Abstract

I develop a framework to analyze the robust emissions tax policy for a stock pollutant when the environmental authority is not fully confident about its estimated model of pollution dynamics and, in contrast to previous research, the degree of model mistrust may change over time. I characterize the effect of time-varying model mistrust on emission taxes, pollution stocks and welfare. The general results of this paper show that introducing the possibility of a time-varying degree of model mistrust produces different emission taxes, abatement and welfare compared to the traditional assumption of a time-fixed model mistrust. This result holds even if the probability that the model mistrust may change in the future is small. If the environmental authority expects that the model uncertainty may decrease in the future then current emissions taxes should also decrease. Conversely, if the model mistrust may increase in the future then an active approach compatible with the Precautionary Principle is optimal and current emissions taxes should also increase.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

In this paper I develop a framework to study the regulation of a stock pollutant where, in contrast to previous literature, the degree of trust that the environmental authority has in its estimated model is allowed to change over time. A time-varying degree of model uncertainty can arise when changes in key environmental, technological, and economic variables affect the trust that the environmental authority has on the accuracy of its estimated model. For example, Lang (2014) and Herrnstadt and Muehlegger (2014) show that unusual changes in weather increases the concerns about climate change. Herrnstadt and Muehlegger (2014) show that these concerns extend to pro-environment congressional votes. Moreover, previous literature has shown that environmental and economic systems can experience shifts to different dynamic systems. Polasky et al. (2011), Crepin et al. (2012), de Zeeuw and Zemel (2012) mention how these dynamic system shifts can take place in ecological, terrestrial, global climate, consumer choice, financial markets, cultural, and political systems. Thus, an environmental authority aware that the dynamics of economic and environmental system can change may become more mistrustful about the accuracy of its own estimated model after observing changes in key variables. The degree of mistrust may go back to its original level once these changes and the memory these events have faded away.

The main contribution of this paper is the introduction of a time-varying degree of uncertainty aversion of the environmental authority. To the best of my knowledge, this is the first paper to do this in a dynamic framework in environmental economics. The general results of this paper show that accounting for the possibility of a time-varying degree of uncertainty aversion produces different emission taxes and abatement compared to those from the traditional time-fixed uncertainty aversion models used in the previous literature. For example, if the environmental authority believes that the model uncertainty may be reduced in the future then current emissions taxes should also decrease.

In particular, I model an environmental authority’s time-varying degree of trust in its own model of the pollution stock dynamics by setting up a Markov regime-switching model with an optimistic and a pessimistic regime, where robust control is introduced in both regimes but the degree of model mistrust is higher in the pessimistic regime. The theoretical framework I develop is illustrated using Hoel and Karp’s (2001) functional forms and data because of its simplicity and parsimony, but this setup can be modified and implemented in more complex linear quadratic models. This framework is used for normative purposes. This implies that in the decision-making process the environmental authority anticipates the possibility of alternating to a regime with different degree of mistrust using the transition probabilities in the Markov chain.

An emergent literature has adapted robust control to environmental and resource economics and use this new set of tools to obtain optimal policies under Knightian uncertainty. This paper fits neatly into this nascent literature. In one of the first applications, Roseta-Palma and Xepapadeas (2004) implements robust control to resource management decision, particularly water management. Gonzalez (2008) analyzes optimal emissions taxes and welfare under model uncertainty about the evolution of the pollution stock. Vardas and Xepapadeas (2010) analyzes the effect of implementing k-ignorance and robust control to biodiversity management. Funke and Paetz (2011) uses robust control to obtain optimal levels of CO\(_2\) mitigation. Athanassoglou and Xepapadeas (2012) analyzes robust policies for a stock pollutant in the presence of damage control and mitigation. Anderson et al. (2014) introduce robust control in a dynamic integrated framework that allows them to consider model uncertainty with respect to climate and economic dynamics. A common thread in Gonzalez (2008), Vardas and Xepapadeas (2010), and Athanassoglou and Xepapadeas (2012) is the use of robust control to analyze its relationship with the Precautionary Principle. The Precautionary Principles is a vague decision rule that in simple terms proposes that in the face of scientific uncertainty environmental policy should take action to avoid environmental degradation. In general, these studies have found that the use of robust control implies an implementation of the Precautionary Principle in that Knightian model uncertainty leads to a more active environmental policy.

The main contribution of this paper is the introduction of a time-variant degree of mistrust in the environmental authority’s own model of the pollution stock dynamics. The model I present in this paper adapts and improves on the Macroeconomic model in Gonzalez and Rodriguez (2013) using the Hoel and Karp (2001) model as well as the work in Zampolli (2006) and Hansen and Sargent (2008).

I obtain four main results. First, introducing the possibility that the environmental authority may switch to a regime where it has a different degree of trust in its estimated model of the pollution stock dynamics, produces changes in the current level of emissions taxes. This result holds even for a small probability to switch to the other regime and for a short expected duration of the other regime. In general, if the environmental authority believes that there is a possibility to switch to a regime with higher model uncertainty, then an active approach compatible with the Precautionary Principle is optimal by increasing emissions taxes in the current regime. Alternatively, if the environmental authority believes that there is a possibility to switch to a regime with lower model uncertainty, then emissions taxes in the current regime should decrease. These results also hold when the switch to the other regime is permanent. This suggests that if the environmental authority considers the possibility that the model uncertainty may permanently decrease at some point in the future, then current emission taxes should decrease.

Second, increases in the mistrust of the environmental authority’s model of the pollution stock dynamics lead to higher emissions taxes. This is also compatible with the Precautionary Principle and confirms previous results in the literature. However, this result also indicates that decreases in the mistrust in the environmental authority’s model of the pollution stock dynamics lead to lower emissions taxes.

Third, there is an interesting asymmetry in the response of the emissions taxes in each regime to changes in the transition probabilities. Emission taxes in the optimistic regime are more sensitive than those in the pessimistic regime to changes in the transition probabilities.

Fourth, in the presence of a range of possible transition probabilities, an environmental authority in the optimistic regime is better off by assuming the highest transition probability to the pessimistic regime in that range. In general, the environmental authority obtains higher welfare by overestimating rather than underestimating the probability of transiting to the pessimistic regime.

The paper broadly consists of two parts. The first part (Sects. 2, 3) is the theoretical approach. The second part (Sects. 4, 5) is a numerical illustration of the theoretical model. Specifically, the paper is divided into six sections. Section 2 develops the theoretical model. Section 3 shows the analytical solution to the new environmental authority problem. Section 4 presents the data used to calibrate the model. Section 5 presents and analyzes the numerical results. Section 6 concludes and suggests paths for future research.

2 Model

In this model, the environmental authority regulates a stock pollutant (namely CO\(_2\)) using emissions taxes. Pollution damages and abatement costs are quadratic while a linear transition equation describes the evolution of the pollution stock. As in Gonzalez (2008), Athanassoglou and Xepapadeas (2012), and Funke and Paetz (2011), I assume Knightian model uncertainty on the evolution of the pollution stock. This type of uncertainty can stem from the complexity of physical and economic systems, the lack of reliable historical data or the inability to perform controlled experiments. For example, Millner et al. (2013) concludes that given the current scientific knowledge, climate systems cannot be described by a unique probability distribution. This means that the environmental authority is unable to assign unique probability distributions to alternative models of the pollution stock dynamics. Moreover, this implies that the environmental authority’s model of the pollution stock dynamics is misspecified in unknown ways. These include a wide range of misspecified dynamics mentioned in Athanassoglou and Xepapadeas (2012) such as wrong parameters, autocorrelated errors, feedbacks, nonlinearities, irreversibility, and hysteresis effects. Wrong parameters in this model can include the miscalculation of the firms’ abatement costs and their response to emissions taxes, the natural decay in the pollution stock, and the emission sources in the baseline case. The degree of Knightian model uncertainty represents the amount of mistrust that the environmental authority has in its estimated model of the pollution stock dynamics.

To keep the model tractable, I consider two regimes that differ only in the degree of mistrust (or Knightian uncertainty) that the environmental authority has in its estimated model of the pollution stock dynamics: optimistic and pessimistic. In the optimistic regime, the environmental authority believes that its estimated model is a close, although not exact, representation of a true unknown model. In the pessimistic regime, the environmental authority has a higher degree of mistrust in its estimated model and believes it is relatively far from the true unknown model.

