Abstract

This study examines the dynamic impact of financial development, energy consumption, trade openness, and economic growth on carbon dioxide (CO2) emissions in Nigeria. We applied autoregressive distributed lag bound testing technique for the period of 1971–2010. The empirical result shows a long-run cointegration relationship among the variables. The long-run estimation result, however, reveals that, economic growth, development of the financial sector and energy consumption have a positive and significant impact on carbon dioxide emissions, whereas trade openness has negative and significant impact on carbon dioxide emissions. The finding suggest that the government should emphasize programs and policies that reduce carbon dioxide emissions by opening the trade sector considering the roles such openness plays in reducing environmental degradation in the country, which directly enhances environmental quality.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

One of the main aims of every economy is to safeguard the environment from continuous degradation due to the incessant problems emanating from environmental decay that hugely costs various governments. Presently, the problem of global warming is among the most serious issues that bother industrialized, emerging, and developing countries because of its consequences of reducing environmental quality. The literature has established that ozone layer depletion is attached to carbon dioxide (CO2) emissions and is the prime cause of global warming (Alam et al. 2012). Recently, the 2015 G-7 general meeting concentrated more on de-carbonation of the global environment through the reduction of carbon dioxide emissions. Recently financial sector performance is linked to other main economic sectors that consume considerable energy which might also affect the environmental quality despite of the sectoral and overall economic growth. According to Yusuf (2014), in Nigeria, 75% of energy consumed comes from fossil fuel; this means that higher consumption of energy leads to higher CO2 emissions in the country. Although firms need substantial amounts of capital to initiate or expand their existing businesses, the expansion of existing or initiation of new businesses might be connected to higher carbon dioxide emissions if the machinery used pollutes the environment and reduces its quality.

Few studies have recently documented the links between financial development, energy consumption and pollution for different regions/countries. These studies found divergent results, some studies established a direct links between energy consumption, and pollution e.g. Tang and Tan (2014), and Islam et al. (2013) in the case of Malaysia, Zhang (2011) in China, Sadorsky (2010, 2011) in the case of Central and Eastern Europe, and Çoban and Topcu (2013) in the case of European Union (EU). This means that financial development and energy consumption increases environmental degradation. Other studies however, found an opposite results, that is financial development improves environmental quality through reduction of carbon dioxide emissions, notable among them includes; Tamazian and Rao (2010) across transition countries, Shahbaz et al. (2013a, b) in Indonesia and Jalil and Feridun (2011) in the case of China. While, Ozturk and Acaravci (2013) found no any substantial effect of financial sector development on CO2 emissions in Turkey, Ali et al. (2015) also concluded that, energy consumption has no any significant impact on financial development in Nigeria.

This study examines the dynamic impact of financial development on CO2 emissions in Nigeria.We control the model specification with energy consumption, trade openness, and economic performance. Despite the huge amount of human and natural resources in the country, which result in it being among the most polluting nations in Africa, and its contributions to accumulating CO2 emissions (see Fig. 1), studies on financial development and other macroeconomic environmental variables are still scarce in the existing literature. Therefore, it is essential to examine this relationship in the context of Nigeria. This study contributes to the literature in three aspects. First, the method we use address the small sample size which is ARDL and compare with the multivariate Johansen test to see the long-run and short-run causality. Second, this issue is not being address in the case of Nigeria. Third, two financial development indicators are used in the analysis namely; domestic credit to the private sector as a percentage of GDP, and domestic credit provided by financial sector as a percentage of GDP. The rest of this paper is organized as follows; “Review of related literature” section reviews the related literature, “Nigeria’s energy sector in brief” section briefly explain the Nigeria’s energy sector; “Econometric methodology and model” section lays out the empirical models, econometric methodology and data; “Estimation results” section offers discussion of the empirical findings. Last, “Conclusion and policy recommendations” section concludes and proposes policy recommendations.

Carbon emissions of selected African countries

Review of related literature

Many studies investigate the relationship between the variable of interest and other control variables in countries across the globe, for example Oh and Lee (2004) examine the link between energy consumption and economic growth for 1981Q1–2000Q4 based on the vector error correction model (VECM). The result shows that no causal link exists in the short-run, while unidirectional causality runs from economic growth to energy consumption. Ang (2007) examines the connection among emissions, energy consumption and output in France for 1960–2000 based on cointegration and VECM techniques. The outcome reveals the presence of a long-run association among the variables. The result also suggests that economic growth stimulates energy consumption and pollution emissions. The causality test shows the existence of a unidirectional causal relationship running from energy consumption to economic growth in the short-run. Hye and Riaz (2008) investigate the association between energy consumption and economic growth during 1971–2007 in Pakistan. They used autoregressive distributed lag (ARDL) and Granger causality test. The short-run causality result shows a two-ways causal relationship between the variables, while a one-way causal relationship exist runs from growth of the economy to energy use in the long-term. Energy consumption does not affect economic growth in the long-run because increases in energy prices stimulate other commodity prices, which increases the costs of doing business and therefore detrimentally affects the economy.

