Abstract

The lithium-ion battery technology as the today’s best available technology is a key in accompanying vehicles electrification. Its end-of-life recovery is lever in overcoming technical challenges towards electromobility deployment, such as battery cost, environmental impact, the availability of constituent materials and the mandatory recycling rate. In this chapter, we focus on economic aspects, in order to assess the end-of-life recovery impact: we analyze the end-of-life cost evolution of lithium-ion batteries to determine whether it will be a source of cost or profit for car manufacturers. We define and analyze two recovery options: on the one hand, simply recycling which is mandatory by regulation and, on the other hand, repurposing for reuse in many second life applications (from residence related applications to energy storage and grid stabilization). To account for the complexity and the long-term horizon of our study (2030), we combine the use of System Dynamics with the Stanford Research Institute Matrix for building scenarios that mix relevant factors such as the electric vehicle market and the proportion of repurposing for reuse. Finally we show that repurposing could lower the battery’s initial cost—under certain conditions regarding the future battery price and the repurposing cost—where recycling might increase it.

Access provided by CONRICYT-eBooks. Download chapter PDF

Similar content being viewed by others

Keywords

1 Introduction

The complexity of the transition to electromobility raises questions about the contributing factors, such as energy, socio-economic, political and technological ones. The latter is the topic of this third part of the book. In this chapter we tackle the battery end-of-life whereas in the next one we will investigate firstly the possibilities offered by electric fleets to provide valuable services to the electrical grids, and secondly how the existing rules need to be redesigned in order to expand this type of new business models.

In the context of climatic change, many countries implied in the Paris COP21 in December of 2015 have announced national targets in reducing the emissions of greenhouse gases. These targets will be revised upward every five years according to various criteria, including the evolution of the technical change. Various technological roadmaps (ERI 2009; IEA 2012, 2014; IPCC 2014) from which the governments try to asses some choices and trade-offs consider as crucial the electrification of the transportation sector via the deployment of electric vehicles. Indeed the transportation sector, road transport in particular, causes of many negative externalities today due to the dependence on oil (European Commission 2014a). In France, over one third of CO2 emissions (the powerful greenhouse gas) was due to transportation in 2010, with road transport accounting for 96 % of the transport emissions. In the United States of America, about 30 % of CO2 emissions and a share of 86.4 % for roads in 2010. In China transport accounted for only 7 % of total emissions in 2010, but with a fast growth rate of the number of vehicles of exactly 11 % in 2010, transport and especially road transport will be increasingly huge for future Chinese CO2 emissions. Therefore it proves critical for every country, whatever its level of economic development is, to develop electric vehicles together with the decarbonization of the mix of electricity in order to mitigate global warming (Alazard-Toux et al. 2014; ERI 2009; Saveyn et al. 2012; Tian and Da Costa 2014).

In the climate package of the European Union (EU), commitments call for a transport sector reduction of 60 % in 2050 compared to CO2 emission levels in 1990 (European Commission 2011) and emission thresholds for new light vehicles (personal cars) are defined up to 130 g of CO2 per km in 2015 and 95 g per km in 2020 (European Regulation No. 443/2009: European Commission 2009; European Regulation No 333/2014: European Commission 2014b). While short-term goals seem attainable by the various car manufacturers (EEA 2015) (the goal of 2015 was completed), those of long term are real challenges and will require radical innovations thanks to the new Electric Vehicles (EV). Indeed fuel cells and other promising technologies being less mature in terms of technology and infrastructure, the industry tends to turn towards EV: hybrid, plug-in hybrid and battery-electric (McKinsey and Company 2010). These EVs mainly use Lithium-Ion Batteries (LIB) that give them greater autonomy. However they crystallize some of the barriers preventing widespread use, such as the cost of the battery, its impact on the overall life cycle assessment of the EV and the availability of constituent materials. Moreover, EU regulation imposed on car manufacturers the recycling of at least 50 % of the battery weight (European Commission 2006). The investigation of the battery end-of-life appears then necessary for the following reasons: lowering the battery/vehicle cost and environmental impact, control of the supply of potentially critical materials and compliance with the regulatory recycling rates.

