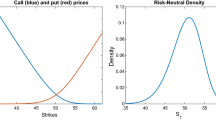

The state price density (SPD) carries important information on the behavior and expectations of the market and it often serves as a base for option pricing and hedging. Many commonly used SPD estimation technique are based on the observation (Breeden and Litzenberger, 1978) that the SPD f(·) may be expressed as

where C t (K, T) is a price of European call option with strike price K at time t expiring at time T and r denotes the risk free interest rate. An overview of estimation techniques is given in Jackwerth (1999). Kernel smoothers were in this framework applied by Äit-Sahalia and Lo (1998), Ä it-Sahalia and Lo (2000), or Huynh, Kervella, and Zheng (2002). Some modifications of the nonparametric smoother allowing to apply no-arbitrage constraints were proposed, e.g., by Äit-Sahalia and Duarte (2003), Bondarenko (2003), or Yatchew and Härdle (2006). Apart of the choice of a suitable estimation method, Härdie and Hlávka (2005) show that the covariance structure of the observed option prices carries additional important information that should to be considered in the estimation procedure. Härdie and Hlávka (2005) suggest a simple and easily applicable approximation of the covariance. A more detailed discussion of option price errors may be found in Renault (1997).

In this chapter, we will estimate the SPD from observed call option prices using the well-known Kalman filter, invented already in the early sixties and marked by Harvey (1989). Kalman filter may be shortly described as a statistical method used for estimation of the non-observable component of a state-space model and it already became an important econometric tool for financial and economic estimation problems in continuous time finance.

Access provided by Autonomous University of Puebla. Download to read the full chapter text

Chapter PDF

Similar content being viewed by others

Keywords

These keywords were added by machine and not by the authors. This process is experimental and the keywords may be updated as the learning algorithm improves.

Bibliography

A¨it-Sahalia, Y. and Duarte, J., 2003, Nonparametric option pricing under shape restric-tions, Journal of Econometrics 116, 9-47.

A¨it-Sahalia, Y. and Lo, A.W., 1998, Nonparametric estimation of state-price densities implicit in financial asset prices, Journal of Finance 53, 499-547.

A¨it-Sahalia, Y. and Lo, A.W., 2000, Nonparametric risk management and implied risk aversion, Journal of Econometrics 94, 9-51.

Bondarenko, O., 2003, Estimation of risk-neutral densities using positive convolution ap-proximation, Journal of Econometrics 116, 85-112.

Breeden, D. and Litzenberger, R., 1978, Prices of State-Contingent Claims Implicit in Option Prices, Journal of Business 51, 621-651.

Franke, J., Härdle, W. and Hafner, Ch., 2008, Statistics of Financial Markets. Springer, Berlin.

Härdle, W., 1991, Applied Nonparametric Regression. Cambridge University Press, Cam-bridge.

Härdle, W. and Hlávka, Z., 2005, Dynamics of State Price Densities. Sonderforschungsbereich 649 Discussion Paper 2005-021, Humboldt-Universität zu Berlin.

Harvey, A. C., 1989, Forecasting, Structural Time Series Models and the Kalman Filter. Cambridge University Press, Cambridge.

Huynh, K., Kervella, P., and Zheng, J., 2002, Estimating state-price densities with nonpara-metric regression. In Härdle, Kleinow and Stahl, eds., Applied quantitative finance, Springer Verlag, Heidelberg 171-196.

Jackwerth, J.C., 1999, Option-implied risk-neutral distributions and implied binomial trees: a literature review, Journal of Derivatives 7, 66-82.

Kellerhals, B. P., 2001, Financial Pricing Models in Continuous Time and Kalman Filtering. Springer, Heidelberg.

Nadaraya, E. A., 1964, On estimating regression, Theory of Probability and its Applications 9(1),141-142.

Renault, E., 1997, Econometric models of option pricing errors. In Kreps and Wallis, eds., Advances in Economics and Econometrics: Theory and Applications, Seventh World Congress, Volume III, Cambridge University Press, Cambridge, 223-278.

Simonoff, J. S., 1996, Smoothing Methods in Statistics. Springer, New York.

Svoj´ik, M., 2007, Application of Kalman Filtering, Diploma Thesis, Charles University in Prague, Faculty of Mathematics and Physics.

Watson, G. S., 1964, Smooth regression analysis, Sankhya, Ser. A 26, 359-372.

Yatchew, A. and Härdle, W., 2006, Nonparametric state price density estimation using constrained least squares and the bootstrap, Journal of Econometrics 133(2), 579-599.

Author information

Authors and Affiliations

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2009 Springer Berlin Heidelberg

About this chapter

Cite this chapter

Hlávka, Z., Svojik, M. (2009). Application of Extended Kalman Filter to SPD Estimation. In: Härdle, W.K., Hautsch, N., Overbeck, L. (eds) Applied Quantitative Finance. Springer, Berlin, Heidelberg. https://doi.org/10.1007/978-3-540-69179-2_11

Download citation

DOI: https://doi.org/10.1007/978-3-540-69179-2_11

Publisher Name: Springer, Berlin, Heidelberg

Print ISBN: 978-3-540-69177-8

Online ISBN: 978-3-540-69179-2

eBook Packages: Mathematics and StatisticsMathematics and Statistics (R0)