Abstract

Pharmaceutical price regulation in Greece is centralized. The National Drug Organization (EOF) is the main regulatory authority functioning under the auspices of the Ministry of Health and Social Solidarity. In 2004, total pharmaceutical expenditure in Greece reached the level of 2.9 billion €, of which 77.9% were public expenditure and the remaining 22.1% private. According to Organization for Economic Cooperation and Development (OECD) data the total per-capita expenditure on pharmaceutical care in Greece is among the lowest in Europe, representing 58% of the EU-12 average. In 1998, Greece introduced a reimbursement list, and the lowest reference pricing system among the 15 European Union member states with the purpose of controlling the growth of pharmaceutical expenditure. The measures proved to be ineffective since pharmaceutical expenditure, after a short-term reduction, continued to increase at similar rates to those before the introduction of price control mechanisms. The average annual increase of pharmaceutical expenditure in Greece over the period 1998–2003 was 7.9%, which is among the highest in the OECD countries (average 6.1%). New pharmaceutical legislation, no. 3457, was enacted on May 8th 2006, aiming at greater access to medicines, improvements to citizens’ quality of life, effective and efficient utilization of health resources, transparency in public management, protecting public health, and maintaining long-term financial viability of the insurance system. The innovative aspect of the new legislation is the abolition of the positive list and the establishment of a rebate system granting the National Insurance Funds a rebate rate paid by the pharmaceutical companies. The purpose of this paper is twofold. First to assess the effectiveness of the positive list introduced in 1988 in Greece, using simple econometric models. Second to present the recent pharmaceutical reforms aimed at the introduction of a rebate system and establishing reimbursement pricing based on the average of the three lowest European prices.

Similar content being viewed by others

Explore related subjects

Discover the latest articles, news and stories from top researchers in related subjects.Avoid common mistakes on your manuscript.

Introduction

Over the last decade European Union member states have introduced several reforms aimed at the control of pharmaceutical expenditure and ensuring at the same time efficiency, equity, and quality of medicines [1, 2]. However, despite the enacted reforms, the share of gross domestic product (GDP= devoted to pharmaceuticals has grown in the EU-15 countries at a very fast rate. In Greece this share increased from 1.1% of GDP in 1985 to 1.7% in 2004 [3]. Similar increases have been observed in Italy [4], Portugal [5], and France [6], being among the highest spenders (1.5–2% of GDP) in the EU-15 [7, 8].European governments have explored a mixture of policies to curb the expansionary trends of pharmaceutical expenditure by controlling prices and consumption. A wide range of pricing policies was implemented based on product price control, (the most common), reference pricing (Germany [9, 10] the Netherlands [11] and elsewhere) and profit control (UK) [12]. Furthermore, in order to control cost, the potential substitution of more-expensive proprietary brand drugs with generics was proposed, but only a few countries gave permission for pharmacists to prescribe in this way. The consumption of drugs was controlled by denying certain lifestyle drugs (cosmetic therapies), or restricting the reimbursement of products included in a list. Positive lists with reimbursed drugs as well as negative lists with non-reimbursed drugs have been issued by European health authorities. Co-payments were also introduced, requiring patients to cover a proportion of the cost of the prescribed drugs. Finally the prescribing behavior of physicians was controlled by issuing guidelines, providing information on less-expensive therapies, and introducing budgetary controls. The level of success in the implementation of the pharmaceutical reforms varies enormously among European countries depending on a large number of factors such as prescribing patterns, industrial policies, and public health measures to mention a few [13, 14].

In 1998, Greece introduced a positive list and the lowest reference pricing system among the 15 European Union member states with the purpose of curbing the growth of pharmaceutical expenditure [15]. The measures proved to be ineffective since pharmaceutical expenditure, after a short-term reduction, continued to increase at similar rates to those before the introduction of price control mechanisms. Over the period 1998 to 2003, according to OECD data, the annual rate of growth of pharmaceutical expenditure in Greece was 7.9%, which is among the highest in the OECD countries (average 6.1%) [16].

