Abstract

The U.S. electricity market is organized in several deregulated regional markets. In this paper we specify a multi-regime switching model to study price dynamics of electricity in the U.S. markets. Our results show that electricity prices from the West and East coasts have different regime dynamics with the latter prices switching more frequently between regimes. Additionally, our methodology suggests that electricity prices are better parameterized by four regimes: the base regime with low volatility; a spike up and a reverse regime both with high volatility and short duration; finally, a fourth one has extremely high volatility. This latter regime describes West coast prices during the California electricity crisis, but East coast prices are also frequently in that regime. We find evidence of price synchronization in the lowest and highest volatility regimes, i.e., prices from the East and West coasts tend to be in the same regimes at the same time.

Financial support from Fundação para a Ciência e Tecnologia is greatly acknowledged (PTDC/EGE-GES/103223/2008).

Access provided by Autonomous University of Puebla. Download chapter PDF

Similar content being viewed by others

Keywords

1 Introduction

The electricity business activity can be roughly characterized by three sectors: generation, transmission, and distribution, which were usually tied within a utility. Generation is the process of generating electric energy from other forms of energy such as hydro energy, fossil fuels, harnessing wind, solar, or through nuclear fission. After being generated, electricity is distributed through high-voltage, high-capacity transmission lines to local regions, where it is consumed. When the electricity reaches the local destination of consumption, it is transformed into a lower voltage and sent through local distribution wires to end-use consumers.

In the U.S., for many years each of these segments was investor-owned but state-regulated or owned by the local municipality. But the 1980s saw the introduction of a wave of deregulatory reforms that reached the electricity sector. Reforms were implemented with the argument that competitiveness would rise and benefit consumers by lowering prices in both the short and long runs.

The establishment of a competitive wholesale electricity market, i.e., a market where competing agents offer and buy electricity was a key element of the deregulation process. While wholesale pricing used to be of the exclusive domain of large retail suppliers, a market in a competitive framework should open up to new participants such as generators, retailers, or financial intermediaries or end-users. To reach this goal, the Federal Energy Regulatory Commission (FERC), the regulatory agency, introduced rules such open access to transmission service tariffs and on the availability of transmission service of networks. Moreover, transmission owners had to provide access to their networks at cost-based prices to end discriminatory practices against unaffiliated generators.

Market power and the potential upsurge of prices are a major issue in the market design of wholesale markets. As will be explained in more detail below, the physical features of electricity favor imperfect competition, and ultimately deregulation could have adverse effects by increasing prices for end-users. Knittel and Roberts (2005) refer that when regulated prices were set by state public utility commissions in order to curb market power and ensure the solvency of the firm. Price variation was minimal and under the strict control of regulators, who determined prices largely on the basis of average costs. In contrast, a wholesale market is based on competitive bidding of supply and demand, and prices are set by market clearance. Given that electricity demand has frequent fluctuations (e.g., extreme temperatures) and that there are no inventories to buffer shocks, prices would fully absorb shocks. Price jumps and spikes in volatility are then inevitable outcomes that must be monitored. Concerns about market power were substantiated by the California crisis in 2000–2001, when market power and exploitation of market design imperfections caused an explosion in wholesale prices.

The deregulated nature of the U.S. electricity market as well as its fragmented structure with many wholesale markets, makes it an interesting case for analyzing the dynamics of prices after deregulation. The literature comparing U.S. electricity prices in different locations is scant. Hadsell et al. (2004) compare electricity volatility in five regions of the U.S. for the period 1996–2001 using a TARCH model; Park et al. (2006) use a vector autoregressive (VAR) model to analyze spot prices in different parts of the U.S. for the period 1998–2002. They find that electricity markets in the Western U.S. are separated from the Eastern markets at contemporaneous time, but this separation disappears for longer time horizons. The relationships between the markets depend on physical assets (such as transmission lines) and institutional arrangements.

