Abstract

The purpose of the paper is to assess the inclusion of social sustainability in the decisions of supply chain in multinational manufacturing organisations in India. Indian organisations are resorting to sustainability-based reporting for greater transparency and for creation of brand value for their organisations. There are tremendous economic upheavals and changes across the complete value chain, and thus, responsible business practices are becoming a necessity for the long-term survival of organisations. Sustainability, as a strategy, is responsible utilisation of resources and is reported through social, economic and environmental factors in an organisation. For sustainability as a strategy, there has to be a complete organisational inclusion and employee engagement through decision making at operational levels along the value chain. The research paper is an empirical study done through a survey using a structured questionnaire to collect information to evaluate decision criteria particularly for social sustainability, from the middle and top level executives in Indian manufacturing organisations. Multinational manufacturing organisations in India are trying to be more responsible because of mandated CSR policy, and thus, sustainability through social factors is getting more prominence. A multiple linear regression analysis is used to explain the correlation and inclusion of social factors on the decision-making process in the supply chain of multinational manufacturing organisations in India. This study reveals that decision making in the supply chain of multinational manufacturing organisations in India specifically in manufacturing industry is incorporating social sustainability. The study highlights that decision making involving social sustainability needs larger frameworks for organisational preference. While the study provides evidence of social sustainability-based practices in multinational manufacturing organisations in India, it does not deal with social sustainability practices. The study also has limitation as has been limited to organisations which follow sustainability practices and make disclosures through GRI framework.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Brundtland Commission Report (WCED 1987) considers sustainability as an interface between economic prosperity with environment and social inclusion for development. The 1992 earth summit at Rio also highlights the integration of three facets for sustainability—economic growth along with social equity along with the carrying capacity of the environment or natural systems in which we operate (Dyllick and Hockerts 2002; Kovacs 2008). Gibson (2006) also asserts that sustainability should necessarily include socio-economic and biophysical matters. The interdependence of socio-economic and biophysical matters and their interrelationship needs to be addressed for a larger complex system, which includes the human beings along with ecological effects for economic equity.

Stakeholders seem to prefer sustainable development or sustainability due to global economic downturn, fiscal and climate changes with rapid urbanisation that is working with limited natural resources (IBM 2009; Gibson 2006; Kiron et al. 2015). Industrialisation, globalisation and increased population are creating stress on the available resources and simultaneously damaging the critical and essential ecological equilibrium.

Increasing complexity is making it important for businesses to adapt new strategies and approaches. Sustainable ways of business are needed to maintain profits, manage and mitigate associated risks and enable greater stakeholder engagement. The literature suggests that sustainable business practices are being included in the organisational realm, and there is an enhancement gradually. Earlier the focus was on economic strategies and philanthropic acts of organisations. Globalisation and interconnected economies have altered social conditions and stakeholder perceptions. This is leading to enhanced exposure and adoption, advocacy of technological innovation to completely transform the way resources are consumed and the production of goods (Agnihotri and Tripathi 2015; Kiron et al. 2015; Ahi et al. 2016).

Sustainability practices have an impact on the overall revenues and profits of an organisation (Kiron et al. 2013; Hummel and Schlick 2016), and over the years stakeholder vigil and interest have increased through regulatory frameworks of government (COP-21, 2015), end user, employees and other stakeholder interests. There is a definite and enhanced interest as also advocacy towards responsible business practices and strategies that incorporate the environment, social and economic factors (Dunphy et al. 2006; Ahi and Searcy 2013).

Social sustainability deals with social issues in the ecosystem of an organisation and is necessary for its long-term sustainability as also to ensure that it uses resources without affecting the quality of life through loss of economic opportunities for people or by affecting societal conditions and the environment (WCED 1987). The social factors/concepts should be broadened to be outside the periphery of daily routine operations of an organisation and extend to varied segments and channel partners across the supply chain to involve trading partners with societies in which they operate (Carter and Rogers 2008; Hutchins and Sutherland 2008).

Social sustainability as a concept has wide array of activities to be followed without consensus on achieving any specific goals, neither in the literature nor in practice (Dempsey et al. 2009). This broad definition makes its practice difficult as it has to consider the consequence of activities for all stakeholders including suppliers, customers, employees and local communities (Chardine-Baumann and Botta-Genoulaz 2014). Organisations are involved in activities right from utilisation of resources, manufacturing of products to delivery of products/information to customers by interfacing with stakeholders through their supply chains.