Soytas and Sari (2009) examines the long-run Granger causality nexus between economic growth, carbon dioxide emissions and consumption of energy in Turkey during 1960–2000. The main finding shows that carbon emission Granger cause energy consumption, but no reverse causality found. Tamazian et al. (2009) examine the relationship between financial markets and economic development on environmental dilapidation in 1992–2004 based on the standard reduced form modeling technique across Brazil, Russia, India, and China (BRIC countries). The finding reveals that financial and economic developments affect environmental quality in the sample countries. Furthermore, the finding shows that higher levels of financial and economic growth lead to a reduction in environmental degradation. Financial liberalization and financial openness lead to reduction in CO2 emissions. Based on the ARDL method covering 1971–2006, Odhiambo (2009) studies the relationship between energy consumption and economic growth in Tanzania; the finding reveals the existence of one-way causality running from overall energy consumption to economic growth. Zhang and Cheng (2009) examine the direction of causality between economic growth, energy consumption, and carbon emissions in China, based on multivariate model of economic growth, energy use, carbon emissions, capital and urbanization during 1960–2007. The finding reveals the existence of unidirectional causality running from GDP to energy consumption, and one-way causality running from energy consumption to carbon emissions in the long run. The finding also suggests that energy consumption and carbon emissions do not leads economic growth.

Tamazian and Rao (2010) examine the dynamic links between financial market development, economic development, institutional quality, and environmental conditions. They applied standard reduced-form modeling method that control for country-specific unobserved heterogeneity and generalized method of moments (GMM) estimation that control endogeneity problems. The sample period covers 1993–2004 across 24 transition economies. The result support Environmental Kuznets Curve (EKC) presumption and the importance of institutional quality and financial development on environmental quality are also recognized in the findings. They also found that, liberalizing financial system without quality institutions is a detriment to environmental conditions.

Zhang (2011) investigates the impact of China’s financial market development on carbon emissions based on cointegration theory, Granger causality test, variance decomposition. The finding reveals that; the development of China’s financial market increases carbon emissions; this means financial market development in the country is attached with negative environmental consequences. It further highlights that; the impact of financial intermediation scale on carbon emissions is higher than that of the indicators of financial development, but it is weaker when consider its influence on the efficiency. When the stock market indicators are use as indicators of financial market development, the results shows that it has substantial on carbon emissions but its efficiency is inadequate. The result finally conclude that among the financial development indicators, FDI is regarded as has lower influence on carbon emissions, this might be connected with its volume in relation to GDP which is considers very low.

Al-mulali and Sab (2012a) investigate the impact of CO2 emissions on economic growth and financial development for 1980–2008 across 30 sub-Saharan African countries. The findings reveal that even with high levels of environmental pollution, energy consumption has a positive and significant impact on financial development and economic growth in the sample countries. Also, Al-mulali and Sab (2012b) examine the links among energy consumption, economic growth, and financial market development across 19 countries for 1980–2008 and report that; energy utilizations significantly affect financial development and economic growth. However, the development is attached to negative environmental consequences because it increases the rate of CO2 emissions in the sample countries. Chaudhry et al. (2012) investigate the impact of energy consumption on economic growth in Pakistan based on the ARDL framework covering 1972–2012. The result suggests that when the variable of oil measured energy use, its effect on economic performance is negative. Abid and Sebri (2011) apply VECM in Tunisia during 1980–2007 and examine the link between energy consumption and economic growth. The outcome shows that, overall, energy consumption promotes economic growth, but at the sectoral level energy consumption negatively affects economic growth. Based on bootstrap panel unit root tests and cointegration approaches, Arouri et al. (2012) study the relationship among CO2 emissions, energy consumption and economic growth through Middle East and North Africa (MENA) countries for 1981–2005. The result indicates that energy consumption has a positive and significant impact on CO2 emissions and a quadratic nature exists between economic growth and CO2 emissions in the region.