On May 8th 2006, the legislative act no. 3457 was enacted, aiming at a substantial reform of the pricing and reimbursement system. The main aim of this legislation was to alter the focus of the pharmaceutical policy in Greece from the negative reimbursement list to a more-pioneering method aiming at the control of pharmaceutical expenditure and reimbursement rates. More analytically, the new legislation claims to ensure equity in terms of access to medicines, improvements in citizens’ quality of life, effective and efficient utilization of health resources, transparency in public management, protection of public health, and long-term financial viability of the insurance system. The innovative aspect of the new legislation is the establishment of a rebate system granting the National Insurance Funds a rebate rate paid by the pharmaceutical companies.

The stated objectives of the current reform appear ambitious and it remains to be seen whether the public administration and insurance system will be able to comply with the proposed reforms.

The purpose of this paper is twofold. First to describe the pricing and reimbursement system in Greece and to highlight the deficiencies in public pharmaceutical policies introduced in 1998 with the aim of controling the evolution of pharmaceutical expenditures. A simple econometric model is explored to assess the effectiveness of positive list. Second to present the recent pharmaceutical reforms initiated with the legislation no. 3457 enacted on 8th May 2006, introducing a rebate system and reference pricing based on the average of the three lowest European prices.

The Greek health system

The Greek health system presents the features of the Southern European model based on a mixture of both Bismarck and Beveridge elements. Following the European taxonomy of health systems, Greece presents a mixture of public contract and public integrated models financed by a mixture of: (1) social insurance contributions, (2) general taxation, and (3) private payments. Greece is the country with the highest private expenditure among the EU member states and second, after the USA, among the OECD countries [17, 18]. Health care is provided by the public sector (NHS), social insurance agencies, and the private sector. In Greece, the responsible body for national strategy as well as for overall health policy issues is the Ministry of Health and Social Solidarity, which sets priorities at a national level, defines the extent of funding for proposed activities and allocates health resources. Moreover it is responsible for health care professionals and coordinates the hiring of new health care personnel, subject to approval by the ministerial cabinet.

In Greece, the establishment of the National Health System (NHS) was realized in 1983 (law 1397/1983, published in Government Gazette 143Α, 7.10.1983), aiming at the removal of economic barriers to access, equitable, and comprehensive health care coverage by all citizens. Since then, several reforms have been introduced with limited success to ensure efficiency and equity in the health resources. [19]. In 2001, Greece introduced the law 2889, which redefined the social objectives and introduced extensive organizational reforms for the regionalization and management of the health resources. Seventeen health regions were established and emphasis was given to decentralization of the decision-making and management of the system. Despite the good intentions of the reformers the system remained very centralized [20].

In addition to the Ministry of Health and Social Solidarity, around 30 insurance funds participate in the governance of the public health care system. Social insurance funds provide health and pharmaceutical coverage (see Table 1) and operate under the supervision of the Ministry of Employment and Social Security. Assignment to a fund depends on the occupation of the insured and not on his/her income level. The range of services covered, and the contribution rates, are jointly approved by the Ministry of Employment and Social Security and the Ministry of National Economy.

The largest insurance fund in Greece, is the Institute of Social Insurance (ΙΚΑ), covering 50.5% of the Greek population and providing a wide spectrum of health services to urban population blue- and white-collar workers. The Organization of Agricultural Insurance (OGA), provides health care to the rural population (18.5%) covered under a means-tested system. OAEE-TEVE and OAEE-TAE are the insurance funds for merchants, manufacturers, and small trade businessmen (16.2%) (see Table 1). The rest of the population is covered under specific insurance funds, i.e. TSAY, for medical professionals, pharmacists, and dentists, TSMEDE for civil engineers and architects, OTE for telecommunication employees, DEY for those employed in the electricity company, NAT-BANK for national banking, and finally PORTS for those employed in the ports of Greece. Table 1 presents the number of direct and indirect insured population under each of these organizations.

The spectrum of primary and hospital services, as well as pharmaceutical care varies enormously among the insurance organizations. In Fig. 1 we present the pharmaceutical expenditure per insured population undertaken by the insurance organizations. The insured population in ports, banks, public utilities [electricity (DEH) and telecommunication (OTE) industry] enjoy four times higher pharmaceutical expenditure compared to those insured by OAEE-TAE and OAE-TEVE. The average pharmaceutical expenditure in Greece paid by the insurance agencies in 2006 amounted to 505 € with a standard deviation of 255.3 €. The estimated coefficient of variation, which shows the degree of dispersion around the mean, is 50.6%.

