Abstract

Financial development as a concept is multifaceted with no clear measurement or definition. Inference via individual proxies may result in an incomplete understanding of the relationship between financial development and economic growth, since sole proxies are unlikely to capture the true capacity of financial development. To address this issue, this paper utilizes a multiple indicators multiple causes (MIMIC) model to create a more complete measure of financial development. In doing this, we treat banking sector and stock market developments as two latent indicators of financial development and use the MIMIC model to predict them which are used as their proxies. Using data from 101 countries over the period 1990–2014, we use the predicted values of the two latent variables as regressors, among other controls, in the growth regression. We find a robust negative relationship between banking sector development and economic growth, whereas the effect of stock market development on economic growth is positive up to a threshold after which the effect becomes negative.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

The role of financial development on economic growth is a widely researched area in the endogenous growth literature. Levine (2005) advocated that financial systems facilitate economic growth through five core functions by: (1) easing the exchange of goods and services through the provision of financial payments, (2) pooling and mobilizing savings from investors, (3) collecting ex-ante information about future investments and allocating capital, (4) monitoring investments and carrying out corporate governance and (5) facilitating trading, diversification and the management of risk. However, both theoretical and empirical research disputed the relative merits of financial development on economic growth. Miller (1998), for example, recommended that the issue is too obvious to even consider, and Lucas (1988) opined that the role of financial systems is overstated. Recent empirical studies have also emphasized on the vanishing effect of financial depth on economic growth (Demetriades and Law 2006; Rousseau and Wachtel 2002, 2011).Footnote 1

Two broad views, namely the banking sector and the stock market development, were considered while analyzing the role of financial development on growth. Even with this classification, ambiguity persists with regard to the merits of banks and stock markets: whether their role should be viewed as substitutes/complimentary or one is superior to the other in promoting economic growth [see Stiglitz (1985), Bencivenga and Smith (1991) and Stulz (2002) on superiority of the role of banking sector; Jansen and Murphy (1990), Boot and Thakor (1997) and Boyd and Smith (1998) otherwise]. Merton and Bodie (1995) and Levine (1997) postulated that neither the banking sector nor the stock market is central to economic growth-rather the delivery of an environment matters where financial services can be effectively provided. This concept is supported by La Porta et al. (1998) along with the importance of the legal heritage in defining a growth-promoting financial environment. Therefore, the theoretical arguments suggested by advocates of financial development can be presented in terms of four competing theories, viz., the bank-based view, the market-based view, the financial services view and the law and finance view.Footnote 2

Given the lack of consensus on the finance–growth nexus theoretically, the question still remains on the role of financial development in promoting economic growth empirically, although there are a plethora of studies in the literature. Based on a cross-sectional data for 80 countries and using liquid liabilities as a ratio to GDP and gross claims on the private sector as a ratio to GDP (banking sector depth), King and Levine (1993) found a positive and statistically significant effect in the growth regression. Levine and Zervos (1998) included both bank and stock market development and documented that both banking sector development and stock market development (in the form of stock market efficiency but not the size of the market) affected economic growth. Levine et al. (2000) and Beck et al. (2000) provided more evidence in this direction using different types of instruments, panel data and econometric techniques, to identify the presence of a causal relationship going from finance to growth.

Researchers also questioned the robustness of the finance–growth relationship. Rodrik (2008) and Rodrik and Subramanian (2009) emphasized on the over-importance of the role of finance in economic development. Arestis and Demetriades (1997) and Arestis et al. (2001) documented the importance of institutional factors and criticized the one-size-fits-all nature of cross-sectional exercises. The role of institutional factors was also emphasized by Demetriades and Law (2006) who showed that financial depth does not affect growth in countries with poor institutions. Rousseau and Wachtel (2002) found the absence of finance–growth nexus in countries with double-digit inflation, whereas Rousseau and Wachtel (2011) found a vanishing effect of financial depth. They found that credit to the private sector does not have a statistically significant impact on GDP growth. Rioja and Valev (2004), using private credit as a ratio to GDP and liquid liabilities as a ratio to GDP for banking sector development, found that the differential effect of financial development on economic growth depends on income levels—the strongest results are found in middle-income economies, but these results become weaker for high-income economics.

The differential impact of financial development in the finance–growth relationship was addressed by Loayza and Ranciere (2006) using a panel autoregressive distributed lag model and mean-group (pooled mean-group) estimator developed by Pesaran and Smith (1995) and Pesaran et al. (1999). Their results (mean-group estimator) showed that financial intermediation exerts positive effects on economic growth in the long run. However, the short-run parameters that are not restricted to be the same across countries indicated a negative relationship between financial intermediation and economic growth.