Hossain (2012) evaluates the causal relationship among CO2 emissions, energy consumption, economic growth, foreign trade and urbanization in Japan during 1960–2009. The results show that the more energy consumed in Japan, the higher the environmental degradation, but in the long-run the results show that economic growth, trade openness, and urbanization have no significant impact on environment quality. Alam et al. (2012) use VECM and the Granger-causality test to investigate the dynamic links among energy consumption, electricity consumption, CO2 emissions, and economic growth in Bangladesh. The result suggests a unidirectional causality running from energy consumption to economic growth in both the short-run and the long-run. However, bidirectional causality exists between electricity consumption and economic growth, but no causality exists in the short-run. Unidirectional causality also exists that runs from energy consumption to CO2 emissions, and CO2 emissions Granger-cause economic growth in both the short and long-run. Islam et al. (2013) examines the effect of financial development, economic growth, and population growth on energy uses in Malaysia. Their finding reveals that uses of energy positively affect financial development and economic growth in both the short-run and the long-run. However, the impact of population growth on energy consumption is only sustainable in the short-run. Govindaraju and Tang (2013) use the Granger causality approach and investigate the causal nexus among CO2 emissions, economic growth, and coal consumption in China and India. The results establish the long-run relationship among the variables in China but not in India. The causality result for China indicates the presence of unidirectional causality running from economic growth to CO2 emissions, and bidirectional causality existing between both economic growth and coal consumption and CO2 emissions and coal consumption. Conversely, in the case of India only short-run causality is present that is running from economic growth to CO2 emissions and from CO2 emissions to coal consumption, and two-way causality is seen in India. Unidirectional causality also exist that run from economic growth to coal consumption in India.

Shahbaz et al. (2013a) examine the link between energy consumption and economic growth by incorporating financial development and openness in trade in China. They applied ARDL approach during 1971–2011. The finding shows that energy consumption, financial sector development and trade have a positive and substantial impact on economic growth. Also Shahbaz et al. (2013b) apply ARDL and examine the dynamic links among economic growth, energy consumption, trade openness, development of the financial sector and CO2 emissions in Indonesia for 1975Q1–2011Q2. The results suggest that economic growth could increases the consumption of energy and CO2 emissions, whereas development of the financial sector and financial and trade liberalization reduce CO2 emissions. However, based on VECM, the causality result reveals the existence of the feedback hypothesis between consumption of energy and CO2 emissions, bi-directional causality between economic growth and CO2 emissions, and unidirectional causality running from development of the financial sector to CO2 emissions.

Çoban and Topcu (2013) uses the system-generalized method of moments (s-GMM) and examines the impact development of the financial sector on energy consumption across European Union (EU) member countries for 1990–2011. The finding shows that development of the financial sector has an essential impact on energy consumption among old EU member countries regardless of the indicator of financial development used. However, the impact on new member countries of the EU relies on the type of financial development indicator used; for example, when the banking sector indicator is applied, the effect shows an inverted U-shape whereas it demonstrate no significant link when the stock market indicator is used.

The dynamic impact of financial development, trade, economic growth, energy consumption and carbon emissions was investigated by Ozturk and Acaravci (2013) in Turkey. The study cover the period of 1960–2007 based on autoregressive distributed lags (ARDL) technique. The long-run relationship is established including the square of real income per capita as the first stage that will give the condition to proceed and estimate the long-run effects. The main finding suggests that, when the level of foreign trade to GDP ratio increases it lead to an increase in the level of per capita carbon emissions. This means foreign trade contributes to the reduction of environmental quality in Turkey as it increase the level of carbon emissions. It is however found that, financial development has no any significant impact on carbon emissions in the long-run. The result of the study also support Environmental Kuznets Curve (EKC) hypothesis in the study country. This means at the initial stage the level carbon emissions increases with the level of income, but when it reach the stabilization point level carbon emissions declines with income.

Mahalik and Mallick (2014) determine the nexus among consumption and energy, economic growth and financial development in India for the period of 1971–2009 using the ARDL approach. The finding reveals that energy consumption has a positive and significant impact on the ratio of urban population, but a negative impact on economic growth and financial development. The result also shows that urban population growth negatively affects economic growth, while energy consumption has a positive impact on it. Uçan et al. (2014) apply panel cointegration analysis and examine the impact of renewable and non-renewable energy consumption on economic growth for 15 EU member countries for 1990–2011. The finding shows the existence of a long-run relationship among the variables, and the Granger-causality test reveals unidirectional causality running from non-renewable energy consumption to economic growth. Osigwe and Arawomo (2015) apply Granger-causality approach and examine the causal nexus among energy consumption, oil price and economic growth in Nigeria. The result shows a bi-directional causal relationship between energy consumption and economic growth. However, when electricity is used as a proxy of energy consumption, bidirectional causality exists between energy consumption and economic growth as well as price of electricity and its uses. However, no causal relationship exists among kerosene consumption, kerosene prices and economic growth.

Based on the ARDL approach Ali et al. (2015) investigates the impact of financial development on energy consumption in Nigeria using quarterly data from 1972Q1–2011Q4. The finding suggests that variables are cointegrated as the null hypothesis is rejected at the 1% level of significance. The short-run result reveals that development of the financial sector and economic growth has a negative and significant impact on energy consumption, whereas energy prices have a positive and significant impact. The long-run result however, shows that the impact of financial development on energy consumption is negative and insignificant, while economic growth has a negative albeit significant impact on energy consumption and energy prices still remain positive and significant for energy consumption.