Policy makers facing Knightian uncertainty are unable to use the traditional expected probabilities approach. I use robust control, as presented in Hansen and Sargent (2008), in both regimes to deal with the model mistrust in the dynamics of the pollution stock. Robust control in economics is a practical way to implement the minmax solution of Gilboa and Schmeidler (1989) and represents a special case of the more general criterion developed by Klibanoff et al. (2005), Klibanoff et al. (2006), and more recently by Millner et al. (2013) in the context of climate policy.Footnote 1

I introduce a Markov chain to capture the possibility of change in the degree of mistrust, i.e. the possibility of switching between the pessimistic and optimistic regimes. As in Zampolli (2006) I assume that the transition probabilities are exogenous. This is similar to the assumption that dynamic systems shift randomly and exogenously in de Zeeuw and Zemel (2012), among others. Moreover, this implies that the degree of mistrust changes randomly and independently of the environmental authority’s actions. I interpret this as the occurrence of exogenous random events that may affect the trust that the environmental authority has on its estimated model of the pollution stock dynamics. The use of the Markov chain also indicates that the switch to another regime is not predicted with total certainty and that it is dependent on the current state.

2.1 Basic Model of the Environmental Authority

The basic model and functional forms are adapted from Hoel and Karp (2001). It is assumed that the model has one representative firm and one policy maker. The firm minimizes the net cost of abatement, H, given by:

where f, a, and b are positive parameters and \(x_t\) is the firm’s emissions at time t. The net cost of abatement, H, balances the firm’s benefits and costs of abatement.

The firm learns the value of all parameters at the beginning of each period and minimizes abatement costs every period. The firm’s optimal level of emissions in the absence of any regulation is the following:

In the presence of taxes, the firm minimizes tax payments plus abatement cost, and the resulting optimal level of emissions is:

where \(M_t\) is the tax per unit of pollution.

Pollution damages (D) are a quadratic function of the present level of pollutant concentrations (\(S_t\)) represented by the following function

where c and g are parameters. Current pollutant stocks depend on the remaining stock and pollutant emissions from the previous period:

where \(0< \alpha < 1\) is the retention coefficient and represents the natural decay in the pollutant stock and \(\varepsilon _{t+1}\) is an stochastic disturbance.

The environmental authority’s choice of emissions taxes (\(M_t\)) affects current and future costs and benefits. Future payoffs are reduced by the discount factor \(\delta \). Substituting Eq. (3) into Eqns. (5) and (1), the basic problem of the environmental authority is expressed as choosing an infinite sequence of emissions taxes to minimize the expected discounted infinite sum of pollution damages and abatement costs.

Subject to the pollution evolution equation:

where \(\beta \equiv -\frac{1}{b}\) and \(\phi \equiv f + a\bar{x}\).

The Knightian model uncertainty considered in this paper is on the evolution of the stock given by Eq. (7).

2.2 Robust Control and Two Regimes

I now introduce an environmental authority that believes that its estimated model of the pollution stock evolution, given by Eq. (7), is only an approximation to a true unknown model of the pollution stock dynamics.

Assumption 1

The environmental authority is unable to assign a unique probability distribution to the alternative models of the evolution of the pollution stock and consequently faces Knightian uncertainty.

To simplify the model, I consider two regimes (\(r=1,2\)) that only differ in the degree of model mistrust (i.e. Knightian model uncertainty): optimistic and pessimistic.Footnote 2 I define regime 1 and 2 as the optimistic and pessimistic regime, respectively. In the optimistic regime 1 (\(r=1\)), the environmental authority has a high degree of trust in its estimated model and believes that it is a close representation of the true unknown model. In the pessimistic regime 2 (\(r=2\)), the environmental authority has a lower level of mistrusts in its estimated model and believes it is relatively far from the true unknown model. To simply notation, the current regime \(r_t\) is denoted by i and the next period regime \(r_{t+1}\) by j where \(i,j=1,2\).

Assumption 2

The environmental authority uses robust control in both regimes to deal with the mistrust in its own estimated model of the pollution stock dynamics.

In particular, I implement robust control following the approach of Hansen and Sargent (2008). I assume that the reader is not familiar with robust control and present a concise explanation of the essence of robust control under the current model.

The purpose of robust control is to provide the policy maker (the environmental authority, in this case) with a policy rule that works reasonably well even if its model does not coincide with a true unknown model, as opposed to a policy rule that is optimal if it does but possibly disastrous if it does not. The environmental authority defines a set of likely models around its original estimated model. This set contains the environmental authority’s estimated model and the worst-case model. The environmental authority suspects that a third model, the true unknown model, is also located in this set. In robust control the environmental policy follows Gilboa and Schmeidler (1989) and adopts the emissions tax policy from the worst-case model. This is done not because the environmental authority believes that the worst-case emissions shock will take place, but rather because this is the emissions tax policy that behaves reasonably well under Knightian model uncertainty.

A useful and common interpretation of robust control is as a zero-sum two-player game between the environmental authority and an “evil” nature. In this fictitious game, the evil nature introduces a distortion \(\omega _{t+1}\) in the pollution evolution equation and the environmental authority responds using emissions taxes.Footnote 3 The evil nature uses this distortion to hurt the environmental authority by making emissions shocks higher and more persistent. Therefore, Eq. (7) in each regime is modified as follows:

The evil nature’s distortion \(\omega _{t+1, i}\) is a new control variable and its value depends on the current period’s regime (\(r_{t}=i)\) and ultimately on the history of the pollution concentrations:

This type of distortion means that the model is misspecified in unknown ways that include a wide range of misspecified dynamics mentioned in Athanassoglou and Xepapadeas (2012) such as wrong parameters, autocorrelated errors, feedbacks, nonlinearities, irreversibility and hysteresis effects. Wrong parameters in this model can include the miscalculation of the firm’s abatement costs and its response to emissions taxes, the natural decay in the pollution stock, and the emission sources in the baseline case. The distortion \(\omega _{t+1, i}\) needs to be bounded or the evil nature will produce infinite damage to the environmental authority. The bound is given by the following equation:

where \( \mu _i\) is the bound in regime i. Equation (10) is added to the set of constraints of the environmental authority’s maximization problem and its Lagrange multiplier is denoted by \(-\frac{1}{2}\theta _{t+1,i}\). This new parameter \(\theta _{t+1, i} > 0\) is known as the “free” parameter in the robust control literature and represents the degree of mistrust that the environmental authority has in its estimated model. The values of \(\theta _i\) come from outside the model and are chosen according to the degree of model mistrust of the environmental authority. Small values of \(\theta _i\) are chosen when the environmental authority is pessimistic about its model because they allow the evil nature to introduce a large distortion \(\omega _{t+1}\) in the dynamics of the pollution stock. This produces an emissions tax policy for a larger set of alternative models of the pollution stock dynamics. Alternatively, large values of \(\theta _i\) imply an optimistic environmental authority because the evil nature can only introduce small distortion \(\omega _{t+1}\) to the pollution stock dynamics. This produces an emissions tax policy for a smaller set of alternative models of the pollution stock dynamics.

The values of \(\theta _{t+1, i}\) are bounded by \(\theta _{t+1, i} \in (\underline{\theta }, \infty )\). The lower bound \(\underline{\theta }\) represents the highest degree of model mistrust for which is possible to obtain a robust emissions tax policy.Footnote 4 At the upper bound, when \(\theta _{t+1, i} \rightarrow \infty \), the model mistrust completely dissipates and the environmental authority is fully confident that its estimated model represents the true model.