Demirgüç-Kunt et al. (2011) suggested that the relationship between financial development and economic growth is more complex than first perceived and the relationship between the two differs across income levels of countries. Arcand et al. (2012) found evidence to support the non-monotone nature of the relationship between banking sector depth and economic growth. They argued that the marginal effects of banking sector depth are in fact negative when credit enters and exceeds the range of 80–100% of private credit as a ratio of GDP. The non-monotone nature was documented by Cecchetti and Kharroubi (2012) while analyzing the impact of private sector credit to GDP on growth rate of GDP per worker.

From the above empirical literature, it is clear that emphasis was placed on the use of a single indicator—either the banking sector development or the stock market development. The result varied depending on the sample of countries, the indicators being used to measure banking sector (stock market) development and also on the estimation methodology. However, financial development is a multifaceted concept that encapsulates various functions. Čihák et al. (2012) argued that banking sector and stock market development can be examined via four principle variables: depth, efficiency, stability and access. Furthermore, Demirgüç-Kunt and Levine (2008) stressed on the complexity of financial development and suggested that the empirical studies may have inadequately captured the true capacity of financial systems in their ability to provide financial services.

We contribute in the existing literature in two ways: first we model financial development as a multifaceted concept. Since there is no obvious and universally accepted measure of financial development, we view it as a latent variable. Specifically, we consider banking sector and stock market developments as two latent variables that are used as measures of financial development. Instead of using observed indicators of financial development as proxy variables in the growth regression, we use the multiple indicators multiple causes (MIMIC) model to construct indices of financial development (banking sector and stock market developments). Use of several indicators to construct indices of financial development via the MIMIC model is, in our view, a better way to address the problem.Footnote 3 The advantage of the MIMIC model is that it gives us information on how the observed indicators and the causal variables are related to the latent indicators of financial development. Furthermore, the predicted values of the latent variables can be viewed as indices of financial development. Thus, construction of financial development indices via the MIMIC model is our first contribution to the existing literature.

In the MIMIC model, we use either private credit as a ratio of GDP or liquid liabilities as a ratio to GDP (proxy for banking sector depth) along with net interest margin (proxy for banking sector efficiency) to construct the latent variable representing banking sector development. We use stock market capitalization as a ratio of GDP (proxy for stock market depth) and the turnover ratio (proxy for stock market efficiency) to construct the latent variable representing stock market development. In our framework, we model the latent variables as functions of ‘causal variables’ such as growth in per capita GDP, trade as a ratio of GDP, net FDI inflow as a ratio to GDP. Using the constructed indices as measures of financial development, we then analyze the impact of financial development on economic growth by using them in the growth regression along with other control variables. Here, we exploit both country heterogeneity and endogeneity of financial development indicators. In particular, we employ the system generalized method of moments (GMM) estimator of Arellano and Bover (1995) and Blundell and Bond (1998) in the dynamic panel context. This is our second contribution in the existing literature.

Using data from 101 countries during the period 1990–2014, we find ample support to indicate the negative relationship between banking sector development and economic growth. Our results show that banking sector development exerts a negative and significant impact on growth. The effect of stock market development on economic growth is nonlinear. It impacts on economic growth positively but only up to a threshold after which the effect of stock market development becomes negative. We perform various robustness exercises to validate the obtained results.

The rest of the paper is organized as follows: Sect. 2 outlines the methodology. The data and empirical results are reported in Sect. 3. Section 4 concludes the paper.

2 Methodology

To examine the issue in question, we use the MIMIC model (also known as the structural equation model, SEM). The MIMIC model can be viewed as a variant of the linear independent structural relationships (LISREL) model of Joreskog and Sorbom (1999a, b) and Bollen (1989). The model was first introduced by Goldberger (1972). To motivate the use of the LISREL model, we argue that financial sector development and stock market development are latent variables which are manifested in various observed indicators. In turn, these indicators are related to a set of observed exogenous factors. In our framework, we consider banking sector development and stock market development as two latent variables. The latent construct for the banking sector development, η1, is linearly related to some observable exogenous variables (x) plus an error term. Similarly, the latent construct for the stock market development, η2, is also linearly related to a set of observable exogenous variables (x) plus an error term. Some or all of these exogenous variables can be common. The latent variables \( \eta_{1} \) and \( \eta_{2} \) determine linearly together with some disturbance terms, a set of observable endogenous indicators (\( y \)). The model can be formally written as

where \( y_{it} \) is a vector of ‘p’ indicators of the latent variables for country i, observed in time t, \( x_{it} \) is a vector of ‘q’ ‘causal’ variables determining \( \eta_{1it} \) and \( \eta_{2it} \) for country i in time period t. The (p × 1) error vector \( \varepsilon_{it} \) constitutes zero mean measurement errors associated with the indicators,\( y_{it} , \) while \( \zeta_{1it} \) and \( \zeta_{2it} \) are zero mean scalar structural errors that capture un-modeled variables affecting \( \eta_{1} \) and \( \eta_{2} \).

