Abstract

In this paper, we discuss the fuzzy portfolio selection problems in multi-objective frameworks. A comprehensive model for multi-objective portfolio selection in fuzzy environment is proposed by incorporating mean-semivariance model and data envelopment analysis cross-efficiency model. In the proposed model, the cross-efficiency model is formulated within the framework of Sharpe ratio; bounds on holdings, and cardinality constraints are also considered. The nonlinear constrained multi-objective portfolio optimization problem cannot be efficiently solved by using traditional approaches. Thus, a multi-objective firefly algorithm is developed to solve the relevant model. Finally, an example verifies the validity of the proposed approaches.

Similar content being viewed by others

Explore related subjects

Discover the latest articles, news and stories from top researchers in related subjects.Avoid common mistakes on your manuscript.

1 Introduction

The mean-variance (M–V) model proposed by Markowitz (1952) has made tremendous contribution to the modern portfolio selection theory, in which return is quantified as the mean and risk as the variance. Since then, many researchers have improved and expanded the M–V model based on different risk measurements, see for instance, mean-semivariance models (Markowitz 1959; Grootveld and Hallerbach 1999), mean absolute deviation (MAD) model (Konno and Yamazaki 1991), mean semiabsolute deviation models (Speranza 1993; Ogryczak and Ruszczynski 1999), mean absolute deviation skewness model (Konno et al. 1993), etc. All above researches are based on the probabilistic framework where the returns of securities are regarded as random variables with probability distributions. However, because the financial markets are complex, and we sometimes lack enough historical data, it is difficult to obtain the precise probability distributions of the security returns. With the help of fuzzy set theory proposed by Zadeh (1965), a number of scholars have studied portfolio selection problems in fuzzy environment, for instance, Carlsson et al. (2002), Gupta et al. (2008), Wang et al. (2011), Liu and Zhang (2013), Chen (2015), Chen et al. (2018), Vercher and Bermúdez (2015), Mehlawat (2016) and Liagkouras and Metaxiotis (2018).

Data Envelopment Analysis (DEA) approach proposed by Charnes et al. (1978) is a mathematical programming-based approach for measuring relative efficiency of decision-making units (DMUs) that have multiple inputs and outputs. Subsequently, it turns out that DEA is a worthy tool for evaluating performance in a wide range of fields, such as the interesting applications in health care (Sherman 1984), education (Avkiran 2001), environment (Fried et al. 2002), banking (Grigorian and Manole 2006), energy (Hu and Kao 2007). In addition to above applications, in recent years, DEA method has been applied to portfolio performance evaluation. Murthi et al. (1997) first applied DEA method to portfolio performance evaluation and concluded that the proposed approach is consistent with traditional Sharpe index (Sharpe 1966) and Jesnen Index (Jensen 1968). Joro and Na (2006) developed a portfolio performance measure in a mean-variance-skewness framework by utilizing a non-parametric DEA method. Branda (2013) introduced new efficiency tests, in which deviation and return measures were regarded as the inputs and outputs, respectively. Lim et al. (2014) presented a DEA cross-efficiency method and proposed a new model called DEA M–V cross-efficiency model. Liu et al. (2015) evaluated the efficiency of portfolios by constructing DEA models and proved that the DEA frontiers can approximate the real frontier of portfolios with big enough sample size. More recently, Gouveia et al. (2017) used the value-based DEA method to assess the performance of Portuguese mutual fund portfolios. Zhou et al. (2018) proposed a DEA frontier improvement approach under the M–V framework. Later, Zhou et al. (2018) presented a segmented DEA approach based on data segment points, and proved that the approach was effective and practical in evaluating the cardinality constrained portfolio performance. Tarnaud and Leleu (2017) presented an idea that performance measurement of portfolios with DEA should not rely on a technology defined through a production process that assimilates risk to an input generating some return. Zhou et al. (2018) proposed a multi-objective evolutionary algorithm based on decomposition and DEA approach for portfolio optimization. It should be noted that above researches are based on the assumption that security returns are random variables instead of fuzzy variables. At present, few researchers have applied the DEA approach to fuzzy portfolio evaluation problems. Chen et al. (2018) presented three kinds of DEA-based fuzzy portfolio efficiency evaluation models in different risk measures.