The main contribution of this paper is precisely that \(\theta _{t+1, i}\) takes on different values on each regime, representing different degrees of mistrust of the environmental authority. Thus, \(\theta _{t+1, 1}\) and \(\theta _{t+1, 2}\) represent the value of \(\theta _{t+1, i}\) in the optimistic regime 1 \((r_t=i=1)\) and in the pessimistic regime 2 \((r_t=i=2)\), respectively. Similarly, the worst-case shock values associated with \(\theta _{t+1, 1}\) and \(\theta _{t+1, 2}\) are \(\omega _{t+1, 1}\) and \(\omega _{t+1, 2}\), respectively. The values of \(\theta _{t+1, i}\) in the model are constrained as follows:

The first part of the restriction, \(0 < \underline{\theta }\) is necessary to assure that the problem is a minmax. The second part of the restriction \(\underline{\theta } < \theta _{t+1, 2}\) guarantees that the level of pessimism is reasonable, i.e. the environmental authority is not catastrophist but rather mistrusting of its own model. The second part of the restriction, \( \theta _{t+1, 2} < \theta _{t+1, 1}\), indicates a higher degree of model mistrust of the environmental authority in regime 2 than in regime 1. The last part of the restriction, \( \theta _{t+1, 1} < \infty \), denotes that the environmental authority mistrusts its own estimated model in both regimes. The following expression summarizes the two regimes:

subject to the restrictions in Eq. (11).

2.3 Switching Between Regimes Using a Markov Chain

I now introduce the Markov chain as the mechanism through which the environmental authority can switch from one regime to the other. In its general form, the Markov chain captures that \(\theta _{t+1, i} \) can switch between \(\theta _{t+1, 1}\) and \(\theta _{t+1, 2}\). I follow Zampolli (2006) and assume that:

Assumption 3

The regime \(r_{t+1}\) follows a first-order Markov chain with transition probabilities that are exogenous, time-invariant, and given by the following transition matrix:

where \(p=Pr\{r_{t+1}=j=2 \mid r_t=i=1 \}\) is the probability to switch from regime 1 to regime 2; and \(q=Pr\{r_{t+1}=j=1 \mid r_t=i=2 \}\) is the probability to switch from regime 2 to regime 1.

A Markov chain is an appropriate choice to model the environmental authority’s time-varying mistrust in its own model because: (i) changes in trust are not predicted with total certainty; (ii) it allows the approximation of more general non-linear time-varying processes; (iii) the degree of mistrust may be dependent on the current state of the environment and the economy; and (iv) changes in trust are not tied to a particular parameter.

Assumption 4

The next regime \(r_{t+1}\) is revealed at the end of the period t after policy action has been decided.

This assumption implies that when the environmental authority chooses the policy rule, \(r_{t}\) is known but \(r_{t+1}\) is still uncertain. Hence, the uncertainty is about where the system will be at time \(t+1\), \(t+2\) and so forth. The transition probabilities (p, q) represent the uncertainty about the type of regime in the next period, after the emissions shock has been observed by the environmental authority. Thus, the probabilities in \(\mathbf{P}\) are pre-switch. The information set of the environmental authority at time t is the following:

2.3.1 Switching to Permanent Regimes

In its general form the Markov chain represents the possibility to alternating between regimes. However, the transition probabilities can be set up in such a way that once the environmental authority has switched to a different regime, the new regime is now permanent. That is, there is a one-time switch, but not alternating, between regimes. This is accomplished by setting q or p equal to zero in the relevant regime. Two interesting cases emerge from this type of set up.

In the first case, pessimism may only experience a one-time permanent decrease in the future. Assume the environmental authority is in the pessimistic regime 2, and set \(p=0\) and \(q>0\). In this case the environmental authority’s degree of pessimism may go down next period (with probability of q). Once in the optimistic regime, the environmental authority’s degree of optimism remains the same. In this set up, observed events or scientific knowledge may give the environmental authority greater confidence about the accuracy of its own estimated model.

In the second case, pessimism may only experience a one-time permanent increase in the future. Assume the environmental authority is in the optimistic regime 1, and set \(q=0\) and \(p>0\). In this case the environmental authority’s degree of pessimism may go up next period (with probability of p). Once in the pessimistic regime, the environmental authority’s degree of pessimism remains the same.

2.4 Time-Varying Mistrust Problem of the Environmental Authority

In the new problem, the environmental authority attempts to minimize the expected discounted infinite sum of pollution damages and abatement costs using \(M_{t, i}\) while the evil nature tries to maximize it using \(\omega _{t+1, i}\). Incorporating Eq. (10), using \(- \frac{1}{2}\theta _{t+1, i}\) as its Lagrange multiplier, and following Zampolli (2006), the new optimal problem of the policy maker can be expressed as solving the following pair of intertwined Bellman equationsFootnote 5:

subject to Eq. (8) in each regime. The current regime represented by \(i =1, 2\) follows the Markov process of Eq. (13) and the values of \(\theta _{t+1, i}\) satisfy the restrictions of Eq. (11). Moreover, \(\nu (S_{t,i}, i)\) represents the continuation value of the dynamic programing problem as function of the pollution stock and the current regime. The regime indicator \(i=1,2 \) implies that the solution produces an optimal steady-state value of \(M_{i}\), \(\omega _{i}\) , \(S_{i}\), and \(\nu (S_{i}, i)\) for each regime.

The next step is to transform the environmental authority’s problem into its space-state representation to solve it as a linear quadratic problem (LQP). Thus, I define the following vectors and matrix:

Next, I substitute \(\widetilde{\mathbf{M}}_{t, i}\), \(\widetilde{\mathbf{B}}\) and \(\widetilde{\varvec{\varLambda }}_{i}\) into the problem given by Eqs. (15) and (8). Since the Riccati equations for the traditional LQP emerges from the first-order conditions alone and the first-order conditions for extremizing a quadratic criterion function match those for and ordinary (non-robust) LQP with two control (see Hansen and Sargent 2008), then the problem consists of finding the controls \(({\widetilde{\mathbf{M}}}_{t,i})_{t=0}^{\infty }\) in order to extremize current and discounted expected losses.Footnote 6 Thus, the problem of the environmental authority is given by the following pair of intertwined Bellman equations:

subject to Eqs. (11), (13), and the new pollution evolution equationFootnote 7:

3 Analytical Solution

Solving the extremization problem of the previous section is equivalent to finding a contingent policy rule \({ \widetilde{\mathbf{M}}}_{t, i}\). The solution is given by the following feedback rule:

Following Kendrick (1981), Zampolli (2006), and Hansen and Sargent (2008); substituting the matrices and vectors in the problem and after extensive algebra I find that the feedback matrices take the following form:

where \(\varvec{\Gamma }_{i}=\Bigl ( \sum ^{2}_{j=1} \mathbf{P}_{i,j} [\delta { \widetilde{\mathbf{B}}' }{} \mathbf{V}_{j} { \widetilde{\mathbf{B}}} + \varvec{\widetilde{\varLambda }}^{'}_{j}]\Bigr )^{-1}\) and \(i,j=1,2\). \(\mathbf{V}_i\) and \(\rho _i\) are the solution to the Riccati matrices and vectors, respectively. Similarly, I obtain the following solution to the Riccati matrices and vector:

where \(\varvec{\Phi }_{i}=\sum ^{2}_{j=1} \mathbf{P}_{i,j} \delta \alpha \mathbf{V}_{j} \mathbf { \widetilde{B}} \) and \(i,j=1,2.\) Equations (19) and (20) show that the solutions of Eqs. (21) and (22) produce one Riccati matrix and vector for each regime (\(\mathbf{V}_1\), \(\mathbf{V}_2\), \(\varrho _1\), \(\varrho _2\)). The solutions to the Riccati matrix and vector are interrelated across regimes. That is, the solution to \(\mathbf{V}_1\) depends on \(\mathbf{V}_2\) and vice versa. The solution to \(\varrho _1\) depends on \(\mathbf{V}_1\), \(\mathbf{V}_2\) and \(\varrho _2\). Similarly, the solution to \(\varrho _2\) depends on \(\mathbf{V}_1\), \(\mathbf{V}_2\) and \(\varrho _1\).

