losses and industry membership, although as the sensitivity tests indicate, this does not drive our results. Third, the sample periods differ.

6 Conclusion

The decline in the value relevance of accounting information has been the focus of much academic research, with increasing conservatism in accounting commonly cited as a driving force behind this decline. This paper explicitly tests this assertion by examining the association between the trends in value relevance and conservatism.

We use two measures of conservatism, BR-CONS, a comprehensive metric of the extent to which book values are biased downwards, based on Beaver and Ryan (2000), and C-SCORE, a measure, developed in Penman and Zhang (2002), of the downward bias in book values that results from the most commonly observed conservative accounting practices—the expensing of R&D and advertising and use of LIFO inventory valuation. We examine the trends in value relevance for firms conditioned on levels of and trends in conservatism. We measure value relevance using three approaches, the adjusted R 2 of regressions of price on contemporaneous earnings and book value, the adjusted R 2 of regressions of returns on contemporaneous scaled earnings and changes in earnings, and market-adjusted perfect foresight returns.

We find little support for the assertion that increasing conservatism drives the decline in value relevance. Specifically, we cannot, in any specification, show that firms with increasing conservatism experience a greater decline in value relevance relative to firms with steady conservatism. In fact, we generally observe the most significant decline in value relevance in firms where conservatism has not been increasing. Further, when we adjust income statements and balance sheets for the effects of conservatism, we find the value relevance of adjusted financials to be generally lower and trends in value relevance to be unaffected.

These results make it implausible that increasing conservatism is driving any decline in value relevance and hence can be of interest of accounting policy makers. Typically, arguments are made ascribing the decline in value relevance to increasing conservatism. However, we show that the decline in value relevance is either the same or less pronounced for groups with increasing conservatism as compared to groups with steady conservatism. One interpretation of this result is that the increased reliability conferred by conservatism has not come at the expense of declining relevance of accounting information for valuation. In other words, there does not appear to be a tradeoff between relevance and reliability, contrary to what many opponents of conservatism have argued. This is potentially important to consider in the light of recent moves towards fair value accounting, which typically reduce conservatism in financial statements.

Notes

This tradeoff is discussed in depth in the FASB’s Conceptual Framework (FASB 1980; FASB 2004).

Results are virtually identical if we use the average adjusted R 2 from 48 separate industry regressions each year.

The trend in incremental adjusted R 2 for loss adjustment is a significant +0.13% per year. The trend for industry controls is insignificant. Given the substantial improvement in adjusted R 2, we continue to use industry controls.

Brown et al. (1999) also recommend using scalars such as total assets and sales as deflators for per-share regressions. We rerun the price regressions scaling by assets or sales. Results and trends across groups are similar and not tabulated.

Results are virtually identical if we estimate the regressions using book-to-market as the dependent variable and the negative of the sum of the time and firm-fixed effect as our measure of conservatism.

Results are virtually identical if we set missing returns to the market return instead of zero.

Correspondingly declines in activities subject to conservative accounting lead to decreases in the downward bias on book values and create an upward bias in income.

From footnote 2, page 354 of Lev and Zarowin (1999).

We measure the trend in conservatism for a firm in year t by running firm-specific regressions with BR-CONS or C-SCORE in years t − 4 to t as the dependent variable and year as the independent variable, ensuring that at least three years of data are available. We use a trend-based approach instead of year-over-year changes in conservatism because conservatism measures (especially BR-CONS) can be unstable over short periods.

The results are similar if we exclude utilities and financial services.

The results are similar without the deletion of extreme observations.

BR-CONS measures conservatism after controlling for delayed recognition of gains and losses. As it can be affected by past application of conditional conservatism, it is unlikely to be perfectly correlated with C-SCORE.

FASB statements that have precipitated increased conservatism include SFAS 68 (Research and Development Arrangements, 1982), SFAS 106 (Employer's Accounting for Postretirement Benefits Other Than Pensions, 1992), and SFAS 123 (Accounting for Stock-Based Compensation, 1995 revised 2004). However, the accounting standards related to the expensing of R&D (SFAS 2, issued 1974) have stayed constant throughout the period analyzed.

The average value relevance reported in this paper (77.3% across 30 years) is higher than that reported in prior research. As seen in Fig. 1a, b, this is largely attributable to the controls for losses and industry. Adding variables such as R&D, advertising, and sales growth to the regression leads to insignificant increases in adjusted R 2 (less than 2%), considerably lower than the incremental R 2 for the controls for losses and industry. This validates the use of earnings and book values as summary statistics for the value relevance of accounting.

The difference in adjusted trends, 0.15%, is insignificant (t-stat = 0.82). If the difference had been 0.30%, the t-stat would have been 1.65, significant at the 10% level.

The difference in adjusted trends between the groups is 0.27%, marginally insignificant with a t-stat of 1.52. A difference of 0.293% would have been significant at the 10% level.

The difference in adjusted trends between the groups is 0.31%, insignificant with a t-stat of 1.16. A difference of 0.44% would have been significant at the 10% level.

We use a tax rate of 35% for our tax-adjustment of the balance sheet and income statement. Results are virtually identical if we use a time varying rate of taxes based on prevailing corporate tax rates.

