Abstract

A common definition of liquidity in real estate investment is the ability to sell property assets quickly at full value, as reflected by transaction volume. The present paper makes methodological and conceptual contributions in the study and understanding of liquidity. First, we extend the Fisher et al. (Real Estate Economics, 31(2), 269–303, 2003) Fisher et al. (The Journal of Real Estate Finance and Economics, 34(1), 5–33, 2007) methodology for the separate tracking of changes in reservation prices on the demand (potential buyers) and supply (potential sellers) sides of the asset market. We show how to apply the methodology to a repeat sales indexing framework, allowing application to typical commercial property transaction price datasets, which lack appraisal valuations or complete data regarding property characteristics. We also use a Bayesian, structural time series approach to estimate the indexes. These methodological enhancements enable much more granular supply and demand index estimation, including at the metropolitan level. Second, we propose a Liquidity Metric based on the indexes, and show that the normal liquidity dynamic in commercial property asset markets is “pro-cyclical”, that is, price and trading volume tend to move together, with demand tending to lead supply. Additionally, we observe an “anomalous” dynamic that occurs about 25 percent of the time, in which the Liquidity Metric declines while consummated prices are rising. This anomalous dynamic is often associated with the end of a period of rapid price growth.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction and Motivation

Liquidity, defined as the ability to sell assets quickly at full value, is crucial in any investment asset class. This is particularly true in the case of commercial real estate, as private property markets are not liquid in the same way as public securities markets such as equities and bonds. In the private real estate asset class, liquidity is often effectively indicated by the volume of trading as a fraction of the inventory, the turnover ratio. In theory, the turnover ratio is directly related to the inverse of the expected time on the market for asset sales, and this is confirmed by empirical evidence (Van Dijk 2018).

But how does liquidity “happen” in the private property market and what are the underlying dynamics of liquidity in commercial real estate? Liquidity is inextricably bound to price. Ceteris paribus, it is easier to sell an asset more quickly for a lower price. Price dynamics and liquidity dynamics must be viewed together. At the aggregate level of the asset market as a whole, the fundamental phenomenon is how the market seeks equilibrium, the balance between supply and demand that determines both the consummated transaction prices and the quantity of trading volume that we observe in the market over time. The classical perspective on the dynamics of market equilibrium was first put forth by Walras, with the concept of “tatonnement”.Footnote 1

The key point about tatonnement that is relevant here is that, at any given price, the observable difference in the quantity of supply offered and the quantity of demand bid determines how the price must change in order to balance those two quantities. The Walrasian auctioneer calls out a price, and if there are more buyers than sellers at that price, then she adjusts the price upward, and vice versa. It is the empirical observation of quantities that moves the price toward equilibrium over time. Fundamentally, quantity changes are observed first, followed by price adjustments. Prices respond to imbalances in quantity.

In many markets, this plays out in a characteristic empirically observable lead/lag relationship between quantity and prices. For example, in labor markets, typically the unemployment rate must fall below some “full employment” level before there is much upward pressure on wages. In the real estate space markets, we typically see changes in occupancy before we see major changes in effective rents. Vacancy must fall below the so-called “natural rate” in the space market before rents on new leases in the market start to climb much in effective terms.

In investment property asset markets, volume tends to change slightly before prices, and there is typically a “pro-cyclical” relationship between trading volume and price, both in levels and first differences or returns. Normally, at the typical quarterly frequency at which real estate markets are tracked, when volume is rising, asset transaction prices are also rising, and vice versa. Private property markets are famously cyclical, with historically long (though not completely smooth) upswings followed by rapid and deep downturns. Three such cycles have characterized the previous half-century in the U.S. and the major downturns have been characterized by a drying up of liquidity in the market.Footnote 2

Fisher et al. (2003, 2007) (hereafter FGGH and FGP, respectively) explored the dynamic relationship between price and volume, and explained and quantified it by developing separate historical indexes of the movements (percentage price changes) in the reservation prices on the demand (potential buyers) and supply (potential sellers) sides of the asset market. They noted that the demand side reservation prices of potential investors in the market tended to move slightly before, and in a more extreme way, than the supply side reservation prices of the existing property owners. Buyers have a low cost option to postpone or rent whereas sellers have substantial carrying and transactions costs, and this greater flexibility may make buyers more responsive to shocks in the economy, accounting for the typical pro cyclical volume. Given the inertia in the market, the result is strongly pro-cyclical variable liquidity.

This earlier research focused on two key considerations from an investment perspective. First, variable liquidity means that the observed consummated transaction prices are associated with substantially different “ease of trading” at different points in the price cycle. It is relatively easy to sell many properties relatively quickly at the transaction prices observed during the upswing. Prices that characterize the consummated deals during the downturn reflect far fewer sales that (presumably) are associated with longer time on the market or more challenging conditions for selling. Thus, there is an “apples vs oranges” problem in comparing transaction prices across time, and therefore in the interpretation of empirical transaction price indexes. Metrics important for investment analysis such as volatility and covariance are in a sense biased or incomplete if based only on consummated transaction price indications.Footnote 3

Second, given the pro-cyclical relationship (positive correlation) between trading volume and price, and the observed lead/lag relationship between buyers’ and sellers’ reservation prices, FGGH proposed that the demand side effectively drives the market. They therefore proposed that a “constant liquidity value” index that controls for the above-noted apples-vs-oranges problem should be based on the demand-side reservation price index. If one wishes to construct an index of price movements that would preserve constant liquidity in the asset market, then such an index should track the demand side reservation price movements. It is to the buyers that sellers must sell their properties. Buyers bring liquidity (money) into the market.

The analytic construct of the “constant liquidity value” index developed by FGGH essentially collapsed the price and volume dimensions of the asset market onto a single price dimension based on the demand side of the market. The idea is that this construct presents a more complete picture of the asset market, and a useful metric for quantitative comparisons of the private real estate asset class with the more “constantly liquid” public securities asset classes, for purposes of investment analysis.Footnote 4

In the present paper we seek to update and improve the previous construct. The FGGH and FGP methodology was very limited in the type of property asset transaction price data that it could use. It required not only data on transaction prices and turnover ratios, but also rich hedonic data, or else high quality and consistent contemporaneous appraised values, of all the properties in the relevant population. The empirical analysis could only focus at the national aggregate level, and even so with a fair amount of noise in the resulting historical indexes.

Furthermore, there is no “iron law” that requires buyers always to lead sellers in the property asset markets. We need not always observe pro-cyclical variable liquidity. There are alternative market behaviors in which, effectively, sellers drive the market price changes, causing volume and price to move in opposite directions. For example, “sell-off” behavior is not uncommon in the stock market. It is characterized by rising volume associated with falling prices.Footnote 5

The other type of alternative liquidity dynamic in which sellers drive the pricing is characterized by falling liquidity while prices are rising, just the opposite of sell-off behavior. We will refer to falling liquidity and rising prices as “anomalous” liquidity dynamics (or simply as, “the anomaly”, which we sometimes note in the history of property asset markets). In anomalous liquidity, the supply side of the market drives prices up by pulling back on the supply of properties for sale as sellers raise their reservation prices. Although the supply side is in that sense in “the drivers seat”, anomalous liquidity could still be caused by the lead/lag relationship of buyers (potential investors) moving ahead of sellers (existing property owners). Buyers are still driving the liquidity dimension of the market.

Suppose that at the quarterly frequency buyers tend to lead sellers (in reservation price changes), and that there is inertia especially in sellers’ reservation prices (often referred to as “sticky prices”).Footnote 6 Now consider what happens after a recovery or a boom has driven up prices. Suppose the buy-side pauses, buyers’ reservation prices grow less fast or start to fall, but sellers’ reservation prices still have strong upward momentum. If sellers’ reservation prices keep growing sufficiently to push the equilibrium price higher, then we would observe rising prices and falling volume: “the anomaly”.