Our study analyzes price dynamics of U.S. regional markets by regime-switching models (RSM). These models, introduced by Hamilton (1989), have been extensively used to model electricity prices as they accommodate well electricity price features such as asymmetric volatility, jumps, and spikes.Footnote 1 The computational burden in model estimation, which increases with the number of time series, observations, and regimes is a hindrance to their empirical application. Our estimation algorithm overcomes these limitations and allows the study of the cyclical behavior of several electricity price time series in a parsimonious way, providing new insights on the existence of common regimes and the synchronization between them. Moreover, this approach recognizes different regime-switching dynamics of electricity prices, so far not addressed in the literature. In addition, the flexible modeling of observed returns using Gaussian mixture distributions makes it more appropriate for non-Gaussian returns (see, e.g., McLachlan and Peel 2000; Dias and Wedel 2004).

To study price dynamics in different regions of the U.S., we take the Dow Jones U.S. Electricity Price Indexes. These price indexes cover several geographical regions of the United States. We conclude that prices in the same U.S. region share the same regime dynamics, i.e., prices of the East (West) coast markets behave similarly. The best model parametrization has four regimes. The extremely high volatility regime describes West Coast prices during the California electricity crisis, but prices of the East coast markets are also frequently in that regime. Regional electricity markets seem to differ in the time spent in each regime. West market prices spend more time in the low volatility regime than East coast markets. Strikingly, the time they spent in the spike regime is similar despite the episode of the California crisis. To address the question of whether prices of the East and West coasts are in the same regime at the same time, we compute synchronization measures between and within regimes. We find evidence of price synchronization in the lowest and highest volatility regimes, i.e., prices from the East and West coasts tend to be in those regimes at the same time.

The rest of the chapter is organized as follows. Section 2 gives an overview of the main changes in the U.S. electricity markets. Section 3 describes the data. Section 4 introduces the econometric methodology. Section 5 presents and discusses the empirical results. Section 6 analyzes the synchronization between the different electricity markets and, finally, Sect. 7 concludes the paper.

2 The Establishment of a Wholesale Market

The deregulation process targeted two key features of the utility sector: monopolies and natural barriers to entry. Joskow (1997) describes that the deregulation process had two main goals. First, to separate the potentially competitive functions of generation and retail from the natural monopoly functions of transmission and distribution. Second, to establish a wholesale electricity market and a retail electricity market.

Ideally, a wholesale market should have a sound free-market base such as competitive supply offers, demand bids and prices set by market-clearance. To achieve this, it urged to push for the breakdown of barriers to entry and attraction of new players into the market. In 1996 a set of measures were implemented to ease entry and enhance competition. For instance, established transmission owners had (i) to provide access to their networks at cost-based prices, (ii) to end discriminatory practices against unaffiliated generators and marketers, (iii) to expand their transmission networks if they did not have the capacity to accommodate requests for transmission service, and (iv) to provide non-discriminatory access to information required by third parties to make effective use of their networks.

These measures were reinforced by the FERC Order 2000 issued in December 1999. This contained a new set of regulations designed to facilitate the “voluntary” creation of large regional transmission organizations to solve problems created by the balkanized control of U.S. transmission networks and alleged discriminatory practices affecting independent generators and energy traders seeking to use the transmission networks of vertically integrated firms.

The particular features of the electricity operations are a hindrance to competition. Monopolies emerge as an outcome of economies of scale of the generation process and the losses from long-distance transmission. To truly compete in the distribution sector, rival firms should duplicate wire networks. However, the duplication of infrastructures is inefficient as there is a need to keep the system adequacy, i.e., the balance between inflow and outflow at all times. The failure to balance leads to the collapse of the grids which has severe economic losses.Footnote 2,Footnote 3.

Market power also arises because of the inelasticity of energy demand. This naturally leads to high prices at peak times as demand rises above the production capacity of generators and further price increases result in little additional supply or reduction of demand. The prices then naturally reflect the scarcity of supply relative to demand.

Given that electricity is not storable, inventories cannot be used to load the grid and smooth prices over time. As a result, deregulated prices are characterized by volatility that varies over time and occasionally reaches extremely high levels, commonly known as “price spikes”.

