Abstract

Long before current graphic, visualization and geometric tools were available, John E. Littlewood (1885–1977) wrote in his delightful Miscellany:

A heavy warning used to be given [by lecturers] that pictures are not rigorous; this has never had its bluff called and has permanently frightened its victims into playing for safety. Some pictures, of course, are not rigorous, but I should say most are (and I use them whenever possible myself). (Littlewood, A mathematician’s miscellany. London: Methuen, 1953, p. 53)

Over the past 5–10 years, the role of visual computing in my own research has expanded dramatically. In part this was made possible by the increasing speed and storage capabilities—and the growing ease of programming—of modern multi-core computing environments. But, at least as much, it has been driven by my group’s paying more active attention to the possibilities for graphing, animating or simulating most mathematical research activities.

Access provided by Autonomous University of Puebla. Download chapter PDF

Similar content being viewed by others

Keywords

- Visual theorems

- Experimental mathematics

- Digital assistance

- Randomness

- Normality of numbers

- Short walks

- Planar walks

- Fractals

- Protein conformation

- Elliptic integrals

- Modular functions

- Special functions

- Partitions

- Generating functions

1 Introduction

The computer has in turn changed the very nature of mathematical experience, suggesting for the first time that mathematics, like physics, may yet become an empirical discipline, a place where things are discovered because they are seen.—David BerlinskiFootnote 1

In this chapter I want to talk, both generally and personally, about the use of tools in the practice of modern research mathematics. To focus my attention I have decided to discuss the way I and my research group members have used tools primarily computational (visual, numeric and symbolic) during the past 5 years. When the tools are relatively accessible I shall exhibit details; when they are less accessible I settle for illustrations and discussion of process.

Long before current graphic, visualization and geometric tools were available, John E. Littlewood, 1885–1977, wrote in his delightful Miscellany:

A heavy warning used to be given [by lecturers] that pictures are not rigorous; this has never had its bluff called and has permanently frightened its victims into playing for safety. Some pictures, of course, are not rigorous, but I should say most are (and I use them whenever possible myself). (Littlewood, 1953, p. 53)

Over the past 5 years, the role of visual computing in my own research has expanded dramatically. In part this was made possible by the increasing speed and storage capabilities—and the growing ease of programming—of modern multi-core computing environments (Borwein, Skerritt, & Maitland, 2013). But, at least as much, it has been driven by my group’s paying more active attention to the possibilities for graphing, animating or simulating most mathematical research activities.

1.1 Who I Am and How I Got That Way

In my academic lifetime, tools went from graph paper, log tables, slide rules and slipsticks to today’s profusion of digital computational devices. Along the way came the CURTA, HP programmable calculators, TI calculators, and other transitional devices not to mention my grandfather’s business abacus. When a radically new tool has come along, it can be adapted very quickly as was the case with the use of log-tables in the early seventeenth century after Brigg’s 1616 improvement of Napier’s 1614 logarithms and the equally rapid abandonment of slide-rule in the 1970s after 350 years of ubiquity. I feel obliged to record that well into the 1980s business mathematics texts published compound interest tables with rates up to 5 % when mortgage rates were well over 20 %.

Let me next reprise material I wrote for a chapter for the 2015 collection The Mind of a Mathematician (Borwein, 2012).

I wish to aim my scattered reflections in generally the right direction: I am more interested in issues of creativity á la Hadamard (Borwein, Liljedahl, & Zhai, 2010) than in Russell and foundations, or Piaget and epistemology…and I should like a dash of “goodwill computing” thrown in. More seriously, I wish to muse about how we work, what keeps us going, how the mathematics profession has changed and how “plus ça change, la plus ça reste pareil”,Footnote 2 and the like while juxtaposing how we perceive these matters and how we are perceived. Elsewhere, I have discussed at length my own views about the nature of mathematics from both an aesthetic and a philosophical perspective (see, e.g., Gold & Simons, 2008; Sinclair, Pimm, & Higginson, 2007).

I have described myself as ‘a computer-assisted quasi-empiricist’. For present more psychological proposes I will quote approvingly from Brown (2009, p. 239):

…Like 0l’ Man River, mathematics just keeps rolling along and produces at an accelerating rate “200,000 mathematical theorems of the traditional handcrafted variety …annually.” Although sometimes proofs can be mistaken—sometimes spectacularly—and it is a matter of contention as to what exactly a “proof” is—there is absolutely no doubt that the bulk of this output is correct (though probably uninteresting) mathematics.—Richard C. Brown

I continued: Why do we produce so many unneeded results? In addition to the obvious pressure to publish and to have something to present at the next conference, I suspect Irving Biederman’s observations below plays a significant role.

“While you’re trying to understand a difficult theorem, it’s not fun,” said Biederman, professor of neuroscience in the USC College of Letters, Arts and Sciences. …“But once you get it, you just feel fabulous.” …The brain’s craving for a fix motivates humans to maximize the rate at which they absorb knowledge, he said. …“I think we’re exquisitely tuned to this as if we’re junkies, second by second.”—Irving BiedermanFootnote 3

Mathematical tools are successful especially when they provide that rapid ‘fix’ of positive reinforcement. This is why I switched from competitive chess to competitive bridge. Being beaten was less painful and quicker, reward was more immediate.Footnote 4

In Borwein (2012) I again continued: Take away all success or any positive reinforcement and most mathematicians will happily replace research by adminstration, more and (hopefully better) teaching, or perhaps just a favourite hobby. But given just a little stroking by colleagues or referees and the occasional opiate jolt, and the river rolls on. For a fascinating essay on the modern university in 1990 I recommend Giametti (1990).

The pressure to publish is unlikely to abate and qualitative measurements of performanceFootnote 5 are for the most part fairer than leaving everything to the whim of one’s Head of Department. Thirty-five years ago my career review consisted of a two-line mimeo “your salary for next year will be …” with the relevant number written in by hand.

At the same time, it is a great shame that mathematicians have a hard time finding funds to go to conferences just to listen and interact. Csikszentmihalyi (1997) writes:

[C]reativity results from the interaction of a system composed of three elements: a culture that contains symbolic rules, a person who brings novelty into the symbolic domain, and a field of experts who recognize and validate the innovation. All three are necessary for a creative idea, product, or discovery to take place.—Mihalyy Csikszentmihalyi

We have not paid enough attention to what creativity is and how it is nurtured. Conferences need audiences and researchers need feedback other than the mandatory “nice talk” at the end of a special session. We have all heard distinguished colleagues mutter a stream of criticism during a plenary lecture only to proffer “I really enjoyed that” as they pass the lecturer on the way out. A communal view of creativity requires more of the audience.

And the computer as provider of tools can often provide a more sympathetic and caring, even better educated, audience.

1.2 What Follows

We first discuss briefly in Sect. 3.2 what is meant by a visual theorem. In Sect. 3.3 we talk about experimental computation and then turn to digital assistance. In a key Sect. 3.4 we examine a substantial variety of accessible examples of these three concepts. In Sect. 3.5 we discuss simulation as a tool for pure mathematics.

In the final three sections, we turn to three more sophisticated sets of case studies. They can none-the-less be followed without worrying about any of the more complicated formulae. First in Sect. 3.6 comes dynamic geometry (iterative reflection methods Aragon & Borwein, 2013) and matrix completion problems Footnote 6 (applied to protein conformation Aragon, Borwein, & Tam, 2014) (see Case Studies I). In Sect. 3.7 for the second set of Case Studies, we then turn to numerical analysis (see Case Studies II). I end in Sect. 3.8 with description of recent work from my group in probability (behaviour of short random walks Borwein & Straub, 2013; Borwein, Straub, Wan, & Zudilin, 2012) and transcendental number theory (normality of real numbers Aragon, Bailey, Borwein, & Borwein, 2013).

1.3 Some Early Conclusions

I have found it is often useful to make some conclusions early. So here we go.

-

1.

Mathematics can be done experimentally (Bailey & Borwein, 2011a) (it is fun) using computer algebra, numerical computation and graphics: SNaG computations. Tables and pictures are experimental data but you cannot stop thinking.

-

2.

Making mistakes is fine as long as you learn from them, and keep your eyes open (conquering fear).

-

3.

You cannot use what you do not know and what you know you can usually use. Indeed, you do not need to know much before you start research in a new area (as we shall see).

-

4.

Tools can help democratize appreciation of and ability in mathematics.

2 Visual Theorems and Experimental Mathematics

In a 2012 study On Proof and Proving (ICMI, 2012), the International Council on Mathematical Instruction wrote:

The latest developments in computer and video technology have provided a multiplicity of computational and symbolic tools that have rejuvenated mathematics and mathematics education. Two important examples of this revitalization are experimental mathematics and visual theorems.

2.1 Visual Theorems

By a visual theorem Footnote 7 I mean a picture or animation which gives one confidence that a desired result is true; in Giaquinto’s sense that it represents “coming to believe it in an independent, reliable, and rational way” (either as discovery or validation) as described in Bailey and Borwein (2011b). While we have famous pictorial examples purporting to show things like all triangles are equilateral, there are equally many or more bogus symbolic proofs that ‘\( 1+1=1 \)’. In all cases ‘caveat emptor’.