This suggests that the anomaly will tend to occur when and where prices are high, relative to the past, or relative to other markets. In such circumstances potential buyers may tend to become “exhausted”, wary or cautious because of the high prices. But property owners are still running up their reservation prices based on recent past history.

The anomaly would therefore tend to signal either an imminent downturn in market prices, or else at least a flattening of the past upward growth trend (a pause in the boom). However, such prediction would not be guaranteed to be fulfilled. There could be “false positives”, occurrences of the anomaly that are not followed by flat or down markets. Potential buyers might change their minds, perhaps in response to good news, and quickly resume an upward trajectory in their reservation prices sufficient to resume volume growth and keep equilibrium prices rising.

How prevalent are such anomalous market conditions, and how often do they signal an imminent downturn? This is one question we shall explore in this paper.

While the above described conceptual exploration is of great interest in advancing our understanding of real estate markets, the core and substance of the present paper is to update and enhance the FGGH methodology. We develop a much more sophisticated version of the demand and supply indexes developed in FGP, and then examine some implications of the resulting empirical findings.Footnote 7

Fundamentally, the supply and demand reservation price indexing methodology is based on the fact that both transaction prices and volume in the asset market reflect the underlying reservation prices on the two sides of the market. In essence, volume is a function of the difference of buyers’ minus sellers’ reservation prices (higher buyer and lower seller reservation prices lead to more trading, and vice versa), while prices in consummated deals are a function of the sum of buyers’ and sellers’ reservation prices (divided by 2 to strike a deal at the midpoint). This difference in how the two sides of the market are reflected in volume and price allows us to separately quantify changes in the two underlying phenomena: buyers’ and sellers’ reservation prices.

As noted, in the FGGH framework, the demand side reservation price index is taken as a “constant-liquidity” value index for the asset market. But the supply side reservation price index is also of interest in its own right. It reveals sentiment among property owners. During periods of uncertainty, both rational search theory and behavioral economic theory predict that property owners would tend to react conservatively, holding back from selling into a down market. The supply side index would reveal this phenomenon as a rise in sellers’ reservation prices (or at least, a “stickiness” in reducing their prices compared to buyers).

In the present study we extend the FGGH and FGP methodology to a repeat sales indexing framework. This enables us to develop demand and supply reservation price indexes for a much larger and broader population of properties that need not be appraised and need not have rich hedonic data. We apply our methodology to the Real Capital Analytics Inc (RCA) property transaction database. This database captures approximately 90 percent of all commercial property transactions in the US over $2,500,000 in value.

The main benefit of using the repeat sales methodology is that it takes care of all unobserved heterogeneity that is constant over time (Bailey et al. 1963), which as noted is a particularly important consideration in commercial real estate. In order to apply the FGGH method in a repeat sales framework, we adapt the sample selection methodology for repeat sales models developed earlier by Gatzlaff and Haurin (1997). Another key innovation in our methodology is to use a Bayesian, structural time series model for index estimation, building on the work of Francke (2010) and Francke and van de Minne (2017). These enhancements allow us to estimate supply and demand indexes at a much more granular level, in part because they allow us to use the much larger RCA database. As a result, we are able to estimate reliable, robust supply and demand indexes at the metropolitan level, for a number of major metros in the U.S.

In this study, we construct quarterly supply and demand indexes for every major metropolitan area in the United States from 2005Q1–2018Q2. Indexes of seven large metropolitan areas are published and updated regularly on the website of the MIT Center for Real Estate Price Dynamics Platform.Footnote 8 Indexes of other metropolitan areas are available upon request. Our historical period includes the Global Financial Crisis (GFC), which had not yet occurred at the time when FGGH and FGP published their work. The GFC is a particularly interesting period for observing the behavior of the two sides of the market, how the demand collapsed first, while property owners behaved much more conservative and held on to higher reservation prices.

In this paper we will present indexes of eight large metropolitan areas for which we have sufficient data to avoid any issues of excess noisiness in the indexes. However, for ease of presentation, we will focus mostly on the results for two representative metros: New York City and Phoenix. These two provide a fascinating “tale of two cities”, as they represent very different underlying urban form and space markets, and displayed interestingly different responses during the GFC. New York is a high price, land supply constrained market with high historical price growth, typical of so-called “first tier” (or “gateway”) asset markets. Phoenix is characterized by sprawl and high supply elasticity in the space market, and is a “secondary” market in the institutional real estate investment industry.

Our results show that the demand indexes in both cities went down a full year earlier than the supply indexes during the Crisis. In Phoenix, the demand index also went up first after the trough of the crisis. In New York, supply and demand bounced back up together. In New York, property owners’ reservation prices hardly dropped even during the worst of the crisis, suggesting an impressive confidence in the NYC real estate market on the part of property owners in view of a financial crisis that hit New York particularly hard. The gap between demand and supply price movements was much greater in Phoenix than in New York, resulting in a much greater greater loss of liquidity in the Phoenix market.

The remainder of this paper is organized as follows. “Reservation Prices and Liquidity” describes our methodology for constructing demand and supply reservation price indexes. “Data” describes the data used in our empirical study. “Results” presents our empirical results. Finally, “Conclusions” concludes.

Reservation Prices and Liquidity

First, we discuss the theory of demand and supply in real estate in “Model”. Our methodology also follows from this. “Estimation of Supply and Demand Indexes” gives the estimation procedures.

Model

The setup of the model is similar to that in FGGH: Heterogeneous properties are traded among heterogeneous agents in a double-sided search market. Both buyers and sellers set their reservation prices based on property characteristics and the market situation:

Here RP is the reservation price and subscripts i and t denote the property and time period, respectively. Superscripts b and s represent buyers and sellers. X is a property-specific 1 × K vector of property characteristics and α is the corresponding K × 1 coefficient vector, and εb, εs, are independent normally distributed error terms with mean zero. \({\beta _{t}^{b}}\) and \({\beta _{t}^{s}}\) are common trends across the reservation prices of all buyers and sellers, respectively. These reflect the market-wide movements of buyers and sellers that we are interested in.

In a search market, we observe a transaction if \(RP_{i,t}^{b} \geq RP_{i,t}^{s}\). The frequency distributions of reservation prices of buyers and sellers are displayed in Fig. 1. The shaded area is the intersection between the distributions and depicts transaction volume (a larger area reflects more transactions). The outcome of the transaction price Pi,t depends on both the sellers’ and buyers’ bargaining power. We follow Wheaton (1990) and FGGH by assuming that the transaction price is the midpoint between the buyer’ and sellers’ reservation price.Footnote 9 The average midpoint price that we observe in the market as of a given time is denoted as P0 in Fig. 1. In a booming period, the distribution of the reservation price of buyers moves to the right.Footnote 10 This movement results in more transactions and a higher observed average midpoint price, denoted by P1. Finally, in a bust, buyers move their reservation prices to the left. The intersection area will be smaller which reflects a lower transaction volume and the observed midpoint price will move down to P2. For illustration purposes, these figures are presented in price levels. Usually, as in price indexes, we track changes in these midpoint prices and the index is calibrated at a given starting value (e.g. 100 as we do in this paper).

