Abstract

In a seminal article, Levine et al. (2000) provide cross-sectional evidence showing that financial development has positive average impact on long-run growth, using a sample of 71 countries. We argue that the evidence is sensitive to the presence of outliers.

Access provided by Autonomous University of Puebla. Download chapter PDF

Similar content being viewed by others

Introduction

The effect of financial development on long-run GDP growth is a long-memory controversial issue in economics. As noted by Levine (2003), the issue seems to divide economists in two groups. On the one side, there are those who argue, following Schumpeter (1912), that financial development accelerates growth. On the other side, there are those who maintain, following Robinson (1952), that financial development simply follows growth. The same type of disagreement seems to divide the opinions of two recent Nobel laureates. Indeed, while Miller (1998) considers that “financial markets contribute to economic growth in a proportion that is almost too obvious for serious discussion”, Lucas (1988) points out that “the importance of financial matters is very badly over-stressed”.

This brief introduction helps to show that the topic of the link between finance and growth is mainly an empirical issue related to the estimation of the causal impact of financial development on real growth. In this manuscript, we focus on the cross-sectional evidence provided by Levine et al. (2000).

Using indicator-variables on the legal origin of the countries in their sample as reported by La Porta et al. (1998), Levine et al. (2000) measure the causal impact of financial development on the mean of the conditional growth distribution, finding evidence of positive impact. Although the authors perform an outliers’ sensitivity analysis and argue in favour of the robustness of their results, Levine et al. (2000) do not use a median-regression technique to identify potential outliers. We do exactly the latter and find that the mean-based results provided by Levine et al. (2000) are not entirely robust to the presence of outliers.

Empirical strategy

The data-set explored in this paper can be downloaded from the website of Ross Levine, at: http://www.econ.brown.edu/fac/Ross{_}Levine/IndexLevine.htm. The sample descriptive statistics are reported by Levine et al. (2000, p. 68)Footnote 1. The sample has a cross-sectional dimension and contains detailed information on 71 countries over the 1960–1995 period.

Levine et al. (2000, henceforth LLB) use three indicators of financial development: PRIVATE CREDIT, i.e. credit by deposit money banks and other financial institutions to private sector divided by GDP; COMMERCIAL-CENTRAL BANK, i.e. assets of deposit money banks divided by assets of deposit money banks plus central bank assets; and finally LIQUID LIABILITIES, i.e. liquid liabilities of the financial system (currency plus demand and interest-bearing liabilities of banks and non-banks financial intermediaries) divided by GDP.

LLB distinguish among three types of conditioning sets: the simple conditioning set, including the average number of schooling years in 1960 and the level of GDP in 1960; the policy conditioning set, which extends the simple conditioning set by considering measures of government size, inflation, black market premium, openness of trade; and the full conditioning set which, in turn, extends the policy conditioning set by adding indicators of revolutions and coups, political assassinations, and ethnic diversity.

Using the generalized method of moments (GMM), LLB estimate an empirical model of the following type:

where G represents the average growth rate of real GDP per-capita in country i = 1, …, 71 from 1960 to 1995, F is an indicator of financial development of type j (one of the three previously described indicators), X is a conditioning set of type h (one of the three previously described conditioning sets), and β1 is the main parameter of interest.

The first-stage regression results are based on a regression model of the following type:

where Z is a set of legal-origin dummies playing the role of instrumental variables for financial development (the Scandinavian origin is the excluded category).

To re-evaluate the empirical findings by LLB, we first try to replicate their results using a two-step efficient GMM estimator. Afterwards, we look for potential outliers by using a median-regression technique. Specifically, we keep the issue of the endogeneity of F into account by implementing the procedure suggested by Arias et al. (2001), which is an instrumental-variable technique for quantile regression (IVQR) and consists of two stages. In the first stage, we run an ordinary-least-squares estimation of model (2) and obtain predicted values of F which are used for replacing actual values of F in model (1). In the second stage, we run a quantile-regression estimation of model (1), using the quantile-regression estimator of Koenker and Bassett (1978). Since our interest is the median impact, we focus on the fifth decile (IVQR5).