Note that, all above-mentioned researches focus either on developing different portfolio selection models, or on presenting various portfolio performance evaluation models. But, no research has yet been carried out from both above aspects. Recently, Mashayekhi and Omrani (2016) proposed a fuzzy multi-objective portfolio selection model based on M–V model and DEA cross-efficiency models to simultaneously consider return, risk and the efficiency of the portfolio. To the best of the authors’ knowledge, except for the above one work, there is few research on constructing fuzzy portfolio evaluation model by integrating M–V model and DEA cross-efficiency model. Especially, when return distributions of securities are asymmetric, using variance as risk measure leads to an unsatisfactory prediction of portfolio behavior. This lack of works has motivated this work. In this paper, we will develop a comprehensive model for fuzzy multi-objective portfolio selection by incorporating fuzzy mean-semivariance model and DEA cross-efficiency model. It should be noted that the cross-efficiency model is formulated within the framework of Sharpe ratio.

With the introduction of some practical constraints including cardinality constraint in multi-objective frameworks, the multi-objective portfolio selection problem has become popular; and the complexity of computation makes it be the NP-hard problems (Shaw et al. 2008). Several researchers have attempted to solve this problem by a variety of techniques, but exact solution methods may fail to obtain an optimal solution in reasonable time; and the computation time grows rapidly with the problem size. Using metaheuristics in this case is imperative. At present, several scholars have applied metaheuristic optimization techniques including evolutionary algorithms (EAs) for multi-objective portfolio optimization problem, such as Krink and Paterlini (2011), Anagnostopoulos and Mamanis (2011), Bermúdez et al. (2012), Lwin et al. (2014), Saborido et al. (2016) and Liagkouras and Metaxiotis (2018). In 2008, a new biologically inspired metaheuristic algorithm, known as the firefly algorithm (FA), was developed by Yang (2008). Since the introduction of FA, it has been successfully applied to various optimization problems, see the survey by Fister et al. (2013) and Yang and He (2013). However, to our knowledge, few researchers have applied FA for solving fuzzy multi-objective portfolio optimization problems with complex realistic constraints. In addition, the basic FA was developed for unconstrained issues and exhibits some deficiencies when solving the constrained multi-objective model. Therefore, a multi-objective FA is developed for the fuzzy multi-objective portfolio optimization model.

In summary, this paper discusses the fuzzy portfolio selection problem, in which return, risk, and the efficiency of the portfolio are considered simultaneously. The main contributions of this paper are as follows: (1) we propose a comprehensive model for fuzzy multi-objective portfolio selection by incorporating fuzzy mean-semivariance model and DEA cross-efficiency model. Especially, inspired by the ideas of Sharpe ratio (SR), the cross-efficiency model is formulated within the framework of SR; and (2) we develop a multi-objective firefly algorithm (MOFA) to solve the proposed multi-objective portfolio optimization model.

The rest of the paper is organized as follows. Section 2 presents the proposed fuzzy multi-objective portfolio comprehensive model. In Sect. 3, the multi-objective firefly algorithm is introduced. After that, an example is given to verify the validity of the proposed approaches in Sect. 4. Finally, the conclusion of the paper is summarized in Sect. 5.

2 Model formulation

2.1 Possibilistic mean-semivariance portfolio model

Similar to Carlsson et al. (2002) and Chen (2015), we assume that the returns of assets are trapezoidal fuzzy numbers. Let security return \(r_i\) be a trapezoidal fuzzy number with tolerance interval \([a_i, b_i]\), left width \(\alpha _i\) and right width \(\beta _i\), i.e., \(r_i=(a_i,b_i,\alpha _i,\beta _i)\) with \(\gamma -\) level sets \( [r_i]^{\gamma }=[a_i-(1-\gamma )\alpha _i, b_i+(1-\gamma )\beta _i], i=1,2,\ldots , n. \)