The set of Eqs. in (21) and (22) are examples of discrete Lyapunov equations. There are different methods to solve this type of equations. For the numerical solution, I choose a simple iteration on the Riccati matrices and vectors because of the small dimensionality of the model. First, I iterate jointly on \(\mathbf{V}_1\) and \(\mathbf{V}_2\) until convergence is achieved for each of them. Second, I use the solution to \(\mathbf{V}_1\) and \(\mathbf{V}_2\) from the previous step and iterate jointly on \(\varrho _1\) and \(\varrho _2\) until convergence is achieved. The solution to the Riccati equation for each regime \(\mathbf{V}_i\) places a weight on the Riccati equation of the next period regime \(\mathbf{V}_j\) equal to the probability of transiting to that regime \(\mathbf{P}_{i,j}\).

The optimal steady state solution for the pollution stock is obtained by substituting the right hand side of the feedback rule into the pollution stock dynamics equation in steady state and solving for \(S_i\).

The optimal steady state solution for the vector containing the emissions tax and the worst-case shock is obtained by substituting Eq. (23) into the feedback rule.

The small dimensionality of the model allows me to simplify Eq. (24) to obtain the robust emissions tax rule for each regime:

The main goal of environmental authority is to obtain the robust emissions tax policy given by Eq. (25). The transition probabilities and the degree of model mistrust in both regimes are included in the feedback coefficients \(F_{M, i}\), \(F_{\omega , i}\), \(f_{M, i}\) and \(f_{\omega , i}\). If the environmental authority is optimistic about its estimated model, then the relevant emissions tax policy corresponds to Eq. (25) when \(i=1\). If the environmental authority is pessimistic about its estimated model, then the relevant emissions tax policy corresponds to Eq. (25) when \(i=2\).

The environmental authority’s steady state welfare losses for each regime are given by the following expression:

where \(S_i\) and \({\widetilde{\mathbf{M}}}_i\) are given by Eqs. (23) and (24), respectively.

3.1 Overall and Regime-Specific Model Mistrust

An important difference between the model presented in this paper and the traditional robust control model is that the degree of model uncertainty is tied to the free parameters \(\theta _i\) and the transition probabilities. In particular, the transition probabilities act as bounds on \(\theta _i\) and limit the ability of the evil nature to hurt the environmental authority. Therefore, to better understand the responses of the environmental authority to changes in the different parameters, it is useful to differentiate between two types of uncertainty: regime-specific and overall.

Definition 1

Regime-specific model mistrust is the degree of uncertainty that the environmental authority has in its estimated model of the pollution stock in a specific regime and it is given by \(\theta _i\), where lower values of \(\theta _i\) represent higher levels of model mistrust.

The regime-specific uncertainty in regime 1 is given by \(\theta _1\) and the regime-specific uncertainty in regime 2 is given by \(\theta _2\). Thus, the regime-specific uncertainty is equivalent to the model uncertainty considered in the traditional robust control problems. In this model, the degree of regime-specific model mistrust is higher in regime 2 than in regime 1, i.e. \(\theta _1 >\theta _2\).

Definition 2

Overall model uncertainty, denoted by \(\pi \), is the degree of trust that the environmental authority has in its time-varying model (shown at the end of Sect. 2.4) that includes the regime specific uncertainties and the transition probabilities in the Markov chain. Higher values of \(\pi \) represent a time-varying model that is closer to the non-robust original model and consequently a lower degree of overall model uncertainty.

The signs below the variables in the right-hand side of Eq. (27) indicate their individual effect on the value of \(\pi \). Higher values of \(\theta _i\) decrease the degree of pessimism in a given regime i and consequently decrease the total amount of pessimism in the time-varying model, which is represented by a higher \(\pi \). Higher values of p increase the total amount of pessimism in the time-varying model and consequently lower \(\pi \) because: (i) if the current regime is 1, the probability to switch to the pessimistic regime is higher; and (ii) if the current regime is 2, the expected duration of the optimistic regime 1 (given by \(p^{-1}\)) is lower. Higher values of q decrease the total amount of pessimism in the time-varying model and consequently increase \(\pi \) because: (i) if the current regime is 1, the expected duration of the pessimistic regime 2 (given by \(q^{-1}\)) is lower; and (ii) if the current regime is 2, the probability to switch to the optimistic regime is higher.

The parameters p, q and \(\theta _{t+1, i}\) that directly determine the degree of overall model uncertainty \(\pi \) are exogenous to the model. By definition \(p \in (0,1)\) and \(q \in (0,1)\). Thus, at the beginning of Sect. 5 and in Appendix 1, I discuss in detail how to choose values of \(\theta _{t+1, i}\) for different combinations of (p, q) to obtain reasonable values of \(\pi \).

4 Data

The data for this study are taken from Hoel and Karp (2001) for the case of global warming. This allows me to compare the results to those reported in the previous literature. Abatement costs are measured in billions of 1990 dollars. The initial stock of pollution is 800 billion tons for 1990. Table 1 presents the parameter values according to the definitions of the variables in the present study.

The values for g and c correspond to conservative estimates of the pollution damage function. The values for b, a and f correspond to a moderate estimate of 1 % loss of Gross World Product for a 50 % reduction in emissions. The discount factor is set to \(\delta =0.97\).Footnote 8

5 Numerical Results

In this section, I solve the policy maker problem using the parameter values in Table 1 and the combinations of \(\theta _{t+1, 1}\) and \(\theta _{t+1, 2}\) obtained from the procedure detailed in Appendix 1. I analyze the steady state results for emissions taxes, CO\(_2\) stocks and welfare losses for different combinations of p, q and \(\pi \). I remove the time subscripts from all the variables but leave the regime indicators, i.e. \(\theta _{t+1, {1}} = \theta _{1}\); \(\theta _{t+1, {2}} = \theta _{2}\); \(\omega _{t+1, {1}} = \omega _{1}\); and \(\omega _{t+1, {2}} = \omega _{2}\).

I use two degrees of overall model uncertainty \(\pi =10, 20\,\%\). The value of \(\pi \) represents the probability that the environmental authority can pick the correct model between two competing models of the pollution stock dynamics. Lower values of \(\pi \) indicate a diminished ability of the environmental authority to pick the correct model and consequently higher overall model uncertainty. Appendix 1 details the procedure to obtain \(\pi =10, 20\,\%\). This procedure is just one of the many ways to find reasonable values of \(\theta _{1}\) and \(\theta _{2}\). For example, Gonzalez (2008) and Athanassoglou and Xepapadeas (2012) choose values of \(\theta \) that generate small and reasonable deviations from a benchmark model. The most important consideration is to choose values of \(\theta _{1}\) and \(\theta _{2}\) that do not produces extreme values of the emissions taxes and pollution stocks. Therefore, the combinations of \(\theta _{1}\) and \(\theta _{2}\) I use have the following features: (i) Eq. (11) is satisfied; (ii) \(\theta _{1}\) is large enough that the results in regime 1 are close to those from the deterministic model without robustness, (iii) increases of \(\theta _2\) produce very small changes in the results of regime 2 and (iv) \(\theta _{1}> > \theta _{2}\).

The results are generated as follows. I start with \(p=q=0.1\) and a given combination \(\theta _1\) and \(\theta _2\) that satisfy the aforementioned conditions and produce \(\pi =10\,\%\). Next, I change the combination of (p, q) and I adjust \(\theta _1\) to keep \(\pi \) at 10 %. This adjustment of \(\theta _{1}\) after changing (p, q) is necessary to keep \(\pi \) constant because, as discussed in Sect. 3.1 and shown in Eq. (27), changes in the transition probabilities affect \(\pi \). I continue this procedure for all combinations of (p, q) between (0, 0) and (1, 1). To obtain the results for \(\pi =20\,\%\), I use the same procedure but adjust \(\theta _1\) to produce \(\pi =20\,\%\).Footnote 9

Table 2 shows the steady state emissions taxes and the CO\(_2\) concentrations in the optimistic regime 1 and in the pessimistic regime 2 for selected values of p, q and \(\pi \). To keep the exposition succinct, I show the results for the worst-case shock in Appendix 2. The first two columns present different combinations of p and q. Columns three to six contain the steady state emissions taxes in each regime (\(i=1,2\)) for \(\pi =10\,\%\) and \(\pi =20\,\%\). Columns seven to ten show steady state CO\(_2\) concentrations in each regime for \(\pi =10\,\%\) and \(\pi =20\,\%\).

