Abstract

This chapter uses the Global Trade Analysis Project (GTAP) model to explain the relative benefits of India aligning with Gulf Cooperation Council (GCC) countries. We use a GTAP-8 database to handle the general equilibrium model of 19 regions over 15 commodity groups. The discussion endeavors to analyze the expected gains from the India–GCC trade agreement, which has been signed but has not been put into effect. From our analysis, we conclude that India will be a net loser while GCC countries will be net gainers under this free trade agreement (FTA). The loss to India will appear on the current account because of unfavorable terms-of-trade with GCC countries. The same loss will be reflected as a welfare loss, and Indian policy planners are advised to work in the direction needed to convert the expected losses into substantial gains.

Access provided by CONRICYT-eBooks. Download chapter PDF

Similar content being viewed by others

1 Introduction

India and the Gulf Cooperation Council (GCC) are partners in various trading arrangements around the world. Until now, India has been party to 37 such trading arrangements, out of which 9 have been proposed but not acted on, 4 have been signed but not enacted, 11 have had negotiations launched, and 13 have been signed and put into effect.

The GCC group is the latecomer in adopting the policies of regional trade agreements. Currently, it is a party to 9 such trading arrangements, of which 1 is proposed but not acted on, 5 have had negotiations launched, 2 are signed but not enacted, and 1 has been signed and put into effect.

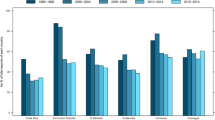

Figure 10.1 presents the engagements of both parties with other regions in the world through the policy of regional trade agreements (RTAs) of the World Trade Organization (WTO). The table included in the figure shows the number of trade agreements through which both are linked with other regions of the world. The first column shows the corresponding partner region with which both states/parties are linked through a trade agreement.

List of free trade partners of India and the GCC (Source: The pattern of figures adapted from Arora et al. 2015)

It is worth mentioning that any trade agreement between countries passes through four stages before its implementation. An agreement is firstly proposed (PA) by the policymakers of member countries after which the extent of the proposed agreement is linked to via joint study groups. Subsequently, the agreement is officially signed (SO) by the member countries. After they offer approval, negotiations (NL) are held on the items to be included in positive and negative lists as per the trade agreement. Finally, after the successful negotiations and consensus, an agreement is signed and brought into effect (SE).

Table 10.1 and Fig. 10.1 present a statewide number of trade agreements through which both countries are linked with other major regions of the world. They have also signed a free trade agreement with each other. The Framework Agreement on Economic Cooperation between India and the GCC was signed on August 25, 2004. As per the agreement, both parties shall consider ways and means for extending and liberalizing trade relations.

The GCC as a collective entity has tremendous geographical and economic significance for India. The Gulf countries constitutes the “immediate” neighborhood of India separated only by the Arabian Sea. India, therefore, has a vital stake in the stability, security, and economic well-being of the Gulf nations. As a group, the GCC has increasingly determined the economic, political, and security policies of its member states. The GCC countries are moving ahead rapidly with their economic integration efforts. The GCC has emerged as a major trading partner for India. It has vast potential as India’s investment partner for the future. The GCC’s substantial oil and gas reserves hold vital importance for India’s energy needs. The GCC countries are collectively host to a large Indian expatriate community. In short, the GCC offers tremendous potential for cooperation in trade, investment, energy supply, manpower, and so on.

In this chapter, we study the impact of trade liberalization between India and the GCC using the GTAP model framework. For this purpose, the entire study has been divided into six sections including the present introductory one. Section 2 presents the economic and commercial relations between India and GCC countries. In Sect. 3, simulation scenarios and data aggregations have been defined. In Sect. 4, implications of tariff reforms in the GTAP model have been discussed in brief. Section 4 presents the simulation results of the GTAP model, and the final section concludes the study.