Modern technology properly mastered allows for a much richer set of tools for discovery, validation, and even rigorous proof than our precursors could have ever imagined would come to pass—and it is early days. That said just as books on ordinary differential equations have been replaced by books on dynamical systems, the word visual now pops up frequently in book titles. Unless ideas about visualization are integrated into the text this is just marketing.

2.2 On Picture-Writing

The ordinary generating function associated with a sequence \( {a}_0,{a}_1,\dots, {a}_n,\dots \) is the formal seriesFootnote 8

while the exponential generating function is

Both forms of generating function are ideally suited to computer-assisted discovery.

George Pólya, in an engaging eponymous American Mathematical Monthly article, provides three compelling examples of converting pictorial representations of problems into generating function solutions (Pólya, 1956):

-

1.

In how many ways can you make change for a dollar?

This leads to the (US currency) generating function

$$ \begin{array}{c}{\displaystyle \sum_{k=1}^{\infty }}{P}_k{x}^k=\frac{1}{\left(1-{x}^1\right)\left(1-{x}^5\right)\left(1-{x}^{10}\right)\left(1-{x}^{25}\right)\left(1-{x}^{50}\right)},\\ {}\end{array} $$which one can easily expand using a Mathematica command,

Series[1/((1-x)*(1-x^5)*(1-x^10)*(1-x^25)*(1-x^50)), {x, 0, 100}]

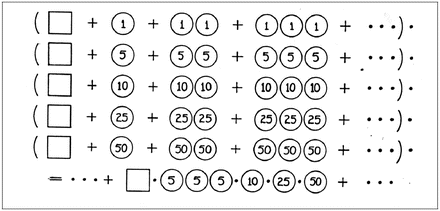

to obtain P 100 = 292 (242 for Canadian currency, which lacks a 50 cent piece). Pólya’s illustration is shown in Fig. 3.1.

Fig. 3.1

Pólya’s illustration of the change solution (courtesy Mathematical Association of America)

We look at a related generating function for counting additive partitions in Example 3.4.6.

-

2.

Dissect a polygon with n sides into n − 2 triangles by n − 3 diagonals and compute D n , the number of different dissections of this kind.

This is illustrated in Fig. 3.2 and leads to the fact that the generating function for \( {D}_3=1,{D}_4=2,{D}_5=5,{D}_6=14,{D}_7=42,\dots \)

$$ \begin{array}{c}D(x)={\displaystyle \sum_{k=1}^{\infty }}{D}_k{x}^k\\ {}\end{array} $$satisfies

$$ \begin{array}{c}D(x)=x\kern0.3em {\left[1+D(x)\right]}^2,\\ {}\end{array} $$whose solution is therefore

$$ \begin{array}{c}D(x)=\frac{1-2x-\sqrt{1-4x}}{x}.\\ {}\end{array} $$The Mathematica command

Fig. 3.2

The first few sets of dissections

Series[((1 - 2 x) - Sqrt[1 - 4 x])/x, {x, 0, 10}]

returns

$$ \begin{array}{l}2x+4{x}^2+10{x}^3+28{x}^4+84{x}^5+264{x}^6+858{x}^7\hfill \\ {}\kern12pt +2860{x}^8+9724{x}^9+33592{x}^{10}+O\left({x}^{11}\right).\hfill \end{array} $$with list of coefficients

$$ \{0,2,4,10,28,84,264,858,2860,9724,33592\} $$and D n+2 turns out to be the nth Catalan number \( \left(\genfrac{}{}{0ex}{}{2n}{n}\right)/ \left(n+1\right) \). This can be discovered using Sloane’s wonderful Online Encyclopedia of Integer Sequences as illustrated in Fig. 3.3. Note that we only used the first six non-zero terms and had four left to ‘confirm’ our experiment.

Fig. 3.3

Using https://oeis.org/ to identify the Catalan numbers

-

3.

Compute T n , the number of different (rooted) trees with n knots. Footnote 9

This is a significantly harder problem so we say less:

The ordinary generating function of the T n becomes a remarkable result due to Cayley, namely

$$ T(x)={\displaystyle \sum_{k=1}^{\infty }}\kern0.3em {T}_k{x}^k=x\kern0.3em {\displaystyle \prod_{k=1}^{\infty }}\kern0.3em {\left(1-{x}^k\right)}^{-{T}_k}, $$(3.3)where remarkably the product and the sum share their coefficients. This can be used to produce a recursion for T n in terms of \( {T}_1,{T}_2,\dots, {T}_{n-1} \), which starts: \( {T}_1=1,{T}_2=1,{T}_3=2,{T}_4=4,{T}_5=9,{T}_6=20,\dots \).

In each case, Pólya’s main message is that one can usefully draw pictures of the component elements—(a) in pennies, nickels dimes and quarters (plus loonies in Canada and half dollars in the USA), (b) in triangles and (c) in the simplest trees (with the fewest knots).

That said, I often find it easier to draw pictures from generating functions rather than go in the other direction. In any event, Pólya’s views on heuristic reasoning and his books on problem solving (Pólya, 1981, 1990) remain as engaging, if idiosyncratic, today as when first published.Footnote 10

2.2.1 Proofs Without Words

In Fig. 3.4 we reproduce three classic proofs without words—though most such proofs benefit from a few words of commentary. In Fig. 3.5 we display three modern (dynamic geometry) proofs without words from http://cinderella.de/files/HTMLDemos/Main.html.Footnote 11

Three classical proofs without words

Three modern proofs without words

Figure 3.4 shows from left to right the following three results:

-

1.

Pythagoras theorem;

-

2.

\( 1+3+5+\left(2n-1\right)={n}^2 \);

-

3.

\( 1/2+1/4+1/8+\cdots =1 \).

The Pythagorean proof is from the Zhou Bi Suan Jing which dates from the Zhou Dynasty (1046 BCE–256 BCE), and is one of the oldest recorded.

Figure 3.5 shows from left to right the following three results:

-

1.

Pythagoras theorem;

-

2.

\( \sqrt{2} \) is irrational as suggested by Tom ApostolFootnote 12;

-

3.

How to inscribe three tangent circles in a triangle.

Needless to say, the advantage of a modern construction—when there really is one—is largely lost on the printed page, which does not allow one to see the dynamics. We somewhat repair that damage in Fig. 3.6 by showing three illustrations of different configurations for fractals—zoom-invariant objects—built on circles of Apollonius.Footnote 13 In this case we perturbed slightly the configuration on the left to that in the middle and then the right, and see the different appearance of the fractals produced by the same rules.

Three fractals generated by different Apollonian configurations

3 Experimental Mathematics

The same ICMI study (2012), quoting (Borwein & Devlin, 2008, p. 1), says enough about the meaning of experimental mathematics for our current purposes:

Experimental mathematics is the use of a computer to run computations—sometimes no more than trial-and-error tests—to look for patterns, to identify particular numbers and sequences, to gather evidence in support of specific mathematical assertions that may themselves arise by computational means, including search.

Like contemporary chemists—and before them the alchemists of old—who mix various substances together in a crucible and heat them to a high temperature to see what happens, today’s experimental mathematicians put a hopefully potent mix of numbers, formulas, and algorithms into a computer in the hope that something of interest emerges.

3.1 Experimental Mathodology

I originally mistyped ‘mathodology’ intending ‘methodology’, but I liked the mistake and have kept it. We started (Borwein & Devlin, 2008) with Justice Potter Stewart’s famous 1964 comment on pornography: “I know it when I see it.”

A bit less informally, by experimental mathematics I intend, as discussed in Borwein and Bailey (2008) and elsewhere:

-

1.

Gaining insight and intuition;

-

We illustrate this repeatedly below by drawing many simple functions. Almost always, as in Example 3.4.3, we see things in a picture that were not clear in our mind’s eye.

-

Sometimes, as in Example 3.4.2, a new pattern jumps out that we were not originally intent on studying. By contrast, in Example 3.4.9 we show how the computer can tell you things, such as that a number is algebraic, that you can then verify but probably would never find.

-

-

2.

Discovering new relationships;

-

3.

Visualizing math principles;

-

4.

Testing and especially falsifying conjectures;

-

5.

Exploring a possible result to see if it merits formal proof;

-

In a traditional Lemma–Theorem–Corollary version of deductive mathematics, one has to prove every step of a chain of arguments to get to the end. Suppose there are six steps in a complicated result, and the third is a boring but hard equation, whose only value is that it leads to step six. Then it is appropriate to challenge step six a lot, before worrying about proving step three.

-

-

6.

Suggesting approaches for formal proof;

-

7.

Computing replacing lengthy hand derivations;

-

Example 3.3.1 discusses this for matters like taking roots, or factoring large numbers.

-

It also the case that many computations that used to be too lengthy to perform by hand are no longer so. For instance, the Maple fragment

$$ \mathtt{add}\left(\mathtt{ithprime}\left(\mathtt{k}\right),\mathtt{k}=\mathtt{1}..\mathtt{1}\mathtt{00000}\right); $$returned the sum of the first 105 primes, 62660698721, in 0. 171 s. Adding a million took much longer though! My preference on tests, rather than banning calculators or computers, is to adapt the questions to make them computationally aware.Footnote 14

-

-

8.

Confirming analytically derived results.

-

I illustrate this in Example 3.4.12 by confirming some exact results knowing only their general structure.

-

All of these uses play a central role in my daily research life. We will see all of these eight notions illustrated in the explicit examples of Sect. 3.3.2 and of Sect. 3.4.