The purpose of the paper is to assess the social sustainability efforts of multinational manufacturing organisations in India. These organisations have significant operations across the globe originating either in India or in other geography. To assess their social sustainability efforts, a quantitative assessment was made by collecting information through a structured questionnaire to evaluate whether social sustainability is included in decision criteria of supply chain managements. The data were collected at pan-India level through corporate executives working in multinational manufacturing organisations. Its inclusion in decision criteria of executives is important.

-

To assess whether social sustainability and its factors are being incorporated in supply chain decisions of multinational manufacturing organisations in India.

The study provides evidence of inclusion of social sustainability practices and will assess and pave the way for more research on the topic and its practice. As per the study, there is a significant relation between decisions taken in the supply chain management of an organisation and social sustainability factors of multinational manufacturing organisations in India. Section 2 deals with the literature and social sustainability in multinational manufacturing organisations in India. Section 3 in the paper deals with research methodology followed by conclusion and scope for further research.

2 Literature review

2.1 Social sustainability

Social sustainability or organisations resorting to its practices benefit the communities in which they operate. Such organisations increase/enhance the human and societal capital by adapting practices in sync with the societal stakeholders. Further, they add value to the society and to various stakeholders by furthering the societal capital and helping the stakeholders understand the motivation for their activities (Dyllick and Hockerts 2002).

Social sustainability is necessary as it assists the human species and other flora/fauna with proper use of available resources. It is important for living beings to flourish, prosper and develop with informed and engaged systems and governmental measures. It will enhance the economic and environmental well-being of the planet. There is a need to understand the nuances or technical aspects of sustainability for a more inclusive transition into sustainable future incorporating changes from everyday life (Magis and Shinn 2009; Vallance et al. 2011; Dempsey et al. 2009).

Researchers and practitioners point out that social sustainability is comparatively less practiced, discussed and developed of the three sustainability factors, viz., the environment, economic and social sustainability (Mani et al. 2016; Vallance et al. 2011). The literature shows that social sustainability/practices are often considered together with environment and economic sustainability (Magis and Shinn 2009; Hutchins and Sutherland 2008; Dempsey et al. 2009). Researchers feel that economic survival has greater focus for stakeholders, organisations and environmental sustainability than social sustainability (Kaur and Sharma 2016). Social sustainability practices can help organisations/practitioners become sustainable with inclusion of various sustainability factors (Seuring and Muller 2008; Kaur and Sharma 2016; Mani et al. 2016) and can also improve their brand and organisational image among stakeholders by addressing social issues (Kaur and Sharma 2016).

In supply chain management, conceptual clarity is missing from social sustainability, (Vallance et al. 2011). The literature also mentions an inherent lack of a conceptual, comprehensive framework to measure and manage social sustainability, especially in the manufacturing and operations domain in developing nations like India (Gopal and Thakkar, 2015; Dempsey et al. 2009).

There are systemic limitations in adaption and acceptability of sustainability practices, especially in social sustainability in developing nations such as India. Developing nations are usually laggards in adaption of newer practices for a holistic and inclusive development, and the difference is due to unique supply chain characteristics and challenges that are different from developed economies (Mani et al. 2016). Economic, environmental and social aspects of sustainability will have an impact in developing nations beyond the organisational boundaries with rise in climate change and globalisation. Due to assertion by various stakeholders, international agencies, government organisations, etc., greater attention is now paid to economic and environmental sustainability in supply chains as compared to social aspects (Gopal and Thakkar 2015).

For wider adoption of sustainability practices, environmental goals and practices need social acceptance. Society resists change when its goals and implications are not understood (Assefa and Frostell 2007; Vallance et al. 2011). Cultural differences and social norms also limit its acceptance (Ashby et al. 2012).

Research is lacking in understanding the correlation between social sustainability and the performance of businesses/organisations (Mani et al. 2016; Vallance et al. 2011). Research is needed to enhance the understanding of practitioners and improve the dimension to leverage sustainability practices, especially social sustainability in organisations. This is in contrast to the developed economies, where globalisation and stakeholder insistence have forced organisations to address social sustainability. Typically, social sustainability inclusion for sustainable practices is through various channel partners and supply chain linkages. Also, numerous studies have been advocating improving profitability, revenues, global trade and risk management through sustainability-based practices (Kaur and Sharma 2016; Mani et al. 2016) and competitiveness (Sodhi 2015).