Market power and imperfect competition have well-known economic implications such as high profits for sellers at the cost of higher prices for consumers contradicting the aims of the deregulation process. Moreover, increased volatility and subsequent losses represent additional risks for market participants which for instance has led to the emergence of power derivatives markets. Market power has other detrimental effects on economic growth because high energy costs imply an increase of costs for firms and price volatility also creates uncertainty which tends to postpone investment decisions.

Finally, market power affects the reliability and credibility of wholesale markets. The California electricity crisis in 2000–2001 is a good illustration of what can go wrong in the deregulation process due to imperfections in the deregulated market. Energy traders created artificial shortages in days of peak demand to increase prices and company profits. The explosion of prices and the rolling blackouts adversely affected many businesses dependent upon a reliable supply of electricity, and inconvenienced a large number of retail consumers.Footnote 4 The California state suffered from multiple large-scale blackouts, and one of the state’s largest energy companies collapsed with harmful economic effects.Footnote 5

3 Data

We use Dow Jones U.S. Electricity Price Indexes to analyze electricity prices in different regions of the U.S. Indexes. These prices cover different regions of the U.S. market, namely the West and East coasts. From the West region, and conditional on data availability, we use California and Oregon Border (COB), Four Corners (Utah, Colorado, New Mexico and Arizona), Mid Columbia (Washington) and Palo Verde (Arizona) prices indexes; from the East region, we use CINERGY (Ohio, Indiana) and PJM (Pennsylvania) interconnection which is the world’s largest competitive wholesale electricity market. These indexes are volume-weighted averages of wholesale electricity transactions and provide a clear spot market indication for over-the-counter trading in that region.

Our sample covers prices from 6th January 1999 through 7th July 2010, for a total of 601 price observations. Prices are weekly, from Wednesdays like Mjelde and Bessler (2009), and in U.S. dollars. Let \( P_{it} \) be the observed weekly closing price of market i on day t, \( i = 1, \ldots ,n \) and \( t = 0, \ldots ,T \). Thus, the weekly rates of return are defined as the log-rate percentage: \( y_{it} = 100 \times \log \left( {P_{it} /P_{i,t - 1} } \right),\;t = 1, \ldots ,T \).

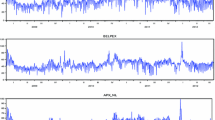

Figure 1 depicts electricity prices for the entire period. Electricity prices show extraordinary volatility during 2000–2001, the period of the California electricity crisis. Prices in the East coast—CINERGY and PJM—also tend to show frequent price spikes.

Dow Jones electricity price indexes

Table 1 summarizes the descriptive statistics for the returns. The mean is positive for all series, except for CINERGY. As expected, electricity returns show high dispersion (standard deviation) and kurtosis. Interestingly, West region prices tend to show positive skewed distributions, whereas East coast series are negatively skewed. The heavy tails and skewness of the distributions turn out to reject the normality for all time series (Jarque Bera test, p-value < 0.001).

The stylized characteristics of these price returns—cyclical behavior, jumps, and spikes—provide ground for applying regime switchings models.

4 Methodology

The methodology applied in this work falls within the regime switching framework. Regime switching models (RSM) have been extensively applied in economics and finance research and the modeling of electricity prices is no exception (see, e.g., Deng 1998; Ethier and Mount 1998). In a meta-analysis of several econometric approaches, Bierbrauer et al. (2007) conclude that a major strength of regime switching models over other econometric models is its flexibility in accommodating extreme observations. In particular, the model allows for consecutive spikes in a very natural way, as well as the switching of prices to the ‘normal’ regime after a spike.Footnote 6 In short, these models are a parsimonious representation the unique characteristics of power prices. Moreover, regimes are able to describe the price jumps caused by different levels of demand and supply (see, e.g., Andreasen and Dahlgren 2006; Bierbrauer et al. 2007; Deng 1998; Ethier and Mount 1998; Huisman and Mahieu 2003; Janczura and Weron 2010, 2012). In particular, they capture specific characteristics such as the spiky and nonlinear behavior of electricity prices (Bierbrauer et al. 2007; Mari 2006; Weron et al. 2004). Thus, the introduction of nonlinearities by the regime-switching mechanism admits temporal breaks in model dynamics.