Chang (2015) applies Sadorsky (2010) and examines the marginal effect of financial development on energy consumption and income across 53 economies in 1999–2008. The result reveals that in developing and emerging market countries higher consumption of energy is consistent with increases in income, in developed countries, it temporarily increases with income up to a given threshold. When private and domestic credits are used as a measure of financial development, energy consumption increases with the level of financial development in low-income economies. Conversely, when stock market indicators represent financial development, consumption of energy marginally reduces with the level of financial development in advanced countries, but financial development rises with consumption of energy in higher income, emerging and developing countries.

Farhani and Ozturk (2015) empirically examine the causal nexus between CO2 emissions, real GDP, energy consumption, financial development, trade openness, and urbanization in Tunisia during 1971–2012. Moreover, they applied distributed lag (ARDL) bounds testing technique to cointegration and error correction method (ECM). The main empirical finding shows that financial development variable has a positive and significant impact on environmental pollution. This means development of the financial sector is at the detriment of the environmental pollution in Tunisia. The monotonic positive relationship is also found between GDP and CO2 emissions. This means the research does not support the idea of environmental Kuznets curve (EKC) hypothesis. The Granger causality result reveals that financial development is a significant factor that plays a key role in the Tunisian economy.

Ali et al. (2016) applied the heterogeneous panel model techniques of mean group (MG), pooled mean group (PMG), and panel cointegration, dynamic ordinary least squares (DOLS), and fully modified OLS (FMOLS) and examine the dynamic impact of biomass energy consumption on economic growth during 1980–2011 in selected sub-Saharan African countries. The result based on PMG, as the most preferred method suggests that biomass energy consumption, capital stock and human capital have a positive and significant impact on economic growth. When alternative techniques of panel cointegration, and DOLS and FMOLS are applied, variables are cointegrated based on panel cointegration, FMOLS and panel OLS results ratify what is obtained from PMG, while the finding based on DOLS reveal that biomass energy consumption and capital stock also have a positive and significant impact on economic growth and human capital became insignificant based on DOLS.

Rafindadi and Ozturk (2017) applied autoregressive distributed lag bounds test method to cointegration and the Bayer–Hanck combined cointegration test to examine the impact of financial development on energy consumption in South Africa. The model is however controlled with the variables of trade openness and economic growth. The main finding suggests that development of the financial sector is among the key determinants of energy demand in the country studied. Furthermore, the result shows that affluence positively influences energy consumption, and also trade openness increases the level of energy used. Nasreen et al. (2017) used bounds test for cointegration and Granger causality methods and examined the nexus among financial stability, economic growth, energy consumption and carbon dioxide (CO2) emissions in South Asian countries during 1980–2012. The key empirical finding reveals financial stability enhances the quality of South Asian environment. However, economic advancement, consumption of energy, as well as population density has adverse effects on environmental quality across the sample countries in the long-run. The finding of this study also support environmental Kuznets curve (EKC) hypothesis which presumes an inverted U-shaped exist between income and environmental condition. The Granger causality tests the evidence unidirectional causality running from financial stability to CO2 emissions Pakistan and Sri Lanka.

Salahuddin et al. (2018) applied autoregressive distributed lag (ARDL) bounds testing approach using Kuwait data for the period 1980–2013. The objective is to investigate the effects of economic growth, electricity consumption, foreign direct investment (FDI), and financial development on environmental quality. The key empirical findings reveal that; economic growth, electricity consumption, and FDI enhance carbon dioxide emissions both in the short and long-run. However, the VECM Granger causality result shows that; economic growth, and electricity consumption Granger-causes carbon dioxide emissions.

Nigeria’s energy sector in brief

Nigeria is currently the sixth largest oil producer in the global oil market and has an estimated reserve of 36.2 billion barrels; it is the most populated black nation with more than 150 million people based on the latest (2006) census estimates. Nigeria and South Africa demand more than 40% of energy in the African sub-region (World Energy Outlook 2014), and Nigeria is the second country after Algeria in terms of gas deposits in the African continent (Sambo 2008). Based on the Energy Information Administration (EIA)Footnote 1 report of 2010, energy consumption in Nigeria is about 4.4 quadrillion Btu (111,000 kilotons of oil equivalent) and 82% of the amount consumed is from traditional biomass and waste. The real data in Fig. 1 shows the distribution of carbon emission of some African countries. It shows that Nigeria is among the most polluting nations in Africa, Angola is second to Nigeria in the series albeit with a very wide margin.