3.2 When Science Becomes Technology

What tools we choose to use—and when—is a subtle and changeable issue.

Example 3.3.1 (When Science Becomes Technology).

We ‘unpack’ methods when we want to understand them or are learning them for the first time. Once we or our students have mastered a new tool we ‘repack’ it. For instance,

which factors as

If we are teaching or taking a course in factorization methods, we may well want to know ‘how’ this was done. In most contexts, we are happy to treat the computer as a reliable tool and to take the answer without further introspection.

In like fashion,

will be computed by most packages to the displayed precision. We can confirm this since

If we wish to understand what the computer has done—probably by Newton’s method, we must go further, but if we only wish to use the answer that is irrelevant. The first is science or research, the second is technology. \( \diamondsuit \)

The William Lowell Putnam competition taken each year by the strongest North American undergraduate students has conventionally had one easy question (out of 12) based on the current year.

Example 3.3.2 (A 1998 Putnam Examination Problem).

The problem was

Let N be the positive integer with 1998 decimal digits, all of them 1; that is, N = 1111…11. Find the thousandth digit after the decimal point of \( \sqrt{N} \).

This can be done by brute force

> evalf[10](sqrt(add(10^k,k=0..1997))/10^1000;

which is not what the posers had in mind. \( \diamondsuit \)

Example 3.3.3 (A 1995 Putnam Examination Problem).

The problem requests

Evaluate:

Express your answer in the form \( \left(a+b\sqrt{c}\right)/ d \), where a, b, c, d are integers.

Proof.

If we call the repeated radical above α, the request is to solve for

and a solve request to a CAS will return

We may determine the last reduction in many ways (1) via identify, (2) using the inverse symbolic calculator (ISC), (3) using a resolvent computation to find the quadratic polynomial satisfied by α as given by Eq. (3.5), or (4) by repeatedly computing the square root. Indeed identify will return the answer directly from (3.4) which already agrees with the limit to 20 places. □

With access to computation the problem becomes too straight-forward. \( \diamondsuit \)

I next recall some continued fraction notation. Figure 3.7 shows the two most common ways of writing a simple or regular continued fraction—in this case for π. For any α > 0, this represents the process of going from

and repeating the process, while recording the integer part \( \left\lfloor \alpha \right\rfloor \) each time. This is usually painful to do by hand but is easy for our computer.

The simple continued fraction for π (L) in compact form (R)

Example 3.3.4 (Changing Representations).

Suppose I wish to examine the numbers

and

As floating point numbers there is nothing to distinguish them; but the Maple instruction convert(alpha,confrac); returns the simple continued fraction for α in compact form (Borwein and Bailey, 2008)

while convert(beta,confrac); returns

So, in this new representation, the numbers no longer look similar. As described in Borwein and Bailey (2008), Borwein and Devlin (2008), and Bailey and Borwein (2011a), continued fractions with terms in arithmetic progression are well studied, and so there are several routes now open to discovering that \( \alpha ={I}_1(2)/ {I}_0(2) \) where for ν = 0, 1, 2, …

For instance, on May 23, 2014, entering "continued fraction" "arithmetic progression" into Google returned 23,700 results of which the first http://mathworld.wolfram.com/ContinuedFractionConstant.html gives the reader all needed information, as will the use of the ISC. My purpose here was only to show the potential power of changing a representation. For example, the continued fraction of the irrational golden mean \( \frac{\sqrt{5}+1}{2}=1.6180339887499\dots \) is [1, 1, 1, …]. Figure 3.8 illustrates the golden mean, and also provides a proof without words that it is irrational as we discuss further in the next section.

The golden mean \( a+b:a=a:b \)

It is a result of Lagrange that an irrational number is a quadratic if and only if it has a non-terminating but eventually repeating simple continued fraction. So quadratics are to continued fractions what rationals are to decimal arithmetic. This is part of their power. \( \diamondsuit \)

As the following serious quotation makes clear, when a topic is science and when it is technology is both time and place dependent.

A wealthy (15th Century) German merchant, seeking to provide his son with a good business education, consulted a learned man as to which European institution offered the best training.“If you only want him to be able to cope with addition and subtraction,” the expert replied, “then any French or German university will do. But if you are intent on your son going on to multiplication and division – assuming that he has sufficient gifts – then you will have to send him to Italy.”Footnote 15

3.2.1 Minimal Configurations

Both the central picture in Fig. 3.5 and the picture in Fig. 3.8 illustrate irrationality proofs. Traditionally, each would have been viewed as showing a reductio ad absurdum. Since the development of modern set theory and of modern discrete mathematics it is often neater to view them as deriving a contradiction from assuming some object is minimal.

For example, suppose that the (a + b) × a rectangle was the smallest integer rectangle representing the golden mean in Fig. 3.8, then the a × b rectangle cannot exist. Because of the geometric simplicity of this argument, it is thought that this may be the first number the Pythagoreans realized was irrational. Figure 3.5, by contrast, illustrates a reductio. If we continue, we will eventually get to an impossibly small triangle with integer sides. A clean picture for minimality is shown in Fig. 3.9.

A minimal configuration for irrationality of \( \sqrt{2} \)

Example 3.3.5 (Sylvester’s Theorem, Bailey & Borwein, 2011b).

The theorem conjectured by Sylvester in the late nineteenth century establishes that given a finite set of non-colinear points in the plane there is at least one ‘proper’ line through exactly two points. The first proof 40 years later was very complicated. Figure 3.10 shows a now-canonical minimality proof.

A minimal configuration for Sylvester’s theorem

The objects used in this picture are pairs (L, p) where L is a line through at least two points of the set and p is the closest point in the set but not on the line. We consider the \( \left(\overline{L},\overline{p}\right) \) with \( \overline{p} \) closest to \( \overline{L} \). We assert that \( \overline{L} \) (the red horizontal line) has only two points of the set on it. If not two points lie on one side of the projection of \( \overline{p} \) on \( \overline{L} \). And now the black line L 0 through \( \overline{p} \) and the farther point on L, and p 0 the red point nearer to the projection constructs a configuration \( \left({L}_0,{p}_0\right) \) violating the minimality of \( \left(\overline{L},\overline{p}\right) \).

Subtle, ingenious and impossible to grasp without a picture! Here paper and coloured pencil are a fine tool. \( \diamondsuit \)

3.3 Mathematical Discovery (or Invention)

Giaquinto’s attractive encapsulation: “In short, discovering a truth is coming to believe it in an independent, reliable, and rational way” Giaquinto (2007, p. 50) has the satisfactory consequence that a student can discover results whether known to the teacher or not. Nor is it necessary to demand that each dissertation be original (only that the results should be independently discovered).

Despite the conventional identification of mathematics with deductive reasoning, Kurt Gödel (1906–1978) in his 1951 Gibbs Lecture said: “If mathematics describes an objective world just like physics, there is no reason why inductive methods should not be applied in mathematics just the same as in physics”. He held this view until the end of his life despite—or perhaps because of—the epochal deductive achievement of his incompleteness results.

Also, one discovers that many great mathematicians from Archimedes and Galileo—who apparently said “All truths are easy to understand once they are discovered; the point is to discover them.”—to Gauss, Poincaré, and Carleson have emphasized how much it helps to “know” the answer. Two millennia ago Archimedes wrote to EratosthenesFootnote 16 “For it is easier to supply the proof when we have previously acquired, by the method, some knowledge of the questions than it is to find it without any previous knowledge”. Think of the Method as an ur-precursor to today’s interactive geometry software—with the caveat that, for example, Cinderella actually does provide certificates for much Euclidean geometry.

As 2006 Abel Prize winner Lennart Carleson describes in his 1966 ICM speech on his positive resolution of Luzin’s 1913 conjecture (about the pointwise convergence of Fourier series for square-summable functions) after many years of seeking a counterexample he decided none could exist. The importance of this confidence is expressed as follows:

The most important aspect in solving a mathematical problem is the conviction of what is the true result. Then it took 2 or 3 years using the techniques that had been developed during the past 20 years or so.

3.4 Digital Assistance

By digital assistance I mean use of artefacts as:

-

1.

Modern Mathematical Computer Packages—symbolic, numeric, geometric or graphical. Symbolic packages include the commercial computer algebra packages Maple and Mathematica, and the open source SAGE. Primarily numeric packages start with the proprietary matlab and public counterparts Octave and NumPy, or the statistical package (R). The dynamic geometry offerings include Cinderella, Geometer’s Sketchpad, Cabri and the freeware GeoGebra.

-

2.

Specialized Packages or General Purpose Languages such as Fortran, C++, Python, CPLEX, PARI, SnapPea and MAGMA.

-

3.

Web Applications such as: Sloane’s Encyclopedia of Integer Sequences, the ISC,Footnote 17 Fractal Explorer, Jeff Weeks’ Topological Games, or Euclid in Java.Footnote 18

-

4.

Web Databases including Google, MathSciNet, ArXiv, GitHub, Wikipedia, MathWorld, MacTutor, Amazon, Wolfram Alpha, the DLMF (Olver, Lozier, Boisvert, & Clark, 2012) (all formulas of which are accessible in MathML, as bitmaps, and in TE X) and many more that are not always so viewed.