2 Economic and Commercial Relations of India and the GCC

2.1 Trade Profile

India enjoys longstanding ties with GCC states. It has increased imports of oil and gas from the GCC. Its trade and investment opportunities have been growing. There is a presence of approximately 6.5 million Indian workers in the region. All these factors are of vital interest to India. India’s economic linkages with the GCC have increased steadily, especially due to growth in oil imports. These linkages continue to make steady progress to date. During 2013–2014, India’s exports to the GCC were US$ 48,221 billion. The bilateral two-way trade during the period was US$ 147,615 billion, and it has been growing at a steady pace. India’s trade with the GCC states during the years 2010–2011, 2011–2012, 2012–2013 and 2013–2014 are given in Table 10.2. Further, Table 10.3 shows the trend of India–GCC trade over the past five years. This table shows that India’s trade balance with the GCC is highly negative, to the tune of US$ 51,172.69 million in the year 2013–2014.

In terms of total trade figures, the GCC is the largest trading partner of India and also has a share of 19.31% in total trade with India. The major items of Indian exports and imports to the GCC are the main commodities of Indian exports to the GCC including commodities with HS code 27 (mineral fuels; mineral oils and products of their distillation; bituminous substances; mineral waxes), commodities of HS code 71 (natural or cultured pearls, precious or semiprecious stones, premetals clad with premetal and articles thereof; imitation jewelry; coins), and products of HS code 10 (cereals); Similarly, products in categories 27 and 71 have a major share in Indian imports from PGC.

2.2 Tariff Profile of India and GCC

The tariff profile of a region provides the level of protection of that region over the traded products. A country’s level of protection is determined by its own tariffs and nontariff barriers imposed on imports from partner countries. It is calculated by evaluating the annual average tariff rate over all the products. A higher level of protection from member countries is associated with significant trade creation and trade diversion effects.

Table 10.4 illustrates various indicators of the level of protection from all partner countries in the world. It shows that India’s level of protection relative to the GCC is much higher. If the level of trade between the member countries is very high, then the gains associated with the policy of regional trade agreements are highly dependent upon the level of protection of the member countries. A higher level of initial protection or barriers (i.e., initial tariff rate and nontariff barriers) would lead to larger gains afterwards.

2.3 Comparative Advantage Statistics for India and the GCC

Vast differences in comparative advantage over products are beneficial for member countries to be in a trade agreement. The present study calculates bilateral Revealed Comparative Advantage (RCA) productwide to show the comparative advantage of both the countries (see Table 10.5). It may be noticed that India enjoys the highest comparative advantage in processed rice followed by plant-based fibers. However, the GCC’s highest comparative advantage is observed in oil products, where the observed difference between the Indian comparative advantage index and that of the GCC is very high. The value of the comparative advantage index for India in oil production is zero and that of the GCC is 94.17.

Further, the second highest RCA value for GCC partners is observed for petroleum and coal products, with a value of 5.85. The third most important product in the GCC’s trade basket is gas with an RCA value of 2.06. From Table 10.5, it is evident that for the GCC, a few products have an RCA above unity, while India has a number of products with values above unity in the same index. Thus, India has a huge potential to enhance trade relations with the GCC and the partner can offer oil, petroleum, coal products, and gas to purchase the products for which India enjoys a relative comparative advantage. In the same way, both partners may explore the gains of international trade.

2.4 Trade Intensity Index for India and the GCC

Further, calculation of the trade intensity index in Table 10.6 is used to measure the country’s export competitiveness in a particular market. This helps to shed light on the issue of the extent of domestic substitution in production by partner countries. The index explains the role of any country/region in another country’s trade. The comparison of Table 10.6 with Table 10.5 produces interesting evidence; it may be inferred from comparison of the two that the TII is high for the products in which the nation gain’s comparative advantage, and vice versa. For food products, the trade intensity of India is very high, while for oil and gas products, the trade intensity of the GCC is high enough.

3 Construction of Simulation Scenarios and Data Aggregations

3.1 Simulation Scenarios

Table 10.7 provides data on the tariff reduction for the GCC and India in the two models taken for consideration. In model I, both the regions have to levy the same tariff rate on all the sectors. India charges more in all sectors so it needs to cut more on the tariffs to bring the duty to a level equal to the GCC region’s duty. The proposed reduction for both regions is reported in the table under the column for model I. In model II, both regions need to cut the tariff duties to a zero level. Again, it is observed that India reduces more compared to the GCC. From Table 10.7, it is observed that India charges more tariffs in the sector of processed foods by 58.67% and in sector HS-10 it charges less duty by 2.3%.