Carlsson and Fullér (2001) introduced the notions of crisp possibilistic mean and crisp possibilistic variances of fuzzy numbers. Easily seen that if \(r_i=(a_i,b_i,\alpha _i,\beta _i)\) is a trapezoidal fuzzy number then

and

Furthermore, the possibilistic mean of the return associated with the portfolio \((w_1, w_2, \ldots , w_n)\) can be obtained as

and the possibilistic variance of return associated with the portfolio \((w_1, w_2, \ldots , w_n)\) as

where \(w_i\) is the proportion of security \(i, i=1,2,\ldots ,n.\)

Taking the possibilistic mean of portfolio return as return measure and the possibilistic variance as the risk measure, several researchers have proposed various types of fuzzy portfolio models in the mean-variance framework, such as Carlsson et al. (2002) and Liagkouras and Metaxiotis (2018). However, when return distributions of securities are asymmetric, using variance as risk measure leads to an unsatisfactory prediction of portfolio behavior. Therefore, some scholars employed semivariance as an alternative risk measure to qualify the portfolio risk, see for instance Markowitz (1959), Ballestero (2005), Zhang et al. (2012) and Liu and Zhang (2015). In this paper, we employ the lower possibilistic semivariance to measure the risk of portfolio. Based on Carlsson and Fullér (2001), and Saeidifar and Pasha (2009), Zhang et al. (2012) presented the definition of the lower possibilistic semivariances of fuzzy number A with \([A]^{\gamma }=[\underline{a}(\gamma ),\bar{a}(\gamma )]~ (\gamma \in [0,1])\), as follows,

Besides, the lower possibilistic semivariance of return related with the portfolio \((w_1, w_2, \ldots , w_n)\) can be expressed by

In the following, we use the possibilistic mean of portfolio return as return measure and the lower possibilistic semivariance as the risk measure. Furthermore, the possibilistic mean-semivariance portfolio model can be formulated as the following bi-objective programming problem:

Constraint (7)(a) denotes the budget constraint, namely, all the money available should be invested. Constraint (7)(b) denotes the cardinality constraint which imposes a limit on the number of assets in the portfolio. Constraint (7)(c) ensures that if any of security i is held (\(z_i=1\)) its proportion \(w_i\) must lie no less than \(\varepsilon _i\) and no more than \(\delta _i\) while if no security i is held (\(z_i=0\)), its ratio \(w_i\) is zero. Constraint (7)(d) is the integrality constraint. Constraint (7)(e) ensures that short selling is not allowed.

2.2 A comprehensive model for fuzzy multi-objective portfolio selection

Nowadays, the DEA cross-efficiency model, developed by Doyle and Green (1994), has applied to the fuzzy portfolio selection problems, see for example Ruiz and Sirvent (2017) and Mashayekhi and Omrani (2016). However, there are two shortcomings for cross-efficiency evaluation in portfolio selection. The first one is the lack of portfolio diversification and the second one is the ‘ganging-together’ phenomenon (Tofallis 1996). To address this issue, Lim et al. (2014) proposed a DEA M–V cross-efficiency model by taking the cross-efficiency into the M–V framework. Mashayekhi and Omrani (2016) presented an integrated fuzzy multi-objective Markowitz-DEA cross-efficiency model. In this paper, we will propose a comprehensive model for fuzzy multi-objective portfolio selection by incorporating fuzzy mean-semivariance model and DEA cross-efficiency model. It should be noted that, in Mashayekhi and Omrani (2016), the integrated model was formulated within the framework of Markowtiz’s mean-variance. However, in this paper, based on the Sharpe ratio (SR) (Sharpe 1966), the cross-efficiency model is formulated within the framework of SR. For a DMU (decision-making unit) l, returns and risks are replaced by the means and variances of the cross-efficiency scores, respectively. The proposed DEA cross-efficiency model is expressed as follows:

where \(\overline{e}_i\) is the cross-efficiency score of DMU i, \(\mathrm{cov}(e_i, e_j)\) is the covariance between DMU i’s cross-efficiencies (\(e_i\)) and DMU j’s cross-efficiencies (\(e_j\)).

To solve the model (8), cross-efficiencies (\(e_j\) ) should be first obtained. The basic steps of obtaining \(e_j\) are summarized as shown in below.