Average pharmaceutical expenditure for the major insurance agencies in Greece, 2006

Pharmaceutical expenditure

In 2004, the total pharmaceutical expenditure in Greece reached the level of 2.9 billion €, of which 77.9% was public expenditure and the remaining 22.1% private (see Table 3). According to OECD data the total per capita expenditure on pharmaceutical care in Greece is among the lowest in Europe, representing 58% of the EU-12 average (Fig. 2).

Per-capita pharmaceutical expenditure in the EU-12 countries, 2003

Examining the aggregate national data published by the National Statistical Service of Greece for the period 1995–2004, the nominal total public pharmaceutical expenditure increased from 1,210 million € in 1995 to 2,916 million € in 2004. The corresponding increase in the public pharmaceutical expenditure was from 858 million € in 1995 to 2,272 million € in 2004, and the private pharmaceutical expenditure was from 352 million € in 1995 to 644 million € in 2004 (see Table 2). In relative terms, the share of pharmaceutical expenditure to total health expenditure increased from 15.7% in 1995 to 17.8% in 2004.

Looking at the proportion of GDP devoted to the pharmaceutical sector (see Fig. 3) we observe a slight reduction in 1998 after the launch of the reimbursement list (Fig. 3).

Pharmaceutical expenditure in Greece as a percentage of GDP, 1991–2004

It is worth mentioning that in 1998, the Greek government introduced two measures to curb pharmaceutical expenditures: (a) the launching of a positive list, and (b) a recalculation of prices of all pharmaceutical products according to the lowest price in Europe (EU-15). The second measure brought about the one-off effect on the reduction of expenditure rather than the positive list per se.

Overall we can see in Fig. 3, that the cost containment measures had a short-term effect followed by an upward trend over the period 1998–2004. The effects of the positive list on the evolution of health expenditure are discussed further in the next section.

Pharmaceutical price regulation

Most European Union member states (EU-25) have established responsible bodies for publishing pricing and reimbursement guidelines [21, 22]. However, price setting remains a national health policy issue. The price regulation process is based on an agreement between the country’s health authorities and the pharmaceutical industry. The purpose of the agreement is usually to approve safe and effective medicines at reasonable prices, encouraging investment and competitive economic policies. An increasing number of European countries have introduced economic evaluation in their reimbursement decisions for pharmaceutical price regulation [23]. Finland and the Netherlands refer to cost-effectiveness and patients’ quality of life criteria to determine the real value of a medicine. Other countries like Austria, Belgium, Denmark, Ireland, Italy and Portugal take into account a variety of economic criteria. In the UK the National Institute for Clinical Excellency (NICE) undertakes a more-rigorous approach to economic evaluation. NICE was established on 1st April 1999 and its role is to make recommendations to clinicians and managers on: (1) economic appraisal of new and existing technologies, (2) development of clinical guidelines, and (3) specification of audit technologies [24–26]. Following the 2003 German health reform, the Institute for Quality and Efficiency in Health Care (IQWIG) was established in Germany to start operation in October 2004. Article 139a of the Social Code Book V defines the following aims: (1) evaluation of the current state of medical knowledge on diagnostic and therapeutic schemes for selected group of diseases, (2) evaluation of quality and efficiency of services provided by the statutory health insurance, (3) assessment of drug effectiveness, (4) development of evidence based guidelines, (5) recommendations for disease management, and (6) dissemination of information on evidence-based therapies, quality, and efficiency of health services [27].

In Greece the issue of economic evaluation was initially discussed in 2001, when the author of the paper, as president of the committee for guidelines to Economic Evaluation, submitted a report to the Ministry of Health [28]. The report was distributed to the Industry and the Hellenic Association of Pharmaceutical Companies (SFEE). The majority of the Industry and SFEE expressed the view that the introduction of a fourth hurdle into the regulatory environment would complicate the reimbursement process and was considered inappropriate. The economic evaluation guidelines scheme was abandoned.

Pharmaceutical regulation in Greece is highly centralized. The National Drug Organization (EOF) is the main regulatory authority functioning under the auspices of the Ministry of Health and Social Solidarity (see Fig. 4).