2.2 Indian organisations and sustainability

Developing countries like India are one of the fastest growing economies and have to balance growth and consumption of resources for equitable distribution to stakeholders. Decision makers need to build frameworks to manage not only their own organisational resources, capabilities but also to remain socially responsive to various stakeholders with respect to utilisation of resource, capabilities and distribution of economic gains (Mani et al. 2016; Campbell 2007; Sodhi 2015).

In relation to climate change and sustainability, the Indian government regulates business responsibility and community development through the Companies Act 2013 (Agnihotri and Tripathi 2015). Most organisations in India have either developed or followed global practices in sustainability and other initiatives (Agnihotri and Tripathi 2015; and Kothari 2013). Only a limited number of organisations disclose information on sustainability initiatives based on globally accepted reforms such as Global Reporting Initiative (GRI).

Nevertheless, some researchers (Kothari 2013; Kaur and Sharma 2016) claim that there exists awareness and intention among multinational global organisations towards sustainable development or sustainability-based practices. Multinational manufacturing organisations in India are resorting to increased disclosure practices following the international guidelines such as Global Reporting Initiative (GRI) framework.

Dyllick and Hockerts (2002) argue that social inclusion has been through corporate social responsibility (CSR) policies or practices. Majumdar et al. (2015), and Kaur and Sharma (2016) claim that social inclusion or sustainability practices are followed through CSR spends. The CSR is mandated through polity, especially in India, through Companies Act 2013 which is at 2% of the profits. Kiron et al. (2013) and Mani et al. (2016) claim that CSR and social sustainability both stress on the importance of ethical behaviour and social inclusion through holistic economic development by organisations. Hutchin & Sutherland (2008) argue that CSR and social sustainability have intrinsic linkages with each other and many definitions of CSR deal with ethical and socially responsible business practices.

Kaur and Sharma (2016) claim that it is mostly large multinational organisations in India with supply chains across different countries and geographies that are keen on implementing sustainability practices/disclosures following global practices. For multinational organisations, sustainability practices and disclosures allow them to be more responsible for their stakeholders, reverse risk and improve the efficiency, productivity, product quality of their supply chain to capture more business value (Dauvergne and Lister 2012), and this is aided by turmoil in the economies worldwide.

Sustainability or sustainable development transcends the boundaries of social, economic and environmental framework for global business and organisations need to work holistically through frameworks and strategies to transcend the triple pillars of sustainability, viz., social, economic and environmental for inclusive development (Ahi et al. 2016; Mani et al. 2016; Kiron et al. 2015). The literature also identifies that a number of organisations resort to sustainability as part of their supply chain management practices (Ahi et al. 2016).

Adaption of sustainability practices is challenging in developing countries. It can be attributed to significant differences in social, cultural, technological paradigms of developing countries (Mani et al. 2016). Authors also suggest a need for more research on adaption of social sustainability practices in developing countries due to differences in requirements, code of conduct, cultural differences and socio-economic context between developed and developing countries. Organisations operating at global level are host to a number of challenges for the implementation and practice of social sustainability which is unique to each region and country. Organisations thus, as a strategy, address the significant ones or significant challenges (Kiron et al. 2013; Dauvergne and Lister 2012).

Organisations in developing countries, particularly India, disclose their sustainability practices through annual corporate sustainability reports. These disclosures are aimed at stakeholders to communicate practices followed, and strategies and approaches adapted to address various social, environmental and economic factors/issues. These reports serve as a barometer or disclose an organisation’s strategies, actions and practices towards social and environmental responsibility, social inclusion and sustainability, integration of sustainability practices in the organisation’s business plans at all levels of interactions and operations (Tate et al. 2009; Majumdar et al. 2015; Kaur and Sharma 2016).

In India, organisations disclose sustainability practices using GRI guidelines (Majumdar et al. 2015; Kaur and Sharma 2016). The disclosures convey their sense of responsibility, sustainability progress, including those aimed at investors and customers. Organisations, mostly multinational organisations (Kaur and Sharma 2016), use sustainability as strategy for risk management and thoughtful utilisation of resources in a responsible manner with development across their supply chain.