3.2 Data Aggregations

In both of the above models, 19 regions—namely, India, the GCC, China, Japan, the Republic of Korea, New Zealand, Malaysia, Singapore, Australia, the Rest of Oceana, the Rest of East Asia, the Rest of Southeast Asia, the Rest of South Asia, North America, Latin America, European Union-25, the Middle East and North Africa, Sub-Saharan Africa, and the Rest of World—have been taken into consideration in details furnished in Table 10.8. These regions include all the countries of the world to see the impact of the FTA between India and the GCC countries.

In addition, 15 commodity groups have also been created to portray the impact of the FTA on commodity trading. The groups in these models cover all goods and services used in the GTAP-8 model. However, these 15 groups—namely, HS-27, HS-71, HS-10, HS-85, HS-84, HS-63, HS-62, Grains Crops, Meat and livestock, Extraction, Processed food, Light Manufacture, Heavy Manufacture, Utility and Consumption Goods, and Other Services—are categorized on the basis of their share in India’s trade with the GCC countries. In Table 10.9, the commodity groups with the prefix HS have been created for those commodities that have the highest shares in India–GCC trade.

4 Implications of Tariff Reforms

4.1 Trade Effects

With the formation of a free trade agreement, prices of imported goods from countries in the free trade area will decrease due to the reduction in tariffs on the imports. This will permit countries entering into an FTA to shift from expensive imports from the outside world to purchase cheaper imports from within the circle of member nations, thereby resulting in trade creation among them. Thus, a change in trade policy (e.g., tariff liberalization) affects not only the price index/level of the composite goods, but also the relative prices of other goods/products. Any trade policy shock will also have an effect on the entire trade flow (i.e., Imports from different countries).

Trade diversion results when shifting imports from a country selling at a high price to a country with a comparative advantage in the traded commodity (in this case commodity g) to a country that is less efficient in producing the goods in question. This shift takes place due to the formation of a trade bloc. Trade diversion in our example is neutral because an increase in imports from the partner countries is balanced by reduction in the imports from all the other countries. The net effect is a reallocation of the market share among the exporting countries with the overall imported quantity not changing. As per the main concepts of trade creation and trade diversion given by Viner, the above concepts are very difficult to test because calculation of the costs of production of various tradable commodities in different countries is complex. Also, Viner’s analysis is in the nature of a partial equilibrium, which does not explain how the welfare can be calculated in the case of a multigood trading world.

In most studies, the concepts of trade creation and trade diversion are generally used in the sense of an increase in trade from a member country and a shift of trade from a nonmember to a member country. In view of the foregoing, instead of using the terms “trade creation” and “trade diversion,” we use the terms trade “generation” and “shifting” which can be calculated in the GTAP model by using the following equations:

where VIWS (i, r, s) is the value of imports of i from r to s valued CIF tradable only; VXWD (i, r, s) are the exports of i from r to s valued FOB (tradable only); PCIF is the CIF world price of commodity i supplied from r to s; PFOB is the FOB world price of a commodity supplied from r to s; QXS is the quantity of exports of product i from r to s. The variables in lowercase letters are the percentage counterparts of the original level variables as defined above. To calculate the changes in imports and exports in a post-simulation environment, one can simply subtract the new value of imports from the existing value of imports in the base data. Similarly, changes in the values of exports can be calculated.

4.2 Welfare Effect

In the GTAP model, measurement of economic welfare depends on a household’s own consumption expenditure, government consumption expenditure (government spending on public goods and services), and the net national savings that will benefit future consumption. Any distortion in the model has an effect on these variables and thus affects the economic welfare of a region. Estimation of the GTAP model provides the regional equivalent variation (EV) measure in monetary terms, which represents the welfare effect in this model.

From a household point of view, the GTAP model measures the cost to the household of the same bundle of goods, before and after a given policy shock. In other words, it is the difference between the expenditure required to obtain the new level of utility at initial prices and the initial expenditure. The regional household utility level depends on the per capita household consumption, per capita government expenditure, and per capita savings. Any change in this aggregate utility level provides the welfare effect of this model.