Application and pricing procedure in Greece

EU directives 65/65/EEC, 75/318/EEC, 75/319/eec and current EU pharmaceutical legislation constitute the basis for market regulation. Overall the operating regulatory environment is considered fair and transparent [29]. Pharmaceutical companies are required to prepare an application dossier in order to start the procedure for a drug authorization. The application dossier is submitted to the National Drug Organization (EOF) (stage A). The contents of the submitted file dossier should comply with the instructions issued by the organization. The requirements for an application dossier are list on the website of EOF and are in line with the European committee’s guidelines. These requirements can be recapitulated as follows [30]:

-

Proposed trade name

-

Conciseness

-

Name of active substance(s)

-

Sponsor-holder

-

Identification (national/local)

-

Proposed distribution

-

Product’s life expectancy

The price committee at the Ministry of Development deals with the pricing process. A three-month period is usually required for an effective decision (stage B), which is circulated back to the pharmaceutical company. A prerequisite for price setting is the marketing of the product in at least one European country. The responsibility for pricing of pharmaceuticals lies with the Ministry of Development, which issues official prices subject to the consent of the Ministry of Health [31]. The prices of pharmaceuticals are regularly published in a price bulletin, which is distributed to all pharmacies. Prices for all medicinal products are determined by the Ministry of Development (see Fig. 4), which takes into account the following criteria:

-

Wholesale prices of imported products. These are fixed at the lowest ex-factory European price to which import expenses and other charges that apply are added.

-

Wholesale prices of the locally manufactured or packaged products, which are defined by talking into account production and distribution costs, adding the profit margin of the producer as well as other charges that may apply.

-

The derived price is verified against the price of the same product in other European Union countries and the lowest price in the ΕU is applied.

-

The wholesale price is the price at which the pharmacist purchases medicines. This price includes the wholesaler’s profit and compulsory discounts to pharmacists. For wholesalers, the gross profit margin is fixed at 8.43%, based on the net price of the producer or importer (the wholesaler purchase price) or at 7.78% on the wholesale price (the pharmacy purchase price).

-

The retail price is the wholesale price plus the pharmacist’s profit margin and value-added tax (VAΤ). The retail price is uniform throughout the country except for some districts where reduced VAT rates apply. The pharmacist’s gross profit margin is 35% of the wholesale price. The VAΤ rate is the same for both prescription-only and over-the-counter (OTC) products, and is set at 8% on top of the price that derives from the wholesale price plus the pharmacist’s gross profit margin. Νο other surcharges apply.

-

The prices of generic products are set at 80% of the retail price of the respective branded medicine. Generic substitution is not permitted in Greece. The prices of over-the-counter (OTC) products in Greece are also regulated. The criteria used for calculating the price of an OTC product are the same as those of prescription-only medicines. Moreover, OTC products can only be sold by pharmacies and represent only 9% of the pharmaceutical market.

-

The hospital price of a drug is the wholesale price reduced by 13%. Α hospital is supplied with medicines directly from the pharmaceutical companies according to the needs of each clinical department. The procurement procedure is carried out by hospital pharmacies. Α special hospital scientific committee gives approval for a new product to be ordered.

Reimbursement is based on a three-tired system of co-payment (25, 10 and 0%). The rate of co-payment for a prescription drug is uniform for all insurance funds and is set at 25%. A co-payment of 10% applies to medicines for the beneficiaries of cash benefits for low-income pensioners (EKAS) and chronic diseases. including Parkinson’s disease, chronic pulmonary cardiac disease, osteoporosis, inocystic disease, coronary heart disease, tuberculosis and asthma. The 0% co-payment category includes medicines used for malignant neoplasms, diabetes mellitus, psychosis, epilepsy, hemophilia, renal failure, multiple sclerosis, paraplegia, quadriplegia, and cytostatic medicines.

Public hospitals dispense medicinal products to the poor at no charge.

The 1998 reimbursement list

In 1998, according to article 20 of act no. 2458/1997, Greece introduced a reimbursement list, and the lowest reference pricing system among the 15 European Member States with the purpose of controling the growth of pharmaceutical expenditure. A medicine was reimbursed in Greece if it was included in the positive list, which was uniform for all social insurance funds. This list was regularly revised and updated [32]. A product could not be included in the list unless it had been first granted a market authorization from the Ministry of Health and Social Solidarity. The list was published in the press and in the official gazette of the Greek government.