Econometric methodology and model

To specify ARDL form of vector error correction model, we followed Khan et al. (2005), Fosu and Magnus (2006), and the model is specify as follows:

where \({ \ln }CO_{2}\) is the log of CO2 emissions, \({ \ln }FD\) is the log of financial development, \({ \ln }EC\) is the log of energy consumption, \({ \ln }Y\) is the log of economic growth, \({ \ln }TO\) is the log of trade openness and subscript t denote time period. Initially, we estimated Eq. (1) based on OLS followed by testing Wald test of F-test in order to test the joint significance of the coefficients of lagged variables with a view to observe if long-run relationship among the variables is present.

The next step is to test the null hypothesis \(H_{0 }\) = \(\beta_{1 }\) = \(\beta_{2 }\) = \(\beta_{3 }\) = \(\beta_{4 }\) = \(\beta_{5 }\) = 0 which indicated that there is no cointegration against alternate \(H_{a } \ne \beta_{1 } \ne \beta_{2 } \ne \beta_{3 } \ne \beta_{4 } \ne \beta_{5 } \ne 0\) which indicated that there is cointegration among the variables. Pesaran et al. (2001) suggested that if the value of the calculated F-test is larger than the upper bound critical value, null hypothesis of no cointegration will be rejected which suggests the existence of long-run relationship. While, if the value of estimated F-test is below the critical value null hypothesis cannot be rejected which means there is no long-run relationship, and if the value of the estimated F-test is within lower and upper critical value the result remains inconclusive (Pesaran and Pesaran 1997). The long-run coefficients of ARDL will be tested based on Eq. (2):

Schwarz Bayesian Criterion (SBC) is used to select lag length of the model and applied error correction model in order to determine short-run relationships of the variables;

We followed Pesaran and Pesaran (1997) in order to test the stability of the long-run coefficients and the short-run dynamics through the use of cumulative sum of recursive residuals (CUSUM) and the cumulative sum of squares of recursive residuals (CUSUMSQ).

Data

The data used for this study range from 1971 to 2010 and are all obtained from World Development Indicators (WDI 2015), World Bank. We use CO2 emissions in kilo terms (kt) as a proxy of CO2 emissions, and domestic credit to the private sector as a ratio of gross domestic product (GDP) is a proxy to measure financial development. Energy consumption is measured by fossil fuel consumption that involving coal, oil, petroleum, or natural gas products, real GDP is used as a proxy of economic growth, and the sum of exports and imports as a ratio of GDP is used to measure trade openness. The descriptive statistics and correlation of the variables is presented in Tables 1 and 2 respectively. The variables shows no much correlation which means we don’t have problem of multicollinearity in the series.

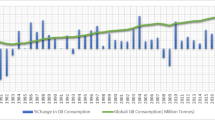

Figure 2 depicts the time plots of the variables used in the analysis. The distribution of the CO2 emissions, financial development, energy consumption, economic growth, and trade openness is presented during 1971–2010. As shown in Fig. 2, the CO2 emissions keep increasing in Nigeria from 2000 and decline slightly around 2007–2009. This may be due to global financial crisis, but it rises in 2010 again as a result of increase in energy consumption. The financial development (FD) in the country is promoted and its performance keeps rising since 2005, compared to previous years the performance of the financial market is dwindling and it might be related to poor government economic policies in the country [e.g. Structural Adjustment Program (SAP)], but rises during 2005 and decline around 2009, which might also be related to global financial crisis.

Time plots series of the variables

The variable that capture economic growth (Y) is also shows a swing in nature, but increases from 2005 consistently up to 2010. This shows a country’s resilience in absorbing the shocks of the global financial crisis as the performance of the economy is not highly affected. The level of trade openness (TO) in Nigeria is quite volatile for the sample period; the plot depicted a higher level of trade openness around 2000 possibly due to democratic dispensation, but started declining around 2004 up to 2010. Therefore, we hypothesize the financial development has a strong link with the level of environmental quality, and the more energy is consumed, the higher the possibility of more carbon emissions and the end result will be higher pollution and consequently reduce environmental quality.

Estimation results

Before estimating the main model, we estimated unit roots based on augmented Dickey Fuller (ADF) and Phillips Perron (PP) to identify the order of integration of the variables. The ADF and PP unit root test results in Table 3 show that only energy consumption is stationary at level means is I(0) variable, while financial development, CO2 emissions, economic growth, and trade openness are non-stationary at level but become stationary after taking the first difference which means the four variables are I(1). ARDL is a suitable method to apply because the model can accommodate the combination of I(0) and I(1) variables (Pesaran et al. 2001).

Cointegration result

The ARDL cointegration test result is reported in Table 4, the calculated F-statistics (5.92) is larger than upper bound critical values as obtained in the Narayan table. This means the variables are cointegrated as we reject the null hypothesis at the 5% level of significance. Since the long-run relationship is established, we next estimate our Eq. (2) to obtain long-run coefficients; the result is shown in Table 5.

