Abstract

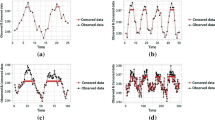

We propose a minimum mean absolute error linear interpolator (MMAELI), based on theL 1 approach. A linear functional of the observed time series due to non-normal innovations is derived. The solution equation for the coefficients of this linear functional is established in terms of the innovation series. It is found that information implied in the innovation series is useful for the interpolation of missing values. The MMAELIs of the AR(1) model with innovations following mixed normal andt distributions are studied in detail. The MMAELI also approximates the minimum mean squared error linear interpolator (MMSELI) well in mean squared error but outperforms the MMSELI in mean absolute error. An application to a real series is presented. Extensions to the general ARMA model and other time series models are discussed.

Article PDF

Similar content being viewed by others

Avoid common mistakes on your manuscript.

References

Abraham, B. (1981). Missing observations in time series,Comm. Statist. A. Theory Methods,10, 1643–1653.

Beveridge, S. (1992). Least squares estimation of missing values in time series,Comm. Statist. Theory Methods,21, 3479–3496.

Brubacker, S. R. and Wilson, G. T. (1976). Interpolating time series with application to the estimation of holiday effects on electricity demand,J. Roy. Statist. Soc. Ser. C,25, 107–116.

Dagum, E. B., Cholette, P. A. and Chen, Z. G. (1998). A unified view of signal extraction, benchmarking, interpolation and extrapolation of time series,International Statistical Review,66, 245–269.

Damsleth, E. (1980). Interpolating missing values in a time series,Scand. J. Statist.,7, 33–39.

Dunsmuir, W. and Robinson, P. M. (1981). Estimation of time series models in the presence of missing data,J. Amer. Statist. Assoc.,76, 560–568.

Ferreiro, O. (1987). Methodologies for the estimation of missing observations in time series,Statist. Probab. Lett.,5, 65–69.

Gómez, V. and Maravall, D. (1994). Estimation, prediction, and interpolation for nonstationary series with Kalman filter,J. Amer. Statist. Assoc.,89, 611–624.

Gómez, V., Maravall, A. and Pena, D. (1999). Missing observations in ARIMA models: Skipping approach versus additive outlier approach,J. Econometrics,88, 341–363.

Grenander, U. and Rosenblatt, M. (1957).Statistical Analysis of Stationary Time Series, Wiley, New York.

Harvey, A. C. and Pierse, R. G. (1984). Estimating missing observations in economic time series,J. Amer. Statist. Assoc.,79, 125–131.

Jones, R. H. (1980). Maximum likelihood fitting of ARMA models to time series with missing observations,Technometrics,22, 389–395.

Kohn, R. and Ansley, C. F. (1986). Estimation, prediction, and interpolation for ARIMA models with missing data,J. Amer. Statist. Assoc.,81, 751–761.

Ljung, G. M. (1982). The likelihood function for a stationary Gaussian autoregressive-moving average process with missing observations,Biometrika,69, 265–268.

Ljung, G. M. (1989). A note on the estimation of missing values in time series,Comm. Statist. Simulation comput.,18, 459–465.

Luceño, A. (1997). Estimation of missing values in possibly partially nonstationary vector time series,Biometrika,84, 495–499.

Parzen, E. (1984).Time Series Analysis of Irregularly Observed Data, Springer, New York.

Peña, D. and Tiao, G.C. (1991). A note on likelihood estimation of missing values in time series,Amer. Statist.,45, 212–213.

Penzer, J. and Shea, B. (1997). The exact likelihood of an autoregressive-moving average model with incomplete data,Biometrika,84, 919–928.

Pinkus, A. M. (1989).On L 1-approximation, Cambridge University Press, London.

Tong, H. (1990).Nonlinear Time Series: A Dynamical System Approach, Oxford University Press, Oxford.

Venables, W. N. and Ripley, B. D. (1994).Modern Applied Statistics with S-Plus, Springer, New York.

Wei, W. W. S. (1990).Time Series Analysis: Univariate and Multivariate Methods, Addison-Wesley, Redwood City, California.

Whittle, P. (1963).Prediction and Regulation by Linear Least Square Methods, English University Press, London.

Wincek, M. A. and Reinsel, G. C. (1986). An exact maximum likelihood estimation procedure for regression-ARMA time series models with possibly nonconsecutive data,J. Roy. Statist. Soc. Ser. B,48, 303–313.

Author information

Authors and Affiliations

Additional information

This research was supported by a CityU Research Grant and Natural Science Foundation of China.

About this article

Cite this article

Lu, Z., Hui, Y.V. L 1 linear interpolator for missing values in time series. Ann Inst Stat Math 55, 197–216 (2003). https://doi.org/10.1007/BF02530494

Received:

Revised:

Issue Date:

DOI: https://doi.org/10.1007/BF02530494