In other words, welfare change in the GTAP model is measured by a change in the aggregate utility, due to any distortion, specified over per capita private household consumption, per capita government expenditure, and per capita savings. The calculation of EV provides the value of the same percentage change in the level of utility in terms of money value. Let us consider two policy options, the existing one with prices p 0 and income m 0 and a policy shock with price p 1 and income m 1; then the equivalent variation can be expressed as:

where μ(q; p, m), called the money metric indirect utility function, measures how much income the consumer would need at price q to be as well off as he or she would by facing price p and having income m. McDougall (2001) obtained the EV associated with a perturbation to the GTAP model (see Chap. 8 for details on GTAP methodology and welfare effect).

4.3 Terms of Trade Effect

Terms of trade in a region are defined as the ratio of the price index received for tradable goods produced in region r (PSW) compared to the price index paid for tradable goods used in the same region (PDW). This measure in the GTAP model includes the sales of net investments to the global bank and purchases of savings from the global bank. Equation (10.5) shows the percentage change in terms of trade (tot) as the difference between percentage change in PSW and PDW.

Further, the trade balance of any region is defined as the difference between exports and imports. The variable defined in Eq. (10.6) is the change in the trade balance, which represents changes in the current accounts of each region:

where VXWREG is the value of exports from region r evaluated at fob prices and VIWREG is the value of imports in region r evaluated at CIF prices; vxwreg and viwreg are the percentage changes in the actual variables.

5 GTAP Simulation Results

In this section, the results of changes in imports and exports, welfare, and terms of trade have been compared for both models. By looking at EV for India in Table 10.10, in FTA with the GCC, the value of EV is found to be negative under the framework of both the level duty and zero duty models. However, although India’s EV in model II is negative, the loss in model II is less than expected under model I. However, for the GCC, a positive EV has been observed under both models. A positive EV reflects the welfare gain while the negative value indicates a welfare loss. We may conclude that Indian welfare will deteriorate while the GCC countries’ welfare will improve because of the India–GCC trade agreement. The model II of zero duty must be preferred, under which the loss of India is less and the gain of welfare for the GCC countries is higher.

Further, to analyze the causes of expected loss and gains to India and the GCC countries, the components of EV have been reported in Table 10.10. Among three components, namely, allocative efficiency gains, terms of trade gains (current account), and investment saving (capital account) gains, the latter two components are negative for India under model I. However, under model II, terms of trade become unfavorable to India while favorable to the GCC countries after the agreement becomes effective.

The product market efficiency will improve while the factor market efficiency will remain stagnant for India. For the GCC countries, the product market efficiency will improve while the factor market allocative efficiency will deteriorate little bit. An improvement in the allocative efficiency in the product market will signify that the products will be available in both countries at cheaper rates while the factor prices will increase a little bit in the GCC countries which will adversely affect the allocative efficiency of these countries in the factor market.

In sum, the major cause of welfare loss to India under the India–GCC agreement seems to be unfavorable/deteriorated terms of trade. To analyze the causes of deterioration in terms of trade, we need to analyze the impact of said trade agreement on India–GCC imports and exports; unfavorable terms of trade may be noticed either because of lower exports or higher imports. In both models, India tends to import more from the GCC after the trade agreement is in effect. Table 10.11 provides this change: the value of Indian imports will rise on entering into the FTA with the GCC, as per both models, and also in all sectors.

In model II, India’s total imports will increase more than in model I. The expected increase of imports for India from the GCC in model I is US$ 4577.89 million (i.e., US$ 235,426.53 million – US$ 230,848.11 million), while in model II it is US$ 9988.41 million (i.e., US$ 240,836.52 million – US$ 230,848.11 million). However, for the GCC countries, the expected increase in imports is US$ 1365.81 million under model I in comparison to US$ 3718.66 million in model II. The highlight products in the Indian import bill from the GCC group include HS-27 and Other Services. By looking at the distribution of all products, the condition of India’s FTA with the GCC following model II seems better as compared to model I.