All entail data-mining in various forms. Franklin (2005) argues Steinle’s “exploratory experimentation” facilitated by “widening technology”, as in pharmacology, astrophysics, medicine and biotechnology, is leading to a reassessment of what legitimates experiment; in that a “local model” is not now prerequisite. Sørenson (2010) cogently makes the case that experimental mathematics—as ‘defined’ above—is following similar tracks.

These aspects of exploratory experimentation and wide instrumentation originate from the philosophy of (natural) science and have not been much developed in the context of experimental mathematics. However, I claim that e.g., the importance of wide instrumentation for an exploratory approach to experiments that includes concept formation also pertain to mathematics.

In consequence, boundaries between mathematics and the natural sciences and between inductive and deductive reasoning are blurred and getting more so. (See also Avigad, 2008.) I leave unanswered the philosophically vexing if mathematically minor question as to whether genuine mathematical experiments (as discussed in Borwein & Bailey, 2008) exist even if one embraces a fully idealist notion of mathematical existence. They sure feel like they do.

3.5 The Twentieth Century’s Top Ten Algorithms

The modern computer itself, being a digital repurposable tool, is quite different from most of its analogue precursors. They could only do one or two things. The digital computer, of course, greatly stimulated both the appreciation of and need for algorithms and for algorithmic analysis.Footnote 19 These are what allows the repurposing. This makes it reasonable to view substantial mathematical algorithms as tools in their own right.

At the beginning of this century, Sullivan and Dongarra could write “Great algorithms are the poetry of computation”, when they compiled a list of the ten algorithms having “the greatest influence on the development and practice of science and engineering in the twentieth century”.Footnote 20 Chronologically ordered, they are:

-

#1.

1946: The Metropolis Algorithm for Monte Carlo. Through the use of random processes, this algorithm offers an efficient way to stumble toward answers to problems that are too complicated to solve exactly.

-

#2.

1947: Simplex Method for Linear Programming. An elegant solution to a common problem in planning and decision-making.

-

#3.

1950: Krylov Subspace Iteration Method. A technique for rapidly solving the linear equations that abound in scientific computation.

-

#4.

1951: The Decompositional Approach to Matrix Computations. A suite of techniques for numerical linear algebra.

-

#5.

1957: The Fortran Optimizing Compiler. Turns high-level code into efficient computer-readable code.

-

#6.

1959: QR Algorithm for Computing Eigenvalues. Another crucial matrix operation made swift and practical.

-

#7.

1962: Quicksort Algorithms for Sorting. For the efficient handling of large databases.

-

#8.

1965: Fast Fourier Transform (FFT). Perhaps the most ubiquitous algorithm in use today, it breaks down waveforms (like sound) into periodic components.

-

#9.

1977: Integer Relation Detection. A fast method for spotting simple equations satisfied by collections of seemingly unrelated numbers.

-

#10.

1987: Fast Multipole Method. A breakthrough in dealing with the complexity of n-body calculations, applied in problems ranging from celestial mechanics to protein folding.

I observe that eight of these ten winners appeared in the first two decades of serious computing, and that Newton’s method was apparently ruled ineligible for consideration.Footnote 21 Most of the ten are multiply embedded in every major mathematical computing package. The last one is the only one that occurs infrequently in my own work.

Just as layers of software, hardware and middleware have stabilized, so have their roles in scientific and especially mathematical computing. When I first taught the simplex method more than 30 years ago, the texts concentrated on ‘Y2K’-like tricks for limiting storage demands.Footnote 22 Now serious users and researchers will often happily run large-scale problems in Matlab and other broad spectrum packages, or rely on CPLEX or, say, NAG library routines embedded in Maple.

While such out-sourcing or commoditization of scientific computation and numerical analysis is not without its drawbacks, I think the analogy with automobile driving in 1905 and 2005 is apt. We are now in possession of mature—not to be confused with ‘error-free’—technologies. We can be fairly comfortable that Mathematica is sensibly handling round-off or cancellation error, using reasonable termination criteria and the like. Below the hood, Maple is optimizing polynomial computations using tools like Horner’s rule, running multiple algorithms when there is no clear best choice, and switching to reduced complexity (Karatsuba or FFT-based) multiplication when accuracy so demands. Though, it would be nice if all vendors allowed as much peering under the bonnet as Maple does.

3.6 Secure Knowledge Without Proof

Given real floating point numbers

Helaman Ferguson’s integer relation method—see #9 of Sect. 3.3.5 above—called unhelpfully PSLQ, finds a nontrivial linear relation of the form

where a i are integers—if one exists and provides an exclusion bound otherwise. This method is very robust. Given adequate precision of computation (Borwein and Bailey, 2008) it very rarely returns spurious relations.

If a 0 ≠ 0, then (3.6) assures β is in the rational vector space generated by

Moreover, as a most useful special case, if \( \beta :=1,{\alpha}_i:={\alpha}^i \), then α is algebraic of degree n (see Example 3.4.9).

Quite impressively here is an unproven 2010 integer relation discovery by Cullen:

We have no idea why it is true but you can check it to almost any precision you wish. In Example 3.4.10 we shall explore such discoveries.

3.7 Is ‘Free’ Software Better?

I conclude this section by commenting on open-source versus commercial software. While free is very nice, there is no assurance that most open source projects such as GeoGebra (based on Cabri and now very popular in schools as replacement for Sketchpad) will be preserved when the founders and typically small core group of developers lose interest or worse. This is still an issue with large-scale commercial products but a much smaller one.

I personally prefer Maple to Mathematica as most of the source code is accessible, while Mathematica is entirely sealed. This is more of an issue for researchers than for educators or less intense users. Similarly, Cinderella is very robust, unlike GeoGebra, and mathematically sophisticated—using Riemann surfaces to ensure that complicated constructions do not crash. That said, it is the product of two talented and committed mathematicians but only two, and it is only slightly commercial. In general, software vendors and open source producers do not provide the teacher support that has been built into the textbook market.

4 A Dozen or So Accessible Examples

Modern graphics tools change traditional approaches to many problems. We used to teach calculus techniques to allow graphing of even reasonably simple functions. Now one should graph to be guided in doing calculus.

Example 3.4.1 (Graphing to Do Calculus).

Consider a request in a calculus text to compare the function given by \( f(y):={y}^2 \log y \) (red) to each of the functions given by \( g(y):=y-{y}^2 \) and \( h(y):={y}^2-{y}^4 \) for \( 0\leqslant y\leqslant 1 \); and to prove any inequality that holds on the whole unit interval.

The graphs of f, g are shown in the left of the picture in Fig. 3.11, and the graphs of f, h to the right. In any plotting tool we immediately see that f and g cross but that \( h\geqslant f \) appears to hold on [0, 1]. Only in a neighbourhood of 1 is there any possible doubt. Zooming in—as is possible in most graphing tools—or re-plotting on a smaller interval around 1 will persuade you that f(y) > h(y) for 0 < y < 1. This is equivalent to \( k(x):= \log (x)-1+1/ x>0 \) and so that is what you try to prove. Now it is immediate that k′(x) < 0 on the interval and so k strictly decreases to k(1) = 0 and we are done.□

The functions f and h (L) and f and g (R)

Likewise, computer algebra systems (CAS) now make it possible to find patterns which we prove ex post facto by induction. Before CAS many of these inductive statements might have been inaccessible.

Example 3.4.2 (Induction and Computer Algebra).

We all know how to show

with or without induction. But what about

Consider the following three lines of Maple code.

> S:=(n,N)->sum(k^n,k=1..N):

> S5:=unapply(factor(simplify(S(5,N))),N);

> simplify(S5(N)-S5(N-1));

The first line defines the sum \( {\displaystyle {\sum}_{k=1}^N}{k}^n \). The second finds this sum for n = 5 and makes it into a function of N. We obtain:

The third line proves this by induction—on checking that S5(1) = 1. The proof can of course be done by hand. Jakob Bernoulli (1655–1705) invented his Bernoulli numbers Footnote 23 and associated polynomials in part to evaluate such sums. Indeed, using the same code with N = 10 we arrive at a proof that

and so that

and

This later computation by Bernoulli is accounted as the first case of real computational number theory. Likewise

We finish with interior palindromes in each of the three sums centered at the ‘3’ and leave its explanation and other apparent patterns to the reader. Of course, unlike Bernoulli, we could simply have added the three sums without finding the closed form but then we would know much less.□

Large matrices often have structure that pictures will reveal but which numeric data may obscure.

Example 3.4.3 (Visualizing Matrices).

The picture in Fig. 3.12 shows a 25 × 25 Hilbert matrix on the left and on the right a matrix required to have 50 % sparsity and non-zero entries random in [0, 1].

The Hilbert matrix (L) and a sparse random matrix (R)

The 4 × 4 Hilbert matrix in Maple is generated by with(LinearAlgebra); HilbertMatrix(4); which code produces

from which the general definition should be apparent. Hilbert matrices are notoriously unstable numerically. The picture on the left of Fig. 3.13 shows the inverse of the 20 × 20 Hilbert matrix when computed symbolically and so exactly. The picture in the middle shows the enormous numerical errors introduces if one uses 10 digit precision, and the right shows that even if one uses 20 digits, the errors are less frequent but even larger.