Buyers’ and sellers’ reservation price distributions at different points in the cycle consistent with pro-cyclical liquidity (buyers driving market price movements)

By estimating a normal hedonic or repeat sales regression model we are able to track changes in the average midpoint price per time period: \(\beta _{t}=\frac {1}{2}({\beta _{t}^{b}}+{\beta _{t}^{s}})\), other coefficients \(\alpha =\frac {1}{2}(\alpha ^{b}+\alpha ^{s})\), and residuals \(\varepsilon _{i,t}=\frac {1}{2}(\varepsilon _{i,t}^{b}+\varepsilon _{i,t}^{s})\):

Let \(S_{i,t}^{*}=RP_{i,t}^{b}-RP_{i,t}^{s}\) and substitute (1) and (2) to obtain:

Note that \(S_{i,t}^{*}\) is latent, instead we observe Si,t = 1 if a transaction is consummated. That is, we only observe a sale (Si,t = 1) when \(\textit {RP}_{i,t}^{b} \geq RP_{i,t}^{s}.\)

Let \(\gamma _{t}={\beta _{t}^{b}}-{\beta _{t}^{s}}\), ωj = αb − αs, and \(\eta _{i,t}=\varepsilon _{i,t}^{b}-\varepsilon _{i,t}^{s}\). The probability of sale can be quantified by estimating the following probit model:

here Φ is the cumulative density function (CDF) of the normal distribution. Note that S includes both a subscript i (property) and t (time period): A property is “tracked” over time. Si,t takes the value 1 when the property is sold (once, twice etc.), and 0 when it is not sold in a given period. The γt reflects the shift in the probability of sale in a given time period. Following FGGH, the inverse Mills ratio (IMR, λi,t) is calculated from the probit results. The probit estimation only yields the coefficients up to an estimated scale factor, σ:Footnote 11

Deviating from FGGH, we estimate the transaction price model only on repeat sales. This has the advantage that we can take care of all unobserved heterogeneity that is fixed over time, which is of importance in the heterogeneous commercial real estate market. It does require the assumption that the property remains unchanged between the two sales. Although we can never be completely sure, we are able to observe whether the property is bought for redevelopments. If this is the case, we discard the property (see “Data”).

It also requires some adjustments to the FGGH method. In the next steps, we will discuss these adjustments. We start with the selection corrected repeat sales model of Gatzlaff and Haurin (1997, henceforth GH). The main goal of GH is to correct for the selection bias of second sales versus first sales. The main aim of our set-up is to correct for the bias of sales (either first or multiple) versus no sales. However, with some adjustments we can still apply the GH-model. The two equations for the first and repeat sale conditional on the sale being observed are:

Here, fir and sec denote the time of first and second sale, respectively. Subscripts fir and sec can take any time-period t. In the remainder of the paper, subscripts fir and sec explicitly refer to the first and second sale, whereas t refers to any time period (i.e. quarters) within the sample and is irrespective of the first or second sale. Further, P denotes the (log) transaction price. Note that the equation includes two selection correction variables: λi,fir and λi,sec. These are the IMRs for the first and second sale, respectively. In GH, where the goal was to correct for a repeat sales correction bias, these are derived by estimating a bivariate probit on the probability of a single sale on the one hand and the probability (conditional on the first sale) of a repeat sale on the other hand. Here, were are not interested in correcting for this selection bias, but we simply want to calculate the development of the probability of sale over time, hence we estimate a normal probit as given by Eq. 6. The IMR (λi,t) for properties that are sold in a given time period, is calculated as the fraction of the probability density and the cumulative density of a given observation in the probit:Footnote 12

Here, Φ is the CDF of the normal distribution, ϕ the probability density function (PDF) of the normal distribution, subscripts i and t denote property and time period, respectively.

The σ coefficients in Eqs. 10 and 12 are covariances between the errors terms of the selection and sale equations. More specifically, the covariance matrix of the four error terms (ηi,fir, ηi,sec, εi,fir, εi,sec) is defined as:

Subtracting (10) from (12) and adding disturbance terms results in the repeat sales equation of GH:

By taking the exponential of βt, we get a price index. The correlations that appear in Eq. 15 are σ1,3, which is the covariance between the error terms of the first selection equation (ηi,fir) and the first sale equation (εi,fir), σ1,4, which is the covariance between the error terms of the first selection equation (ηi,fir) and the second sale equation (εi,sec), σ2,3, which is the covariance between the error terms of the second selection equation (ηi,sec) and the first sale equation (εi,fir), and σ2,4, which is the covariance between the error terms of the second selection equation (ηi,sec) and the second sale equation (εi,sec).

In order to estimate constant-liquidity (buyers’ reservation price) indexes (per FGGH), it is necessary to include a time trend in the probit (e.g. by including time fixed effects in the probit). It is not clear whether this should be included in the probit on first sales, on repeat sales, or on both (the original GH model does not include any time fixed effects). Furthermore, it is not straightforward how to derive \(\hat {\sigma }\) (see Eq. 21) and which \(\hat {\gamma _{t}}\) (i.e. the time fixed effects of the first or repeat sale in, for example, a bivariate probit) should be used to calculate the supply and demand indexes in a later stage (see Eqs. 23 and 24). Therefore, our proposition is to estimate the following repeat sales equation:

This does impose restrictions on the coefficients (σ1,4, σ1,3, σ2,4, and σ2,3) on the selection correction variables (λi,fir and λi,sec). More specifically, the restrictions are (i) σ2,3 = σ1,4 = 0 and (ii) σ2,4 = σ1,3 = σε,η. Restriction (i) implies that there is no correlation between the error terms of the first selection (sale) equation and the second sale (selection) equation. This means that the reason to buy cannot be related to the realized gain or loss in the future. Therefore, it is important to remove properties built for redevelopment from the data. Restriction (ii) implies that the correlation between the first sale and the first selection is equal to the correlation of the second sale and the second selection. This means that the decision to buy or sell must be “normal”. For example, if a the second sale was in distress, and the first one is not, this assumption is violated. Therefore, properties sold in distress need to be removed.

In GH, the selection equations were estimated in a bivariate probit and these assumptions were not necessary. Since the selectivity in a repeat sales model (i.e. the selection effects of second sales versus single sales) was the main goal of GH, these correlations needed to be explicitly modeled. In our set-up, we are merely interested in the selection effect of no sale versus a sale, either a first or multiple. Hence, these assumptions are not very restrictive in our case. Moreover, these assumptions are also implicitly made for observations that are sold more than once when deriving supply and demand indexes in the widely applied hedonic framework of FGGH. Finally, as mentioned, one can account partly for these factors by applying the appropriate data filters. We do acknowledge that the restrictions on σ could lead to small biases and also acknowledge the potential of loosening these restrictions in future research. For example, removing properties sold in distress, might results in a positive index bias during the GFC. Another topic worthwhile exploring would be to examine the correlation between the first selection equation and the second sale equation. This could give interesting insights in, for example, speculation. Likewise, the correlation between the first sale equation and second selection equation could provide interesting insights in anchoring.Footnote 13

In order to apply the method in thin markets, the time trend in the repeat sales equation is modeled as a random walk with an additional autoregressive (AR) parameter on the returns. As discussed in more depth in Van de Minne et al. (2020) an AR representation (inertia) is inherent to the price formation process in the real estate market. We therefore specify the returns in the state equation as an AR process with parameter (ρ):

The identifiability of the “probit σ” for a hedonic framework is discussed in the Appendix of FGGH and will also be briefly discussed here. Let \({\sigma _{s}^{2}}=\text {Var}(\varepsilon _{i,t}^{s})\), \({\sigma _{b}^{2}}=\text {Var}(\varepsilon _{i,t}^{b})\), and \(\sigma _{s,b}=\text {Cov}(\varepsilon _{i,t}^{s},\varepsilon _{i,t}^{b})\). Note that these are the (co)variances of Eqs. 1 and 2. The scale parameter, the “probit σ”, is equal to \(\sigma ^{2}={\sigma _{s}^{2}}+{\sigma _{b}^{2}}-2\sigma _{s,b}\), which is what we need to solve for. Following FGGH, our model assumes constant variance of time and random matching between buyers and sellers, hence we can assume Cov\((\varepsilon _{i,t}^{b},\varepsilon _{i,t}^{s})=0\). This simplifies the expression: \(\sigma ^{2}={\sigma _{s}^{2}}+{\sigma _{b}^{2}}\). The conditional expected variance of the pricing errors (\(\varepsilon _{i,t}^{2}\)) in a hedonic model follows from the known relations for the moments of the truncated bivariate normal distribution (Johnson and Kotz 1972):