The finding reveals that, financial development has a positive and significant impact on CO2 emissions; this means that when financial development increases by 1% in Nigeria, it stimulates CO2 emissions to increase by 0.133%. Therefore, financial development is attached to negative environmental consequences as it creates more carbon emissions. This finding corroborates the findings of Al-mulali and Sab (2012b) across a sample of 19 countries and Al-mulali et al. (2015a, b) for 23 selected European countries suggesting that financial development reduces environmental quality; however, it calls into question the result found across 129 countries by Al-mulali et al. (2015a, b). The variable of economic growth also has a positive and significant impact on CO2 emissions, as a 1% increase in economic growth leads to a 0.687% increase in CO2 emissions; energy consumption is also positive and statistically significant on CO2 emissions, as 1% increase in energy consumption can lead to a 0.915% increase of CO2 emissions. The finding validates the result of Al-mulali and Sab (2012a) across 30 African countries. While trade openness has a negative and significant impact on CO2 emissions, it further reveals that when trade openness increases by 1% in Nigeria, it leads to a 0.530% decline of CO2 emissions; thus, trade openness does not increase CO2 emission but rather reduces it in the case of Nigeria. This finding is also in line with Al-mulali et al. (2015a, b).

As shown in Table 6, the short-run dynamics of the variables indicate that financial development, economic growth, and energy consumption have a positive and significant impact on increased CO2 emissions. However, trade openness does not have any significant impact on CO2 emission in the short-run. This means trade openness does not have any short-run impact on CO2 emission, but rather a long-run impact as shown by the long-run result above. The error correction term is negative and statistically significant, as expected by econometric theory and exhibits convergence from the short-run to the long-run (Banerjee et al. 1998). This reconfirms the existence of a long-run relationship among the variables. The error correction coefficient is 0.62 or 62% adjustment occurred in a year (annual data). This implies that for any deviation to achieve full adjustment (100%), it u take about the duration of 1.6 years to converge to long-run equilibrium.

To confirm the consistency and efficiency of the model, a diagnostic test is carried out and the result is reported in Table 7. The outcome of the four diagnostic tests of Lagrange multiplier, serial correlation, Ramsey’s misspecification, and Jacque–Bera normality and the autoregressive conditional heteroscedasticity tests show that our model passed all the four diagnostics tests because we cannot reject any hypothesis and this demonstrates the consistency and efficiency of our model. The stability of the model is also confirmed by the cumulative sum of recursive residuals (CUSUM) and cumulative sum of squares of recursive residuals (CUSUM of squares) in Figs. 3 and 4 respectively (refer to Appendix). The blue lines for both CUSUM and CUSUMSQ lie within the critical bounds and are significance at 5%, which means the model is highly stable over the sample period.

Plot of cumulative sum of recursive residuals

Plot of cumulative sum of square of recursive residuals

We also estimate Johansen and Julius (JJ) cointegration test. The result as reported in Table 8 shows that, there exists a long-run relationship among the variables as trace statistics is greater than the critical value at 5% level of significance. Therefore the JJ cointegration test confirms the earlier ARDL long-run relationship among the variables under investigation, and therefore substantiates the reliability of our main finding.

Robustness checks

To check the consistency and reliability of the main finding, we used an alternative indicator of financial development which is the domestic credit provided by financial sector as a percentage of GDP in order to verify our main finding. The finding is reported in Table 9 and reveals that, null hypothesis of no cointegration can be rejected at all the three significance level because the calculated F-statistics value is 19.83. Hence, we rely on 1% which is stronger statistically, and therefore the result confirmed our earlier finding of the main model, that the variables under investigation have long-run relationship.

Conclusion and policy recommendations

This study examines the dynamic links among CO2 emissions, energy consumption, trade openness, economic growth, and financial development in Nigeria. The ARDL bound test approach is applied for the period of 1971–2010. The F-test results show that these variables are cointegrated or there is a long-run relationship among the variables. The coefficients of the long-run result reveal that financial development, economic growth, and energy consumption have a positive and significant impact on CO2 emissions. The short-run dynamics relation reveals that financial development has positive and statistically significant determinant of CO2 emissions, while economic growth, energy consumptions, and trade openness have a negative and significant impact on CO2 emissions.

The policy implication suggested by the research outcome is that; policy makers in Nigeria are faced with two challenges of balancing between achieving high levels of financial development and improving environmental quality simultaneously, without which financial sector development could lead to massive environmental degradation considering its influence on triggering more CO2 emissions. The authority needs to explore alternative modes of energy consumption (e.g. green energy) to reduce the continuous environmental degradation in the country that is caused by excessive fossil fuel consumption which leads to higher CO2 emissions, depletion of the ozone layer, and hence increased global warming. Another policy alternative is to adopt suitable trade openness policies that will help in reducing the level of carbon dioxide emissions and hence improve environmental quality.

Notes

Details on EIA can be accessed at: http://www.eoearth.org/view/article/152513/.