GRI (GRI 2002, 2015) framework is a joint effort of Environmental Responsible Economies (CERES) and the United Nation Environment Program (UNEP) for sustainable leadership. The collaboration helps organisations and stakeholders to understand and communicate better about sustainable practices and their role in societal development. The communication is also intended to provide guidelines for improving the effectiveness of sustainability disclosures. Further, Hedberg and Malmborg (2003) mention that organisations produce corporate sustainability reports seeking legitimacy. As companies face multiple reporting pressures, of late, there is a growing demand for a reporting standard acceptable worldwide and has legitimacy across global organisations. GRI framework provides this standard as also transparency and accountability through a worldwide, and multi-stakeholder network of global organisations in adoption of sustainability practices (Tata Sustainability Report, 2012–2013) Tables 1, 2, 3 and 4.

GRI (2002, 2015) uses a hierarchical framework in three focus areas, namely, social, economic and environmental. The three areas further outline the categories of sustainability with their dimensions and indicators. The GRI guidelines outline which dimensions should be considered in a particular category. Disclosures are outlined using GRI principles in various categories at operational level, and at overall organisation level as well (Labuschagne et al. 2007).

Inclusion of sustainability practices for holistic development is important. Social sustainability is a key factor for integration of economic and environment sustainability as well. There is a need and urgency for sustainable development through which social and environmental issues must be addressed whether at policy, personal or organisational level. Social sustainability needs more research due to the complex nature of the concept and lack of research in it (Mani et al. 2016). Researchers like Gibson (2006) also state that for sustainability assessments at operational, tactical and strategic levels, the main focus should be on the factors. These factors, in turn, will affect the organisations to evaluate and compare their efforts for the purpose of sustainability.

To evaluate social sustainability efforts and the decision making of multinational Indian manufacturing organisations using GRI guidelines, an empirical, quantitative research using GRI listed factors was formulated.

Social sustainability as envisaged by Majumdar et al. (2015) is through CSR philanthropy and because of mandatory requirement for organisations in India through the Companies Act 2013. Organisations address sustainability issues by measuring the environmental impact and with their social implications regarding the survival and improvement of standard of living for the stakeholders involved. Disclosures and reviews suggest that more work needs to be done and there is significant gap between the action plans and the gauged efforts of the organisations for sustainability and the relevant business practices (Kiron et al. 2013). They also concluded that organisations they surveyed considered social and environmental issues as tremendously important. Accordingly, the majority of respondents considered social, environmental concerns such as pollution or employee health important. But when the actions were compared, there was tremendous disconnect and 40% of respondents reported that organisations were addressing them. Only 10% of respondents said that their companies fully tackle them. Researchers further conclude that organisations incorporating sustainability as a practice have sustainability as their top permanent agenda for making it a business case in relation to employee engagement and sustainability strategy implementation (Kiron et al. 2013).

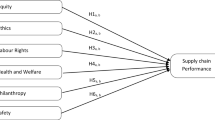

Hence, a hypothesis was formulated to understand whether social sustainability factors are incorporated into the decision making of multinational manufacturing organisations in India:

Hypothesis

H0: No significant relation exists between decisions taken in the supply chain management of an organisation and social sustainability factors in supply chain management.

H1: There is a significant relation between decisions taken in the supply chain management of an organisation and social sustainability factors.

3 Research methodology

For understanding the decision making of multinational manufacturing organisations in India to incorporate social sustainability in the supply chain, a quantitative research was designed using a structured questionnaire. To validate the content, a focus group pilot was done involving two academicians and six industry/sustainability practitioners. The purpose was to gather their feedback and incorporate it in the structured questionnaire and the variables used.

Multinational manufacturing organisations in India use the GRI framework for disclosures pertaining to sustainability practices (Kothari 2013; Majumdar et al. 2015). Organisations in India are adapting sustainability practices as business partners or the up/downstream partners of supply chain of multinational global organisations (Kaur and Sharma 2016; Majumdar et al. 2015).

The questionnaire used GRI framework for social factors to measure sustainability using the variables denoted below. The standard GRI framework with social sustainability variables was used on five-point Likert scale (Saraswat and Tewari 2015; Kaur and Sharma, 2016; GRI, 2002, 2015). For each variable as denoted below, the executives of the organisations were asked questions from the structured questionnaire or were requested for a survey to gauge whether the decision making in supply chain has social sustainability dimension.