As expectation for the squared errors we plug in the squared residuals of the repeat sales model \(\hat {\varepsilon }_{i,t}^{2}\). Note that FGGH use the sum of squared residuals (SSR) from a hedonic model. However, the SSR from a hedonic model with pair fixed effects is equivalent to the SSR of our repeat sales model.Footnote 14\(\hat {\sigma }_{\varepsilon ,\eta }^{2}\) is the square of the estimated coefficient on the IMR, \(\hat {\gamma }_{t}+X_{i}\hat {\omega }\) is the linear prediction from the probit model, and \(\hat {\lambda }_{i,t}\) is the estimated IMR.Footnote 15 To solve for \(\sigma _{\varepsilon }^{2}\) we further plug in the estimates of the probit (\(\hat {\gamma }_{t}, \hat {\omega }\), and \(\hat {\lambda }_{i,t}\)) and repeat sales estimates (\(\hat {\varepsilon }_{i,t}^{2}\) and \(\hat {\sigma }_{\varepsilon ,\eta }^{2}\)):

Here N is the number of observations from a hedonic model, so in our case that would be the number of repeat sales times 2.Footnote 16 Also note that we stack the repeat sales data: every pair gets two observations (buy and sell). In this case we also use the level of the IMR of the first and second sale instead of the difference.

In order to derive the buyers’ and sellers’ reservation price indexes, we combine the probit sale probability and repeat sales price model results to obtain the demand/supply indexes (FGGH). As estimated values we have: \(\hat {\gamma _{t}}=(\hat {{\beta _{t}^{b}}}-\hat {{\beta _{t}^{s}}})/\hat {\sigma }\) (from Eq. 7) and \(\hat {\beta _{t}}=\frac {1}{2}(\hat {{\beta _{t}^{b}}}+\hat {{\beta _{t}^{s}}})\) (from Eq. 3) \(\rightarrow \hat {{\beta _{t}^{s}}}=2\hat {\beta _{t}}-\hat {{\beta _{t}^{b}}}\). Substituting the latter in the former, we get the buyers’ reservation (constant-liquidity) price index:

Further substitution yields the sellers’ reservation price index:Footnote 17

The demand and supply reservation price indexes defined in this paper suggest a way to explicitly quantify liquidity in the property market, and thereby to track liquidity dynamics. Recall our earlier discussion on the pro-cyclical nature of liquidity in levels. As the frequency distribution of the buyers’ reservation prices (on the left) overlaps more with that of the sellers (on the right), there is greater trading volume, hence, greater liquidity (Fig. 1). More buyers have reservation prices greater than those of sellers. In our methodology we track changes in the degree of overlap over time. The (changes in) the degree of overlap is a function of the central tendencies in the two distributions, the (changes in) positions of the two distributions relative to each other on the horizontal axis. This is formalized in our probit model (6) in which the sale propensity is determined in the aggregate each period by the market sale propensity, γt, which is given by: \(\gamma _{t}={\beta _{t}^{b}}-{\beta _{t}^{s}}\), the buyers’ minus sellers’ reservation price distributions’ central tendencies. In the supply and demand reservation price indexes, this essentially equals the vertical difference of the demand minus the supply index levels in each period.

Thus, we define an intuitive Liquidity Metric in a given market in a given period as the difference of the demand minus supply index level. But we normalize and scale this difference by dividing it by the consummated transaction (midpoint) price index level in that same period. Thus our Liquidity Metric is given by:

Considering that we calibrate all three indexes to have equal average levels across the entire history, this gives the level of the Liquidity Metric an intuitively pleasing interpretation. It is the amount of combined movement up in buyers’ and down in sellers’ reservation prices that would bring the market to its long-run (historical) average liquidity (essentially, trading volume turnover ratio). In the Liquidity Metric the necessary price movements (to bring the market to long-run average liquidity) are expressed in terms of percentage of the current average consummated transaction price level in the market. Essentially, the Liquidity Metric quantifies relative market liquidity in terms of relative price change. Equation 25 makes it clear that liquidity is essentially measured by the probit propensity to sell in the current time period, dimensioned and scaled to the current prevailing price level.

To clarify the Liquidity Metric, consider a simple numerical example. Suppose in a given period in a given asset market the demand index level is 120 and the supply index level is 110. Therefore, by construction, the consummated price index level is 115. The Liquidity Metric would be: (120-110)/115 = 10/115 = 8.7%. The fact that the Liquidity Metric is a positive percentage means that the market is currently at above-average liquidity. The 8.7% specifically means that some combination of a reduction in buyers’ average reservation prices (decrease in demand) and/or an increase in sellers’ average reservation prices (decrease in supply) totaling 8.7% of the current average price level prevailing in the market, would bring liquidity in the market back down to its long-run average. For example, buyers might lower their reservation prices by 5% and sellers might increase their reservation prices by 3.7%, pulling the two sides of the market apart by 8.7% of current average prices.

The Liquidity Metric makes explicit, and quantifies, the type and magnitude of underlying movements on the two sides of the market that fundamentally determine liquidity. It thereby provides a quantitative measure of the “heat” of the market: positive is “hot”, negative is “cold”, and the magnitude of the Liquidity Metric percentage tells “how hot” or “how cold” in terms of current price index levels.

Estimation of Supply and Demand Indexes

We estimate the model in a two-step approach (Heckman 1979), after the estimation we combine the results of the first and second estimation steps. We first estimate probit (6) by maximum likelihood. We subsequently calculate the IMRs of the first and second sales. We then plug in the difference between the IMRs in the repeat sales model as given by Eq. 16. We estimate the repeat sales model in a Bayesian framework similar to the Commercial Property Price Indexes published by RCA (Van de Minne et al. 2020). The difference is that we use normally distributed errors instead of t-distributed errors in order to use the multivariate normality with the probit. Also, we do not allow the signal and noise to vary over time for the sake of simplicity and consistency with the theory.

As explained in Francke and van de Minne (2017), estimating repeat sales models in a structural time series framework, especially with AR components, is very difficult using the Kalman filter. We therefore estimate the model with Markov Chained Monte Carlo simulations. More specifically, we use the No-U-Turn-Sampler (NUTS) to estimate the indexes (Hoffman and Gelman 2014; Carpenter et al. 2016). The repeat sales indexes are estimated over 4 parallel chains with different initial values. We use 6,000 iterations per chain of which 3,000 are warm-up iterations that we discard. Hence, the total sample size is 12,000. Following Van de Minne et al. (2020), we use the \(\hat {R}\) combined with the effective sample size to determine the convergence of the model. We additionally investigate the Monte Carlo error and the Heidelberger-Welch stationarity and halfwidth statistics (Koehler et al. 2009; Heidelberger and Welch 1981).

Finally, we calculate the supply and demand reservation price indexing by combining the probit and repeat sales using Eqs. 23 and 24.

Data

We use transaction data from Real Capital Analytics (RCA) to estimate the indexes between 2005Q1 and 2018Q2. RCA captures more than 90% of the properties with a sale price of $2,500,000 or more.Footnote 18 A high capture rate is fundamentally important for our methodology since the probit results should reflect the probability of sale with respect to the whole population. In general there is no “census” of commercial properties in the U.S., and we don’t have a clearly defined specialized population of properties such as the NCREIF population. Therefore, we need to assume that the RCA database does represent the entire population of interest. In effect, if a property has been sold at least once during 2000-2018, we assume it is in the population of interest, otherwise it is not. We are confident that RCA’s high capture rate combined with the fact that RCA has been recording transactions since 2000 ensures that almost all properties in the investment universe are in our data. Another way of viewing this assumption is that properties that are not in the data after 18 years might never become part of the investment universe that investors are interested in (i.e. properties that trade on a regular basis).Footnote 19

The descriptive statistics for the two metropolitan markets that we will cover in detail (New York and Phoenix) are presented in Table 1. The number of properties is more or less constant in the data, which provides confidence that the capture rate of the data is satisfactory. We are not able to identify whether a property gets demolished. We do observe if a property is bought for the purpose of redevelopment. These properties are removed for the reasons outlined in “Model”. For the same reasons, properties sold in distress are removed.