The above model is a special case of the LISREL model in which there is no measurement error in the \( x \) variables. We used the standard maximum likelihood method to estimate the model using Stata. After estimating the model parameters, the latent factor scores can be predicted (for example, see Joreskog and Goldberger (1975)). We use these predicted scores to analyze the impact of financial development on economic growth in the next step after controlling for various other growth-determining factors. Specifically, we estimate the following regression:

where git refers to growth in per capita gross domestic product (measured in constant PPP) in country i at time t, yit−1 is the natural logarithm of per capita gross product of country i at time t − 1 (consistent with the β-convergence hypothesis in the growth literature), the predicted latent scores for banking sector development (\( \hat{\eta }_{1it}^{{}} \)) and financial sector development (\( \hat{\eta }_{2it}^{{}} \)) and a set of other control variables (wit) that are consistent with the conditional convergence in the growth literature. In particular, the wit variables include rate of population growth, ratio of savings to GDP, telephone lines per 100 people, inflation, net inflow of foreign direct investment as a proportion to GDP, openness (total trade in goods and services as a ratio to GDP) and percentage of population (out of the total population) residing in rural areas. We estimate Eq. (2) using the system-GMM estimator where we instrument both the predicted latent scores for financial development and lagged per capita income via GMM style instruments.Footnote 4

3 Data and empirical results

We divide this section in several subsections. In the first subsection we introduce the dataset, and in the next subsection we report the descriptive statistics. Section 3 discusses estimation of the latent banking sector and stock market development scores. In Sect. 4, we use these predicted scores to examine its impact on economic growth. Section 5 performs some sensitivity analysis.

3.1 Data

We use the World Bank, ‘Financial Development and Structure Dataset’ as of June 2016.Footnote 5 We supplement this dataset with the World Development Indicators data. Given the data unavailability mainly on banking and stock market development indicators, we restrict our sample from 1990–2014. The data are annual in nature. Our sample consists of 104 countries observed over the period 1990–2014. The latent banking sector development score is estimated by the following two indicators: Private credit issued by deposit money banks and other financial institutions as a ratio to GDP as a measure of depth and the net interest margin as a measure of efficiency. Stock market capitalization as a ratio to GDP and stock market turnover ratio are used as the depth and efficiency indicators to construct the latent stock market development score.Footnote 6 We believe that both latent scores have been caused by growth in per capita GDP at the constant PPP, first-lag of the natural logarithm of level of per capita GDP (at constant PPP), openness (total trade in goods and services as a ratio to GDP), and the level of net inflow of foreign direct investment as a ratio to GDP, which in turn is our causal variable. While many often argue the relationship of financial development that leads toward the enhancement of economic growth, the work of Calderon and Liu (2003) suggests that the relationship between the two is in fact one of a bi-directional relationship thereby suggesting that the influence of growth or the demand for financial services is equally important in the role of financial development. In addition, Do and Levchenko (2004) argue that policies tailored to enhance openness to external trade typically have positive effects on financial development. This view is supported by Hanh (2010) who provide evidence to suggest that the opening up an economy to trade seems to be a precondition to the expansions of financial development within an economy. Existing literature also documented the role of foreign direct investment as an important determinant of both bank and stock market development.

3.2 Empirical results

3.2.1 Descriptive statistics

Indicators of both the banking and stock market sectors are assumed to be observed imperfectly in terms of the indicators. For each sector, one can use different dimensions of observed indicators. Čihák et al. (2012) classified such indicators into four dimensions: depth, efficiency, stability and access.Footnote 7 In our paper, we concentrate mainly on depth and efficiency.Footnote 8 The depth indicator for the banking sector shows more variability compared to the efficiency indicators. For the stock market, the depth indicator captured by market capitalization is higher than that of the value traded but also shares a greater variability.

Table 1 presents the summary statistics of all the indicators, causal and growth-determining variables. The average growth rate in per capita GDP is around 2%, whereas average inflation rate stands at − 4%. The openness variable has an average of 89.68, and the average of net FDI inflow stands at 4.93. About 35% of the total population lives in the rural areas, and about 27% of the population has a fixed telephone lines. Except for growth in per capita GDP, all the other variables are positively skewed and the presence of excess kurtosis is more in the stock market indicators compared to the banking sector indicators.