The criteria for inclusion in the list of medicinal products that are reimbursed by the state were:

-

Product’s proven therapeutic efficacy

-

Safety

-

The average cost of daily treatment (CDT)

-

The level of reimbursement of the medicinal product by other ΕU member states

-

Any data that the committee responsible for the positive list may consider appropriate

The principle criterion for the inclusion of a medicinal product in the list was its therapeutic impact, which was evaluated on the basis of the severity of the disease treated, the product’s effectiveness/safety ratio, the availability of alternative treatments with or without medicines, and the target population. Furthermore, in order for a product to be included in the positive list, its average cost of daily treatment, which was calculated by the members of the list Ccommittee, should be equal to or lower than the reference for the pharmaco-therapeutic category in which the product was included.

Community directive 89/105

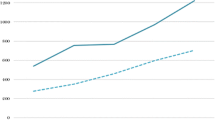

According to this directive the procedure for inclusion of a drug product in the list should not exceed 90 days. In Greece delays in the inclusion of medicinal products in the reimbursement list were beyond this limit and this directive was violated. According to the IMS data the average delay between marketing authorization and accessibility to patients in Greece dropped from over 500 days in 2004 to 335 days in 2006 (Fig. 5). Despite the impressive progress over the two-year period Greece remains one of the EU countries with the longest delays. In Spain this time is around 248 days and in Sweden 128 days (see Fig. 5).

Average time delay between marketing authorization and effective market access. European Agency for the Evaluation of Medicinal (EMEA) Products with marketing authorization between 30th June 2001 and 30th June 2005

A characteristic example of the Greek delays in the inclusion of the new products was the latest publication of the reimbursement list. When this list came into force in March 1st 2004, it did not include drugs priced after July 2002. The pharmaceutical industry brought an action against Government policies and the Greek council of state judged in January 2005 that the pharmaceutical pricing as unconstitutional. The court expressed the view that a sole-country reference, that of the lowest price in Europe, was by itself an inadequate criterion for assessing the cost and price of a locally produced or imported drug. Hence, the pricing system was found to violate the principles of free trade and fair competition introduced initially by the Treaty of Rome, and should be replaced by a more-rigorous analysis based on price calculations based on more countries.

Assessing the impact of the 1998 list

The introduction of a positive list in 1998 influenced both the demand and supply sides of the Greek pharmaceutical market. In this section an attempt is made to assess the impact of the positive list upon health expenditure. To do this we use the OECD time-series data for Greece covering the period 1970–2003. The empirical specification of the model is the traditional one explored in the vast literature of health economics [33, 34]. For the purpose of our analysis we adopt the following double logarithmic form:

where:

- GDP:

-

= real gross domestic product per capita

- THE:

-

= total (public and private) pharmaceutical expenditure per capita

- a and b :

-

= parameters to be estimated

- u :

-

= the usual stochastic term

The main hypothesis that should first be empirically verified is the sign of the parameter b, the income elasticity. If the sign of the parameter b is greater than one then, following the voluminous literature of health economics, health is characterized as a luxury good [35]. This implies that per-capita pharmaceutical expenditure rises faster than the GDP. The empirical findings are shown in Table 3.

In the logarithmic relationship (see Table 3) the estimated parameters are statistically significant at a high statistical level (p < 0.001), (see column 5 of Table 3). Furthermore the values of the coefficient of determination R 2 show that the empirical models can explain more than 95% of the evolution of pharmaceutical expenditure in Greece. The estimated elasticity is 1.02, supporting the findings in the literature [36, 37]. It should be stated that, apart from income, there are additional factors that influence pharmaceutical expenditure. For instance on the demand side there are other important determinants such as ageing. The elderly consume more medicines due to their chronic conditions and the general deterioration of their health. Tastes for more-effective and probably more-expensive therapies are also an important factor.

Important supply-side determinants of per-capita pharmaceutical expenditure is the number of physicians per 1,000 population (who may prescribe more) as well the number of pharmacists per 1,000 population. In Fig. 6 we present the relationship between specialized doctors and pharmacists per 1,000 populations. Greece appears to be the country with the highest number of specialized physicians.