Step 1. Because of the existence of negative values in inputs and outputs, this paper uses the additive variable returns to scale (VRS) DEA model with a range-adjusted measure (RAM) of inefficiency. The additive model with a range-adjusted measure (RAM) of inefficiency is as follows:

where \(q_{ik}\) and \(p_{rk}\) represent the cost of input i and the price of output r for DMU k, respectively. n, m and s are the numbers of DMUs, inputs and outputs, respectively. \(x_{ij}\) and \(y_{rj}\) are the amount of the \(i\hbox {th}\) input and the \(r\hbox {th}\) output for the \(j\hbox {th}\) DMU, respectively. And \(\varepsilon _k\) is a positive infinitesimal value. The model (9) maximizes DMU’s efficiency score and optimizes the weight for all DMUs simultaneously. The directional vectors \(R^-_i\) and \(R^+_r\) can be defined as:

Step 2. Let \(^*\) represent the optimal solution of model (9). The efficiency score of other DMUs are obtained by using the weights that DMU k has chosen. The cross-efficiency of DMU l with the weights of DMU k (\(e_{kl}\)) can be expressed as follows:

Step 3. A matrix of cross-efficiencies are obtained as \(E = (e_{kl} ), \quad (k, l=1,2, \ldots ,n), \) where \(e_{kl}\) is the cross-efficiency of DMU l evaluated by DMU k. The cross-efficiency score of DMU l can be calculated as the average of \(l\hbox {th}\) column:

Based on above discussions, we incorporate fuzzy mean-semivariance model and SR-based DEA cross-efficiency model to construct a comprehensive model for fuzzy multi-objective portfolio selection, which is formulated as follows:

3 Multi-objective firefly algorithm

3.1 The basic FA

The firefly algorithm (FA), which was inspired by the social and flashing activity of fireflies, was proposed by Yang (2008). The FA follows the three rules:

1. Fireflies are attractive to each other regardless of the sex.

2. Attractiveness is based on brightness. So a less bright firefly moves toward a brighter firefly. The attractiveness and brightness are inversely proportional to distance.

3. The landscape of the objective function value is the brightness of fireflies.

Let \(w_i\) be the \(i\hbox {th}\) firefly in the population, where \(i=1, 2, \ldots , SN,\) and SN is the population size. The attractiveness between two fireflies \(w_i\) and \(w_j\) can be calculated as follows:

where D is the dimension of the problem, \(r_{ij}\) is distance between \(w_i\) and \(w_j\), and \(w_{i,k}\) and \(w_{j,k}\) are the \(k\hbox {th}\) component element of \(w_i\) and \(w_j\), respectively. Further, the parameter \(\beta _{0}\) denotes the attractiveness at the distance \(r=0\), and \(\gamma \) is the light absorption coefficient. By the suggestions of Yang (2008), \(\gamma \) is set to \(1/\varGamma ^2\), where \(\varGamma \) is the length scale for designed variables.

In the FA, the firefly with less brightness is attracted to the firefly with more brightness. The movement equation of firefly i moves to firefly j can be stated as:

where \(\alpha _t\) is randomization parameter, and \(\in ^t_i\) is a vector of random numbers from uniform distribution. Equation (12) consists of three terms. The first term is the current position of a firefly. The second term is the form of attractiveness function which is a monotonically decreasing function. The third term is the randomization.

3.2 The proposed MOFA

3.2.1 Initialization

At the initialization step, following Bacanin and Tuba (2014), FA generates SN random populations using

where \({\text {rand}}(0,1)\) is a random number uniformly distributed in [0, 1].

3.2.2 Constraint handling

(1) Boundary constraint. If the initially generated value for the \(j\hbox {th}\) parameter of the \(i\hbox {th}\) firefly does not fit in the scope [\(\varepsilon _j\), \(\delta _j\)], it is being modified:

(2) Cardinality constraint. Decision variables \(z_{i,j}\ (i=1, 2, \ldots , SN,j=1, 2, \ldots ,n)\) are generated randomly by applying

where \(\phi \) is random real number between 0 and 1.