Social factors as defined by GRI (GRI 2002) framework are defined in four categories, viz.

The approach for data collection was the quantitative survey using a structured questionnaire that was administered on middle and senior-level executives of multinational manufacturing organisations in India. Researchers and scholars consider survey as a useful method to collect a large amount of information/ideas. It has the advantage as it can help gauge the relationships among different independent and dependent variables (Prentice and Miller 1992).

Random sampling was used, and correspondents were chosen after screening them through two preliminary questions.

-

The first one is if their organisation follows sustainability practices, and

-

The second one is sustainability disclosure practices in their organisations.

Respondents who were decision makers and had complete knowledge of sustainability efforts/business practices in their organisation were contacted through e-mail and social media. The respondents were senior management people with the title of Chief Executive Officer, Chief Scientific Officer, President, Vice-President, Manager-Manufacturing, Manager-Others. A total of 600 questionnaires were shared with respondents in various organisations through an online link (Google form). They were requested for their feedback using an online survey/interview depending on their convenience. Data were also collected through interviews using the structured questionnaire with top management and some middle-management personnel of some organisations. From online survey, 204 responses were received. Two hundred complete responses were selected for further analysis. Another 174 responses were collected through structured interview for the same questionnaire with some of the top management of organisations. In total, 374 responses were selected for further analysis. In total, 25 multinational manufacturing organisations were contacted for the survey. Of the 25, 16 organisations have operations originating in India and the rest have their base outside of the country but with significant presence/operations in the country.

The summary of data collected from the survey using GRI social factors is given below. Information on revenues was collected using the structured questionnaire from the survey, and the responses have been compiled.

A multiple linear regression analysis is used to explain the correlation and inclusion of social factors on the decision-making process in the supply chain of multinational manufacturing organisations in India.

4 Results and discussion

Regression analysis is an effective tool to measure the dependence among variables. Multiple regression analysis is used by researchers to study the relationship between an independent variable and more than one dependent variable (Chauhan 2015).

Social sustainability factors were taken as the independent variables for measuring sustainability initiatives of supply chain (dependent variable) of the organisations.

The variables are further defined and outlined as the questionnaire was developed further.

Cronbach alpha was calculated from the collected responses (0.886). Multiple linear regression analysis (Chauhan 2015) was done to explain the correlation and effect of social sustainability factors on the decision in the supply chain of private manufacturing organisations, i.e. the relation of independent variables of social sustainability factors with the dependent variable of measuring sustainability in the supply chain of an organisation.

Data collected for the questionnaire were also tested for reliability using Cronbach alpha (0.886). Reliability measurement is important to ascertain the fact that a scale should consistently reflect the construct it is measuring, which indicates a level of consistency for a multiple item scale. Hence, to measure reliability, Cronbach alpha measurement was done and a value greater than 0.7 was considered reliable (Chauhan 2015; Ma Ga Yang 2013).

Multiple linear regression analysis using SPSS-20 is used to understand the relationship between multiple social sustainability independent variables and sustainability initiatives of supply-chain-dependent variable.

To understand the relation between decisions taken in the supply chain management of an organisation and social sustainability factors of the supply chain,

-

(a)

Table 5 shows that the value of R is not very close to 1, nevertheless at 0.554 it shows a relation between variables (Chauhan 2015). The literature identifies that the value of R if is closer to 1, validates predicted values closer to the actual values. Usually, the value of R, which represents the correlation between the predicted values of dependent variable and the actual values of the dependent variable, ranges from (−1) to (+1). Higher values thus indicate that predicted values are closer to the actual value (Chauhan 2015).

Table 5 Summary of the multiple linear regression analysis (Chauhan 2015) using SPSS-20 -

(b)

Table 5, a summary of the multiple linear regression analysis (Chauhan 2015) using SPSS-20, shows that the Durbin–Watson for the error terms has positive autocorrelation. According to the literature, the value of Durbin–Watson has to be two (2) and a value lower than this shows a positive autocorrelation among the responses (Chauhan 2015).