In this chapter we will analyze the end-of-life cost evolution of LIB to determine whether it will be a cost or a profit for car manufacturers. These latter already raise this question in order to guide their strategies (the research chair on electromobility “Armand Peugeot”/CentraleSupélec and ESSEC, France, which supported our research work is a good example). To investigate our research question, we will define and analyze two recovery options: (i) The recycling which is mandatory by regulation; (ii) The repurposing for reuse in second life applications (from residence related applications to energy storage and grid stabilization: see Törkler 2014). The end-of-life cost is the sum of the costs of these two options: recycling being mandatory and repurposing will take place before recycling if profitable. To account for the complexity and the long-term horizon of our study (i.e. 2030), we combine the use of System Dynamics (Sterman 2000) with the Stanford Research Institute Matrix for building scenarios. Our set of six techno-economic scenarios show that it is possible the recovery could not lower the initial LIB cost, or even increase it by 26 % in the worst case; And in the case when it is possible to reduce this initial cost, it is the repurposing that would contribute to it, even if this initial cost reduction is weak (11 % of the initial cost in the best case).

Section 8.2 now introduces the technical scope about battery and recovery technologies: these concepts are necessary for understanding the subsequent analysis. Our approach and results will be detailed in Sects. 8.3 and 8.4 respectively. Section 8.5 concludes this chapter.

2 Battery and Recovery Technologies

2.1 Battery

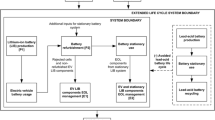

For vehicle electrification needs, several battery technologies are available: nickel cadmium (Ni–Cd), nickel metal hydride (Ni–MH) and lithium-ion (LIB). Nevertheless LIBs are more adapted and used (energy density, voltage of cells, lifespan and memory effect). A LIB is made up of the electrochemical (set of modules, which are composed primarily of cells) and the electrical and support part (battery management system, connecting cables and cooling system) (see Fig. 8.1).

Therefore the basic component in a battery is the cell. A cell consists of an electrolyte, a separator, an anode (negative electrode) and a cathode (positive electrode). Each of the two electrodes is composed of a conductor and an active material. The negative active material of the anode is usually graphite. The positive active material of the cathode is a combination of lithium and a metal oxide, which varies from one technology to another. It is this latter that defines the properties of the LIB (lifespan, safety, capacity, and cost) (and gives it its name). In this chapter, we selected two families of key technologies:

-

Nickel-Manganese-Cobalt based batteries (NMC) with the average composition Li(Ni 1/3 Mn 1/3 Co 1/3 )O 2 (ADEME 2013; Hoyer et al. 2014);

-

Iron phosphate based batteries (LFP) with the composition LiFePO 4 .

In terms of materials contained in a LIB, Fig. 8.2 shows the average proportions in a pack. They are found in the following:

Analytical decomposition of an EV pack

-

Steel and iron: casing of the battery cells, bolts;

-

Aluminum and copper: electrode conductors, cables, electronic boards;

-

Plastics: casing of the battery, cables, separator;

-

Graphite: negative active material of the anode;

-

Lithium: electrolyte and positive active material of the cathode;

-

Cobalt, Nickel, Manganese, iron, phosphorus: positive active material of the cathode;

-

And solvents.

The mass of a LIB is proportional to its capacity, it depends on the vehicle electrification level: hybrid “HEV” (1–2 kWh, about 30 kg), plug-in hybrid “PHEV” (5–15 kWh, about 150 kg) and battery-electric “BEV” (over 15 kWh, about 250 kg).

2.2 Recovery Options

Two main LIBs recovery options can be considered: recycling (as required by EU regulation) and repurposing for reuse in 2nd life applications. Due to the evolution of LIB technology and still very low volumes reaching the end-of-life, these recovery options are in their infancy: a structured recovery network does not therefore exist today (since emergent actors, emergent recovery technologies, low volumes, short term contracts between automakers and recyclers).

