Abstract

Sustainable real estate provides an opportunity to tackle climate change while achieving better financial outcomes. Given the amount of greenhouse gas emissions from buildings, we know that climate change cannot be solved without addressing energy efficiency in buildings. Moreover, sustainable real estate provides an opportunity for better financial outcomes and thus presents a major investment opportunity over at least the next two decades. Yet we lack a true and robust picture of what is necessary of buildings on a global basis. This chapter aims to provide a roadmap of the many sustainable real estate strategies that are imperative to reaching our collective global emissions reduction goals.

Access provided by Autonomous University of Puebla. Download chapter PDF

Similar content being viewed by others

Buildings can seem boring to many. But within the world’s current andfuture building stock could well lay the most important area of work ahead for ensuring better environmental and socialfuture outcomes.

Sustainable real estate is in fact a critical baseline for establishing better financialoutcomes, as not fixing for the track we are headed down regarding climate change would likely be economically disastrous, perhaps in the many tens of trillions of dollars.Footnote 1

If we are to solve for climate change, however, efficiency emerges as the most important area of carbon reduction potential to be achieved. The International Energy Agency argued in its World Energy Outlook in 2014Footnote 2 that for a 2-degree world, over US $1 trillion in annual investment will be needed on average by 2040, with a majority of this amount falling into the efficiency category.

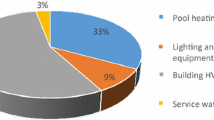

While efficiency can be a broad term touching all sectors, real estate is a large percentage of the existing global carbon footprint and therefore a large percentage of carbon reduction potential as well. For example, in the US (Fig. 2.1), the largest components of electricity use are residential (38.5%) and commercial (35.4%), and electricity use is the largest component of energy consumption, making building efficiency a very large percentage of what is possible and necessary.

Retail sales of electricity, end use by percent of ultimate customer (https://www.c2es.org/energy/use/residential-commercial)

Hence, if necessary reductions in the carbon footprint are expected and necessary from efficiency and finance, and buildings make up the majority of the carbon footprint of consumption, then efficiency in existing buildings stock, both current and new, becomes one of the biggest investment opportunities and this could create a useful paradigm of sorts with increasing and specific focus.

Consider as well the effects of automation, technological innovation, and globalization.Footnote 3

These trends are likely unstoppable and create unrest in previously developed countries where jobs for those less skilled are suddenly disappearing. Add to this what we call the effect of “the entrenched nature of the status quo,” largely in the form of people driving existing cars longer and operating existing buildings and power plants past the original length of time expected, and this creates an unsustainable path for ongoing carbon emissions versus reductions required.

In economies which are otherwise economically vibrant, retrofitting at scale and sustainable real estate more generally therefore becomes a means of establishing adequate jobs and necessary efficiency including through creative financing mechanisms so that governments do not take on the entire financial burden.

Many studies show rents are higher and residents happier in more efficient buildings that take into account the environment or otherwise create healthier and happier spaces for both living and working conditions. While often thought of as coming best from new building stock, this could come from revised existing stock as well. The area of retrofit finance is largely untapped but could form a “new deal” of sorts and is arguably essential given this entrenched nature of the status quo previously mentioned. This “new deal” could be politically palatable as well to a disgruntled voting public in countries such as the US and UK where 2016 elections went in unexpected directions. So we see improving existing building stock as a critical and often overlooked component of what might be necessary and possible.

On the new building front, for all the good work occurring on new building standards, there is also growing concern about measurement and net impact, specifically whether standards such as Leadership in Energy and Environmental Design (LEED) and BREEAM (Building Research Establishment Environmental Assessment Method) bring about actual environmental impact reductions, and if so whether they are sufficient. In addition, new building development can often lag behind what might be necessary to create overall levels of necessary building efficiency, given the long time it takes to replace building stock more generally.

At minimum, better standards, methods of analysis, and reporting are needed to ensure that when sustainable real estateprojects are chosen through upfront design, there is a specific understanding of what improvement in net impacts are likely and possible, perhaps even from a scenarios perspective, including the better financialoutcomes which result from better design choices.

The Rocky Mountain Institute (RMI) has seen all this as well, and is an example of an organization working diligently and thoughtfully to increase efficiency solutions being deployed, including through more efficient cooling and building functionality. RMI, which has long worked in China and increasingly as well in India where climate solutions are being implemented rapidly, sees that 35% of global energy is consumed by buildings, and 60% of consumed energy occurs in buildings, so the potential is clear. They aim to reduce energy consumption in buildings by 390 trillion BTUs (British thermal units) in the US alone, the equivalent of decommissioning 17 coal power plants.Footnote 4

Better standards are also needed on the financing side of building efficiency, with some early examples of energy efficiency financing being achieved by the green banks and infrastructure banks in states such as Connecticut, Rhode Island and New York, and in Europe surrounding groups such as Energy Efficiency Financial Institutions Group (EEFIG) and their new underwriting toolkit,Footnote 5 but as per Chap. 5, much more work is needed in Europe on this basis.

Region by region, more and better work is happening, such as Siemens rebuilding Cairo,Footnote 6 cities banding together to fight climate change,Footnote 7 cities creating benchmarkingordinancesFootnote 8 and otherwise creating positive environments for new building design and related technological improvement.

Yet we lack a true and robust picture of what is necessary of buildings on a global basis. What would be really helpful is a roadmap of what we need to do and should do in each category of building by region (and by category of owner as well given the significant percentage of family owned building empires doing arguably not enough on this subject in cities such as New York).

We hope that this text starts to provide a roadmap of the many strategies that need to run in parallel to achieve the sustainable real estate sector we now know we can achieve. It can only be achieved through will, intent, design, and successful implementation. We hope to have at least started on this path with this effort.

Notes

- 1.

- 2.

- 3.

- 4.

- 5.

- 6.

- 7.

- 8.

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2019 The Author(s)

About this chapter

Cite this chapter

Krosinsky, C. (2019). The Relevance of Real Estate in Solving Climate Change. In: Walker, T., Krosinsky, C., Hasan, L.N., Kibsey, S.D. (eds) Sustainable Real Estate. Palgrave Studies in Sustainable Business In Association with Future Earth. Palgrave Macmillan, Cham. https://doi.org/10.1007/978-3-319-94565-1_2

Download citation

DOI: https://doi.org/10.1007/978-3-319-94565-1_2

Published:

Publisher Name: Palgrave Macmillan, Cham

Print ISBN: 978-3-319-94564-4

Online ISBN: 978-3-319-94565-1

eBook Packages: Business and ManagementBusiness and Management (R0)