In the probit equation, we control for property size (in log square feet), property type (Apartment, Hotel, Industrial, Office, Retail, and Other), whether the property is in the Central Business District (CBD), and construction period (< 1920, 1920 − 1945, 1946 − 1989, and ≥ 1990). We also use the construction year to filter out properties that were not yet built. Since properties sometimes transact before the construction has been finished, we include the property in the probit data two years before completion. If the probit model is estimated without property characteristics, this provides comparable results (not shown). In effect, the probit model may be viewed as being akin to a model of market trading volume (turnover ratio) across time, scaled to normal probability and applied at the disaggregate (individual property) level.

We see in the data that in both New York and Phoenix, the crisis is clearly visible in both the number of sales and average transaction price. In 2009 the number of transactions is about 50% lower than in 2008 and 70-80% lower than in 2007. The average property size is more or less equal over the sample. Most properties sold in Phoenix are outside of the CBD, whereas in New York most are within the CBD. Properties in New York are, on average, older than in Phoenix and the average construction year increases somewhat over the sample as newly constructed properties enter the data-set.

As noted, we have selected New York and Phoenix for detailed analysis because of those two cities rather opposite characteristics. New York is an old, high-price, high-density, supply-constrained “monocentric” city, while Phoenix is a young, low-cost, rapidly growing, sprawling “polycentric” city with little supply constraints. Phoenix also has only about one-fourth the sample size for index estimation purposes. In the institutional real estate investment industry, New York is the premier US “first tier” (or “gateway” city or “major” market), attracting large amounts of foreign capital investment, while Phoenix is considered a “secondary” market city that does not attract much foreign investment. By examining these two cities in detail, we will get a good idea how our methodology works in these two extreme examples. It will also be interesting to see how these two very different property investment markets behaved during the history covered by our data, regarding their price and liquidity dynamics. (As noted, the FGGH and FGP approach did not enable application to the individual metropolitan market level.)

Results

As noted before, our estimation procedure consists of multiple steps. First, we estimate the probability of sale by Eq. 6 and calculate the IMR. Second, we estimate a repeat sales model including the difference in the IMR by estimating (16). Finally, we derive the supply and demand reservation price indexes by combining the probit and repeat sales results using Eqs. 23 and 24.

Probability of Sale

The estimates for the probability of sale for the two markets are shown in Table 2. The estimates of the time fixed effects (γt in Eq. 6) are shown in Fig. 2. The magnitude of the coefficients cannot be interpreted directly, but the sign can be interpreted. Furthermore, the relative effects of the categorical variables can be interpreted.Footnote 20

Raw and smoothed/seasonally adjusted estimates of the time fixed effects in the probit equation (γt) for the two markets over 2005Q1 and 2018Q2

In general, larger properties have a somewhat higher probability of sale, although the effect is only marginally significant. In New York, properties located in the CBD sell significantly quicker. With respect to property types, apartments sell the quickest in both markets and “other” (i.e. elderly homes, nursing cares, parking facilities etc.) sell the slowest. Hotel, industrial and office buildings sell roughly at the same speed. The newest buildings (built after 1990) sell the quickest in New York. In Phoenix, the differences between the construction periods is not significant.

The estimates of the time fixed effects are somewhat noisy (Fig. 2). Also, the estimates show a seasonal pattern. Therefore we follow FGP and smooth and seasonally adjust these coefficients. More specifically, we use a local linear trend model with a seasonal factor to efficiently distinguish between signal and noise.

The probability of sale in New York dropped more than 30% by mid 2009 compared to 2007 and recovered gradually to the pre-crisis level between 2010 and 2015. Since 2015, the probability of sale seems to be somewhat decreasing.

The probability of sale in Phoenix decreased by more than 60% during the crisis. The probability of sale increased between 2010 and 2016, but has never recovered fully to the pre-crisis level. Also, starting in 2016 there is a small decrease in the probability of sale in Phoenix (until the last quarter).

It is interesting to note the similarity in the longitudinal profiles of sale probability across the two markets, that is, the high contemporaneous cross-correlation in liquidity. In the real estate investment industry, changes in the flow of capital appear not to discriminate much across metro markets, in the 2005-18 period of history that we cover. Longitudinal changes are much greater than cross-sectional changes, and the longitudinal dynamics are strongly cyclical.Footnote 21 We see the same pattern across all of the metro areas we have examined (see “Measuring Liquidity and the Price-Liquidity Dynamics Anomaly”). It is important to note, however, that this similarity in dynamics does not necessarily imply that the average probability of sale is similar across different markets. The baseline level of sales, for example, could be substantially different.

Repeat Sales Indexes

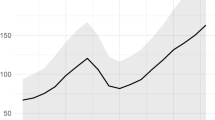

The repeat sales asset price indexes for New York and Phoenix are shown in Fig. 3. These are the consummated transaction price indexes that follow from the estimation of Eq. 16. The indexes are, by construction, on the midpoint between the demand and supply indexes, that is, on the midpoint of the central tendencies of the buyers’ and sellers’ reservation prices. Of course, as with all indexes, they represent only the relative longitudinal changes, benchmarked to an arbitrary value of “100” at the index inception date of 2005Q1.

Repeat sales indexes of commercial real estate in New York and Phoenix between 2005Q1 and 2018Q2

The impact of the GFC on consummated prices is clearly visible in the graph. Prices in New York dropped only about 20% in 2008-10.Footnote 22 New York started recovering in 2010 and the prices surpassed the pre-crisis level in 2013. In contrast, Phoenix crashed farther and recovered much more slowly. Average prices of consummated transactions excluding distressed properties dropped some 40% mostly before 2010, before finally bottoming in 2011. Substantial recovery in Phoenix did not really take off until 2016 when prices increased by almost 25%. But Phoenix price levels at the end of the sample are still lower than the pre-crisis peak.

The price model statistics and the estimate of the coefficient on the difference of the IMR are presented in Table 3. All model statistics are satisfactory, the Monte Carlo error (MC error) is very close to 0 and the effective sample size (Neff) relative to the number of samples is 0.58 and 0.68 for New York and Phoenix, respectively (note that the number of samples is 12,000 for every model). The Heidelberger stationary statistic is equal to 1, indicating that the test is passed by every parameter in the model (a parameter gets the value 1 if the test is passed). The same holds for the Heidelberger halfwidth statistic, which is close to 1. This indicates that the number of chains is high enough. Finally, the \(\hat {R}\) values close to 1 indicate that the models have converged well.

Supply and Demand Indexes

The indexes for demand and supply reservation prices that follow from Eqs. 23 and 24 are shown in Figs. 4 and 5 (mind the difference in scale). Following FGP, the indexes are calibrated to have starting value levels (2005Q1) such that the mean levels of the supply, demand, and consummated price indexes across the entire history are all equal, with the consummated price index arbitrarily set to start at a value of 100.

Supply, demand, and consummated transaction price indexes of the New York City metropolitan area

Supply, demand, and consumated transaction price indexes of the Phoenix metropolitan area

In both markets, the demand-side (or constant-liquidity) indexes seem to move quicker and in a more extreme manner than the supply-side indexes. The demand-side indexes (buyers’ reservation prices) decrease about a year before the supply-side indexes (sellers’ reservation prices) during the Financial Crisis. The recovery also happens earlier among the potential buyers, especially in Phoenix. The demand-side indexes also lead the consummated price indexes in time. Buyers’ reservation price indexes therefore serve effectively as leading indicators for market transaction price indexes. But clearly, the demand-side indexes lead the supply-side reservation price indexes even more. Indeed, this analysis makes explicity how the reason for buyers’ reservation prices leading consummated transaction prices is that the property owners (potential sellers) on the supply side of the market are more sluggish at adjusting their reservation prices. Property owners tend to exhibit classical “sticky prices” in terms of their reservation prices.