Proposition 1

Regardless of the current regime, increases in the overall model mistrust (denoted by lower values of \(\pi \)) lead to higher emissions taxes for any given combination of (p, q).

This aggressive use of emissions taxes in the presence of higher model uncertainty is consistent with the Precautionary Principle and with previous research on robust control and model uncertainty (Funke and Paetz 2011; Gonzalez 2008; Hansen and Sargent 2008; among others).

The effects of changes only in p or q without compensating changes in \(\theta _i\) to keep \(\pi \) constant are relatively straight forward and are shown in Appendix 3. In the rest of the paper, I concentrate the analysis to the effect of (p, q) for a constant value of \(\pi \) by adjusting \(\theta _1\) as mentioned above. This allows me to isolate the effects due only to different transition probabilities from those of higher overall model uncertainty.

5.1 Responses to p and q in the Optimistic Regime 1

5.1.1 Emissions Taxes Response

To better understand the response of emissions taxes to changes in the transition probabilities, it is useful to understand the choices faced by the environmental authority in regime 1 assuming these probabilities were unknown to the environmental authority. In the optimistic regime 1, the environmental authority faces the possibility to switch to the pessimistic regime 2 where it will have to counteract a higher worst-case emission shock. If the environmental authority increases taxes in regime 1, preempting a possible switch to regime 2, abatement costs increase in the current period but the pollution stock and damages decrease in the next period. If the environmental authority moves to the pessimistic regime 2 in the next period then, the tax increase and the higher abatement costs of the previous period were a good idea because the evil nature would be less able to inflict damage through \(\omega _2\). However, if the environmental authority remains in the optimistic regime 1 in the next period, then the higher emissions taxes of the previous period were not a good idea because too much abatement has taken place. Another option for the environmental authority is to ignore the possibility to switch to regime 2. In this case, if the environmental authority switches to regime 2 in the next period, then the evil nature can inflict substantial damage.

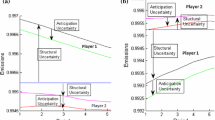

When the transition probabilities are known to the policy maker these trade offs will include the actual values of the transition probability (p), the expected duration of the pessimistic regime (\(q^{-1}\)) and the severity of the worst-case shock in the pessimistic regime 2 (\(\omega _2\)). Figure 1 plots the contour lines for emissions taxes and CO\(_2\) concentrations in regime 1 and 2 for \(\pi =10\,\%\) and complements the information in Table 2.Footnote 10 The results for regime 1 and 2 are presented in the first and second column, respectively. Emissions taxes and CO\(_2\) concentrations are shown in the top and bottom row, respectively.Footnote 11

Regime 1 and 2 emissions taxes and CO\(_2\) concentrations for \(\pi =10\,\%\)

Table 2 and Fig. 1 show that the lowest emissions taxes take place when \(p=q=0\). Assuming the environmental authority is initially optimistic \(p=q=0\) implies that there is just one optimistic regime.

Proposition 2

When the environmental authority is optimistic about its own model, introducing the possibility to switch to a pessimistic regime increases emissions taxes, even if this transition probability (given by p) is small.

Proposition 3

In general, higher values of p and q lead to higher emission taxes in the optimistic regime.

Changes in p produce two counteracting effects. First, increases in p make the overall model more pessimistic which tends to increase emissions taxes. Second, to keep the model uncertainty unchanged the worst-case shock in the pessimistic regime has to decrease. The numerical results in Fig. 1 and Table 2 indicate that the first effect dominates and increases in p lead to higher emissions taxes. Emissions taxes are more sensitive to changes in p as \(p\rightarrow 1\). For \(p > 0.9\) emissions taxes respond for the most part to changes in p and are barely affected by changes in q. Thus, for large values of p the environmental authority’s main concern is to be prepared (with higher emissions taxes) for a likely switch to the pessimistic regime 2.

Changes in q also produce two counteracting effects on emissions taxes. First, higher values of q make the overall model less pessimistic because it implies a lower expected duration of the pessimistic regime and this tends to decrease emissions taxes. Second, to keep overall model uncertainty unchanged, the expected worst-case shock in the pessimistic regime increases which tends to increase emissions taxes. The numerical results in Table 2 and Fig. 1 show that, in general, the second effect dominates and emissions taxes increase with q. That is, for a constant level of model uncertainty (\(\pi \)), a decrease in the expected duration of the pessimistic regime (higher q) leads to higher emissions taxes in the current optimistic regime because the environmental authority is concerned that the evil nature would hit harder in case it switches to the pessimistic regime. The only exception is for values of p close to one, in that case emissions taxes have a negligible response to changes in q.

The largest emissions taxes take place when both p and q are large. This implies that emissions taxes will be high when the probability to switch to the pessimistic regime is high, the expected duration of the pessimistic regime is low but a large worst-case shock awaits the environmental authority if it switches to the pessimistic regime. A large worst-case shock can inflict significant damage to the environmental authority even if the expected duration is low because of the long persistence of CO\(_2\) stocks.

5.1.2 CO\(_2\) Stocks Response

The steady state concentrations of CO\(_2\) in Table 2 and Fig. 1 are of limited use because they include the worst-case shock from the fictitious evil nature the environmental authority has created to obtain a robust emissions tax rule. Nevertheless, analyzing steady state concentrations of CO\(_2\) helps to: (i) check on the validity of the emissions tax policy and the overall model, and (ii) explain the environmental authority’s welfare losses.

CO\(_2\) stocks in the optimistic regime 1 follow a similar pattern as the emissions taxes with respect to changes in the transition probabilities and the degree of model uncertainty. At first sight, this result seems counterintuitive because taxes and stocks should move in opposite directions. In the robust control two-player, zero-sum game, the environmental authority will increase taxes when faced with a higher worst-case shock. However, this is not enough to completely offset the effect of the worst-case emission shock on the pollution stock because higher emissions taxes imply higher abatement costs and losses. Consequently, pollution stocks will: (i) increase despite higher emissions taxes and (ii) follow a similar pattern as emissions taxes.

5.2 Responses to p and q in the Pessimistic Regime 2

5.2.1 Emissions Taxes Response

To better understand the response of emissions taxes to changes in the transition probabilities in regime 2, it is useful to understand the choices and trade offs of the environmental authority assuming these probabilities are unknown to the environmental authority. In regime 2, the environmental authority faces the possibility to switch to the optimistic regime 1, where it will have to counteract a lower worst-case emission shock. If the environmental authority reduces current emissions taxes, anticipating a possible switch to the optimistic regime, then abatement costs are reduced this period but at the expense of higher pollution stocks and damages in the next period. Lower emissions taxes are a good idea if the environmental authority switches to the optimistic regime because it did not incur in excessive abatement. However, if the environmental authority remains in the pessimistic regime in the next period, the evil nature is be able to inflict higher damage. Another option for the environmental authority is to ignore the possibility of switching to regime 1 and set emissions taxes assuming that regime 2 is permanent. In this case, if the environmental authority switches to regime 1 in the next period emissions taxes will be high and too much abatement will take place.

Table 2 and Fig. 1 show the numerical solutions to these trade offs in regime 2 assuming the transition probabilities are known.

Proposition 4

Emissions taxes in regime 2 are mostly insensitive to changes in either p or q.

This result suggests that once the environmental authority is pessimistic, most of the effect of the transition probabilities has already been incorporated in the robust emissions tax policy. A likely explanation is that the main concern of the environmental authority, as it faces the worst-case emission shock in the pessimistic regime, is to keep emissions low because of the long persistence of CO\(_2\).

Changes in p produce two counteracting effects. First, increases in p imply a lower expected duration of the optimistic regime making the overall model more pessimistic which tends to increase emissions taxes. Second, to keep the model uncertainty unchanged the worst-case shock in the pessimistic regime has to decrease. The numerical results in Fig. 1 and Table 2 indicate that for the most part the first effect slightly dominates. Thus, higher values of p produce small increases in emissions taxes.