3.3 Evolution of the used indicators

This subsection describes the evolution of some of the selected indicator of financial development for OECD countries and low-/middle-income countries. For banking sector depth, we use private credit as a ratio to GDP, whereas for stock market, market capitalization is being used as the depth indicator. Figure 1 presents the evolution of depth indicators for OECD and low-/middle-income countries. For the OECD countries, the depth indicator shows a steady increase until 2009 and then showing a dip until 2014. In comparison, the low-/middle-income countries portray a different pattern regarding the banking sector depth indicator showing a continuous rise except a slight fall in 2002 and in 2003. This could be partially due to the rapid growth of pan-African banking (PABs) groups; in between 2006 and 2010, the number of subsidiaries of the seven largest PABs has increased from less than 50 to almost 90 operations (IMF 2015). The stock market depth indicator displays large swings for both the OECD and the low-/middle-income countries. Particular drop in the market capitalization has been observed in 2001–2002 for both the OECD and the low-/middle-income countries. This could be partially due to the dot-com bubble. The stock market depth indicator has again experienced a downward turn in 2007–2008 due to the global financial crisis for both the OECD and low-/middle-income countries and in 2011–2012 for the OECD countries due to the European sovereign debt crisis. The same pattern has also been observed stock market efficiency indicator as captured by turnover ratio (Fig. 2b). In Fig. 2a, we display the efficiency indicator for banking sector and stock market, respectively, using net interest margin as the efficiency indicator for the bank. For the OECD countries, the net interest margin shows a more or less declining trend after 1992 until 2008 and then again from 2012 to 2014. The net interest margin for the low-/middle-income countries displays an increasing trend from 1992 to 1999 and then more or less a downward path. Reduction in interest income on loans could plausibly explain this pattern. No definitive pattern has been observed for the stock market efficiency indicator.

Banking sector and stock market depth indicator. Note: For banking sector depth, we use financial system deposits as a ratio of GDP, whereas for stock market, market capitalization is being used as the depth indicator

a Banking sector efficiency indicator. b Stock market efficiency indicator. Note: For banking sector efficiency, we use net interest margin, whereas for stock market, turnover ratio is being used as the efficiency indicator

3.4 Banking sector and stock market development score

The results of the banking sector and stock market development scores are reported in Table 2. We use a within transformation of the variables to take into account the unobserved heterogeneity (country fixed-effects) and then standardize the variables. One of the indicators (in our case depth) of each construct is normalized to unity for identification purposes.

To account for some of the complexities found in the financial development literature, we disaggregate our sample into two subsamples. It is argued in the literature that as economies develop the relative structure of banking sector and stock markets changes (see Boyd and Smith 1998). Therefore, it is important to accommodate this relationship across various income groups.Footnote 9 Regarding banking sector development, we observe that the net interest margin is statistically significant in all income groups and exerts a negative effect on banking sector development. The net interest margin reflects the total interest gained relative to interest paid out on banks liabilities. As such, if a greater net interest is acquired by banks this may reflect a reduction in overall competition within the banking sector. Thus, what is good for one bank may not be good for the banking sector as a whole. This is supported by the recent work of Saksonova (2014) who suggests that a declining net interest margin can be seen as a positive development as it suggests greater efficiency of the banking system in redistributing resources. In addition, a net interest margin can decline due to greater competition or financial and technological innovations. Looking at the causal variables, we note that all variables are statistically significant across all subsections and are of same sign apart from foreign direct investment in the high-income group. Most notably, economic growth exerts a negative impact on banking sector development. Perhaps the impact captures the effect of economic growth on net interest rate margin. In good economic conditions, domestic banks tend to increase deposit rates to attract more deposits in order to boost their lending capacity. At the same time, they may charge lower rates to loans, since during good economic conditions credit risks are generally lower.

Looking at the latent construct for stock market development, we find that our measure for stock market efficiency (turnover ratio) is less robust across subsamples than its counterpart for banks. The turnover ratio is statistically significant for both the full sample and the high-income sample, and it exerts positive effect. The turnover ratio reflects the total number of shares traded relative to the average number of shares outstanding. Therefore, high turnover ratio shows strong liquidity in the market and low transaction costs and consequently high efficiency of the market and therefore greater stock market development. However, if the stock market becomes too large and too liquid, they exert a negative impact on the financial system.Footnote 10 We observe that the relationship between growth and stock market development is in fact positive and statistically significant. Furthermore, we find that the effects of foreign direct investment are consistently positive and statistically significant across all sample groups which is supported by Claessens et al. (2001).

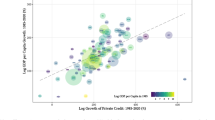

In ‘Appendix 1,’ we display the scatter plots along with the correlation coefficient between the predicted latent construct for the banking sector and stock market development for model 2 and model 3. We observe in both cases the correlation coefficient is positive, although the correlation decreases when we add stability measure of banking sector development and stock market while constructing latent construct.