The application of RSM has been hindered by two (related) practical issues: computational burden and the number of regimes allowed. Because of the computational burden, seminal works set up two regimes a priori (see Deng 1998 and Ethier and Mount 1998). Huisman and Mahieu (2003) are the first to propose a three-regime model, but with constraints: the initial jump regime is immediately followed by the mean-reversing regime and then moves back to the base regime. Using electricity price data from the Dutch, German, and the United Kingdom markets, they found that a regime-switching model performs better than a stochastic jump model specification for both mean-reversion and spikes. Our work departs from previous studies because we do not impose a priori the number of regimes that best captures the features of the electricity time series and proposes a joint analysis of distinct electricity markets.

We use the heterogeneous regime-switching model (HRSM) in Dias et al. (2008, 2009) and Ramos et al. (2011). This statistical model defines classes of regime-switching models based on the similarity of the dynamics within each class. An advantage of this approach is that we can see whether different time series share regimes (or regime dynamics). This model assumes two different types of discrete latent variables or states:

-

1.

each time series belongs to a specific group or cluster, say \( w \in \{ 1, \ldots ,S\} \). A model with S clusters is called a HRSM-S;

-

2.

each specific time series is modeled as a regime-switching model with K regimes and \( z_{it} \in \{ 1, \ldots ,K\} \) for all \( t = 1, \ldots ,T \) is the state occupied by the time series i at time t. Transitions between the K regimes over time follow a first-order Markov process.

Based on the definition of \( y_{it} \) introduced previously, let \( f({\mathbf{y}}_{i} ;\varphi ) \) be the density function of the electricity time series i. The HRSM-S is defined by:

where: (a) \( f(w_{i} ) \) is the probability of time series i belongs to cluster w; (b) \( f(z_{i1} |w_{i} ) \) is the initial-regime probability, i.e., the probability that time series i starts the sequence in regime k conditional on belonging to the cluster w; (c) \( f\left( {z_{it} |z_{i,t - 1} ,w_{i} } \right) \) is a latent transition probability, i.e., the probability of being in a particular regime at time \( t \) conditional on the regime at time \( t - 1 \) and within the cluster \( w \). Assuming a time-homogeneous transition process, \( p_{jkw} = P\left( {Z_{it} = k|Z_{i,t - 1} = j,W_{i} = w} \right) \) is the relevant parameter. Thus, for cluster \( w \) the transition probability matrix is

with \( \sum\nolimits_{k = 1}^{K} p_{jkw} = 1 \). Thus, the HRSM-S extends the traditional RSM as it allows cluster specific regime-switching dynamics.

The last term in Eq. (1) is the observed data density conditional on the regimes, \( f\left( {{\mathbf{y}}_{i} |w_{i} ,z_{i1} , \ldots ,z_{iT} } \right) \). Assuming that the observed return at a particular time depends only on the regime at that time, i.e., conditional on the latent state \( z_{it} \), the response \( y_{it} \) is independent of returns and regimes at other time points:

The probability density of the return \( i \) at time \( t \) conditional on the regime occupied at time \( t \), \( f(y_{it} |z_{it} ) \), is assumed to have a normal density function. For regime \( k \), this distribution is characterized by the parameter vector \( \boldsymbol{\theta}_{k} = (\mu_{k} ,\sigma_{k}^{2} ) \), i.e., the expected return or mean (\( \mu_{k} \)) and risk or variance (\( \sigma_{k}^{2} \)). The right-hand side of Eq. (1) shows that we are dealing with a mixture model consisting of time-constant latent variable \( w_{i} \) and \( T \) realizations of the time-varying latent variable \( z_{it} \). As in any mixture model, the observed data density \( f({\mathbf{y}}_{i} ;\boldsymbol{\varphi} ) \) results from marginalizing over the latent variables, in this case over the \( S \cdot K^{T} \) mixture components (see McLachlan and Peel 2000). Since \( f({\mathbf{y}}_{i} ;\boldsymbol{\varphi} ) \) is a mixture of densities across clusters and regimes, it defines a flexible Gaussian mixture model that can accommodate deviations from normality in terms of skewness and kurtosis (see, e.g., Dias and Wedel 2004 and Pennings and Garcia 2004).