Higher values of q have two contradictory effects. First, they tend to decrease emission taxes because it implies a higher probability to switch to the optimistic regime. Second, to keep overall model uncertainty constant, the worst-case emission shock in the pessimistic regime has to increase which tends to increase emission taxes. Table 2 and Fig. 1 show that for most values of q (particularly for large values of p and q) the second effect slightly dominates and consequently higher values of q lead to small increases in emissions taxes. Emission taxes are the lowest for \(q>0\) when \(p=0\). That is, emissions taxes in the current pessimistic regime will be lower, for any given \(q>0\), if the possible reduction in the fear of model misspecification is permanent.

5.2.2 CO\(_2\) Stocks Response

As explained in Sect. 5.1.2, the interest in the pollution stocks is mostly to check the validity of the results and its role in explaining the environmental authority’s welfare losses. In the pessimistic regime 2, the response of CO\(_2\) pollution stocks to changes in p, q and \(\pi \) follow the same pattern as the worst-case shock (shown in Appendix 2). The main reason for this type of response is that (as mentioned above) emissions taxes in regime 2 are mostly insensitive to changes in p and q. Thus, CO\(_2\) stocks will move with the changes in the worst-case emissions shock. An increase in p generates higher overall model uncertainty, leading to lower \(\omega _2\) (to keep overall model constant) and consequently to lower CO\(_2\) stocks. In addition, as mentioned above, changes in q have a small effect on emissions taxes, the worst-case shock, and consequently on CO\(_2\) stocks.

5.3 Emissions Taxes Across Regimes

The results in Table 2 and Fig. 1 also allow me to compare emissions taxes and stocks across regimes for a given level of overall model uncertainty. Using Eq. (13), the feedback matrices for regime 1 can be expressed as follows:

where \(\varOmega _1 = (1-p) [{ \widetilde{\mathbf{B}}' }{} \mathbf{V}_{1} { \widetilde{\mathbf{B}}} + \varvec{\widetilde{\varLambda }^{'}}_{1} ] + p [{ \widetilde{\mathbf{B}}' }{} \mathbf{V}_{2} { \widetilde{\mathbf{B}}} + \varvec{\widetilde{\varLambda }^{'}}_{2}] \) and \(\varPsi = \delta { \widetilde{\mathbf{B}}'}\). The feedback matrices for regime 2 take the following form:

where \(\varOmega _2 = q \bigl [{ \widetilde{\mathbf{B}}' }{} \mathbf{V}_{1} { \widetilde{\mathbf{B}}} + \varvec{\widetilde{\varLambda }^{'}}_{1} \bigr ] + (1-q) \bigl [{ \widetilde{\mathbf{B}}' }{} \mathbf{V}_{2} { \widetilde{\mathbf{B}}} + \varvec{\widetilde{\varLambda }^{'}}_{2}\bigr ] \). Equations (28) to (31) show that when \(p > (1-q)\) the terms \(\mathbf{V}_{2}\), \(\varvec{\widetilde{\varLambda }}_2\) and \(\varrho _2\) have a higher weight on the feedback matrices of regime 1 (\(\mathbf{F}_{1}\), \(f_1\)) than on those of regime 2 (\(\mathbf{F}_{2}\), \( f_2\)). This leads to higher emissions taxes in regime 1 than in regime 2. Similarly, when \(p < (1-q)\) the terms \(\mathbf{V}_{2}\), \(\varvec{\widetilde{\varLambda }}_2\) and \(\varrho _2\) have a higher weight on the feedback matrices of regime 2 (\(\mathbf{F}_{2}\), \(f_2\)) than on those of regime 1 (\(\mathbf{F}_{1}\), \( f_1\)), leading to higher emissions taxes in regime 2 than in regime 1. The terms \(\mathbf{V}_{2}\), \(\varvec{\widetilde{\varLambda }}_2\), and \(\varrho _2\) produce higher emissions taxes because they contain \(\theta _2\), allowing the evil nature to inflict more damage. Finally, emissions taxes are the same in both regimes when \(p=(1-q)\) because \(\mathbf{V}_{2}\), \(\varvec{\widetilde{\varLambda }}_2\) and \(\varrho _2\) have the same weight in each regime.

5.4 Environmental Authority’s Welfare Losses

In this subsection, I analyze the environmental authority’s losses in steady state, given by Eq. (26), for different values of p, q and \(\pi \). The objective of the environmental authority is to minimize the losses, and they are the lowest when \(p=q=0\) in regime 1 (for a given value of \(\pi \) ) because there is only one optimistic regime. Losses increase with higher CO\(_2\) stocks (and consequently with larger worst case emission shocks) because the pollution damage function is quadratic on CO\(_2\) stocks and these cannot take on negative values. Similarly, losses increase with higher emissions taxes because the abatement cost function is quadratic in emissions taxes and these are positive in all the results.

To facilitate the analysis and discussion, I use the normalized losses (\(J^{n}_i\)) defined as the Euclidean distance between the actual losses (\(J_i\)) and those from the solution to the original problem without model uncertainty (\(J_{0}\)) given by Eqs. (6) and (7).

Equation (32) indicates that larger values of \(J^{n}_i\) represent higher welfare losses for the environmental authority. Table 3 shows the normalized losses \(J^{n}_i\) for selected values of p, q and \(\pi =10, 20\,\%\).

The first two columns show selected combinations of the transition probabilities (p, q). Columns three to four presents the normalized losses in regime 1 and 2 (respectively) for \(\pi =10\,\%\). Columns five and six show the normalized losses in regime 1 and 2 (respectively) for \(\pi =20\,\%\). In the previous subsection, I showed that emissions taxes and CO\(_2\) stocks increase with higher overall model mistrust. The results in Table 3 show that increases in overall model mistrust (denoted by a lower \(\pi \)) also produce higher welfare losses.

Figure 2 plots the contour lines of the environmental authority’s normalized losses in regime 1 and 2 for \(\pi =10\,\%\).

Regime 1 and 2 normalized environmental authority’s losses for \(\pi =10\,\%\)

Table 3 and Fig. 2 shows that in the optimistic regime 1, the environmental authority’s losses increase with higher values of p and q. As mentioned before, increases in p or q lead to higher emissions taxes, worst-case emission shocks, CO\(_2\) concentrations and consequently higher losses.

In the pessimistic regime 2, the losses follow for the most part a similar pattern (although not the same) as the CO\(_2\) concentrations in regime 2. The environmental authority’s losses are mostly insensitive to changes in q when \(q>0.1\). However, when \(q<0.1\), increases in q generate higher losses for the environmental authority. An interesting pattern emerges in that the losses change from highly sensitive (vertical response lines) when \(q < 0.1\) to highly insensitive (horizontal response lines) when \(q>0.1\). The response of the losses to changes in p is the opposite of the response to changes in q. When \(q>0.1\) higher values of p produce lower the losses and when \(q<0.1\) the losses are mostly unresponsive to change in p.

5.5 Pessimistic and Optimistic Errors

An environmental authority may find it difficult to obtain precise estimates of the transition probabilities in the Markov chain. This can be the result of a lack of previous applicable experiences where the environmental authority has become more or less mistrustful about its model. The environmental authority is more likely to define intervals for p and q but the model can be solved only for point values of the transition probabilities. In this subsection, I attempt to provide more guidance as to what type of assumed transition probabilities are better for the environmental authority given that objective point estimates are not readily available. I do this by analyzing if the environmental authority is better off by over or under estimating the probability of transiting to the pessimistic regime.

My approach follows, with some differences, the procedure outlined in Zampolli (2006). First, I assume that the environmental authority is in the optimistic regime 1. Second, I assume that the environmental authority does not know the true transition probability p, but chooses a transition probability \(\hat{p}\). Third, I choose a fixed value for q. Fourth, I obtain the losses using the emissions taxes associated with \(\hat{p}\) but the values of \(\theta _1, w_1\) associated with p. I perform this exercise for all the pairs \((\hat{p},p)\). By construction, for every true p, minimal losses occur when the chosen and true probability to switch to the pessimistic regime are the same, i.e. \(\hat{p}=p\). I divide the losses for every p by the losses when \((\hat{p},p)=(0,0)\) and denote these new losses as \(J_{\hat{p},p}\).

Figure 3 shows the losses \(J_{\hat{p},p}\) for all the pairs \((\hat{p},p)\) of chosen and true probabilities of switching from the optimistic to the pessimistic regime for \(q=0.25, 0.5, 0.75\).