Table 2 also reports the estimated residual variances and the diagnostics statistics. We observe that our model for the ‘high-income’ countries did not perform well according to the RMSEA statistic, but it shows good fit for the other two samples of countries. Although not reported, we allowed indicators representing banking sector and stock market development to be correlated. We observe that for full sample and sample representing low- and middle-income countries, the bank depth and stock market depth variables are positively and significantly correlated. Although the correlation coefficient between bank depth and stock market depth variable is positive, it is found not significant for high-income country sample.

We examine the sensitivity of our analysis by using different variables to construct the latent index for banking sector and stock market development. Table 3 reports our results. Here for banking sector depth, we use three variables, namely financial system deposits as a ratio of GDP, private credit by deposits money banks and others as a ratio of GDP and liquid liabilities as a ratio of GDP. We also introduce bank stability measure proxied by the z-score where we use volatility as the proxy for stock market stability. As before, we use net interest margin as banking sector efficiency measure, whereas for stock market efficiency we use turnover. We also altered the measure of efficiency indicator for banking sector where instead of using net interest margin we used bank overhead costs as a ratio of total assets.Footnote 11 Our results in terms of the variables that we used in Table 2 remain qualitatively the same. We observe that different banking depth measures are related to each other positively. Bank stability measure is never significant, whereas the stock market stability measure is negative and always significant.

Table 4 reports the results for our growth regression using latent constructs from Table 2 and Table 3 for the full sample, high-income and middle-/low-income groups. Consistent with the previous literature, we allow for non-monotonic relationship between growth and banking sector development latent construct. We differ from the existing studies, however, by including the non-monotonic relationship between growth and stock market development latent construct. We also control for several variables following the previous literature in the growth determinant regression. These are: growth rate of population, savings to GDP ratio, inflation, trade openness, foreign direct investment/GDP, fixed telephone lines per 100 people and rural population. Finally, we include time dummies to take into account the impact of aggregate macroeconomic shocks.

We observe across all estimates (columns 1–6), using the predicted latent scores from Table 2 and 3, that the linear effects of banking sector development are negative and statistically significant. In comparison, we find equally consistent findings of stock market development, where the linear effect is in fact positive. For the quadratic latent scores, banking sector development is positive but insignificant across all estimates barring column (3). However, for the stock market development scores, the coefficient is negative and significant. These findings are consistent for the high-income countries. For the middle-/low-income samples in columns (3) and (6), we find negative but insignificant effect. In general, the positive effect of stock market development on economic growth may hold up to a threshold as the quadratic term is negative and statistically significant. The inverted U-shaped relationship depicts that the benefits gained from stock market development (i.e., the enhancement of mainly stock market depth and efficiency) are only beneficial to economic growth up to a certain limit and thereafter becomes negative, especially for high-income economies. Thus, if stock market grows too high and become too liquid, it would have a negative impact on the financial system via decreasing corporate governance as feared by Stiglitz (1985) and Bhide (1993). The recent global financial crisis has also raised concerns regarding the size of financial systems compared to the size of the domestic economy. Rajan (2005) was concerned about the dangers of financial development and suggested that the presence of a large and complicated financial system increased the chance of a ‘catastrophic meltdown.’ Easterly et al. (2000) also documented the presence of a non-monotone relationship between financial depth and volatility of output growth.

Regarding the latent construct of the banking sector, we provide a number of reasons for the negative relationship between banking sector development and economic growth, which is inconsistent with previous studies. First, many of the aforementioned studies test the causal relationship between banking sector development and economic growth via a single indicator. However, as previously argued the concept of development is unlikely to be a single facet. As stated by Demirguc-Kunt and Levine (2001), the previous indicators used to model the role of financial development may not satisfactorily capture the role of banks and markets. In this context, Harrison et al. (1999) found that the net interest margin exerts negative effects upon economic growth. Therefore, our findings could be attributed to the use of broader indicator of banking sector development.

Second, King and Levine (1993), Levine and Zervos (1998) and Beck and Levine (2004), to name a few, found the coefficients associated with banking sector development variable are positive and statistically significant across earlier sample periods. However, the more recent work of Rousseau and Wachtel (2011) documents the vanishing effect of banking sector depth in which they found the relationship negative and insignificant using more recent data. This argument is further supported by our analysis.

Third, financial sector competes for resources with the rest of the economy not only in acquiring physical capital, but also in getting highly skilled workers. Financial sector was booming at an increasing rate thereby drawing resources at a phenomenal rate causing overinvestment in terms of the formation of too many companies, overinvestment and employment of too many people, a situation similar to that of dot-com bust. According to Tobin (1984), there is a difference between social and private returns of the financial sector: a large financial sector may drive away talents from the productive sectors of the economy and hence turn out to be inefficient from the societal point of view. Fourth, introduction of derivative instruments led to hedging opportunities and perhaps reduced credit quality resulting in increased financial vulnerability. Here, one can potentially examine the role of bank lending versus non-bank lending to ascertain the differential impact on economic growth. Distinction needs to be made whether lending is used to finance investment in productive assets or to feed speculative bubbles (Beck et al. 2008).