Inverse 20 × 20 Hilbert matrix (L) and 2 numerical inverses (R)

Representative Maple code for drawing the symbolic inverse is:

> with(plots):

> matrixplot(MatrixInverse(HilbertMatrix(20)),

heights = histogram, axes = frame, gap = .2500000000,

color = proc (x, y) options operator, arrow; sin(y*x) end proc);}

It is very good fun to play with pictures of very large matrices constructed to have complicated block structure. Consider the sequence of 2n × 2n matrices Q(n), with entries only 0, 1, 2, 4 which start

We cannot possibly present Q(100) as a symbolic or numerical matrix but Fig. 3.14 visually shows everything both about the matrix and its inverse.□

The matrix Q(100) (L) continuing the pattern in (3.9) and its inverse (R)

Let us continue with a different exploration of matrices.

Example 3.4.4 (Abstract Becomes Concrete).

Define, for n > 1 the n × n matrices A(n), B(n), C(n), M(n) by

(for k, j = 1, …, n) and set \( M:=A+B-C \). For instance,

In my research (Borwein, Bailey, & Girgensohn, 2005, §3.3), I needed to show M(n) was invertible. After staring at numerical examples without much profit, I decided to ask Maple for the minimal polynomial of M(10) using

> MP:=LinearAlgebra[MinimalPolynomial]: MP(evalm(M(10)),t);

and was surprised to get \( {t}^2+t-2 \). (One way to write B in Maple is

> B:=n->matrix(n,n,(i,j)->(-1)^(j+1)*binomial(2*n-j,i-1));

and there are many other formats.) I got the same answer for M(30) and so I knew \( M{(n)}^2+M(n)=2I \) for all n > 1 or equivalently that

But why? I decided to explore A, B, C with the same tool and discovered that A and C satisfied t 2 = 1 and B satisfied t 3 = 1. This led me to realize that A, B, C generated the symmetric group on three elements and so to a computer discovered proof that M was as claimed.

As an illustration of the robustness of such discoveries, if we change the \( i=1,j=10 \) entry in M(10) to ε ≠ 0 from 0, we find the minimal polynomial is far from as simple: \({t^4} + 2\;{t^3} - 3\;{t^2} - 4\;t + 4 - \left( {252\;{t^2} + 252\;t - 504} \right),\) which also shows the discontinuity at ε = 0. Similarly, for the 5 × 5 Hilbert matrix we get

The constant term is of course giving minus the determinant. When I was a student characteristic and minimal polynomials seemed to be entirely abstract and matrix decompositions were in their infancy. Now they are technology. \( \diamondsuit \)

Example 3.4.5 (Hardy’s Taxi-Cab).

Hardy when visiting Ramanujan in hospital in 1917 remarked that his taxi’s number, 1729, was very dull. Ramanujan famously replied that it was very interesting being the smallest number expressible as a sum of two cubes in two distinct ways (not counting sign or order):

Let us ask “what is the second such number? As in Sect. 3.2.2, we can look at a generating function—this time for cubes. The coefficients of C 2(q) will be 0 when n is not the sum of two cubes, 1 when n = 2m 3, 2 when \( n={m}^3+{k}^3 \) for k ≠ m. If there are two distinct representations, the coefficient will be 4. The Maple fragment

> C:=convert((add(q^(n^3),n=1..20)^2),polynom):C-(C mod 4):

outputs \( 4\kern0.3em {q}^{4104}+4\kern0.3em {q}^{1729} \) which both proves Ramanujan’s assertion and finds that the second example is \( 4104=1{5}^3+{9}^3={2}^3+1{6}^3 \). If we change 20–25 in our code, we uncover the third such number. Alternatively entering just the first two into the OIES produces sequence A001235 consisting of the ‘taxi-cab numbers’: 1729, 4104, 13832, 20683, 32832, 39312, 40033, 46683, 64232, 65728, 110656, 110808, … \( \diamondsuit \)

Example 3.4.6 (Euler’s Pentagonal Number Theorem).

The number of additive partitions of n, p(n), is generated by

Thus p(5) = 7 since

as we ignore “0” and permutations. Additive partitions are mathematically less tractable than multiplicative ones as there is no analogue of unique prime factorization nor the corresponding structure.

Partitions provide a wonderful example of why Keith Devlin calls mathematics “the science of patterns”. They do sometimes enter the school curriculum through the back-door in the guise of Cuisenaire rods (or réglets), as illustrated by a staircase in Fig. 3.15.

A 10 × 10 Cuisenaire staircase

Formula (3.10) is easily seen by expanding \( {\left(1-{q}^n\right)}^{-1} \) and comparing coefficients. A modern computational temperament leads to:

Question: How hard is p(n) to compute—in 1900 (for MacMahon the “father of combinatorial analysis”) or in 2015 (for Maple or Mathematica)?

Answer: The famous computation by Percy MacMahon of p(200) = 3972999029388 at the beginning of the twentieth century, done symbolically and entirely naively from (3.10) in Maple on a laptop, took 20 min in 1991 but only 0.17 s in 2010, while the many times more demanding computation

took just 2 min in 2009 and 40.7 s in 2014.Footnote 24 Moreover, in December 2008, the late Richard Crandall was able to calculate p(109) in 3 s on his laptop, using the Hardy-Ramanujan-Rademacher ‘finite’ series for p(n) along with FFT methods. Using these techniques, Crandall was also able to calculate the probable primes p (1000046356) and p(1000007396), each of which has roughly 35, 000 decimal digits.Footnote 25

Such results make one wonder when easy access to computation discourages innovation: Would Hardy and Ramanujan have still discovered their marvelous formula for p(n) if they had powerful computers at hand? The Maple code

N:=500; coeff(series(1/product(1-q^n,n=1..N+1),q,N+1),q,N);

Twenty-five years ago computing P(q) in Maple was very slow, while taking the series for the reciprocal of the series for

was quite manageable!

Why? Clearly the series for Q must have special properties. Indeed it is lacunary:

This lacunarity is now recognized automatically by Maple, so the platform works much better, but we are much less likely to discover Euler’s gem:

If we do not immediately recognize the pentagonal numbers, \( \left(3\left(n+1\right)n/ 2\right) \), then Sloane’s online Encyclopedia of Integer Sequences Footnote 26 again comes to the rescue with abundant references to boot.

This sort of mathematical computation is still in its reasonably early days but the impact is palpable.□

Example 3.4.7 (Ramanujan’s Partition Congruences).

Ramanujan had access to the first 200 values of p(n) thanks to MacMahon’s lengthy work which the following Maple snippet reconstructs near instantly:

> N:=200:L200:=

sort([coeffs(convert(series(1/product(1-q^n,n=1..N+1),q,N+1),polynom))]);

The list starts 1, 1, 2, 3, 5, 7, 11, 15, 22, 30, 42, 56, 77, 101, 135, 176, 231, 297, 385, 490, 627… with p(0): = 1, and Ramanujan noted various modular patterns. Namely p(5n + 4) is divisible by 5, and p(7n + 5) is divisible by 7. This is hard to see from a list but a little software can help. The snippet below reshapes the beginning of a list of n × m or more entries into an n × m matrix:

> reshape:=proc (L, n, m) local k;

linalg[matrix](n, m, [seq(L[k], k = 1 .. m*n)])

end proc

For instance, > reshape(L200 mod 5, 8,20) produces the first 160 entries of the list with 20 columns in each of 8 rows as

We now see only zeroes in the columns congruent to 4 modulo 5 and discover the first congruence 5∣p(5n + 4). Similarly, > reshape(L200 mod 7, 8,21) reveals

and ‘discovers’ the second congruence 5∣p(7n + 5) for all \( n\geqslant 0 \). The third congruence 6∣p(11n + 6) for all \( n\geqslant 0 \) can be discovered by appropriate reshaping—and if wished confirmed by taking more terms. These partition congruences are discussed and the first two proved in Borwein and Borwein (1987, §3.5). \( \diamondsuit \)

Maple has since version 9.5 had a function called ‘identify’. It takes many tools such as PSLQ (Sect. 3.3.6) and attempts to predict an answer for a floating point number. A related ISC is on-line at http://isc.carma.newcastle.edu.au/. This lets you enter a real number or a Maple expression and ask the computer “What is that number?”

Another excellent example of how packages are changing mathematics is the Lambert W function (Borwein et al., 2005), whose remarkable properties and development are very nicely described in a fairly recent article by Hayes (2005), Why W? Informally, W(x) solves

As a real function, its domain is \( \left(-1/ e,\infty \right) \). We draw W and the quite similar \( \log \) function on the left of Fig. 3.16. Its use can be traced back to Lambert (1728–1727), and W as a notation was used by Pólya and Szegö in 1925. However, this very useful non-elementary function only came into general currency after it was named and then implemented in both Maple and Mathematica. It is hard to use or popularize an un-named function. Now most CAS know the expansion

with radius of convergence 1/e.

(L) W and \( \log \) (R) \( \left( \log x\right)/ x \)

Example 3.4.8 (Solving Equations with W).

We first look at \( {x}^y={y}^x \).

-

(a)

Let us fix x > 0 and try to solve

$$ {x}^y={y}^x\kern1.5em \mathrm{f}\mathrm{o}\mathrm{r}\ y>0. $$(3.12)Of course, we seek a non-trivial solution with x ≠ y such as \( x=2,y=4 \). The Maple solve command returns

$$ y(x)=\left(\frac{-x}{ \log x}\right)W\left(\frac{- \log x}{x}\right). $$(3.13)This may confuse initially more than help. If we take logarithms in (3.12) and rearrange, we are trying to solve

$$ \frac{ \log y}{y}=z:=\frac{ \log x}{x} $$(3.14)for y > 0.