Relationship between pharmacists and specialised physicians per 1,000 population, 2002

A detailed analysis of the prescribing pattern of Greek physicians and its impact upon pharmaceutical expenditure would provide interesting results for pharmaceutical policy.

Despite the importance of these determinants to pharmaceutical expenditures we do not attempt here a detailed empirical investigation, because such a task is outside the scope of the study.

The impact of the positive list is assessed by inserting into the above logarithmic function a dummy variable taking the value of one for the period 1998–2003 and zero for all previous years, i.e., 1970–1997. Hence:

where:

THE, and GDP as above

- a, b, and c :

-

= parameters to be estimated

- u :

-

= the usual stochastic term.

- List:

-

= dummy variable.

- ListT :

-

= 1 for the period 1998–2003 when positive list in effect

- ListT :

-

= 0 otherwise

It becomes important to investigate the sign of the parameter c. If c is positive then the list did not influence the expansion of pharmaceutical expenditure. If c is negative then the list introduced a downturn in the evolutionary process of the pharmaceutical expenditure. The empirical results of this hypothesis are shown in Table 4.

The sign of the variable List (parameter c) is positive, showing opposite effects from the introduction of the positive list. Ceteris paribus, the introduction of the price list did not prove to be effective in controlling the expansionary trends of pharmaceutical expenditure in Greece. However, we should be cautious in interpreting these results because the estimated parameter is not significant at p < 0.001 but only at p < 0.069 (see column 5 of Table 4). Similar results were reached from two different less-econometric studies conducted by Karokis et al. [38] and Lopatatzidis et al. [39], indicating that the introduction of positive list resulted only in a one-off reduction in the rate of pharmaceutical expenditure.

The new reforms

The Greek government made considerable progress recently by enacting in May 2006, legislative act no. 3457, aiming at full coverage for all medicines except OTCs and lifestyle drugs, and abolishing the old restrictive reimbursement list. A new pricing system was introduced based on the average of the three lowest European prices, of which two are calculated from the former 15 European Member States plus Switzerland and one from the new states that joined the EU after May 2004. The new pricing system is called 2 + 1 and became official policy in December 2005 [40]. The innovative aspect of the new legislation is the establishment of a rebate system granting the National Insurance Funds a rebate paid by the pharmaceutical companies. The rebates will be calculated for the period starting 1st January 2006. The Greek government considers pharmaceutical care an investment in the health of Greek citizens and is proceeding with pharmaceutical reform aimed at greater access to medicinal products, rational prescribing, improvements in quality of life, and long-term financial viability of the insurance organizations. The areas of reforms are discussed below.

Transparency committee (EDAF)

In order to ensure transparency in the approval and reimbursement of drugs, a seven-member committee was proposed by legislative act 3457, to be established in the National Drug Organization (EOF), called thr Transparency Committee in the Reimbursement and Medicinal Products (EDAF). The main tasks of the EDAF are summarized as: (1) to define therapeutic categories, (2) to create clusters of disease, and (3) to classify all medicinal products accordingly. The inclusion of a drug in a therapeutic category is based on objective and transparent criteria defined by the Ministry of Health and Social Solidarity. The decision of EDAF is published in the official government gazette. A reference price is calculated per therapeutic category by taking into account the entire original medicinal products included in the category. The public sector (primary-care units and hospitals) and the insurance funds reimburse the drugs of each therapeutic cluster up to the level of the reference price. It is stated in the legislation that the government undertakes the responsibility to develop therapeutic clustering over the period of the next two years.

Rebate pricing

A rebate price is calculated for each therapeutic category. The mathematical form determining the rebate price is the following:

where Y represents a coefficient defining the reduction of the retail price.

The rebate prices for each medicinal product are published in a price bulletin. The rebate amount is calculated by multiplying the rebate price by the quantity of drugs purchased per therapeutic cluster. According to the proposed legislation the public sector would fully reimburse the product. The pharmaceutical manufacturer or distributor will pay a rebate, which is defined as the difference between the price reimbursed by the social insurance funds and the reference price for the therapeutic cluster.