In terms of the other variables, we find that the lagged real GDP per capita is negative and statistically significant thus supporting the β-convergence theory. Furthermore, we find that the rate of population growth and the ratio of gross domestic savings to GDP have negative and positive coefficients, respectively, thereby supporting the Solow model. Finally, the impact of net foreign direct investment remains positive and significant for the low-/middle-income countries, although the impact is negative for the high-income countries. Inflation and rural population have the expected signs and are more or less statistically significant. Physical infrastructure captured by telephones lines per 100 people is significant and has a positive coefficient. The coefficient associated with trade openness is positive and significant for the full sample and for the sample of high-income countries.

In sum, our findings conflict with earlier work of and Rousseau and Wachtel (2002) and Beck and Levine (2004) who found positive monotonic effects of banking sector and stock market development on economic growth. Based on our positive and significant finding of the effects of stock market development along with its non-monotonic relationship, we argue that it is important not to overlook the implications of the stock market on economic growth in future works.

3.5 Sensitivity analysis

To examine the robustness of our results we estimate multiple variations of our model to study the strength of the relationship between banking sector and stock market development on economic growth. As such, we examine sensitivity of our findings to variable substitution, sample duration and sub-sampling based on median disaggregation. Table 5 reports these results.

First, we estimate the results in the proceeding section by using several alternative indicators of both banking sector and stock market depth in the estimation of the latent constructs and on growth (based on Table 2). Starting with the of banking sector depth, we estimate all models by using liquid liabilities as a ratio to GDP as an alternative to private credit as a ratio to GDP as in Čihák et al. (2012) and others. Notably, the use of liquid liabilities as an indicator of depth for the banking sector still gives the same significance and sign in the full sample estimate. For the full sample (labeled as 1 in Table 5), we observe marginal changes in the relative effects of financial development on growth, namely, a decrease in the coefficient of the linear term of banking sector development from − 0.076 to − 0.064 and amplification of stock market development coefficient from 0.047 to 0.060.

Second, we test the sensitivity of our results to ensure the qualitative robustness of our estimates, by re-estimating our model using the data from 2001–2014. Here, we experiment with using both private credit and liquid liabilities as measures of banking sector depth. We report the results in Columns 3 and 4 (labeled as 2 and 3) in Table 5 for the full sample. We find that for the full sample the quadratic term of the scores of stock market development is no longer significant.

Third, based on the estimated latent construct for banking sector and stock market development, we divide the countries in two samples: the first sample consists of those countries for which estimated latent construct for banking sector (stock market development) exceeds its median value and the second sample is for those counties for which it is below the median. Columns 4 and 5 report the results where splitting of the sample is based on banking sector development, whereas in columns 6 and 7, we report the same using stock market development splitting. Here, we use private credit as the measure of banking sector depth. Our results remain qualitatively the same except that the quadratic term of the scores of stock market development is no longer significant.

We also conduct a subsample analysis dividing our sample in two subsamples: 1990–2007 and 2008–2014. Our results once again reflect more or less same findings with some exceptions: (a) lagged real GDP per capita although is negative and statistically insignificant for all and for low-/middle-income countries for the 2008–2014 period and (b) square of stock market latent score although negative but not significant for the subsample for all and for low-/middle-income countries.

4 Conclusion

This paper examined the empirical relationship between financial development and economic growth. Many earlier empirical studies, using a single indicator of financial development, concluded that financial development promotes economic growth. In light of the recent financial crisis, the relevance of such a relationship is challenged. As financial systems expand in size and complexity, the use of a single indicator, which is unlikely to capture the true capacity of financial development, is hardly appropriate. Consequently, the use of a single indicator in the growth regression might give wrong results because there is no single universally accepted indicator of financial development. Our paper attempted to overcome such shortcoming by treating the banking sector development and stock market development as two separate latent indicators of financial development. We used a multiple indicators multiple causes model in which the latent variables determined a host of observed indicators such as private credit as a ratio of GDP, net interest margin, stock market capitalization as a ratio of GDP, turnover ratio, etc. On the other hand, the latent variables are also explained by some causal variables such as growth in per capita GDP, trade as a ratio of GDP, net FDI inflow as a ratio to GDP. We first estimated the latent variables and then use their predicted values as regressors, among other controls, in the growth regression using data from 101 countries over the period 1990–2014. We found a robust negative relationship between banking sector development and economic growth. The effect of stock market development on economic growth is positive up to a threshold after which the effect becomes negative.