Losses for \((\hat{p},p)\) and \(q=0.25,0.5,0.75\)

In each graph of Fig. 3, the losses \(J_{\hat{p},p}\) are zero at the main diagonal where \(\hat{p} = p\). As in the previous subsection, the losses computed in this subsection tend to increase for higher values of q, because the worst-case shock increases to keep unchanged the overall degree of model mistrust. The losses \(J_{\hat{p},p}\) are greater in the right side of the main diagonal and they increase as the assumed and true values of p are farther apart.

To evaluate and characterize the optimal behavior of the environmental authority, I define two types of errors: optimistic and pessimistic.

Definition 3

The optimistic error is the sum of the welfare losses when the environmental authority underestimates the probability of switching to the pessimistic regime, i.e. \(\hat{p}<p\).

Definition 4

The pessimistic error is the sum of welfare losses when the environmental authority overestimates the probability of switching to the pessimistic regime, i.e. \(\hat{p}>p\).

In Fig. 3, the pessimistic error is the volume under the plane to the left of the main diagonal for a given interval of \(\hat{p}\). Similarly, the optimistic error is the volume under the plane to the right of the main diagonal for a given interval of \(\hat{p}\). Figure 3 suggests that the optimistic error is greater than the pessimistic error because the losses are higher in the right side of the main diagonal. I confirm this result by computing and comparing the optimistic and pessimistic errors for all the intervals of (p, \(\hat{p}\)) and different values of q. Table 4 displays the optimistic minus the pessimistic error for selected values of (p, \(\hat{p}\)) and q.Footnote 12

The positive values in every cell of Table 4 indicate that the optimistic error is greater than the pessimistic error for the corresponding interval of \(\hat{p}\). For example, in the fourth column of Table 4, when \(\hat{p} \in (0.3, 0.5)\) the environmental authority obtains higher welfare (i.e. lower losses) by assuming \(\hat{p}= 0.5\) (the highest transition probability in the range) for any value of q.

Proposition 5

In the absence of a unique transition probability, the environmental authority obtains higher welfare by assuming the highest probability of switching to the pessimistic regime in a given range of likely transition probabilities.

6 Conclusions

In this paper, I develop a model to analyze the regulation of a stock pollutant where the trust that the environmental authority has on its own estimated model of the pollution stock dynamics can vary through time. The environmental authority may become more or less pessimistic about the accuracy of its estimated model as a result of changes in key environmental or economic variables. I consider two regimes that differ only in the degree of model mistrust: optimistic and pessimistic. In the optimistic model, the environmental authority has more trust in the accuracy of its estimated model to represent the true dynamics of the pollution stock than in the pessimistic regime. I use robust control in both regimes to deal with model mistrust. However, the degree of robustness differs in each regime. I introduce a Markov chain as the mechanism through which the environmental authority can switch between the optimistic and the pessimistic regimes.

The main finding is that introducing the possibility of switching to a regime with a different degree of model uncertainty changes emissions taxes in the current regime. This result holds even for a small probability to switch to the other regime or a short expected duration of the other regime. In general, if the environmental authority believes that there is a possibility to switch to a regime with higher model uncertainty, then an active approach compatible with the Precautionary Principle is optimal by increasing emissions taxes in the current regime and overestimating the probability to switch to such regime. Alternatively, emissions taxes in the current regime decrease when the environmental authority believes that it is possible to switch to a regime with lower model uncertainty. In this sense, the direction of the change in current emissions taxes will depend on what the environmental authority believes can happen to the current degree of model mistrust.

Several extensions to this model can be incorporated in future research. Considering a higher number of regimes and adjusting the transition probabilities to consider the case where the model uncertainty decreases through time is an interesting path for future work. Moreover, considering three regimes would introduce a middle regime where the degree of overall model uncertainty can increase or decrease in the next period. More complex models, such as Anderson et al. (2014), can incorporate the main elements of the framework presented in this paper to account for time-varying uncertainty aversion or analyze if robust control rules can be sensitive to the economic cycle. In addition, modifying the current model and solution to include endogenous transition probabilities or structured regime changes are interesting, albeit challenging, paths for future work. Finally, to gain further insight, future research can compare the emissions tax rules in this paper to those under different model uncertainty assumptions and policy instruments (e.g. quotas, command and control policies).

Notes

The model and the solution method can be extended to a N number of regimes.

Hansen and Sargent (2008) show that the timing of the protocols does not change the solution. That is, the solution of the sequential game is equivalent to solving a simultaneous game. Moreover, the sequence of the moves between the nature and the environmental authority do not affect the solution.

\(\underline{\theta }\) is also known as the breakdown down point in \(H_{\infty }\).

In the case of \(i,j=1\ldots N\), the policy maker problem is expressed as solving N intertwined Bellman equations. When a regime is absorbing the Bellman equation and solution for that regime (presented in the next section) is unrelated to the other regime.

In this case, extremizing (ext) refers to minimizing the welfare losses with respect to emissions taxes, \(M_{t, {i}}\), and maximizing it with respect to \(\omega _{t+1, {i}}\).

The constraint given by Eq. (10) is already incorporated in the criterion function.

This discount factor corresponds to a continuous discount rate of 3 % (\(\delta =0.97=e^{-0.03}\)), which is commonly used in policy analysis. For example, the EPA (2010) recommends the use of 2–3 % annual discount rates. A different discount factor will affect the level of the steady state solutions but the main findings of this paper will not be affected.

The choice of \(\theta _1\) as adjustment is arbitrary but does not affect any of the conclusions in the paper. Similar results for the same \(\pi \) are obtained if \(\theta _2\) is adjusted and \(\theta _1\) is kept constant or if both of \(\theta _1\) and \(\theta _2\) are adjusted. Keeping one \(\theta \) constant across all solutions is done for computational ease.

The contour graphs for \(\pi =20\,\%\) follow the same pattern as those in Fig. 1 for the respective variable. These graphs can be obtained from the author upon request.

Overall model uncertainty is constant within each figure and between the rows of the table.

Zampolli’s (2006) analysis of the losses differs in that he computes the sum of the losses from a specific value of p in a given range of \(\hat{p}\). The main result does not change under this methodology: the environmental authority always obtains lower losses by choosing the highest transition probability to the pessimistic regime in the \(\hat{p}\) range. The step-by-step procedure, matlab implementation and full set of numerical results can be obtained from the author upon request.

The Matlab implementation can be obtained form the author upon request.

References

Anderson, E., William, B., Hansen, L. P., & Sanstad, A. H. (2014). Robust analytical and computational explorations of coupled economic-climate model with carbon-climate response. The Center for Robust Decision Making on Climate and Energy Policy, working paper 13-05.

Athanassoglou, S., & Xepapadeas, A. (2012). Pollution control with uncertain stock dynamics: When, and how, to be precautious. Journal of Environmental Economics and Management, 63, 304–320.

Crepin, A. S., Biggs, R., Polasky, S., Troell, M., & de Zeeuw, A. (2012). Regime shifts and management. Ecological Economics, 84(15), 22.

de Zeeuw, A., & Zemel, A. (2012). Regime shifts and uncertainty in pollution control. Journal of Economic Dynamics and Control, 36, 939–950.

Environmental Protection Agency (EPA). (2010). Guidelines for preparing economic analysis. Washington, DC: National Center for Environmental Economics, Office of Policy.

Funke, M., & Paetz, M. (2011). Environmental policy under model uncertainty: A robust optimal control approach. Climatic Change, 107, 225–239.

Gilboa, I., & Schmeidler, D. (1989). Maxmin expected utility with non-unique prior. Journal of Mathematical Economics, 18, 141–153.

Gollier, C., Jullien, B., & Treich, N. (2000). Scientific progress and irreversibility: An economic interpretation of the precautionary principle. Journal of Public Economics, 75, 229–253.

Gonzalez, F. (2008). Precautionary principle, robustness and optimal taxes for a stock pollutant with multiplicative risk. Environmental and Resource Economics, 41(1), 25–46.

Gonzalez, F., & Rodriguez, A. (2013). Monetary policy under time-varying uncertainty aversion. Computational Economics, 41(1), 125–150.