Note that the quantile-regression estimator of Koenker and Bassett (1978) is highly robust to the presence of extreme values of the dependent variable (Buchinsky, 1994, p. 411). As we will see in the next section, this feature turns out to be useful for the identification of potential outliers. Further, note that, by running (in the second stage) a simple ordinary-least-squares estimation of model (1) rather than a quantile regression, one obtains a standard two-stage-least-squares (2SLS) estimate of β1, measuring the mean impact of F on G. We present both IVQR5 and 2SLS estimates.

Estimation Results

First of all, it is worth stressing that we are able to perfectly replicate the findings of LLB on p. 43, related to model (2).

Table 6.1 presents our main estimation results, related to model (1). The first four columns compare the GMM estimates provided by LLB, and reported in Column 1, with our GMM (replication exercise), 2SLS and IVQR5 estimates. The last four columns focus on the outliers’ sensitivity analysis, performed using the GMM estimator.

Column 2 vs. Column 1

Unlike model (2), we are not able to perfectly replicate the GMM resultsFootnote 2 reported by LLB on p. 46. However, the only relevant difference concerns with the coefficient of the variable COMMERCIAL-CENTRAL BANK (say CCB), in the group of results that are related to the policy conditioning set. Specifically, LLB claim that the coefficient of CCB is statistically significant at 5% level while we find that this coefficient is not statistically significant (p-value 0.160). Nevertheless, as one can see by comparing Column 1 and Column 2, our replication exercise confirms the results presented by LLB.

Column 3 vs. Column 1

Interestingly, we find that the 2SLS estimates, focusing on the impact of F on the conditional mean of G (likewise the GMM estimator), are consistent with the GMM findings obtained by LLB, even for the above-referred case of the CCB coefficient.

Column 4 vs. Column 1

In contrast to the GMM and 2SLS findings, the IVQR5 estimation provides a different picture of the causal nexus between financial development and growth. Particularly, six out of the nine estimated coefficients are not statistically significant at 5% levelFootnote 3, thus suggesting that the median impact of financial development on growth is doubtful.

In addition, the results on the median impact seem to be at odds with the evidence on the mean impact provided by LLB (and confirmed by our replication analysis). Particularly, since our median-based estimator is not sensitive to the presence of extreme values of the dependent variable, the natural step onwards consists of checking whether the mean-based results by LLB are driven by the existence of countries with extreme values of growth.

Column 5 vs. Column 1

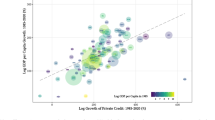

We test the extreme-values’ hypothesis by running a two-step efficient GMM estimation of model (1) and using a sample that excludes those countries whose growth rates are higher than 6%, as suggested by the box-plot in Fig. 6.1. These countries are Korea, Malta and Taiwan (the box-plot seems to indicate that there are only two very high-growth countries, but they are actually three because two points are overlapping; see Table 6.2). Specifically, the fifth column in Table 6.1 reports that none out of the nine estimated coefficients is statistically significant at 5% level, with only one being significant at 10% level. All the coefficients have the expected positive sign but their magnitude is lower than suggested by LLB. Therefore, the cross-sectional evidence on the average positive impact of financial development on real GDP growth disappears if three very high-growth countries are removed from the LLB sample.

Box-plot of the growth distribution

Column 6 vs. Column 1

Since Fig. 6.1 also indicates the existence of two (overlapping) extremely-low values of growth (see Table 6.2), we perform a further GMM estimation by excluding those countries whose growth rates are lower than − 2%, i.e. Zaire and Niger. In this case, however, the estimation results, presented in the sixth column of Table 6.1, are roughly consistent with those proposed by LLB.