Our contributions to the literature are as follows. First, our treatment financial sector development in terms of two latent indicators, viz., banking sector and stock market development, is rich and flexible. Our model not only showed how financial indicators affect growth (as done by the traditional models), but also showed how these unobserved indicators are determined and how they affect their observed counterparts. To better understand the relationship between financial development and economic growth, studies should consider both the relationships simultaneously, as we did. Second, from an econometric perspective we provided an alternative to the traditional method and estimate the effects of financial development on growth by using the predicted values of two latent indicators, among other controls, and controlling for endogeneity. To the best of our knowledge, this paper is the first of its kind to test the relationship of financial development and economic growth using the MIMIC methodology. Given our results, we encourage future studies to test the non-monotone relationship of stock markets as well as the banking sector.

In summary, given the negative relationship found between banking sector development and economic growth we argued that financial regulation is required in an attempt to reduce the role on the banking sector, in line with Basel III. Alternatively, we suggested that stock market development should be encouraged yet constraints are advised to stop stock markets becoming too big and too liquid. Otherwise, returns of stock market development at some point would become smaller than the cost of instability (de la Torre et al. (2011)) thereby resulting in the non-monotone relationship even stronger as we obtained.

Notes

Financial depth in general refers using private credit as a fraction of GDP as a measure; but the concept of financial development is much broader (see de la Torre et al. 2011 for details).

For details see Levine (2002).

Differently, Rose and Spiegel (2012) used the MIMIC model to examine the causes and consequences of 2008 financial crisis.

See Čihák et al. (2012) for details and various update of the same data set over the years.

For both banking sector and the stock market, we used different indicators to measure depth and efficiency. The results remain qualitatively similar to those reported in the paper.

For details on these indicators and classification, see Čihák et al. (2012).

The reasons for not including accessibility measure as accessibility are completely different from the other measures that have been used.

These income groups are defined in the World Bank database.

In our sample, around 31% of observations has stock market turnover higher than the overall average, whereas 50% of observations is above the median.

Results are not reported here to save space but are available from the authors upon request.

References

Arcand JL, Berkes E, Panizza U (2012) Too much finance? IMF Working Paper 12/161

Arellano M, Bover O (1995) Another look at the instrumental-variable estimation of error-components models. J Econom 68:29–52

Arestis P, Demetriades P (1997) Financial development and economic growth: assessing the evidence. Econ J 107: 783–799

Arestis P, Demetriades PO, Luintel KB (2001) Financial development and economic growth: the role of stock markets. J Money Credit Bank 33:16–41

Beck T, Levine R (2004) Stock markets, banks, and growth. J Bank Finance 28:423–442

Beck T, Levine R, Loayza N (2000) Finance and the sources of growth. J Financ Econ 58:261–300

Beck T, Buyukkarabacak B, Rioja F, Valev N (2008) Who gets the credit? and does it matter? household vs. firm lending across countries. Policy Research Working Paper Series 4661, The World Bank

Bencivenga V, Smith BD (1991) Financial intermediation and endogenous growth. Rev Econ Stud 58:195–209

Bhide A (1993) The hidden costs of stock market liquidity. J Financ Econ 34:31–51

Blundell R, Bond S (1998) Initial conditions and moment restrictions in dynamic panel data models. J Econom 87:115–143

Bollen KA (1989) Structural equations with latent variables. Wiley, London

Boot AW, Thakor AV (1997) Financial system architecture. Rev Financ Stud 10:693–733

Boyd JH, Smith BD (1998) The evolution of debt and equity markets in economic development. Econ Theor 12:519–560

Calderon C, Liu L (2003) The direction of causality between financial development and economic growth. J Dev Econ 72:321–334

Cecchetti SG, Kharroubi E (2012) Reassessing the impact of finance on growth. BIS working paper number 381

Čihák M, Demirgüç-Kunt A, Feyen E, Levine R (2012) Benchmarking financial development around the World.” World Bank Policy Research Working Paper 6175, World Bank, Washington, DC

Claessens S, Demirgüç-Kunt A, Huizinga H (2001) How does foreign entry affect the domestic banking system? J Bank Finance 25:891–911

de la Torre A, Ize A, Schmukler S (2011) Financial development in Latin America and the Caribbean: the road ahead. The World Bank Latin American and Caribbean Studies

Demetriades P, Law SH (2006) Finance, institutions and economic development. Int J Finance Econ 11:245

Demirgüç-Kunt A, Levine R (2008) Finance, financial sector policies, and long-run growth. World Bank Policy Research Working Paper No. 4469, World Bank, Washington, DC

Demirgüç-Kunt A, Córdova EL, Pería MSM, Woodruff C (2011) Remittances and banking sector breadth and depth: evidence from Mexico. J Dev Econ 95:229–241

Do Q-T, Levchenko AA (2004) Trade and financial development. Policy Research Working Paper Series 3347, The World Bank

Goldberger AS (1972) Structural equations methods in the social sciences. Econometrica 40:979–1001