The next two sections introduce further details on the recovery options plausible.

2.2.1 Repurposing for Reuse in 2nd Life Applications

2nd life applications refer to possible uses of repurposed LIBs after the first automotive life. Under the European Li-Ion Battery Advanced Manufacturing (ELIBAMA) project,Footnote 1 Törkler (2014) classifies 2nd life applications according to the following three categories:

-

Residence related application (3–4 kWh);

-

Commercial applications (25 kWh–4 MWh): Telecommunication towers, Light commercial, Uninterruptible power supply (UPS), etc.;

-

Energy related/industrial applications (up to 50 MWh): Renewable energy storage, Grid stabilization, etc.

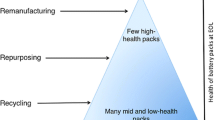

Repurposing for 2nd life use is about dismantling the battery to a defined level, test and replace defective parts, reassemble them into a new configuration and add a battery management system (Ahmadi et al. 2014). Regarding the repurposing processes, they remain to be defined. The main issue is the definition of a good dismantling level: pack, module, cell, or even at the cathode level (Ganter et al. 2014; Georgi-Maschler et al. 2012; Ramoni and Zhang 2013). Precise quantitative data (costs, benefits, advantages, etc.) per process, which as we have shown, is today not even defined. Thus our repurposing modeling is done generically, regardless of the repurposing process, which will be defined later.

2.2.2 Recycling

The EU directive 2006/66/EC sets the regulatory framework for the treatment of batteries and accumulators at end-of-life. It imposes for EV batteries: (i) The establishment of a collection and a recycling system; and (ii) The requirement to recycle at least 50 % of the battery weight. Therefore the recycling objective is simply the achievement of these regulatory targets, while recovering the value contained in the LIB materials.

These materials are found at different levels in the battery (electrode, cell, pack), in different proportions (remember Figs. 8.1 and 8.2), as well as with a different contribution to the recovered value. Operations of extraction, separation and purification are required consequently. Kwade (2010) identifies four possible basic processing operations: Dismantling; Mechanical conditioning; Pyrometallurgical conditioning; And hydrometallurgical conditioning. These operations could be combined in several ways to form five recycling alternatives. The scientific and industrial state of the art by Idjis (2015) considers two recycling processes as shown in Fig. 8.3. Each process is a succession of three operations, the recovered materials at each operation are described in the bottom. We denote Process 1 by P1 and Process 2 by P2.

Considered recycling processes

We notice that the recovery of materials contained in the positive active material (which are difficult to access) requires an elaborate recycling process, therefore a high cost. This is why materials such as lithium are not recycled today. In the future, with the development of EV, the level of criticality of any material will certainly justify the economic benefit of its recycling, which will reduce this initial criticality.

We have highlighted above the so-called System Dynamics methodology (Sterman 2000) i.e. a feedback loop. The concept of feedback loop can be explained using the analogy of vicious or virtuous circles, wherein an influence spreads among several factors and returns back to the factor that initially generated it.

3 Our Approach

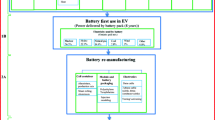

SD is a systems-thinking methodology suitable for the analysis of large-scale complex systems wherein heterogeneous factors interact. “The objective is to analyze, understand and predict the behavior of this system over time by analyzing its changing factors” (Sterman 2000). For our study, this means: (i) Identifying the factors that create the dynamics of end-of-life volumes, recycling profitability, repurposing profitability and end-of-life profitability; (ii) Modeling of internal laws of behavior between these factors and their time simulations in several scenarios. This was done in a much broader study by Idjis (2015), in which other objectives such as material criticality and compliance with recycling targets are investigated (Fig. 8.4).

Overview of the LIB recovery network SD model (Idjis 2015)

As shown in the figure above, a SD model is a set of factors related by links of causalities. The feedback loops are represented with the bold arrows and the negative signs indicate that these are negative ones. In the next Fig. 8.5, we will focus on the recycling profitability diagram as one example to explain the whole model.