(3) Budget constraint. For the constraint \(\sum _{i=1}^nw_i=1\), we set \(\psi =\sum _{i=1}^nw_{i,j}\) and put \(w_{i,j}= w_{i,j}/\psi \) for all assets that satisfy \(j=1, 2, \ldots ,n\). The same approach for satisfying this constraint was used in Cura (2009).

3.2.3 Firefly movement

(1) For a dominated firefly i, the movement of the firefly toward firefly j that dominates itself is calculated as in the original FA implementation (Yang 2008):

The position of each individual can be updated sequentially, by computing the fitness of each particle and updating them during every iteration of the cycle.

(2) For a non-dominated firefly, each value of objectives is defined a weight vector to calculate the integrated best solution \(g^t_*\). The \(g^t_*\) minimizes a combined objective via the weighted sum

where \(\omega _k\) is a random number uniformly distributed between 0 and 1. \(f_k\) is the \(k\hbox {th}\) objective. To ensure the sum of \(\omega _k\) equal to 1, the weight is normalized that \(\omega _k'=\omega _k/\sum ^{3}_{k=1}\omega _k\). To maintain a diverse set of non-dominated solutions along the Pareto front, for each iteration, \(\omega _k\) should be regenerated randomly.

Approximate efficient frontier in the case of \(m = 8\). a GA, b PSO, c FA, d MOFA

Then, the firefly moves by

where \(g^t_*\) is currently the best position achieved by the given set of \(\omega _k\). And we use

where \(\alpha _0\) is the initial randomness factor.

Finally, the implementation procedure of MOFA is described as Algorithm 1.

4 Numerical experiments

We consider an example introduced by Mashayekhi and Omrani (2016). In this example, the data source is taken from 52 firms of the stock exchange market in Iran. The trapezoidal fuzzy return of 52 securities are shown in Table 1. In addition, the data required for inputs and outputs of DEA are obtained from the latest financial statements which are published by the firms (period 21 March 2013 to 21 December 2013). As in Mashayekhi and Omrani (2016), 16 financial input/output parameters are employed, which are presented in Table 2. Solving the model (9), the cross-efficiency scores of firms are presented in Table 3.

4.1 Algorithm experiment

The parameters of the MOFA are set as follows: the max generation is set to 100, \(SN = 50\), \(\alpha _0 = 0.5\), \(\beta _0 = 0.2\), \(\gamma =1\). Moreover, \(\varepsilon _i\) and \(\delta _i\) are set to 0.05 and 0.2, \(i=1, 2, \ldots ,n\). Other values of control parameters employed for genetic algorithm (GA), particle swarm optimization (PSO) and basic FA are presented below.

GA settings: The crossover probability \(p_c\) and the mutation probability \(p_m\) are set to 0.9 and 0.1, respectively. The selection method is roulette wheel and the crossover method is one-point crossover.

PSO settings: The inertia weight factor \(\omega \) is 0.8, the learning factors, \(c_1\) and \(c_2\) are both set to 1.5.

Basic FA settings: The values of parameters are the same as those of MOFA.

In addition, a total of 20 runs for each experimental setting are conducted.

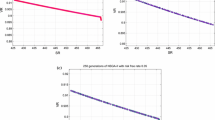

Given the cardinality \(m = 8\), the performance indicator parameters such as maximum, minimum, mean, and standard deviation (SD) of the three objectives using different algorithms are tabulated in Table 4. The best results are marked in bold. From Table 4, it can be easily observed that, in most cases, the minimum, maximum, and mean results obtained by the MOFA are better than those listed for the other algorithms. That is, the proposed MOFA is more accurate solution than some of the other standard heuristic algorithms. Moreover, we find that the values of SD obtained by the MOFA is higher than those obtained by GA and PSO, indicating that the MOFA leads to the diversity of solution.

The approximate efficient frontiers produced at random by GA, PSO, FA and MOFA in the case of \(m = 8\) are shown in Fig. 1. It is obvious that among the four algorithms, the distribution of the MOFA is the best, while that of the other three algorithms are more concentrates. Additionally, we can see that, in most cases, the solutions by MOFA have large return, small risk and better Sharpe ratio of efficiency.