From Table 10.12, it can be observed that Indian exports under the FTA with the GCC will reach US$ 226,114.94 million under model I, while the same figure will be US$ 231,188.58 million under model II when tariffs are reduced to zero. Thus, in reducing duty to a zero level, the increase in Indian exports to the GCC will be higher to a level of US$ 5073.64 million. Consequently, model II is a better choice for Indian planners to gain from an India–GCC free trade agreement.

Further, if the gains in imports and exports are compared, the Indian imports will increase at higher rate (US$ 9988.41 million) than its exports (US$ 9368.25 million) and, therefore, will adversely affect the terms of trade. In the case of the GCC countries, a gain in exports (US$ 9152.86 million) is higher than the gain in imports (US$ 3718.66 million), thus the terms of trade will be positively affected for the GCC nations. Therefore, it may be inferred that the unfavorable terms of trade between India and the GCC nations after the trade agreement is in effect will be noticed because of the higher growth of Indian imports than the growth rate of Indian exports to the GCC nations. Consequently, the welfare loss will occur to India. The converse argument is valid for the GCC nations to whom the welfare gain will be noticed because of more favorable terms of trade with India.

6 Concluding Remarks

The aim of this study was to work out the possible gains from an India–GCC free trade agreement that has been signed by these two regions but is still not in effect. Some trade indices such as RCA and TII in the GCC trade with India have been provided to substantiate the argument in favor of present study. The composition of commodities in the GCC trade with India have been constructed to highlight important products. The degree of protection in India–GCC trade has been discussed in terms of tariff rates levied by both sides in all sectors.

After studying the GCC trade and tariff profile with India, two models have been simulated. Firstly, the countries are assumed to impose equal duties, so that there will be zero variation in duties among the partner countries. Secondly, the partner countries are assumed to reduce the duties up to a zero level, that is, a free trade area will be established among partner nations.

From comparison of the two models, it appears that model II (i.e., the zero duty model) is the better option under which an Indian loss is minimum and a gain by the GCC group of countries is higher. Indian trade will surely be enhanced by the agreement, but Indian imports are expected to increase at a higher rate than its exports. Thus, the agreement will adversely affect Indian terms of trade with the GCC countries. The adverse effect on terms of trade will be reflected in welfare changes that appear to be negative for India.

However, affiliates of the GCC group are found to be the beneficiaries of the FTA under evaluation. The exports of these countries are found to be increasing at a higher rate than their imports. Thus, the terms of trade effect will be positive and favorable to the GCC countries. The favorable terms of trade effect has been reflected in the positive welfare gain to these nations. Thus, it may be inferred that zero duty trade agreement is better for partner countries of the India–GCC trade agreement. The expected gains to the GCC countries are high while the gains to India are only in terms of allocative efficiency in the product market. The share of India will increase marginally in world trade but the adverse impact on its welfare, deterioration in its current account, and so on, are the grey areas of the India–GCC free trade agreement. Indian policy planners are advised to work out suitable policy packages so that the growth of exports under such an agreement may surpass the growth of imports and so that a favorable effect of such an agreement on current accounts may be generated.

References

Arora, R., Singh, S., & Mathur, S. K. (2015). Assessment of the proposed India-China Free Trade Agreement: A general equilibrium approach. Journal of Centrum Cathedra, 8(2), 81–108. https://doi.org/10.1108/JCC-08-02-2015-B002

McDougall, R. (2001). A new regional household demand system for GTAP. Revised in 2003. GTAP technical paper no. 20, Purdue University.

Author information

Authors and Affiliations

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2017 The Author(s)

About this chapter

Cite this chapter

Arora, N., Mohajeri, P. (2017). Gains from the India–GCC Free Trade Agreement: A General Equilibrium Analysis. In: Mathur, S., Arora, R., Singh, S. (eds) Theorizing International Trade. Palgrave Macmillan, Singapore. https://doi.org/10.1007/978-981-10-1759-9_10

Download citation

DOI: https://doi.org/10.1007/978-981-10-1759-9_10

Published:

Publisher Name: Palgrave Macmillan, Singapore

Print ISBN: 978-981-10-1758-2

Online ISBN: 978-981-10-1759-9

eBook Packages: Economics and FinanceEconomics and Finance (R0)