A Granger causality analysis confirms the lead/lag relationship: Changes in the demand-side indexes Granger cause changes in the consummated price indexes in both markets. The lead/lag relationship is of course even stronger between potential buyers and potential sellers (property owners).Footnote 23

In New York, suppliers’ reservation prices remained surprisingly constant through the GFC, which suggests that property owners remained very confident about the New York commercial real estate market.Footnote 24 The difference between peak and trough reservation prices on the supply side was only 16%, compared to 29% on the demand side. After the crisis, supply and demand show a joint recovery in New York. In Phoenix, suppliers’ reservation prices remained sluggish through as late as 2015Q4. The difference between peak and trough is also much larger in Phoenix: Sellers’ reservation prices went down by more than 30% and buyers’ reservation went down by 47% (Fig. 6).

Magnitude of the 2008-09 crash (upper) and the 2010-18 recovery (lower). Markets are ranked by order of price crash magnitude

Figures 13, 14, 15, 16, 17, and 18 in the Appendix plot demand and supply indexes for six other markets, including all five of the other so-called “Major Markets” in the U.S., as well as Seattle (which is a strong secondary market). All of these other markets show very similar features to what we have described in common between New York and Phoenix. In general, demand moves sooner or quicker and more extremely than supply. This is also visible in the crash and recovery magnitudes (Fig. 6). We observe the biggest drops in demand in Phoenix and Chicago. The strongest recovery in demand is visible in San Francisco and New York, which were not the markets with the biggest drop in demand.

Measuring Liquidity and the Price-Liquidity Dynamics Anomaly

The Liquidity Metric as defined in Eq. 25 is a convenient construct for exploring the nature of liquidity dynamics in commercial property investment markets, including the relationship between price and liquidity over time. Recall that the conventional wisdom has been that property asset markets are characterized by pro-cyclical variable liquidity, that is, price and volume moving together. We noted in “Introduction and Motivation” this type of relationship can be viewed as buyers (the demand side of the market) driving the price movements. We confirmed in “Supply and Demand Indexes” that for the two very different metros of New York and Phoenix the demand indexes do indeed tend to lead the supply indexes in time, and to move more extremely. This is consistent with volume and price moving together, and with volume tending to lead price. Let us now explore this question in more depth.

Figure 7 shows the FGP-based supply and demand indexes that were published by the MIT Center for Real Estate until 2011, based on the NCREIF population of properties. The indexes are quarterly from 1984 to 2011, and are at the national aggregate (“all property”) level. The Figure shows the demand index in red, the supply index in green, and the consummated transaction price index in black, all keyed to the left-hand vertical axis. The price index is calibrated to an inception value of 100 in 1984, while the supply and demand indexes are each calibrated to have inception values that give all three indexes the same long-run average value level across the entire history. The yellow line traces the Liquidity Metric, as we have defined in “Model”, keyed to the right-hand vertical axis.Footnote 25

U.S. aggregate supply, demand, and consummated transaction price indexes of FGP based on NCREIF data (left axis) and liquidity metric based on the difference between demand and supply. The shaded areas include periods where prices were increasing and liquidity was decreasing, e.g. “The Anomaly”

These older (FGP methodology, NCREIF data) supply and demand indexes cover a much longer period of history than we can study with the RCA database, but they stop in 2011 (and as noted, the NCREIF population of properties is rather specialized, and much smaller and narrower than the RCA data). The history in Fig. 7 includes two major downturns: One at the end of the 1980s/early-90s and the more recent GFC downturn of 2008-09. Visually, it is apparent in the Figure that demand tends to slightly lead supply (and therefore, demand leads consummated transaction prices). We also see that, indeed, in general pro-cyclical variable liquidity holds. Usually price and liquidity move together. When the Liquidity Metric (yellow line) is positive in levels (hence liquidity is above its long-run equilibrium), prices are generally rising, and rising more rapidly when the Liquidity Metric is greater in magnitude. The market price downturns are associated with negative values in the Liquidity Metric (in levels), and are most sharply decreasing in the case of the GFC.

We can quantify the historical manifestation of the conventionally expected pro-cyclical price/volume relationship in the quarterly 1984-2011 history shown in the Figure. In 82 of the 108 calendar quarters in the history, price and liquidity are moving together (either both increasing or both decreasing). The remaining 26 quarters display the “anomalous” price/liquidity relationship we introduced in “Introduction and Motivation”, in which price is rising while liquidity is falling. These anomalous time periods are indicated by the gray shaded vertical columns in the Figure.Footnote 26

It is interesting to note that the price-liquidity dynamics anomaly tends to occur just before a major downturn or flattening of a previous upward trend in the market. This would make sense based on the demand/supply lead/lag behavior noted previously, as described in “Introduction and Motivation”. However, it is also important to note that, at least with the older, more noisy indexes, the anomaly does not always indicate a subsequent downturn or even a flattening. There can be “false positives”, as suggested in our discussion in “Introduction and Motivation”.

Figure 8 shows how the underlying reservation price movements on the two sides of the market would cause the price-liquidity anomaly. Essentially, declining volume with rising consummated transaction prices must be associated with a pull-back in supply relative to demand, sellers raising their reservation prices more than buyers (or perhaps even with buyers lowering their RP s, pulling back on demand, but not enough to offset the price effect of the sellers’ behavior). As noted, such behavior could be associated with buyers becoming “exhausted” or wary about how high prices have become, while sellers are still wanting to reflect recent strong upward momentum in the market (or are simply pulling back out of conservatism in the face of uncertainty). The point is that the anomaly is probably like a “yellow warning light” flashing. The market may not be headed for a correction, but it well could be.

Buyers’ and sellers’ reservation price distributions consistent with increasing pricing and declining volume, e.g. the anomaly

The next step is to look at how the Liquidity Metric and the price-liquidity anomaly play out more recently in our enhanced methodology, larger transaction population example metros of New York and Phoenix. Figures 9 and 10 show the supply, demand, and price indexes, and the Liquidity Metric and the anomaly, for New York and Phoenix respectively, for our quarterly history covering 2005-18. The conventions in the graphs are the same is before (red = demand, green = supply, black = price, yellow = Liquidity Metric, shaded bars are quarters of the anomaly). In both metros, the anomaly occurred just prior to the GFC crash in the markets, and has not occurred again since, until 2016, when it has occurred again in both markets.

Supply, demand, and consummated transaction price indexes of the New York City metropolitan area (left axis) and liquidity metric based on the difference between demand and supply. The shaded areas include periods where prices were increasing and liquidity was decreasing, e.g. “The Anomaly”

Supply, demand, and consummated transaction price indexes of the Phoenix metropolitan area (left axis) and liquidity metric based on the difference between demand and supply. The shaded areas include periods where prices were increasing and liquidity was decreasing, e.g. “The Anomaly”

In the Appendix at the end of this paper, we similarly show the results for six other markets, all five other so-called “Major Metros”, plus Seattle.Footnote 27 In general, the results in these other markets are similar to what we see in New York and Phoenix. The anomaly occurred just before the GFC crash, and has only occurred again since 2016. (Seattle is an exception to the latter point. See Figs. 13, 14, 15, 16, 17, and 18 in the Appendix.)