A simplified diagram of the recycling profitability dynamics

The diagram is explained as follow: the profitability of any recycling process, ‘P’ is driven by the recycling profit and cost. The recycling cost is calculated based on the volume treated, the initial investment, the fixed cost, the variable cost and the transportation cost; While the recycling benefit is induced also by the treated volume, the income from the resale of recycled materials and the income from car manufacturers. Finally we have highlighted a feedback loop (in bold, Fig. 8.5) we explain as follow: if the income from the resale of recycled materials is not enough to get the profitability of recycling, the car manufacturer will offset this deficit. Conversely, if the income from the resale of recycled materials is sufficient, the car manufacturer might even receive compensation from this income.

In our prospective study, we have combined the SD with scenarios. The choice of the Stanford Research Institute (SRI) matrix was done because of its suitability with the characteristics of our SD model: complexity, heterogeneous factors and emergence (Acosta and Idjis 2014). The SRI matrix is a crossing of two dimensions of factors that dictate primarily the dynamic evolution of the SD model. The scenarios introduced below are derived from Idjis (2015) (Table 8.1). The first dimension (left side) is about end-of-life volume creation (with two variables) and the second one (top side) is about end-of-life profitability (three variables). Then a particular scenario is a crossing of particular assumptions for these variables.

For example in the S1 scenario, the electric vehicles sales volume is from the IEA’s 2DS energy scenario (IEA 2012). This latter is based on proactive environmental policies to contain global warming to 2° (2DS) in 2050, unlike the 4° scenario (4DS). These vehicles have a capacity of 30 kWh and 12.5 kWh for EVs and PHEVs respectively. In the S1 scenario, 80 % of end-of-life automotive LIBs undergo 2nd life reuse before recycling. The main technology is based on nickel, manganese and cobalt (NMC) and the transport cost will decrease from 1500 €/t in 2020 to 1000 €/t in 2030.

As a reminder, we consider a European geographical area. The model is simulated from 2010 (first sales of electric vehicles based on LIBs) until 2050. This is consistent with the literature on EV sales and metals consumption (IEA 2012; Miedema and Moll 2013; Pasaoglu et al. 2012). In this timeframe, the LIBs will be the reference technology to be recovered at least until 2040 and beyond with post LIB batteries.

4 Results and Discussion

Section 8.4 analyzes the recycling, repurposing and end-of-life profitability.

4.1 Recycling Profitability

In order to analyze recycling profitability, we define the recycling cost and the global recycling cost that is equal to the recycling cost plus the transport cost for recycling. These two could be positive or negative: Positive as a source of cost for automakers when the income from the resale of recycled materials does not guarantee the recycling profitability; And negative as a source of profit for car manufacturers.

We calculate a recycling cost that allows a five years return on investment period, and a capital productivity of the order of 2 in 20 years (common industry standards), with a discount rate of 8 % (Hein et al. 2012; Hoyer et al. 2014; Neubauer et al. 2012). This cost will be analyzed in Process 1 (P1) and Process 2 (P2) (see Fig. 8.3) in the six scenarios described above, with sensitivity analysis for each.

Figure 8.6 shows that in 2020, we gat a recycling cost ranking in accordance with the treated end-of-life volumes in each scenario, with a maximum recycling cost of 2500 €/t in S4. For the six scenarios, we observed a decline in the recycling cost between 2020 and 2025 due to economies of scale. From 2025, we notice three trends: Declining for the pair (S1 and S4); Stagnation for (S2 and S5); And increase for (S3 and S6). Cost stagnation and increase in S2/S5, S3/S6 respectively, is due to the increase in the proportion of LFP at the expense of the NMC batteries that have a bigger recycling revenue (NMC = 1569 €/t; LFP = 593 €/t).

Evolution of the recycling cost in P1 in the six scenarios

As for P1, we show the same trends in P2 in the next Fig. 8.7.