References

Abid, M., & Sebri, M. (2011). Energy consumption–economic growth nexus: Does the level of aggregation matter? International Journal of Energy Economics and Policy, 2(2), 55–62.

Alam, M. J., Begum, I. A., Buysse, J., & Van Huylenbroeck, G. (2012). Energy consumption, carbon emissions and economic growth nexus in Bangladesh: Cointegration and dynamic causality analysis. Energy Policy, 45, 217–225.

Ali, H. S., Law, S. H., Yusop, Z., & Chin, L. (2016). Dynamic implication of biomass energy consumption on economic growth in Sub-Saharan Africa: Evidence from panel data analysis. GeoJournal, 82(3), 493–502.

Ali, H. S., Yusop, Z. B., & Hook, L. S. (2015). Financial development and energy consumption nexus in Nigeria: An application of ARDL bound testing approach. International Journal of Energy Economics and Policy, 5(3), 816–821.

Al-Mulali, U., Ozturk, I., & Lean, H. H. (2015a). The influence of economic growth, urbanization, trade openness, financial development, and renewable energy on pollution in Europe. Natural Hazards, 79(1), 621–644.

Al-Mulali, U., & Sab, C. N. B. C. (2012a). The impact of energy consumption and CO2 emission on the economic growth and financial development in the Sub Saharan African countries. Energy, 39(1), 180–186.

Al-mulali, U., & Sab, C. N. B. C. (2012b). The impact of energy consumption and CO2 emission on the economic and financial development in 19 selected countries. Renewable and Sustainable Energy Reviews, 16(7), 4365–4369.

Al-mulali, U., Tang, C. F., & Ozturk, I. (2015b). Does financial development reduce environmental degradation? Evidence from a panel study of 129 countries. Environmental Science and Pollution Research, 22, 14891.

Ang, J. B. (2007). CO2 emissions, energy consumption, and output in France. Energy Policy, 35(10), 4772–4778.

Arouri, M. E. H., Youssef, A. B., M’henni, H., & Rault, C. (2012). Energy consumption, economic growth and CO2 emissions in Middle East and North African countries. Energy Policy, 45, 342–349.

Banerjee, A., Dolado, J., & Mestre, R. (1998). Error-correction mechanism tests for cointegration in a single-equation framework. Journal of Time Series Analysis, 19(3), 267–283.

Chang, S. C. (2015). Effects of financial developments and income on energy consumption. International Review of Economics & Finance, 35, 28–44.

Chaudhry, I. S., Safdar, N., & Farooq, F. (2012). Energy consumption and economic growth: Empirical evidence from Pakistan. Pakistan Journal of Social Sciences, 32(2), 371–382.

Çoban, S., & Topcu, M. (2013). The nexus between financial development and energy consumption in the EU: A dynamic panel data analysis. Energy Economics, 39, 81–88.

Farhani, S., & Ozturk, I. (2015). Causal relationship between CO2 emissions, real GDP, energy consumption, financial development, trade openness and urbanization in Tunisia. Environmental Science and Pollution Research, 22(20), 15663–15676.

Fosu, O. A., & Magnus, F. J. (2006). Bounds testing approach to cointegration: An examination of foreign direct investment trade and growth relationships. American Journal of Applied Science, 3(11), 2079.

Govindaraju, V. C., & Tang, C. F. (2013). The dynamic links between CO2 emissions, economic growth and coal consumption in China and India. Applied Energy, 104, 310–318.

Hossain, S. (2012). An econometric analysis for CO2 emissions, energy consumption, economic growth, foreign trade and urbanization of Japan. Low Carbon Economy, 2012(3), 92–105.

Hye, Q. M. A., & Riaz, S. (2008). Causality between energy consumption and economic growth: The case of Pakistan. The Lahore Journal of Economics, 13(2), 45–58.

Islam, F., Shahbaz, M., Ahmed, A. U., & Alam, M. M. (2013). Financial development and energy consumption nexus in Malaysia: A multivariate time series analysis. Economic Modelling, 30, 435–441.

Jalil, A., & Feridun, M. (2011). The impact of growth, energy and financial development on the environment in China: A cointegration analysis. Energy Economics, 33, 284–291.

Khan, M. A., Qayyum, A., & Saeed, A. S. (2005). Financial development and economic growth: The case of Pakistan. Pakistan Development Review, 4(44), 819–837.

Mahalik, M. K., & Mallick, H. (2014). Energy consumption, economic growth and financial development: Exploring the empirical linkages for India. The Journal of Developing Areas, 48(4), 139–159.

Narayan, P. K. (2005). The savings and investment nexus for China: evidence from cointegration tests. Applied Economics, 37, 1979–1990.