The estimation of the HRSM-S parameters is performed by the maximum likelihood (ML) method. Given the presence of missing data (clusters and regimes), the expectation-maximization (EM) algorithm (Dempster et al. 1977) is a natural choice for maximizing the log-likelihood function: \( \ell (\boldsymbol{\varphi};{\mathbf{y}}_{i} ) = \sum\nolimits_{i = 1}^{n} \log f({\mathbf{y}}_{i} ;\boldsymbol{\varphi} ) \). Since the EM algorithm at the Expectation-step requires the computation and storage of \( S \times K^{T} \) entries of \( f\left( {w_{i} ,z_{i1} , \ldots ,z_{iT} |{\mathbf{y}}_{i} } \right) \) for each time series, computation time and computer storage increases exponentially with the number of time points. However, for regime-switching models, a special variant of the EM algorithm has been proposed that is usually referred to as the forward-backward or Baum-Welch algorithm (Baum et al. 1970) and will be used here.

A key issue in regime-switching modeling is the decision on the optimal number of regimes needed. For the HRSM-S, the selection of the number of clusters (\( S \)) and regimes (\( K \)) is based on the Bayesian information criterion (BIC) of Schwarz (1978) given by

where \( N_{S,K} \) is the number of free parameters in the regime-switching model and \( n \) is the sample size. The combination \( (S,K) \) with the minimum BIC identifies the best model.

5 Empirical Results

This section reports the estimates of the HRSM-S applied to electricity indexes. We estimate models with the density function given by Eq. (1) for different values of S (\( S = 1, \ldots ,8 \)) and K (\( K = 1, \ldots ,8 \)). For each combination, we use 1000 different sets of random starting values to minimize the impact of local maxima. A solution with two latent classes (\( S = 2 \)) and four regimes (\( K = 4 \)) yields the lowest BIC value (log-likelihood = −16258.8; number of free parameters = 39; and BIC = 32587.6). This means that the best solution incorporates two types of regime dynamics and four regimes.

Table 2 summarizes the results for the distribution of electricity prices across latent classes. Each latent class indicates a cluster, i.e., a group of prices that shares the same regime dynamics. Electricity prices are classified into two clusters, indicating that East coast electricity prices have different dynamics from those of the West coast (i.e., CINERGY and PJM are in latent class 2, whereas other price indexes are in latent class 1). The class assignments always have probability one, i.e., there is no uncertainty about the classification of these time series.

Regimes are described in Table 3. The first set of rows shows the estimates of the probability \( P(Z) \): the average proportion of returns in each regime over time. Overall, electricity prices are in regime 1 16.2 % of the time, in regime 2 7.4 % of the time, in regime 3 58.4 % of the time, and in regime 4 18.0 % of the time.

The next set of rows presents the expected returns and variance of each regime. Regimes are sorted by mean returns; regime 1 has the lowest returns and regime 4 the highest. Regimes 1–3 have negative mean returns. Regime 1 has very negative mean returns and high volatility, while regime 2 has negative mean returns and the highest volatility of all regimes; regime 3 has negative mean returns and the lowest volatility, which resembles ‘the base regime’.Footnote 7 Regime 4 has positive returns and the variance is similar to that of regime 1, it is the ‘up spike’ or the ‘up’ regime. The daily standard deviation for regimes 1, 2, 3 and 4 are 22.7, 88.0, 11.6 and 24.6, respectively. The extremely high volatility of regime 2 should be noted as it shows levels not reported in previous studies.

Results in Table 4 shows why electricity prices do not share the same dynamics, or are in different clusters. The first row gives the estimated probabilities of being in a particular regime for each cluster, i.e., electricity time series have different regime probabilities across classes.