Francis and Schipper’s (1999) classification uses average R&D intensity by 3-digit SIC code over the 1950 through 1981 period. We use the Fama and French’s (1997) industry classification over our sample period (1975 through 2004). Results remain similar if we use the exact industry classification they do. The 6% threshold ensures that the number of observations in the high-technology and other groups is similar.

References

Barth, M. E., Beaver, W. H., & Landsman, W. (2001). The relevance of value relevance research for financial accounting standard setting: Another view. Journal of Accounting and Economics, 31, 77–104.

Basu, S. (1997). The conservatism principle and the asymmetric timeliness of earnings. Journal of Accounting and Economics, 24, 3–37.

Beaver, W., & Ryan, S. (2000). Biases and lags in book value and their effects on the ability of the book-to-market ratio to predict book return on equity. Journal of Accounting Research, 38, 127–148.

Beaver, W., & Ryan, S. (2005). Conditional and unconditional conservatism in accounting: Concepts and modeling. Review of Accounting Studies, 10, 269–309.

Blair, M. & Wallman, S. (2001). The growing intangibles reporting discrepancy from unseen wealth: Report of the Brookings task force on intangibles.

Bliss, J. H. (1924). Management through accounts. New York, NY: The Ronald Press Co.

Brown, S., Lo, K., & Lys, T. (1999). Use of R2 in accounting research: Measuring changes in value relevance over the last four decades. Journal of Accounting and Economics, 28, 83–116.

Collins, D., Maydew, E., & Weiss, I. (1997). Changes in the value relevance of earnings and book values over the past 40 years. Journal of Accounting and Economics, 24, 39–68.

Core, J., Guay, W., & Van Buskirk, A. (2003). Market valuations in the new economy: An investigation of what has changed. Journal of Accounting and Economics, 34, 43–67.

Dontoh, A., Radhakrishnan, S., & Ronen, J. (2004). The declining value-relevance of accounting information and non-information-based trading: An empirical analysis. Contemporary Accounting Research, 21, 795–812.

Easton, P., & Harris, T. (1991). Earnings as an explanatory variable for returns. Journal of Accounting Research, 29, 19–36.

Elliott, R., & Jacobsen, P. (1991). U. S. accounting: A national emergency. Journal of Accountancy, 172(5), 54–58.

Fama, E., & French, K. (1997). Industry costs of equity. Journal of Financial Economics, 43, 153–193.

Francis, J., & Schipper, K. (1999). Have financial statements lost their relevance? Journal of Accounting Research, 37, 319–352.

Givoly, D., & Hayn, C. (2000). The changing time-series properties of earnings, cash flows, and accruals: Has financial reporting become more conservative? Journal of Accounting and Economics, 29, 287–320.

Hayn, C. (1995). The information content of losses. Journal of Accounting and Economics, 20, 125–153.

Holthausen, R. W., & Watts, R. (2001). The relevance of the value relevance literature for financial accounting standard setting. Journal of Accounting and Economics, 31, 1–75.

Jenkins, E. (1994). An information highway in need of capital improvements. Journal of Accountancy, 177(5), 77–82.

Kieso, D., Weygandt, J., & Warfield, T. (2004). Intermediate accounting. New York, NY: Wiley.

Klein, A., & Marquardt, C. (2006). Fundamentals of accounting losses. The Accounting Review, 81, 179–206.

Lev, B., & Sougiannis, T. (1996). The capitalization, amortization, and value-relevance of R&D. Journal of Accounting and Economics, 21, 107–138.

Lev, B., & Zarowin, P. (1999). The boundaries of financial reporting and how to extend them. Journal of Accounting Research, 37, 353–385.

Nakamura, L. (2003). A trillion dollars a year in intangible investment and the new economy. In J. Hand & B. Lev (Eds.), Intangible assets. Oxford: Oxford University Press.

Penman, S. (2009). Accounting for intangible assets: There is also an income statement. Abacus, 45, 358–371.

Penman, S., & Zhang, X. (2002). Accounting conservatism, the quality of earnings, and stock returns. The Accounting Review, 77, 237–264.

Revsine, L., Collins, D., & Johnson, B. (2005). Financial reporting and analysis. Upper Saddle River, NJ: Prentice Hall.

Sever, M., & Boisclaire, R. (1990). Financial reporting in the 1990s. Journal of Accountancy, 170(5), 36–41.

Sterling, R. (1967). Conservatism: The fundamental principle of valuation. Abacus, 3(2), 109–132.

Stewart, B., I. I. I. (2002). Accounting is broken, here’s how to fix it. A radical manifesto. Evaluation, 5(1), 1–32.

Watts, R. (2003). Conservatism in accounting Part I: explanations and implications. Accounting Horizons, 17, 207–221.

Acknowledgments

We thank Steve Ryan (the editor), two anonymous referees and seminar participants at Cornell University, Harvard Business School, IIM-Bangalore, INSEAD, Rice University, Seton Hall University, Yale University, JAAF Conference, Baruch/Columbia/NYU/Rutgers Four Schools Conference, and HKUST Summer Accounting Symposium.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Balachandran, S., Mohanram, P. Is the decline in the value relevance of accounting driven by increased conservatism?. Rev Account Stud 16, 272–301 (2011). https://doi.org/10.1007/s11142-010-9137-0

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11142-010-9137-0