Nasreen, S., Anwar, S., & Ozturk, I. (2017). Financial stability, energy consumption and environmental quality: Evidence from South Asian economies. Renewable and Sustainable Energy Review, 67, 1105–1122.

Odhiambo, N. M. (2009). Energy consumption and economic growth nexus in Tanzania: An ARDL bounds testing approach. Energy Policy, 37(2), 617–622.

Oh, W., & Lee, K. (2004). Energy consumption and economic growth in Korea: Testing the causality relation. Journal of Policy Modeling, 26(8), 973–981.

Osigwe, A. C., & Arawomo, D. F. (2015). Energy consumption, energy prices and economic growth: Causal relationships based on error correction model. International Journal of Energy Economics and Policy, 5(2), 408–441.

Ozturk, I., & Acaravci, A. (2013). The long-run and causal analysis of energy, growth, openness and financial development on carbon emissions in Turkey. Energy Economics, 36, 262–267.

Pesaran, M. H., & Pesaran, B. (1997). Working with Microfit 4.0: Interactive econometric analysis [Windows version]. Oxford: Oxford University Press.

Pesaran, M. H., Shin, Y., & Smith, R. J. (2001). Bounds testing approaches to the analysis of level relationships. Journal of Applied Economics, 16, 289–326.

Rafindadi, A. A., & Ozturk, I. (2017). Dynamic effects of financial development, trade openness and economic growth on energy consumption: Evidence from South Africa. International Journal of Energy Economics and Policy, 7(3), 74–85.

Sadorsky, P. (2010). The impact of financial development on energy consumption in emerging economies. Energy Policy, 38(5), 2528–2535.

Sadorsky, P. (2011). Financial development and energy consumption in Central and Eastern European frontier economies. Energy Policy, 39, 999–1006.

Salahuddin, M., Alam, K., Ozturk, I., & Sohag, K. (2018). The effects of electricity consumption, economic growth, financial development and foreign direct investment on CO2 emissions in Kuwait. Renewable and Sustainable Energy Reviews, 81, 2002–2010.

Sambo, A. S. (2008). Matching electricity supply with demand in Nigeria. International Association of Energy Economics, 4, 32–36.

Shahbaz, M., Hye, Q. M. A., Tiwari, A. K., & Leitão, N. C. (2013a). Economic growth, energy consumption, financial development, international trade and CO2 emissions in Indonesia. Renewable and Sustainable Energy Reviews, 25, 109–121.

Shahbaz, M., Khan, S., & Tahir, M. I. (2013b). The dynamic links between energy consumption, economic growth, financial development and trade in China: Fresh evidence from multivariate framework analysis. Energy Economics, 40, 8–21.

Soytas, U., & Sari, R. (2009). Energy consumption, economic growth, and carbon emissions: Challenges faced by an EU candidate member. Ecological Economics, 68(6), 1667–1675.

Tamazian, A., Chousa, J. P., & Vadlamannati, K. C. (2009). Does higher economic and financial development lead to environmental degradation: Evidence from BRIC countries. Energy Policy, 37(1), 246–253.

Tamazian, A., & Rao, B. B. (2010). Do economic, financial and institutional developments matter for environmental degradation? Evidence from transitional economies. Energy Economics, 32(1), 137–145.

Tang, C. F., & Tan, B. W. (2014). The linkages among energy consumption, economic growth, relative price, foreign direct investment and financial development in Malaysia. Quality & Quantity, 48, 781–797.

Uçan, O., Aricioglu, E., & Yucel, F. (2014). Energy consumption and economic growth nexus: Evidence from developed countries in Europe. International Journal of Energy Economics and Policy, 4(3), 411–419.

World Development Indicators. (2015). http://databank.worldbank.org/data/reports.aspx?source=world-development-indicators. Accessed April 5, 2015.

World Energy Outlook. (2014). http://www.worldenergyoutlook.org/media/weowebsite/africa/Fact_sheet_I_Africa_energy_today.pdf. Accessed May 14, 2016.

Yusuf, S. A. (2014). Impact of energy consumption and environmental degradation on economic growth in Nigeria. Munich Personal RePEc Archive.

Zhang, Y. J. (2011). The impact of financial development on carbon emissions: An empirical analysis in China. Energy Policy, 39(4), 2197–2203.

Zhang, X. P., & Cheng, X. M. (2009). Energy consumption, carbon emissions, and economic growth in China. Ecological Economics, 68(10), 2706–2712.

Acknowledgements

All the papers cited in this manuscript are fully acknowledged.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

There is no any conflict of interest in this paper.

Rights and permissions

About this article

Cite this article

Ali, H.S., Law, S.H., Lin, W.L. et al. Financial development and carbon dioxide emissions in Nigeria: evidence from the ARDL bounds approach. GeoJournal 84, 641–655 (2019). https://doi.org/10.1007/s10708-018-9880-5

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10708-018-9880-5