-

(c)

The value of F in Table 6, which is the summary of ANOVA, carried on dependent variable of sustainability is greater than 4, and hence, the null hypothesis is rejected; p value at 95% confidence level is significant.

Table 6 Summary of ANOVA carried on dependent variable of sustainability using SPSS-20

Therefore, the alternate hypothesis of a significant relation between decisions taken in the supply chain management of an organisation and social sustainability factors in supply chain management of manufacturing organisations in India with global operations is accepted (Chauhan 2015). The data collected depict considerable and significant relation, though not very strong, between various social sustainability variables and sustainability of supply chain.

The decisions of executives of the management of supply chain incorporate social sustainability factors. This relationship is significant and must pave the way for organisations to enhance their efforts for social sustainability. Organisational engagement is important to make the supply chains sustainable and enhance the quality of living of local communities with better economic parity. Supply chains are an important part of organisational involvement in procurement of resources in manufacturing, sales and in delivery to the end user. Enhanced social sustainability efforts by some organisations will increase research and practice for adoption of sustainability.

5 Conclusion

Indian organisations follow sustainability practices primarily due to enhanced regulation, stakeholder preference and risk management. Usually, Indian organisations having global presence work to create a business model adapting sustainability initiatives in which social sustainability is also linked to corporate social responsibility paradigms. This creates an ability in the organisations to sustain risk in supply chain and enhances bottom-line profitability, and brand recognition through sustainability practices for greater profits and stakeholder engagement.

Indian organisations making sustainability disclosures for greater transparency adapt GRI guidelines follow government regulations while keeping in mind the stakeholder preference, and consumer and employees’ interest. Sustainability practices need to include social sustainability. Social sustainability and factors in business practices help the organisations to include various social issues in the realm of society in which they operate. Social sustainability is essential for inclusive growth, equitable distribution of generated income and for prosperity of the societies involved as a whole. Greater stakeholder engagement will affect the long-term survival of the organisations and will help in integrating social dimensions of up/downstream trading partners Tables 7 and 8.

Social sustainability is a mechanism through which organisations adapt to add value to the communities in which they operate. In India, the social sustainability practices are through the inclusion of CSR-based practices due to mandatory inclusion of 2% of profits as per Companies Law Act, 2013.

The quantum of social labour practices is increasing by involving the social fabric of communities. Multinational manufacturing organisations need to adapt and measure sustainability initiatives not only for economic sustainability but also for environment and social sustainability to transform the organisations and the communities in which they operate. Sustainability practices help organisations to improve their bottom line, increase revenue, brand value and ensure greater stakeholder engagement. Sustainability practices need inclusion across the fabric of an organisation with collaboration. Social sustainability covers approaches and practices with emphasis on process redesign, financial modelling and the skill of communicating and engaging with external stakeholders. There is a significant relation between decisions made in the supply chain management of an organisation and social sustainability factors.

This work has identified a relation and using multiple linear regression analysis technique establishes that social sustainability is being adapted in the supply chain management of organisations in India, particularly in manufacturing with global, multinational operations. Additionally, the research has identified the framework/factors in respect of social sustainability. Social sustainability-based business practices and disclosures are identified/planned around these variables. Indian manufacturers are taking steps to include social sustainability-based practices, while ensuring profitability through global operations. These are very niche steps but necessary for more research, innovation and inclusion of sustainability practices in organisations worldwide.

This research contributes by providing evidence of adaption of social sustainability factors. This adds to the existing knowledge framework in sustainable supply chain management as there are only limited studies focusing on social sustainability in multinational manufacturing organisations based in India.

6 Scope for further research and Limitations of the study

The social factors/variables defined by GRI (2002, 2015) used in organisational disclosures can be used by researchers/practitioners to further innovate and define sustainable practices around them. Social sustainability-related factors/variables can further be measured for the supply chain management of organisations to build socially responsive organisations. Researchers can further study the practices incorporating social sustainability particularly in supply chain management of organisations and may also look to link organisational revenue/profit with social sustainability.

The limitations of this study are:

-

While it provides evidence of social sustainability-based practices in multinational manufacturing organisations in India, it does not deal with social sustainability practices.

-

The study has been limited to organisations which follow sustainability practices and make disclosures through GRI framework.

References

Agnihotri, K. & Tripathi, R. (2015).Corporate sustainability: A mantra for business excellence. In Paper presented at international conference on evidence based management. BITS-Pilani: Excellent Publishing house (vol. 1, pp. 309–403).