Approximate efficient frontiers in the case of \(m = 8, 10, 12\) and 15. a\(m = 8\), b\(m = 10\), c\(m = 12\), d\(m = 15\)

4.2 Model experiment

For the proposed model (10), given m = 8, 10, 12 and 15 respectively, some Pareto solutions are presented in Tables 5, 6, 7 and 8. First, we present the diversity of portfolio regarding mentioned criteria. For example, in Table 5, there are portfolios with return ranging from 0.0853 to 0.1789, and the Sharpe ratio of efficiency is between − 0.2542 and − 0.5471 among the solutions of the proposed model. Moreover, decision makers can weigh their preferences between mentioned criteria in choosing portfolios from Pareto solutions which are calculated from the model (10). For instance, in Table 7, there are portfolios which have return (0.1720 \(\rightarrow \) 0.1715), Sharpe ratio of efficiency (− 0.5842 \(\rightarrow \) − 0.2522) and nearly risk (0.0362 \(\rightarrow \) 0.0358). If the decision maker are more effect-oriented, he/she can choose the seventh portfolio, whereas if he/she wants higher returns, he/she can choose the first portfolio. Similarly, the fourth portfolio and the fifth one have nearly Sharpe ratio of efficiency (− 0.2785 \(\rightarrow \) − 0.2758) with different return (0.1236 \(\rightarrow \) 0.1368) and risk (0.0175 \(\rightarrow \) 0.0184). Then, risk avoiders can choose the former portfolio, while risk suitors can choose the latter.

Moreover, approximate efficient frontiers are shown in Fig. 2 in the case of m = 8, 10, 12 and 15. From Fig. 2, it also can be found that the portfolios are well-diversified and the investor can choose the satisfying portfolio based on the preferences between three investment objectives.

Finally, in order to illustrate the effectiveness of the proposed model (10), given \(m=6\), under \(\delta \) = 0.2, 0.4 and 0.6, respectively, we compare the results with those obtained by the possibilistic mean-semivariance portfolio model, i.e., model (7). Three objective function values, i.e., return, risk and SR, are given in Table 9. From Table 9, it can be easily observed that, in most cases, the proposed model (10) increases the portfolio efficiency at nearly identical returns. In addition, we can find that the Sharpe ratio of efficiency obtained by the proposed model is better than those obtained by the possibilistic mean-semivariance portfolio model.

5 Conclusion

This paper presented a comprehensive model for fuzzy multi-objective portfolio selection model based on mean-semivariance and DEA cross-efficiency models. Inspired by the ideas of Sharpe ratio, a novel cross-efficiency model was presented. Furthermore, we formulated a comprehensive model simultaneously considered return, risk, the efficiency of the portfolio, bounds on holdings, and cardinality. Moreover, the multi-objective firefly algorithm (MOFA) was developed to solve the proposed model. In order to illustrate the proposed approach, a case study involving 52 firms were considered. The numerical results showed that there are good diversity of objectives between Pareto solutions of the proposed model for investors to trade-off.

For future research, some other variant objectives or realistic constraints can be added to the proposed model (e.g., skewness, kurtosis, and liquidity). In addition, some widely adopted metrics, such as generation distance (GD), spacing (S), diversity metric (\(\triangle \)), can be used to evaluate the performance of the MOFA.

References

Anagnostopoulos K, Mamanis G (2011) Multiobjective evolutionary algorithms for complex portfolio optimization problems. Comput Manag Sci 8:259–279

Avkiran NK (2001) Investigating technical and scale efficiencies of Australian Universities through data envelopment analysis. Socio-Econ Plan Sci 35:57–80

Bacanin N, Tuba M (2014) Firefly algorithm for cardinality constrained mean-variance portfolio optimization problem with entropy diversity constraint. Sci World J 2014:721521

Ballestero E (2005) Mean-semivariance efficient frontier: a downside risk model for portfolio selection. Appl Math Finance 12:1–15

Bermúdez JD, Segura JV, Vercher E (2012) A multi-objective genetic algorithm for cardinality constrained fuzzy portfolio selection. Fuzzy Sets Syst 188:16–26