The right of Fig. 3.16 shows that the function \( \left( \log x\right)/ x \) is positive only on \( 1<x<\infty \) and then and only then has two solutions—except for x = e where the maximum of 1∕e occurs—and now in Maple solve(log(x)/x=z,x) returns \( -W\left(- \log\ z\right)/ z \). This solution is shown on the left in Fig. 3.17 where z implicitly must satisfy 0 < z < 1∕e. This yields (3.13), shown in the center of Fig. 3.17, where we know now that x > 1 is requisite. For instance, \( {y}_3:=-3W(-( \log \kern0.15em 3)/ 3)/ \log \kern0.15em 3=2.478052685\dots \ne 3 \) solves \( {3}^{y_3}={\left({y}_3\right)}^3. \)

Fig. 3.17 Now, we may not know W but our computer certainly now does. For instance, identify(0.56714329040978) returns W(1) and the Taylor series for y(x) around e starts

$$ \begin{array}{l}y(x)=\mathrm{e}-\mathrm{sign}\kern0.15em \left(x-\mathrm{e}\right)\left(x-\mathrm{e}\right)+\frac{5\kern0.3em {\mathrm{e}}^{-1}\left(\mathrm{sign}\left(x-\mathrm{e}\right)+1\right)}{6}{\left(x-\mathrm{e}\right)}^2\\ {}\kern2.65em +O\left({\left(x-\mathrm{e}\right)}^3\right)\hfill \end{array} $$(3.15)as shown on the right of Fig. 3.17. For x > e, \( y(x)=1/ (3\mathrm{e})\left(11\kern0.3em {\mathrm{e}}^2-13\kern0.3em x\mathrm{e}+5\kern0.3em {x}^2\right) \) while for x < e we get the trivial solution x.

-

(b)

A parametric form of the solution is \( x={r}^{1/ \left(r-1\right)},y=rx={r}^{r/ \left(r-1\right)} \), for r > 1. Equivalently with \( r=1+1/ s \), where s > 0, we have \( x={(1+1/ s)}^s,y={(1+1/ s)}^{s+1} \). This is shown in Fig. 3.18.

Fig. 3.18

Parametric solutions of (3.12) separated by y = e

-

(c)

Repeated exponentiation. How many distinct meanings may be assigned to product towers for the n-fold exponentiation

$$ {x}^{\ast_n^x}={x}^{x^{x^{x{\cdots}^x}}}? $$Recursions like x 1 = t > 0 and \( {x}_n={t}^{x_{n-1}} \) for n > 0 have been subjected to considerable scrutiny. We can check that the solution to t x = x is \( t\mapsto -W\left(- \log \kern0.2em t\right)/ \log \kern0.2em t \) which solution exists for \( t\in \left[{e}^{-e},{e}^{1/ e}\right] \). \( \diamondsuit \)

Example 3.4.9 (Finding Algebraic Numbers).

Both Maple and Mathematica have algorithms that can predict if a number is algebraic and even find its minimal polynomial. We described this a little further in Sect. 3.3.6. For instance, using identify—with no tuning of parameters—as with

> Digits:=20:a:=evalf(7^(1/2)+3^(1/2));identify(a);

returns

but

> Digits:=20:a:=evalf(2^(1/3)+3^(1/2));identify(a);

returns

meaning Maple could not identify the surd from 20 digits. The ISC at http://isc.carma.newcastle.edu.au/advancedCalc runs tuned algorithms and will identify the constant as shown in Fig. 3.19.

Identifying \( {2}^{1/ 3}+{3}^{1/ 2} \)

However:

> Digits:=30:a:=evalf(2^{1/3}+3^{1/2});identify(a);

returns

which allows us to recover \( {2}^{1/ 3}+{3}^{1/ 2} \). For example, we can factor in \( \mathrm{Q}\left(\sqrt{3}\right) \) using the command:

> factor(_Z^6-9*_Z^4-4*_Z^3+27*_Z^2-36*_Z-23,sqrt(3));

which yields

The quadratic formula now applies to determine that the only real roots of the sextic polynomial are \( {2}^{1/ 3}\pm \sqrt{3} \).□

We can do more exciting things of this kind.

Example 3.4.10 (What is that Number?).

Let us illustrate it for the integral

whose origins are described in Sect. 3.5. We plot R(a) in Fig. 3.20. (We used the hypergeometric form given below. Maple will find this form if you input (3.16).) Note that the graph is consistent with the fact that \( \mathcal{R} \) increases to the blue asymptote \( \mathcal{R}\left(\infty \right)=\frac{\pi }{2}. \) You may be able to evaluate some other values by hand.

The function \( \mathcal{R}(a) \) for 0 < a < 30

Most CAS will answer that the values of \( \mathcal{R}\left(1/ m\right) \), for \( 1\leqslant m\leqslant 6 \), are

We then check that \( \mathcal{R}\left(1/ 7\right)=\frac{5}{6}- \log 2 \) and \( \mathcal{R}\left(1/ 8\right)=-\frac{152}{105}+\frac{\pi }{2} \). From this it should be plausible that

for rational numbers \( {a}_n,{b}_n \). As experimental confirmation of this conjecture we can check that

If we ask the computer for \( \mathcal{R}(2) \), we get a complicated (ostensibly complex) expression that simplifies to \( \frac{\sqrt{2}}{4}\left(2\kern0.3em \pi + \log \left(17-12\kern0.3em \sqrt{2}\right)\right). \) If we try PSLQ for \( a:=2,2/ 3,2/ 5,\dots \) we discover that each such sum evaluates in terms of three basis vectors:

For instance,

If, however, we leave out the constant term ‘1’, we find

but have no such luck as we need that pesky constant term.

Actually, Borwein, Crandall, and Fee (2004) give a closed form for every instance of \( \mathcal{R}\left(\frac{p}{q}\right) \) with p, q positive integers.□

We turn to another example where the CAS provides a proof that we would not have been likely to arrive at without the current tools.

Example 3.4.11 (π Is Not 22∕7).

Even Maple or Mathematica ‘knows’ this since

though it would be prudent to ask ‘why’ it can perform the integral and ‘whether’ to trust it?

-

1.

Assuming we trust our software, the integrand is strictly positive on (0, 1), see Fig. 3.21, and so the answer in (3.17) is an area which is necessarily strictly positive, despite millennia of claims that π is 22∕7.

Fig. 3.21

The integrand in (3.17)

-

2.

Quite accidentally, 22∕7 is one of the early continued fraction approximation to π—and is why it is a pretty reasonable approximation to π. These commence:

$$ 3,\frac{22}{7},\frac{333}{106},\frac{355}{113},\dots $$but no one has found a way to replicate (3.17) for these other fractions. Some coincidences are just that—happenstance. Similarly, there is no good reason why \( {e}^{\pi }-\pi =\underline{19.9990999}7918947576\dots \), but it is most impressive on a low precision calculator.

-

3.

We turn to proving π is not \( \frac{22}{7} \) with computational help. In this case, taking the indefinite integral provides immediate reassurance. We obtain

$$ \begin{array}{ccc}{\int}_0^t\kern0.3em \frac{x^4{\left(1-x\right)}^4}{1+{x}^2}\kern0.3em \mathrm{d}\mathrm{x}& =& \frac{1}{7}\kern0.3em {t}^7-\frac{2}{3}\kern0.3em {t}^6+{t}^5-\frac{4}{3}\kern0.3em {t}^3+4\kern0.3em t-4\kern0.3em \arctan (t)\\ {}\end{array} $$as differentiation and simplification—by hand or by computer—easily confirms. Now the Fundamental theorem of calculus proves (3.17). A traditional proof would probably have developed the partial fraction expansion and thence performed the integral.

-

4.

One can take this idea a bit further. Note that

$$ {\mathit{\int}}_0^1\kern0.3em {x}^4{\left(1-x\right)}^4\mathrm{d}x=\frac{1}{630}. $$(3.18)Hence

$$ \begin{array}{c}\frac{1}{2}{\mathit{\int}}_0^1\kern0.3em {x}^4{\left(1-x\right)}^4\mathrm{d}x<{\mathit{\int}}_0^1\frac{{\left(1-x\right)}^4{x}^4}{1+{x}^2}\kern0.3em \mathrm{d}x<{\mathit{\int}}_0^1{x}^4{\left(1-x\right)}^4\mathrm{d}x.\\ {}\end{array} $$ -

5.

Combine this with (3.17) and (3.18) to derive: \( 223/ 71<22/ 7-1/ 630<\pi <22/ 7-1/ 1260<22/ 7 \) and so re-obtain Archimedes’ famous

$$ 3\frac{10}{71}<\pi <3\frac{10}{70}. $$(3.19)Note that by not cancelling the zeros on the right it is much easier to see that \( 1/ 7>10/ 71 \). All rules must be broken occasionally.

Even without using (3.19), a glance at Fig. 3.21 shows how small the error is. Indeed the maximum occurs at 1∕2 with maximum value a tiny 1∕320.