Finally, before concluding, it is of interest to highlight another aspect of our findings. Across all of the metro areas that we have examined in depth, Fig. 11 depicts the history of the Liquidity Metric in each market, while Fig. 12 depicts the corresponding price indexes. Notice how similar the Liquidity Metric values are across all the metros, across the history, much more similar than are the price indexes. This reinforces a point we noted earlier at the end of “Probability of Sale” in our discussion of Fig. 2. Liquidity (changes) reflects trading volume (changes), which is essentially determined by (changes in) capital flows, which are national or even global in nature. Asset prices (changes) are more complex. While they do too reflect (changes in) capital flows (hence the generally pro-cyclical volume/price relationship, both in levels and returns), they also reflect other factors that are more local or unique to a specific metro area. Most notable among the latter is the space market, which reflects unique features of the economic base of the metro area and the real estate development climate and physical and political constraints in each market. It seems that capital tends to flow much more uniformly, relative to all major investment markets in the U.S., while equilibrium prices reflect the reality and the expectations surrounding real estate operating cash flows that vary more across metros.

Liquidity Metric in eight metropolitan areas in the US

consummated transaction price indexes in eight metropolitan areas in the US

Conclusions

In this paper we extend the constant-liquidity index methodology introduced by (Fisher et al. 2003). Conceptually, we explore the implications of supply-side and demand-side reservation price indexing for studying the dynamics of liquidity in commercial investment property markets. Methodologically, we introduce two main innovations: (i) We cast the method in a repeat sales framework, and (ii) we estimate the model in a structural time series format. We also provide a new perspective on defining the subject “population” of properties, as all properties that have ever been sold in a comprehensive, high capture rate transaction price database. As a result, we can disentangle reservation prices of buyers and sellers for commercial real estate at the city level without needing a substantial set of property characteristics. We apply our model using data provided by RCA. RCA tracks properties over $2,500,000, or the typical institutional / large private investor space. In this paper we focus in depth on two cities of very different urban characteristics: New York and Phoenix. We also provide results for six other major metropolitan areas.

Tracking demand and supply separately not only gives us more insight into the investment real estate market, it can also be used as a predictive model. Indeed, supply tends to move slower than demand, perhaps due to anchoring and loss aversion (Anenberg 2011; Bokhari and Geltner 2011; Clapp et al. 2018) and issues related to mortgage debt (Genesove and Mayer 2001). The consummated transaction price index that is usually estimated in a repeat sales framework also lags behind the reservation prices of buyers. We find that in both New York and Phoenix demand dropped a full year prior to supply during the crisis. We further find that buyers’ reservation prices went down by 29% and 46% in New York and Phoenix, respectively. In New York, reservation prices of sellers only dropped moderately by 17% compared to the large drop in Phoenix of 40%.

Finally, we define and explore a Liquidity Metric based on the difference between buyers’ minus sellers’ reservation price indexes. We document that, while markets normally display pro-cyclical variable liquidity (price and volume moving together), about 25% of the calendar quarters exhibit what we dub “anomalous” price-liquidity dynamics, with liquidity falling while prices are still rising. The anomaly often, though not always, is a harbinger of a downward turn in the market pricing. Recently, we see this anomaly in all but one of the metro areas we have examined. Reservation prices of sellers are increasing more than reservation prices of buyers. This may suggest that buyers have become “exhausted” or wary of the recent price levels in these major markets.

Notes

Leon Walras (1834-1910): “Elements d’economie politique pure”, Paris, 1874.

See for example Chapter 7 in: Geltner et al. (2014).

Appraisal based indicators would be similarly incomplete, as they are based on observed transaction prices.

Traders in the stock market may not view that market as being “constantly liquid”. But compared to the frictions and time required for trading real assets, from the perspective of private real estate markets, effectively the stock market is “always liquid”.

Such behavior is much less common in real estate markets. However, a famous instance of sell-off behavior in real estate was the neighborhood “tipping point” phenomenon of housing market racial segregation in U.S. cities in the 1950s and 60s.

Goetzmann and Peng (2006) present a slightly different approach to develop supply and demand indexes that provides similar results. The FGP methodology was employed by the MIT Center for Real Estate to produce and publish during 2006-2011 a quarterly-updated set of demand and supply indexes based on the National Council of Real Estate Investment Fiduciaries (NCREIF) population of properties.

The markets are Boston (BOS), Chicago (CHI), Los Angeles (LA), New York City (NYC), San Francisco (SF), Seattle (SEA), and Washington D.C. (DC). The website URL is http://pricedynamicsplatform.mit.edu/.

We will not pursue the relationship between bargaining power, list prices, and information asymmetries here since this would result in difficulties of identification of the reservation price changes. See Carrillo (2013) and Han and Strange (2015) for a discussion on bargaining power and Guren (2018) on the role of asking prices in search markets. Suffice it to say that buyers and sellers consider the current market conditions when deciding on their reservation prices. For a discussion on the uncertainty of the sellers’ information in search models, see Anenberg (2016).

The distribution of sellers might also move, but it is generally accepted that buyers respond more quickly than sellers, see Genesove and Han (2012), Carrillo et al. (2015), and Van Dijk and Francke (2018). So in our case the buyer reservation prices move more to the right than seller reservation prices. As noted in FGGH, this is the criterion that determines pro-cyclical variable liquidity (price and volume moving together), in effect, buyers driving the price movements.

The conditions for the identifiability of this “probit σ” in our context are discussed later on.

For properties that are not sold in a given time period, the IMR would be calculated as the fraction of the probability density and (1-cumulative density). We don’t need this intermediate outcome for further derivations and therefore will refrain from a discussion on this.

Anchoring should now be captured by the supply and demand indexes. Take the example of a bust, supply will decrease by less compared to the case of no anchoring, hence the supply and demand indexes will be further apart and liquidity will go down by more. In case of speculation, this should go the other way around: a relatively modest drop in demand in a bust compared to the case without speculation and vice versa in a boom.

The SSR and MSE are equivalent, but the individual squared errors are different. However, since we are eventually interested in the MSE, we can safely assume \(E(\varepsilon _{i,t}^{2}|S_{i,t}=1)=\frac {1}{2}E(\varepsilon _{i,fir}^{2}|S_{i,t}=1)+\frac {1}{2}E(\varepsilon _{i,sec}^{2}|S_{i,t}=1)\), where fir is the first sale and sec is the second sale.

Note that we estimate the coefficient on the difference of the IMR. However, the restriction σ24 = σ13 = σε,η implies that the coefficient on the difference (σε,η) is the same as the coefficient on the level of the IMR of the first and second sale.

When a property has more than 2 sales, for example 3 sales, this would result in 4 observations in the hedonic model with 2 pair fixed effects. Hence the second sale enters twice.

In case one would want to include bargaining power in the model, the price index βt and other coefficients α, could be replaced by weighted averages of the buyers’ and sellers’ valuations: \(\beta _{t}=w_{t}{\beta _{t}^{b}}+(1-w_{t}){\beta _{t}^{s}}\) and α = wtαb + (1 − wt)αs. Here, wt could be the (time-varying) bargaining power of buyers. In that case the buyers’ reservation price index would be \(\hat {{\beta _{t}^{b}}}=\hat {\beta _{t}}+w_{t}\hat {\sigma }\hat {\gamma _{t}}\). We will leave such an extension for further research and assume that \(w_{t}=\frac {1}{2}\).

Once a property is captured in the database, it remains in the data, even if a subsequent sale price is below $2,500,000.

Many owner-occupied properties, so-called “corporate real estate”, are effectively not in the investible universe.

Another option would be to present marginal effects. The supply and demand indexes, however, require the “raw” coefficients. Therefore, we present the coefficients instead.

The correlation between the probability of sale in New York and Phoenix is 0.92 in (index) levels and 0.66 in first differences.

Recall, however, that this without including sales of distressed properties.

Both Granger causality analyses are significant at the 1% level and are based on a VAR model with 4 lags estimated separately for each market.

Note again that this is apart from distressed properties.

The original FGP methodology, NCREIF based indexes published by the MIT/CRE are somewhat noisy. For our purposes here we have smoothed the indexes using a five-quarter centered moving average. This does not induce a lag bias, but we do lose both the first and last two quarters of the history.