An unfulfilled promise

Health technology assessment (HTA) agencies have been increasingly established across Europe aiming at the analysis of short- and long-term social and economic consequences of the use of new drugs and modern technology. HTAs are also used for efficient decision-making about the reimbursement of pharmaceuticals and to make recommendations on their effective and efficient use. The significance and the effects of HTAs on decisions vary among the European countries. For instance while in the UK there is only one HTA (NICE), in Germany there are two official agencies, i.e., DIMDI for health economics analysis, and IOWiG for outcome assessments [41]. In Denmark HTA is examined with reference to four aspects: technology (clinical evidence), economy, patient, and organization [42]. However, the contribution of HTA agencies to efficient decision-making is controversially criticized. Maynard et al. [43] argue that. although NICE in the UK was established as a rationilizing mechanism to ensure efficient prioritization, it has creating inflationary pressure in NHS health expenditure.

In Greece, following European experience, in the draft legislation under article 11, a HTA agency was proposed for the evaluation of health technology assessment (OATY). The legal status of the OATY was envisaged to be a private law entity, supervised by the Ministry of Health and Social Solidarity. The purpose of the agency was to evaluate new health technology, therapeutic interventions, clinical practices, and disease management. Despite the importance of such an agency the Ministry of National Economy expressed some reservations concerning the establishment of such an institution and at the last minute it was removed from the legislative act no. 3457 and the discussion was postponed to future decisions.

Greece is at a crossroads of reform. Some may acknowledge the good intentions behind the introduction of pharmaceutical reforms. However, some scepticism should be expressed about the implementation of the announced reforms. The EDAF has been proposed but not yet established. The rebate system has not been implemented due to significant problems with regard to the readiness of the insurance organizations to fully computerize their system for electronic prescribing, and the public bureaucracy to modernize its structures following the European trends in adopting new public management and efficient decision-making. Future pharmaceutical policies should consider the long-term feasibility and accountability in implementing the proposed reforms. Emphasis should be given to quality of care, access to effective therapies, and HTA for rationaling and efficient prioritization in the pharmaceutical sector.

References

Ess, S.M., Schneewiss, S., Szucs, T.D.: European health care policies for controlling drug expenditure. Pharmacoeconomics. 21(2), 89–103 (2003)

Jacobzone, S.: Pharmaceutical policies in OECD countries: reconciling social and industrial goals. OECD Labour Market and Social Policy Occasional Papers, No. 40, OECD, Paris (2000)

Kousoulakou Ch.: The market for medicines in Greece. IOBE, Greece (2006)

Ghislandi, S., Krulichova, I., Garattini, L.: Pharmaceutical policy in Italy: towards a structural change? Health Policy 72(1), 53–63 (2005)

Gouveia Pinto C., Teixeira I.: Pricing, reimbursement of pharmaceuticals in Portugal. Eur. J. Health Econ. 3(4), 267–270 (2002)

Imai, Y., Jacobzone, S., Lenain, P.: The changing health system in France. OECD Economics Department Working Papers No. 269. OECD, Paris (2000)

Mossialos, E., Mrazek, M., Walley, T. (eds).: Regulating pharmaceuticals in Europe: Striving for efficiency, equity, and quality. Open University Press, Berskshire (2004)

OECD (2005) Health data file. OECD, Paris

Schulenburg, JM., Uber, A.: Current issues in German health care Pharmacoeconomics 12(5), 517–523 (1997)

Zweifel, P., Crivelli, L.: Price regulation of drugs: lessons from Germany. J. Regulat. Econ. 10, 257–273 (1996)

De Vos, C.M.: The 1996 pricing and reimbursement policy in the Netherlands. Pharmacoeconomics 10(suppl 2), 75–80 (1996)

Oliver, A.: The English National Health Service: 1979–2005. Health Econ. 14, S75–S99 (2005)

Mossialos, E., Mrazek, M., Walley, T.: Regulating pharmaceuticals in Europe: striving for efficiency equity, and quality. European Observatory. Open University press, Berskshire (2004)

Kanavos, P.: Pharmaceutical pricing and reimbursement policies in Europe. Script Report (2002)

Yfantopoulos, J.: Economic policy and guidelines for the control of pharmaceutical expenditure (in Greek). University of Pelloponnessos. Series on Social and Educational policies, pp 61–74 (2005)

OECD.: Health Data 2005 Statistics and Indicators for 30 Countries. OECD Paris (2005)