Evolution of the recycling cost in P2 in the six scenarios

The difference with P1 lies in the initial and the long-term (around 2030) recycling costs. The maximum recycling cost is 5500 €/t for S4 in 2020. The long-term recycling cost stabilizes at 600 €/t in S1/S4; 900 €/t in S2/S5; and 1250 €/t in S3/S6.

The recycling cost in P2 is higher than the one in P1 in between 600 and 700 €/t. This is due to pyrometallurgical conditioning requiring a higher investment (special installations to treat toxic gas from pyrolysis) than the mechanical conditioning.

As there are other factors (which remained unchanged in the six scenarios) that affect the profitability of recycling, we have proceeded to a sensitivity analysis to investigate the effect of these other uncertain factors. It includes the following:

-

Increase and decrease of 50 % in the variable recycling cost;

-

Annual increase of 1 and 2 % in the materials resale price;

-

Decrease of % 2nd life to 20 and 0 %;

-

And the evolution of NMC technology towards nickel or manganese enriched ones.

Considering these four sensitivity analysis, the recycling cost could stabilize in the long term (i.e. 2030) in between −1000 and 1600 €/t, as shown in the following two graphs of Fig. 8.8.

Possible values of the long term recycling cost in both processes

Remind this cost does not include the transportation cost. This latter varies between 1000 and 1500 €/t, depending on the scenario and the period (see Table 8.1). By including it, the overall recycling costs varies in between 0 and 3100 €/t. We conclude that recycling would remain a net cost in the battery end-of-life, charged to the car manufacturer in all our designed scenarios.

4.2 Repurposing Profitability

The objective is now to assess the conditions for the profitability of this recovery option and its impact on the LIB end-of-life cost. To do so we calculate the repurposing margin as follow: repurposing margin (€/kWh) = repurposed LIB selling price – (variable cost of repurposing + transportation cost). This latter is of considerable importance because it indicates a potential source of profit for car manufacturers, which could enhance the LIB end-of-life profitability.

Repurposing exists only in scenarios S1/S4 (80 % of end-of-life available volume) and S2/S5 (20 % of volume). For the four scenarios, we have calculated the unprofitability thresholds (Table 8.2) compared to reference values shown in the appendix (Tables 8.8 and 8.9).

When repurposing is profitable, we have a long-term (2030) repurposing margin value between 9.7 and 15.8 €/kWh as shown in the next Fig. 8.9.

Possible values of the repurposing margin in the long term

We conclude that the repurposing profitability is dependent on the developments of some influencing factors: LIB price, fixed and variable repurposing cost. Under favorable conditions, the repurposing margin is at least 9.7 €/kWh. This could enhance the end-of-life profitability as shown in the next section.

4.3 End-of-Life Profitability

Considering the recycling cost in both processes and the repurposing margin, we calculated the end-of-life cost in the six scenarios. As for recycling, we distinguish the end-of-life cost (recycling cost—repurposing margin) and the global end-of-life cost (global recycling cost—repurposing margin). Looking at the intervals of the recycling cost possible values (Fig. 8.8) and the repurposing margin ones (Fig. 8.9), we obtain the following ranges for the LIB end-of-life cost in the long term (see Fig. 8.10).

Possible values for the end-of-life cost in the two processes

Figure 8.10 shows that in P1 (on left), the end-of-life is always beneficial in scenarios S1/S4 and S2/S5, what is not always true in P2. S3/S6 remains a net cost in all situations. If the transportation cost is included into recycling (which is 1000 €/t in S1/S4; 1250 €/t in S2/S5; and 1500 €/t in S3/S6) then we get the following ranges for the global end-of-life cost in the long term (see Fig. 8.11).

Possible values for the global end-of-life cost in the two processes

Comparing P1 and P2 above, we deduce the importance of minimizing the transportation cost because this latter greatly increases the LIB end-of-life cost.

After analyzing the LIB end-of-life cost, we can conclude with the overall life cycle cost. This latter includes the LIB initial price and global end-of-life cost (Fig. 8.12). Our interest is to answer the question raised in the introduction: in what extent recovery (recycling/repurposing) is a source of profit or cost in the LIB overall life cycle.