West coast prices (latent class 1) have 0.67 probability of being in regime 3 (the base regime), whereas in the East coast (latent class 2) this probability is reduced to 0.43. East coast prices spend more time in spike regimes with probabilities of regimes 1 and 4 adding up to 0.488; on the other hand, probabilities of spike regimes from the West coast add up to only 0.261. Notwithstanding, both have a similar probability of being in the crisis regime, regime 2, despite the well-known crisis in California.

In the second row, we present the transition probabilities between the regimes for each group. It means that the closer the diagonal value is to one, the higher the regime persistence. In other words, once an electricity price enters a given regime, it is likely to stay in the same regime for some period of time.

All prices show regime persistence for regimes 2 and 3, those with the highest and lowest volatility. Inversely, regimes 1 and 4 do not show persistence, i.e., the likelihood of continuing in regime 1 and 4 is very small (spike regimes). West coast prices have a 0.802 probability of jumping from regime 4 to regime 1 and East coast prices a 0.733 probability. This means that after spiking up, there is a high probability that prices will go down. It is likely that prices from regime 1 jump to regime 3, the base regime, or spike again to regime 4, highlighting a very dynamic nature.

The (mean) sojourn time is the expected time that a price takes to move out of a given regime and is measured in weeks. It is given for regime \( k \) and conditional on the latent class \( w \) by \( 1/(1 - p_{kkw} ) \). Naturally, regimes with regime persistence have higher sojourn times. Regimes 2 and 3, the ones that show persistence, have sojourn times of 8 and 14 weeks for West coast, while mean times for spike regimes are around 1 week. Prices from the East coast stay in regime 3, the base, for shorter periods of time. Again, the evidence suggests that returns in the East coast are more volatile and change more often between regimes than those of the West coast.

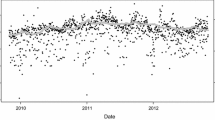

Figures 2 and 3 show the regime-switching dynamics in electricity prices in each group through time. It depicts the posterior probability of being in each regime at period t. Electricity has a dynamic nature and its frequent switches between regimes are notorious. The figures depict how the groups of prices have different patterns of regime switching. Light grey areas correspond to regime 3, the base regime, as revealed already by the probabilities.

Price dynamics in the U.S. West Coast. This figure shows the estimated posterior regime probability in latent class 1

Price dynamics in the U.S East Coast. This figure shows the estimated posterior regime probability in latent class 2

West coast prices were usually in regimes 3 (light grey), 4 (white), and 2 (dark grey) during the California crisis. The dynamics of East coast prices are consistent with the information in the tables, namely the shorter durations of regimes and the frequent switching. Regime 2, the one with the highest volatility, occurs frequently in the East coast. Interestingly, the period of the California electricity crisis is clearly identified by the dark grey area in the figure. This episode, well captured by regime 2, seems to be time specific and has not occurred again in the West coast.Footnote 8 It is also interesting to note that in the East coast, periods of extremely high volatility occurred frequently after 2001 and prices spikes often seem to occur.

Our results support a four regime parametrization contrasting with previous works such as Huisman and Mahieu (2003), Bierbrauer et al. (2007), Janczura and Weron (2010) that used three regimes; however, their study did not use U.S. data which included the particular episode of California Crisis with extremely high volatility due to price manipulation.

6 Electricity Synchronization

In this section we look at the synchronization of the regimes. To measure synchronization and co-movement in the electricity price series, we compute the association between prices using the posterior probability of being in regime \( k \). In other words, synchronization is measured by the likelihood that prices share regime \( k \) at the same period \( t \).

Let \( \hat{\alpha }_{it} \) be the estimated probability that electricity price \( i \) at time \( t \) will be in regime \( k \). To obtain a number in the full range of real numbers, this probability is expressed using the logit transformation:

Synchronization is quantified using the product-moment correlation between the logits for two time series. Our logit-based measure does not suffer from distortion caused by outliers because it filters out extreme observations of prices.

Table 5 shows the correlation between price time series. Panel A shows the probability of two electricity price series being in regime 1 at the same time, and the other panels for the other regimes.

For prices in the same cluster, or geographical area, it is likely that correlation within the cluster is high since they share the same regime dynamic. However, if electricity price indexes are in different clusters, it is interesting to see whether there is synchronization so as to gain some insights about common drivers.