Ahi, P., Jaber, M. Y., & Searcy, C. (2016). A comprehensive multidimensional framework for assessing the performance of sustainable supply chains. Applied Mathematical Modelling, 40, 10153–10166.

Ahi, P., & Searcy, C. (2013). A comparative literature analysis of definitions for green and Sustainable supply chain management. Journal of Cleaner Production, 52, 329–341.

Ashby, A., Leat, M., & Hudson-Smith, M. (2012). ‘Making connections: A review of supply chain management and sustainability literature. Supply chain management. An International Journal, 17(5), 497–516.

Assefa, G., & Frostell, B. (2007). Social sustainability and social acceptance in technology assessment: a case study of energy technologies. Technology in Society, 29, 63–78.

Campbell, J. L. (2007). Why would corporations behave in socially responsible ways? An institutional theory of corporate social responsibility. Academy of Management Review, 32, 946–967.

Carter, C. R., & Rogers, D. S. (2008). A framework of sustainable supply chain management: moving toward new theory. International Journal of Physical Distribution and Logistics Management, 38(5), 360–387.

Chardine-Baumann, E., & Botta-Genoulaz, V. (2014). A framework for sustainable performance assessment of supply chain management practices. Computers & Industrial Engineering, 76, 138–147. doi:10.1016/j.cie.2014.07.029.

Chauhan, A. K. (2015). Regression. Research analytics-a practical approach to data analysis. New-Delhi: Dream Tech Press.

Dauvergne, P., & Lister, J. (2012). Big brand sustainability: Governance prospects and environmental limits. Global Environmental change Elsevier, 1(3), 36–45.

Dempsey, N, Bramley, G, Power, S & Brown, C (2009).The social dimension of sustainable development: Defining urban social sustainability. Sustainable Development. DOI: 10.1002/sd.417. Retrieved 15 December, 2016 from https://www.researchgate.net/publication/229889535.

Dunphy, D., Griffiths, A., Benn, S (2006). Organisational change for corporate sustainability. Retrieved December 10, 2014, from http://www.sustenn.com/files/user_files/25_Frederic_Laloux/dunphyorganizational-change-for-corporate-sustainability.pdf.

Dyllick, T., & Hockerts, K. (2002). Beyond the business case for Corporate Sustainability. Business Strategy and the Environment, 11, 130–141. doi:10.1002/bse.323.

Global reporting Initiatives. (2002). Retrieved December 11, 2014 from https://www.globalreporting.org/reporting/G3andg3-1/guidelines-online/TechnicalProtocol/Pages/MaterialityInTheContextOfTheGRIReportingFramework.aspx.

Global Reporting Initiative. (2015). Retrieved on 15 December 2016 from <https://www.globalreporting.org/resourcelibrary/GRIG4-Part1-Reporting-Principles-and-Standard-Disclosures.pdf>.

Google form (n.d.). Online Survey form. Retrieved on October 15, 2014 from https://www.google.co.in/forms/about/.

Gopal, P.R.C., Thakkar, J. (2015). Sustainable supply chain practices: an empirical Investigation on Indian automobile industry. Production, Planning and Control. pp no.1–16

Gray. R. (2010). Is accounting for sustainability actually accounting for sustainability and how would we know? An exploration of narratives of organisations and the planet. Retrieved 21 June 2016 from http://www.sciencedirect.com/science/article/pii/S0361-3682(09)00042-7.

Gibson, R. B. (2006). ‘Sustainability assessment: Basic components of a practical approach. Impact Assessment and Project Appraisal, 24(3), 170–182.

Hedberg, C. J., & Malmborg, F. V. (2003). The global reporting initiative and corporate sustainability reporting in Swedish companies. Corporate Social Responsibility and Environment Management, 10, 153–164.

Hummel, K & Schlick, C. (2016).The relationship between sustainability performance and sustainability disclosure-Reconciling voluntary disclosure theory and legitimacy theory. Journal of Accounting Public Policy xxx (2016) xxx–xxx.(Article in Press)

Hutchins, M., & Sutherland, J. (2008). An exploration of measures of social sustainability and their application to supply chain decisions. Journal of Cleaner Production, 16, 1688–1698.