The components of the LIB overall life cycle cost

To do this we first analyze the effect of the ‘global recycling cost’ and the ‘repurposing margin’ separately, and then together through the ‘global end-of-life cost’. Remind of the long-term possible values of these three points in Table 8.3.

In order to harmonize these costs and report them to one LIB, we consider an average LIB with a weight of 250 kg and a capacity of 20 kWh. Regarding the LIB initial price in the long term, we consider an average price of 150 €/kWh (Table 8.9). Therefore we get the following equivalent costs for recycling in Table 8.4. The effect on the LIB overall life cycle cost is calculated in the last column of the table below.

Ultimately, recycling will be neutral in the LIB overall life cycle cost (0 €/kWh) in the best case. In the worst case, recycling will increase the LIB overall life cycle cost by 26 % (39 €/kWh).

Moving to repurposing, still considering an average LIB of 250 kg and 20 kWh, a future LIB price of 150 €/kWh, we get the following equivalent margins (see Table 8.5). We mention them with a negative sign to mean the reduction effect in the LIB overall life cycle cost (profit).

In the long term, when repurposing is developing, the LIB overall life cycle cost may be reduced by 11 % in the best case. In the worst case, it will be done by just 6 %.

Finally we analyze the effect of the recovery (recycling and repurposing) on the LIB overall life cycle cost, through the LIB global end-of-life cost. Still considering an average LIB of 250 kg and 20 kWh, a future LIB price of 150 €/kWh, we get the following equivalent costs in Table 8.6.

In the long term, and in the best case, where repurposing is developing and the global recycling cost is null, the LIB overall life cycle cost may be reduced by 11 %. In the worst case, corresponding to no repurposing and a global recycling cost of 3100 €/t, the LIB overall life cycle cost may be increased by 26 %.

5 Conclusion

In this chapter, we have investigated the recovery of lithium-ion batteries from particularly the end-of-life cost effect on the economy of the LIB and the EV. We have identified two recovery options: (i) Recycling: mandatory by EU regulation, with two main processes (P1 for mechanical and P2 for pyrometallurgical: Fig. 8.3); (ii) Repurposing for 2nd life reuse will only develop if the economic conditions are favorable.

For recycling, we have determined that the cost is higher in the pyrometallurgical process (P2). In 2030, recycling could generate value for car manufacturers in certain conditions (high volume and bigger share of NMC batteries). However, by adding the transportation cost of LIBs for recycling, we only can reach equilibrium (zero cost) in the best case. Hence our results underline the need to properly model and minimize costs of logistics in transportation. The repurposing analysis allowed us to identify the conditions for this recovery option to be profitable. In the long term, repurposing could generate from 9.7 to 15.8 €/kWh of profits. This will significantly enhance the LIB end-of-life profitability.

In the analysis of the end-of-life cost, we have considered simultaneously the two recovery options. We concluded that it is possible that the recovery cannot lower the initial LIB cost, or even increase it by 26 % in the worst case. In the case that it is possible to reduce this initial cost, it is the repurposing that would contribute to it, even if this reduction is weak (11 % of the initial cost in the best case).

Finally we would like to mention a few avenues of research that are worth exploring in the future. As we did with the LIB end-of-life economic cost, future research would consist in assessing the environmental effect of the LIB recovery with life-cycle assessment (ISO 14040:2006). Indeed, the analysis of financial is very relevant to automakers, but the impacts on the environment must be analyzed too, since all stakeholders are facing them.

Notes

- 1.

The objective of the ELIBAMA project is to enhance and accelerate the creation of a strong European automotive battery industry structured around industrial companies already committed to mass production of Li-ion cells and batteries for EV: https://elibama.wordpress.com/.

References

Acosta, C., Idjis, H., 2014. State of the art of scenario planning: Proposal of a classification of scenario building existing methods according to use (Mémoire thématique). Ecole Centrale Paris.