We find a clear distinction of synchronization of regimes. For regimes with regime persistence, there is synchronization between groups (Regimes 2 and 3 present synchronization within and between groups) but we do not find evidence of synchronization for the other two regimes. To put it simply, when prices of the West coast are in the base (or the highest volatility) regime, it is likely that prices of the East coast are also in the base (or the highest volatility) regime. Conversely, it is not likely that prices of the East and West coasts will be found in regimes 1 and 4 at the same time. The correlation is high between returns within classes, but close to zero between the different geographical areas.

7 Conclusion

The 1980s saw the implementation of a wave of deregulatory reforms in the U.S. electricity sector. Wholesale electricity markets were transformed from a highly regulated government controlled system into deregulated local markets. The increase in competition of wholesale markets changed price dynamics and increased price volatility, exposing consumers and producers to significantly greater risks.

We draw on the literature that has proposed multi-regime frameworks to characterize electricity prices. We depart from previous work because we do not impose a fixed number of regimes a priori. Our findings suggest that a four-regime parametrization offers a better characterization of the price dynamics: a base regime, an extremely high volatility regime, a spike up regime, and a reverse regime. Our results show that electricity prices from West and East coasts have different regime dynamics with the latter prices switching more often between regimes. Additionally, our methodology suggests that electricity prices are better parameterized by four regimes: the base regime with low volatility; a spike up and a reverse regime both with high volatility and short duration; and a fourth one with extremely high volatility. The extremely high volatility regime describes West coast prices during the California electricity crisis, but East coast prices are also frequently in that regime. We find evidence of price synchronization in the lowest and highest volatility regimes, i.e., prices from the East and West coasts tend to be in those regimes at the same time.

In summary, in this chapter we describe and compare the price dynamics of electricity prices in the wholesale electricity markets of U.S. East and West coasts. The characterization of joint price dynamics is of great importance to financial market participants and may be useful in making optimal risk management decisions.

Notes

- 1.

- 2.

The grid needs to be constantly surveyed and cannot be under or overloaded. This implies that if wires owned by different companies were allowed to interconnect to form a single network, then the flow on one line could affect the capacity of other lines in the system to carry power creating risky unbalances.

- 3.

A recent case of grid collapse happened in India. India has increased the number interconnections between regional grids, approaching a single national grid. A breakdown in one part of the grid loaded other parts of the grid massively making the system collapse.

- 4.

Energy traders took power plants offline for maintenance in days of peak demand. This increased power prices sometimes by 20 times its normal price.

- 5.

- 6.

Other econometric approaches such as stochastic jump models have been applied in energy price modeling. Comparisons show that regime-switching models present many advantages in modeling the spiky and nonlinear behavior of electricity prices over competing techniques (Bierbrauer et al. 2007; Janczura and Weron, 2010; Mari 2006; Weron et al. 2004).

- 7.

We will apply terminology common to previous papers to characterize regimes: base, reverse, and spike regimes.

- 8.

The case of California led to specific measures in order to prevent similar cases. For instance, Moulton (2005) mentions the introduction of mitigation procedures after the energy crisis in California (2000–2001).

References

Andreasen J, Dahlgren M (2006) At the flick of a switch. Energy Risk 71–75

Baum LE, Petrie T, Soules G, Weiss N (1970) A maximization technique occurring in statistical analysis of probabilistic functions of Markov chains. Ann Math Stat 41(1):164–171

Bierbrauer M, Menn C, Rachev ST, Truck S (2007) Spot and derivative pricing in the EEX power market. J Bank Finance 31(11):3462–3485

Dempster AP, Laird NM, Rubin DB (1977) Maximum likelihood from incomplete data via EM algorithm. J R Stat Soc Ser B-Methodol 39(1):1–38

Deng S (1998) Stochastic models of energy commodity prices and their applications: mean reversion with jumps and spikes. PSERC Working Paper 98–28

Dias JG, Vermunt JK, Ramos S (2008) Heterogeneous hidden Markov models. In: Brito P (ed) Proceedings in computational statistics COMPSTAT 2008. Physica/Springer, Heidelberg, pp 373–380