Never Trust References In 1971 Dalziel published this development in Eureka, a Cambridge student magazine of the period. Integral (3.17) was earlier on the 1968 William Lowell Putnam examination, an early 1960s Sydney honours exam, and traces back to a 1944 paper by the self-same Dalzeil who opted not to reference it 27 years later.Footnote 27 The message here is that what might appear to be a primary source may well not be, and even the author may not necessarily tell you the whole truth.□

The take away from Examples 3.4.2 and 3.4.11 is that whenever a CAS can do a definite sum, product or integral, it is well worth seeing if it can perform the corresponding indefinite one.

I have built a little function ‘pslq’ in Maple that when input data for PSLQ predicts an answer to the precision requested but checks it to ten digits more (or some other precision). This makes the code a real experimental tool as it predicts and confirms. One of my favourite uses of it is to quickly check answers for a lecture in cases where I know the general form of an answer but cannot remember all the details.

Example 3.4.12 (Preparing for Class).

In all serious computations of π from 1700 (by John Machin) until 1980 some version of a Machin formula (Borwein and Bailey, 2008) was used. This is a formula which writes

for rational numbers \( {a}_1,{a}_2,\dots, {a}_n \) and integers \( {p}_1,{p}_2,\dots, {p}_n>1 \). When combined with the Taylor series for \( \arctan \), namely

This series when combined with (3.20) allows one to compute \( \pi =4 \arctan (1) \) efficiently, especially if the values of p n are not too small.

For instance, Machin found

while Euler discovered

The code in Fig. 3.22 used 20 digits to confirm (3.22) to 30 digits. The input is a Maple or numeric real, followed by a list of basis elements, and the third variable is the precision to use. The code in Fig. 3.23 used 20 digits to likewise confirm (3.21) to 30 digits.

Finding equation (3.22)

Finding equation (3.21)

The code in Fig. 3.24 used 20 digits to find another relation and confirm it to 30 digits. This is what happens if you mistype 1∕3 for 1∕5.

Finding an unexpected equation

If, however, as in Fig. 3.25, you use 1∕9 instead of 1∕8 you get a ‘mess’.

When no relation exists

This shows that when no relation exists the code will often find a very good approximation but will use very large rationals in the process. So it diagnoses failure both because it uses very large coefficients and because it is not true to the requested 30 places.□

We next find the limit of an interesting mean iteration—an idea we take up again in Example 3.8.1. Recall that a mean M is any function of positive numbers a and b which always satisfies \( \min \left\{a,b\right\}\leqslant M\left(a,b\right)\leqslant \max \left\{a,b\right\}. \) A mean is strict if M(a, b) = a or M(a, b) = b implies a = b as is true for the arithmetic mean \( A\left(a,b\right):=\frac{a+b}{2} \), the geometric mean \( G\left(a,b\right):=\sqrt{ab} \) or the harmonic mean \( H\left(a,b\right):=\frac{2 ab}{a+b} \). Every mean clearly is diagonal meaning that M(a, a) = a.

Theorem 3.4.13 (Invariance Principle, Borwein & Borwein, 1987).

Suppose M,N are means and at least one is strict. The mean iteration given by \( {a}_{n+1}=M\left({a}_n,{b}_n\right) \) and \( {b}_{n+1}=N\left({a}_n,{b}_n\right) \) is such that the limit \( L\left(a,b\right)={\displaystyle { \lim}_n}{a}_n={\displaystyle { \lim}_n}{b}_n \) exists and is necessarily a mean. Moreover, it is the unique continuous and diagonal mapping satisfying for all n:

Proof.

We sketch the proof (details may again be found in Borwein & Borwein, 1987, Chap. 8). One first checks that the limit, being a pointwise limit of means is itself a mean and so is continuous on the diagonal. The principle follows since, L being diagonal satisfies

as asserted.□

A simple but satisfying application of Theorem 3.4.13 is to show that with \( {a}_0:=a>0,{b}_0:=b>0 \), the mean iteration

converges quadratically to \( \sqrt{ab} \).

Example 3.4.14 (Finding a Limit).

Consider the iteration that takes positive numbers \( {a}_0:=a,{b}_0:=b \) and repeatedly computes the mixed arithmetic-geometric means:

In this case convergence is immediate since \( |{a}_{n+1}-{b}_{n+1}|=|{a}_n-{b}_n|/ 2 \). The following Maple function will compute the Nth step of the iteration to the precision of the environment.

L:=proc(a0,b0,n) local a,b,c,k;a:=evalf(a0);b:=evalf(b0); for k to n do

:=evalf((a+sqrt(a*b))/2);b:=evalf((b+sqrt(a*b))/2);a:=c;od;a;end;

If we set the precision at 14 digits and try identify(L(2,1,50)); we get \( 1/ \log 2 \) and identify(L(3,1,50)); gives \( 2/ \log 3 \). After checking that x = 4 gives \( 3/ \log 4 \) and 5 behaves similarly, it seems worthwhile considering \( \log (x)L\left(x,1\right) \). We only want a few digits so we plot \( F(x):=L\left(x,1,5\right) \log\ x \) on [1∕3, 3]. The result in Fig. 3.26 is a straight line and strongly supports the conjecture that \( L(x,1)=(x-1)/ \log\ x \) in which case \( L\left(a,b\right)=b\left(a/b-1\right) \log \left(a/b\right)=\left(a-b\right)/ \left( \log a- \log b\right). \) Even dull plots can be interesting. \( \diamondsuit \)

The function \( x\mapsto L(x) \log \kern0.15em x \) on [1∕3, 3]

We are ready to prove our conjecture.

Example 3.4.15 (Carlson’s Logarithmic Mean).

Consider the iterations with \( {a}_0:=a>0,{b}_0:=b>a \) and

for \( n\geqslant 0 \). If asked for the limit, you might make little progress. But suppose we have just completed Example 3.4.14. Then we can see that answer is the logarithmic mean

for a ≠ b and a (the limit as \( a\to b \)) when a = b > 0. We check that

since \( 2 \log \frac{\sqrt{a_n}}{\sqrt{b_n}}= \log \frac{a_n}{b_n} \). The invariance principle of Theorem 3.4.13 then confirms that \( \mathcal{L}\left(a,b\right) \) is the limit. In particular, for a > 1,

which quite neatly computes the logarithm (slowly) using only arithmetic operations and square roots. \( \diamondsuit \)

And finally, we look at two examples that emphasize that no initial pattern is a proof. They involve the highly oscillatory sinc function

which is plotted in Fig. 3.27.

The sinc function

Example 3.4.16 (Inductive Reasoning Has Its Limits).

Consider

Then—as Maple and Mathematica are able to confirm—we have the following evaluations:

As explained in detail in Borwein et al. (2005, Chap. 2), the seemingly obvious pattern is then confounded by

where the fraction is approximately 0. 99999999998529… which, depending on the precision of calculation used, numerically might not even be distinguished from 1.

These integrals now called the Borwein integrals have gathered a life of their own as illustrated in Fig. 3.28 and http://oeis.org/A068214/internal.□

What is beauty?

In case this caution against inductively jumping to conclusions was not convincing, consider the next example.

Example 3.4.17 (Inductive Reasoning Really Has Its Limits).

The following “student’s dream” identity of a sum equalling an integral again engages the sinc function:

where the denominators range over the odd primes up to 29, was first discovered empirically.

Provably, the following is true: The analogous “sum equals integral” identity remains valid for ‘29’ replaced by any one of more-than-the first 10176 primes but stops holding after some larger prime, and thereafter the “sum less the integral” is positive but much less than one part in a googolplex. An even stronger estimate is possible assuming the generalized Riemann hypothesis (GRH) (Baillie, Borwein, & Borwein, 2008). What does it mean for two formulas to differ by a quantity that can never be measured in our assumed-to-be finite universe?□

5 Simulation in Pure Mathematics

Pure mathematicians have not frequently thought of simulation as a relevant tool though it has a long lineage. An early and dubious example of simulation of π is called Buffon’s needle. The Comte de Buffon (1700–1778) was an early vegetarian and his claimed result is much too good—it gets too accurate a result for the sample size (Fig. 3.29).

Simulating π

5.1 Monte Carlo Simulation of π

Stanislaw Ulam (1900–1984) can be considered the inventor of modern Monte Carlo sampling methods—named for the casino parlours of that city. See also the first of our top ten algorithms in Sect. 3.3.5. Such simulations were crucial during the Manhattan project when early computers were inadequate to perform the needed computations, even though they intrinsically are not efficient. One expects to need n 2 measurements to get an accuracy of O(1∕n). An easy illustration is simulation of π.

Example 3.5.1 (Why a Serial God Should Not Play Dice).

Consider inscribing a circle in a square pan of side one, and sprinkling a fine particle (e.g., salt or grain) and counting the proportion of particles that fall in the circle. It should approximate π∕4 as that is the area of the circle.

If one can pour all the particles at once and uniformly over the square, this is a fast and parallel method of estimating π. But if one has to do this in serial it is painfully slow. One can do this at the computer by selecting pairs of pseudo-random numbers in the square 0 < x, y < 1 and counting how often \( {x}^2+{y}^2\leqslant 1 \). Four times that proportion should converge to π. \( \diamondsuit \)

Despite the slowness of the method, in the early days of personal computers I implemented this on each new desktop or laptop. It was a terrible way to compute π but a great way to test the random number generator. I would start the program and after a few thousand trials would have roughly 3. 14. When I looked again the next morning I might have converged to 3. 57… or some such because the built-in random number generator was far from random.