ADEME, 2013. Élaboration selon les principes des ACV des bilans énergétiques, des émissions de gaz à effet de serre et des autres impacts environnementaux. Induits par l’ensemble des filières de véhicules électriques et de véhicules thermiques, VP de segment B (citadine polyvalente) et VUL à l’horizon 2012 et 2020. Agence de l’Environnement et de la Maîtrise de l’Energie.

Ahmadi, L., Fowler, M., Young, S.B., Fraser, R.A., Gaffney, B., Walker, S.B., 2014. Energy efficiency of Li-ion battery packs re-used in stationary power applications. Sustainable Energy Technologies and Assessments 8, 9–17.

Alazard-Toux, N., Criqui, P., de Lavergne, J.-G.D., Hache, E., Le Net, E., Lorne, D., Mathy, S., Menanteau, P., Safa, H., Teissier, O., 2014. Les scénarios de transition énergétique de l’ANCRE, Revue de l’Energie.

Avicenne Energy, 2014. xEV Market 2014-2025. Impact on the battery business. Presented at the EEVC, Brussels.

Cready, E., Lippert, J., Pihl, J., Weinstock, I., Symons, P., 2003. Technical and economic feasibility of applying used EV batteries in stationary applications (No. SAND2002-4084). Sandia National Labs., Albuquerque, NM (US); Sandia National Labs., Livermore, CA (US).

EEA, 2015. Global search on data, maps and indicators — European Environment Agency (EEA) [WWW Document]. URL http://www.eea.europa.eu/data-and-maps/find#c1=Graph&c1=Map&b_start=0&c6=transport (accessed 4.14.15).

ERI, 2009. China’s Low Carbon Development Path by 2050: Scenario analysis of Energy Demand and Carbon Emissions, Science Press. Energy Research Institue.

European Commission, 2014a. Statistical pocketbook 2014 - Transport. European Commission.

European Commission, 2014b. Regulation (EU) No 333/2014 of the European Parliament and of the Council of 11 March 2014 amending Regulation (EC) No 443/2009 to define the modalities for reaching the 2020 target to reduce CO 2 emissions from new passenger cars.

European Commission, 2011. White Paper on Transport: towards a competitive and resource efficient transport system.

European Commission, 2009. Regulation (EC) No 443/2009 of 23 April 2009 setting emission performance standards for new passenger cars as part of the Community’s integrated approach to reduce CO2 emissions from light-duty vehicles.

European Commission, 2006. Directive 2006/66/EC of the European parliament and of the council of 6 September 2006 on batteries and accumulators and waste batteries and accumulators and repealing Directive 91/157/EEC.

Ganter, M.J., Landi, B.J., Babbitt, C.W., Anctil, A., Gaustad, G., 2014. Cathode refunctionalization as a lithium ion battery recycling alternative. Journal of Power Sources 256, 274–280.

Georgi-Maschler, T., Friedrich, B., Weyhe, R., Heegn, H., Rutz, M., 2012. Development of a recycling process for Li-ion batteries. Journal of Power Sources 207, 173–182.

Hein, R., Kleindorfer, P.R., Spinler, S., 2012. Valuation of electric vehicle batteries in vehicle-to-grid and battery-to-grid systems. Technological Forecasting and Social Change 79, 1654–1671.

Hoyer, C., Kieckhäfer, K., Spengler, T.S., 2014. Technology and capacity planning for the recycling of lithium-ion electric vehicle batteries in Germany. Journal of Business Economics.

Hoyer, C., Kieckhäfer, K., Spengler, T.S., 2013. Impact of mandatory rates on the recycling of lithium-ion batteries from electric vehicles in Germany, in: Nee, A.Y.C., Song, B., Ong, S.-K. (Eds.), Re-Engineering Manufacturing for Sustainability. Springer Singapore, pp. 543–548.

Idjis, H., 2015. La filière de valorisation des batteries de véhicules électriques en fin de vie : contribution à la modélisation d’un système organisationnel complexe en émergence (phdthesis). Université Paris-Saclay.

IEA, 2014. Energy Technology Perspectives 2014 - Harnessing Electricity’s Potential. International Energy Agency, Paris.