Herrnstadt, E., & Muehlegger, E. (2014). Weather, salience of climate change and congressional voting. Journal of Environmental Economics and Management, 68, 435–448.

Hansen, L. P., & Sargent, T. J. (2008). Robustness. Princeton: Princeton University Press.

Hoel, M., & Karp, L. (2001). Taxes versus quotas for a stock pollutant with multiplicative uncertainty. Journal of Public Economics, 82, 91–114.

Kendrick, D. (1981). Stochastic control for economic models. New York: McGraw-Hill.

Klibanoff, P., Marinacci, M., & Mukerji, S. (2005). A smooth model of decision making under ambiguity. Econometrica, 73, 1849–1892.

Klibanoff, P., Marinacci, M., & Rustichini, F. (2006). Ambiguity aversion, robustness, and the variational representation of preferences. Econometrica, 74, 1447–1498.

Lang, C. (2014). Do weather fluctuations cause people to seek information about climate change? Climatic Change, 125(3), 291–303.

Millner, A., Dietz, S., & Heal, G. (2013). Scientific ambiguity and climate policy. Environmental and Resource Economics, 55(1), 21–46.

Polasky, S., de Zeeuw, A., & Wagener, F. (2011). Optimal management with potential regime shifts. Journal of Environmental Economics and Management, 62, 229–240.

Roseta-Palma, C., & Xepapadeas, A. (2004). Robust control in water management. Journal of Risk and Uncertainty, 29, 21–34.

Vardas, G., & Xepapadeas, A. (2010). Model uncertainty, ambiguity and the precautionary principle: Implications for biodiversity management. Environmental and Resource Economics, 45, 379–404.

Zampolli, F. (2006). Optimal monetary policy in a regime-switching economy: The response to abrupt shifts in exchange rate dynamics. Journal of Economic Dynamics and Control, 30, 1527–1567.

Author information

Authors and Affiliations

Corresponding author

Appendices

Appendix 1: Choice of \(\theta _1\) and \(\theta _2\)

As mentioned in the main text, the environmental authority’s degree of mistrust about its own model has to come from outside the model in each regime. In Eq. (11) I narrow down the possible values of \(\theta _{t+1, 1}\) and \(\theta _{t+1, 2}\). The goal of this Appendix is to satisfy Eq. (11) by simultaneously finding numerical values of \(\theta _{t+1, 1}\) and \(\theta _{t+1, 2}\) that represent an environmental authority that is optimistic about its estimated model of pollution concentration dynamics in regime 1 and pessimistic in regime 2.

I follow with some differences the procedure outlined in Gonzalez and Rodriguez (2013) that adapts Hansen and Sargent’s (2008) detection error probability approach to include Markov switching and simultaneously choose \(\theta _{t+1, 1}\) and \(\theta _{t+1, 2}\).Footnote 13 I consider two models: the original non-robust model without model uncertainty (given by Eqs. 6–7) and the time-varying model uncertainty model at the end of Sect. 2.4. The procedure consists of finding values of \(\theta _{{t+1, 1}}\) and \(\theta _{{t+1, 2}}\) for which it is statistically difficult to distinguish between the original and the time-varying model in regime 1 and that also satisfy Eq. (11).

First, I obtain the solution for the pollution stock in the original non-robust model:

where \(\ddot{k}=(\alpha + \beta \ddot{F})\) and \(\ddot{H}= \beta \ddot{f} + \bar{x}\). Similarly, I obtain the solution for the pollution stock in the time-varying model:

where \(k_i=(\alpha + { \widetilde{\mathbf{B}}} \mathbf{F}_i)\) and \(H_i=({ \widetilde{\mathbf{B}} }f _i + \bar{x}) \). Next, I define the time-varying model in regime 1 as follows:

The worst-case shock assuming that the pollution stock was generated by the original model is given by:

The worst-case shock assuming that the pollution stock was generated by the time-varying model is then:

The log-likelihood ratio under the original model is then:

The log-likelihood ratio under the time-varying model is then:

I produce 200 random draws over \(\ddot{\varepsilon }_{t+1}\) and \(\breve{\varepsilon }_{t+1}\) and use Eqns. (35) and (37) above to simulate 200 years (\(T=200\)) of the pollution stock, which is roughly the amount of recorded CO\(_2\) emissions data. Next, using Eqns. (38) and (41), I compute \(\ddot{w}\), \(\breve{w}\), \(\ddot{r}\), and \(\breve{r}\).

I perform 1000 simulations of this procedure and obtain the frequency, over all the 1000 simulations, for which \(\ddot{r}\) and \(\breve{r}\) are less than zero:

The error detection probability is then defined as follows:

In this paper, I use the error detection probability as the measure of model uncertainty and set \(\pi = prob(\theta _1, \theta _2, p, q) \). The environmental authority will pick the correct model with probability of one when \(\pi =0\) and it is equally likely to pick either model when \(\pi =0.5\). Therefore, when \(\pi \rightarrow 0.5 \) overall time-varying model uncertainty is small and consequently it is difficult for the environmental to distinguish between the two models. When \(\pi \rightarrow 0\) the overall time-varying model uncertainty is large and it is easy for the environmental authority to distinguish between the two model. Following Hansen and Sargent (2008), I choose values of \(\theta _{{t+1, 1}}\) and \(\theta _{{t+1, 2}}\) associated with \(\pi \) of 0.1 and 0.2 because they correspond to commonly used confidence intervals of 95 and 90 %, respectively.

A drawback of the error detection probability algorithm in this context is that it does not generate a unique set of values of \(\theta _{{t+1, 1}}\) and \(\theta _{{t+1, 2}}\) for each \(\pi \). Therefore, in each of the simulations, I include additional restrictions on the possible parameters of \(\theta _i\). In particular, I select a combination of \(\theta _{1}\) and \(\theta _2\) for each pair (p, q) that satisfies Eq. (11) and produces the desired value of \(\pi \) (0.1 or 0.2) for which: (i) \(\theta _{1}\) is large enough that the results in regime 1 are close to those of the original non-robust model, (ii) increases of \(\theta _2\) produce almost no changes in the results of regime 2 and (iii) \(\theta _1>> \theta _2\).

One last clarification is pertinent. I do not claim that the error detection probability is the only measure of overall model uncertainty. Rather, I use the error detection probability associated with the time-varying model along with a set of restrictions outlined above to find values of \((\theta _1, \theta _2)\) that generate reasonable levels of robustness.

Appendix 2: Worst-Case Shock Numerical Results

In this Appendix, I present the solution for the worst-case shock. To keep the exposition succinct I only show the contour graphs.

Regime 1 and 2 worst-case emissions shocks for \(\pi \) = 10, 20 %

The two graphs in the first row of Fig. 4 show the worst-case shock (\(\omega \)) for all the different combinations of the transition probabilities for regime 1 and regime 2 when \(\pi =10\,\%\). The second row show the results when \(\pi =20\,\%\).

Appendix 3: Emission Taxes for Uncompensated Changes in p and q

In this Appendix, I show the effect of uncompensated changes in the transition probabilities. That is, changes in p and q without the corresponding change in \(\theta _2\) to keep the time-varying model uncertainty the same. Figure 5 shows the contour graph of emission taxes in each regime. The degree of overall model uncertainty varies across the graph but it is \(10\,\%\) at \(p=q=0.1\). Uncompensated increases in p produce a higher overall model uncertainty and generate lower emissions taxes in both regimes, although emission taxes are mostly insensitive to changes in p in regime 1. Uncompensated increases in q produce a lower overall model uncertainty and generate higher emissions taxes in both regimes, although emission taxes are mostly insensitive to changes in q in regime 2. These results along with those of Sects. 5.1 and 5.2 show that increases in the overall model uncertainty due to either higher p, lower q or higher \(\theta _i\) lead to higher emission taxes.

Emission taxes under uncompensated changes in p and q

Rights and permissions

About this article

Cite this article

Gonzalez, F. Pollution Control with Time-Varying Model Mistrust of the Stock Dynamics. Comput Econ 51, 541–569 (2018). https://doi.org/10.1007/s10614-016-9622-z

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10614-016-9622-z