Branda M (2013) Diversification-consistent data envelopment analysis with general deviation measures. Eur J Oper Res 226:626–635

Carlsson C, Fullér R (2001) On possibilistic mean value and variance of fuzzy numbers. Fuzzy Sets Syst 122:315–326

Carlsson C, Fullér R, Majlender P (2002) A possibilistic approach to selecting portfolios with highest utility score. Fuzzy Sets Syst 131:13–21

Charnes A, Cooper WW, Rhodes E (1978) Measuring the efficiency of decision making units. Eur J Oper Res 2:429–444

Chen W (2015) Artificial bee colony algorithm for constrained possibilistic portfolio optimization problem. Physica A 429:125–139

Chen W, Gai YX, Gupta P (2018) Efficiency evaluation of fuzzy portfolio in different risk measures via DEA. Ann Oper Res 269:103–127

Chen W, Wang Y, Mehlawat MK (2018) A hybrid FA–SA algorithm for fuzzy portfolio selection with transaction costs. Ann Oper Res 269:129–147

Cura T (2009) Particle swarm optimization approach to portfolio optimization. Nonlinear Anal Real World Appl 10:2396–2406

Doyle JR, Green R (1994) Efficiency and cross-efficiency in data envelopment analysis: derivatives, meanings and uses. J Oper Res Soc 45:567–578

Fister I, Fister I Jr, Yang XS, Brest J (2013) A comprehensive review of firefly algorithms. Swarm Evol Comput 13:34–46

Fried HO, Lovell CAK, Schmidt SS, Yaisawarng S (2002) Accounting for environmental effects and statistical noise in data envelopment analysis. J Prod Anal 17:157–174

Gouveia MDC, Neves ED, Dias LC, Antunes CH (2017) Performance evaluation of Portuguese mutual fund portfolios using the value-based DEA method. J Oper Res Soc 3:1–13

Grigorian DA, Manole V (2006) Determinants of commercial bank performance in transition: an application of data envelopment analysis. Comp Econ Stud 48:497–522

Grootveld H, Hallerbach W (1999) Variance vs downside risk: Is there really that much difference? Eur J Oper Res 114:304–319

Gupta P, Mehlawat MK, Saxena A (2008) Asset portfolio optimization using fuzzy mathematical programming. Inf Sci 178:1734–1755

Hu JL, Kao CH (2007) Efficient energy-saving targets for APEC economies. Energy Policy 35:373–382

Jensen MC (1968) The performance of mutual funds in the period 1945–1964. J Finance 23:389–416

Joro T, Na P (2006) Portfolio performance evaluation in a mean-variance-skewness framework. Eur J Oper Res 175:446–461

Konno H, Yamazaki H (1991) Mean-absolute deviation portfolio optimization model and its applications to Tokyo stock market. Manag Sci 37:519–531

Konno H, Shirakawa H, Yamazaki H (1993) A mean-absolute deviation-skewness portfolio optimization model. Ann Oper Res 45:205–220

Krink T, Paterlini S (2011) Multiobjective optimization using differential evolution for real-world portfolio optimization. Comput Manag Sci 8:157–179

Liagkouras K, Metaxiotis K (2018) Multi-period mean-variance fuzzy portfolio optimization model with transaction costs. Eng Appl Artif Intell 67:260–269

Lim S, Oh KW, Zhu J (2014) Use of DEA cross-efficiency evaluation in portfolio selection: an application to Korean stock market. Eur J Oper Res 236:361–368

Liu WB, Zhou ZB, Liu DB, Xiao HL (2015) Estimation of portfolio efficiency via DEA. Omega 52:107–118

Liu YJ, Zhang WG (2013) Fuzzy portfolio optimization model under real constraints. Insur Math Econ 53:704–711

Liu YJ, Zhang WG (2015) A multi-period fuzzy portfolio optimization model with minimum transaction lots. Eur J Oper Res 242:933–941

Lwin K, Qu R, Kendall G (2014) A learning-guided multi-objective evolutionary algorithm for constrained portfolio optimization. Appl Soft Comput 24:757–772