IEA, 2012. Energy Technology Perspectives 2012: Pathways to a Clean Energy System. International Energy Agency, Paris.

IPCC, 2014. Climate Change 2014: Mitigation of Climate Change, Fifth Assessment Report. IPCC Working Group III.

Kwade, A., 2010. On the way to an “intelligent” recycling of traction batteries. Presented at the 7th Braunschweiger Symposium on Hybrid, Electric Vehicles and Energy Management, Braunschweigh.

Lux Research, 2015. Crossing the Line: Li-ion Battery Cost Reduction and Its Effect on Vehicles and Stationary Storage. Lux Research.

McKinsey and Company, 2010. Portfolio of Power-trains for Europe: A Fact-Based Analysis.

Miedema, J.H., Moll, H.C., 2013. Lithium availability in the EU27 for battery-driven vehicles: The impact of recycling and substitution on the confrontation between supply and demand until2050. Resources Policy 38, 204–211.

Neubauer, J.S., Pesaran, A., Williams, B., Ferry, M., Eyer, J., 2012. A techno-economic analysis of PEV battery second use: Repurposed-battery selling price and commercial and industrial end-user value (SAE Technical Paper No. 2012-01–0349). SAE International, Warrendale, PA.

Pasaoglu, G., Honselaar, M., Thiel, C., 2012. Potential vehicle fleet CO2 reductions and cost implications for various vehicle technology deployment scenarios in Europe. Energy Policy 40, 404–421.

Ramoni, M.O., Zhang, H.-C., 2013. End-of-life (EOL) issues and options for electric vehicle batteries. Clean Techn Environ Policy 15, 881–891.

Saveyn, B., Paroussos, L., Ciscar, J.-C., 2012. Economic analysis of a low carbon path to 2050: A case for China, India and Japan. Energy Economics 34, S451–S458.

Sterman, J., 2000. Business Dynamics: Systems Thinking and Modeling for a Complex World. Irwin/McGraw-Hill, New York.

Swart, P., Dewulf, J., Biernaux, A., 2014. Resource demand for the production of different cathode materials for lithium ion batteries. Journal of Cleaner Production 84, 391–399.

Tian, W., Da Costa, P., 2014. A Sectoral Prospective Analysis of CO2 Emissions in China, USA and France, 2010-2050. Presented at the The 4th IAEE Asian Conference. IAEE, Beijing, China.

Törkler, A., 2014. Electrodes and cells manufacturing white paper:Batteries Refurbishing & Reuse. ELIBAMA.

Umicore, 2010. The UMICORE Process: Recycling of Li-ion and NiMH batteries via a unique industrial Closed Loop.

Väyrynen, A., Salminen, J., 2012. Lithium ion battery production. The Journal of Chemical Thermodynamics, Thermodynamics of Sustainable Processes 46, 80–85.

Acknowledgment

This research benefits from the support of the Chair “PSA Peugeot Citroen Automobile: Hybrid technologies and Economy of Electromobility”, so-called Armand Peugeot Chair led by CentraleSupélec, ESSEC and sponsored by PEUGEOT CITROEN Automobile.

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Appendix

Appendix

The Appendix highlight the main assumptions used in our SD model, starting from the recycling costs, which are derived from bibliographic research (Hoyer et al. 2013, 2014) and industrial announcements (Umicore 2010) (Table 8.7).

The following Tables 8.8 and 8.9 give the main assumptions for repurposing costs and LIB prices. In this chapter, we have adopted the mean values.

Rights and permissions

Copyright information

© 2017 Springer International Publishing Switzerland

About this chapter

Cite this chapter

Idjis, H., da Costa, P. (2017). Is Electric Vehicles Battery Recovery a Source of Cost or Profit?. In: Attias, D. (eds) The Automobile Revolution. Springer, Cham. https://doi.org/10.1007/978-3-319-45838-0_8

Download citation

DOI: https://doi.org/10.1007/978-3-319-45838-0_8

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-319-45837-3

Online ISBN: 978-3-319-45838-0

eBook Packages: EnergyEnergy (R0)