IBM. (2009). Sustainability on a Smarter Planet: Going Green and Beyond. New York: IBM.

Kaur, A., & Sharma, P. C. (2016). Global organisations and SME in India: A comparative study of sustainability initiatives. Journal of Sustainable Development, 9(3), 65–76.

Kiron, D., Kruschwitz, N., Haanaes, K., Reeves, M., Kehrbach, S. K. F., & Kell, G. (2015). Joining forces: Collaboration and leadership for sustainability. Cambridge: Massachusetts Institute of Technology.

Kiron, D., Kruschwitz, N., Rubel, H., Reeves, M., Katrin, S., & Kehrbach, F. (2013). Sustainability’s Next Frontier. Cambridge: Massachusetts Institute of Technology.

Kothari, A (2013).Development and ecological sustainability in India: Possibilities for Post-2015 framework. Oxfam India working paper series. Retrieved from 21 May 2015 from http://www.environmentportal.in/files/file/development%20and%20ecological%20sustainability%20in%20india.pdf.

Kovacs, G. (2008). Corporate environmental responsibility in the supply chain. Journal of Cleaner Production, 16(15), 1571–1578.

Labuschagne, C, Brent, A.C & Erck, R.P.G.V (2007). Assessing the sustainability performances of industries. Journal of cleaner production, Retrieved from http://repository.up.ac.za/bitstream/handle/2263/4325/Labuschagne_Assessing%282005%29.pdf?sequence=1.

Ma Ga yang (2013). Developing a Focal Firm’s Sustainable Supply Chain Framework: Drivers, Orientation, Practices and Performance Outcomes (PhD thesis, The university of Toledo, United States)

Magis, K., & Shinn, C. (2009). Emergent themes of social sustainability. In J. Dillard, V. Dujon & M.C. King (Eds.), Understanding the Social Aspect of Sustainability. New York, NY: Routledge. Retrieved on 21 June 2016 from

Majumdar, U., Rana, N., & Sanan, N. (2015). India’s top companies for CSR and sustainability. India: Futurescape-IIM Udaipur.

Mani, V., Gunasekaran, A., Papadopoulos, T., Hazen, B., & Dubey, R. (2016). Supply chain social sustainability for developing nations: Evidence from India. Resources, Conservation and Recycling, 111, 42–52.

Marsden, C. (2000). The new corporate citizenship of big business: Part of the solution to sustainability. Business and Society Review, 105(1), 9–25.

McKenzie, S (2004).Social sustainability towards some definitions. Hawke Research Institute Working Paper Series No 27. Magill, South Australia: Hawke Research Institute, University of South Australia.

Prentice, D. A., & Miller, D. T. (1992). When small effects are Impressive. Psychological Bulletin, 112(1), 160–164.

Saraswat, A. & Tewari, R. (2015). Measuring Business strategy and information system alignment for Sustainable Organizations. Paper presented at International Conference on evidence based management. BITS-Pilani: Excellent Publishing House.

Schwarz, J., Beloff, B. & Beaver, E. (2002).Use sustainability metrics to guide decision-making. Retrieved May 5, 2013, from www.cepmagazine.org.

Seuring, S., & Muller, M. (2008). From a literature review to a conceptual framework for sustainable supply chain management. Journal of Cleaner Production, 16, 1699–1710.

Sodhi, M. S. (2015). Conceptualizing social responsibility in operations via stakeholder resource-Based view. Production Operation Management, 24(9), 1375–1389.

Tata Consultancy Services 2012–2013. (2013). Corporate sustainability report-2013. Mumbai: Tata consultancy services.

Tate, W. L., Ellram, L. M., & Kirchoff, J. F. (2009). Corporate social responsibility reports: A thematic analysis related to supply chain management. Wiley Periodicals Inc. doi:10.1111/j.1745-493X.2009.03184.x.

Vallance, S., Perkins, H. C., & Dixon, J. E. (2011). What is social sustainability ? A clarification of concepts. Geoforum, 42, 342–348.

WCED. (1987). Our common future. Oxford: Oxford University Press.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Kaur, A., Sharma, P.C. Social sustainability in supply chain decisions: Indian manufacturers. Environ Dev Sustain 20, 1707–1721 (2018). https://doi.org/10.1007/s10668-017-9961-5

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10668-017-9961-5