Because transaction volume can be somewhat noisy at the quarterly frequency, we only consider the price-liquidity dynamic to be “anomalous” if it continues for at least two consecutive quarters. Also note that while the anomalous periods are characterized by sellers driving the price movement, this is not inconsistent with the earlier fundamental point that buyers drive liquidity. Indeed, the anomalous periods are characterized by declining liquidity precisely because fewer buyers are willing to pay the prices sellers are wanting.

These six metros have sufficient data to yield very robust and reliable results with minimal noise.

References

Anenberg, E. (2011). Loss aversion, equity constraints and seller behavior in the real estate market. Regional Science and Urban Economics, 41(1), 67–76.

Anenberg, E. (2016). Information frictions and housing market dynamics. International Economic Review, 57(4), 1449–1479.

Bailey, M.J., Muth, R.F., & Nourse, H.O. (1963). A regression method for real estate price index construction. Journal of the American Statistical Association, 58, 933–942.

Bokhari, S., & Geltner, D. (2011). Loss aversion and anchoring in commercial real estate pricing: Empirical evidence and price index implications. Real Estate Economics, 39(4), 635–670.

Carpenter, B., Gelman, A., Hoffman, M., Lee, D., Goodrich, B., Betancourt, M., Brubaker, M.A., Guo, J., Li, P., & Riddell, A. (2016). Stan: a probabilistic programming language. Journal of Statistical Software, 20, 1–43.

Carrillo, P., De Wit, E., & Larson, W. (2015). Can tightness in the housing market help predict subsequent home price appreciation? Real Estate Economics, 43(3), 609–651.

Carrillo, P.E. (2013). To sell or not to sell: Measuring the heat of the housing market. Real Estate Economics, 41(2), 310–346.

Clapp, J.M., Lu-Andrews, R., & Zhou, T. (2018). Anchoring to purchase price and fundamentals: Application of salience theory to housing cycle diagnosis. Real Estate Economics.

Fisher, J., Gatzlaff, D., Geltner, D., & Haurin, D. (2003). Controlling for the impact of variable liquidity in commercial real estate price indices. Real Estate Economics, 31(2), 269–303.

Fisher, J., Geltner, D., & Pollakowski, H. (2007). A quarterly transactions-based index of institutional real estate investment performance and movements in supply and demand. The Journal of Real Estate Finance and Economics, 34(1), 5–33.

Francke, M.K. (2010). Repeat sales index for thin markets. The Journal of Real Estate Finance and Economics, 41(1), 24–52.

Francke, M.K., & van de Minne, A. (2017). The hierarchical repeat sales model for granular commercial real estate and residential price indices. The Journal of Real Estate Finance and Economics, 55(4), 511–532.

Gatzlaff, D.H., & Haurin, D.R. (1997). Sample selection bias and repeat-sales index estimates. The Journal of Real Estate Finance and Economics, 14(1), 33–50.

Geltner, D., Miller, N., Clayton, J., & Eichholtz, P. (2014). Commercial Real Estate Analysis and Investments (3e). OnCourse Learning.

Genesove, D., & Han, L. (2012). Search and matching in the housing market. Journal of Urban Economics, 72(1), 31–45.

Genesove, D., & Mayer, C. (2001). Loss aversion and seller behavior: Evidence from the housing market. The Quarterly Journal of Economics, 116(4), 1233–1260.

Goetzmann, W., & Peng, L. (2006). Estimating house price indexes in the presence of seller reservation prices. Review of Economics and Statistics, 88(1), 100–112.

Guren, A.M. (2018). House price momentum and strategic complementarity. Journal of Political Economy, 126(3), 1172–1218.

Han, L., & Strange, W.C. (2015). The microstructure of housing markets: Search, bargaining, and brokerage. In Handbook of Regional and Urban Economics, (Vol. 5 pp. 813–886). New York: Elsevier.

Heckman, J.J. (1979). Sample selection bias as a specification error. Econometrica:, Journal of the Econometric Society 152–161.

Heidelberger, P., & Welch, P.D. (1981). A spectral method for confidence interval generation and run length control in simulations. Communications of the ACM, 24(4), 233–245.

Hoffman, M.D., & Gelman, A. (2014). The no-U-turn sampler: Adaptively setting path lengths in Hamiltonian Monte Carlo. Journal of Machine Learning Research, 15(1), 1593–1623.

Johnson, N., & Kotz, S. (1972). Distributions in Statistics: Continuous Multivariate Distributions. New York: Wiley.

Koehler, E., Brown, E., & Haneuse, S.J.-P. (2009). On the assessment of Monte Carlo error in simulation-based statistical analyses. The American Statistician, 63(2), 155–162.

Van de Minne, A., Francke, M., Geltner, D., & White, R. (2020). Using revisions as a measure of price index quality in repeat-sales models. The Journal of Real Estate Finance and Economics, 60(4), 514–553.

Van Dijk, D. (2018). Residential real estate market liquidity in Amsterdam. Real Estate Research Quarterly, 17(3), 5–10.

Van Dijk, D.W., & Francke, M.K. (2018). Internet search behavior, liquidity and prices in the housing market. Real Estate Economics, 46(2), 368–403.

Wheaton, W.C. (1990). Vacancy, search, and prices in a housing market matching model. Journal of Political Economy, 98(6), 1270–1292.

Acknowledgements

Many thanks go to seminar participants at the ASSA 2019, Bouwinvest, De Nederlandsche Bank, ERES 2018, MIT Real Estate Price Dynamics Platform, Ortec Finance, RCA Index Seminar 2017, Real Estate Finance & Investment Symposium 2018, Weimar School 2018, and ZEW ReCapNet 2018 conferences and seminars. In particular thanks to John Clapp, Martijn Dröes, Peter van Els, Edward Glaeser, Marc Francke, and Jakob de Haan, Robert Hill, Martin Hoesli, R. Kelley Pace, Miriam Steurer, and an anonymous referee for providing detailed comments. Finally, thanks to Real Capital Analytics for supplying the data. The views expressed are those of the authors and do not necessarily reflect the position of DNB.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher’s Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix: Additional markets

Appendix: Additional markets

Supply, demand, and consummated transaction price indexes of the Boston metropolitan area (left axis) and liquidity metric based on the difference between demand and supply. The shaded areas include periods where prices were increasing and liquidity was decreasing, e.g. “The Anomaly”

Supply, demand, and consummated transaction price indexes of the Chicago metropolitan area (left axis) and liquidity metric based on the difference between demand and supply. The shaded areas include periods where prices were increasing and liquidity was decreasing, e.g. “The Anomaly”

Supply, demand, and consummated transaction price indexes of the Los Angeles metropolitan area (left axis) and liquidity metric based on the difference between demand and supply. The shaded areas include periods where prices were increasing and liquidity was decreasing, e.g. “The Anomaly”

Supply, demand, and consummated transaction price indexes of the San Francisco metropolitan area (left axis) and liquidity metric based on the difference between demand and supply. The shaded areas include periods where prices were increasing and liquidity was decreasing, e.g. “The Anomaly”

Supply, demand, and consummated transaction price indexes of the Seattle metropolitan area (left axis) and liquidity metric based on the difference between demand and supply. The shaded areas include periods where prices were increasing and liquidity was decreasing, e.g. “The Anomaly”

Supply, demand, and consummated price indexes of the Washington D.C. metropolitan area (left axis) and liquidity metric based on the difference between demand and supply. The shaded areas include periods where prices were increasing and liquidity was decreasing, e.g. “The Anomaly”

Rights and permissions

About this article

Cite this article

van Dijk, D., Geltner, D.M. & van de Minne, A.M. The Dynamics of Liquidity in Commercial Property Markets: Revisiting Supply and Demand Indexes in Real Estate. J Real Estate Finan Econ 64, 327–360 (2022). https://doi.org/10.1007/s11146-020-09782-5

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11146-020-09782-5

Keywords

- Liquidity

- Commercial real estate

- Bayesian repeat sales price index

- Equilibrium dynamics

- Constant liquidity index