5.2 Finding a Region of Convergence

The cardioid at the left of Fig. 3.30 was produced by a scatter plot while trying to determine for which complex numbers \( z=b/ a \) an improper continued fraction due to Ramanujan, \( \mathcal{R}\left(a,b\right) \), converged. It is given for complex numbers a and b by

see Borwein et al. (2005, Ex. 53, p. 69).

(L) cardioid discovered by simulation. (M) and (R) a fractal hidden in \( \mathcal{R} \)

As often I first tried to compute R(1, 1) and had little luckFootnote 28—it transpires that for \( a=b\in \mathrm{\mathbb{R}} \) convergence is O(1∕n) but is geometric for a ≠ b. So what looks like the simplest case analytically is the hardest computationally. We did eventually determine from highly sophisticated intermediate steps that:

Theorem 3.5.2 (Four Formulae for \( \mathcal{R}\left(a,a\right) \)).

For any a > 0

Here \( {}_2{F}_1 \) is the hypergeometric function defined in (3.35). If you do not know the ψ or \( \Psi \) (‘psi’) function, you can easily look it up once you can say ‘psi’. Notice that

now allows us to evaluate \( R\left(1,1\right)= \log 2 \) as discussed in Example 3.4.10.

The development of this theory exploited modular and theta functions. We used the square counting theta functions \( {\theta}_3(q):={\displaystyle {\sum}_{n=-\infty}^{\infty }}{q}^{n^2} \) and \( {\theta}_4(q):={\theta}_3\left(-q\right) \). The pictures on the right of Fig. 3.30 shows the level sets of the modulus of the ratio \( {\theta}_4(q)/ {\theta}_3(q) \) for \( q:=r{e}^{i\theta } \) in the first quadrant; black regions have modulus exceeding one. From this simple recipe comes beautiful fractal complexity.

After making no progress analytically, Crandall and I decided to take a somewhat arbitrary criterion for convergence and colour yellow the points for which the fraction seemed to converge. Treating the iteration implicit in (3.26) as a black box, we sampled one million starting points and reasoned that a few thousand mis-categorizations would not damage the experiment. Figure 3.30 is so precise that we could identify the cardioid. It is the points where

and since for positive a, b the fraction satisfies

this gave us enormous impetus to continue our eventually successful hunt for a rigorous proof (Borwein & Crandall, 2004; Borwein, Borwein, Crandall, & Mayer, 2007).

Example 3.5.3 (Digital Assistance, \( arctan(1) \) and a Black-Box).

Consider for integer n > 0 the sum

The definition of the Riemann sum means that

Even without being able to do this Maple will quickly tell you that

Now if you ask for 100 billion terms of most slowly convergent series, a computer will take a long time. So this is only possible because Maple knows

using the imaginary i, and it has a fast algorithm for our new friend the psi function. Now identify(0. 78539816339746) yields \( \frac{\pi }{4} \).

We can also note that

is another Riemann sum. Indeed, \( {\sigma}_n-{\tau}_n=\frac{1}{2n}>0 \). Moreover, experimentally it seems that τ) increases and \( {\sigma}_n \) decreases to π∕4.

If we enter “monotonicity of Riemann sums” into Google, one of the first entries is http://elib.mi.sanu.ac.rs/files/journals/tm/29/tm1523.pdf which is a 2012 article (Szilárd, 2012) that purports to show the monotonicity of the two sums. The paper goes on to prove that if f: [0, 1] → R is continuous, concave and decreasing then \( {\tau}_n:=\frac{1}{n}{\displaystyle {\sum}_{k=1}^n}\ f(\frac{k}{n}) \) increases and \( {\sigma}_n:=\frac{1}{n}{\displaystyle {\sum}_{k=0}^{n-1}}\kern.5em f(\frac{k}{n}) \) decreases to \( {\int}_0^1f(x)\kern0.3em \mathrm{d}x \). Moreover, if f is convex and decreasing, then instead \( {\sigma}_n \) increases and τ n decreases.

All proofs are based on looking at the rectangles which comprise the difference between τ n+1 and τ n as in Fig. 3.31 (or the corresponding sums for \( {\sigma}_n \)). This is

Difference in the lower Riemann sums for \( 1/ \left(1+{x}^2\right) \)

In the easiest case, each bracketed term

has the same sign for all n and \( 1\leqslant k\leqslant n \) as happens for concave or convex and decreasing (for increasing consider − f).

But in Szilárd (2012) the author mistakenly asserts this for \( 1/ \left(1+{x}^2\right) \) which has an inflection point at \( 1/ \sqrt{3} \). It appears, on checking in a CAS, that \( {\delta}_n(k)+{\delta}_n\left(n-k\right)\geqslant 0 \) which will repair the hole in the proof. Indeed, this suggests we consider \( g(x):=\frac{f(x)+f(1-x)}{2} \) which for \( f(x):=1/ \left(1+{x}^2\right) \) is concave on [0, 1] and has the same value for (3.28). The details of a correct result based on symmetric Riemann sums are to be found in Borwein, Borwein, and Sims (2015). What a fine example of digital assistance in action! \( \diamondsuit \)

I conclude this section by saying that most of my more sophisticated research computing is an admixture of tools like the ones above—used appropriately and in context. In the remainder of this chapter we look at mathematics originating in my recent research. Details are given in the references but a reader who knows some secondary school algebra, geometry and calculus should be able to follow the broad brushes of what follows. We now turn to three sets of more sophisticated case studies. Remember in each case the pictures are central.

6 Case Studies I: Dynamic Geometry

Dynamic or interactive geometry packages take points and lines as primitive objects—usually in two dimensions—and add various conic sections and the like. Once positioned the entire construction is moveable. Thence, the qualitative ‘generic’ properties of a configuration often become clear very quickly. In Cinderella one can work in various geometries: Euclidean, hyperbolic spherical and more. One can also export a construction as a Java html object useable in a web page. For example, http://www.carma.newcastle.edu.au/jon/lm.html will illustrate much of the next section’s discussion and many additional features.

6.1 Case Study Ia: Iterative Reflections

Let \( S\subset {R}^m \). The (nearest point or metric) projection onto S is the (set-valued) mapping, \( {P}_Sx:={\mathrm{argmin}}_{s\in S}\parallel s-x\parallel . \) The reflection with respect to S is then the (set-valued) mapping, \( {R}_S:=2{P}_S-I. \) The projections and reflection are illustrated in Fig. 3.32 for a convex set (where they are unique) and a non-convex set where they need not be.

Projections and reflections for a convex set (L) and for a non-convex set (R)

Iterative projection methods have a long and successful history going back to von Neumann, Wiener and many others. The basic model (Aragon and Borwein, 2013; Aragon et al., 2014) finds a point in \( A\cap B \) assuming information about the projections on A and B individually is accessible. Precisely we repeatedly compute

The corresponding reflection methods are more recent and often appear more potent.

Theorem 3.6.1 (Douglas–Rachford (1956–1979)).

Suppose \( A,B\subset {R}^m \) are closed and convex. For any x 0 ∈ R m define

If \( A\cap B\ne \varnothing \) , then x n → x such that \( {P}_Ax\in A\cap B \) . Else if \( A\cap B=\varnothing \) , then \( \parallel {x}_n\parallel \to \infty \) .

In Fig. 3.33 we illustrate one step of ‘reflect-reflect-average’ as Douglas–Rachford’s method is also called below.Footnote 29

One step of the Douglas–Rachford method

The method also can be applied to a good model for phase reconstruction, namely for B affine and A a boundary ‘sphere’. In this case we have some few local convergence results and even fewer global convergence results; but much positive empirical evidence—both numeric and geometric—using tools such as Cinderella, Maple and SAGE.

Is Fig. 3.34 showing a “generic visual theorem” establishing global convergence off the (provably chaotic) y-axis? Note the error—scattered red points—from using ‘only’ 14 digit computation.

Trajectories of a Cinderella applet showing 20, 000 starting points coloured by distance from y-axis after 0, 7, 14, 21 steps

Figure 3.35 illustrates that what we can prove (L) is frequently less than what we can see (R). There is nothing new here. The French academy stopped looking at attempts to solve the three classical ruler-and-compass construction problems of antiquity—trisection of an angle, doubling the cube, and squaring the circle—centuries before they were proven impossible during the nineteenth century.Footnote 30

Proven region of convergence in grey

It is quite striking that an algorithm based on three simple operations of high-school geometry can so effective solve complicated real-world problems.

6.2 Case Study Ib: Protein Conformation

We need three concepts. First, a matrix completion problem starts with a fixed class of matrices 𝒜 (say doubly stochastic, symmetric or positive semidefinite) and seeks a matrix A ∈ 𝒜 consistent with knowledge of some prescribed subset of its entries. Of course this is not always possible.

Second, a distance matrix, with respect to metric d on a set X, is a symmetric square n × n matrix (a ij ) with real entries \( {a}_{ij}:={d}^2\left({p}_i,{p}_j\right) \) for points \( {p}_1,{p}_2,\dots, {p}_N\in X \). It is Euclidean if \( X={\mathrm{\mathbb{R}}}^N \) and \( d\left(x,y\right)=\parallel x-y\parallel \) is the metric induced by the Euclidean norm (Gower, 1985).Footnote 31 Note that a ii = 0 for any distance matrix.