Dias JG, Vermunt JK, Ramos S (2009) Mixture hidden Markov models in finance research. In: Fink A, Lausen B, Seidel W, Ultsch A (eds) Advances in data analysis, data handling and business intelligence. Springer, Berlin, pp 451–459

Dias JG, Wedel M (2004) An empirical comparison of EM, SEM and MCMC performance for problematic Gaussian mixture likelihoods. Stat Comput 14(4):323–332

Ethier R, Mount T (1998) Estimating the volatility of spot prices in restructured electricity markets and the implication for option values. Working Paper, Department of Applied Economics and Management, Cornell University. Ithaca, NY

Faruqui A, Chao H, Niemeyer V, Platt J, Stahlkopf K (2001) Analyzing California’s power crisis. Energy J 22(4):29–52

Fong WM, See KH (2002) A Markov switching model of the conditional volatility of crude oil futures prices. Energy Econ 24(1):71–95

Hadsell L, Marathe A, Shawky HA (2004) Estimating the volatility of wholesale electricity spot prices in the US. Energy J 25(4):23–40

Haldrup N, Nielsen F, Nielsen M (2010) A vector autoregressive model for electricity prices subject to long memory and regime switching. Energy Econ 32:1044–1058

Hamilton JD (1989) A new approach to the economic-analysis of nonstationary time-series and the business-cycle. Econometrica 57(2):357–384

Huisman R, Mahieu R (2003) Regime jumps in electricity prices. Energy Econ 25(5):425–434

Janczura J, Weron R (2010) An empirical comparison of alternate regime-switching models for electricity spot prices. Energy Econ 32(5):1059–1073

Janczura J, Weron R (2012) Efficient estimation of Markov regime-switching models: An application to electricity wholesale market prices. AStA Adv Stat Anal 96:385–407

Joskow PL (1997) Restructuring, competition and regulatory reform in the U.S. electricity sector. J Econ Perspect 11(3):119–138

Knittel C, Roberts MR (2005) An empirical examination of restructured electricity prices. Energy Econ 27(5):791–817

Mari C (2006) Regime-switching characterization of electricity prices dynamics. Phys A Stat Theor Phys 371(2):552–564

McLachlan G, Peel D (2000) Finite mixture models. Wiley, New York

Mjelde JW, Bessler DA (2009) Market integration among electricity markets and their major fuel source markets. Energy Econ 31(3):482–491

Moulton JS (2005) California electricity futures: the NYMEX experience. Energy Econ 27(1):181–194

Park H, Mjelde JW, Bessler DA (2006) Price dynamics among U.S. electricity spot markets. Energy Econ 28(1):81–101

Pennings JME, Garcia P (2004) Hedging behavior in small and medium-sized enterprises: the role of unobserved heterogeneity. J Bank Finance 28(5):951–978

Ramos S, Vermunt J, Dias J (2011) When markets fall down: are emerging markets all equal? Int J Finance Econ 16:324–338

Schwarz G (1978) Estimating dimension of a model. Ann Stat 6(2):461–464

Weron R, Bierbrauer M, Trück S (2004) Modeling electricity prices: jump diffusion and regime switching. Phys A 336:39–48

Woo C (2001) What went wrong in California’s electricity market? Energy 26(8):747–458

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2014 Springer-Verlag Berlin Heidelberg

About this chapter

Cite this chapter

Dias, J.G., Ramos, S.B. (2014). An Overview of Electricity Price Regimes in the U.S. Wholesale Markets. In: Ramos, S., Veiga, H. (eds) The Interrelationship Between Financial and Energy Markets. Lecture Notes in Energy, vol 54. Springer, Berlin, Heidelberg. https://doi.org/10.1007/978-3-642-55382-0_9

Download citation

DOI: https://doi.org/10.1007/978-3-642-55382-0_9

Published:

Publisher Name: Springer, Berlin, Heidelberg

Print ISBN: 978-3-642-55381-3

Online ISBN: 978-3-642-55382-0

eBook Packages: EnergyEnergy (R0)