Column 7 vs. Column 1

As an additional robustness check, to deeper inspect the results presented in Column 5, we run a GMM estimation using a sample that excludes the country with the highest growth rate, i.e. Korea. The seventh column in Table 6.1 shows that the cross-sectional evidence on the causality between finance and growth becomes mixed. On the one hand, the results based on the simple conditioning set are in line with those provided by LLB. On the other hand, if the conditioning set is extended (see policy and full conditioning), the results point against a causal positive average impact of financial development on growth because only one out of six coefficients is significant at 5% level.

Column 8 vs. Column 1

As a final check, we perform a further GMM estimation using a sample that excludes the two countries with the highest growth rates, i.e. Korea and Malta. Again, the results point against the LLB findings because only three out of nine coefficients are found to be significant at 5% level. The results are very similar to those obtained when just Korea is removed from the sample (Column 7).

Conclusions

This paper provides four main results. First, the cross-sectional evidence due to LLB is replicable. Second, there is preliminary evidence that financial development does not affect the median of the conditional long-run growth distribution. Third, if three very high-growth countries are removed from the LLB sample (Korea, Malta and Taiwan), the evidence that financial development has average positive causal effect on growth disappears. Fourth, if the country with the highest growth rate is removed from the sample (Korea), the evidence becomes mixed. Summing up, the cross-sectional results provided by LLB are sensitive to the presence of outliers (with Korea playing a fundamental role).

Notes

- 1.

We perfectly replicate the sample descriptive statistics.

- 2.

As already mentioned, we use a two-step efficient GMM estimator, selected (among the existing types of GMM estimators) for being the one that, after repeated replication attempts, provides the closest estimates to those presented by LLB. It is worth stressing that LLB do not clearly report which type of GMM estimator is used in their cross-sectional analysis.

- 3.

The standard errors are bootstrapped.

References

Arias O, Hallock KF, and Sosa-Escudero W (2001) Individual Heterogeneity in the Returns to Schooling: Instrumental Variables Quantile Regression Using Twins Data. Empir Econ 26:7–40

Buchinsky M (1994) Changes in the U.S. Wage Structure 1963–1987: Application of Quantile Regression. Econometrica 62:405–458

Koenker R, and Bassett G (1978) Regression Quantiles. Econometrica 46:33–50

La Porta R, Lopez de Silanes F, Shleifer A et al. (1998) Law and Finance. J Polit Econ 106:1113–1155

Levine R (2003) More on Finance and Growth: More Finance, More Growth? Federal Reserve Bank of St. Luis Review 85:31–46

Levine R, Loayza N, and Beck T (2000) Financial Intermediation and Growth: Causality and Causes. J Monetary Econ 46:31–77

Lucas RE Jr (1988) On the Mechanics of Economic Development. J Monetary Econ 22:3–42

Miller MH (1998) Financial Markets and Economic Growth. J Appl Corporate Finance 11:8–15

Robinson J (1952) The Interest Rate and Other Essays. Macmillan, London

Schumpeter J (1912) Theorie der Wirtschaftlichen Entwicklung. Duncker & Humblot, Leipzig

Acknowledgements

Financial support from the FCT-Portugal is gratefully acknowledged. For useful comments and discussions, the author would like to thank Monica Andini, Santiago Budría, Ricardo Cabral, Günther Lang, Marco Pagano, Pedro Telhado Pereira, and the participants at “The Economics of Imperfect Markets” conference (Rome, 16–17 May 2008). The usual disclaimer applies.

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2010 Springer Physica-Verlag Berlin Heidelberg

About this chapter

Cite this chapter

Andini, C. (2010). Financial Development and Long-Run Growth: Cross-Sectional Evidence Revised. In: Calcagnini, G., Saltari, E. (eds) The Economics of Imperfect Markets. Contributions to Economics. Physica-Verlag HD. https://doi.org/10.1007/978-3-7908-2131-4_6

Download citation

DOI: https://doi.org/10.1007/978-3-7908-2131-4_6

Published:

Publisher Name: Physica-Verlag HD

Print ISBN: 978-3-7908-2130-7

Online ISBN: 978-3-7908-2131-4

eBook Packages: Business and EconomicsEconomics and Finance (R0)