Hurst, J.: Performance measurement and improvement in OECD health systems: overview of issues and challenges. Measuring up: Improving health systems performance in OECD countries. OECD, Paris (2002)

OECD.: The reform of health care systems: a review of seventeen OECD countries. Health policies studies. OECD, Paris (1994)

Yfantopoulos, J.: Health Economics: Theory and Policy, 2nd edn. Dardanos, Atthens (2006)

Yfantopoulos J.: The welfare state in Greece. In: Metaxas A.J., (eds) About Greece, pp 263–179. Koryfi Publication, Athens (2004)

Scherer, F.M.: The pharmaceutical industry. In: Culyer, A.J., Newhouse, J., (eds) Handbook of health economics. Elsevier, Amsterdam (2000)

Mrazek, M.: Comparative approaches to pharmaceutical price regulation in the European Union Croatian Med. J. 43(4), 453–461 (2002)

Maynard, A., Bloor, K.: Regulating the pharmaceutical industry. Br. Med. J. 315, 200–201 (1997)

Hutton, J., Maynard, A.: A NICE challenge for health economics. Health Econ. 9, 89–93 (2000)

Buxton, M.: Implications of the appraisal function of the National Institute for Clinical Excellence (NICE). Value Health 4(3), 212–216 (2001)

http://WWW.nice.org.uk

http://WWW.g-ba.de

Yfantopoulos, J., Karagianni, V., Kafetzopoulos V.: Guidelines for economic appraisal in Greece. Ministry of Health and Welfare, Athens (2001)

SFEE.: The market of pharmaceuticals in Greece. Hellenic Association of Pharmaceutical Companies, Greece (2005)

http://WWW.eof.gr

Kontozamanis , V., Mantzouneas, E., Stoforos, C.: An overview of the Greek pharmaceutical market. Eur. J. Health Econ. (4), 327–333 (2003)

Greek Government Gazette.: Legislative Act No. 2458/1997 on Positive List (1997)

Newhouse, J.P.: Medical care expenditure: A cross national survey J. Human Resources 12(1), 115–125 (1977)

Hitiris, T., Posnett, J.: The determinants and effects of health expenditure in developed countries J. Health Econ. 11, 173–181 (1992)

Di Matteo, L.: The income elasticity of health care spending A comparison of parametric and nonparametric approaches Eur. J Health Econ 4(1), 20–29 (2003)

Kanavos, P., Yfantopoulos, J.: Cost containement and health expenditure in the EU: a macroeconomic perspective. In: Mossialos, E., Le Grand, J. (eds.) Health care and cost containmenet in the European Union, pp 155–196. Ashgate, England

Sen, A.: Is health care a luxury? New evidence from OECD data. Int. J. Health Care Finance Econ. 5, 147–164 (2005)

Karokis, A., Christodoulopoulou, A., Tsiaras, T., Mossialos, E.: Pharmaceutical price controls and positive drug list effects on total and social insurance pharmaceutical expenditure. Paper presented at the ISPOR Conference, Amsterdam (2000)

Lopatatzidis, A., Hatziandreou, E., Nectarios, M.: Assessment of the effects of a positive drug list in primary care prescribing in Greece (in Greek). Social Security Fund, Athens (2001)

Greek Government Gazette (2006) Legislative Act. No. 3457/2006. Reform of the pharmaceutical care system. Gazette no.93 (May 8th 2006), pp 925–928

Kulp, W., Greiner W.: Health Economics and HTA. Bundesgesumdheitsblatt Gesundheitsforschung Gesundheitsschutz 49(3), 257–263 (2006)

Draborg, E., Andersen, C.k.: Recommendations in health technology assessments worldwide. Int. J. Technol. Assess. Health Care Spring 22(2), 155–160 (2006)

Maynard, A., Bloor, K., Freemantle, N.: Challenges for the National Institute for Clinical Excellence. Br. Med. J. 329, 227–229 (2007)

Acknowledgments

I am grateful to Prof. Wolfgang Greiner and two anonymous reviewers for their useful comments on previous drafts. All possible errors and omissions are the sole responsibility of the author.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Yfantopoulos, J. Pharmaceutical pricing and reimbursement reforms in Greece. Eur J Health Econ 9, 87–97 (2008). https://doi.org/10.1007/s10198-007-0061-6

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10198-007-0061-6