Hanh PTH (2010) Financial development, financial openness and trade openness: new evidence. FIW working paper no. 60

International Monetary Fund (2015) Pan-African banks: opportunities and challenges for cross-border oversight, prepared by a staff team led by Charles Enoch et al., Washington, D.C., International Monetary Fund

Jansen MC, Murphy KJ (1990) Performance pay and top-management incentives. J Polit Econ 98:717–738

Joreskog KG, Goldberger AS (1975) Estimation of a model with multiple indicators and multiple causes of a single latent variable. J Am Stat Assoc 70:631–639

Joreskog KG, Sorbom D (1999a) LISREL 8: structural equation modeling with the SIMPLIS command language. Scientific Software International, Lincolnwood, p 9

Joreskog KG, Sorbom D (1999b) LISREL 8 user’s reference guide. Scientific Software International, Lincolnwood

King GR, Levine R (1993) Finance and growth: Schumpeter might be right. Q J Econ 108:717–737

La Porta R, Lopez-de-Silanes F, Shleifer A, Vishny RW (1998) Law and finance. J Polit Econ 106:1113–1155

Levine R (1997) Financial development and economic growth: views and agenda. J Econ Lit 35:688–726

Levine R (2002) Bank-based versus market-based financial systems: which is better? J Financ Intermed 11:398–428

Levine R (2005) Finance and growth: theory and evidence, chap 12. In: Aghion P, Durlauf S (eds) Handbook of economic growth, vol 1, vol 1. Elsevier, Amsterdam, pp 865–934

Levine R, Zervos S (1998) Stock markets, banks and economic growth. Am Econ Rev 88:537–558

Levine R, Loayza N, Beck T (2000) Financial intermediation and growth: causality and causes. J Monet Econ 46:31–77

Loayza N, Ranciere R (2006) Financial development, financial fragility and growth. J Money Credit Bank 38:1051–1076

Lucas R (1988) On the mechanics of economic development. J Monet Econ 22:3–42

Merton RC, Bodie Z (1995) A conceptual framework for analysing the financial environment. In: Crane DB et al (eds) The global financial system: a functional perspective. Harvard Business School, Boston

Miller MH (1998) Financial markets and economic growth. J Appl Corp Finance 11:8–14

Pesaran MH, Smith RP (1995) Estimating long-run relationship from dynamic heterogeneous panels. J Econ 68:79–113

Pesaran MH, Shin Y, Smith RP (1999) Pooled mean group estimation of dynamic heterogeneous panels. J Am Stat Assoc 94:621–634

Rajan RG (2005) Has financial development made the world riskier? NBER working paper no. 11728

Rioja F, Valev N (2004) Does one size fit all? An examination of the finance and growth relationship. J Dev Econ 74:429–447

Rodrik D (2008) Second-best institutions. Am Econ Rev 98:100–104

Rodrik D, Subramanian A (2009) Why did financial globalization disappoint? IMF Staff Papers 56:112–138

Rose AK, Spiegel MM (2012) Cross-country causes and consequences of the 2008 crisis: early warning. Jpn World Econ 24:1–16

Rousseau PL, Wachtel P (2002) Inflation thresholds and the finance–growth nexus. J Int Money Finance 21:777–793

Rousseau PL, Watchtel P (2011) What is happening to the impact of financial deepening on economic growth? Econ Inq 49:276–288

Saksonova S (2014) The role of net interest margin in improving banks’ asset structure and assessing the stability and efficiency of their operations. Proc Soc Behav Sci 150:132–141

Stiglitz J (1985) Credit markets and the control of capital. J Money Credit Bank 17:133–152

Stulz R (2002) Financial structure, corporate finance, and economic growth. In: Demirguc-Kunt A, Levine R (eds) Financial structure and economic growth: cross-country comparison of banks, markets and development. MIT Press, Cambridge, pp 143–188

Tobin J (1984) On the efficiency of the financial system. Lloyds Bank Rev 153:1–15

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

We declare that we have no conflict of interest.

Ethical approval

This article does not contain any studies with human participants or animals performed by any of the authors.

Additional information

Publisher’s Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

We would like to thank Bertrand Candelon, Editor-in-Chief and an anonymous referee for helpful comments.

Appendices

Appendix 1

Relationship between banking sector and stock market deveopment predicted latent construct all countries (1990–2014)

Relationship between banking sector and stock market deveopment predicted latent construct all countries (1990–2014)

Appendix 2

See Table 6.

Rights and permissions

About this article

Cite this article

Cave, J., Chaudhuri, K. & Kumbhakar, S.C. Do banking sector and stock market development matter for economic growth?. Empir Econ 59, 1513–1535 (2020). https://doi.org/10.1007/s00181-019-01692-7

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00181-019-01692-7