Markowitz H (1952) Portfolio selection. J Finance 7:77–91

Markowitz H (1959) Portfolio selection: efficient diversification of investments. Wiley, New York

Mashayekhi Z, Omrani H (2016) An integrated multi-objective Markowitz-DEA cross-efficiency model with fuzzy returns for portfolio selection problem. Appl Soft Comput 38:1–9

Mehlawat MK (2016) Credibilistic mean-entropy models for multi-period portfolio selection with multi-choice aspiration levels. Inf Sci 345:9–26

Murthi BPS, Choi YK, Desai P (1997) Efficiency of mutual funds and portfolio performance measurement: a non-parametric approach. Eur J Oper Res 98:408–418

Ogryczak O, Ruszczynski A (1999) From stochastic dominance mean-risk model: semideviation as risk measure. Eur J Oper Res 116:33–50

Ruiz JL, Sirvent I (2017) Fuzzy cross-efficiency evaluation: a possibility approach. Fuzzy Optim Decis Mak 16:1–16

Saborido R, Ruiz AB, Bermudezc JD, Vercher E, Luque M (2016) Evolutionary multi-objective optimization algorithms for fuzzy portfolio selection. Appl Soft Comput 39:48–63

Saeidifar A, Pasha E (2009) The possibilistic moments of fuzzy numbers and their applications. J Comput Appl Math 223:1028–1042

Sharpe WF (1966) Mutual fund performance. J Bus 39:119–138

Shaw DX, Liu S, Kopman L (2008) Lagrangian relaxation procedure for cardinality-constrained portfolio optimization. Optim Method Softw 23:411–420

Sherman HD (1984) Hospital efficiency measurement and evaluation, empirical test of a new technique. Med Care 22:922–938

Speranza MG (1993) Linear programming models for portfolio optimization. J Finance 14:107–123

Tarnaud AC, Leleu H (2017) Portfolio analysis with DEA: prior to choosing a model. Omega 75:57–76

Tofallis C (1996) Improving discernment in DEA using profiling. Omega 24:361–364

Vercher E, Bermúdez JD (2015) Portfolio optimization using a credibility mean-absolute semi-deviation model. Expert Syst Appl 42:7121–7131

Wang B, Wang S, Watada J (2011) Fuzzy portfolio selection models with value-at-risk. IEEE Trans Fuzzy Syst 19:758–769

Yang XS (2008) Nature-inspired metaheuristic algorithms. Luniver Press, London

Yang XS, He X (2013) Firefly algorithm: recent advances and applications. Int J Swarm Intell 1:36–50

Zadeh LA (1965) Fuzzy set. Inf Control 8:338–353

Zhang WG, Liu YJ, Xu WJ (2012) A possibilistic mean-semivariance-entropy model for multi-period portfolio selection with transaction costs. Eur J Oper Res 222:341–349

Zhou ZB, Jin QY, Xiao HL, Wu Q, Liu WB (2018) Estimation of cardinality constrained portfolio efficiency via segmented DEA. Omega 76:28–37

Zhou ZB, Liu XH, Xiao HL, Wu SJ, Liu YY (2018) A DEA-based MOEA/D algorithm for portfolio optimization. Clust Comput 4:1–10

Zhou ZB, Xiao HL, Jin QY, Liu WB (2018) DEA frontier improvement and portfolio rebalancing: an application of china mutual funds on considering sustainability information disclosure. Eur J Oper Res 269:111–131

Acknowledgements

This research was supported by the Beijing Municipal Education Commission Foundation of China (No. KM201810038001). The author Mukesh Kumar Mehlawat acknowledges the financial support through DST PURSE Phase II Grant from University of Delhi, Delhi, India.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors declare no conflict of interest.

Ethical approval

This article does not contain any studies with human participants or animals performed by any of the authors.

Additional information

Communicated by Y. Ni.

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

About this article

Cite this article

Chen, W., Li, SS., Zhang, J. et al. A comprehensive model for fuzzy multi-objective portfolio selection based on DEA cross-efficiency model. Soft Comput 24, 2515–2526 (2020). https://doi.org/10.1007/s00500-018-3595-x

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00500-018-3595-x